by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EST] The second episode of the Confluence of Ideas podcast is available!

A German breakthrough? Since unification, Germany has supported the EU with certain qualifications. The primary goal, at least from the German point of view, is to prevent giving the rest of the profligate Europeans free access to German saving. As part of that fear, Germany has resisted the creation of a Eurozone bond, a bond that would have the full faith and credit of all the nations of the Eurozone. Although such a bond would be a significant competitor to the U.S. Treasury and raise the likelihood that the EUR would become a viable reserve currency, Germany has feared that its free-spending neighbors would borrow using this bond and force Germany to make good on the paper. So far, a single bond hasn’t developed and that means a foreign nation holding EUR as reserves must choose a national bond to hold. Given the divergence in yield and credit quality, this can be a difficult choice. Another area of disagreement has been over deposit insurance. It would be better for the Eurozone, since everyone has the same central bank, to have a unified regulatory structure. This would include unified deposit insurance. However, for reasons similar to its opposition to a Eurobond, Germany fears that a bad failure in another Eurozone nation could force German savers to spend money to bail out foreign depositors. That opposition may be cracking. Germany’s finance minister, Olaf Scholz, indicated he might support a unified deposit insurance program. If such a program does develop, it would reduce the risk for Eurozone banks and likely give their equities a lift.

China’s Eurobond: Although the Eurozone doesn’t issue a Eurobond, apparently China does. China has just issued a Euro-denominated bond, the first in 15 years. The Chinese financial authorities sold €4 bn of bonds with seven-, 12- and 20-year maturities. Half of the proceeds were issued in the seven-year at a 0.197% yield, with the remainder split equally between the other two maturities. The 12-year carried a yield of 0.618% and the 20-year has a yield of 1.078%. Demand was quite strong, with a bid/cover of 4.87x. Part of the reason demand was strong is that China is considered a safe credit (even though it can’t print euros) and the seven-year yield compares favorably to a -0.5% German yield. We suspect China has issued this paper to diversify its funding base; foreign-issued EUR paper is only about 5% of the world’s foreign denominated bonds, with USD dominating nearly all the rest.

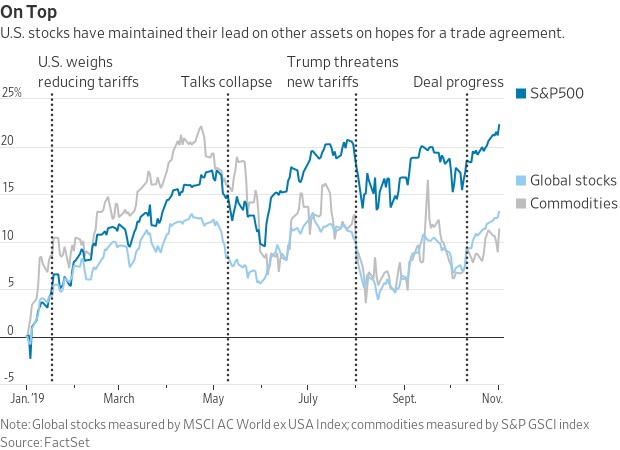

China trade: Optimism on a trade deal is high. Both sides seem to want a deal, and there is evidence that the Chinese leadership is preparing its citizens for a partial, not complete, removal of tariffs. The Chinese position seems to be a measured and proportional removal of tariffs on both sides. There is a problem with this plan, unfortunately, which is that the U.S. has a much larger target of Chinese imports to apply tariffs. A pure one-for-one removal will leave China at a disadvantage. This issue may be leading Chinese negotiators to overplay its hand. In effect, China seems to want a near full removal of tariffs for opening up agricultural trade and promising to guard intellectual property. This would seem to take away President Trump’s favorite trade tool—the tariff. If China is really insisting that the U.S. forgo future tariffs for what it has offered, this will look like a cave by the U.S., something the White House probably won’t accept. This all means that risk markets have been rising on expectations of a trade agreement; if that deal fails, as small as it will likely be, the reaction will be negative for equities.

