by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Good morning! The market is currently digesting the latest tariff announcements from the president. In sports news, OKC Thunder guard Shai Gilgeous-Alexander scored 51 points in the team’s recent victory, making his team the first in the competitive Western Conference to reach 50 wins this season. Today’s Comment will explore how tariffs are already impacting economic activity, why the Federal Reserve’s independence is being called into question, and other market-related developments. As usual, the report will also cover key domestic and international data releases.

Stagflation Fears Rise: The latest Purchasing Managers’ Index (PMI) from the Institute for Supply Management revealed that manufacturing output growth has stagnated, while prices surged at their fastest pace since 2022. The weak reading has heightened concerns that ongoing trade tensions are starting to weigh on economic output.

- The February ISM Manufacturing Index came in at 50.3, down from the previous month’s reading of 50.9. Although the report remained above the contraction threshold of 50, the expansion was primarily driven by a sharp increase in manufacturing prices, which have reached their highest level since June 2022. Meanwhile, new orders and employment both fell into contraction territory.

- While the recent reading remained above the 12-month average of 48.6, the frequent mentions of uncertainty among respondents suggest that firms are growing more concerned about their economic prospects in the future. Their worries appear to center on navigating US trade tensions with Mexico, Canada, and China, as businesses struggle to determine how to invest in this evolving environment. This challenge is further compounded by fluctuating tariff rates and uncertainty over potential policy responses.

- On Monday, President Trump announced plans to follow through on his threat to impose tariffs as a punitive measure against countries he claims are not doing enough to curb the flow of fentanyl into the US. Mexico and Canada will face a 25% tariff on all goods, with the exception of Canadian energy products, which will be subject to a lower import tax of 10%. Meanwhile, tariffs on Chinese goods will double from 10% to 20%. He is also weighing additional tariffs on steel, aluminum, and food imports.

- In response, Canada has imposed a 25% tariff on $20.6 billion worth of US goods, including orange juice, peanut butter, wine, and coffee. A second round of tariffs targeting cars, trucks, and steel is also expected to take effect in the coming weeks. Meanwhile, China has retaliated by targeting US agricultural products with a 15% tariff, and Mexico plans to announce its response later today.

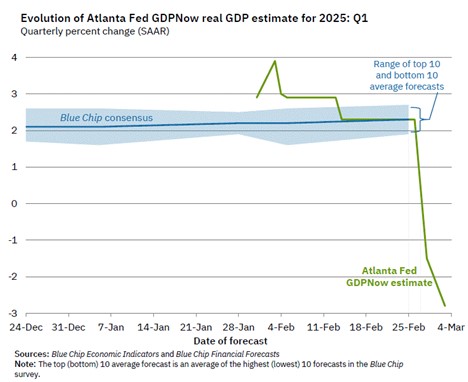

- Economic data is already beginning to reflect the impact of trade war concerns. Following the report’s release, the Atlanta Fed’s GDPNow forecast for Q1 2025 fell further into contraction territory, dropping from -1.5% to -2.8%. This decline was driven by a rise in imports, as well as a slowdown in consumption and investment, all of which have weighed heavily on GDP growth.

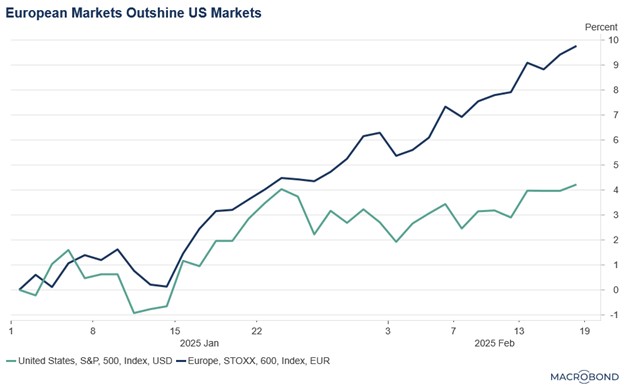

- While it is still too early to assess the full economic impact of the ongoing trade war, US equities may continue to find support as investors attempt to gauge the extent of rising trade tensions. So far, the S&P 500 has fallen by as much as 5% from its all-time high, but a rebound could occur if there are signs that these tariffs are being reversed.

