In our most recent asset allocation rebalancing, we added foreign allocations to our portfolios. Over the past few years, we had generally avoided allocations to non-U.S. markets in asset allocation portfolios due to two primary concerns. First, the dollar had been appreciating as a result of an improving U.S. economy and policy divergences between the U.S. and the rest of the world. The Federal Reserve was raising rates and tapering its balance sheet while the majority of other nations were still adding monetary stimulus. Second, we have had secular concerns about the stability and attractiveness of foreign investing in a world where the U.S. is seemingly reducing its hegemonic role.

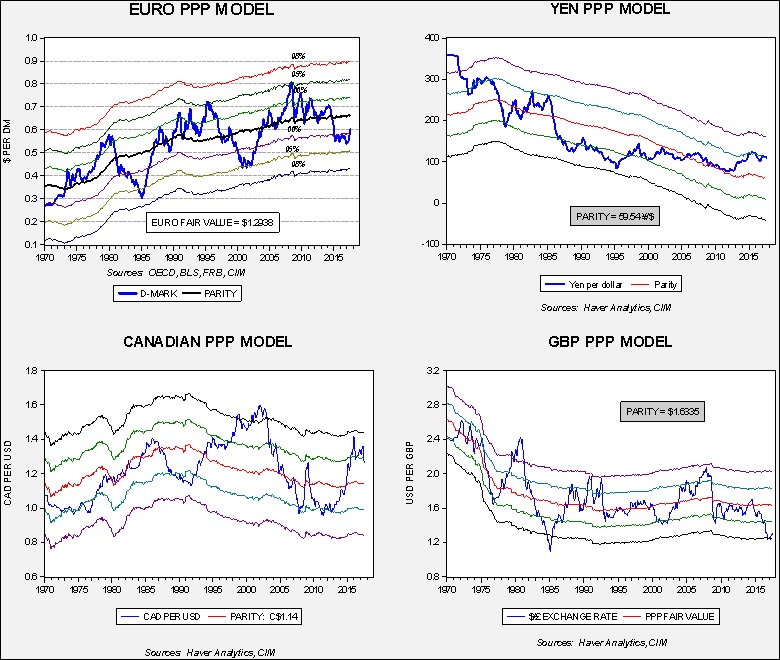

We previously noted that the dollar was deeply undervalued on a purchasing power parity basis and vulnerable to depreciation. The catalysts for dollar weakness appear to be coming from two sources. First, the FOMC is moving very slowly to tighten policy while the rest of the world’s central banks are finally withdrawing policy stimulus. Second, uncertainty surrounding American governance appears to be undermining investor confidence and leading to dollar selling. In this week’s report, we wanted to update the valuation levels for the dollar against the yen, euro, Canadian dollar and British pound.

This chart shows four purchasing power parity models for the aforementioned currencies. In all four cases, the dollar was trading “rich” by more than one standard error, and nearly two standard errors from parity in two cases. Over the past two months, three of the four currencies have begun to appreciate and are indicating some modest improvement in valuation. However, these models all suggest that the dollar is still overvalued and thus, even with the recent depreciation, the greenback is still overvalued. Hence, the narrative that a weaker dollar should support further gains in overseas assets remains viable. If history is any guide, we are still in the early stages of a dollar reversal that should remain in place for the foreseeable future.

At the same time, the secular concerns about the impact of the withdrawal of U.S. hegemony will likely be a bearish factor for overseas investments. For now, we expect the dollar’s weakness to overshadow concerns over global stability. But, as some point, possibly in the next couple of years, the dollar will be closer to fair value and the case for foreign investment will be more difficult to justify.

[Posted: 9:30 AM EDT] Hawkish comments from the BOE continue to lift the GBP. Here is what we are watching today:

North Korea launches (yawn): As expected, North Korea launched a missile that passed over the Japanese island of Hokkaido. The missile appears to be an intermediate-range ballistic missile, not an ICBM. This missile’s distance exceeded the recent one over Japan and shows North Korea can now threaten Guam. Market reaction thus far has been enlightening. The usual flight to safety trade is long JPY, Treasuries and gold. All are lower today. Geopolitical tensions exhibit a pattern in markets over time. Unless conditions escalate significantly, each event has less impact with repetition. We have seen this pattern with terrorist events and now we are seeing it with missile launches. It does not appear that Kim Jong-un is taking into account Western financial market behavior with his provocations but, if he did, this one would be rather disappointing.

Terrorist attack in the London Underground: There was a terrorist attack in a London subway platform this morning. It appears to be an improvised explosive device that injured 22 people, none seriously. There was no obvious market impact, although follow-on attacks after these events do occasionally occur. We will continue to monitor the news flow.

Venezuela suspends dollar auctions, prices oil in EUR: Venezuelan President Maduro has indicated that his nation, in a bid to dilute the impact of U.S. sanctions, will be invoicing oil in EUR going forward. Iraq did something similar under Saddam Hussein. This scheme probably won’t work well for Caracas. The U.S. is a major trading partner with Venezuela and forcing U.S. firms to use EUR will simply discourage American buyers further. In addition, having EUR will increase the cost of servicing dollar-denominated debt, in that it will take another step in translation to adjust the debt. This move smacks of desperation.

The return of the Italian lira? Three of Italy’s largest political parties are calling for a dual currency to trade alongside the EUR. The Five Star Movement, the Northern League and Silvio Berlusconi’s Forza Italia have all proposed introducing a new currency following the election scheduled for next year. Italian lawmakers are using this as a threat to Brussels to allow Italy to violate the fiscal spending rules. In the last ECB press conference, Draghi shot down this idea, saying that there is only one legal tender in the Eurozone, the EUR. If Italy were to exit the Eurozone, it would be a serious blow to European unity, perhaps a bigger problem than Brexit. Although we have been bullish the EUR, this position would need to be reevaluated if this parallel currency movement gains momentum.

Bitcoin tumbles: China has outlawed cryptocurrency exchanges and various financial leaders in the U.S. have said derogatory things about these currencies. Bitcoin, the predominant cryptocurrency, has fallen over 30% recently. The sharp decline is an indication of the ephemeral nature of cryptocurrencies.

(Source: Bloomberg)

Saudi news: There were a few items of interest emerging from Saudi Arabia. First, Sputnik (admittedly, not the most reliable of sources) is saying the kingdom is looking for a vendor to build nuclear reactors for electrical power. The report indicates that no U.S. firms will be asked to bid on the project (which seems odd, given the warm relations the president seems to have with the king). The worry, of course, is that this plan will eventually lead to the kingdom getting nuclear weapons. Second, the crown prince appears to be behind a series of arrests designed to stifle dissent. According to reports, a number of clerics have been arrested.[1] We have been hearing rumors that the royal family is working to curtail the influence of the clerical establishment in a bid to loosen Saudi Arabia’s rather stodgy social scene. In addition to clerics, others have been arrested as well, including a member of the royal family. The NYT reports that Jamal Khashoggi, a long-tenured journalist and commentator, has moved to the U.S., fearing arrest.[2]

Iran deal approved: Yesterday, we noted that President Trump had to renew the Iran deal, which was expiring. Although there is growing concern he will end the deal, he did approve it yesterday but is indicating that he intends to curtail Iran’s influence in the region.

