(NB: Due to the Thanksgiving holiday, the next report will be published on December 6.)

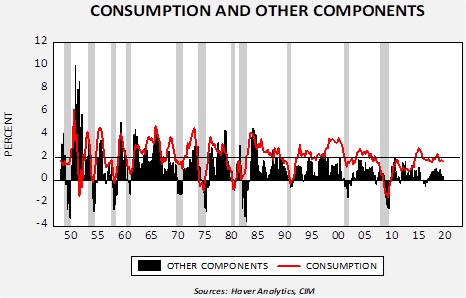

The health of the consumer is critical to the future path of economic growth. For the most part, consumption is accounting for most of the growth in the economy.

This chart shows the four-quarter average of the contribution to real GDP from consumption compared to the net of the contribution from government, investment and net exports. Over recent business cycles, the contribution outside of consumption has diminished. The other sign from the data is that the risk of recession rises when consumption’s contribution declines below 2%.

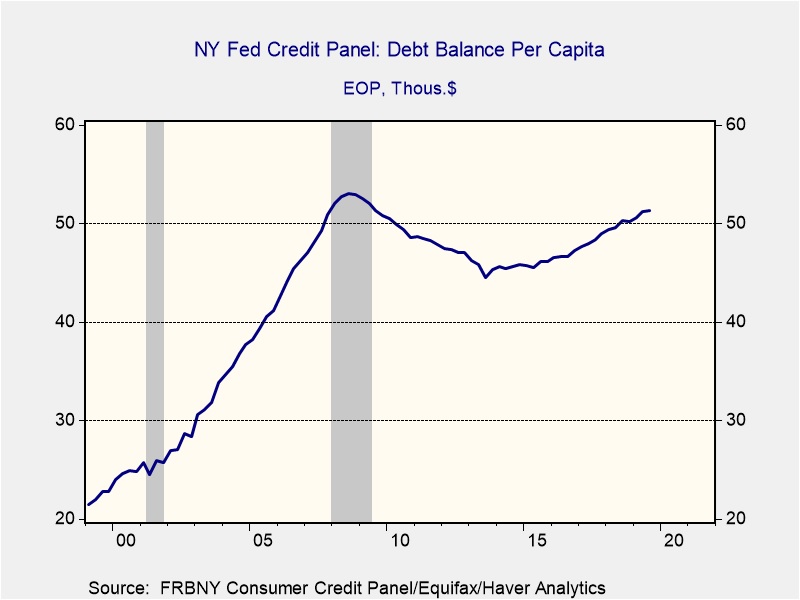

Household debt plays a role in consumption. The New York FRB has a data series on consumer debt that has just been recently updated. The balance of household debt is now $13.95 trillion, a new record high. However, on a per capita basis, we remain below the previous record.

From its peak of $53.0k in Q3 2008, this measure of debt declined to $44.5k in Q3 2013. Since then, it has gradually increased. However, it has not reached levels that would trigger significant concern. In the last expansion, per capita debt growth was 10.9%; in this expansion the average growth is -0.4%.

