Tag: oil

Asset Allocation Bi-Weekly – #164 “China Cuts Its Energy Imports” (Posted 6/15/26)

Asset Allocation Bi-Weekly – China Cuts Its Energy Imports (June 15, 2026)

by Patrick Fearon-Hernandez, CFA | PDF

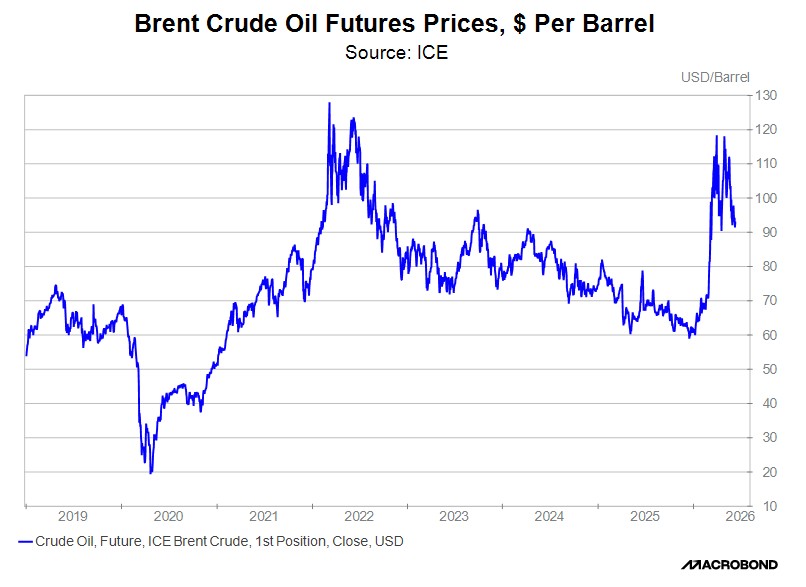

As we’ve noted before, the most immediate economic and financial market risk from the Iran war is the possibility of further price hikes for oil, natural gas, and some other commodities that depend heavily on shipping through the Strait of Hormuz. Because of the war, the strait has now been essentially shut down for more than three months. Global energy and other commodity prices have indeed increased. As shown in the chart below, near Brent crude oil futures prices jumped approximately 50% in the weeks after the war started on February 28. However, the escalation in prices has been relatively contained and prices have even started to fall back recently. That’s despite assurances from economists and energy analysts that prolonged closure of the strait would inevitably lead to further price hikes. In this report, we show that a massive pullback in Chinese energy imports has probably been a key reason why prices haven’t risen as much as feared, at least so far. We also show that the pullback in Chinese energy demand has helped set the stage for recent stock market dynamics.

The unexpected pullback in energy prices was a mystery in recent weeks, especially since official data and anecdotes suggested that the closure of the strait was forcing countries around the world to use up their inventories. For example, the International Energy Agency warned in its May market review: “The world is drawing oil inventories at a record pace as importing countries confront unprecedented disruptions to Middle Eastern supplies.” According to the IEA, global oil stocks had plummeted by almost 250 million barrels since the start of the war, with even steeper declines if stranded stockpiles in the Middle East are excluded. Such inventory depletion would normally be expected to boost prices.

