The business cycle has a major impact on financial markets; recessions usually accompany bear markets in equities. We have created this report to keep our readers apprised of the potential for recession, which we plan to update on a monthly basis. Although it isn’t the final word on our views about recession, it is part of our process in signaling the potential for a downturn.

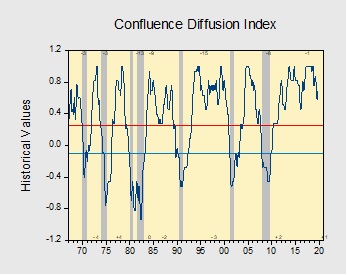

Data released for August suggests the economy is still in expansion, but a slowdown in manufacturing and signals of financial weakness continue to be a drag on the index. Currently, our diffusion index shows that nine out of 11 indicators are in expansion territory, with several indicators approaching warning territory. The index has fallen from +0.636 to +0.575.[1]

The chart above shows the Confluence Diffusion Index. It uses a three-month moving average of 11 leading indicators to track the state of the business cycle. The red line signals when the business cycle is headed toward a contraction, while the blue line signals when the business cycle is headed toward a recovery. On average, the diffusion index is currently providing about seven months of lead time for a contraction and three months of lead time for a recovery. Continue reading for a more in-depth understanding of how the indicators are performing.

A volatile day: Yesterday was a volatile day in the financial markets as two issues dominated.

The U.N. speech: President Trump’s address to the U.N. was hawkish. He reiterated his “America First” stance, criticized China for its intellectual property acquisition tactics and defended his use of tariffs. His remarks on China were quite strong, suggesting that the country’s economic development policies were unfair to the U.S. and the rest of the world, and that America’s trade policy was designed to force China to change those policies. China is continuing to make what appears to be good-will gestures on trade; today, for example, they purchased pork. However, we note that China’s pork supply situation is precarious; it is quite likely that China is framing these purchases as good-will gestures when, in reality, it really needs the “other white meat” due to supply shortages caused by the African Swine Fever virus. We also note that China wants tariffs removed as preconditions for a broader deal, which isn’t likely. Financial markets want a deal with China; it may not occur. The president also singled out Iran for its repressive regime and its threat to Middle East peace. He also argued for the defense of borders. Overall, the talk suggested that the administration was not likely to ease its stance on China, and that deglobalization remains the likely path of policy.

Impeachment: Speaker Pelosi indicated she would support an impeachment inquiry against President Trump over the Ukraine issue. Impeachment proceedings raise market uncertainty. We have only had three such events in American history, and only two in an era of modern financial markets. The events really don’t tell us much about how equity markets will behave during impeachment proceedings.

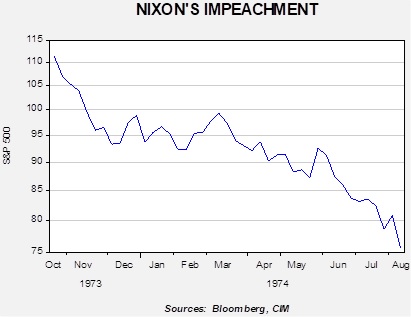

This chart shows the weekly S&P 500 Friday close. We measure the Nixon impeachment from October 9, 1973, the Friday before the “Saturday Night Massacre,” until his resignation. The Nixon impeachment event (it’s important to remember that he resigned before the articles of impeachment were sent to the Senate) occurred in a major bear market for equities. Although the political actions likely played a role in the drop, it’s important to note that the impeachment nearly coincided with a recession (the downturn began in November 1973 and continued into March 1975) and oil prices rose 235% from October 1973 to January 1974. Thus, the impeachment probably played a role in the market decline, but other factors were also important.

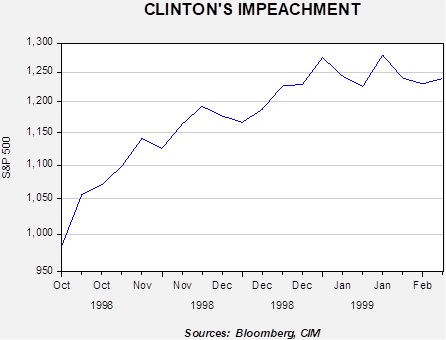

Same data as above. We time Clinton’s impeachment from the House of Representatives vote to conduct an impeachment inquiry until the president was acquitted by the Senate. The economic environment was generally positive, and equity markets were in a strong bull market. We do note that equities had declined during impeachment due to the collapse of Long-Term Capital Management, and the Russian debt default. Thus, some of the gain is exaggerated. Still, this shows that if economic and market conditions are favorable, the bearish impact of impeachment is probably muted.

So, what should we think about with this impeachment issue? Here are our preliminary thoughts:

Impeachment is not a judicial process, but a political one. Barring a revelation that is egregious, it is highly unlikely the Senate, by a two-thirds majority, will vote to enforce impeachment. In fact, it is possible that majority leader McConnell might not even hold a vote on the articles. We don’t expect the president to actually be impeached.

It will have an impact. Legislative activity will grind to a halt. USMCA probably won’t get passed this year. Congress is funding the government with short-term spending bills making the odds of a temporary closure elevated. The White House will be distracted, and due to the constant turmoil, may not have the “bench” to deal with impeachment and all the other issues the nation faces. Fortunately, the White House does have strong figures involved in the China and Europe trade negotiations. However, the bad news is that they are not always unified, and the president may struggle to act as an arbiter between the two sides if he is consumed with impeachment.

Iran may take advantage of this turmoil. The Mullahs likely believe the chances of getting a favorable deal with the U.S. improve with a different president. Thus, Iran may be emboldened to escalate tensions in the region. Under impeachment, if the president decides to attack Iran in response to an escalation, he could be accused of a “wag the dog” tactic. This accusation would not be unprecedented. President Clinton launched bombing raids on al Qaeda targets in August and December of 1998; the first occurred when Monica Lewinsky was about to testify on the scandal, and the latter as the House was about to vote on articles of impeachment. Clinton had defensible reasons for the bombing, but the timing did look suspicious. At the same time, one does not need to be a Ph.D. economist to know the global economy is weak and the U.S. economy is approaching stall speed. An event that drives oil to $100+ per barrel would probably be enough to tip the world and the U.S. into a full-blown recession. History shows that re-election during a recession is rare.