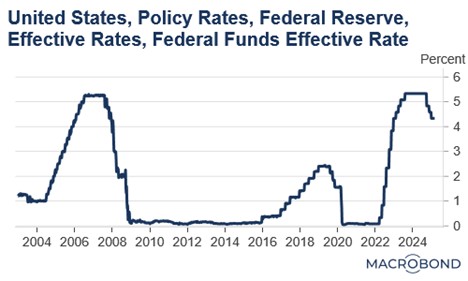

Fed Independence in Focus: A group of Republican lawmakers are turning their attention to the Federal Reserve, aiming to review the central bank’s authority over monetary policy and bank regulation. This scrutiny marks an early sign that the Fed’s independence could be at risk.

- On Tuesday, a House task force that was established to scrutinize the Fed will hold its first hearing. The committee will begin its examination of the Fed’s authority by reviewing its original 1913 charter. This review comes amid the president’s ongoing efforts to test the limits of executive authority, as he seeks to expand his control over government operations.

- While the president has shown relative restraint in his criticism of the Fed — with Treasury Secretary Scott Bessent noting that the administration aims to focus on long-term yields — he has repeatedly expressed dissatisfaction with its reluctance to cut interest rates. Several days prior to the January 28-29 FOMC meeting, President Trump went so far as to claim that he understands interest rates better than the central bank’s officials.

- Currently, pressure on the Fed is likely to undermine the central bank’s ability to maintain autonomy in its decision-making, as it grapples with inflation persistently above the 2% target and an economy showing signs of slowing. New tariffs are likely to add to those challenges as they will further contribute to price pressures at a time in which goods have been a reliable source of drag on the overall index.

- The US dollar may face significant risks from increased scrutiny of the Fed, as a perceived lack of central bank independence could undermine global confidence in investing in the United States. However, this scenario may strengthen the case for gold, as investors could turn to the precious metal as a safe-haven alternative.

US Suspends Aid: President Trump has decided to withhold additional aid to Ukraine following President Zelensky’s reluctance to agree to a peace deal without security guarantees. While the decision was widely anticipated, its potential spillover effects remain unclear.

- The order specifically targets military weapons used to prolong the conflict, as President Trump has repeatedly expressed his desire to achieve peace on the continent after years of fighting. He has also stated that he would welcome President Zelensky back to the White House once Zelensky demonstrates a genuine commitment to pursuing peace.

- In response to the US’s reluctance to provide assistance to Ukraine, Europe has swiftly moved to increase its defense spending. European Commission President Ursula von der Leyen announced that the EU will activate a mechanism enabling member states to allocate an additional 650 billion EUR ($685 billion) toward defense over the next four years. Additionally, the bloc plans to issue 150 billion EUR ($158 billion) in loans to further support these efforts.

- The combination of the US’s reluctance to provide financial support and growing doubts about its commitment to global security has sparked widespread concern. Several figures within President Trump’s orbit, including Tesla CEO Elon Musk, have openly questioned the US’s role in NATO. This has prompted European officials to pursue a dual approach with some pushing for reconciliation with the Trump administration, while others are advocating for greater unity among European nations.

- While it is unlikely that the EU will be able to fully assume responsibility for its security in the short term — given budgetary constraints and limited experience — a shift toward greater spending and independence from the US is expected to benefit European defense companies. These firms are likely to see significant gains from increased military expenditures.

Big Beautiful Bill: The Senate is working on revising the House budget bill to align with some of President Trump’s tax promises. However, disagreements have emerged over the figures, as the Senate aims to ensure that the budget impact from the tax changes remains minimal.

- Senate Republicans are working to revise the House budget bill, with a particular focus on the SALT (State and Local Tax) deductions, which have been a point of contention. While the House aims to raise the deduction cap, the Senate prefers to keep it at the current level.

- The two sides will need to resolve their disagreements to pass a tax bill through budget reconciliation, a process that allows them to bypass a Senate filibuster, which would otherwise require 60 votes for passage.

- While the bill is likely to pass, the scale of the tax cuts remains uncertain. That said, a final version could be ready by summer, barring any significant setbacks.