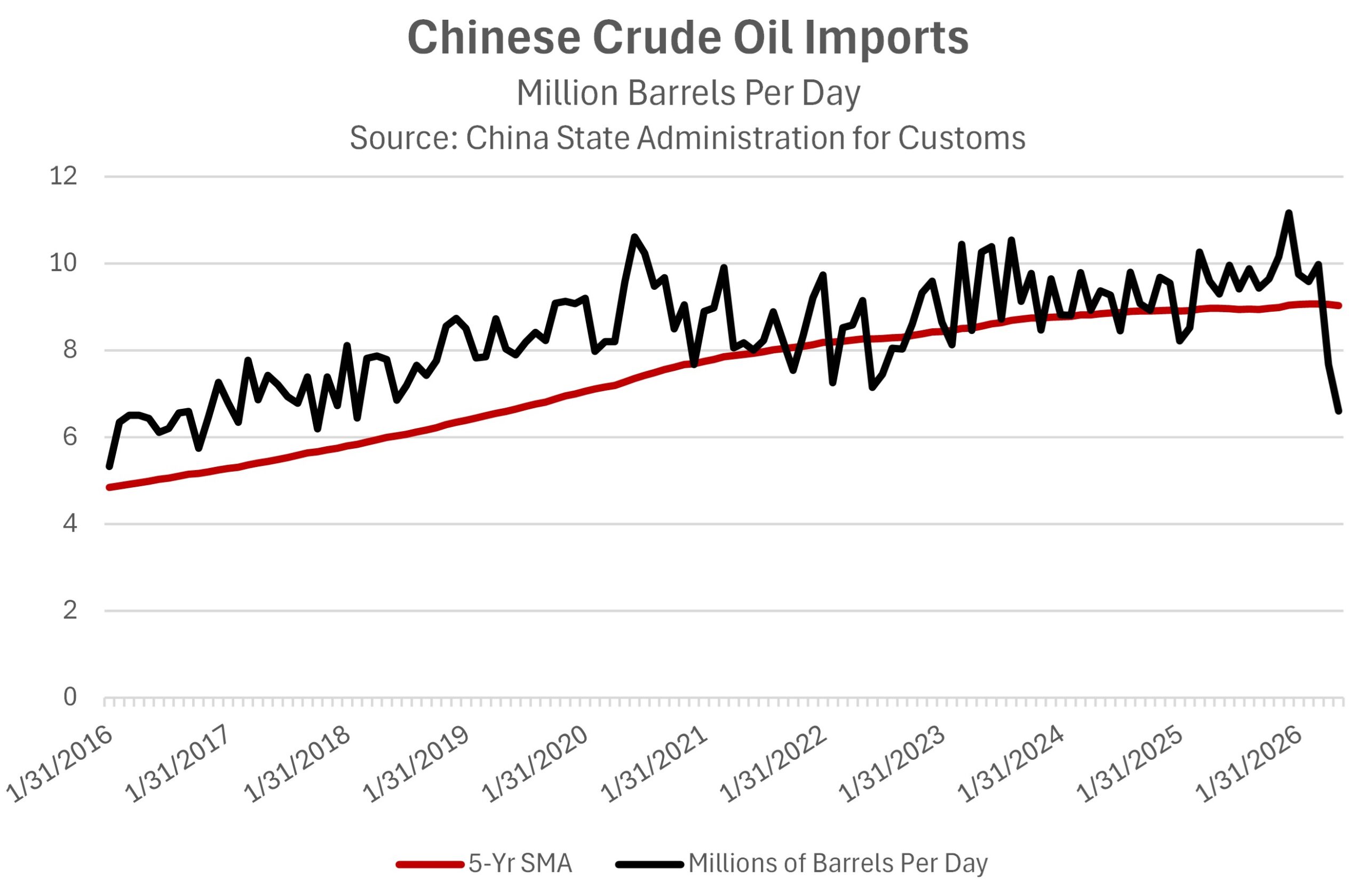

More recent data appears to solve the mystery about why energy prices haven’t risen further and have even fallen back. Recent data shows Chinese oil imports have dropped to approximately 6.6 million barrels per day, down 38% from the average of about 10.6 mbpd in 2025. The drop of about 4.0 mbpd equates to almost 4% of current global oil demand. It could also offset much of the net reduction in global oil shipments through the strait, which analysts estimate to be between 6.0 and 12.0 mbpd.

Chinese energy imports and inventories are notoriously opaque, so these figures are uncertain. Nevertheless, if China really has cut its energy imports as indicated, it would go far toward explaining why energy prices have started to pull back, at least for now. We still believe that a long delay in opening the strait would keep alive the risk of further energy inventory depletion and renewed price spikes. However, China’s apparent disdain for paying elevated prices and its willingness to cut back deliveries is having a salutary impact on global prices and helping calm the world’s financial markets for now.