It’s late in the political cycle. Andrew Johnson’s impeachment event was also near the end of his term. In some respects, the inquiry could cloud the president’s re-election campaign. It also might garner him sympathy. However, it’s important to note that the last two impeachment events occurred in second terms. Thus, they had a different impact on the subsequent election, compared to a president under the cloud of impeachment who is running for re-election. In addition, it makes it hard for Democratic party candidates to discuss plans and goals for office when the media’s focus is mostly on the impeachment proceedings. Thus, the impeachment will also affect the Democrats nominating process. (Our quick take? The Ukraine issue probably hurts Biden and helps Warren.)

There are already warnings from commentators that this impeachment could “hurt the presidency.” If the U.S. is withdrawing from hegemony, the president’s powers, which expanded during the superpower period, will likely be curtailed over time. The Constitution has been “stretched out of shape” during America’s hegemony period mostly because a superpower has to make decisions quickly, and the weak executive envisioned by the founders doesn’t fit with hegemonic responsibilities. However, if the U.S. isn’t going to maintain its superpower role, there is less need for a strong executive. Thus, some reigning in of the executive would be expected, and this impeachment fits in that scenario.

Our focus will remain on the economy and markets. Given the tumultuous nature of the Trump presidency, the sentiment impact may not be all that profound. Financial markets have become accustomed to constant political turmoil, and thus should be able to digest this situation too. However, as noted above, we do have two concerns. First, it may be difficult to manage relations with China in the midst of this turmoil; if Lighthizer becomes the dominant figure in the chaos, there will be no deal with China. Second, we fear the financial, but especially the oil, markets are underestimating the risk of further Iranian escalation. As a result, these two areas will be where we most closely monitor events.

Wealth Tax: Presidential candidate Bernie Sanders has joined Elizabeth Warren in endorsing a tax on assets for individuals that have a net worth of more than $16 million, and married couples with a net worth of over $32 million. The revenue for the proposed tax would be used to promote government programs such as universal healthcare. In addition to its appeal to labor, the idea has become increasingly popular with members of the capital class, with Bill Gates stating that he “wouldn’t be against the tax.” Moreover, although a wealth tax makes conceptual sense, it doesn’t appear to be all that practical. The primary issue is that the value of one’s assets is somewhat subjective; therefore, there is a strong incentive for people to undervalue their assets on their tax returns. Even though the government could just send auditors to value these assets, it would likely prove overly burdensome. Another proposed solution to the problem would be for the government to have the right to buy assets at the listed price, but even that seems burdensome. However, as we have mentioned in the past, this wealth tax is just another example of the country moving away from an efficiency cycle, and into an equity cycle. We have doubts that a wealth tax will ever be enacted; other nations that have tried to implement them tended to abandon the effort because of the difficulty in processing the levy. However, the mere threat tends to have a dampening effect on asset prices.

Magnets: The U.S. is importing rare earth magnets at the fastest pace since 2016. Most likely, firms are concerned that the supply will be curtailed if the U.S. and China can’t reach a trade agreement, so they are stockpiling the materials.

The U.K. Supreme court rules against PM Johnson: In an 11-0 verdict, the U.K. high court ruled this morning that the Johnson government acted illegally when it prorogued Parliament. John Bercow, the speaker of the Parliament, has indicated lawmakers will return tomorrow morning. The GBP rallied modestly on the news. It is unclear exactly what happens now. The current government is in minority. Under current law, Johnson needs a two-thirds majority to call elections and earlier attempts to bring elections have failed. However, the official opposition party, Labour, is a mess—it is obvious the next election will be about Brexit and the party doesn’t have a clear stance. And, there is a looming deadline coming on Halloween. There is not enough time to create a new arrangement and it remains possible that the U.K. could crash out of the EU simply because no one can figure out how to avoid it. It appears the most logical solution would be a delay of Brexit and new elections to form a government with a full mandate to do something. However, it is just as likely that new elections will not bring a clear path to either leaving or staying in the EU due to the deep divisions within the U.K.

Here is a way of thinking about this issue. The EU and globalization in general offer citizens of a particular nation a tradeoff—prosperity for sovereignty. In other words, joining a supranational union (the EU), or large multinational trade deals (WTO, TPP, TTIP, NAFTA) requires participating nations to give up some level of sovereignty. In return, the broad trade arrangement makes economies more efficient and supports growth (prosperity). However, when the fruits of that prosperity are not shared among the majority of households, a common condition in Western nations at present, those “left behind” are not necessarily better off economically but have given up sovereignty as well. As a result, the position of the left-behinds is that getting sovereignty back can’t hurt, and they don’t feel they are giving up much prosperity either. This group becomes the opposition to globalization. This problem is, to some extent, the heart of the globalization debate and is key to the Brexit issue.

Isolated Iran: In a somewhat surprising development, France, Germany and the U.K. have all blamed Iran for the recent missile and drone attack on Saudi Arabia. PM Johnson has called for a new deal, which would effectively end (JCPOA). This is an interesting turn of events; the EU has created a financial workaround for Iran to continue exporting, although it hasn’t been very effective. We suspect two factors are in play. First, the EU is deeply worried that an outbreak in hostilities would lead to oil shortages negatively affecting Europe’s economy and second, we doubt these nations would make such statements if they thought the U.S. would use them to justify military action. In other words, these leading EU nations must believe that the Trump administration is not likely to use military force. Thus, the EU has turned on Iran, leaving the Mullahs increasingly isolated.

So far, the bet against the U.S. using military action against Iran has been a good one. At present, the only military action that appears to be under consideration is cyber, which has the characteristic of deniability. Despite the appearance that escalation isn’t likely, we caution that conditions can change. Iran is in a difficult spot; sanctions are crushing its economy, and the U.S. is in no hurry to negotiate. No other nations appear interested in helping them out. Desperation in Iran may lead to further aggression. The creator of the archetypes of American foreign policy, Walter Russell Mead, has an op-ed today where he notes that Trump is a Jacksonian, and he lays out “red lines” that would likely trigger a military response. For now, time is on the side of the U.S. There is no need to escalate, but that doesn’t mean Iran won’t. It is quite possible that financial markets are underestimating the chances of a conflict and higher oil prices.

