Author: Rebekah Stovall

The 2024 Outlook: Slow-Bicycle Economy (December 18, 2023)

by Patrick Fearon-Hernandez, CFA, Thomas Wash, Bill O’Grady, and Mark Keller, CFA

Summary of Expectations | PDF

The Economy

Economic Growth

We expect the U.S. economy to continue growing into 2024, but its momentum has been slowing, and slowing momentum will put the economy at increased risk of recession. As the growth rate continues to moderate or slow, the economy will become increasingly susceptible to shocks such as a domestic financial crisis or a major geopolitical event that saps confidence.

Just as riding a bike too slowly makes it difficult to stay in balance, slowing economic growth will increase the risk of a downturn in the economy.

Recession Risk

Reflecting the risks inherent in a slower-growing economy, we believe the economy is slightly more likely to slip into a recession in 2024 than it is to avoid one. Nevertheless, if a recession does transpire, we believe it will be relatively mild and short-lived.

Inflation & Monetary Policy

In any case, slowing demand growth and the Federal Reserve’s aggressive interest rate hikes since early 2022 will probably lead to further moderation in consumer price inflation. That should allow the Fed to avoid or at least minimize any further rate hikes, but we expect policymakers to try to keep rates high for an extended period to make sure inflation pressures are eliminated.

Elections

The U.S. presidential election in November 2024 could have a big impact on key asset classes. At this point, it appears to be a close race between President Biden and former President Trump, but there is an elevated chance that some third-party candidate or candidates could join the race.

The elevated political uncertainty could keep investors cautious. In contrast, if one candidate appears to break from the pack, or if the election is thrown into the House of Representatives, risk assets could be pushed sharply higher or lower than in our base case.

Market Outlook

Fixed Income

As investors come to accept the Fed’s “higher for longer” stance toward interest rates, we think intermediate- and longer-term U.S. Treasury obligations will be susceptible to selling pressure in 2024, pushing the yield on the benchmark 10-year Treasury note to 4.90% or more.

* The spreads between investment-grade corporate obligations and Treasuries have recently been unusually low, in part reflecting the way many firms refinanced and termed out their debt when interest rates were ultra-low during the coronavirus pandemic. Spreads could remain tight, but if a recession does materialize, we would still expect them to widen to take account of the increased credit risk.

* Similarly, the spread between below-investment-grade corporates and Treasuries is also low, but it would likely widen even more dramatically if economic growth falters.

U.S. Equities

For U.S. large capitalization equities, we forecast that the S&P 500 price index will be between 4,060 and 5,090 at the end of 2024, with a single point forecast of 4,580.

* The rise in the U.S. stock market in 2023 was heavily concentrated among just a few large cap growth stocks. Stocks with smaller capitalizations lagged, making them better values now. We therefore think small cap stocks will outperform in 2024.

* Similarly, value stocks lagged in 2023, likely setting them up to outperform in 2024.

Foreign Equities

We continue to believe that the performance of foreign equities will largely depend on the value of the dollar. Continued strength in the greenback in 2024 is likely to be a headwind for foreign equities, although prudent investors will still want some exposure to the asset class for diversification and as a hedge against any unexpected dollar weakening.

Commodities

Finally, we expect gold and precious metals to be supported in 2024 by a range of factors, including the end of the Fed’s interest rate hikes, safe-haven buying amid today’s increased geopolitical tensions, and strong buying by central banks.

Broader commodities would face headwinds if a recession materializes, but they could snap back by year’s end if any such downturn ends up being short and mild, as we expect.

Weekly Energy Update (December 14, 2023)

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA | PDF

(N.B. The Weekly Energy Update is going on indefinite hiatus. Next year, look for a new report format.)

Crude oil prices are continuing to break down despite OPEC+ efforts to restrain supply.

Commercial crude oil inventories fell 4.3 mb compared to forecasts of a 2.0 mb draw. The SPR was unchanged, which puts the net draw at 4.3 mb.