Going forward, if this trend continues, it will have big implications. For example, China’s ability to forego expensive energy imports helps validate its “all of the above” energy policy, in which it has invested in the full span of possible energy sources, ranging from coal, oil, and natural gas to nuclear, wind, and solar. China is now benefiting from the flexibility it has gained from having such a broad array of energy sources. We also think this situation illustrates how much economic flexibility China has gained from building its enormous strategic reserves of energy and other commodities. Although China won’t reveal the true level of its inventories, outside analysts estimate that they are currently several times bigger than the US’s Strategic Petroleum Reserve. It would be no surprise if governments around the world now take a lesson from China’s approach and try to adopt a similar all-of-the-above energy policy and start rebuilding inventories once the war is over and prices come back down.

For the financial markets, the decline in oil prices wrought by China’s import cuts has probably been a key reason for the recent modest retreat in inflation concerns and in government bond yields. For example, the yield on 10-year Treasury notes fell from about 4.65% in mid-May to about 4.45% at the start of June. We suspect this has encouraged investors to return to the frenzied buying of US large cap technology stocks related to artificial intelligence. It has also arrested investors’ early 2026 rotation toward value stocks. As we noted above, however, the continued war in Iran is likely still depleting energy inventories around the world, including in China. That likely translates into a continued risk of further energy price spikes and rising bond yields in the coming months if the war isn’t resolved.

Don’t miss our accompanying podcasts, available on our website and most podcast platforms: Apple | Spotify

Asset Allocation Bi-Weekly – #163 “The UAE’s Exit From OPEC” (Posted 6/1/26)

Asset Allocation Bi-Weekly – The UAE’s Exit From OPEC (June 1, 2026)

by Bill O’Grady | PDF

On May 1, the United Arab Emirates (UAE) formally exited both the Organization of the Petroleum Exporting Countries (OPEC) and the broader OPEC+ grouping of major oil producers. Such exits are not unheard of. For example, Indonesia suspended its membership in OPEC in 2015. However, Indonesia left the cartel not because it wanted to produce more oil, but because it had become a net oil importer. Qatar left the cartel in 2019, but there were several factors that led to its exit, including the fact that it had become more of a natural gas producer and Saudi Arabia and the UAE had isolated the country over its fostering of the news organization Al Jazeera.

Unlike Indonesia, the UAE has excess oil production capacity that represented about 25% of the cartel’s total. Like Qatar, tensions between Saudi Arabia and the UAE are elevated. The two countries have supported opposing sides in Yemen, for example.

In the immediate term, the UAE’s decision won’t affect the oil markets significantly. That’s because the Strait of Hormuz remains mostly closed. Although the UAE does have a pipeline to the Gulf of Oman, bypassing the strait, it is currently already fully utilized. Thus, the UAE can’t increase its oil output or exports until the US-Israeli war against Iran comes to some sort of resolution. But once that occurs, there will likely be a market impact.

Just what sort and how much of an impact is the focus of this report. To understand why the UAE’s action is important, it’s worth examining the role of cartels in the oil market. Oil supply has a tendency to be “lumpy.” On occasion, large oil fields are discovered and developed. Once these fields begin producing, supply usually increases dramatically. Oil demand is price inelastic, which means that in the short run demand doesn’t immediately react to the increase in supply. A glut of oil occurs, which brings sharply lower prices. Usually, suppliers react to the drop in price by reducing output. However, oil fields have limited flexibility in boosting or cutting output as oftentimes it can be very costly to reopen a well once it has been shut in. Oil is also unique compared to other commodities in that there is an incentive to continue producing once a well is operational because, if a producer were to stop, there would be nothing to prevent other drillers from pulling oil from the same field.[1]