We are from the government and are here to help: China announced it will place CPC officials in 100 private firms in China. The official reason given for this move is to “boost local manufacturing,” but it is rather obvious that the goal is to force these firms to follow government directives. For years, Chinese law has given the government power to place officials in firms for monitoring purposes. However, prior to Xi, firms were allowed near complete freedom to operate. That may be changing.

China and trade: Equity markets continue to tick higher on hopes of a trade thaw. Treasury Secretary Mnuchin said he expects top-level U.S. and Chinese trade negotiators to meet during the week of October 7. Mnuchin also claimed some progress was made at last week’s deputy-level meetings. However, we have two areas that suggest caution. First, the DOJ reports that China is accelerating its theft of trade secrets. Second, Matt Pottinger has been appointed deputy national security advisor. Pottinger is considered a hawk on China, meaning that an important figure in the administration will be likely framing a hostile policy toward China.

European Union-Italy: EU leaders agreed to adjust their immigration policy to help the new government in Rome. Germany and France would automatically take in some migrants rescued in the Mediterranean, while other EU nations would volunteer to take in some refugees landing in Italy. The deal could help to stabilize EU politics by undermining anti-immigrant populists.

China: Commenting on three regional banks rescued by various entities since May, central bank chief Yi warned that some regional lenders have overstretched into high-risk loans, and that their top shareholders would face “primary responsibility” if they failed. Yi said he wouldn’t sharply cut interest rates, but he did ask banks to lend more to local clients in the real economy.

Odds and ends: The opposition to Maduro in Venezuela appears to be fracturing, meaning it will be even more difficult to oust the current government. In a surprising development, the Bolsonaro government in Brazil has slashed tariffs on more than 2300 products. Traditionally, Brazil has leaned toward import substitution policies for development, meaning it created tariff barriers which allowed local firms to make goods that could be more cheaply imported. Reversing this policy will tend to lower inflation and increase productivity; it will also, at least initially, increase unemployment and local firms will face import competition.

In Part I of this report, we reviewed the U.S. current account problem and examined how the persistent deficit affects the economy. We also discussed how the U.S. current account deficit is tied to American hegemony and ways the deficit could be addressed.

This week, using the background established in Part I, we will introduce the Competitive Dollar for Jobs and Prosperity Act (CDJPA). Along with details of the proposed law, we will discuss the macroeconomics of the CDJPA and how it would affect the dollar’s reserve currency status. We will then examine the potential political effects of the bill, the likely retaliation from foreign nations and, as always, conclude with potential market ramifications.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EDT]

Happy Monday! It’s the Autumnal Equinox today. For sports fans, it’s a wonderful time of year. Baseball playoffs are being set. The NFL is in full swing, and college football is operating too. The NHL preseason has begun. The GM strike rolls into its second week. Here is what we are watching this morning:

BREAKING: U.K. SUPREME COURT WILL ISSUE RULING TOMORROW MORNING ON PROROGUING PARLIAMENT.

The U.N. General Assembly meetings begin: Although we doubt anything of substance will emerge from these meetings, Iranian leaders will be in town and discussions about climate change are on the agenda. Ukraine’s president will also attend. The U.S. is likely to try to move the U.N. to criticize Iran’s recent attack on Saudi Arabia, but we are not optimistic on this front. We are monitoring the recent whistleblower accusations, and the widespread youth protests for climate change legislation. However, we haven’t moved beyond monitoring because, so far, these issues have not affected financial markets. Nevertheless, impeachment proceedings could dampen investor confidence (or not…it might ease trade tensions). On climate change, we do expect that action will be taken at some point; our focus now is on how the costs of the legislation will be allocated.

Weak Eurozone economy: The Eurozone PMI data (see below) came in soft, at 50.4, just above the 50 expansion line. Financial markets moved from risk-on to risk-off on the news. There is great concern that the Eurozone will drag the global economy into further weakness.

Saudi Arabia and oil: Oil prices declined in the wake of the Eurozone PMI data despite news that repairs to the Saudi infrastructure will likely take much longer than expected, according to private contractors hired to assist in recovery efforts. Worries about demand, caused by slowing global growth, are keeping oil prices from rising on the bullish supply news.

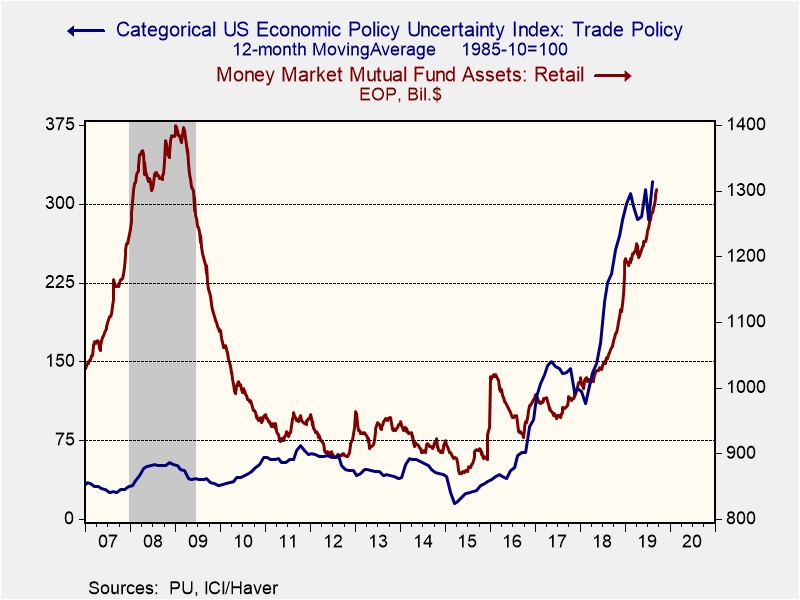

Trade: On Friday, President Trump’s comments that he didn’t want a partial deal with China, that he didn’t need a deal for re-election and reports that a Chinese trade delegation called off visits to farms led to a hard selloff in equities. It turns out that the U.S. asked the Chinese to cancel their visit, worried about the public framing of the tour. Trade uncertainty may be the most important issue that the financial markets are dealing with. Regular readers are familiar with our charts that show U.S. retail money market balances have been ballooning over the past 18 months. The last time we had such an increase in these balances, was into the teeth of the financial crisis. In general, money market funds are generally utilized by higher income households, so the increase in these balances is likely (a) reducing buying power for equities and (b) represents potential liquidity that could propel equities to significantly higher levels. We think the chart below may explain the money market accumulation.

