Tag: China

Bi-Weekly Geopolitical Report – Dragon Boat Diplomacy: China’s Outreach to US Citizens (July 13, 2026)

by Patrick Fearon-Hernandez, CFA | PDF

Developing global macro investment strategy doesn’t just involve geopolitical analysis, economic studies, and financial modeling — or at least it shouldn’t be limited to those disciplines. Relationships and conversations in real life can be just as important. To illustrate why, this edition of our Bi-Weekly Geopolitical Report discusses a reception and cultural performances that the author recently attended at the Embassy of the People’s Republic of China in Washington, DC. The experience offered an opportunity not only to see modern public diplomacy in practice, but also to assess Chinese cultural outreach in real life.

Serious geopolitical and investment research can certainly be focused on analyzing written reports and quantitative data. However, direct engagement with policymakers, diplomats, business leaders, and practitioners often provides context and perspectives that can’t be captured through analysis conducted strictly back at the home office. We therefore describe the event to illustrate the principle. As always, we wrap up the discussion with some implications for investment strategy.

Don’t miss our accompanying podcasts, available on our website and most podcast platforms: Apple | Spotify

Asset Allocation Bi-Weekly – #164 “China Cuts Its Energy Imports” (Posted 6/15/26)

Asset Allocation Bi-Weekly – China Cuts Its Energy Imports (June 15, 2026)

by Patrick Fearon-Hernandez, CFA | PDF

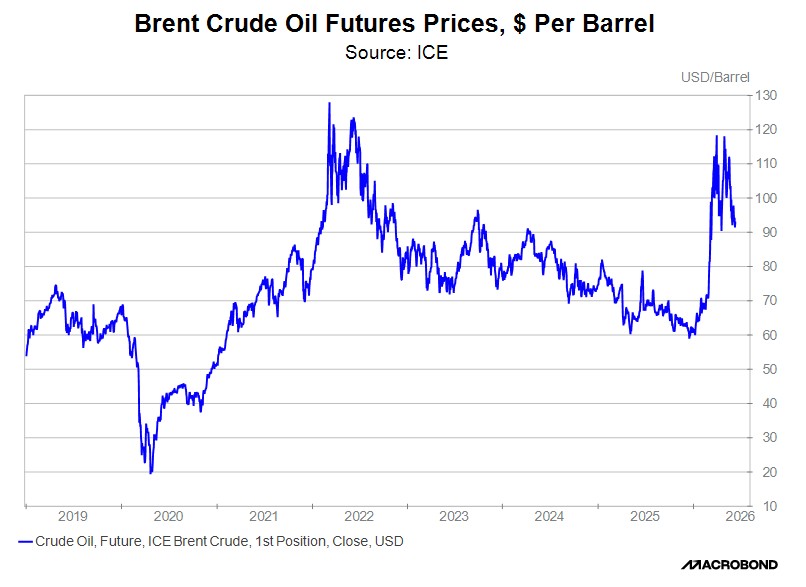

As we’ve noted before, the most immediate economic and financial market risk from the Iran war is the possibility of further price hikes for oil, natural gas, and some other commodities that depend heavily on shipping through the Strait of Hormuz. Because of the war, the strait has now been essentially shut down for more than three months. Global energy and other commodity prices have indeed increased. As shown in the chart below, near Brent crude oil futures prices jumped approximately 50% in the weeks after the war started on February 28. However, the escalation in prices has been relatively contained and prices have even started to fall back recently. That’s despite assurances from economists and energy analysts that prolonged closure of the strait would inevitably lead to further price hikes. In this report, we show that a massive pullback in Chinese energy imports has probably been a key reason why prices haven’t risen as much as feared, at least so far. We also show that the pullback in Chinese energy demand has helped set the stage for recent stock market dynamics.

The unexpected pullback in energy prices was a mystery in recent weeks, especially since official data and anecdotes suggested that the closure of the strait was forcing countries around the world to use up their inventories. For example, the International Energy Agency warned in its May market review: “The world is drawing oil inventories at a record pace as importing countries confront unprecedented disruptions to Middle Eastern supplies.” According to the IEA, global oil stocks had plummeted by almost 250 million barrels since the start of the war, with even steeper declines if stranded stockpiles in the Middle East are excluded. Such inventory depletion would normally be expected to boost prices.