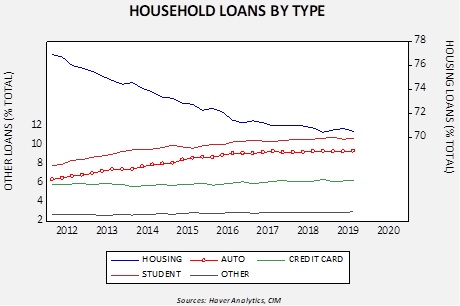

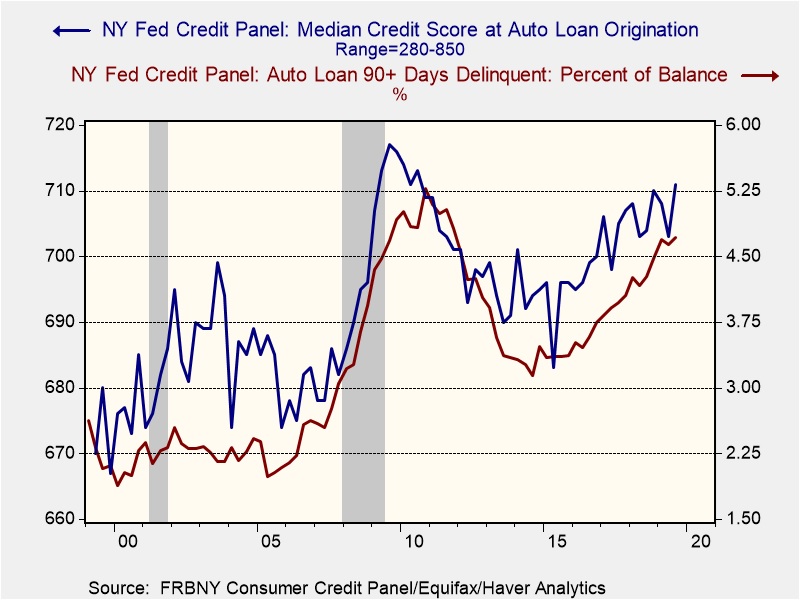

As a percentage of the total, housing debt has been declining relative to auto and student loans.

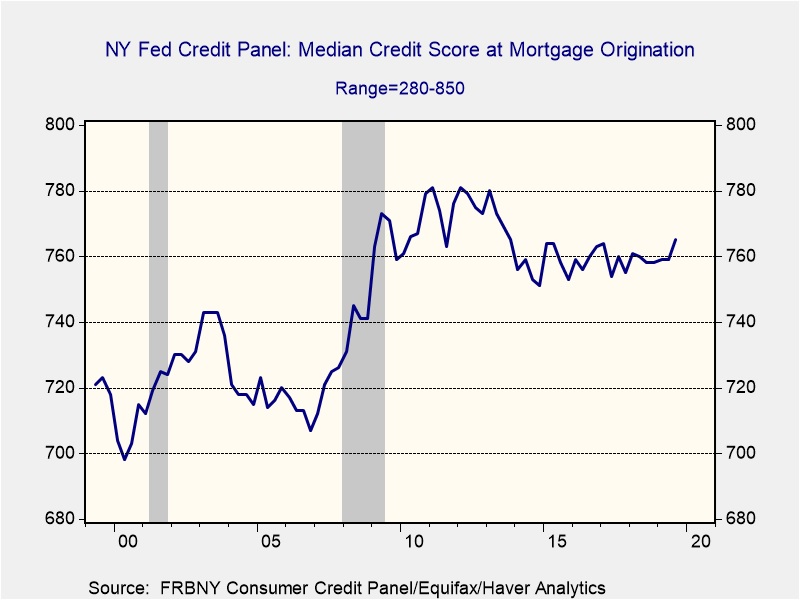

In 2012, housing represented about 76.9% of outstanding household loans; it now stands at 70.5%. Both student and auto loans have increased. The median credit score for mortgages is a rather strong 763.

Auto loans is a bit lower, at 710, but credit quality has been improving, mostly a reflection of higher delinquencies. Lenders appear to be increasing their caution.

Overall, the data suggests that the areas of greatest concern are auto and student loans; lenders do appear to be addressing the auto loan issue by becoming more selective in granting credit. Student loans, which have a 90+-day delinquency rate of around 10% since 2012, are ultimately a public policy issue, but until this issue is resolved these loans will have an adverse impact on spending. If there is going to be a financial crisis, this data would suggest it probably won’t come from the household sector.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EST] Episode #3 of our Confluence of Ideas podcast is now available.

Happy Friday! It’s a slow news day this morning. Financial markets are rather calm. We cover the global PMI data in the foreign section. Here is what caught our attention this morning:

Watching Corbyn: For the upcoming U.K. elections, Labour leader Corbyn unveiled his party’s policy manifesto. The policy proposals are a clear rejection of Tony Blair (and Bill Clinton’s) “third way” of center-left politics. Instead, it is being billed as a return to the 1970s; we would suggest that characterization isn’t radical enough. It would be more like the massive shift in the U.K. economy that occurred after WWII, with sweeping nationalization and much higher taxes on upper income earners. Sometimes the U.K. acts as a leading, or perhaps coincident, indicator of U.S. political trends; for example, Margaret Thatcher preceded Ronald Reagan by about a year and Tony Blair was a contemporary of Bill Clinton. The Brexit issue reflects rising populism in the U.S. One of the key questions for the 2020 election is whether a center-left or a populist-left candidate represents stronger opposition to a right-wing populist incumbent. If Corbyn does poorly in next month’s election, the Democratic Party leadership might conclude that the populist wing isn’t the right path to take. Thus, there may be an imbedded lesson for our election in the upcoming British poll.