[Posted: 9:30 AM EDT] With the exception of the GBP, financial markets were quiet overnight. However, the CPI data and reports that North Korea may be preparing for a missile launch have led to increased volatility. And, there was a lot of news to cover this morning. Here is what we are watching today:

North Korea ready to launch: There are reports that North Korea may be preparing for a new launch. In a similar vein, analysts looking at the recent nuclear test are concluding that it was more powerful than first thought, increasing the likelihood that the Kim regime has developed a thermonuclear device.

The BOE: The Bank of England left policy unchanged, as expected, but in its statement the majority indicated that “some withdrawal of monetary stimulus is likely to be appropriate over the coming months.” The Monetary Policy Committee (MPC) voted 7-2 to keep policy steady, with the two dissenters calling for tighter policy. Although Governor Carney appears to remain dovish, fears of rising inflation are leading the majority of the MPC to lean toward raising rates. The GBP has rallied sharply on the news.

A DACA deal? Twitter lit up yesterday evening with reports that the president, along with “Chuck and Nancy,” made a deal on DACA, where the Democrats would support improved border security. Later, the White House indicated that a “deal” wasn’t done but discussions did occur. It appears the president is willing to trade DACA for border security. The important news here is that the president continues to form a working coalition with Democrats and moderate Republicans to isolate the Freedom Caucus. It isn’t obvious if this will become the main working coalition for this president or if he will create new groups on a continuous basis. However, there isn’t much evidence that President Trump has much sympathy for the Freedom Caucus; he doesn’t seem too inclined to shrink the government, deficits don’t bother him and a dovish Fed is preferred. Thus, isolating the Freedom Caucus may be his working position.

A Chinese deal blocked: The White House has blocked a Chinese investor from purchasing Lattice Semiconductor (LSCC, 5.72). The Committee on Foreign Investment in the U.S. (CFIUS) recommended scotching the deal. If the transaction had been consummated, it would have been the largest Chinese purchase in the U.S. microchip sector. CFIUS was concerned that the purchase would facilitate the transfer of intellectual property to China. Most of the time, once a company realizes that CFIUS isn’t going to approve its deal, it quietly kills it. The fact that Lattice and the purchaser, a private equity firm called Canyon Bridge Partners, continued to push the transaction is odd and suggests the firms may have thought the White House would overrule CFIUS. However, given the administration’s growing wariness of China, this hope seemed misplaced.

Iran nuclear deal at risk? The president must reaffirm the Iran nuclear deal every 120 days. President Trump has expressed displeasure with the Iranian deal; although we expect him to approve it today, we would not be surprised to see him try to reopen negotiations in the coming months. Every 90 days, the White House must certify that Iran is compliant to the agreement. The next date will be October 15th, and there are growing worries that Trump will declare Iran out of compliance. If the Iranian deal falls through, we would expect Iran to rapidly move toward building a bomb.

Russian war games: NATO leaders are watching Russia and Belarus hold large-scale war games. Officially, 12,700 troops are participating but Western government sources put the real numbers near 100k. The concern is that these exercises are a precursor to operations against the Baltic States. Thus, for the next week, the region will be on edge, closely watching the Russian military as it runs its war games.

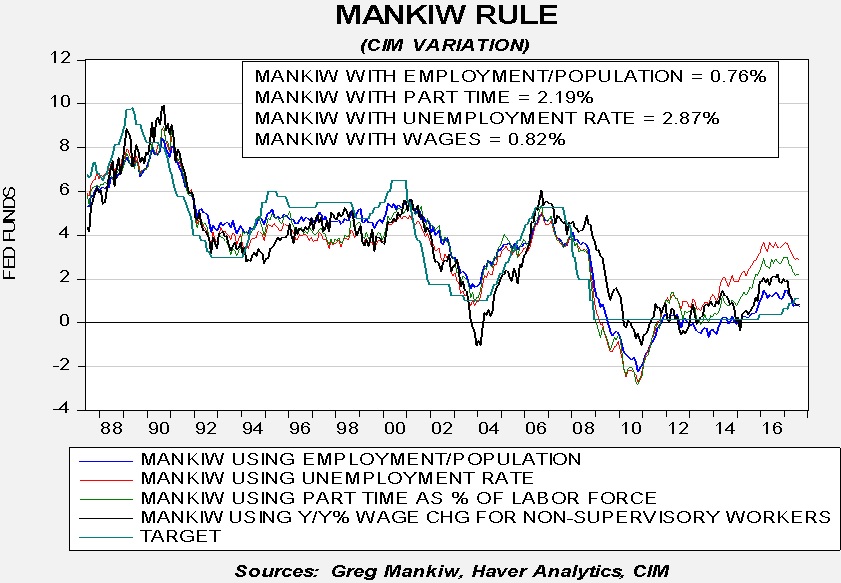

Fed policy: With the release of the CPI data we can upgrade the Mankiw models. The Mankiw rule models attempt to determine the neutral rate for fed funds, which is a rate that is neither accommodative nor stimulative. Mankiw’s model is a variation of the Taylor Rule. The latter measures the neutral rate using core CPI and the difference between GDP and potential GDP, which is an estimate of slack in the economy. Potential GDP cannot be directly observed, only estimated. To overcome this problem, Mankiw used the unemployment rate as a proxy for economic slack. We have created four versions of the rule, one that follows the original construction by using the unemployment rate as a measure of slack, a second that uses the employment/population ratio, a third using involuntary part-time workers as a percentage of the total labor force and a fourth using yearly wage growth for non-supervisory workers.

Using the unemployment rate, the neutral rate is now 2.87%. Using the employment/population ratio, the neutral rate is 0.76%. Using involuntary part-time employment, the neutral rate is 2.19%. Using wage growth for non-supervisory workers, the neutral rate is 0.82%. There wasn’t much change from last month; two of the models, the employment/population ratio and non-supervisory wage growth, are suggesting the Fed has achieved neutral policy. The other two remain elevated and indicate that at least another 100 bps of tightening are necessary to achieve neutral.

To a great extent, the issue for policymakers remains the proper measure of slack. The danger for the financial markets is that the proper measure is wage growth or the employment/population ratio but policymakers believe slack is best measured by involuntary part-time employment or the unemployment rate. If either of the latter two is their measure, policymakers will likely overtighten and prompt a recession. Although the headline data for inflation looks like price level growth is accelerating, core CPI is generally flat on a yearly basis. We are still not seeing much pricing pressure which means the FOMC will likely remain cautious.