The blue line (left scale) is the U.S. Economic Policy Uncertainty Index for trade policy. The index is created by noting the mentions of trade policy and trade issues in the media. When such words are mentioned with greater frequency, the index rises. We have smoothed the day with a 12-month moving average. Note that the increase in the uncertainty index closely matches the increase in money market balances. It appears that concerns about trade and deglobalization have raised investor fears and triggered a desire to build cash balances. We note that the WSJ is reporting on the rise in household saving, especially among wealthier households. Although tax cuts probably played a role in the saving accumulation, the above chart suggests that worries about trade are affecting saving behavior as well. What this data tells us is (a) the trade issue has likely been the major factor behind the current sideways equity market and (b) a resolution of the trade deal could bring these liquidity balances back to the equity market, triggering a very strong rally. At this juncture, we don’t see a reversal in the trade situation anytime soon; if anything, deglobalization is one of the few bipartisan positions in our fractured politics. However, if there is a cooling of tensions, it could be quite bullish for equities.

The repo issue: It does appear that the Fed has addressed the immediate problem of spiking repo rates with a series of monetary injections. However, the NY FRB is now working to figure out why this happened in the first place. Apparently, bank officials are looking at the problem of concentrated bank reserves but seem to believe that the concentration is occurring with the small banks, not the larger ones.

Japan: The Japanese military failed to track several of North Korea’s recent short-range missile launches, apparently because of their low and irregular trajectories. Separately, satellite imagery from two U.S. private-sector organizations show North Korea building a structure to launch its newly developed ballistic missile submarines. Along with last week’s successful missile and drone attacks on Saudi oil facilities, the reports suggest a greater risk that rogue states like North Korea and Iran can now overcome U.S. missile defense systems. This should keep geopolitical risks high, and help maintain a risk bid for crude oil.

Iran: The Iranian government said it will release the British-flagged oil tanker Stena Impero, which it seized in July after Gibraltar’s seizure of an Iranian tanker. Since the Iranian tanker had long since been released, the release of the British ship right after last week’s attack on Saudi oil facilities suggests the move is meant to confuse Iran’s adversaries and obfuscate its true intentions.

Egypt: Protestors rallied against President Al Sisi over the weekend. Although the number of protestors was only in the hundreds, it was Egypt’s first significant bout of demonstrations in years, and the first to openly call for Al Sisi’s ouster over corruption charges. Coupled with Iranian threats and inconclusive Israeli elections, unrest in Egypt would help bolster oil prices.

Interest rates have increased since early September.

(Source: Bloomberg)

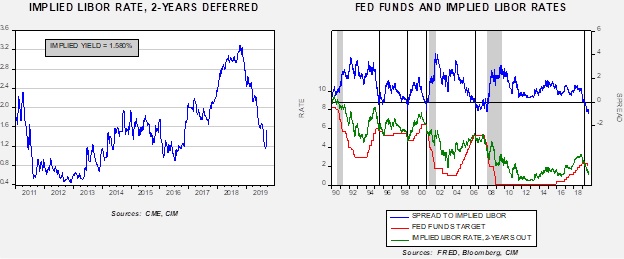

The 10-year T-note yield dipped to 1.45% in early September but has risen strongly since then. What has prompted this rise? Some of the rise appears to be caused by a revaluation of the path of monetary policy.

The chart on the left shows the implied three-month LIBOR rate, two-years deferred, from the Eurodollar futures market. After falling to a low near 1.15%, the yield has jumped to 1.58%. The chart on the right shows this implied rate compared to the fed funds target. Although the backup in the implied rate has reduced the expected decline in fed funds from nearly 100 bps to around 60 bps, the spread remains inverted, meaning the market still expects the Federal Reserve to cut rates somewhere between 50 bps and 75 bps over the next two years.

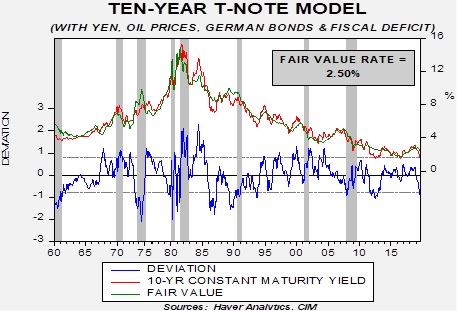

Our 10-year T-note model suggests that long-duration yields are too low, or prices on these instruments are too high.

This chart shows our 10-year T-note yield model. The deviation line is at the one-standard error level. Essentially, the bond market yield is consistent with recession. If the bond market is right and a recession is coming, the chart above suggests that if that recession is a “garden-variety” type, like those seen in the 1990-91 and 2001 downturns, then it would be unlikely that we will see further yield declines. On the other hand, when the model suggests long-dated Treasuries are overvalued and a recession doesn’t follow, the backup in yields is notable. It’s still too early to tell if a recession is coming, but the evidence that one could develop is increasing. Our analysis suggests, however, that the protection that long-duration Treasuries usually offer in a recession and bear market may not be all that significant at current yields. If the above LIBOR analysis is correct, the recent backup in those yields would suggest a fed funds rate of around 1.50% and a fair value 10-year Treasury yield of 2.27%. Thus, the recent backup in yields likely has further to run.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EDT]

Global equity markets are generally higher this morning. The EuroStoxx 50 is up 0.4% from the last close. In Asia, the MSCI Asia Apex 50 closed up 0.1%. Chinese markets were higher, with the Shanghai composite up 0.2% and the Shenzhen index also up 0.2% from the prior close. U.S. equity index futures are signaling a higher open.