China trade: We are hearing both Presidents Xi and Trump saying that a trade deal remains possible. Given the length of time that this phase one deal has taken, we are worried that we may see a “buy rumor, sell fact” action in the markets even if a deal is made.

A cautionary tale: Although the U.S. health care system is littered with flaws, the tort bar, for all its extremes, does act as a threat to poor medical practices. Under a single payer system, we doubt the government would tolerate such annoyances. A report from the U.K. suggests that a single payer system has its own issues as well.

Hong Kong: The territory will hold local council elections on Sunday. These are usually minor affairs with the focus on local issues (noise control, rubbish pickup, etc.) Currently, these seats are dominated by mainstream supporters of the mainland. However, the pro-democracy movement is fielding a large number of candidates, turning the vote into a referendum of sorts on the protest movement. The president has not signed the recent Hong Kong bill. Tokyo and Singapore are trying to lure Hong Kong’s finance industry away from China.

ECB:Christine Legarde gave her first policy speech yesterday and pressed governments to boost investment spending. In some respects, this is an old tune. Finding profitable public, or private investment is difficult. It may be harder to find public investments in a developed economy that actually lifts productivity. However, there is an important embedded signal in this speech; monetary policy may be exhausted and if further stimulus is going to occur, it probably has to come from the fiscal side. Moving the Eurozone this direction will take all of Legarde’s ample political skills. Germany continues to view balanced budgets as a moral imperative and until this view changes, getting increased fiscal spending will be next to impossible.

A tariff twist: There has been much written about who pays the tariffs. The economic term for who pays the tax is called “incidence.” Often, it’s not as simple as it seems. For example, most people believe the payroll tax is shared between the worker and the firm but that’s not usually the case. Most of the time, the worker pays both sides, not just what he sees on his pay stub, because the firm reduces his pay for part, or all the employer portion of the tax depending on labor market conditions. In other words, in the absence of the payroll tax, wages would likely be higher. For tariffs, the incidence is even more difficult to discern. If the foreign firm is determined to maintain market share and faces a price inelastic demand curve, the foreign firm reduces the tariffed item’s price to offset the tax. However, if the foreign firm faces a price elastic demand curve, the tariff may be absorbed by domestic producers, or in higher prices to consumers.

Central bank independence: Judy Shelton, a nominee for Fed Governor, is suggesting that central bank independence isn’t sacrosanct. Although this stance is a reversal from commonly held beliefs since the 1970s, in fact, central bank independence does ebb and flow. During the 1930s into the early 1950s, the Fed got its rate policy from the Treasury to facilitate the latter’s borrowing program. If we are heading into a period of reflation, weakening central bank independence is an element to that project. So, Shelton’s nomination to the Fed should not come as a surprise.

Global financial markets: Managers at the massive hedge fund Bridgewater Associates have reportedly bought $1.5 billion worth of puts on the S&P 500 and Euro Stoxx 50, in a bet that the U.S. and/or European markets could fall significantly by next March. Our analysis suggests there is indeed a heightened risk of recession later in 2020. If so, we think that would imply the equity markets might start falling around mid-year.

Colombia: Hundreds of thousands of demonstrators marched through Bogotá and other cities yesterday to protest corruption, insecurity, and inequality, but it appears the government was able to keep them better controlled and less violent than the protests in places like Hong Kong and Chile. The youthful protests around the world are acting like a contagion, with activity in one country inspiring demonstrations elsewhere, but Colombia’s experience suggests governments could minimize the impact through good preparation and tightened security ahead of the protests. For example, the Colombian government mobilized 170,000 military and police personnel ahead of the demonstrations, shut its border, and imposed a curfew in at least one major city.