In the details, U.S. crude oil production was steady at 13.1 mbpd. Exports fell 0.4 mbpd, while imports declined 0.6 mbpd. Refining activity fell 0.3% to 90.2% of capacity.

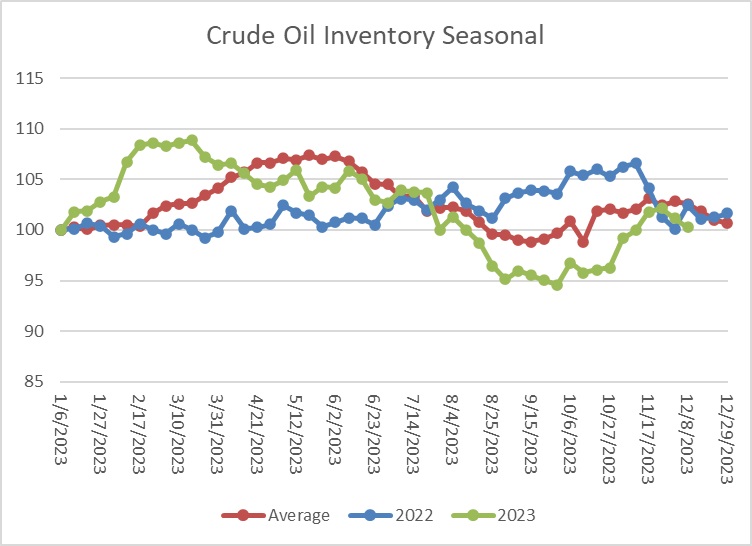

The above chart shows the seasonal pattern for crude oil inventories. Inventories are below seasonal norms but are following a similar pattern.

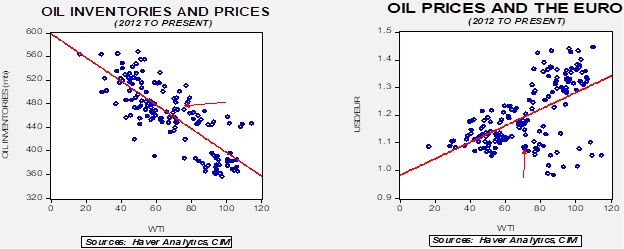

Fair value, using commercial inventories and the EUR for independent variables, yields a price of $66.88. The recent drop in oil prices indicates that the geopolitical risk premium has mostly been priced out of the market.

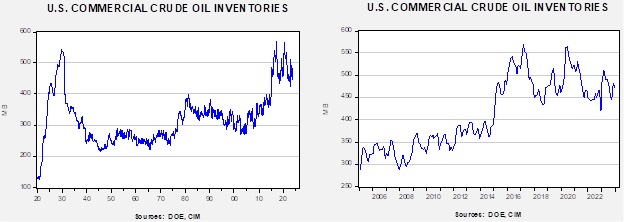

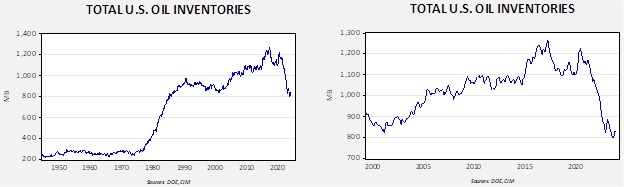

Since the SPR is being used, to some extent, as a buffer stock, we have constructed oil inventory charts incorporating both the SPR and commercial inventories.

Total stockpiles peaked in 2017 and are now at levels last seen in late 1984. Using total stocks since 2015, fair value is $90.16.

Market News:

- COP28 is coming to a close with an agreement. Earlier in the week, it appeared that hopes of ending fossil fuel production had been scotched. The draft agreement didn’t contain commentary on phasing out fossil fuel fuels, mostly on pressure from Saudi Arabia. However, as is often the case, Satan lives in the details. Oil producers signed off after the language surrounding fossil fuels was softened to a “shift” from the energy source as opposed to a “phasing out.” The loopholes have been described as “cavernous.” As we noted earlier, we really don’t think these meetings will bring a serious change in policy. There is no international enforcement mechanism and the temptation to “free ride” the restrictions of other nations is too great.