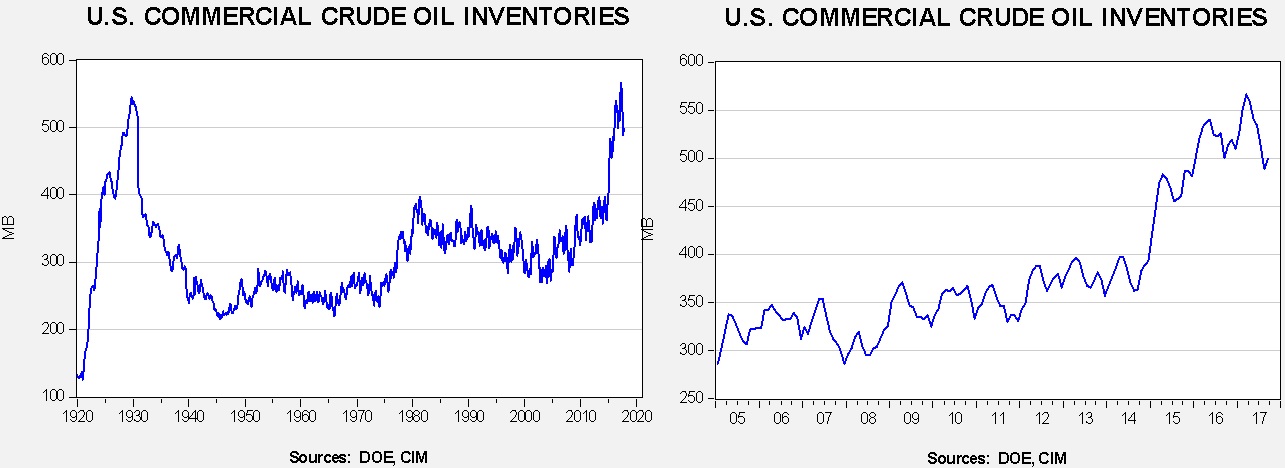

Energy recap: U.S. crude oil inventories rose 5.8 mb compared to market expectations of a 4.8 mb increase.

This chart shows current crude oil inventories, both over the long term and the last decade. We have added the estimated level of lease stocks to maintain the consistency of the data. As the chart shows, inventories remain historically high but have declined. Hurricane Harvey affected the energy market data again this week; the effects should continue for several more weeks.

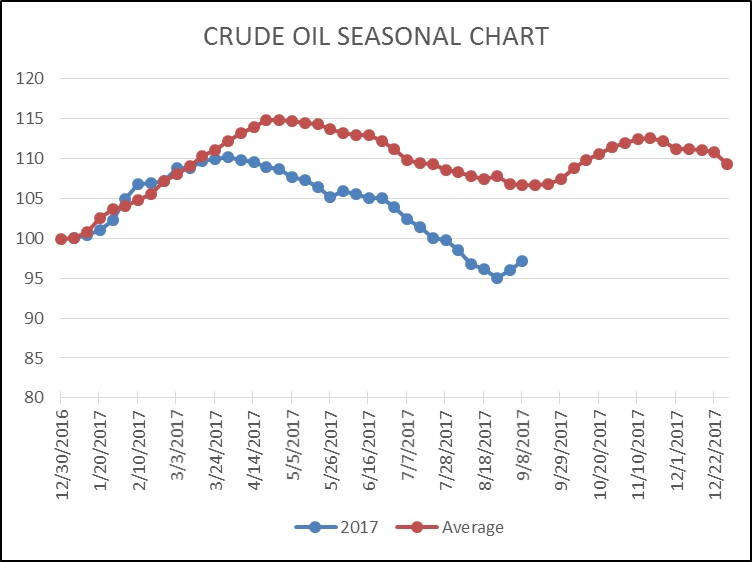

As the seasonal chart below shows, inventories did turn higher again this week but they were affected by the aforementioned hurricane. We are probably going to start the inventory rebuild period sooner than normal this year. Although oil imports remain depressed, dipping nearly 0.5 mbpd, and production recovered by 0.6 mbpd, refinery capacity utilized dropped 2% to 77.7%, or 4.4 mbpd below capacity. Media reports suggest that refineries are working hard to restart operations, but it will probably take a couple of months before the industry can achieve pre-Harvey refinery levels.

(Source: DOE, CIM)

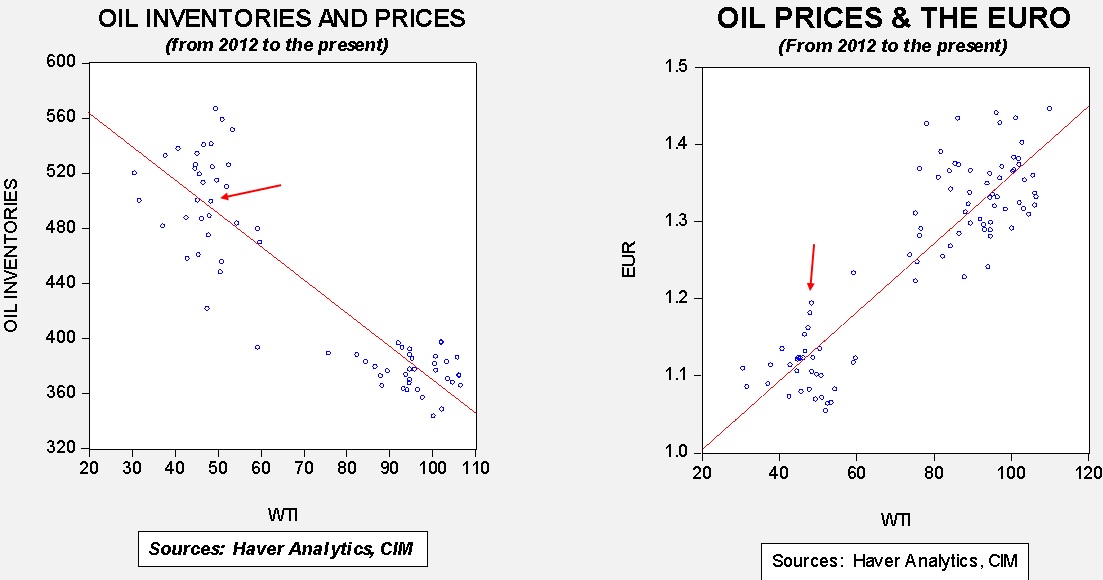

Based on inventories alone, oil prices are undervalued with the fair value price of $51.50. Meanwhile, the EUR/WTI model generates a fair value of $67.07. Together (which is a more sound methodology), fair value is $61.77, meaning that current prices are well below fair value. Although the most bullish factor for oil currently is dollar weakness, the rapid decline in inventory levels is also supportive.

Aramco delay: Saudi Arabia is suggesting that it may delay its IPO of the state oil company, Saudi Aramco, into 2019. That move suggests to us that the Saudis want to give the oil market more time to recover as they would likely want to price the offering in a better environment for oil prices. If so, that would mean they will probably continue to prod OPEC to keep output constrained. We view this as bullish news for the oil markets.

[Posted: 9:30 AM EDT] Financial markets are quiet this morning but there is a good bit of news. Here is what we are watching this morning:

Census releases household income: The media is broadly reporting the Census Bureau report that real household income hit a new record at $59,039 in 2016, up 3.2% from the previous year. Although a clear improvement, most of the trends we have seen over the past four decades remain in place.