Misjudging Trump: We have been getting questions from readers about U.S. Iran policy. So, here is our response. It is starting to look like Iran has concluded that President Trump is a bully who will back down when his bluff gets called. Yesterday, Iran’s foreign minister, Javad Zarif, suggested that a military attack on Iran would trigger “all-out war.” This is a clear and strong threat. Throughout its history since the Iranian Revolution, Iran has generally been cautious in foreign affairs. Although it underwrites audacious acts (e.g., bombing of U.S. troops in Beirut, Khobar Towers bombing in Saudi Arabia), these are usually carried out by proxies or in ways that provide plausible deniability. In the attack on the Saudi oil infrastructure, Iran tried to follow the same script, with the Houthis immediately taking responsibility. However, unless the Houthis are hanging out in southeastern Iran or southern Iraq, it probably wasn’t their doing and Iran had to know that it would be hard to maintain that ruse.

One of our “go-to” tools in analyzing foreign relations and the reactions of presidents is to use Mead’s Archetypes. Regular readers are familiar with the four major ones. We note that these are merely archetypes as no president is a pure reflection of any of the four but all lean toward one. So, here is how we think each archetype would react to last weekend’s events:

Jeffersonian: A Jeffersonian president would be angry that the U.S. was still even in this part of the world, but since we are there we should talk to allies and formulate a response. Military action would be a reluctant and last resort. This president would not have responded to the drone downing.

Wilsonian: The drone downing would have triggered a strong military response. This recent escalation would have led to an ordinance being already in the air. Although this type would try to avoid escalation, its actions usually end up leading to a broader conflict.

Hamiltonian: Always a realist, a Hamiltonian president would be trying to pull out of the Middle East, concluding that China was the real issue and shale oil has made the extensive U.S. commitment to the region unnecessary. However, this president, faced with the problem at hand, would likely attempt to escalate carefully, bombing highly visible but mostly symbolic areas in Iran, e.g. old oil fields that are in decline, secondary industrial sites, etc. In other words, it would send a signal that the U.S. isn’t happy, but also trying to avoid hitting anything that would lead to escalation. This archetype would have attacked after the drone downing.

Jacksonian: This response would have been identical to the Jeffersonian response. These two types are the most isolationist of the four. However, if honor is violated, the response is the most aggressive. So, what would this president react to? The spilling of American blood or the harming of innocents. The response to such events would likely be swift and disproportionate.

We characterize President Trump as Jacksonian. In WWII, Jacksonians were America First supporters…until Pearl Harbor. Then, they wanted to annihilate Japan and Germany. If Iran escalates further and an American is killed, or if Iran’s actions kill children, Trump will likely shift to aggression that is stronger than Tehran expects. However, as long as the escalation avoids these two outcomes, we expect Iran to increase its belligerence, and probably get away with it. As a result, oil markets are probably underestimating the level of risk.

Brexit: A thaw is developing. Although a deal is still a ways off, the two sides are clearly trying to come up with a way to reach an accommodation on the Irish border issue. We have seen the GBP rally on hopes of a deal. If an agreement is forged, we could see a much larger rally in the currency.

A deal of sorts with China: Our base position on China is that the U.S. has concluded Beijing is a strategic competitor that will not fold itself into the U.S.-led order. Because of this a slow decoupling and increased competition is in our future. However, that doesn’t mean an intermediate deal cannot be struck. We note the Trump administration has exempted a large number of Chinese goods from tariffs. U.S. agricultural interests are talking to China as well. These actions might lead to a limited deal that would improve market sentiment. At the same time, Michael Pillsbury, a Hudson Institute analyst and key informal advisor to President Trump, has warned the U.S. will dramatically ramp up pressure on China if a trade deal isn’t struck soon. Pillsbury characterized the current U.S. tariffs against China as “low” and warned they could go as high as 100%.

India: Prime Minister Modi announced a surprise tax cut that will slash the effective corporate rate to 25.17% from the current 34.94%, putting it on par with many other fast-growing Asian countries. New manufacturing firms will face an even lower rate. Indian stocks are surging on the news, but Indian bonds are down on concerns about the fiscal deficit.

Russia: President Putin has again been forced to back down a bit with his political repression, as he faces strong public outcry over the police beating and jailing of aspiring actor Pavel Ustinov during a protest last month. The actor was released on bail today. Putin still has a strong grip on power, but popular discontent is rising and has the potential to destabilize the country.

Saudi Arabia: There are reports that the crown prince is “bullying” wealthy Saudi families into large purchases of the Aramco IPO to bolster the price. Such action is further evidence that the Salman family effectively is “taxing the rich.”

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EDT]

The FOMC meeting turned out hawkish. Other central banks were active today. Trade negotiators from China begin talks in the U.S. today. Here is what we are watching this morning:

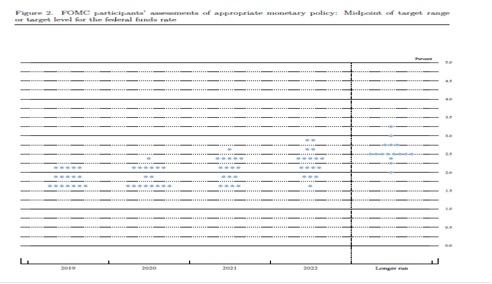

Hawkish Fed: The FOMC did cut rates by 25 bps but nearly everything else about the meeting was disappointing for the doves. The dots plot suggests this will be the last easing that is consistent with the recent easing being more of a mid-course correction instead of being the beginning of an easing cycle. The dots chart below suggests this will be the last rate cut, a position more in line with a correction than an easing cycle. In fact, based on the 2019 dots, 10 members would either hold rates at the current level or increase them by 25 bps. Additionally, next year, the board is nearly equally divided on one more cut or raising rates. The divergence between the FOMC and the markets are stark, not to mention the goals and aspirations for monetary policy from the White House.

Market reaction was swift; treasury yields, especially in the short end, jumped, flattening the yield curve. The dollar appreciated and gold prices fell. Equities did manage to rise, likely on a positive economic outlook from the FOMC. The bottom line: the FOMC isn’t poised to aggressively cut rates unless the situation changes. History tells us that by the time the evidence is clear that the situation has changed, it will be too late to avoid a recession.