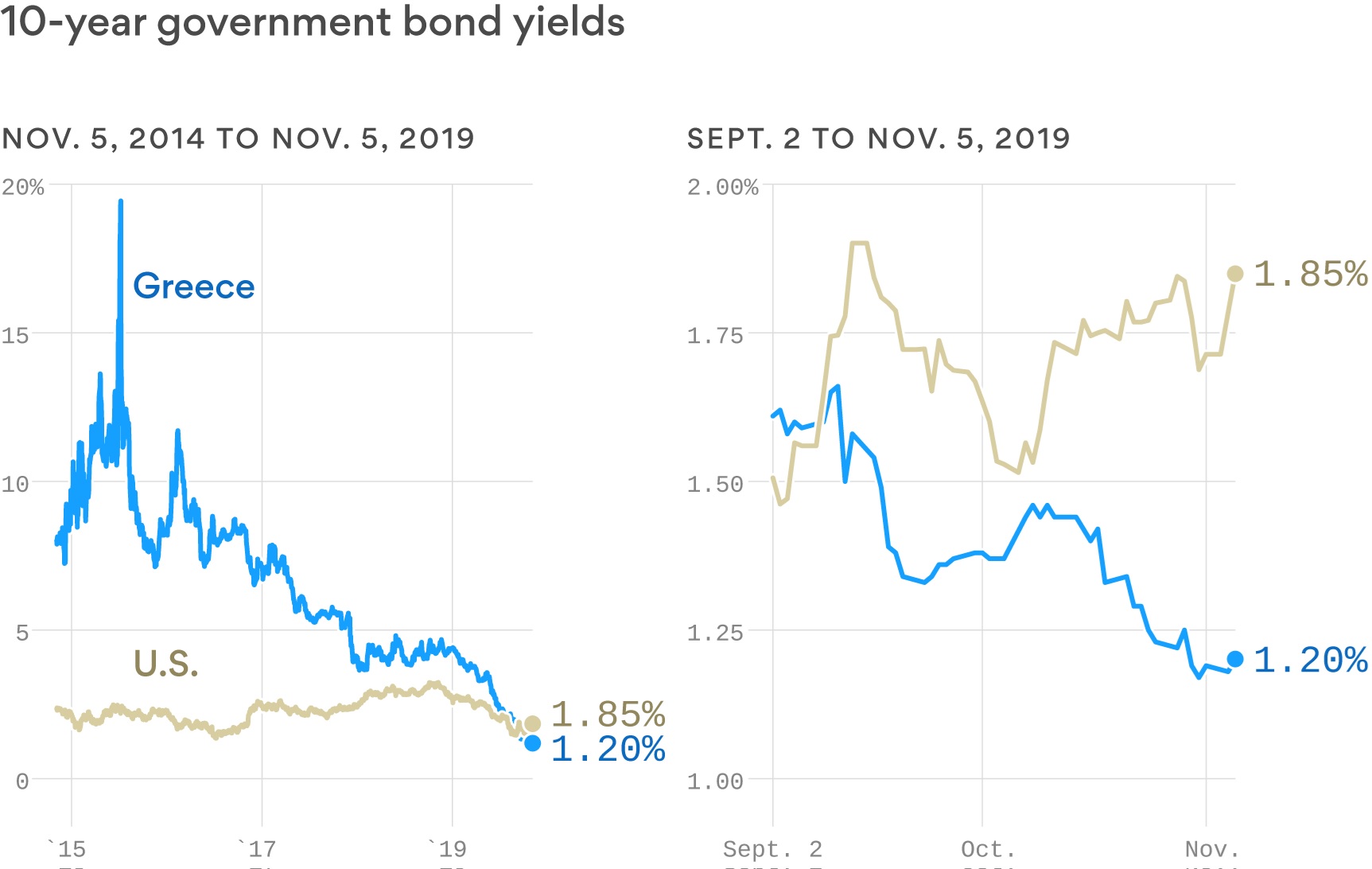

The reason? European inflation remains low and Greece has cleaned up its act after the near debacle earlier this decade. However, we agree it makes little sense to believe that the risk of Greece is less than the U.S. After all, Greece still is issuing bonds in a currency it can’t print. Perhaps this is the clearest evidence yet of the distortions caused by low and negative policy rates.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EST] The second episode of the Confluence of Ideas podcast is available!

Optimism over trade remains elevated; equities are moving higher and safety assets, Treasuries and gold, are suffering. Here are the details:

China trade: There is a lot of news on trade. First, there has been active consideration on both sides to roll back tariffs to secure a deal. Reports indicate that the U.S. might remove the 15% tariff on $112 bn of Chinese goods. Any agreement likely will also remove the $156 bn of tariffs scheduled for mid-December. What is China offering? The key “give” is to buy more agricultural goods, but the promise to buy $50 bn over two years is really more about returning to status quo ante. In 2016 and 2017, China purchased around $20 bn each year. Lifting to $25 bn per year is an improvement, but not a blockbuster. For farmers, this deal would be welcome, but they probably would have preferred to have avoided the issue altogether. The second part of China’s offer is to stabilize the CNY/USD. We are seeing signs of that already. However, this also isn’t a big ask; China has been worried that an overly weak currency could trigger capital flight and there is also concern about China’s growing corporate dollar-denominated debt. Thus, the weaker CNY threat was probably more symbolic than real. Third, China has offered rather vague promises to open up certain markets and respect intellectual property. We harbor serious doubts that China will follow through on these promises in any significant manner.

So, we will likely get a deal. In the end, it’s hard to see how much progress was made. The ultimate goal of the trade conflict was to force China to change its economic model. Using the savings identity, 0 = (I-S) + (G-Tx) + (X-M), China’s private sector oversaves, leaving a negative balance in the first term of the equation. To balance, either the government needs to run larger deficits or the nation needs to run a trade surplus. The U.S. wants an end to the private sector oversaving. We would argue that tariffs are probably not the best way to force this change; the bill proposed by Senators Hawley and Ballwin would likely be more effective.[1] In the end, there was much turmoil but not much evidence of progress.

Still, this outcome is supportive for equities.

When tariff reductions are being considered, equities tend to rise, as do commodities. When new tariff threats emerge, the opposite occurs. Given the cautious positioning seen in the financial markets, a significant lift in equities would not be a huge surprise. At the same time, the president has proven he can turn quickly to put tariffs back into the conversation. Increasingly, though, this looks like it might be a second-term issue.

China easing? The PBOC made a modest cut to its new policy rate, the Medium-Term Lending Facility, to 3.25% from 3.30%. The five-basis point move won’t trigger a huge economic response, but it is likely that this action will be the first of a few to ease monetary conditions in China. If China were to move more aggressively to boost its economy, along with trade peace, we could see a further lift to risk assets.

Iran: In a bid to say it won’t be ignored, Iran announced it will increase its uranium enrichment activity. This move further erodes the Iranian nuclear deal and will make it more difficult to European nations to support Iran against U.S. sanctions. Although this move might increase tensions in the region, we doubt the U.S. will respond to this action; Iran is already heavily sanctioned, and the U.S. has no inclination to engage in military action against Iran.

Other China news: There was little official news from the Fourth Plenum meetings. However, as the meetings ended, some items have filtered out. First, Ren Xuefeng, the CPC secretary for Chongqing, committed suicide at the meetings by leaping off the roof of the hotel where the gathering was being held. There are rumors swirling that he may have been part of a purge by Chairman Xi, or was caught up in a local scandal. Second, the general consensus from the meetings’ end is that Xi is firmly in control. Third, the meetings did discuss Hong Kong. We note that Hong Kong’s leader, Carrie Lam, has been called to Beijing for an unscheduled meeting with Vice Premier Han Zheng. The latter is the state leader in charge of Hong Kong.

In other China news, officials of TikTok, the Chinese subsidiary of the privately held ByteDance, have refused to testify at congressional hearings that were scheduled for today. The company, popular with Americans, is under scrutiny for its privacy controls. The U.S. has launched a national security review of the company.

China-Taiwan: Two months before Taiwan’s presidential election, the Chinese government is offering sweeteners to Taiwanese companies and individuals to ensure a pro-Beijing outcome. For Taiwanese businesses operating on the mainland, the measures would provide preferential land-use rules, the right to invest in passenger and air cargo services, and the ability to apply for financial guarantees from local government funds. For Taiwanese individuals studying or living on the mainland, the measures would ease property purchases and provide Chinese consular protections when traveling abroad. As we reported yesterday, China’s wooing comes as the Trump administration pressures Taiwan to restrict its technology sales to Chinese telecom giant Huawei (002502.SZ, 2.57).

United States: A Financial Times report shows the Trump administration launched just 25 new cases alleging criminal antitrust violations in 2019, marking the biggest drop-off in enforcement since the 1970s. The figures highlight the administration’s focus on company-friendly deregulation, even as its trade and immigration policies get more attention from the press.

A return of the swing producer?OPEC has acknowledged that its production will likely decline over the next five years due to the encroachment of shale production and rising climate activism dampening overall demand. The report by the cartel seems to suggest that it will not fight to boost market share, and instead will reduce its own output to maintain prices. This is the traditional role of the swing producer in the oil markets.

Some of Japan’s biggest economic hiccups have started with a major tax hike, so investors are wondering what will happen following a boost in the country’s value-added tax (a type of sales tax) that went into effect early last month. To lay the groundwork for understanding the VAT hike and its implications, Part I of this report last week provided an overview of the Japanese economy and financial markets, including a discussion of how they’ve performed over the past several decades. The analysis showed just how sharply Japan’s economic growth has slowed since the boom years of the 1970s and 1980s and the implosion of its asset bubble in 1989. Part of the long slowdown simply reflects Japan’s decision to gradually eliminate its post-bubble excess capacity and bad debts. However, we also examined how Japan’s extended revaluation process has been exacerbated by a unique set of headwinds: an aging population, high debt levels and disinflation.