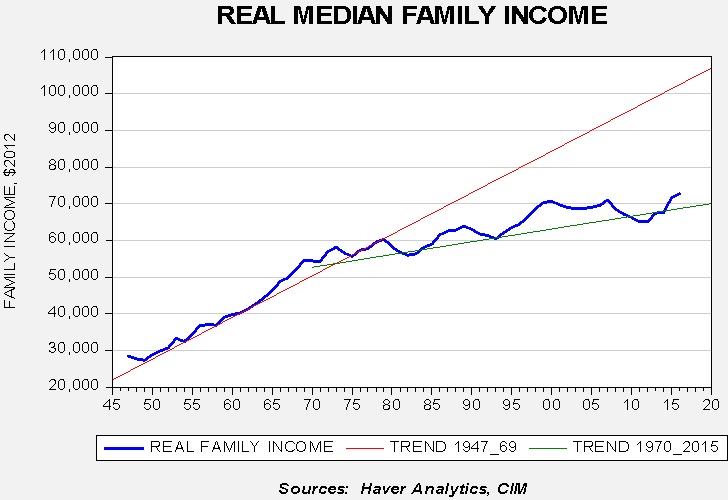

Census has another income unit, families (as compared to households). Family income is for those related by kinship or marriage, whereas household can be any group of cohabitating persons. In terms of family income, we remain on the mostly flat trendline that began in the 1970s.

As this chart shows, until about 1980, real family income was on a rather steep trajectory; after 1980, that trend leveled off substantially. Real family income for 2016 was $72,707; had we stayed on the earlier trendline, this number would be $102,465. When Americans complain about “falling behind” or questioning the American dream, part of that lament is that the trendline fell for family income growth. Why did this happen? There are a number of reasons, but the primary one in our opinion was the combined effect of globalization and deregulation. These two policies, key tenets of supply-side economics, were implemented to corral inflation. Although inflation clearly declined, the cost to society was higher inequality.

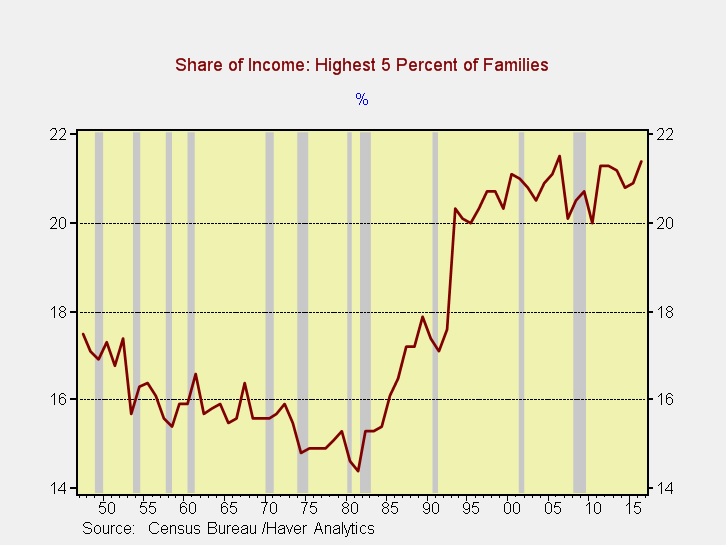

This chart shows the share of family income for the top 5% of families.[1] It reached its minimum in the early 1980s and rose sharply afterward. Essentially, growth in median family income stalled but rose sharply at the high end of the income scales. If a worker could compete in a globalized economy and cope with technology, that worker was amply rewarded. If not, the rewards were far less.

Politically, this disparity fostered the rise of populism. If the income distribution is going to change, we would expect policies designed to increase regulation of the economy and reduce globalization. Those policies would be inflationary over time, which brings us to our next point…

The rise of single-payer sentiment: Sen. Sanders (I-VT) is pushing the Democrat Party into a broad endorsement of single-payer health insurance. Politically, this is a minefield. Eliminating all forms of private insurance will be very disruptive. The hope of single-payer is, “I can get all the health care I want for free.” Of course, this is impossible. Tax rates would balloon to pay for this change unless cost containment is implemented. Clearly, this can be done because other nations do it, too. However, expensive treatments for various maladies are often not covered. The potential for disappointment is high. A much more reasonable approach would be to have a public option for health care and mandate an insurance coverage requirement. That would cover those who can’t afford private insurance. Several European nations use this model and it seems to work rather well. The problem for Democrats is that single-payer is rapidly becoming a litmus test for the primaries but it probably won’t be all that popular with the broad voting public.

Bullish IEA: The International Energy Agency, an arm of the OECD, released its August report today. It showed the oil supply fell 720 kbpd from July to 97.7 mbpd. OPEC cut output by 210 kbpd. Oil demand expectations were also lifted, expected to increase by 1.6 mbpd this year, which would be the strongest demand growth in two years. Meanwhile, Saudi Arabia is in discussions with OPEC to extend the production restriction agreement into mid-2018 (it’s scheduled to end in March 2018) and is chiding the group for cutting production but cutting exports less. Cartel members have been selling oil out of inventory to maintain market share. Saudi Arabia is pressing the group to cut sales, not just production. Oil prices could be poised to rally if Saudi Arabia can extend the output restrictions and convince OPEC to cut exports.

[Posted: 9:30 AM EDT] Yesterday’s market action was consistent with a sharp reversal in the recent risk trade. Amidst concerns about North Korea, the debt ceiling, trends in Washington, hurricane problems, etc., we saw Treasuries and gold rally, the dollar stumble and equities tread water. Those positions reversed yesterday with the dollar and equities rising strongly while the dollar dipped and Treasury yields rose. We are seeing some follow through overnight. It should be noted that renewed tensions with North Korea could bring a return of the aforementioned flight to safety trade. Here are some other items we are watching:

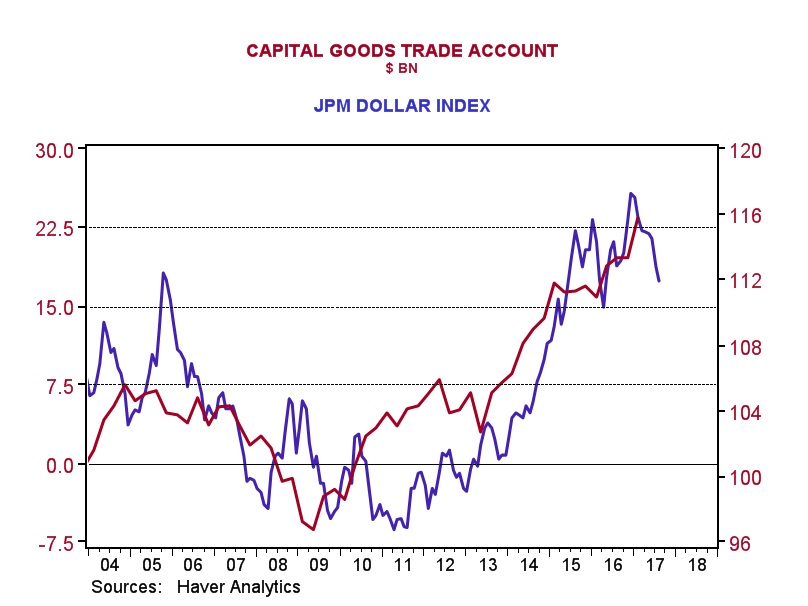

Capital goods balance and the dollar: We took a look at the capital goods trade balance; capital goods are goods designed for investment, e.g., machinery, rolling stock, etc. Over the past 12 years, dollar strength has led to a rising capital goods deficit.

Recent dollar weakness may slow the rising deficit, but a significant narrowing of this deficit would likely require further weakness in the dollar.