Other central banks: The Bank of Japan kept its monetary policy unchanged, as expected, but Governor Kuroda promised to consider further loosening in October. With the Fed and other major central banks loosening policy, Kuroda’s statement amounts to an effort to talk the yen down, but it doesn’t seem to be working. So far today, the yen is up some 0.5% against the dollar. Also, The Bank of England kept its benchmark interest rate unchanged at 0.75%, as anticipated. It also warned rates could go either up or down in the event of a no-deal Brexit, but many policymakers say a cut to stimulate demand would be more likely than a hike to support the pound and reduce inflation pressure.

U.S.-Japan Trade: Economic Revitalization Minister Nishimura said the new U.S.-Japan trade deal will be ready to sign at month’s end. In a sign of what the UK may face in any post-Brexit deal with the U.S., Nishimura admitted that the government would have to provide additional support to farmers and small businesses that would be impacted by the deal.

Growth prospects downgraded: The OECD has reduced its forecast for global growth, calling for growth in 2019 at 2.9%, the lowest since 2009. The group warns that if trade tension remains high, sluggish growth will extend into 2020.

Brexit: There is some movement in addressing what may be the most contentious element of exiting the EU, the border with Northern Ireland. PM Johnson is floating the idea of creating a special economic zone for Northern Ireland, which looks a lot like an early EU plan that would put the trade border on the Irish Sea. More importantly, the Unionist parties appear to be softening their stance on this issue; previously, they had opposed such measures. Creating a trading zone probably can’t be accomplished before Halloween, but the Leavers would probably accept an extension if a way forward can be made on the Irish border issue.

Israel: The elections failed to yield a path to a coalition, as a result we will have one of two outcomes. Either we will see a “national unity government” where the two leading parties form a government, or new elections will be called. So far, the opposition Blue and White Party has rejected forming a national unity government, meaning elections may be coming next.

President Trump campaigned changing America’s hegemonic role, offering to step back from being the “global policeman.” The lack of a military response to this attack is clear evidence that he is doing what he said he would do. However, the U.S. isn’t fully in control of the situation. Iran can continue to escalate; if the only response is sanctions, the mullahs will likely conclude they can act with impunity and engage in additional actions.

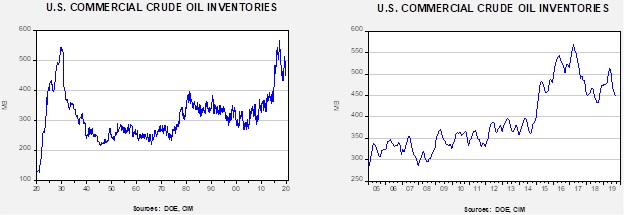

Energy update: Crude oil inventories rose 1.1 mb compared to an expected draw of 2.0 mb.

In the details, U.S. crude oil production was unchanged at 12.4 mbpd. Exports fell 0.1 mbpd while imports rose 0.3 mbpd. The rise in stockpiles was mostly due to falling refinery demand (see below).

(Sources: DOE, CIM)

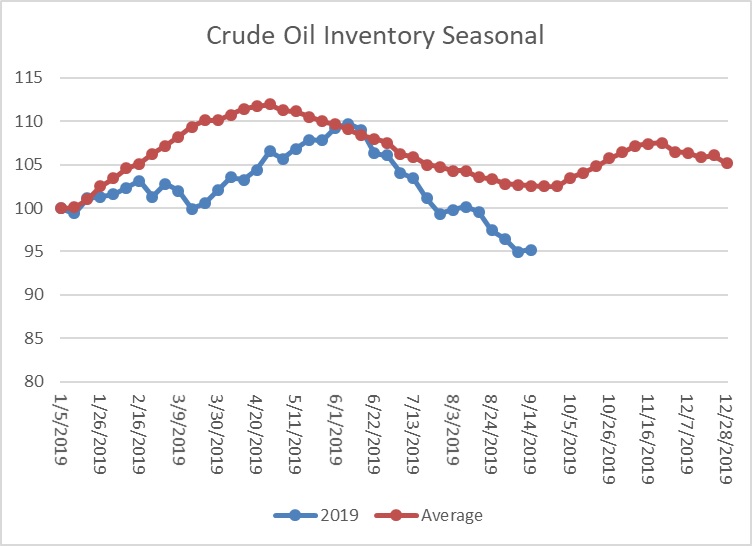

This chart shows the annual seasonal pattern for crude oil inventories. As we approach the end of the spring/summer inventory withdrawal, we are starting the autumn rebuild period at a sizeable deficit. Without aggressive increases in stockpiles, we will likely continue to lag seasonal patterns which, on its own, is bullish.

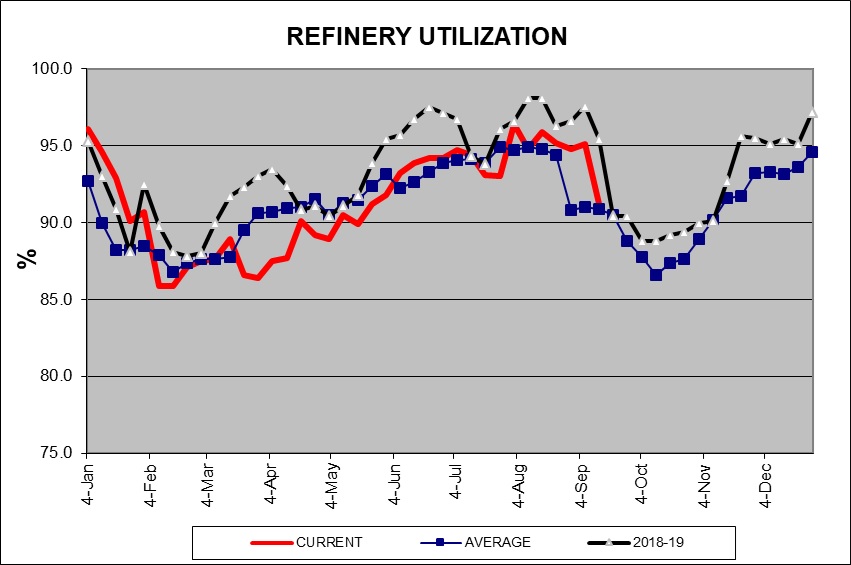

The most important information from this week’s data is that we appear to be starting the autumn refinery maintenance season.