This week, in Part II, we’ll home in on the Japanese government’s geopolitical and domestic priorities and the reasons for its new VAT hike. We’ll also examine why the tax hike doesn’t seem to be hurting the economy as much as past hikes have. As always, we’ll conclude with ramifications for investors as they face Japan’s current economic and financial trends.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EST] The second episode of the Confluence of Ideas podcast is available!

Happy Monday! Optimism reigns—everything is awesome! Trade optimism, helpful monetary policy, decent earnings and modest economic growth are propelling U.S. equities to new highs. The Saudi Aramco IPO is on. Here are the details:

Trade optimism: Commerce Secretary Ross had a number of positive comments on trade over the weekend. First, the secretary is “optimistic” on the first phase of the U.S./China trade deal. On November 13, the U.S. is scheduled to decide if it will apply tariffs on European cars; according to Ross, those tariffs may not be necessary. In addition, Japan reports that the U.S. may be lifting tariffs on its auto exports to the U.S. Although all this news is positive, there are a couple of issues to note. First, China is reiterating that its “core concern” is the lifting of all punitive tariffs, which seems highly unlikely. Second, the American Chamber of Commerce warns that the successful “phase one” of the trade deal is mostly about supporting the farm belt and does little or nothing to bring structural change to China’s economy. Overall, the trade news appears to be causing a clear relief that conditions aren’t going to get worse in the near term. However, the longer-term issues are nowhere close to a resolution.

Saudi Aramco: At long last, the Kingdom of Saudi Arabia announced it will begin the process of taking its state oil company, Saudi Aramco, public. It appears the company will have a valuation of $1.5 trillion, which is less than the royal family had initially hoped. The IPO prospectus will be issued on November 9, with share trading likely in December. There are two macro issues worth noting from this IPO. First, although there is likely a myriad of reasons for the IPO, the fact that the Saudi royal family is selling part of the “family jewel” suggests concern about the long-term viability of oil. Second, once the sale is made, we could see Saudi oil policy shift to retake market share. It is possible the Saudis have been trying to prop up the price of oil in order to boost the valuation of the IPO. Once the sale is made, the kingdom can more easily allow the price to fall to capture market share. Given the obvious financial vulnerabilities in the shale patch, this might be a good time to boost output and depress prices.

Brexit update: One question that was hanging over the upcoming election was the path the Brexit Party would take. If Nigel Farage, the party leader, was comfortable with the plan that PM Johnson had negotiated, he could simply stand down and one could reasonably expect Brexit Party voters would drift to the Tories. If Johnson had managed to get his deal passed, the Brexit Party would have lost its reason for existence. Over the weekend, Farage made his position clear—he has been pressing Johnson to scuttle his deal to get support of the Brexit Party. Johnson refused and now Farage has indicated he will contest the election by putting up candidates from his party across the country. Recent polling shows both Labour and the Conservatives are seeing improvement, while the Liberal-Democrats, the Brexit Party and the Greens are all falling.

United States-China-Taiwan: Over the last year, the Trump administration has repeatedly asked Taiwanese President Tsai Ing-wen to help cut the flow of technology to Chinese telecom giant Huawei Technologies (002502.SZ, 2.57). Specifically, the administration has been pressing Tsai to restrict the amount of semiconductors that Taiwan Semiconductor Manufacturing (TSM, 52.10) can sell to Huawei. TSM accounts for almost 25% of Taiwan’s stock market, and sales to Huawei account for some 10% of its total sales. If Tsai succumbs to the pressure, it would likely be negative for TSM and Taiwanese stocks, in general.

China-East Asia:Negotiations have been completed to establish a new free trade deal between China and the 10 members of the Association of Southeast Asian Nations (ASEAN). The “Regional Comprehensive Economic Partnership” focuses on trade in services, investment, dispute resolution and intellectual property. Signatories reportedly see it as a way to maintain free trade as the U.S. becomes more protectionist. Tellingly, the Trump administration only sent lower level officials to the associated U.S.-ASEAN summit being held in Bangkok today. In response, ASEAN leaders only sent three heads of state to the meeting.

Japan-South Korea: On the sidelines of the big ASEAN meeting today, Japanese Prime Minister Abe and South Korean President Moon held their first meeting since last September, before the countries’ dispute flared up over Japan’s behavior in Korea during World War II. Reports say the meeting was friendly, and more substantial talks on the dispute could still be scheduled. Separately, the speaker of South Korea’s legislature said a bill has been drafted to facilitate “voluntary” donations from Japanese companies to South Koreans who had served as slave laborers before and during the war. It is looking increasingly likely that some such deal could be the way this dispute is resolved. A resolution of the dispute would likely be positive for both Japanese and South Korean equities.

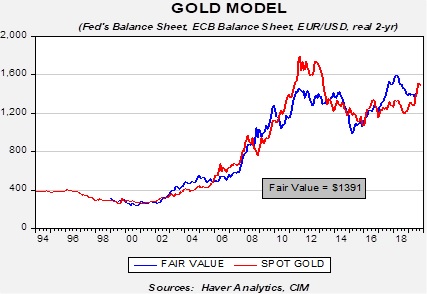

We continue to hold a favorable outlook toward gold despite evidence that current prices may be getting a bit ahead of themselves. Our gold model puts fair value at 1391.

In the coming months, we expect the fair value to rise; both the ECB and the Federal Reserve have resumed expanding their balance sheets. And, the Fed will likely continue to cut rates, which would be expected to reduce the real interest rate on two-year T-notes. The dollar remains overvalued but will likely need a catalyst to trigger depreciation. Still, over time, we do expect gold prices to find support from improving fundamentals.

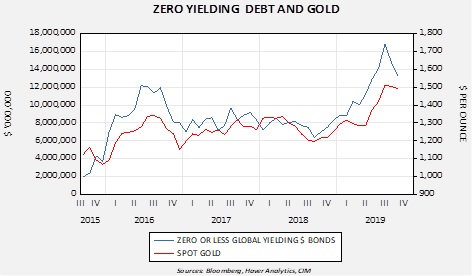

In addition, the high level of zero-yielding debt should be supportive.

We have seen a drop in zero-yielding debt recently, but with slowing global economic growth, a renewed expansion is likely.

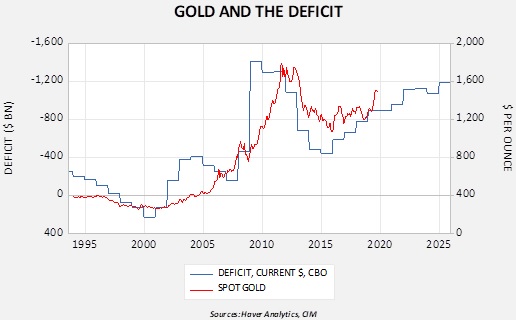

Finally, there is a long-term relationship between gold prices and the level of the fiscal deficit. Although the level of the current deficit does suggest, again, that gold prices might be a bit overvalued currently, the likelihood of expanding deficits should offer underlying support for gold prices.

