by Thomas Wash | PDF

The Federal Reserve’s preferred gauge of price inflation is set for a methodological update, as the Bureau of Economic Analysis (BEA) is expected to implement revisions to its price index for Personal Consumption Expenditures (PCE) as early as September. Early estimates suggest the changes will modestly lower measured PCE inflation, potentially easing the path toward the Fed’s 2% target by reducing the index’s sensitivity to the AI-driven stock market rally.

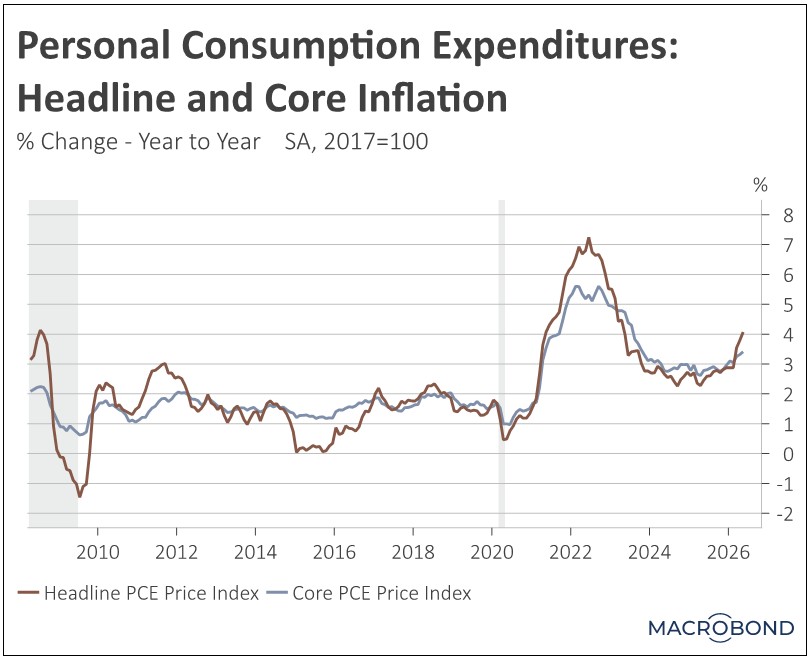

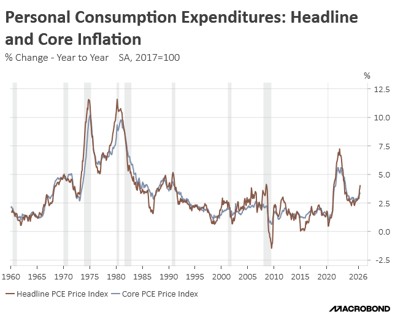

The timing is notable. As shown in the chart below, the Fed has failed to achieve its inflation objective over the past five years, and a downward shift in the index could finally make the target more attainable — both mechanically and in perception.

The revisions to the PCE price index, scheduled for incorporation in the September 30 release, aim to better align the index with actual household spending patterns. Key changes include updates to core inflation calculations and modifications to several categories that have disproportionately influenced recent readings, namely legal services, portfolio management, and computer software and accessories.

The most consequential adjustments are likely to come from portfolio management and software-related components. The BEA will revise its software price index — an area that has been distorted by the surge in AI-fueled demand — by incorporating a broader set of prices, including video game software and web hosting services. This change is expected to lower measured inflation by roughly 0.1 percentage points.

In parallel, the treatment of portfolio management services will shift away from a fee structure tied to assets under management and toward a measure based on firm revenues relative to services rendered. This adjustment is expected to reduce inflation by an additional 0.2 percentage points. Legal services will also be revised, with greater reliance on producer price data, though the impact there is likely to be more modest.

These changes are small but important, since these components have contributed disproportionately to volatility in the core PCE index. While the components account for roughly 4% of the core PCE index, they represent just over 1% of the core consumer price index, underscoring their outsized influence. Their growing weight has amplified swings in measured inflation, complicating the Fed’s effort to return inflation sustainably to target following years of overshooting.

The divergence largely reflects differences in weighting methodology. PCE weights adjust dynamically with shifts in consumer spending, and in recent years, portfolio management services have captured a larger share of expenditures amid rising retail participation in financial markets. At the same time, the recent surge in demand for computing and software has increased the relative weight of technology-related categories.

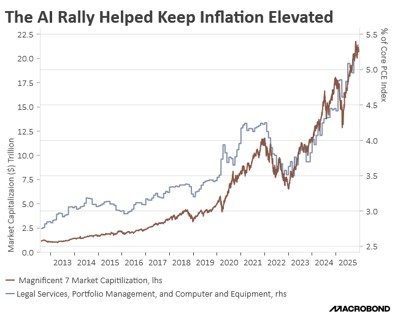

As a result, the PCE price index has become more sensitive to equity market dynamics. The chart above highlights the close relationship between rising asset prices and the growing influence of these components, suggesting that a portion of recent inflation pressure has been indirectly linked to strong market performance. This relationship has not gone unnoticed by Fed Governor Miran, who has suggested that a strong stock market should not count toward inflation.

These revisions will likely lower recent PCE inflation readings, implying that the Fed may have been closer to its 2% target than previously estimated. The most meaningful adjustments stem from changes to portfolio management and software-related categories, which should moderate the influence that the AI-driven surge in equity and software prices has had on the index.

However, this comes with a trade-off. By dampening the sensitivity of these components, the index may become less responsive to downside moves in asset prices. In the event of a correction, particularly if the AI rally were to reverse, the disinflationary impulse flowing through these channels could be more muted.

In short, the revisions may bring measured inflation closer to target, but they do not necessarily make underlying inflation easier to achieve or sustain at that level.