Even though Japan has one of the world’s largest economies and accounts for a hefty share of global stock market capitalization, it isn’t getting nearly as much attention from investors as it did during its boom years in the 1970s and 1980s. In part, that’s because Japan’s economic growth has become slower and more erratic ever since its stock bubble imploded in 1989. Inflation has become worrisomely low, prompting a range of radical fiscal and monetary policies.

Some of Japan’s biggest slowdowns have started with tax hikes, so investors are now worried what will happen after a boost in the value-added tax (VAT) is implemented on October 1. Since it looks like Japan will weather the new tax hike well, it may be a good time to review the recent developments in the Japanese economy and explain why this tax hike doesn’t seem to be causing problems. Part I of this report will provide a primer on the current Japanese economy and financial markets. Next week, in Part II, we will focus on Japan’s geopolitical and domestic priorities, the reasons for the new VAT hike and ramifications for investors.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EDT]

Good morning and happy Monday! It was a busy weekend in front of a busy week. Here are the details:

Baghdadi dead: The leader of Islamic State (IS), Abu Bakr al-Baghdadi, died over the weekend, killing himself with a suicide vest while his compound was raided by U.S. Special Forces. Killing the leaders of such movements, such as the operation against Osama bin Laden, are important psychological events. In the case of al Qaeda, the group continues to operate but the profile of the new leadership is significantly lower, which probably makes sense because having a high profile makes one a high-value target. Although we expect IS to continue, its form will likely be far different than what we saw a few years ago. It more likely will look like al Qaeda; IS will be something akin to a franchise name for similar movements around the world. We strongly doubt it will, in the short run, control enough undisputed territory to be considered a caliphate. At the same time, as the U.S. withdraws from the Middle East and other parts of the world, the ability of IS and fellow travelers to operate will be fostered. So far, the market impact of this event was minimal; if anything, it might be modestly bearish for crude oil.

One of the fallouts of Brexit is the loss of Britain’s contribution to the EU budget. Germany is balking at a projected rise in its expected future contribution. The potential fallout (see below) could be renewed momentum to German populists and nationalists. In other words, even after Brexit is “put to bed,” the remnant EU is likely to struggle with the political fallout for years and will face internal tensions that are likely to be negative for the euro and European equities.

Peronists win: Although it was no surprise that Alberto Fernandez won yesterday’s election in Argentina, the final results were a bit tighter than expected. For investors, the key unknown is how much power his running mate, former president and first lady Cristina Fernandez de Kirchner, will have in the new administration. The more power she wields, the greater the likelihood of default and turmoil.

German regional elections: The state of Thuringia, which resides in the former East Germany, held elections over the weekend. The AfD made a strong showing, seeing its vote share rise to 23.5% from 10.6% in the last election in 2014. The hard-left Die Linke (the Left) party won the most votes, at 31%. The CDU took 21.6%, down 12 points from 2014. The key point of the results is that the center isn’t holding; the hard-left and hard-right now command a majority in this small state and it isn’t likely that any of the parties can form a government. These sorts of outcomes weaken the ability to govern.

CPC plenary session: The CPC will meet this week to hammer out policy for the upcoming year. Chairman Xi waited until the last possible moment to hold this session, which may reflect internal dissention. Xi has come under pressure for deteriorating relations with the U.S. and weakening economic growth. As a result, we will be watching for any signs that Xi may be forced to accommodate these pressures. Look for a rush to get a trade deal with the U.S. or fiscal stimulus. Meanwhile, China is trying to woo foreign firms on the back of new legislation that liberalizes foreign investment. Additionally, the trade talk reports remain favorable.

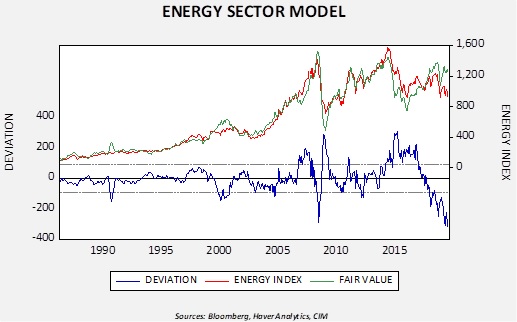

For nearly two years, the energy sector has dramatically underperformed the overall equity market and oil prices.

This chart shows our S&P energy sector model. We regress the overall S&P 500 and oil prices against the energy sector. For most of the index’s history, these two variables explained much of the behavior of the energy sector. The deviation line shows that this is the most significant underperformance of energy over the past thirty years. The current underperformance was preceded by strong outperformance in the two previous years.

So, why are we seeing this underperformance? It isn’t exactly clear. There are a number of candidates to explain the deviation. It may reflect a correction from the earlier outperformance that was likely based on euphoria surrounding fracking. There may be an element that, due to fears of climate change, hydrocarbons are falling into “pariah” status. If this is the case, there may be a long-term underweighting of energy stocks going forward. It may be that energy equity investors believe oil prices are too high and simply won’t “pay up” for equities to match current prices.