In the immediate term, we may see steady to lower gold prices but there are ample fundamental factors that should support future prices.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EDT] The second episode of the Confluence of Ideas podcast is available!

Happy employment Friday and All-Saints Day! We cover the data in detail below, but the quick take is that we have a strong report. Payrolls rose 128k compared to a forecast of 85k. The unemployment rate ticks higher to 3.6%. In other news, China’s data surprises to the upside. The Fourth Plenum ends. The problems of hegemony. Christine Lagarde’s tenure at the ECB begins today. Here are the details:

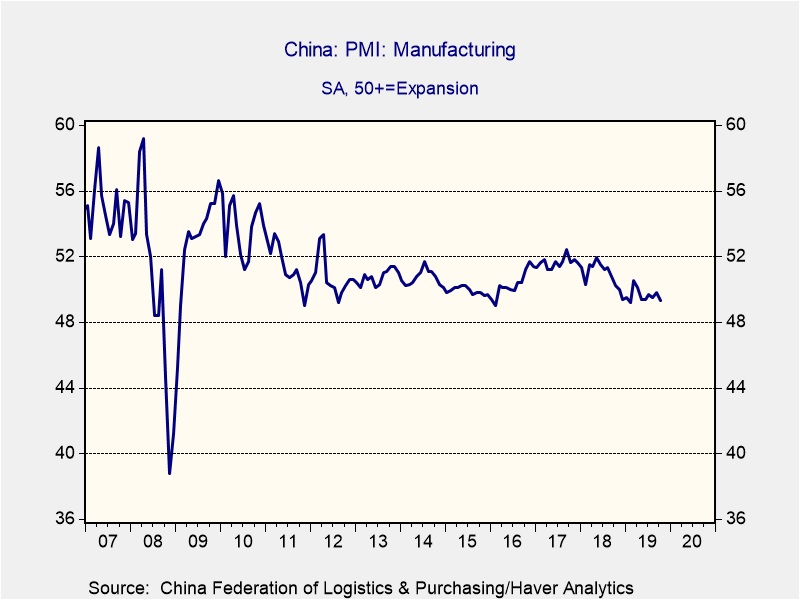

China data: Earlier this week, the government’s PMI series were weak, with manufacturing remaining under the 50-expansion line. In addition to the government data, Caixin, a media company in China, also provides a survey of manufacturing which tends to include more small companies. In a marked divergence from the government’s report, , the highest level in two years. It is not unusual for the two series to disagree but, in the past, the government data tended to be higher than the Caixin report. Thus, the Caixin report was generally held to be more reliable. It isn’t clear what this report is signaling; the strength does diverge from the broader array of data coming out of China. It may be that large firms have been more adversely affected by the trade war compared to smaller firms, which may be more sensitive to the domestic economy. Regardless of the reason, we did see a lift in global equities off this report which offers some hope for global growth.

The Fourth Plenum: The CPC meeting ended yesterday with little news. The lack of information isn’t a surprise; usually, whatever was decided is revealed in the weeks after the meeting. It does appear Hong Kong was on the list of items for discussion. The leadership has indicated it intends to “perfect” the selection of leaders for the former colony. That likely means less democracy.

United Kingdom-Brexit: In a radio interview with Brexit Party leader Farage, President Trump claimed “certain aspects” of Prime Minister Johnson’s new Brexit agreement with the EU would prevent a future U.K.-U.S. trade deal. It’s widely understood that the U.K. would suffer from limited leverage in any trade negotiations with the United States, but Trump’s statement seemed to go beyond that. Farage is reportedly a friend of President Trump, so it could be that Trump is trying to tip the scale in favor of Farage in Britain’s December election. Or, Trump could be calculating that Farage could draw pro-Brexit voters mostly from the Labour Party, clearing the way for a decisive win by Johnson and his Conservative Party.

Meanwhile, bringing his campaign for the December election to full gear, Labour Party leader Corbyn finally started to lay out details on how he would handle Brexit if elected. First, he vowed he would “get Brexit sorted out within six months.” More to the point, he also laid out three key actions he would take to do that: 1) Request another withdrawal deal extension, 2) renegotiate the latest withdrawal deal, and 3) hold a second Brexit referendum.

United States-Mexico-Canada: House Speaker Pelosi yesterday said congressional Democrats and Trump administration officials are close to an agreement in which she would allow a vote on the updated NAFTA treaty in return for adjusting the treaty to toughen its labor and environmental standards. That should provide modest support for U.S., Mexican and Canadian stocks.

United States-India: The WTO said India broke global trade rules by providing some $7 billion in export subsidies to its pharmaceutical, textile, steel and information technology companies. If India fails to end the subsidies within six months, the ruling would allow the United States to impose punitive tariffs. The ruling should be negative for Indian stocks in at least the short term.

A new leader for Islamic State:IS has a new leader. The group acknowledged the death of al-Baghdadi and the “nation’s” spokesman, Abu Hassan al-Mahajir, and announced a new leader, Abu Ibrahim al-Hashemi al-Qurayshi. At this point, no one seems to have any idea who this person is, or even if he really exists. It is likely that this name is a nom de guerre, so analysis will need to go behind the new name to find out who has adopted it.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EDT]

The second episode of the Confluence of Ideas podcast is available!

Happy Halloween! Not to scare, but today’s report is a long one as there is a lot of news to cover. We have a deep dive on the Fed meeting. China trade is good for the short term, not so good long term; the news is pressuring equities this morning. We also have an update on Chinese economic data and our weekly energy update. The Nationals win the World Series. Here are the details:

Fed recap: As expected, the Fed did deliver a 25-bps rate cut. The Fed’s statement and the press conference signaled that the U.S. central bank is likely to pause its recent rate reductions. They did leave room to ease further if conditions warrant but, in the absence of weakness, cuts are complete for now. The bank acknowledged weak investment but also noted that consumption remains robust. In fact, yesterday’s GDP data showed that consumption pretty much dictated growth; the other three components of GDP, investment, net exports and government, broadly offset each other. Thus, as long as consumption holds up, the economy will too.

There were two hawkish dissents, KC FRB’s Esther George and Boston FRB’s Eric Rosengren. In our assessment, these two members are opposing cuts for different reasons. George is a hawkish Phillips Curve adherent and likely opposes cuts on fears that they will be inflationary. Rosengren is a “finance-sensitive” voter, and probably opposes the cut on fears that they will lead to overvalued equity markets. Unlike the last two cuts, St. Louis FRB’s James Bullard did not want a more aggressive cut. The lack of a dovish dissent suggests the voters believe they are not reacting to prevent a recession but are adjusting the policy rate to more closely match economic conditions. In a recession, we would expect a return to ZIRP, so Bullard accepting this statement tends to support the notion of a “mid-course correction.”