- The IEA estimates that the current pledges to reduce fossil fuels will not limit global warning to 1.5oC, meaning that even current promises won’t be enough to limit projected risks from climate change.

- The DOE’s short-term energy outlook is calling for mostly steady prices for crude oil next year but lower gasoline prices.

- Foreign oil companies are exiting Nigeria. This could increase the odds that future production declines.

- Low water levels in the Panama Canal are causing shippers to reroute fuel shipments.

Geopolitical News:

- As we have noted in earlier reports, the plan to limit Russia’s revenue from oil sales has floundered, mostly because Moscow has worked around the insurance ban by building a fleet of old oil tankers. Over 70% of Russian oil sales is not using Western insurance. It will be interesting to see what happens when/if there is an accident involving one of these vessels.

- India paid $84.20 for Russian crude oil in October, well above the $60 cap.

- Although Venezuela continues to threaten Guyana, we doubt Maduro would actually invade. We suspect he will use the threat as a bargaining chip to get sanctions eased. Reports that Venezuela is contacting major oil firms to revive offshore projects is evidence that this may be his plan.

- The presidents of Guyana and Venezuela are set to meet on December 14, with Brazilian President Lula as mediator. Guyana has stated it will defend itself if Venezuela invades.

- So far, the Hamas/Israel conflict has remained contained. We do note that Israel has been making threats to Hezbollah (see below) in Lebanon and the Houthis are continuing to attack Red Sea shipping. Shippers are starting to avoid the area. There is still a chance that the war expands but, so far, Iran seems to prefer to keep it contained.

- The covert conflict between Israel and Iran is said to be continuing unabated.

- Israel is also facing increasing attacks on its northern border. Although they have not escalated to the point where Israel is moving to invade, the Netanyahu government might conclude that since it is already at war it might as well build wider buffers on its borders.

Alternative Energy/Policy News:

- Last week, we noted that COP28 included a nuclear energy push, supported by the U.S. But, once again, China appears to be dominating the effort. China has unveiled a fourth generation reactor, making it the leader in this technology. Perhaps even more troubling is that China is apparently trying to hoard uranium. The country’s buying behavior has sent uranium prices up 70% this year.

- The House has passed a bill banning the import of Russian uranium for nuclear power. However, the bill has an “out” clause that will allow for imports if other viable sources aren’t available.

- Nuclear startups are facing increased difficulty in raising funding and managing the thicket of regulation surrounding nuclear power.

- It is becoming increasingly clear that the U.S. will forego using Chinese EV components, which will slow the adoption of EVs but allow for a domestic industry to develop.

- Additional evidence of weakening EV demand comes from Ford (F, $10.98), which is cutting production of its F-150 Lightening truck.

Is It Different This Time? (December 2023)

A Report from the Value Equities Investment Committee | PDF

For the better part of the past seven years, the broad indexes have been driven by the strength of a handful of mega-cap technology-oriented businesses, namely: Alphabet, Amazon, Apple, Meta, Microsoft, NVIDIA, and Tesla. The narrow focus is beginning to cause some investors to question if there has been a permanent shift in the investment environment, a shift that is so noticeably different from the past that we need to discard the traditional rules of investing and conclude that “this time is different.” That last phrase is credited to Sir John Templeton, investor and philanthropist, who often stated that those are the four most dangerous words for investors. Heeding Sir John’s advice, one should be wary of assuming that current market conditions and trends will persist indefinitely. The failure to recognize underlying similarities to past events may lead to irrational expectations and imprudent investment decisions. This Value Equity Insights report strives to offer some perspective on the bifurcation that has occurred in the current market and provide some historical context in order to help investors navigate the investment landscape more safely.

Background

The market cap-weighted indexes, such as the S&P 500, have been heavily influenced of late by the mega-cap names, and more specifically, the seven technology-oriented businesses mentioned earlier which have been referred to in the media as the Magnificent Seven (M7) due to their recent stellar returns. While the M7 businesses have benefited from a handful of trends centered around a more connected, intelligent, and mobile society (not to mention the COVID lockdowns), their relative stock performance has created a bifurcated and very concentrated market, one that has parallels to many of the past periods of excessive exuberance.