We are not sure which factor accounts for the underperformance but it does pose a problem for asset allocation. Energy is only 2.6% of the growth index for the S&P 500 but 6.4% of the value index. If an investor wanted to tilt his/her portfolio toward value due to concerns about a slowing economy but was worried that the underperformance of energy is a secular trend, the tilt to value might leave that investor with an excessive allocation to energy. Our Asset Allocation Committee recently faced this problem. To deal with this issue, we added a quality factor product to our Asset Allocation portfolios, which will still give us the defense posture without a large energy component. This is one way to address the higher proportion of energy in the value index and create a more defensive posture in asset allocation.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EDT] Happy Friday! Markets are trading quietly this morning. We are watching Johnson’s attempt to bring elections, China/U.S. trade talks, Syria reports and Argentine elections. And, the EU moves to standard time this weekend. Here are the details:

Brexit: PM Johnson has called for elections on December 12. Unfortunately for him, he doesn’t control the process. Under rules passed in 2011, he needs 434 votes in Parliament to bring new elections. There is no evidence to suggest he is even close to getting that number. Comments from opposition party leaders suggest they won’t back new elections without passing the Halloween exit date. They would like the EU to officially grant an extension; in a moment that would make Joseph Heller proud, the EU doesn’t want to establish the new extension date until the election issue is resolved. There are some other ways an election could be called. Johnson could, in a Kafka-like moment, bring a no-confidence motion against his own government. That resolution would only need a simple majority to pass and the SNP would likely join the Tories against the Johnson government. The risk from this outcome is that there would be a two-week period during which other parties could form a government, although the likelihood that Labour could cobble together a majority isn’t very high. However, this approach requires the two-week period plus the minimum time to put an election together, and this maneuver would need to be done before next Thursday. Finally, Johnson could bring a “one-line” bill to Parliament calling for an election; that would only need a simple majority but amendments (e.g., a referendum, lowering the voting age, etc.) could be added to it.

Simply put, the mess continues. The odds of a hard Brexit have been diminished, but that’s about all the progress we have made.

China trade: U.S. and Chinese trade officials will talk today on the latter’s purchase of farm products. Reports indicate that China will agree to buy these products only if the U.S. cancels at least some of the planned and existing tariffs. The U.S. has already agreed to drop $250 bn of tariffs that were scheduled for October 15. China reportedly wants the removal of a 15% tariff on $125 bn of goods that was implemented on September 1. If accepted, that would reduce the tariffs to $250 bn of Chinese imports. From our standpoint, this looks like a big “ask” from the Chinese side. We suspect they will be willing to accept the current state of tariffs but will reduce planned purchases.

Meanwhile, VP Pence, playing the traditional role of an attacking VP, gave a highly critical speech of China as well as U.S. companies that accommodate China’s demands. China strongly rebuffed the speech. To some extent, Pence’s speech and the rebuttal may be simple politicking, rather obvious attempts to improve the negotiating positions. However, it may also be a true reflection of the state of the relationship that may never return to status quo ante.

Argentina’s elections:Argentines go to the polls on Sunday; it appears likely that the Peronists will return to power. What is unknown is how the new government will actually govern. There are two (unrelated) Fernandezes running; Alberto is running for president, while his running mate is the former president, Cristina. Alberto is more center-left, whereas Cristina, both when she was president herself and when aligned with her late husband, is a populist. We suspect Cristina will be the power behind the throne. Financial markets have been betting on the latter for months, expecting another round of default and depreciation.

Things that gives us pause: With the backdrop of the World Series, Rob Drake, a MLB umpire (who, BTW, isn’t working the series), released a tweet suggesting he was armed for a “cival (sic) war” if impeachment takes place. In the U.K., a survey showed that a majority of Leave voters believe that “violence toward MPs is a price worth paying for Brexit.” A majority of Remain voters think that “protests in which members of the public are badly injured is a price worth paying to stop Brexit and remain in the EU.” Even in Canada, divisions are becoming stark. Within hours of the Canadian election on Monday, in which Prime Minister Trudeau retained power with strong support in the country’s east but very little in the west, activists in the western province of Alberta started calling for it to withdraw from Canada, in what they’re calling “Wexit.” For now, Wexit still seems to be a fringe movement, but if it grows it would be a headwind for Canadian assets. Political divisions are transforming into tribal ones, where compromise is becoming impossible and civil unrest is more likely.

United States-South Korea: Finance Minister Hong said South Korea will give up its WTO designation as a “developing country,” following up on U.S. complaints that countries like South Korea and Hong Kong don’t deserve the designation and the preferential treatment it provides in international trade. The main negative impact is expected to be on South Korea’s farmers.

Greece: Parliament has approved a package of economic reforms aimed at boosting investment and accelerating economic growth. The reforms include allowing firms to opt out of some collective bargaining deals and letting local governments outsource some services to private operators. The new rules should add new impetus to Greece’s improving investment climate.

Saudi Arabia-Yemen: The Yemeni government signed a power-sharing deal with separatists in the country’s south, which should help limit the country’s civil war to the separatist Houthis in the north. The deal strengthens the government’s position, but it doesn’t remove the Houthi and Iranian threats to oil facilities in allied Saudi Arabia. The risk bid for oil is likely to remain.

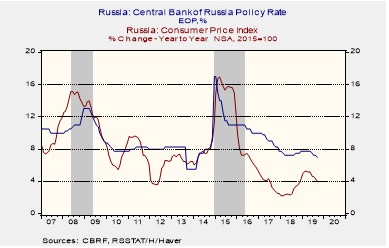

Russia: The central bank today aggressively cut its benchmark interest rate to 6.5% from 7.0% previously, citing a sharp drop in inflation and weak economic growth. The cut was Russia’s fourth this year, and it was twice as big as each of the previous three cuts. The central bank also cut its 2019 inflation forecast to a range of 3.2% to 3.7%.