North Korea: As expected, the UNSC did approve additional sanctions on North Korea. However, these new sanctions are much less than the U.S. wanted. Given that China and Russia have veto power on the Security Council, getting any significant sanctions through the U.N. will be difficult. We do note that most major Chinese banks announced they will not open new bank accounts with North Korean ties. This action might be signaling that the Xi regime does not want to give into U.S. demands via the U.N. but wants to show its displeasure with the Kim regime over its behavior.

La Diada de Catalunya (Day of Catalonia): Yesterday, pro-independence supporters celebrated Catalonia’s national day by gathering in the streets of Barcelona in support of Catalonia’s independence referendum scheduled for October 1st. Last week, the Catalan regional government passed through legislation that would allow its citizens to decide whether to leave or remain as a part of Spain. The Spanish government has denounced the referendum as illegal and is looking for ways to stop the vote from happening. An independent Catalonia could potentially cause headaches for the European Union as there are no guidelines on how to deal with a breakaway state. In the past, the European Union has sought to quash separatist movements by stating that any breakaway state would have to leave and reapply. Currently, polls shows that the remain camp is ahead 49.4% to 41.1%. Although the vote is non-binding, a vote to leave Spain would embolden the separatists as they await the outcome of Brexit negotiations. If the U.K. is able to strike a decent deal with the European Union upon its exit, then separatists will likely argue that Catalonia could negotiate a similar arrangement.

Three weeks ago, we began our series on nationalism. In Part I, we discussed social contract theory before and after the Enlightenment. We examined three social contract theorists, Thomas Hobbes, John Locke and Jean-Jacques Rousseau. In Part II, we recounted Western history from the American and French Revolutions into WWII. From there, we examined America’s exercise of hegemony and the key lessons learned from the interwar period. This week, we will begin with an historical analysis of the end of the Cold War and the difficulties that have developed in terms of the post-WWII consensus and current problems. We will discuss the tensions between the U.S. superpower role and the domestic problems we face. Next, we will analyze populism, including its rise and the dangers inherent in it. As always, we will conclude with market ramifications.

[Posted: 9:30 AM EDT] Sixteen years ago, the U.S. suffered its worst terrorist attack in its history. The nation was changed in numerous ways, both large and small. Every time we fly commercial we are reminded that our safety was compromised. The country is still trying to unwind two wars related to the attack. On the other hand, the fears that the U.S. would suffer a subsequent similar attack have not come to fruition. This is due, in part, to America’s security and intelligence apparatus. It is also due to the likely fact that 9/11 was something of a long shot by al Qaeda that worked much better than expected. In any case, we still remember those directly affected by the event and keep them in our prayers.

Risk-on has returned to the financial markets. Here is what we are watching today:

A quiet Korean Peninsula: Although there was great fear that Kim Jong-un would test another ICBM, nothing occurred over the weekend. It’s possible that, despite Saturday being a major holiday in the DPRK, there are backchannel discussions going on and the lack of launch is a good faith effort. Or, it may mean Kim simply decided to enjoy the weekend. Meanwhile, the UNSC is working on some rather meek sanctions that probably won’t matter much. We would not be surprised to see the U.S. apply unilateral financial sanctions on North Korea, but it won’t be possible to put a direct oil embargo on North Korea because China won’t cooperate. At the same time, the NYT reports that the trade imbalance between North Korea and China is widening.[1] It isn’t clear what currency China uses when it settles trade with North Korea. Nobody wants the North Korean won and so we suspect North Korea simply builds arrears in CNY. Eventually, either trade will stop because firms will no longer want to accept IOUs from the DPRK or the Chinese government will swap the IOUs to pay the firms and settle the debt. Simply put, Chinese trade with North Korea could become more like aid, something we doubt China will continue with indefinitely.

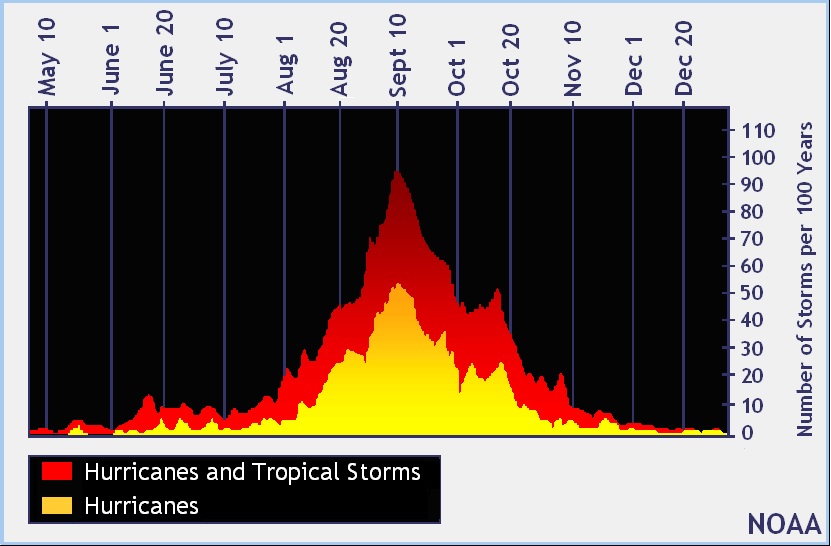

TS Irma: Hurricane Irma, which has been downgraded to a tropical storm, is now at the bend of the Florida panhandle. Although it led to devastation in the Caribbean, the impact on Florida, though significant, has been less than anticipated. It is rapidly turning into a rain event for Georgia and Alabama. Hurricane Jose looks like it is going to circle itself in the Atlantic. We will continue to monitor the storm but, for now, it doesn’t appear to be a threat to the U.S. On average, hurricane season peaks on Sept. 10th, so activity should steadily decline going forward.

China continues to clamp down on cryptocurrencies: China has shut down all virtual trading platforms as it takes steps to rein in cryptocurrencies. These electronic currencies are useful in skirting capital controls, something the Xi administration has been tightening over the past couple of years. Although XBT/USD rates remain elevated, the exchange rate is weakening, probably due to China’s restrictions on the use of cryptocurrencies.

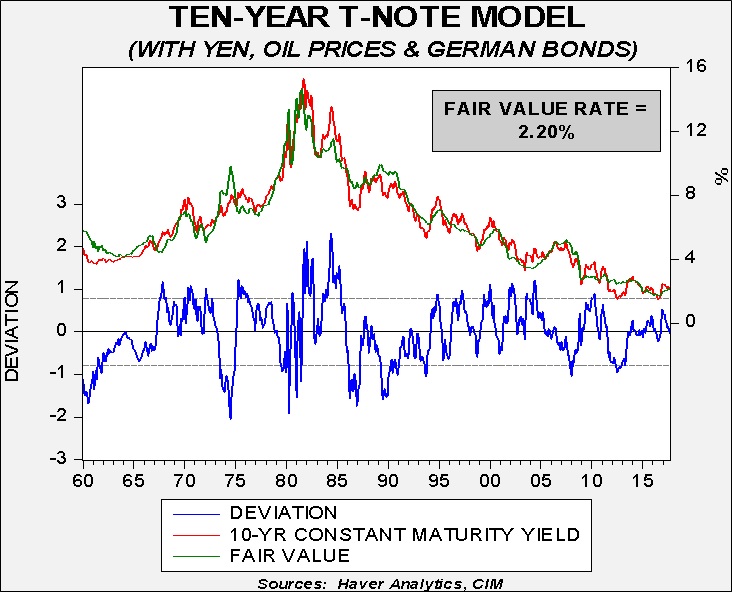

As the FOMC prepares to reduce its balance sheet, it’s a good time to update our views on long-term interest rates. The chart below shows our current estimate of fair value for the 10-year Treasury.

