by Thomas Wash | PDF

The business cycle has a major impact on financial markets; recessions usually accompany bear markets in equities. The intention of this report is to keep our readers apprised of the potential for recession, updated on a monthly basis. Although it isn’t the final word on our views about recession, it is part of our process in signaling the potential for a downturn.

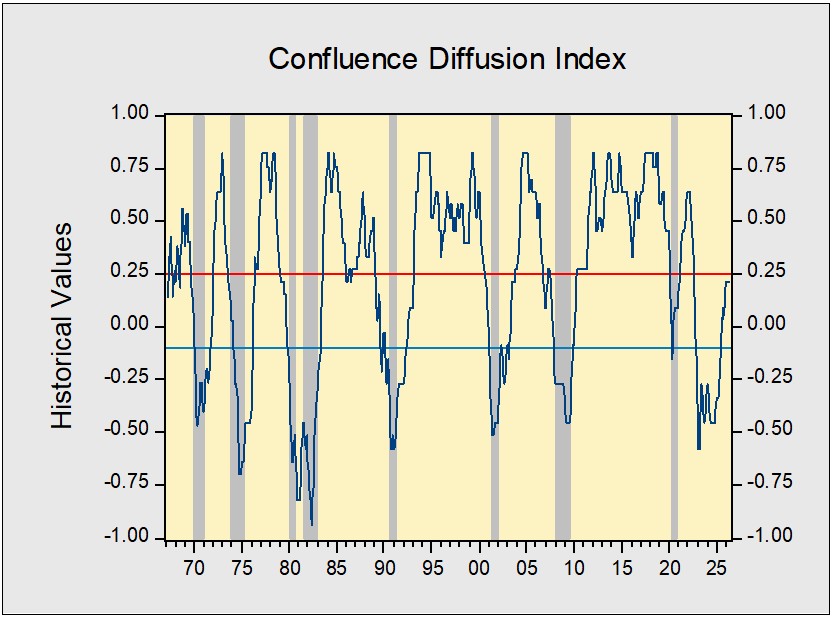

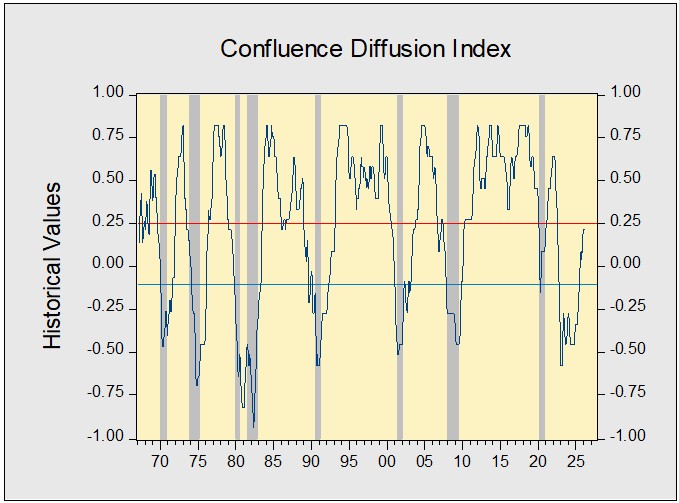

The US economy expanded further in June, continuing to demonstrate resilience. Our proprietary Confluence Diffusion Index held in expansionary territory for the seventeenth consecutive month. While the broader economy continues to be in good shape, we are closely watching a few key areas. Market sentiment is losing momentum, weighed down by geopolitical uncertainty and stretched valuations. Additionally, investment spending remains concentrated in just a few sectors where demand is high, while hiring appears poised to slow in the coming months.