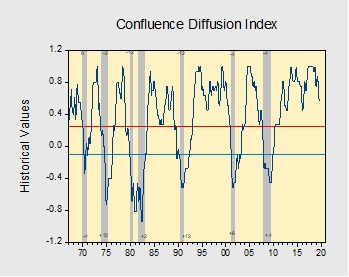

The business cycle has a major impact on financial markets; recessions usually accompany bear markets in equities. We have created this report to keep our readers apprised of the potential for recession, which we plan to update on a monthly basis. Although it isn’t the final word on our views about recession, it is part of our process in signaling the potential for a downturn.

Data released for September suggests the economy is still firmly in expansion, but a slowdown in manufacturing and signals of financial weakness continue to be a drag on the index. Currently, our diffusion index shows that nine out of 11 indicators are in expansion territory, with several indicators approaching warning territory. The index remains unchanged from the prior month at +0.575.[1]

The chart above shows the Confluence Diffusion Index. It uses a three-month moving average of 11 leading indicators to track the state of the business cycle. The red line signals when the business cycle is headed toward a contraction, while the blue line signals when the business cycle is headed toward a recovery. On average, the diffusion index is currently providing about six months of lead time for a contraction and five months of lead time for a recovery. Continue reading for a more in-depth understanding of how the indicators are performing and refer to our Glossary of Charts at the back of this report for a description of each chart and what it measures.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EDT] Good morning! It’s a rather quiet day in earnings season. Mario Draghi holds his last meeting as president of the ECB, Boris Johnson waits for the EU and we have an update on Syria. Here are the details:

ECB: The statement held no surprises. The ECB left rates unchanged and QE of €20 bn per month will begin on November 1. In the press conference, the tone was defiantly dovish. However, market reaction has been very modest, probably because Draghi will be out in just over a week.

Germany: Christian Kastrop, a former finance ministry official who helped author Germany’s constitutional “debt brake,” said in a Financial Times interview that it’s now time to change the law to allow increased borrowing and greater investment in infrastructure, digital technology and climate mitigation. It’s one more sign that global sentiment is shifting, slowly but surely, toward looser fiscal policy as the impact of loose monetary policy peters out.

Syria: President Trump, satisfied with the ceasefire and the new buffer zone, has removed sanctions on Turkey. Kurds are evacuating the buffer zone. The president couched the quick revocation as a reward for Turkey’s adherence to the five-day ceasefire brokered by the United States, but his statements suggest it was actually a doubling down against the bipartisan criticism he has taken for abandoning the long-time U.S. ally.

China in its place: In a recent speech, SoS Pompeo made the following comment:

We’ve reconvened “the Quad” – the security talks between Japan, Australia, India and the Untied (sic) States that had been dormant for nine years. This will prove very important in the efforts ahead, ensuring that China retains only its proper place in the world.

He did not elaborate on what he means by China’s “proper place.” It’s hard to see how that could be anything other than containment. Needless to say, we are sure that Beijing has read this statement and have no doubts it was not welcomed. Although some sort of trade deal next month is likely, the fundamental relationship between China and the U.S. has changed and won’t return to the status quo ante.

In another interesting comment, an unnamed U.S. military officer told reporters that the Japanese government should do more to explain to its citizens the threat China means for the region, suggesting Japan should consider an offensive-defensive stance. This report is additional evidence that the U.S. is steadily removing itself from the stabilization role that it has performed since the end of WWII.

Global unrest: Although it hasn’t had much of an impact on markets, we are paying attention to widespread unrest and protests. One common theme we are noticing is that seemingly modest changes in charges for public services are not being accepted; in fact, the reaction seems far out of proportion. In general, our observation is that disproportional reactions are usually not due to only the apparent catalyst but have longer roots in the past. Mass dissatisfaction has lots of factors behind it but underlying them all is a belief that societal elites are not looking out for the interest of the general public.[1]

Japan-South Korea: Japanese Prime Minister Abe held a short meeting with South Korean Prime Minister Lee, who was in Tokyo this week for the enthronement of Japan’s new emperor. Unfortunately, however, the talks yielded no progress on the dispute over Japan’s behavior in Korea before and during World War II, which we wrote about in a two-part WGR series on Sept. 30 and Oct. 7.

Canada: Even though his Liberal Party lost its parliamentary majority in Monday’s elections, Prime Minister Trudeau said he will not enter into either a formal or informal coalition with rival parties. That suggests Trudeau will have more freedom to form the government he wants, but it also points to potential stalemates or instability as Trudeau will have to pass legislation – and survive any no-confidence motions – by forming ad hoc coalitions. On balance, Trudeau’s approach is probably negative for Canadian risk assets going forward.

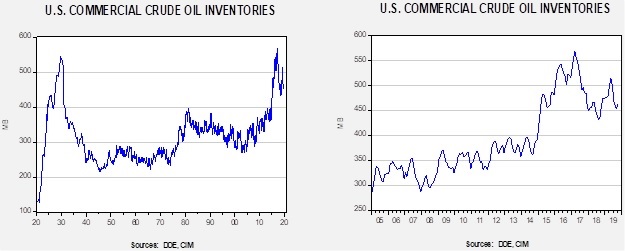

Energy update: Crude oil inventories fell 1.7 mb compared to an expected build of 3.0 mb.