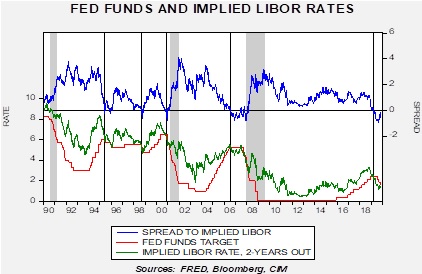

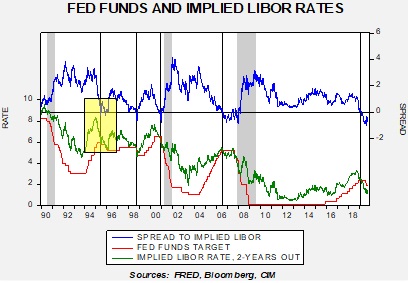

This chart shows the implied three-month LIBOR rate from the Eurodollar futures market along with the fed funds target. The spread between the two rates is the upper line. Inversions are shown by vertical lines. In 1995, the Greenspan Fed abruptly ended a tightening cycle as the spread inverted and generally guided rates based on the behavior of the implied LIBOR rate. The current spread, post the rate cut, is -10 bps. Pausing at this level is defensible in the absence of recession.

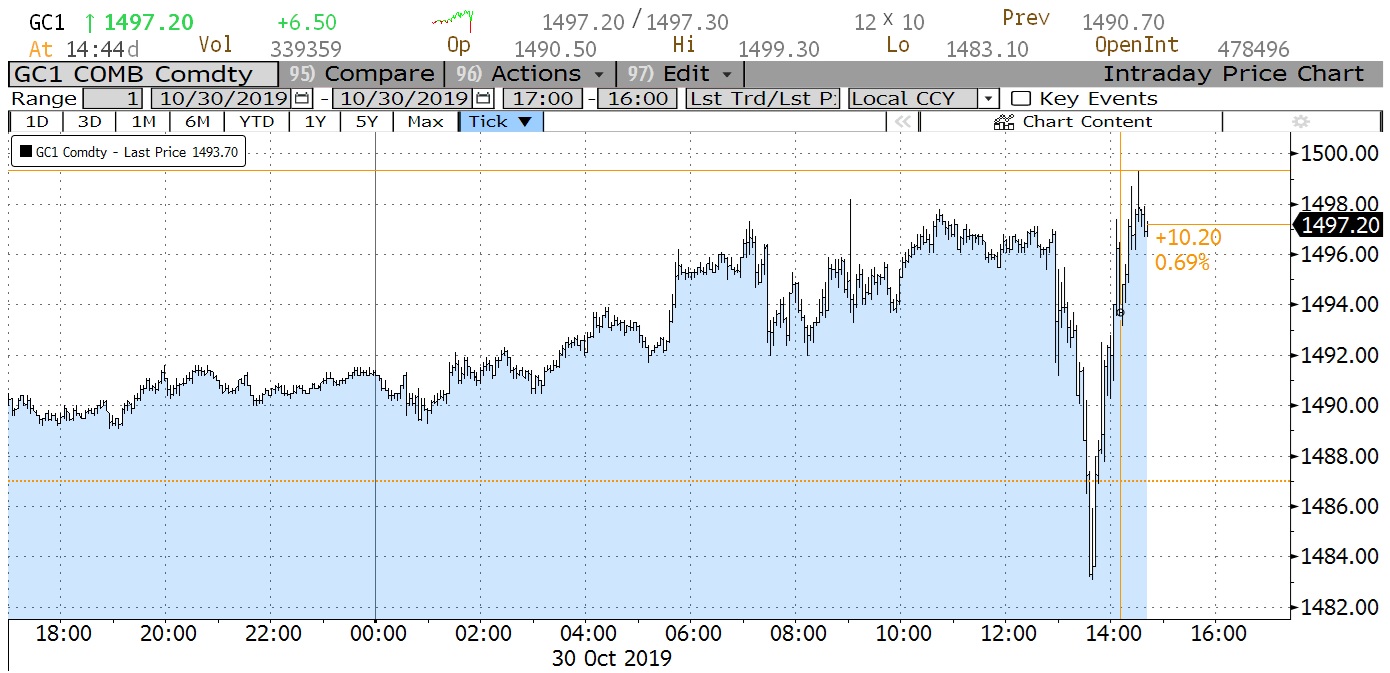

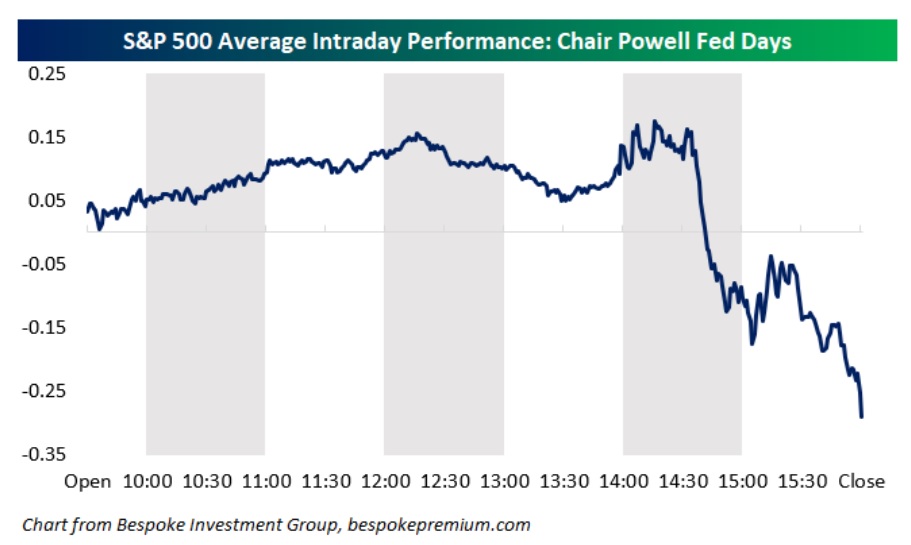

Market reaction was interesting. As the press conference wore on, we saw sentiment shift from hawkish to dovish. The chart below is yesterday’s intraday price action in gold. Note the “V” bottom; the initial reaction to the statement was bearish for gold, but there was a decided shift in sentiment.

(Source: Bloomberg)

When Powell suggested that the Fed was not likely to raise rates anytime soon, it was a tacit admission that the last three rate hikes were a mistake. Here is the relevant comment from the presser:

Q: You have prepared this rate cutting cycle to the insurance cuts in the ’90s. The Greenspan fed took those cuts back after awhile. They raised rates again fairly quickly. I am curious what the onus is for doing that in this cycle. What would you make you guys decide it is appropriate to raise interest rates again?

A: So the reason why we raised interest rates is because generally is because we see inflation as moving up or in danger of moving significantly. We don’t see that now. Inflation moved down in the first quarter of this year. We thought that that was due to some extent to transient factors. That turns out to have been the case. It has moved back up. But it seems to be settling in below 2%. So we really don’t see that risk. And inflation expectations have also kind of moved down and sideways both surveys and market based over the course of this– of really the recent months. And, you know, we think that inflation expectations are very important in driving actual inflation and we are strongly committed to achieving our 2% I inflation objective. So we are not thinking about raising rates right now…What we are thinking now is that our current stance of policy is appropriate. Will remain so as long as the outlook is keeping with the expectations.