Financial Markets

Markets reduced duration exposure amid ongoing geopolitical tensions in the Middle East and growing concerns over the sustainability of AI-related investments. The yield curve flattened as investors began recalibrating their expectations around interest rate hikes, driven by fears that escalating regional uncertainty could stoke inflation and prompt a response from the Federal Reserve. At the same time, rising capital expenditure among major tech companies has fueled worries that these firms may struggle to return capital to shareholders. In response, investors have rotated toward more undervalued sectors. However, given the market’s heavy tech weighting, this rotation has tempered the broader index gains, resulting in a more subdued rise in overall stock prices.

Goods Production & Sentiment

Overall production remains solid, though sentiment among both households and firms is subdued. Housing starts picked up, and spending on capital goods continued at elevated levels. This uptick in activity may partly reflect renewed optimism following a cooling of US-Iran tensions in June. Still, a sense of uncertainty persisted. While factory deliveries improved, overall manufacturing sentiment declined, weighed down by ongoing concerns over persistently high prices. Consumer sentiment edged up from the previous month but still sits below year-ago levels, suggesting that households remain cautious, likely due to worries about inflation. Despite this, spending continues to hold up well.

Labor Market

The job market continues to signal a low-hire, low-fire environment. June employment data came in well below expectations at 57,000 jobs added compared with the consensus forecast of 115,000. The subdued pace of job growth comes as hiring remains fairly concentrated in healthcare services. That said, the unemployment rate edged down slightly from 4.3% to 4.2%, while overall jobless claims continue to trend lower, suggesting that firms are satisfied with current employment levels.

Outlook & Risks

This month’s economic data suggests that the economy is still relatively stable, given the ongoing uncertainty surrounding the Middle East and AI. The resilience appears to be driven by strong demand, supported by a still-tight labor market and a robust push to build out infrastructure to meet growing AI-related needs. While we believe that inflation remains a risk, we continue to expect the economy to expand, likely at a moderate pace over the next 12 months.