In the details, U.S. crude oil production was unchanged at 12.6 mbpd. Exports rose 0.4 mbpd, while imports fell 0.5 mbpd. The decline in stockpiles was mostly due to rising exports but a rise in refinery demand contributed to the draw.

(Sources: DOE, CIM)

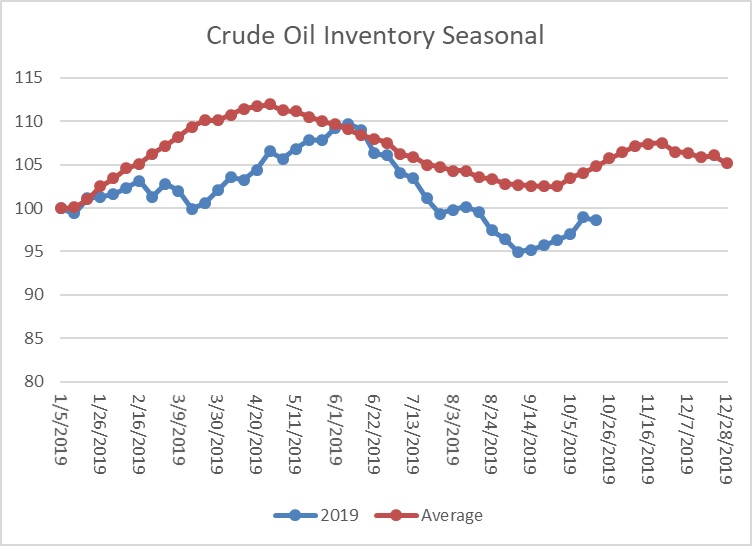

This chart shows the annual seasonal pattern for crude oil inventories. We are now in the autumn build season, which usually lasts into early December. This week’s drop, though modest, is contraseasonal and bullish for crude oil.

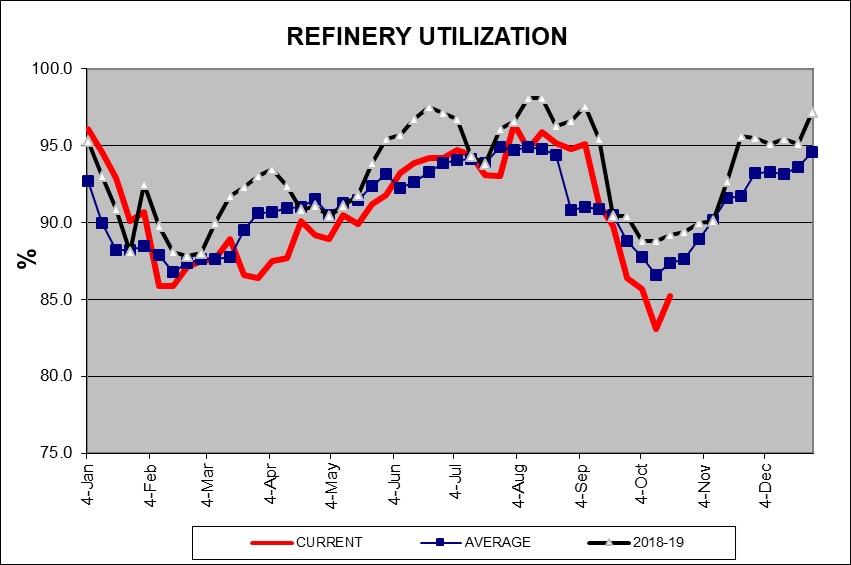

We continue to monitor the autumn refinery maintenance season.

(Sources: DOE, CIM)

This week’s recovery in utilization turned “on schedule.” We would expect refinery operations to rise steadily into year’s end.

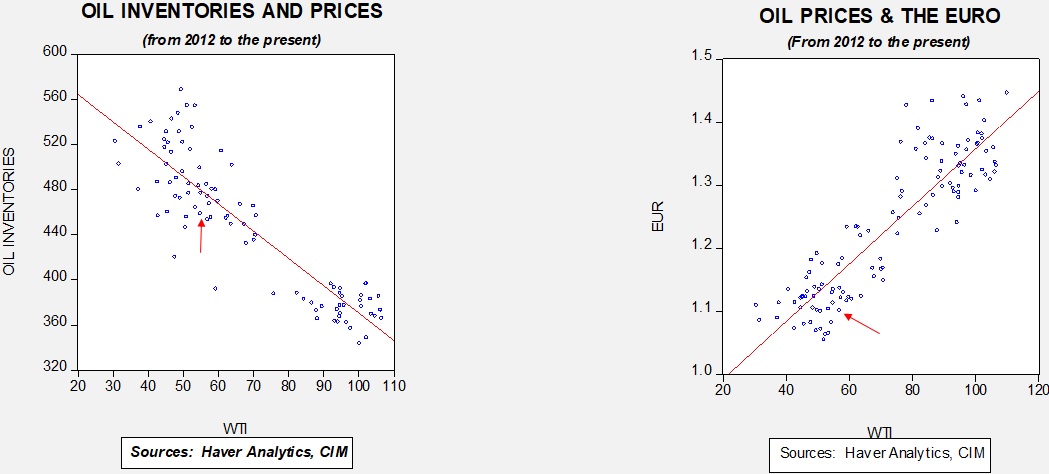

Based our oil inventory/price model, fair value is $62.96; using the euro/price model, fair value is $48.47. The combined model, a broader analysis of oil prices, generates a fair value of $52.73. We are seeing a clear divergence between the impact of the dollar and oil inventories. Given that we are in the maintenance season, we would normally expect inventories to continue to rise. We have been seeing stabilization of oil prices and would expect that to continue for the next few weeks.

