Author: Rebekah Stovall

2022 Outlook: Update #2 – The Tails Become Fatter (July 12, 2022)

by Bill O’Grady, Patrick Fearon-Hernandez, CFA, and Mark Keller, CFA | PDF

In our 2022 Outlook: The Year of Fat Tails, we outlined a forecast with a higher likelihood of events outside the norm. To compensate for the unusual level of uncertainty, we promised to provide frequent updates to the forecast. This report is the second of the year. In the most recent update, we offered four scenarios for the path of monetary policy. Since we published that report in February, the world has seen even bigger changes. The war in Ukraine and the subsequent freezing of Russia’s foreign reserve assets have changed the world in a profound manner that will take years to fully determine. Nevertheless, one change we think is permanent is that globalization as we have practiced it since 1990 is over.[1] That change will have serious ramifications on financial markets.

In the past few weeks, market conditions have changed rapidly. It has become nearly impossible to construct a detailed outlook simply because the details are in flux. In order to offer some structure to our current thinking, this will be a short report with price/yield in an effort to at least provide directional guidance.

Key Forecasts:

- 10-Year Treasury: 3.60% to 3.75%, with caveats about the business cycle (see below)

- S&P 500: Range of 4200 to 3400

- Dollar: Bullish for the rest of the year

- Commodities: Very vulnerable to cyclical factors, but secular trend is favorable

[1] For details, see our Bi-Weekly Geopolitical Reports from March 14, March 28, April 25, and May 9. We also recommend our podcast episodes associated with these reports.

Asset Allocation Bi-Weekly – #79 “The ECB Dilemma” (Posted 7/11/22)

Business Cycle Report (June 30, 2022)

by Thomas Wash | PDF

The business cycle has a major impact on financial markets; recessions usually accompany bear markets in equities. The intention of this report is to keep our readers apprised of the potential for recession, updated on a monthly basis. Although it isn’t the final word on our views about recession, it is part of our process in signaling the potential for a downturn.

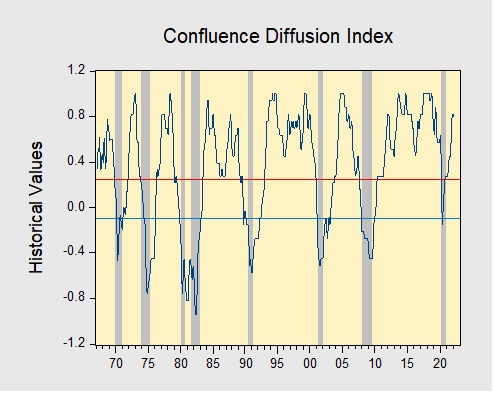

The Confluence Diffusion Index fell for the first time in the expansion. The latest report showed that nine out of 11 benchmarks are in expansion territory. The diffusion index declined from +0.9394 to +0.8789 but remains well above the recession signal of +0.2500.

- Financial indicators were negatively impacted by tighter monetary policy.

- Indicators tied to the goods-producing sector were inconclusive.

- Employment indicators suggests that the labor market remains tight.

The chart above shows the Confluence Diffusion Index. It uses a three-month moving average of 11 leading indicators to track the state of the business cycle. The red line signals when the business cycle is headed toward a contraction, while the blue line signals when the business cycle is in recovery. The diffusion index currently provides about six months of lead time for a contraction and five months of lead time for recovery. Continue reading for an in-depth understanding of how the indicators are performing. At the end of the report, the Glossary of Charts describes each chart and its measures. In addition, a chart title listed in red indicates that the index is signaling recession.

Asset Allocation Bi-Weekly – #78 “The Selling of Austerity” (Posted 6/27/22)

Bi-Weekly Geopolitical Podcast – #12 “The 2022 Mid-Year Geopolitical Outlook” (Posted 6/21/22)

Bi-Weekly Geopolitical Report – The 2022 Mid-Year Geopolitical Outlook (June 21, 2022)

by Bill O’Grady and Patrick Fearon-Hernandez, CFA | PDF

(N.B. Due to the Fourth of July holiday, our next geopolitical report will be published on July 18.)

As is our custom, we update our geopolitical outlook for the remainder of the year as the first half comes to a close. This report is less a series of predictions as it is a list of potential geopolitical issues that we believe will dominate the international landscape for the rest of the year. It is not designed to be exhaustive; instead, it focuses on the “big picture” conditions that we believe will affect policy and markets going forward. They are listed in order of importance.

Issue #1: The Russia-Ukraine War

Issue #2: Xi as China’s President for Life

Issue #3: The Global Food Crisis

Issue #4: Weather Disruptions

Issue #5: Latin American Politics

Issue #6: The U.S. Midterms

Issue #7: Fed Policy and the Dollar

Quick Hits: This section is a roundup of geopolitical issues we are watching that haven’t risen to the level of the concerns described above but should be monitored.