In other words, unlike the 1995 mid-course correction, it is unlikely these cuts will be reversed anytime soon. That led to the bounce in gold, a lift in equities and a rally in fixed income. The lack of fear from a Fed mistake could boost equities into the usual Q4 rally, assuming that there are no issues emerging from trade.

China trade: A new wrinkle emerged on the trade talks. Chile’s President Pinera, due to persistent unrest, has cancelled the APEC leader’s summit that was scheduled for November 16-17. Without this meeting, Presidents Xi and Trump will have to set up a specific meeting of the two leaders There are reports that China is pushing back against large grain purchases, and is unhappy with human rights talks. Despite the cancellation, negotiations continue and some sort of trade arrangement, a small deal, is likely. However, what has reversed equity futures this morning are reports from China that indicate a long-term deal with the U.S. on trade probably isn’t possible. If a major deal isn’t possible, a steady deterioration of relations between the world’s two largest economies is likely.

China economic data: Although we cover the data itself below, we note that the official PMI data came in soft. The government’s official purchasing managers index fell to a seasonally-adjusted 49.3, short of expectations that it would hold steady at the 49.8 reached in September. The index has now been under the 50 level that indicates expansion for six straight months, reflecting both China’s secular slowdown, and the U.S.-China trade war. That bodes poorly for Chinese equities.

Perhaps even more unsettling is Hong Kong’s GDP; preliminary data shows the city-state’s GDP plunged 3.2% in the third quarter, far worse than both the expected decline of 0.5% and the second-quarter fall of 0.6%. By conventional reckoning, that means the economy is now in recession, reflecting the negative impact from continued anti-China political protests, the U.S.-China trade war and capital flight.

A signal of change: The House voted 405-11, in a non-binding resolution, to say the U.S. government should no longer associate itself with the denial of the Armenian genocide that occurred from 1915-23. Turkey vehemently disputes this allegation, and the U.S. has generally avoided taking a position on this issue, especially after WWII, to maintain favorable relations with Ankara. The fact that this resolution passed is a signal of how far relations have deteriorated. Erdogan’s response was rather muted, suggesting the U.S. has “no right to give lessons to Turkey.”

United Kingdom: Labour Party leader Corbyn launched his campaign for the December election by vowing to change the country’s “corrupt” economic system and bring down the “privileged” rich. To make his proposals as concrete as possible, he specifically named multiple high-profile individuals that he would target, including the Duke of Westminster and other landlords that he accused of hiking rents and tearing down economical apartments to build luxury high rises.

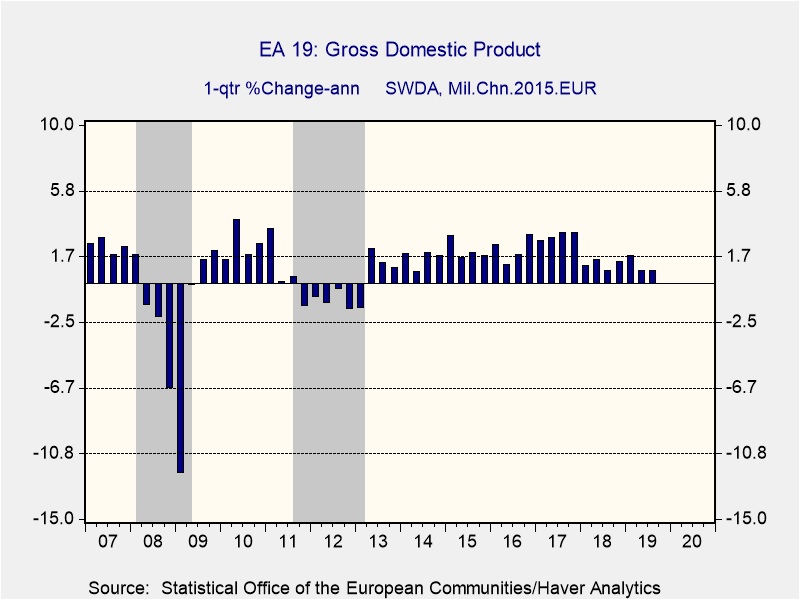

Eurozone: Eurostat today said Eurozone GDP continued to rise tepidly in the third quarter, posting an annualized growth rate of just 0.8% after stripping out seasonal and price effects. That matched the second-quarter growth rate, but it was significantly lower than the 1.7% growth rate in the first quarter.

India-North Korea: The Nuclear Power Corporation of India has confirmed that malware was surreptitiously installed on the computer system of its newest nuclear plant. Even worse, cybersecurity firms have already traced a large data extraction from the plant to the Lazarus Group of North Korean hackers. The hack highlights the continuing risk that rogue states or groups could launch a sudden, unexpected cyberattack on critical facilities around the world.

Energy update: Crude oil inventories rose 5.7 mb compared to an expected build of 0.5 mb.

In the details, U.S. crude oil production was unchanged at 12.6 mbpd. Exports fell 0.4 mbpd while imports jumped 0.58 mbpd. The unexpected rise in stockpiles was mostly due to rising imports which offset improved refinery demand.

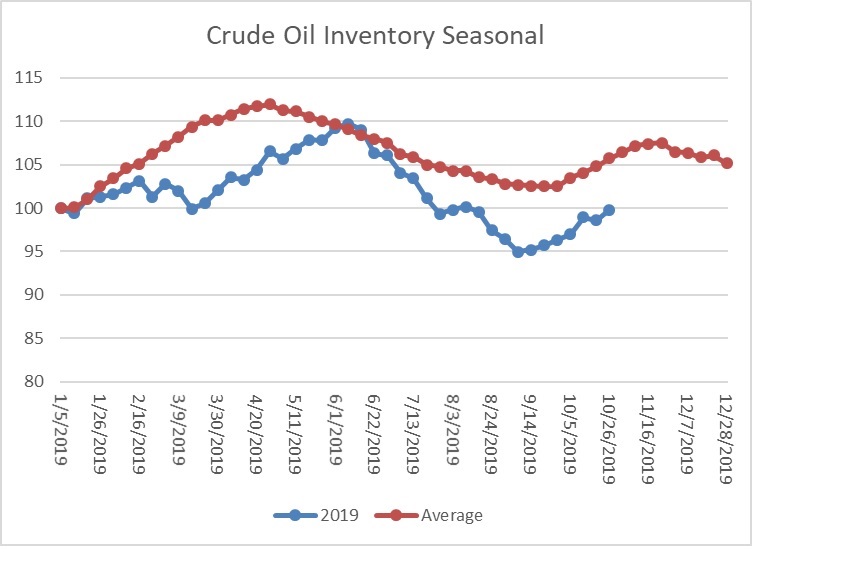

(Sources: DOE, CIM)

This chart shows the annual seasonal pattern for crude oil inventories. We are now into the autumn build season which usually lasts into early December. This week’s rise is normal. We continue to monitor the autumn refinery maintenance season.