The likelihood of a Halloween exit is not zero, but it is highly unlikely. The EU is already signaling it will offer an extension until at least the end of January.

Johnson will press for an election, but that path has two problems:

Labour might not support that outcome; polls suggest Corbyn will lose in an election and he may not want to risk that outcome.

Johnson needs to convince voters in the Brexit Party that he has delivered their outcome by passing the bill. If he can’t, those voters could prevent him from gaining a majority in Parliament. If Brexit had occurred, the reason for the Brexit Party’s existence would no longer be operative and these voters would likely shift to the Tories.

It is possible that, after further review, MPs could decide to implement the passed bill in the 90 days between Halloween and January 31, 2020. In that case, an election would likely follow.

There will be attempts at adding amendments. One such addition might be to signal that the U.K. should consider negotiating on a U.K.-wide customs union. However, that won’t be part of the bill that passed. Another would be a referendum, but it doesn’t appear that has the votes either.

Time is not on Johnson’s side. As MPs have more time to read the complicated document, it is a real risk that the details could cost him some support.

Thus, the status quo will be in place for now. The next big decision, or lack thereof, is probably on the election.

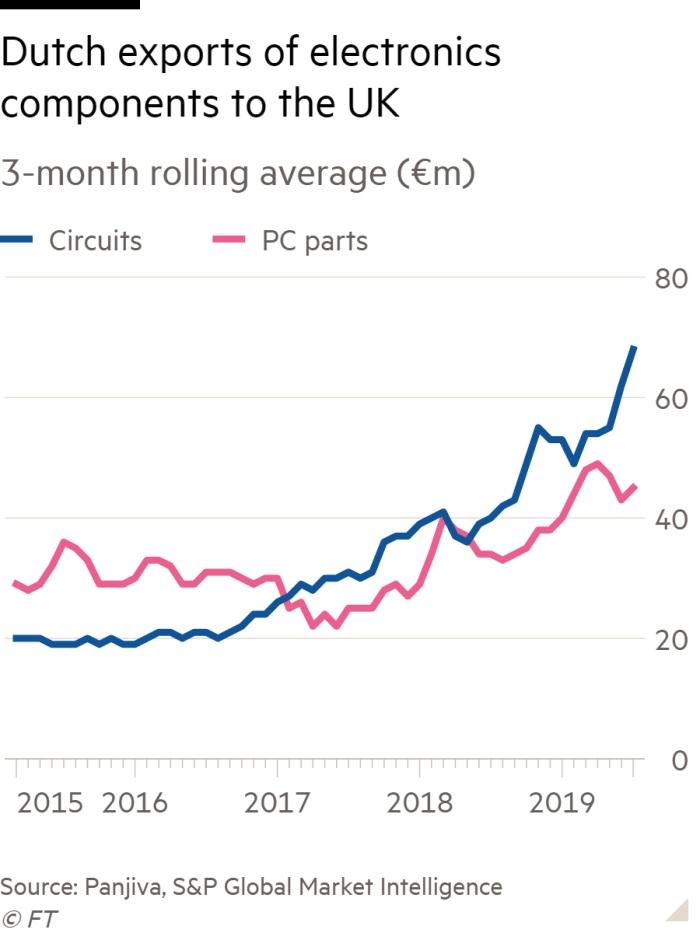

Finally, here is an interesting chart on the Brexit issue. It shows U.K. imports of technology components from the Netherlands. There is a clear increase in imports from mid-2018, when the Brexit vote occurred. One issue that develops under conditions of trade uncertainty is that companies and consumers begin to stockpile critical goods on fears of potential supply disruption. This inventory accumulation, if large enough, can distort economic data, leading to stronger data before the trade disruption occurs and weaker data afterward as the inventoried goods are used up after the trade action is implemented. What could be happening in the U.K. now is that companies and consumers are building inventories, causing the economy to look stronger than it really is; after Brexit, we could see an inventory “hangover.”

Carrie Lam out? The FT is reporting that Beijing is planning to force out the current Hong Kong leader, Carrie Lam, with new leadership. According to reports, Lam will resign at the end of Q1 and an “interim” leader will be appointed by Chairman Xi. Reports suggest the head of the Hong Kong Monetary Authority, Norman Chan, is the frontrunner to replace Lam. It is likely that Beijing hopes removing Lam will ease tensions with protestors. We have our doubts but, clearly, Lam has become unpopular.

Syria:Russia and Turkey have reached an agreement to jointly operate a buffer zone in Syria. The winners? Turkey, which now gets what it wanted—a Kurdish-free zone on its southern border. Other winners are Assad, who ostensibly gets more of his territory back, and Russia, which is rapidly becoming the power broker in the Middle East. Under the deal, the Kurds have six days to retreat more than 20 miles from the Syrian/Turkey frontier. We will now be watching to see if Kurdish forces actually retreat or fight against Turkey (and perhaps some Russian forces) to oppose the new zone. We suspect there will be some fighting but, in the end, without air cover, the Kurds are doomed if they resist. However, over time, we would expect the time-honored tactic of guerrilla warfare to develop, with Kurdish irregulars harassing Turkish troops guarding the new zone.