Asset Allocation Quarterly (Fourth Quarter 2023)

by the Asset Allocation Committee | PDF

- Our three-year forecast includes a relatively mild recession followed by a recovery and the prospect for an economic expansion.

- Geopolitical tensions are elevated with heightened potential for increased turmoil in the Middle East.

- Inflation should moderate in the near-term but may reaccelerate within the forecast period due to structural influences such as deglobalization and labor market tightness.

- The Fed’s monetary policy is likely to ease as economic conditions slow, and we expect a measured and careful approach by the FOMC as the presidential elections draw near.

- We have extended duration by stepping into long-term Treasury bonds for their safety element.

- In domestic equities, we maintain our value bias as well as cyclical sectors and quality factors.

- Exposure to international developed markets was reduced due to continued monetary policy tightening from most developed market central banks.

ECONOMIC VIEWPOINTS

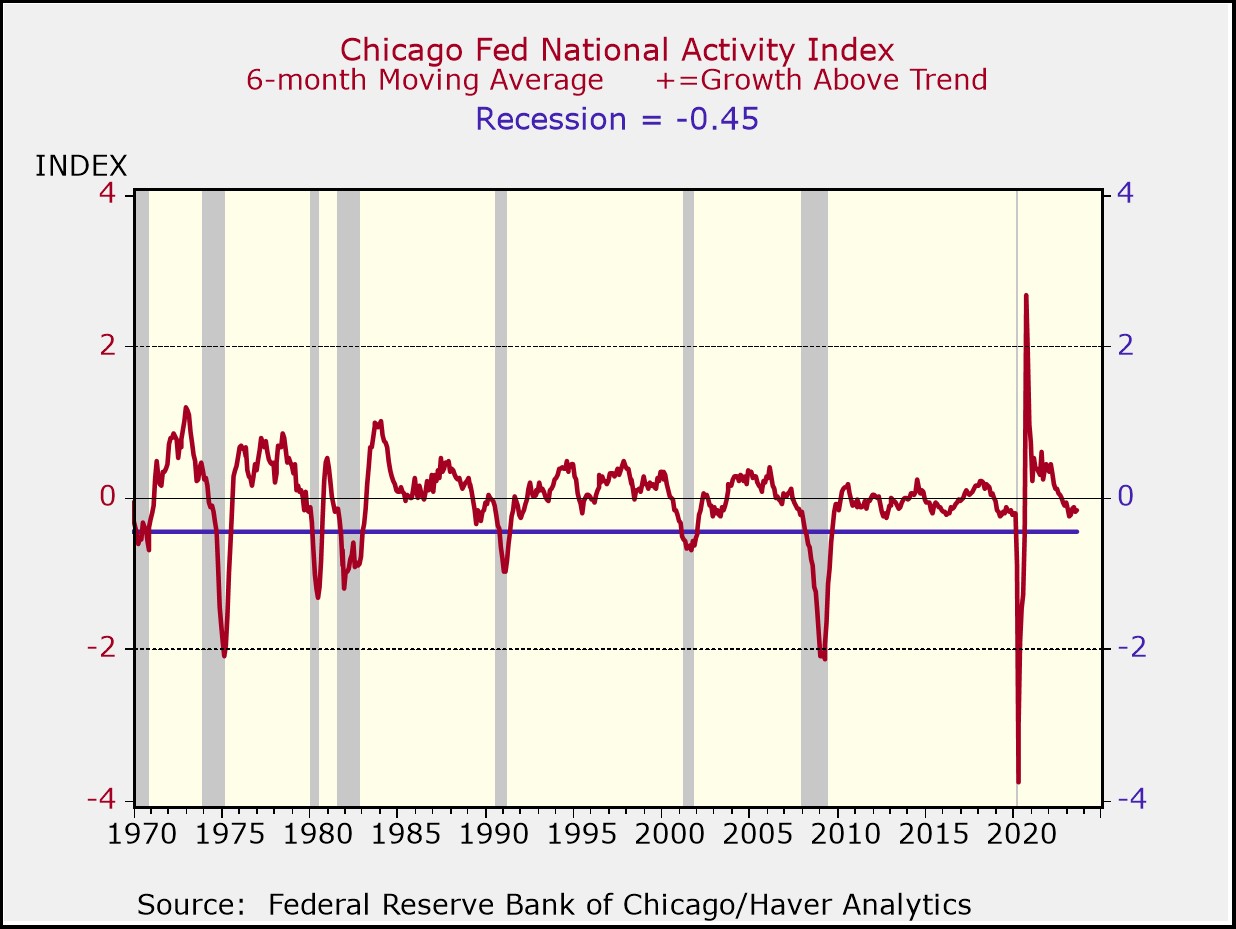

We are still anticipating a mild recession followed by a recovery within our three-year forecast period. While GDP growth has been positive, real-time indicators, such as the Chicago Fed Activity Index and the LEI, are exhibiting slowing growth. The long wait for an impending recession is a self-destructing prophecy to a degree—the more time that market participants have to prepare for a recession, the more opportunity they have to right-size their balance sheets and the less severe the recession is likely to be. Additionally, the Fed is close to, if not at, peak fed funds rates according to many indicators. No further hikes would support the economy and possibly avert a recession but would also allow inflation to run higher than the Fed’s 2% target rate.

Inflation has fallen recently, likely in response to the short-term smoothing of supply-chain problems and tighter monetary policy. Our expectation is that the volatility of inflation will be elevated within the forecast period due to underlying structural issues, such as deglobalization and labor market tightness. The U.S. labor market is expected to remain tight due to demographic shifts following the pandemic-prompted constriction of the 55+ age group labor pool and changing immigration policies. While the workforce is constrained, demand for workers has remained strong due to labor-hoarding and re-shoring. This has caused wage growth to persist at higher levels as compared to pre-pandemic periods. More importantly, wage growth has exceeded inflation over the past few months.