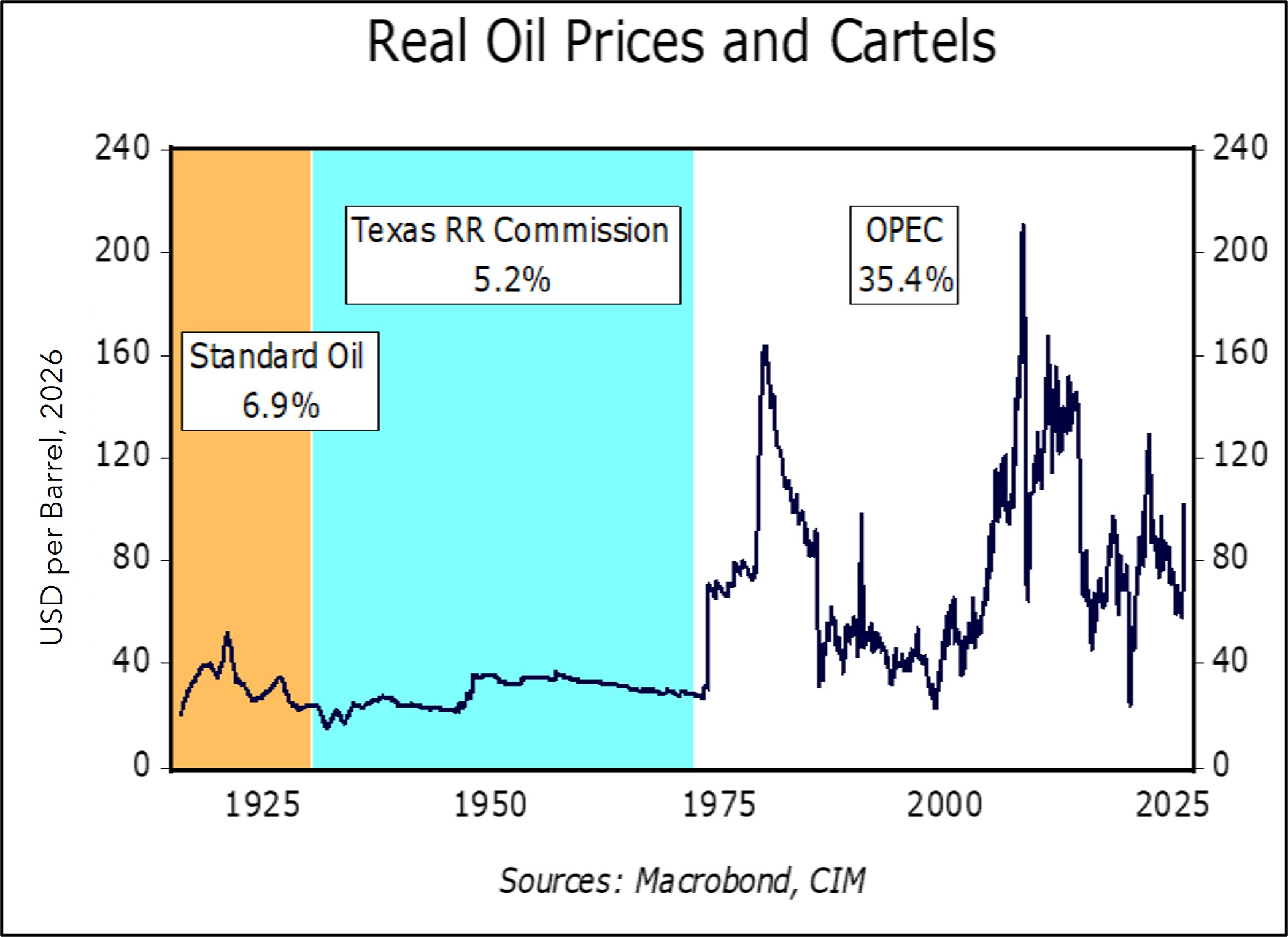

This situation can lead to collapsing prices. When the East Texas Oil Field was discovered during the Great Depression, production soared and caused prices to fall from $1.10 per barrel to $0.15 per barrel. Not only can such a glut be ruinous for producers, but the rush to generate cash flow can lead to overproduction and damaged reservoirs. In this example, the Texas Railroad Commission, which had authority to regulate oil production in the state, used the state militia to enforce production shares. The commission became the de facto cartel manager of the oil market, holding production off the market to keep the price higher than a free market would have generated, while also helping to stabilize prices. The Texas Railroad Commission held this role until 1972, when US consumption matched the state’s production capacity. From this point forward, OPEC became the cartel that manages the oil price.

The chart above shows the inflation-adjusted price of West Texas Intermediate oil, deflated by the US consumer price index. Although Standard Oil was formally broken up in 1911, its successor companies mostly managed production. From 1915 until 1930, the standard deviation of oil prices was 6.9%. The Texas Railroad Commission era shows a standard deviation of 5.2%. Clearly, OPEC has been the least successful cartel in terms of price management, with a standard deviation of 35.4%. But, as the chart shows, it has been successful at managing prices at times. For example, from 1986 through 1999, the standard deviation was 10.0%, even during the Gulf War.