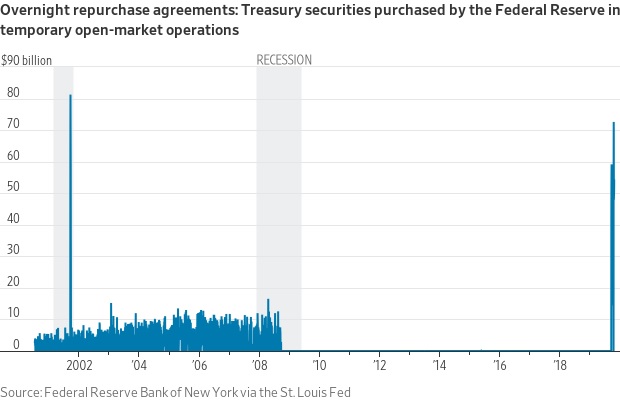

Although officials are continuing to argue that all is well, the size and continuous injection of liquidity is concerning. What we find interesting is that there is a growing dispute over this issue. The banks are arguing that the liquidity problem is due to excessive regulation, while Sen. Warren and others are countering that this may be a manufactured crisis to force a rollback in regulation. Here is the problem—if the banks are right and Warren and others prevent changes in regulation, we could end up with a liquidity crisis. If Warren et al. is right and regulations are rolled back, this could encourage risky behavior and create a financial crisis. It is critical that regulators figure out who is “on the side of the angels” on this one because getting it wrong could have serious consequences.

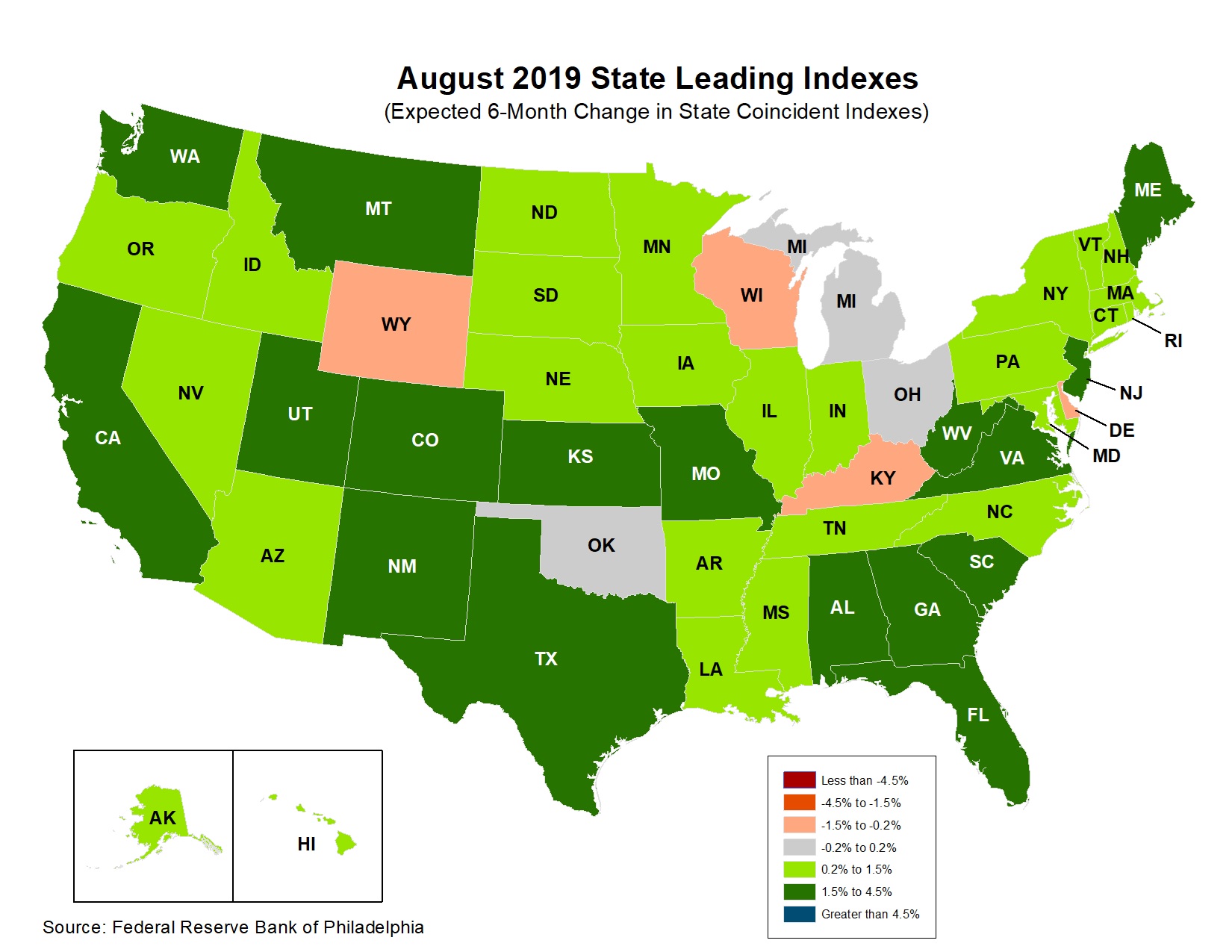

Recessions fears rise: According to a report from the National League of Cities, expected to be released on Monday, two-thirds of finance officers in large cities are predicting a recession within the next two years. As finance managers head into the next fiscal year, many suspect that their government expenditure could outpace revenue. This is worrisome as a reduction in government expenditure can lead to a slowdown in economic activity in these cities. In addition, it is widely believed that a slowdown in cities generally foreshadows a broader slowdown on the national level. Furthermore, fears of localized contractions have been noted on the state level as well. According the Philadelphia Fed’s state leading indicators, five states are expected to contract over the next six months.