A significant longer-term mega-trend supporting domestic economic activity is the re-shoring of manufacturing capacity, including domestic reindustrialization and shortening supply-chains. Geopolitical tensions are likely to remain elevated, further encouraging international polarization into geopolitical blocs. Corporate fixed-asset investment, a proxy for manufacturing capacity expenditures, has been strong following the passage of the CHIPS and Inflation Reduction Acts. Capacity buildouts are multi-year endeavors, which will place increasing demands on construction, labor, and materials initially and skilled labor to operate in the long-term. We believe these pressures, combined with general supply-chain complexities, will further expose inflationary bottlenecks within the economy that will magnify inflation volatility.

The consequences of deglobalization are unfolding, such as the ongoing war in Ukraine and a geopolitical tragedy in the Middle East, which bear the potential to escalate unexpectedly and swiftly. Moreover, while the 2024 U.S. presidential election is rapidly approaching, the market is typically less concerned with the specific election outcome but it does have an aversion to uncertainty. From a market volatility perspective, a quick resolution to the primaries would be beneficial.

STOCK MARKET OUTLOOK

Given the long anticipation of a recession, corporations have likely had opportunity to optimize their inventories and liabilities, hence a deep recession is less likely. Additionally, domestic equity valuations could be supported by U.S. investors repatriating capital due to global geopolitical tensions and the historically high level of cash on the sidelines. Currently, the Technology sector accounts for approximately 28% of the S&P 500, and while optimism around AI and machine learning is strong, earnings within the sector have not kept up with the optimism. It will likely take years for AI to translate to productive uses, similarly to other transformational innovation such as the internet, electricity, and automobiles. In addition to our style tilt toward value over growth, we retain our Aerospace & Defense position and cyclical sector overweights in Energy, Metals & Mining, and Industrials. Remilitarization is accelerating as we see increased conflicts globally. The Mining and Energy sectors are likely to benefit from electrification/green energy policies as electrification is metals heavy.