The model uses fed funds, the 15-year moving average of CPI (an inflation expectations proxy), the yen/dollar exchange rate, oil prices and German bond yields. The current yield is on fair value. Assuming the other variables remain steady, the current yield on the 10-year T-note is assuming the FOMC is going to hold rates steady for the foreseeable future.

Is this assumption on the policy rate reasonable? Currently, fed funds futures don’t reach a 50% chance of a rate hike until the June 2018 meeting, and even by next December the odds of a rate increase are only 67%. We expect the Yellen FOMC to use balance sheet contraction to placate the hawks on the committee and thus avoid increases in fed funds until it becomes abundantly clear that inflation is rising.

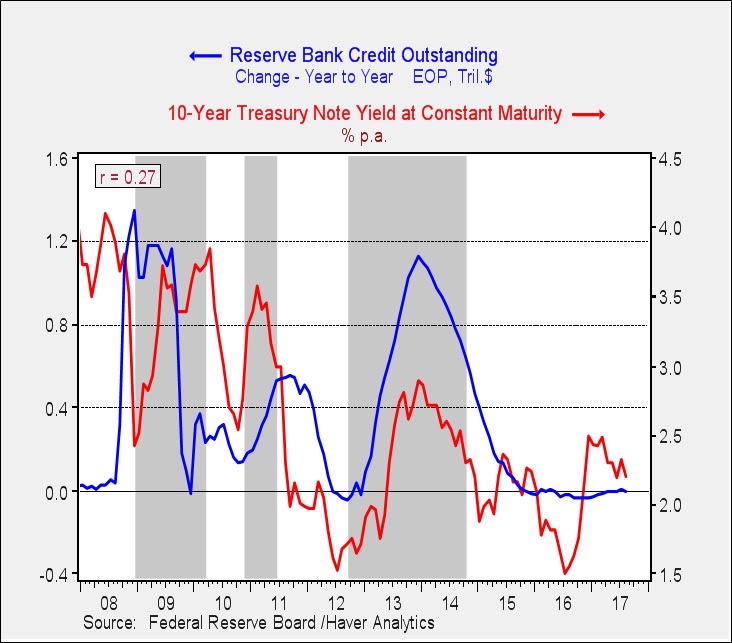

One of the reasons for expanding the Fed’s balance sheet was to lower long-term interest rates. In reality, the evidence of success is mixed.

This chart shows the 10-year T-note yield with the yearly change in the balance sheet. The gray bars show official periods of QE. A zero reading indicates no change in the balance sheet compared to the prior year. Rates fell in QE1, at least initially, although they did rebound as the recession came to an end in mid-2009. However, rates generally rose in QE2 and QE3. Although the Fed was buying longer dated Treasuries, which reduced its supply, it appears the demand may have weakened on fears that QE would trigger inflation. Thus, a case could be made that reducing the balance sheet would have a similar effect and push rates lower.

Our base case is that reducing the balance sheet will have an asymmetric effect on markets; in other words, it won’t have a significant impact on interest rates, unlike the apparent bearish impact that QE2 and QE3 had on long-term interest rates. This is because the FOMC is framing the reduction in the balance sheet as “normalization,” whereas QE was designed to be stimulative. Thus, our analysis suggests that the most important impact of QE was psychological. However, it is possible that QE did more than just boost sentiment; if so, balance sheet normalization could be bullish for long-duration bonds.

[Posted: 9:30 AM EDT] Market action is sluggish this morning; the big story is the continued weakness in the dollar. Here is what we are watching today:

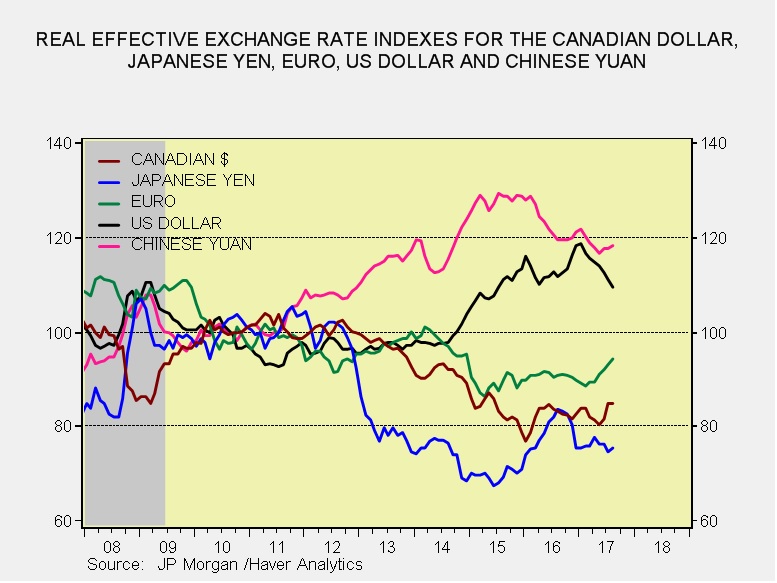

The dollar in perspective: The EUR is threatening $1.210 and the greenback continues to slide despite dovish comments from ECB President Draghi yesterday. The chart below shows the real effective exchange rates for the USD, CAD, EUR, JPY and CNY.

Although the dollar is weakening, it is worth noting that it remains unusually strong against most major currencies except the CNY. If exchange rates are in the process of normalizing, the dollar still has a lot of room to decline. In the foreign economic sector, we note that both China and Germany had disappointing export numbers. Although it’s probably too soon for the dollar’s weakness to have a significant impact on trade, it is possible that we are seeing the early effects. We also note reports that China is becoming “concerned” about currency strength. We remain dollar bears and expect greenback weakness to continue.

Nature bites: Hurricane Irma’s path has shifted westward and is now expected to move through the entire Florida peninsula into Georgia and end up as a depression in Tennessee by next Wednesday. Hurricane Jose looks like it will head into the Atlantic away from the U.S. mainland but is on target to hit Bermuda later next week. Finally, Katia is expected to make landfall near Veracruz tomorrow morning. Adding to Mexico’s woes, the country was hit with a major 8.1 (or, based on some reports, an 8.2) Richter scale earthquake yesterday evening. The epicenter was 60 miles from Mapastepec in the state of Chiapas. This is the most powerful earthquake to hit Mexico in over a century. Tsunami alerts were issued for Ecuador, Vanuatu and New Zealand. All these events will distort economic data for the next two to three quarters.

Warnings of a North Korean missile test: It’s a holiday in North Korea, commemorating the 69th anniversary of the founding of the Democratic People’s Republic of Korea (DPRK). South Korea is reporting that there are signs of another missile test. Worries about tests are boosting the JPY and gold this morning.