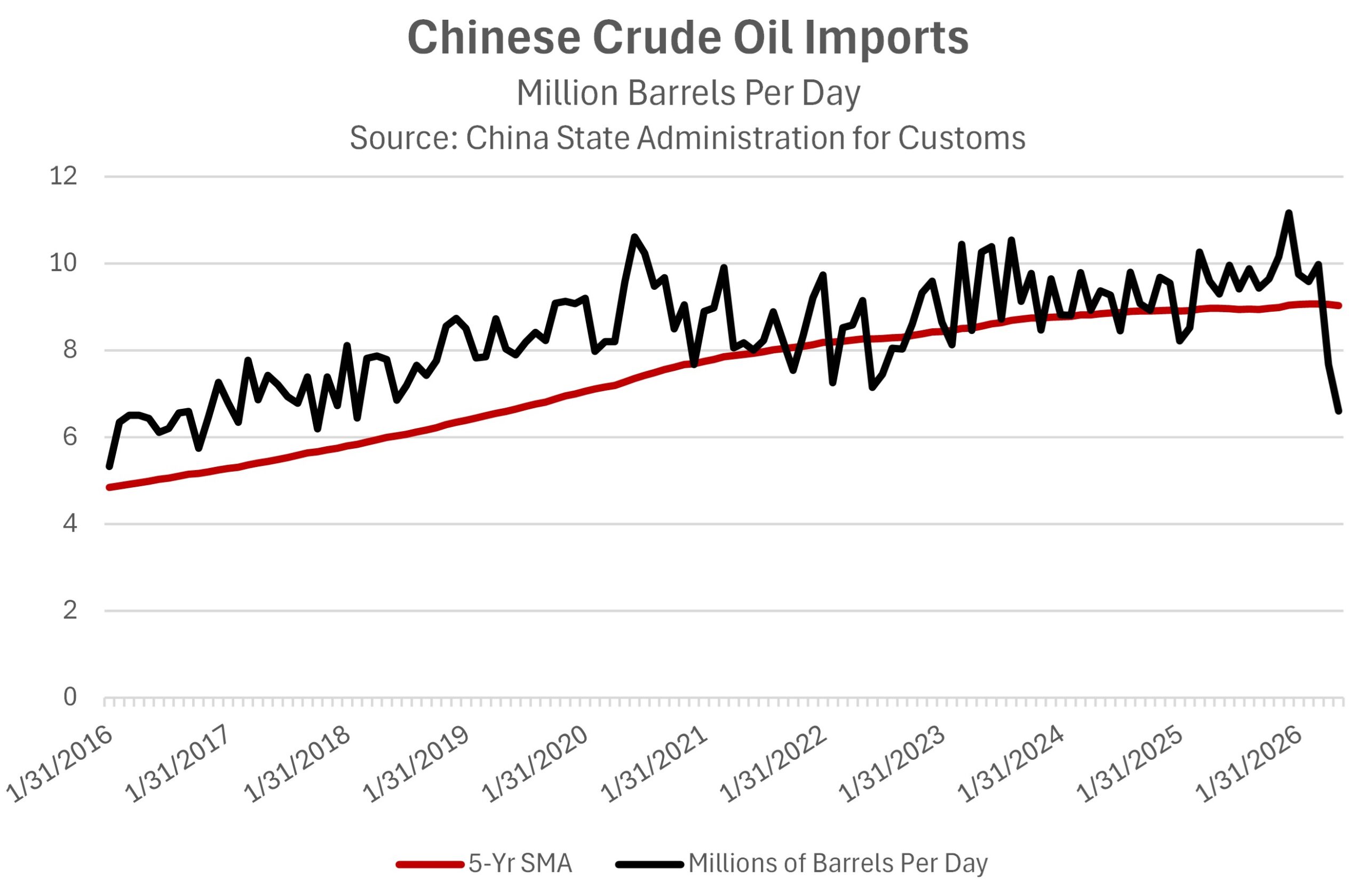

More recent data appears to solve the mystery about why energy prices haven’t risen further and have even fallen back. Recent data shows Chinese oil imports have dropped to approximately 6.6 million barrels per day, down 38% from the average of about 10.6 mbpd in 2025. The drop of about 4.0 mbpd equates to almost 4% of current global oil demand. It could also offset much of the net reduction in global oil shipments through the strait, which analysts estimate to be between 6.0 and 12.0 mbpd.