European complications: One of our themes has been that the U.S. is withdrawing from three conflict zones in the Far East, the Middle East and Europe. Our most recent podcast touches on that theme. Here are a couple of interesting complications that highlight this issue in Europe. First, France has been reluctant to expand the EU to include Albania and North Macedonia. In response, these nations are considering reaching out to China and Russia for support. Second, in the turmoil surrounding impeachment and Ukraine, Hungary has been a background influence. After WWI, when the Austro-Hungarian Empire was broken up, thousands of ethnic Hungarians were scattered across Eastern Europe. Hungary has generally considered this diaspora as part of its citizenry. The nations in which these Hungarians live disagree. In 2010, PM Orban issued Hungarian passports to Hungarians living outside of Hungary. This allowed these Hungarians to vote in Hungary’s elections and they tended to vote for Orban’s party. However, Ukraine doesn’t allow its citizens to hold dual passports; thus, Orban had a problem with Ukraine, which was expressed by raising corruption issues with the U.S. against Ukraine. While this is all now part of the impeachment discussion, the bigger issue is that Europe is riven with similar ethnic dispersions. U.S. power has prevented these issues from dividing Europe, allowing the EU to flourish. However, as the U.S. withdraws, expect more of these sorts of historic claims to become a destabilizing problem for Europe.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EDT] Good morning! It’s rather quiet in the markets this morning. Trudeau wins another term, but not a majority. The Brexit saga continues. No government in Israel. Some background on Chile. Here are the details:

Trudeau wins: PM Trudeau won another term but his party didn’t get a majority, falling 13 seats short. To govern, he will need the support of either the New Democrats, or the Bloc Quebecois. The former won 24 seats, the latter won 32 seats. So far, financial market reaction has been modest as, at least initially, little will change. However, the parties that he will need to partner with in order to gain a majority are much more left wing, and pushing for strong climate change legislation. Both parties are not strongly in favor of USMCA. Thus, we could see a leftward drift in Canadian policy, which would not be favorable for Canadian assets longer term.

Today in Brexit: Today, at 2:00 EDT, the House of Commons will vote on the Withdrawal Agreement Bill. This vote is known as the “second reading.” This is a straight up or down vote on proceeding to further debate. If it fails, the clock essentially stops; the bill will likely be pulled, and there is a possibility of a hard Brexit. If it passes, and it appears it will, then Parliament will decide if the bill will be subject to amendments. That vote will likely happen tomorrow. Labour wants to attach a second referendum for approval; that amendment doesn’t appear to have the votes. There is also a separate amendment that would mean all of the U.K. will remain in the EU customs union instead of just Northern Ireland. That amendment might pass. Johnson, at that point, can either pull the legislation and go to an election, or accept the arrangement, get Brexit done and go to election. If he wins a strong enough majority, he can then move to remove the amendment. We expect him to take the second option; he likely feels that if he can deliver Brexit, his chances of winning an election are very strong (and we would agree with this position), and thus he can use that majority to shape Brexit going forward. It’s important to remember that Brexit is more like the end of the beginning, than the beginning of the end. Once the exit agreement has been struck, the U.K. and the EU will then decide on what sort of trading arrangement will be put in place going forward.

One side note; there is growing speculation that if Northern Ireland remains in the EU customs union but legally in the U.K., the region will have interesting trade characteristics. Suppose the Trump administration applies tariffs to the EU post-Brexit. Those tariffs would apply to the EU but not the U.K. Northern Ireland would then be in the EU customs union, but not subject to the U.S. tariffs. This unique condition could make Northern Ireland a haven for EU companies seeking to avoid U.S. tariffs.

Chinese trade: Chinese officials reported that “substantial progress” had been made during recent talks. Although there is little evidence that the difficult measures are being discussed, a small deal that can be signed next month looks increasingly likely. Yesterday’s equity market rally was due, in part, to trade optimism. However, to push markets to new highs, we will likely need to see the U.S. postpone tariffs due for December. This is possible; however, the administration will likely only agree to a postponement, not a removal. If so, the positive impact will be lessened.

A couple of other notes on China; as China negotiates on trade, it is petitioning the WTO for $2.4 bn in retaliatory tariffs. We also note that, in reaction to slowing economic growth, Chinese officials are returning to a familiar pattern, boosting public works investment to lift growth.