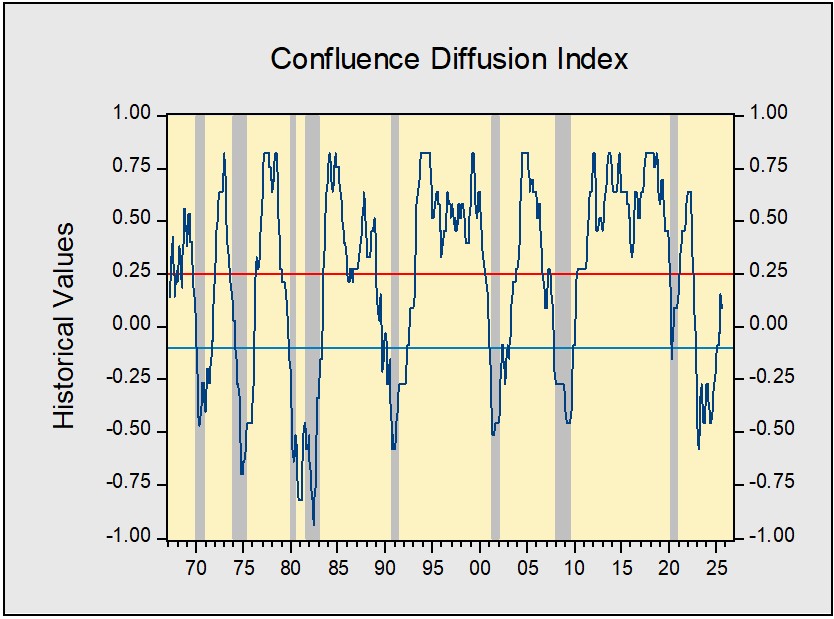

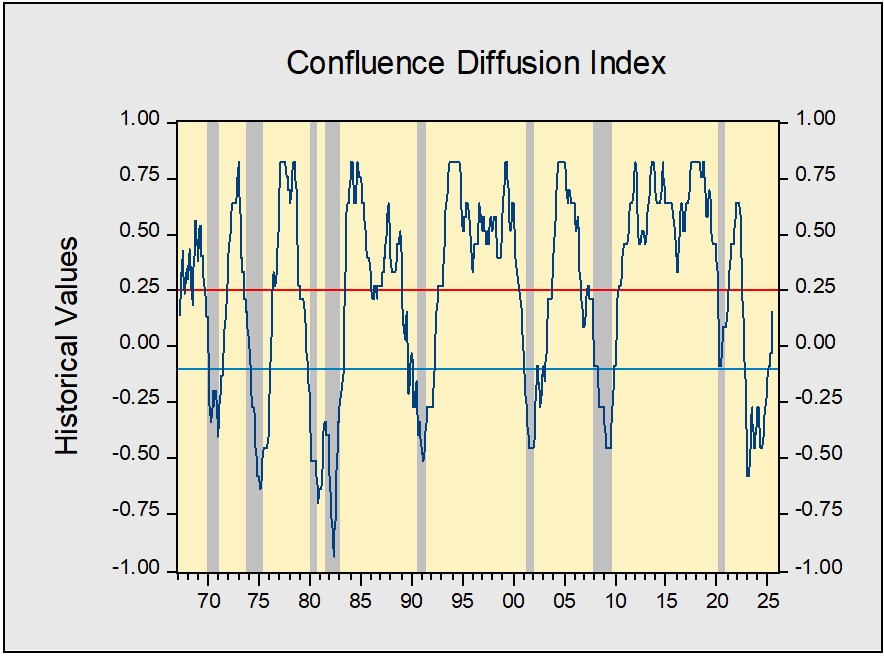

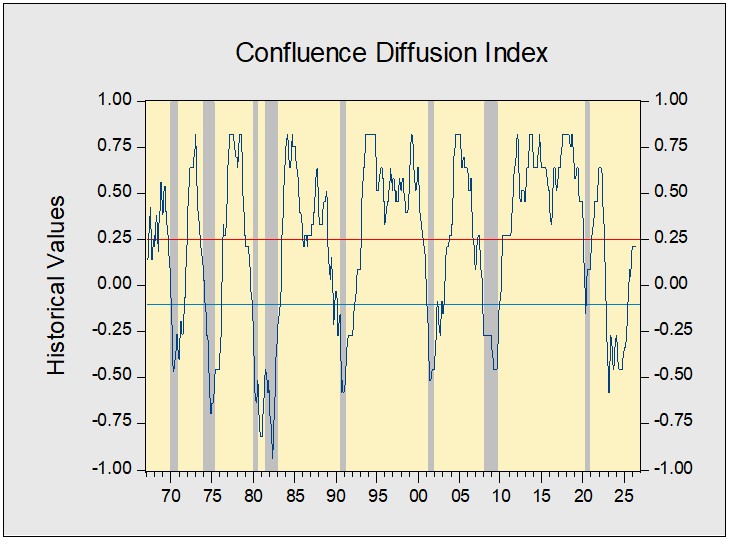

The Confluence Diffusion Index for July, which provides a composite view of the economy based on 11 benchmarks, stayed in expansionary territory based on June data. The index’s value was unchanged at +0.2121, well above the recovery signal threshold of −0.1000. The index shows that the economy remains resilient in the face of geopolitical shocks. Only three of the 11 benchmarks are in contraction, up one from last month.

- Equities cooled amid rising uncertainty over the Middle East and AI-related headwinds.

- Inflation fears eased, supported by progress toward resolving the conflict in Iran.

- The labor market continues to be tight, though demand appears to be gradually fading.

The chart above shows the Confluence Diffusion Index. It uses a three-month moving average of 11 leading indicators to track the state of the business cycle. The red line signals when the business cycle is headed toward a contraction, while the blue line signals when the business cycle is in recovery. The diffusion index currently provides about six months of lead time for a contraction and five months of lead time for recovery. Continue reading for an in-depth understanding of how the indicators are performing. At the end of the report, the Glossary of Charts describes each chart and its measures. In addition, a chart title listed in red indicates that the index is signaling recession.