Chinese energy imports and inventories are notoriously opaque, so these figures are uncertain. Nevertheless, if China really has cut its energy imports as indicated, it would go far toward explaining why energy prices have started to pull back, at least for now. We still believe that a long delay in opening the strait would keep alive the risk of further energy inventory depletion and renewed price spikes. However, China’s apparent disdain for paying elevated prices and its willingness to cut back deliveries is having a salutary impact on global prices and helping calm the world’s financial markets for now.

Going forward, if this trend continues, it will have big implications. For example, China’s ability to forego expensive energy imports helps validate its “all of the above” energy policy, in which it has invested in the full span of possible energy sources, ranging from coal, oil, and natural gas to nuclear, wind, and solar. China is now benefiting from the flexibility it has gained from having such a broad array of energy sources. We also think this situation illustrates how much economic flexibility China has gained from building its enormous strategic reserves of energy and other commodities. Although China won’t reveal the true level of its inventories, outside analysts estimate that they are currently several times bigger than the US’s Strategic Petroleum Reserve. It would be no surprise if governments around the world now take a lesson from China’s approach and try to adopt a similar all-of-the-above energy policy and start rebuilding inventories once the war is over and prices come back down.

For the financial markets, the decline in oil prices wrought by China’s import cuts has probably been a key reason for the recent modest retreat in inflation concerns and in government bond yields. For example, the yield on 10-year Treasury notes fell from about 4.65% in mid-May to about 4.45% at the start of June. We suspect this has encouraged investors to return to the frenzied buying of US large cap technology stocks related to artificial intelligence. It has also arrested investors’ early 2026 rotation toward value stocks. As we noted above, however, the continued war in Iran is likely still depleting energy inventories around the world, including in China. That likely translates into a continued risk of further energy price spikes and rising bond yields in the coming months if the war isn’t resolved.

Don’t miss our accompanying podcasts, available on our website and most podcast platforms: Apple | Spotify

Bi-Weekly Geopolitical Podcast – #82 “The Great Chinese Purge” (Posted 2/27/26)

Bi-Weekly Geopolitical Report – The Great Chinese Purge (February 23, 2026)

by Patrick Fearon-Hernandez, CFA | PDF

One defining feature of the world today is the large share of the global population living under political systems that are authoritarian or moving in that direction. With 1.405 billion people, or about 18% of the global population total, China is the best example of that. Still, we suspect that many people in the West don’t appreciate how authoritarian the country is or how this structure can affect investment prospects both within China and around the world. After all, the end of the Cold War in 1991 allowed many in the West to adopt the pleasant notion that Communist dictatorship was a thing of the past. The great Chinese economic opening and reform program of the last four decades also helped obscure what was happening on the ground from Tibet to Hong Kong.

Now, under General Secretary Xi, a long program of purges in the Chinese military and defense industry has come to a head, driving home just how authoritarian the country has become again. In this report, we examine the purges and their potentially large implications for whether China launches a military seizure of Taiwan and discuss the likelihood that China can remain stable in the event that Xi dies or is incapacitated. As always, we wrap up with a discussion of the ramifications for investors.

Don’t miss our accompanying podcasts, available on our website and most podcast platforms: Apple | Spotify

Confluence Mailbag – #7 “Global Shifts and the Next Market Drivers” (Posted 2/5/26)

Bi-Weekly Geopolitical Podcast – #79 “Investment Implications of the New US National Security Strategy” (Posted 1/12/26)

Bi-Weekly Geopolitical Report – Investment Implications of the New US National Security Strategy (January 12, 2026)

by Patrick Fearon-Hernandez, CFA | PDF

As required by law, the new United States administration released its updated National Security Strategy in December 2025 (NSS 2025). As many observers have noted, the document marks a dramatic shift from the traditional NSS documents of the Cold War and the Globalization eras, not only in terms of threat assessments and priority initiatives, but also in terms of length, tone, and focus. In this report, we drill down to the investment implications of the new strategy if it is implemented as written. Our bottom-line assessment is that the new strategy could lead to significant changes in the global security environment, which in turn portends big potential changes in the global investment environment as well. The new strategy could mean significant shifts in global trade and investment flows, in the nature and origin of investment risks, in the policy responses that might be expected in a crisis, and among the most important policymakers worldwide.

Since we at Confluence have long tracked the evolving geopolitical landscape and identified many of the changes now incorporated in NSS 2025, we have been ahead of the game in adjusting our global strategies. Many of the investment implications we identify here are consistent with the ideas we have presented previously, such as a trend toward fracturing and disintegration among the nations of the world, less efficient trade and investment flows, and increased risk of conflict. In this report, we also offer several new ideas that complement these observations.