Nevertheless, OPEC has struggled to manage prices in this century, with a standard deviation of 24.2%. First, it was unable to contain prices during China’s emergence after joining the WTO in 2001. It also struggled to manage the market following the advent of US shale oil.

The decision by the UAE to leave the cartel will likely further complicate price management. As we noted above, the decision doesn’t matter much while the Strait of Hormuz is blocked. However, once it reopens and supply chains are restored, the UAE’s production will be a bearish factor for oil prices. We expect Saudi Arabia will attempt to maintain price stability for a time, given the country’s history of cutting its output to preserve higher prices. But, as we saw in 1985 and again in 1999, the kingdom eventually decided that it was tired of providing support for “free riders” and punished overproduction by flooding the market with oil, and we would anticipate a similar outcome here. We don’t know when this moment will occur, but traders will have to factor this possibility into prices.

Complicating matters further is the closure of the Strait of Hormuz. Oil consumers now know that this region of the world is an unreliable supplier and will undoubtedly take steps to diversify energy sources moving forward. China’s ability to manage through an “all of the above” strategy will likely support alternative energy sources, such as coal, wind, solar, nuclear, et al. The uncertainty of oil supplies tends to depress demand over time. Therefore, even before the UAE’s decision, oil prices would have eventually had to decline enough to offset the uncertainty surrounding future supply. A smaller OPEC cartel will increase the likelihood of lower prices…eventually.

[1] As highlighted in the “milkshake” scene in the movie There Will Be Blood (1:34).

Don’t miss our accompanying podcasts, available on our website and most podcast platforms: Apple | Spotify

Asset Allocation Bi-Weekly – The Strategic Petroleum Reserve: A Primer (March 30, 2026)

by Bill O’Grady | PDF

On March 11, the International Energy Agency announced a coordinated draw of 400 million barrels from the Strategic Petroleum Reserve (SPR) System maintained by the organization’s member countries. Understanding the reasoning behind this decision requires an examination of the economics of inventory. This analysis will help the reader understand that SPRs are not just protective stockpiles but have a key psychological element as well.

In textbook economics, inventory doesn’t exist. Theory assumes a frictionless world, which means that production and consumption are continuous functions, and production meets consumption instantaneously. Obviously, this condition doesn’t reflect the real world. The classic example is agriculture: production is seasonal, so there are periods when supply is scarce (between harvests) and other periods when supply is abundant (right after the harvest). Inventory smooths out the supply to better meet demand.

Most goods markets have inventory, and many of them have inventory cycles driven either by production or consumption. Analysts usually attempt to determine what is a “normal” inventory for a given time of the year. Once this norm is established, inventory changes can signal the balance of supply and demand in a market. If inventory is below normal, it likely signals a tight market, which would be expected to bring higher prices. Higher prices encourage producers to make more and consumers to consume less, and the opposite is true when inventory is above normal. This pattern suggests that, under normal conditions, we would expect to see an inverse correlation between inventory and price. In general, high inventory levels should be bearish, while low inventory levels should be bullish.

If the correlation between inventory and price is positive, it suggests hoarding. Hoarding occurs when consumers fear that a good will become unavailable. In response, consumers attempt to build their personal inventory by purchasing more than they would usually hold. If markets are functioning normally, hoarding is irrational. Seeing higher prices, producers will boost output, which should provide enough product to ease shortage concerns. However, hoarding doesn’t usually occur in a vacuum. It typically happens in response to an exogenous shock, like a weather event, war, pandemic, etc. The problem with hoarding is that, at the micro level, it’s a perfectly reasonable response that can make the market situation worse at the macro level. Hoarding is a prime example of the “error of composition.”[1]

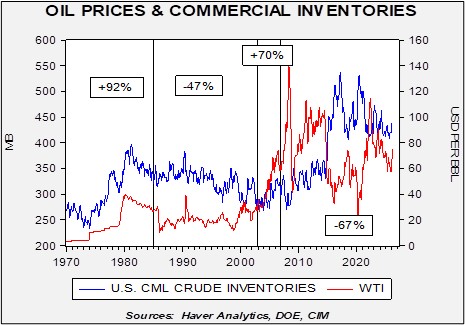

The chart below shows US commercial crude oil inventories and the West Texas Intermediate oil price. We have divided the graph into periods where the correlation between oil prices and inventories flipped. Note that in the 1970s, oil prices and inventories were highly positively correlated, reflecting hoarding. The correlation became positive again from 2003 through 2006 at the end of the China-driven commodity bull market early in this century. The rest of the time, the correlation has been negative, which is what one would expect under normal market conditions.