We remain committed to our value bias across all market capitalizations. We view the sustainability of earnings growth as more attractive in equities categorized as value, with their valuation multiples remaining modest compared to historical data. In addition, the value style has a lower exposure to sectors that we view as overpriced. Although growth has vastly outperformed value year-to-date, we anticipate that we are in the early stages of a value outperformance cycle.

We believe that small and mid-capitalization stock valuations are attractive, with fundamentals continuing to be healthy. Mid-cap stocks remain at historically wide valuation discounts to large cap stocks. We maintain the quality factor, which screens for profitability, leverage, and cash flows, in our small and mid-cap exposures to limit potential risks during economic volatility. This quarter, we introduced a position in a uranium producers industry ETF within our mid-cap exposure. The changing nature of baseload energy production and the policies shaping it have created an opportunity for nuclear energy. Green energy policies have set ambitious goals for reducing fossil fuel usage, while the new green energy technologies cannot currently produce energy to the scale and consistency needed. With the supply of uranium having become crimped over the past decade, we view the supply/demand imbalance to offer a solid opportunity for the exposure.

We reduced our exposure to international developed equities in several strategies, but allocations remain in the more risk-tolerant portfolios. Although valuations remain low, risks have increased. Most developed market central banks persist on the tightening path in an attempt to control inflation. At the same time, economic growth is showing signs of slowing. This creates an environment for potential policy-driven errors. Given the increased geopolitical risks and re-shoring supply-chain activity, the U.S. dollar strength cycle has the potential to extend further than previously anticipated, resulting in additional downward pressure on international equities. Accordingly, in the Aggressive Growth strategy, we exited the emerging markets position due to increased geopolitical and economic growth risks. We believe that return/risk trade-offs are more attractively presented in domestic equities for the more risk-accepting portfolios.

