Daily Comment (October 17, 2019)

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EDT] The EU and the PM Johnson have a deal. Trade news continues. Interesting items emerging from the financial markets. Here are the details:

Brexit: In the wee small hours of the morning (at least in the U.S.), EU and U.K. negotiators made a deal on Brexit. Here are the key points:

- The deal is mostly what PM May delivered with one key difference. The May deal forced the entirety of the U.K. to remain in the EU customs union. Under Johnson, only Northern Ireland is still in the customs union. In effect, there is a trade barrier between the British Isles and the Irish Sea. As we suggested earlier, there was a clear chance that Johnson would sell out the DUP to get a deal. It looks like he did. The U.K. will now be able to negotiate new trade agreements with other nations, but Northern Ireland won’t be included in whatever arrangement emerges.

- The DUP has already come out in opposition. This is to be expected. However, it should be noted that of the 18 seats in Northern Ireland, seven lean republican (support union with Ireland) and so those seven will likely support the deal. After all, Northern Ireland’s economic position is enhanced; it will be a member of both the U.K. and EU customs unions and there won’t be a hard border with the Republic of Ireland. However, for the Unionists this deal is terrifying because it does separate, at least in economic terms, Northern Ireland from the U.K. That is a step toward unification, although it may be a minor one.

- At the same time, the DUP rejection will have an effect on hardline Brexit supporters within the Tories. When the DUP rejected May’s proposal, this group (the “European Study Group”) also rejected her plan. Johnson has to sway this faction without DUP support—not impossible, but not easy either.

- Johnson agreed to language of “maintaining a level playing field” with EU regulations. In theory, this agreement would prevent the U.K. from becoming the “Singapore on the Thames,” a U.K. that is deregulated and thus a threat to the cozy regulated world of the EU. However, this promise is in the political section and is non-binding. Elements of Labour that want Brexit, but want to avoid deregulation might take comfort in this agreement and vote for the deal. Elements of the Conservatives (and the Brexit party) that want the “Singapore” option will have to trust Johnson, and believe these are simple “weasel words.”

- The EU will need to accept this deal. All 27. We suspect they will, but nothing is guaranteed.

- Johnson wants the EU to signal it won’t give the U.K. an extension, thus framing this weekend’s vote in Parliament as either “Johnson’s deal or hard Brexit.” So far, the EU has not supported this position. We would not expect them to, but if Juncker does deliver this for Johnson, it would give him tremendous leverage.