More on Washington: Yesterday, we detailed Trump’s triangulation with the Democrats. There are reports the president is working with lawmakers (mostly Democrats) to end debt ceiling votes. Debt ceiling votes began with WWI; before that, each act of government borrowing required an act of Congress. To handle the increased spending for the war, Congress set a limit for debt and allowed debt spending to occur until the limit was reached. Once reached, a new limit would have to be set. Note that the debt limit pays for spending that has already occurred. About the only impact the debt ceiling vote should have is to act as a reminder to lawmakers that debt is rising. However, it has become a tool of the party in opposition to use the leverage of shutting down the government to get its priorities passed. What is interesting about this potential change is that it is being pushed by a GOP president with Democrat Party support against the will of a significant faction of Congressional GOP members. We will see if the president can craft a workable legislative majority of Democrats and “Tuesday Group” Republicans to isolate the Freedom Caucus in order to pass other legislation.

Catalonia: Catalonia has voted to set a referendum on self-determination (or secession) for October 1, 2017. Madrid opposes the vote and will try to prevent it from occurring. It is possible the courts will prevent the referendum from being held, but even if it is held the Spanish government will likely choose to ignore it. There are various separatist movements in Europe. Scotland has been drifting toward leaving the U.K., and Czechoslovakia split into two states in 1993. This is a real problem for the EU; while EU elites try to unify Europe, states within Europe are facing pressure to split even further. This makes European unity an even more distant goal.

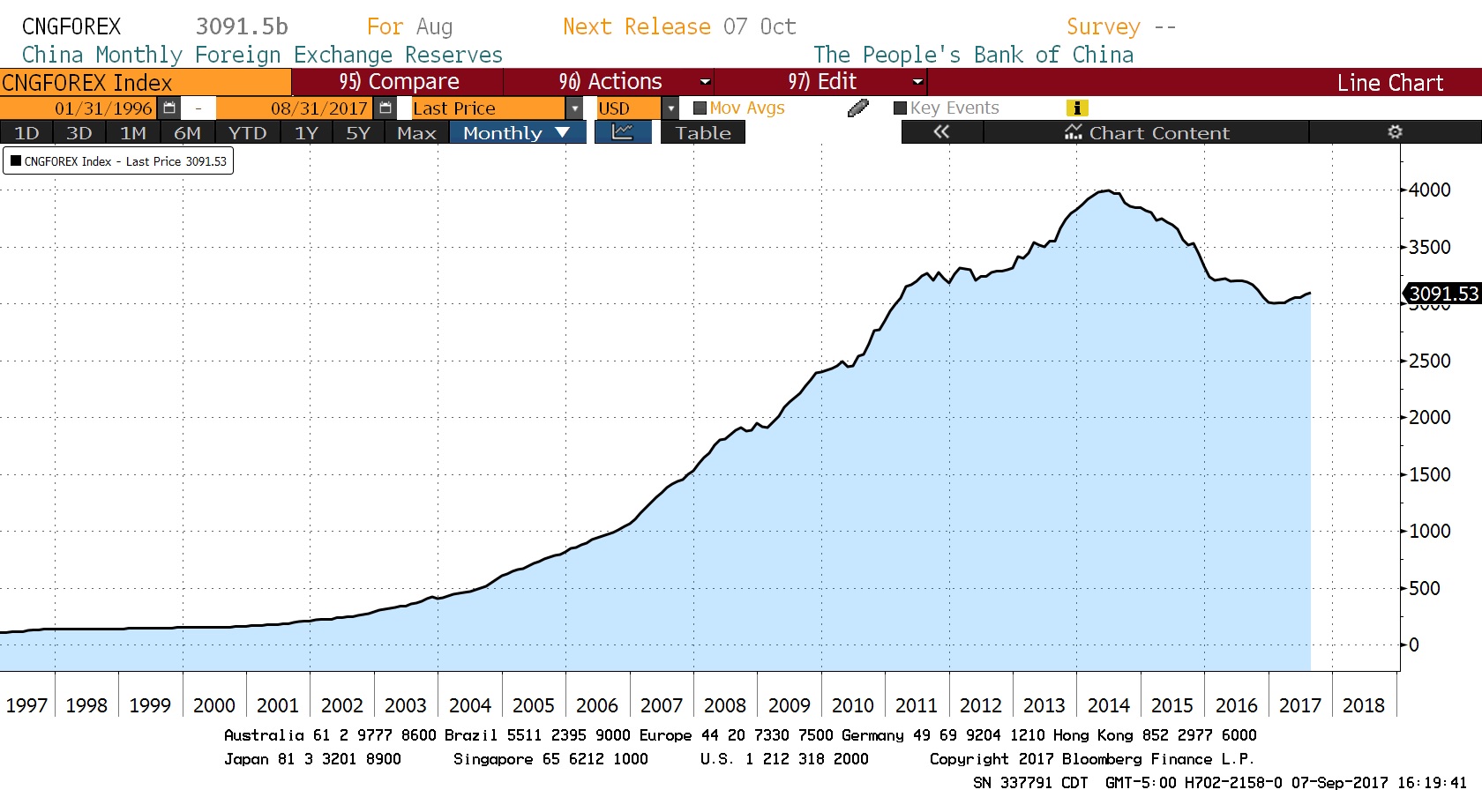

China’s foreign reserves: China’s foreign reserves rose $11 bn to $3.09 trillion.

(Source: Bloomberg)

Although reserves remain well below their 2014 peak, they have recovered from the recent trough of $2.998 trillion. China has taken steps to slow outflows and, thus far, is having some success.

EU rules that nations must take refugees: The EU Court of Justice has ruled that nations must take their assigned quotas of refugees, rejecting actions brought by Slovakia and Hungary.[1] It remains to be seen if these two nations will be forced to take refugees; we actually doubt they will. Many nations in the EU passively rejected their obligations to take migrants coming from the Middle East and Africa. Hungary reacted angrily to the news and Poland may also face retribution from the EU for its rejection of some migrants. This is yet another example of the EU overriding national sovereignty in Europe and will raise political pressure for other nations to follow Britain’s example. That’s why Germany and France are adamant that the U.K. face significant penalties for Brexit to create an example of the cost of leaving the union.

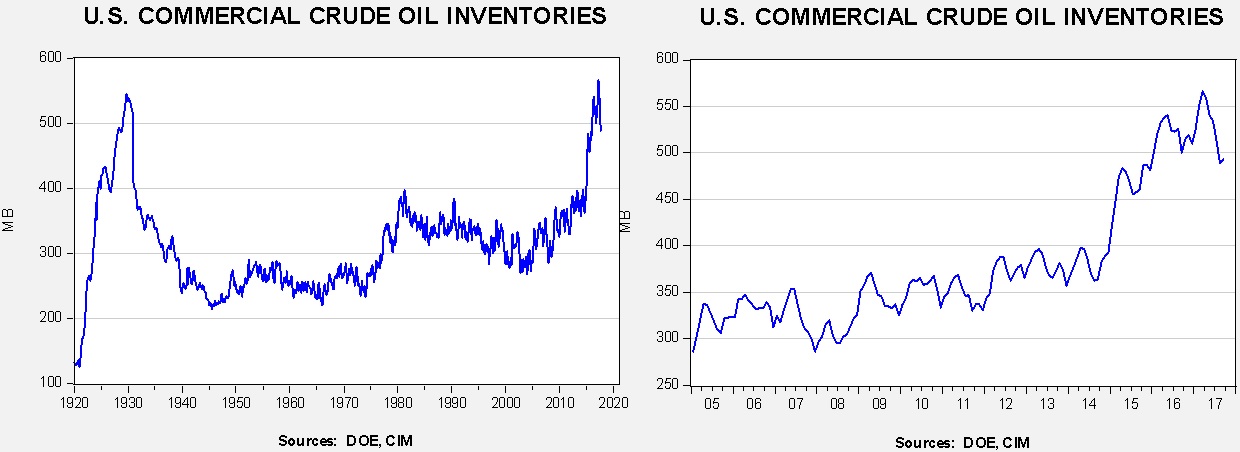

Energy recap: U.S. crude oil inventories rose 4.6 mb compared to market expectations of a 2.5 mb increase.