The thinking behind the creation of SPRs was to reduce the tendency to hoard. If a consumer is worried about physical scarcity (as opposed to high prices), then there is an incentive to stockpile. During the gas lines crisis of the 1970s in the US, it was not uncommon for drivers to wait in line to buy merely a gallon or two of gasoline “just in case.” Strategic reserves serve the purpose of ensuring the availability of supply, which should dampen the desire to hoard.

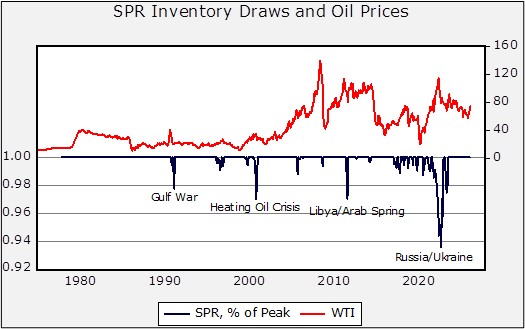

The chart below shows US SPR draws and oil prices. To measure draws, we compare oil prices to the previous month’s peak in the SPR. There are numerous small draws shown as Congress sometimes uses the SPR to fill budget gaps. Often, the SPR oil is “swapped” during supply outages and then usually replaced a month or two later. The major draws, which tend to bring down prices, are noted on the chart.

In our view, the recently announced draw should stabilize oil prices — at 400 million barrels, it’s the largest combined draw in history. However, it’s important to note that the Strait of Hormuz outage amounts to about 20 million barrels per day, meaning this draw could only offset about 20 days of losses. So, we view it as an action that should prevent spikes in oil prices, but it likely won’t be enough to bring down prices sharply without a reopening of the strait.

As our analysis on hoarding shows, if the nations releasing SPR oil keep it within their borders, prices may actually rise. To prevent that, the taxpayers who funded the strategic storage must be willing to “share” with nations that did not. For investors, this is the key factor to monitor. How will we know if the announced SPR release isn’t working? If we see commercial oil inventory and prices rise simultaneously.

[1] A logical fallacy that assumes what is true for an individual is also true for the whole.

Don’t miss our accompanying podcasts, available on our website and most podcast platforms: Apple | Spotify

Asset Allocation Bi-Weekly – #159 “The Strategic Petroleum Reserve: A Primer” (Posted 3/30/26)

Bi-Weekly Geopolitical Podcast – #58 “Syrian Surprise – Implications of a Sudden Regime Change” (Posted 1/13/25)

Bi-Weekly Geopolitical Report – Syrian Surprise: Implications of a Sudden Regime Change (January 13, 2025)

by Daniel Ortwerth, CFA | PDF

On December 8, 2024, the world awoke to a dramatically changed order in the Middle East. Seemingly out of nowhere, the Assad family regime, which had stood for 54 years and withstood 13 years of civil war, fell to a sudden rebel onslaught. What seemingly began only 11 days prior as an isolated effort by a rebel group in the northwest corner of Syria quickly became an unstoppable advance through the country’s major population centers and culminated in the overthrow of the regime, the flight of its leader into exile, and the ascendancy of a new governing authority. Since the new power in Damascus has entirely different loyalties than the regime it deposed, this development throws the regional balance of power into question, with geopolitical and global investment implications.

This report begins with a review of Syrian history and continues with an overview of the pertinent facts of 21st century Syria and the surprise rebel initiative that led to the change of power. Upon this backdrop, we discuss the interests and priorities of the significant regional and global players who have a stake in the future of Syria. As always, we conclude with implications for investors.