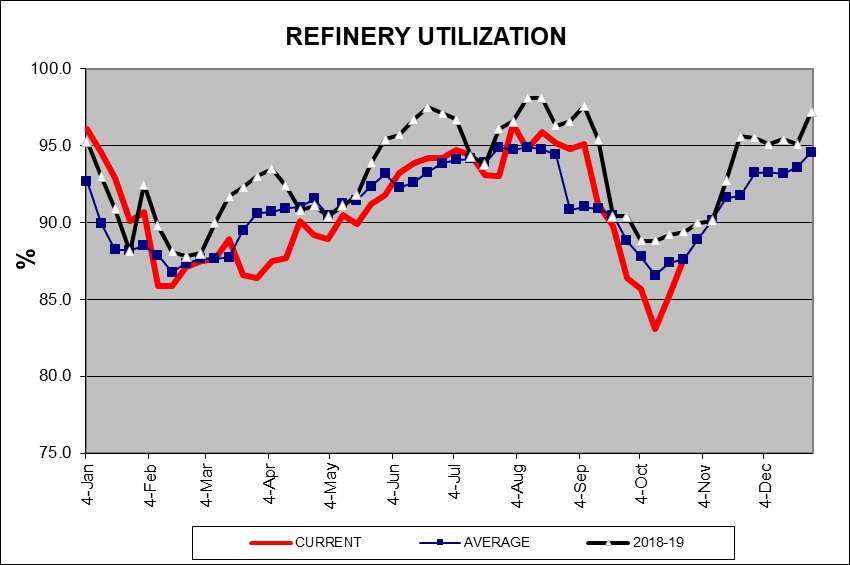

(Sources: DOE, CIM)This week’s recovery in utilization recovered “on schedule”. WE would expect refinery operations to rise steadily into year’s end.

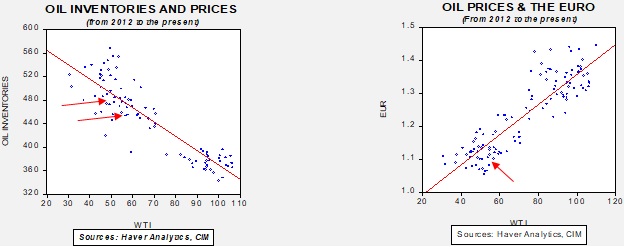

Based our oil inventory/price model, fair value is $61.13; using the euro/price model, fair value is $48.79. The combined model, a broader analysis of the oil price, generates a fair value of $52.27. We are seeing a clear divergence between the impact of the dollar and oil inventories. Given that we are into the maintenance season, we would normally expect inventories to continue to rise. Prices will remain sensitive to Saudi output and tensions in the Middle East.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EDT]

It’s Fed day! We discussed the FOMC meeting in detail yesterday; there’s a quick summary below. It’s also GDP day (see the Economic Releases section below for details). At long last, there will be elections in the U.K., and we also update news from China. Here are the details:

The second episode of the Confluence of Ideas podcast is available!

FOMC day: As we noted yesterday, a rate cut today would shrink the spread between the implied yield from the two-year deferred Eurodollar futures and fed funds to near zero. If the Fed is using the 1995 mid-course correction as an analog, there is a chance of one more rate cut, but a pause would not be out of the question. Given the divisions on the FOMC, squeaking out one more cut is probably about all that Powell can muster. How will the markets take a pause signal? Not well unless the statement suggests the Fed will continue to support the expansion. That language will likely remain, so we don’t expect a bearish surprise there. Finally, it is worth noting that Powell’s press conferences have had a tendency to be hawkish.

Before one decides to engage in a short-day trade, a word of caution—Powell has been learning as he goes along and thus this chart may more reflect his learning curve rather than a hawkish bias. We will recap the meeting tomorrow.

China: Although the fourth plenum is continuing, there is little information emerging from the meetings, as is the custom. In other China news, the regime claims to have eliminated all restrictions on foreign investment and will “neither explicitly nor implicitly” force foreign investors or companies to transfer technologies. However, this new “directive” does not include investments or foreign firms on “negative lists,” which means industries that are barred from foreign involvement. At first glance, this appears to be a major breakthrough. However, it isn’t clear whether this directive has the force of law. Nevertheless, this may be as much as the Trump administration can get and, in reality, even if a law is passed, enforcing such a law may not occur anyway. If the U.S. takes this as a win, it is possible that progress on trade can occur. At the same time, there are conflicting reports about a deal being ready for the November APEC meeting.

In another noteworthy development, Chairman Xi has apparently supported the development of a Chinese blockchain to ostensibly eliminate the need for the S.W.I.F.T. network. That network facilitates money and information transfer between banks. It has been used by the U.S. to enforce sanctions and China would like to undermine that power. The Chinese version of a cryptocurrency would be one managed and monitored by the state.

Brexit: At long last, we will have an election. On December 12, U.K. voters will go to the polls. If a Tory government emerges, Johnson’s plan will likely be the structure of a Brexit deal. If Labour can team up with the SNP, a second referendum will be held. And, if the Liberal-Democrats win, Article 50 will be scrapped. The wild card for the Tories is Nigel Farage’s Brexit Party. He will argue that Johnson has failed to deliver Brexit; if a voter wants out of the EU, the Brexit Party is the only sure way to deliver that outcome. For Labour, the problem is that the party has never fully defined its position on Brexit. And so, there is a chance that working class older Labour supporters will drift to the Tories or the Brexit Party. The Liberal-Democrats may be able to capture younger Remain voters from Labour as well. Labour will try to make the election about anything but Brexit. That might simply not be possible.

So, overall, the new election is a risky maneuver for all involved. Current polls show the Conservatives with a sizeable margin; however, as the last election showed, the British electorate is fluid. It does appear that the odds of crashing out of the EU are nearly zero and the choice is either a staged exit or remain. Accordingly, we are seeing the GBP lift on the news.

Lebanon: We have been reporting about rising unrest around the world; Hong Kong, Bolivia, Chile and Lebanon have all been scenes of civil disorder. In Lebanon, PM Hariri has given up and resigned. Lebanese politics are finely balanced; Shiites, Christians, Sunnis and Druze all hold various parts of the government. Protestors oppose this arrangement, seeing it as an impediment to progress. However, it is unclear what will occur if the current arrangement unravels. In the 1970s, the result was a bloody civil war. Hezbollah, the Shiite group that is arguably the most powerful body in the country, has shown no interest in resigning from the government or participating in a reshuffle.

USMCA: There are fears that the impeachment proceedings will delay a vote on the North American trade deal. However, another issue has emerged; the Trump administration wants to dictate where auto companies can make cars and parts, and receive duty-free treatment under USMCA. This is a remarkable degree of interference into the sourcing and investment decisions of companies, but is a further signal of a swing toward an equality cycle.