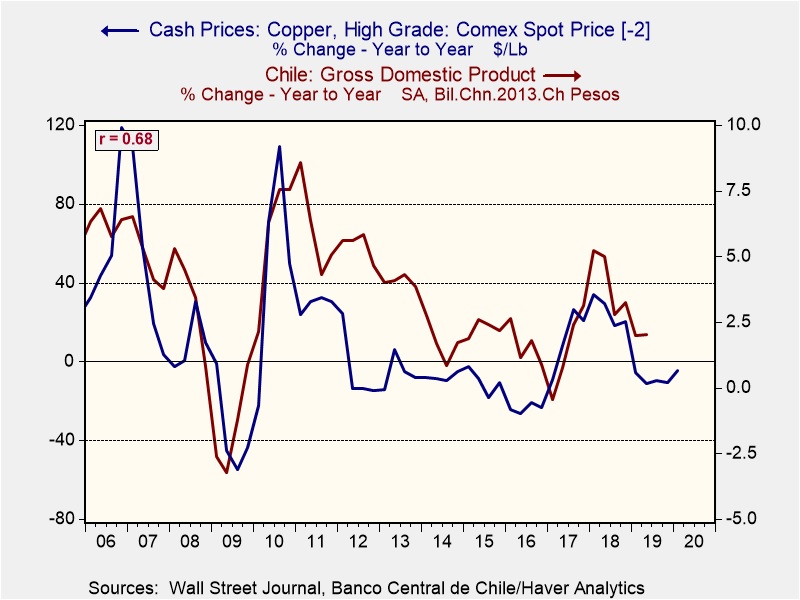

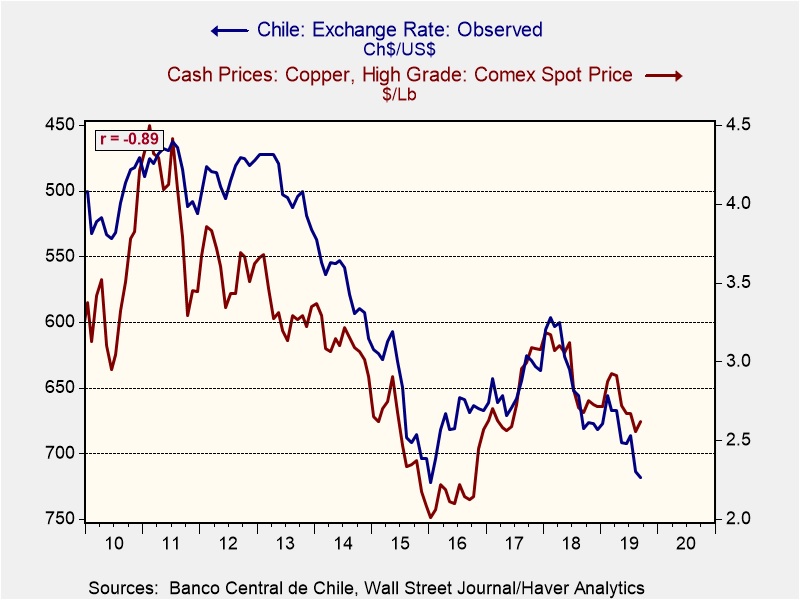

Chile: Unrest continues to spread in Chile, with 12 reported deaths. The key problem is inequality. Chile has leaned towards free markets since Pinochet built the economy on advice from University of Chicago economists. One of the ways the political class tries to deal with the “pie sharing” problem is to expand the pie; that way, those who currently “have” can receive the same, while those who “have not” can get more. Chile’s economic problem is its heavy dependence on copper. GDP tends to lag copper prices by about three quarters.

The exchange rate also closely tracks prices of the red metal. The chart below shows the exchange rate (inverted) relative to the price of copper.

The inequality problem in Chile needs stronger Chinese growth to fix; slowing world growth, but especially in the commodity consuming China, is a problem for commodity suppliers.

Israel: Yesterday, right-wing Prime Minister Netanyahu gave up trying to form a government, so President Rivlin is now widely expected to give a shot to Benny Gantz, the former army chief heading up the center-right Blue and White Alliance. It appears Gantz could form a minority government if he can strike a deal with leftist and Israeli Arab parties.

Bolivia: Authorities this morning resumed issuing vote-count updates from Sunday’s elections, with the numbers now showing leftist President Morales likely to win by enough to avoid a runoff. Initial counts Sunday suggested a runoff would be needed. After an inexplicable lull in count updates, the huge swing is raising concerns of electoral fraud, and protests have erupted.

Japan: Emperor Naruhito completed his accession to the Chrysanthemum Throne today, with Prime Minister Abe shouting “banzai” (meaning “10,000 years”), and spectators ranging from Britain’s Prince Charles to South Korean Prime Minister Lee Nak-yon (though, notably, not South Korean President Moon).

Japan-China: The Japanese and Chinese navies have held their first joint drills since 2011, including the first Chinese naval visit to Japan since 2009. Despite tensions over China’s claims to the South China Sea, the countries’ leaders reportedly want to improve trade and defense ties as the United States takes a more confrontational, protectionist stance against them.

In Part I of this report, we identified the need to stabilize three areas of the world prone to war in order to maintain global peace. We focused on the Middle East and discussed the development of the Carter Doctrine, examining how the doctrine has been enforced since its inception. In this week’s report, we will discuss the reasons for the breakdown of the order prior to President Trump and follow this discussion with the impact of the current president. We will project the likely actions of the nations in the region and, as always, conclude with market ramifications.

The Breakdown of the Order

The key element of the Carter Doctrine was the explicit threat to use military force to prevent outside powers from gaining influence in the Middle East. The tacit element of it was that the U.S. would enforce stability in the region which included honoring existing borders regardless of the internal social problems that the colonial frontiers created. Since the turn of the century, U.S. actions have tended to undermine regional stability. It began as overreach, but it has evolved into neglect.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.