(Sources: DOE, CIM)

The drop in refinery utilization will likely continue for the next four weeks; utilization should begin to rise by mid-October. During this period, inventories usually rise. However, the usual seasonal rise will depend on Saudi production.

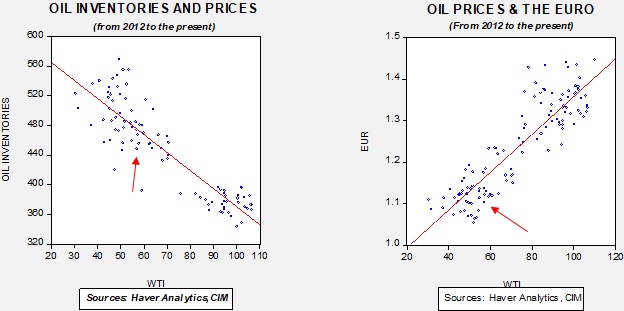

Based on our oil inventory/price model, fair value is $68.30; using the euro/price model, fair value is $48.23. The combined model, a broader analysis of the oil price, generates a fair value of $54.54. We are seeing a clear divergence between the impact of the dollar and oil inventories. Given that we are into the maintenance season, we would normally expect inventories to rise. However, with the Saudi outage, we may see inventories remain constrained, thus prices may find some support from constrained inventory growth. We note that after claiming oil supplies will be restored by the end of the month, the KSA is seeking to import petroleum products from other nations and for customers it has promised to supply with oil, it is offering less valuable grades. Oil prices rose on this report. We remain highly skeptical that Saudi Arabia will be back on line by month’s end.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EDT]

Markets are stable this morning after a wild day in the overnight lending market. The Israeli elections did not yield a clear result. The FOMC meeting concludes today. Here is what we are watching this morning:

The funding problem: We have received many inquiries on the state of the money markets. Yesterday, the money markets were roiled by an apparent funding shortage which sent repo rates soaring.

(Source: Bloomberg)

Bids for fed funds reached the 5% level, well in excess of the upper limit of the fed funds target, currently at 2.25%. For the first time since the onset of QE, the New York FRB conducted overnight repo operations; the NY FRB was authorized to purchase up to $75 bn of collateral to inject cash into the system with about $58 bn being drawn. In an unsettling development, the “plumbing” didn’t work initially, and the operation was delayed by about 25 minutes. The fact that this facility hasn’t been used in over a decade is probably the reason for the delay; it’s possible that a number of people on the NY FRB’s desk had never been involved in such an operation.

However, before we jump into all of that, a bit of history is in order. The Fed used to routinely intervene with repurchase operations before the financial crisis. When banks were in the settlement period at the end of the month, banks with excess reserves would lend them to other banks that were lacking. Occasionally, spikes in fed funds occurred; around holidays, a bank somewhere would find itself short of reserves and by the time they came to the Fedwire, most banks were closed and the ones that were not could lend at a penalty rate. Usually, the next day, the Fed would conduct repo operations to buy securities and put liquidity back into the system.

Then QE happened, and the traditional way that money markets operated was changed. The banks were flooded with reserves, so the Fed could no longer guide the policy rate by adjusting the level of bank reserves. Instead, it began paying interest on reserves and that Interest on Excess Reserves (IOER) rate became how the policy rate was set. There is no incentive for a bank to lend reserves below that rate, so the IOER has become the effective floor for interbank reserve lending.

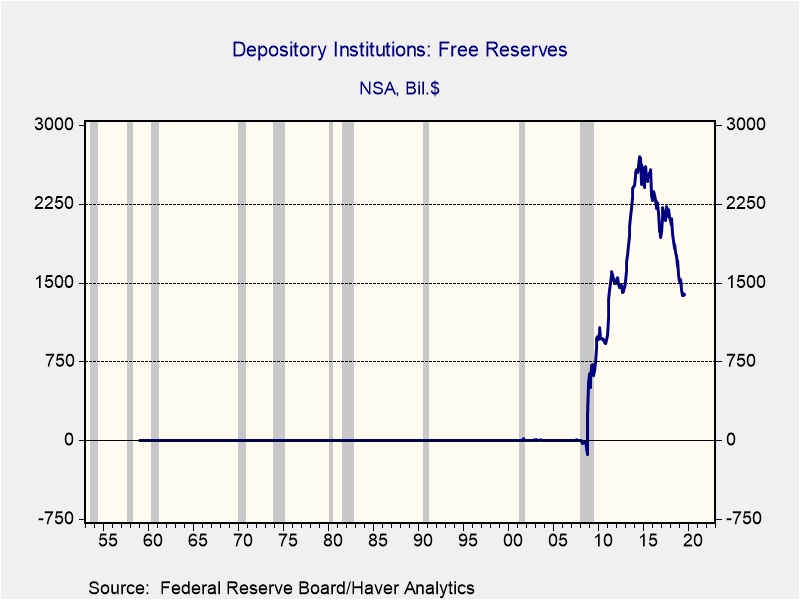

Free reserves are total reserves less required reserves and other borrowings from the Federal Reserve. Other borrowings are very small, so, for practical purposes, free reserves are excess reserves. As the chart shows, excess reserves in the banking system are $1.386 trillion. So, at first glance, it seems odd that a shortage would develop.

Here is what we think is happening:

Perhaps the most interesting part of this issue is the inability of entities to turn securities into cash. Essentially, that is what a repurchase agreement (repo) is. This sort of transaction is the lifeblood of finance. When entities would rather have cash than earn interest on that cash, that signals a problem.

As the charts above shows, there are ample reserves in the aggregate banking system, but there seems to be a problem of serious maldistribution. It appears the major banks are holding the bulk of the excess reserves and seem unwilling to lend them. The big banks complain that they are holding these large reserves due to regulation. Given that regulators have a goal of making the large banks safe, the banks seem content to hold high levels of cash and earn IOER, which is currently around 2.10%. Even with the possibility of risk-free profit at unusually high spreads, banks with reserves did not rush in to take advantage of the spreads. This means (a) they are inept, (b) they need the reserves more than the profits or (c) they don’t trust the counterparties. We lean toward “a, b” but if “c” is the issue, we have a bigger problem.