The new subprime? Years after the financial crisis it appears that consumer installment loans have replaced the controversial sub-prime mortgage as debt vehicle of choice for borrowers with both low credit and savings. As opposed to a credit card, installment loans allow consumers to borrow money for specific purchases. Because rising wages have stagnated for workers, corporations have offered installment loans in order to boost profits and meet consumer demands. That said, the practice of issuing installment loans has come under increased scrutiny as some lenders have begun to take advantage of the lack oversight and have issued loans with interest rates well into the triple digits. The usage of these installment loans is a cause of concern as the economy debt burdens weigh on consumers’ willingness to spend. In addition, increased scrutiny of these instalment loans provides further evidence that economy policy is likely shifting away from favoring efficiency, and more toward favoring equality. Earlier this month, California passed a bill that would effectively limit the amount of interest charged on installments loans to 36% plus the fed funds rate for loans between $2,500 and $10,000.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EDT]

The S&P 500 hit a new record yesterday.[1] There is growing hope of a trade deal. The FOMC meeting begins today. Brexit continues. Here are the details:

China trade: Contours of a trade deal, or ceasefire, are slowly emerging. There are reports that the U.S. will offer to extend tariff delays of 25% on $34 bn of Chinese consumer electronics. These tariffs were initially set for July 2018 but granted exclusions that ran through December 28th of this year. The USTR is said to be considering extending these by another year. This seems like a rather small offer; we haven’t heard anything from the Chinese side most likely because they are holding CPC meetings. Peter Navarro is said to be opposed to the trend of negotiations but, unlike in earlier talks, he and Lighthizer are not together in opposition. From our perspective, a modest extension of tariff exclusions and an offer to buy soybeans seems like a rather small agreement. However, we do note that China is allowing the CNY to appreciate, which may be a signal it is willing to make an arrangement. However, a simple delay in trade hostilities is probably enough to cool market worries and give stocks a boost.

FOMC: Market expectations are calling for a 25 bp rate cut at this week’s meeting, which will end tomorrow. This is a meeting without “dots” so all we will have to work with is the statement and the press conference. What we will be watching for is how the financial markets react to a signal of a pause. Chair Powell still has a large contingent of Phillips Curve adherents who will be less that keen on further cuts in the face of low unemployment. And, equities hitting new highs will weaken the resolve of the few members who worry about financial market froth. If Powell is using the mid-1990s soft landing as a policy guide, we are getting close to a pause point.

This chart shows the implied three-month LIBOR rate from the Eurodollar futures market along with the fed funds target. The spread is the upper line. Inversions are shown by vertical lines. In 1995, the Greenspan Fed abruptly ended a tightening cycle as the spread inverted and generally guided rates based on the behavior of the implied LIBOR rate. The current spread is -40 bps; another 25 bps cut will get us close to a positive spread. It would not surprise us to see the Fed pause if we get a cut tomorrow.

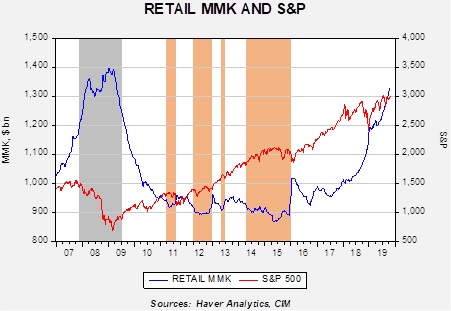

In light of new highs in equity indices, the question then becomes how will equity markets react if the Fed pauses? Most likely, without a steady diet of accommodation, equity markets will probably stall. However, through all of the recent strength, retail money market levels continue to rise.

If investor sentiment swings to euphoria, there is ample fuel for a major rally in equities. For that to occur, we would probably need more than a ceasefire in the trade situation. Nevertheless, the rally in equities while cash levels are increasing is impressive.

Brexit: The saga continues. After seeing an election bill fail, PM Johnson is trying another tactic, this time a simple bill that would allow for an election without a two-thirds majority. So far, the GBP is holding up through these machinations. U.K. betting sites are leaning toward a hung election, where no party wins a governing majority. In the details, at least one major bookie says there are even odds that no party will win an outright majority, while two others put the odds of that outcome at 11/10 (52.4%). All three major bookies put the odds of the Conservative Party winning an outright majority at 10/11 (47.6%), while they put the odds of Labor winning a majority at between 23/1 (4.2%) and 16/1 (5.9%).

Global Investment Flows: In a sign that anti-globalism political leaders aren’t just rolling back trade, the OECD has issued a report showing international investment flows are also dropping. In the first half of 2019, the data shows foreign direct investment across the globe was down some 20% from the second half of 2018. FDI into the United States was down more than 25%.

Japan-South Korea: Media reports yesterday said Japanese and South Korean officials are working on a deal to resolve their dispute over Japan’s behavior in Korea before and during World War II. The deal would focus on compensating Koreans who were subject to forced labor by the Japanese, potentially via an “economic cooperation” fund to be financed by Japanese companies. As we discussed in our WGR of September 30 and October 7, the Japanese government insists that it owes nothing under the 1965 treaty that normalized relations between the countries, while recent South Korean court decisions have allowed Koreans to sue Japanese firms for redress. The proposed deal would allow compensation to be paid in all but name. Today, Japanese officials denied any such deal is in the works, but that could just be political posturing. If such a deal is completed, it would remove a significant cloud over Japanese-South Korean trade, so it would likely be a modest positive for Asian equities.

Hong Kong: Pro-democracy activist Joshua Wong was officially disqualified from running in next month’s local elections, on grounds that his political group has called for Hong Kong to have self-determination. Meanwhile, municipal Chief Executive Carrie Lam denied that Chinese leaders in Beijing are planning to oust her for her failure to control the city’s continuing and increasingly violent anti-China protests. Together, the developments are likely to add more fuel to the protests, and further weigh on the Hong Kong economy and financial markets.

Russia: As a reminder that various Russian organizations continue to push back against President Putin’s narrative of a Great Power Russia where all is well, activists in Moscow today publicly read the names of 40,000 fellow citizens executed by Stalin in 1937-38. The ceremony took place in Lubyanka Square, directly in front of the former KGB headquarters, which is now the headquarters for the KGB’s main successor agency, the Federal Security Service (FSB). Similar readings took place in some 35 cities across the country.

Saudi Arabia: The government opens its third annual Future Investment Initiative conference today, featuring at least five presidents and the chiefs of several major multinational corporations. Given the high-level attendees, the “Davos in the Desert” meeting will have the potential to produce policy or corporate news – and potential mischief by Saudi rival Iran.

Odds and ends: As impeachment accelerates, there is concern that the other business of Congress is getting sidelined. For example, we might see a government shutdown or USMCA may be put at risk. One of the side benefits of the raid that killed al-Baghdadi is that intelligence is gathered from the leader’s compound. Something similar occurred after the raid on bin Laden’s compound. We note that an IS spokesman was killed in an airstrike yesterday.

[1] It’s the 90th anniversary of “Black Tuesday.” The Dow Jones Industrials lost nearly 25% over two days on October 28th and 29th and volume on the 29th reached a record that held for nearly 40 years.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.