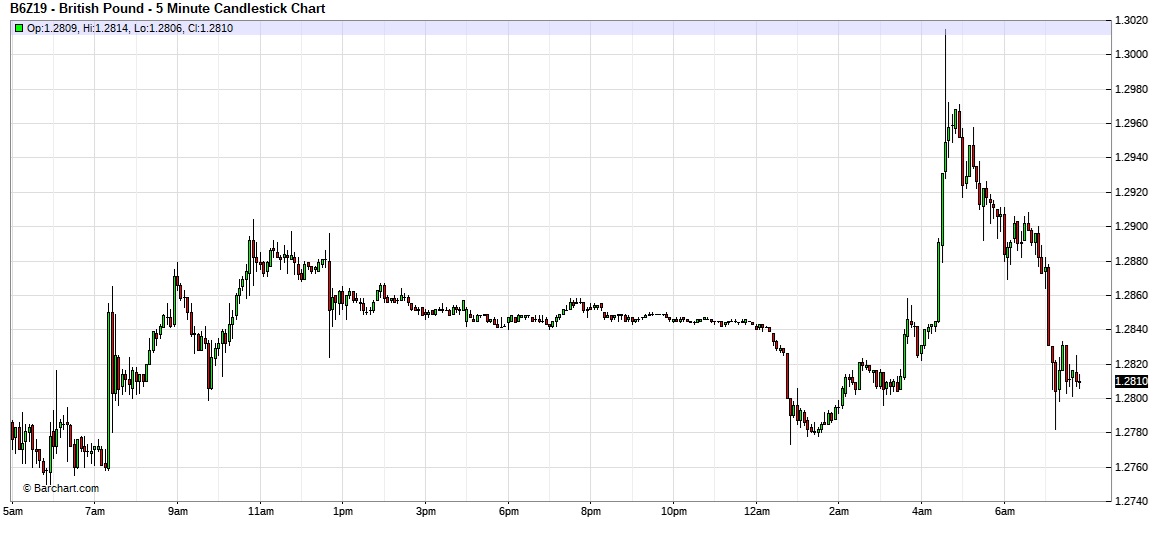

- The GBP initially rallied on news of a deal but has fallen rather sharply on fears thar Parliament will, like it did with May, ultimately reject it. Or, Parliament will require amendments, e.g., approval only after a referendum. So, there is still risk that this could all fall apart. Johnson needs 320 votes. He may not be able to pull this off. He will likely need Labour votes to win and if Johnson’s deal is passed, he will almost certainly win new elections. However, if Johnson can get the EU to make this vote on Saturday either by deal or hard Brexit, he might just pull it off.

European Union: Illustrating how the Brexit deal will affect EU politics, German Chancellor Merkel said Britain’s exit from the union will leave her country with an “excessive burden.” She therefore demanded that Germany get a rebate from the EU budget. Given that Germany’s relative weight in the EU will rise after Britain leaves, she may well get what she demands.

European Central Bank: In a speech yesterday, Bundesbank Chief Weidmann warned against a broadened stimulus policy that many think incoming ECB Chief Lagarde may consider, i.e., buying government bonds in return for infrastructure, or climate change investment. That adds to similar pushback from French, Dutch and Austrian central bankers.

United States: The United Auto Workers and General Motors (GM, 36.65) have reached a tentative deal on a new labor contract, although the ongoing strike could continue for as long as two weeks until union leaders approve it. Whatever the final outlines of the deal, we think the union’s ability to hold out for a full month is a signal of rebounding power for organized labor. If that rebound continues and broadens, it could eventually become a significant headwind for corporate margins, playing into the environment of greater regulation and increased inflation pressure that we think will evolve over time.

China: Even if a truce is reached in the U.S.-China trade war, the Chinese government will struggle to reignite growth with fiscal or monetary stimulus measures. At a conference of local-government development funds this week, officials complained that even if they were given more money, they are running out of attractive infrastructure projects to invest in. That serves as a reminder that China’s economic slowdown doesn’t just reflect the trade war; it also reflects the fact that the economy is maturing and now has fewer attractive investment opportunities than before.

China: Based on a survey across 18 cities, Cushman & Wakefield estimates China’s commercial real estate vacancies stood at 20.0% in the third quarter, up from 16.7% in the third quarter of 2018. The consultancy said the rise in vacancies came not from excess building, but from weaker demand amid the continuing U.S.-China trade war and economic slowdown.

Saudi Arabia: Confirming our view that the successful missile and drone attacks on Saudi oil facilities last month reflect incompetence, U.S. officials revealed they have struggled to convince the Saudis to upgrade their air defense systems. According to one official, “We’ve told them their defense system was not up to speed. But their defense apparatus [and] their central command lack competence.” Even though the attacks failed to give a lasting boost to oil prices, systemic vulnerabilities in the Saudi air defense network and Iran’s desire to cause pain suggests we may see an even bigger attack from Iran in the future, which could have a larger, more lasting impact on the oil markets.

Odds and ends: Scotch distillers, facing a tariff jump, are air freighting their precious liquid to the U.S. to beat the deadline. There has been some rather interesting market action recently. First, there has been a slew of profitable large option trades that have benefited from policy statements made by the Trump administration. There are probably three potential reasons (a) insider leaks, (b) really good algorithms, and (c) there have been a number of these positions that haven’t worked but we don’t hear about those. We reserve judgement for now. Second, Eurodollar futures options traders are placing bets on negative interest rates. We doubt these will be profitable, but the fact they are being made is newsworthy.