An overlooked factor in all of this is dollar strength. Even though the dollar is excessively valued relative to inflation, and in some cases, unit labor costs, the dollar continues to be buoyed. Although the spreads against other nations’ interest rates are usually trotted out as a factor supporting the dollar, the persistence of dollar strength appears to be more like a dollar shortage. In other words, foreign borrowers that have financed in dollars are struggling to acquire dollars to service debt. A side issue is that the attack on Saudi Arabia may have played a role as well. Usually, the KSA funnels around $400 mm per day into the U.S. money markets from oil sales, but with the sudden halt in oil production, it is highly possible that the kingdom is actually doing repos to generate cash to meet its dollar obligations.

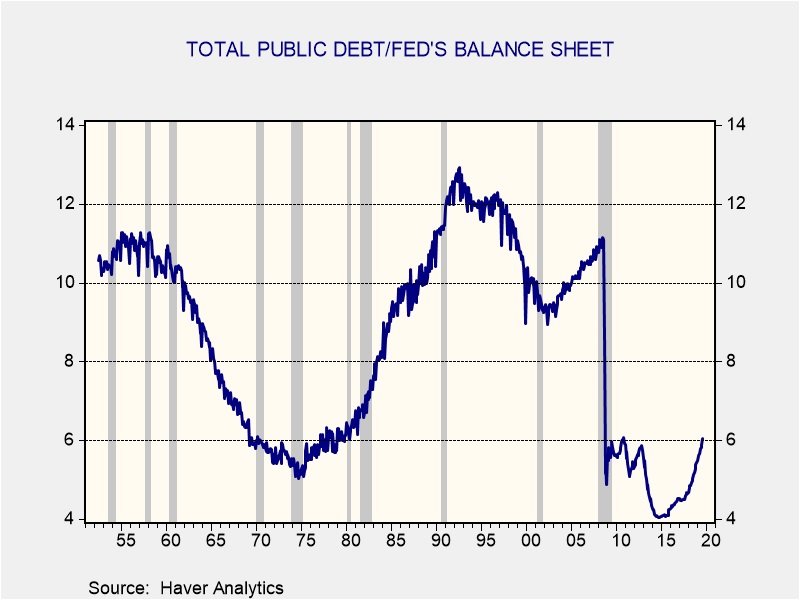

The level of Treasury debt/Fed’s balance sheet has fluctuated over the years but has ranged between 6x to 12x. After QE, the ratio plunged to about 5x, and has fallen as low as 4x. However, the combination of rising Treasury borrowing and a shrinking balance sheet have pushed the ratio to a bit more than 6x. The historical record would suggest this is not an alarming level, but it is possible that in our current environment, the ratio may need to be below 5x for the money markets to have enough liquidity. In other words, the world changed after 2008 and the Fed doesn’t know for sure what are the proper level of reserves. However, it is looking rather obvious that they are too low.

Another thought. Over the past four decades policymakers generally have relied heavily on monetary policy to guide the economy. Discretionary fiscal policy has been used occasionally, but only in emergencies when presidents can prod Congress to act. The problem with monetary policy is that it works through the financial system and its primary tool of stimulation is lending, with refinancing being secondary. However, if the real problem is excessive debt, monetary policy is simultaneously helping and exacerbating the problem. It’s a bit like a drunk trying to postpone the hangover by continuing to accept cocktails. At some point, the debt must be addressed; it’s the job of the political system to assign the cost of adjustment. What policymakers would likely prefer is to use inflation and financial repression to force the adjustment on creditors over a long glide path. Although, inflation can’t be triggered by monetary injection alone (yes, Milton Friedman was wrong); inflation needs reregulation and deglobalization to work, and financial repression needs reregulation of the financial system to force savers to accept negative real rates. We believe this process is underway, but progress is very slow (the last time we dealt with a debt overhang was the Great Depression and it wasn’t really resolved until we had the fiscal expansion with war spending). In the meantime, events may preclude addressing the debt overhang at a measured pace.

So, bottom line, should we be worried? Yes, but it is hard to figure out what exactly to be worried about. It is difficult to see how we are on the cusp of a domestic banking crisis. As noted above, banks seem to have plenty of reserves. Fear itself, along with zealous regulation, may be prompting reserve hoarding and that may be exacerbating the problem. But, for whatever reason, there appears to be a dollar shortage and the Fed can address that by reflating its balance sheet. It probably will also be more aggressive in repo operations, perhaps even establishing a standing facility. However, these events suggest that even though the overall economy may not necessarily need lower rates, the financial system is in desperate need of cash and the Fed, as the global lender of last resort, should probably be cutting rates more aggressively. Still, given the Fed’s history, they don’t tend to act on these “plumbing” issues until a crisis develops. We will continue to monitor this issue and will be the first to admit that it is devilishly complicated. Nevertheless, two things do stand out; first, caution is warranted and second, the Fed should get aggressive in easing. A historical analog might be the 1998 LTCM crisis; Greenspan made a sharp emergency fed funds cut to flood the money markets with dollars. It prevented a crisis but it probably led to the last upleg in the tech bubble in equities.

FOMC:There is no doubt the Fed will cut rates by 25 bps today. Everything else will probably disappoint. We doubt the dots will signal further easing this year and we expect at least one dissent from the KC FRB. Additionally, the press conference will likely be non-committal; do not expect any clarity on the aforementioned money market issues in the presser. If we are right, the yield curve should flatten, gold will ease, equities will likely ease.

Hong Kong: Protestors are increasingly pressing the U.S. to support its movement for democracy. The White House has mostly been non-committal; if the president intervened in the situation, it would likely end any chances of a trade deal. However, that isn’t stopping Congress from getting involved. House bill 3289 has been introduced, titled the Hong Kong Human Rights and Democracy Act of 2019, would force the executive branch to judge if the two systems program is being upheld, and direct the White House to take action if China is deemed to have undermined Hong Kong’s democracy. It is highly unlikely this will pass, but it does show that this issue could become a complication in trade negotiations.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.