BOND MARKET OUTLOOK

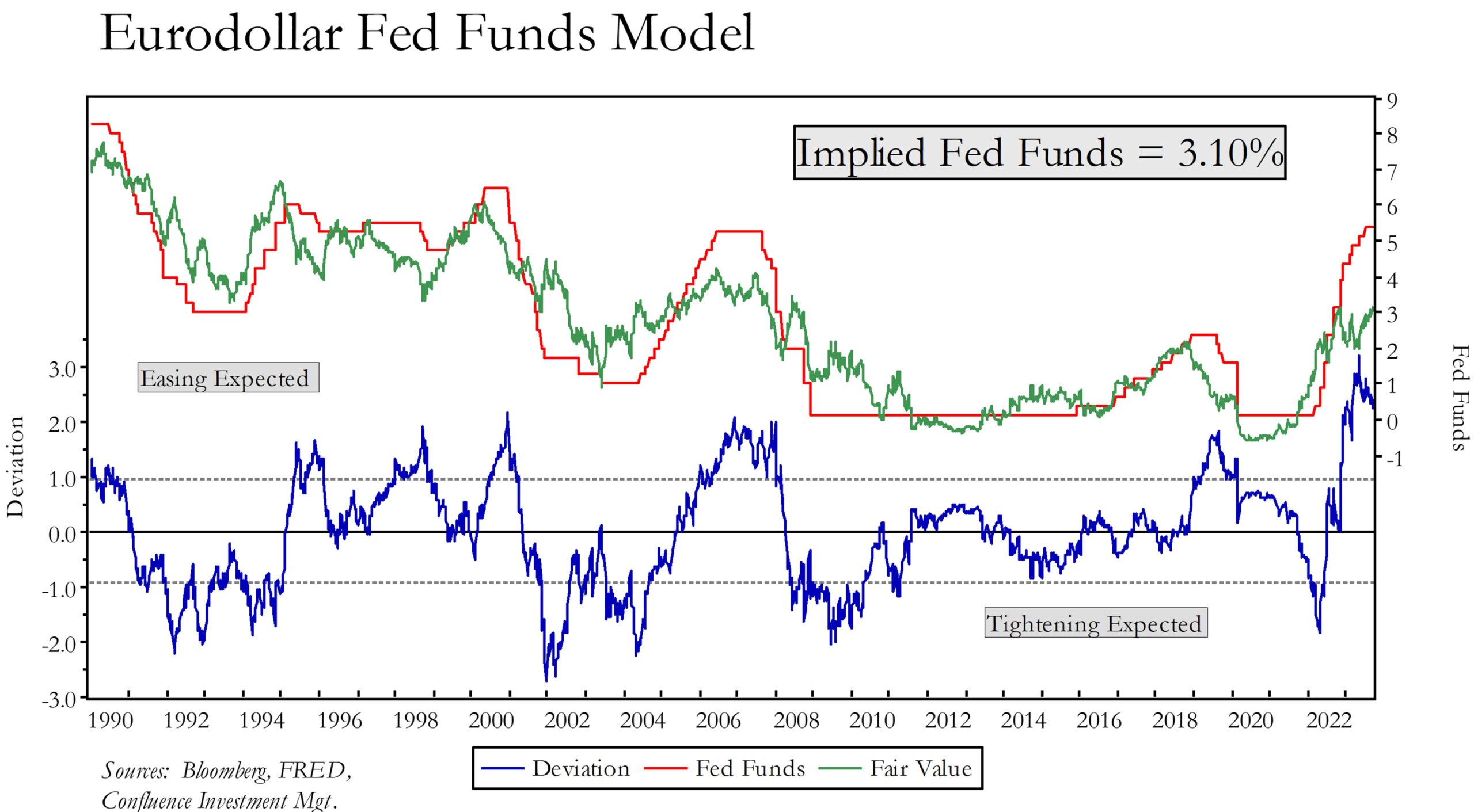

Although the quarter commenced with the market split in its anticipation of a Fed pause versus another increase in the fed funds rate prior to year-end, we believe that inflation will continue to moderate over the next several quarters and, accordingly, the Fed’s monetary policy will begin to ease. This chart indicates that the fed funds rate is well above its implied rate. Naturally there are potential curbs to our assessment, such as the structural forces of deglobalization that have the potential to keep inflation elevated above the Fed’s 2% target. Moreover, the aforementioned mega-trends will likely lead to greater volatility of inflation, especially relative to the docile environment that persisted during the period following the Great Financial Crisis. Nevertheless, the near-term outlook is for the inflation-fighting vehemence of the Fed to modulate, especially as the composition of its voting members turns more dovish next year. Consequently, we find the duration trade to be less fraught with the potential for turbulence that has existed since early 2022, and we expect the yield curve will flatten from its current inversion. This lends us the latitude to extend duration in the strategies from their prior concentration in the short-end and even place limited exposure to long-term U.S. Treasuries to hedge against the potential for even more increased geopolitical risks or a more severe recession.

The expectation for an economic contraction encourages a degree of caution toward investment-grade corporates. While companies carrying investment-grade ratings have sound balance sheets and have termed out their debt, thus avoiding a “debt wall” in the near-term, spreads to Treasuries remain contained relative to historical averages. In contrast, spreads on speculative grade bonds have risen to the point where we find it advantageous to selectively add to our exposure. Although the refinancing wave is poised to affect companies rated B and below over the next two years, with attendant difficulties for their cost of capital, our spec bond position is strictly held in the BB-rated segment which has little exposure to floating rate debt and can be characterized as an equity surrogate where incorporated.

OTHER MARKETS

Despite the currently low valuations of REITs, we expect the sector to continue to lag heading into an economic contraction and a continued high interest rate environment. Therefore, allocations to REITs remain absent in all strategies. In the commodity segment, we maintain a position in gold as a flight to safety asset during economic contractions and as a hedge against elevated geopolitical risks. For portfolios where the allocation to commodities is larger than 5%, we are adding a position in a broad-based commodity ETF with exposure to oil, gas, metals, and agriculture. Turmoil in the Middle East tends to support the broad commodity complex, especially oil and its derivatives.