This chart shows current crude oil inventories, both over the long term and the last decade. We have added the estimated level of lease stocks to maintain the consistency of the data. As the chart shows, inventories remain historically high but they have declined. Hurricane Harvey had a dramatic impact on the energy market data this week; the effects should continue for several more weeks.

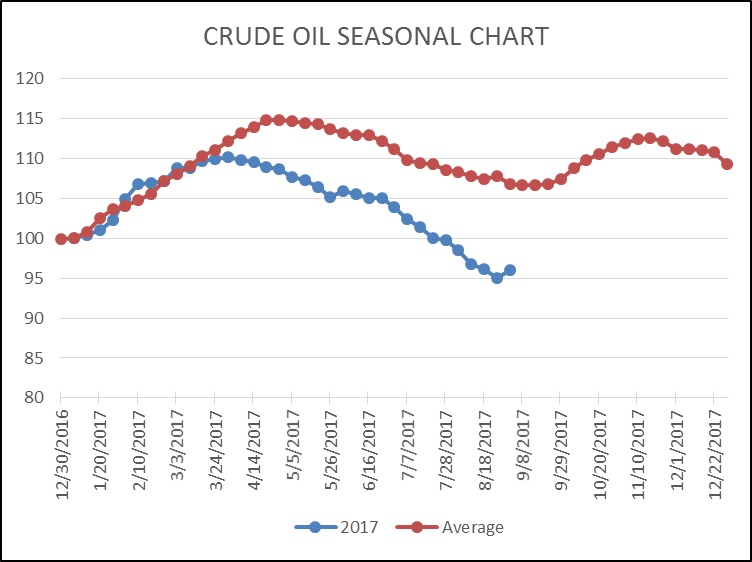

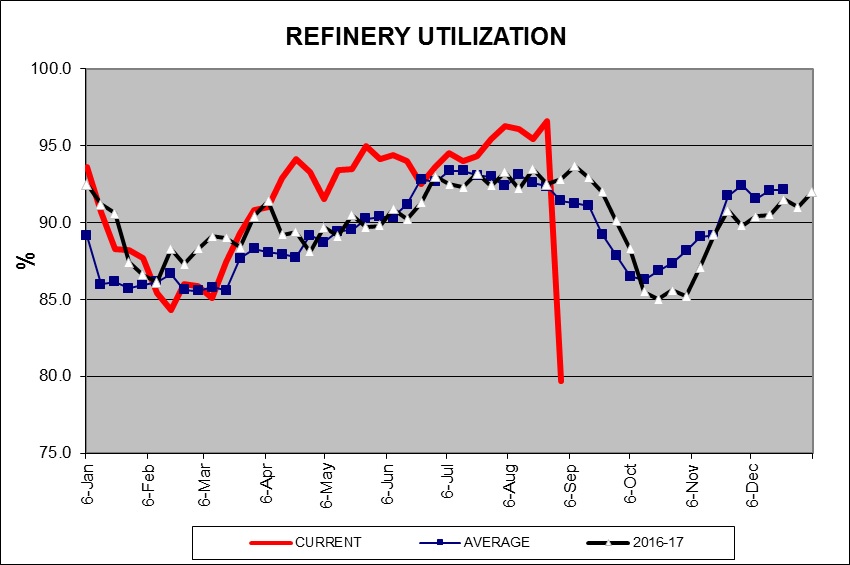

As the seasonal chart below shows, inventories did turn higher this week but they were affected by the aforementioned hurricane. We are probably going to start the inventory rebuild period sooner than normal this year. Although oil imports did decline by nearly 0.9 mbpd and production fell by almost 0.8 mbpd, refinery capacity utilization dropped to 79.7% from 96.6%, or 3.2 mbpd. Media reports suggest that refineries are working hard to restart operations, but it will probably take a couple of months before the industry can achieve pre-Harvey refinery levels.

(Source: DOE, CIM)

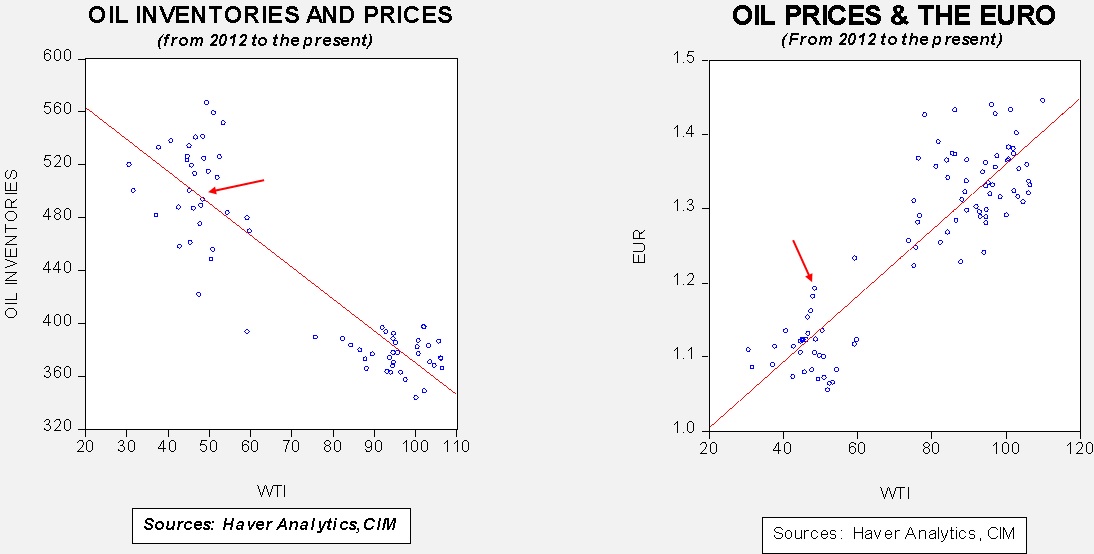

Based on inventories alone, oil prices are undervalued with the fair value price of $53.39. Meanwhile, the EUR/WTI model generates a fair value of $66.68. Together (which is a more sound methodology), fair value is $62.16, meaning that current prices are well below fair value. Although the most bullish factor for oil is currently dollar weakness, the rapid decline in inventory levels is also supportive.

The drop in refinery operations is stunning.

(Source: DOE, CIM)

We do expect operations to recover in the coming weeks. Note that we are close to the onset of the maintenance season. As noted earlier, we do expect to see a recovery in the coming weeks but only to about 85% next month, with a gradual recovery to 90% by winter.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.