Bolivia: To end the political violence since former President Morales was forced from office for allegedly rigging his October 20 reelection, interim President Añez presented a draft law to annul that vote, call a new election, and name a new electoral board to oversee it. The actual date of the new election would depend on when the bill is passed into law.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EST] Episode #3 of our Confluence of Ideas podcast is now available.

Financial markets this morning can best be described as “becalmed.” Not much is moving We cover the Fed minutes and the recent gyrations with trade. OECD downgrades 2020 growth. Yesterday’s energy data is recapped. Here are the details.

Fed minutes: The minutes had no discernible impact on financial markets. Here are the general takeaways from the report:

Policymakers are signaling that they think the current policy rate is appropriate. At the same time, there is ample evidence to suggest that the preponderance of risks is to the downside. Thus, we can conclude that the next move is most likely for lower, not higher rates.

Even this rate cut was not easy. Although the majority apparently supported it, there were two official dissents. Additionally, seven presidents don’t vote each year. The minutes suggested that at least a couple of members vied this cut as a “close call.” This adds to evidence that additional reductions in rates will require clear evidence of slowing.

One of the unknowns about the labor market is if the modest slowdown in payroll growth is due to a weakening economy, or the natural consequence of near full employment. The minutes suggested the members are leaning toward the latter explanation. If they are wrong, and the slowing is an early sign of weakness, the odds of a policy mistake are increased.

In the review of recent money market turmoil, it isn’t obvious if the Fed really understands what has occurred. Perhaps the best analysis of this issue can be found here. If Zoltan Pozsar is correct, the Fed really hasn’t solved the problem. We might see a repeat of the September problem at year’s end. One issue is that the discount window, which allows banks to borrow directly from the Fed if they are short on reserves, is no longer used on fears of creating reputational risk. This development is forcing banks to hold excess reserves.

In discussions, the FOMC is cool to negative nominal rates, instead planning on forward guidance and balance sheet expansion if the zero lower bound is touched again. Our concern is that the Fed’s apparent “success” with these tools in the past has led them to overconfidence.

So, overall, probably not more rate cuts this year, but the odds of a hike are very low.

Here is a technical assessment of the potential decline:

(Source: Bloomberg)

This is the S&P 500 from the summer of 2017. With a couple of violations, the index has moved in a broad upsloping channel since the initial peak after the tax cut passed. Clearly, last year there was a serious violation of the channel; another one occurred recently. If the trade talks are doomed, a pullback to the September lows is likely, or a bit more than 10% from the recent high. Falling to the lower line of the channel would put the index around 2800. That’s probably a reasonable set of parameters for the market over this issue.

Here are the most recent developments on trade. There is breaking news that the U.S. may not implement tariffs scheduled for Dec. 15th if the Phase I talks fail. The White House has not confirmed this report. This decision, if true, would suggest that the White House realizes that adding tariffs to all Chinese imports will affect consumer goods and may be rather unpopular. If so, this might mean that the last leg of tariffs may never be implemented and thus tariffs have become a less potent threat. China has invited the U.S. negotiating team to Beijing for new talks; the U.S. is reluctant to go without clear evidence China is willing to meet U.S. demands. President Trump has blamed China for the lack of progress on trade. China is promoting continued talks. In a warning, former Secretary of State Kissinger warned that if the U.S./China trade conflict isn’t brought under control, the potential exists for it to spiral into a scenario similar to WWI; we would agree with this assessment.

On Dec. 10th, the WTO appeals courts will stop functioning due to the lack of judges. The U.S. has prevented new appointments, effectively ending the WTO’s ability to resolve trade disputes. If the WTO collapses, it will likely mark the end of the post-WWII (but especially the post-Cold War variant) globalization.

Global growth: The OECD is warning that the world is heading toward a low growth rut due to trade disputes and low investment rates. It is projecting 2.9% GDP growth for the world in 2020; any level under 3% is generally considered a recession.

Japan: Prime Minister Abe’s push to amend the country’s pacifist constitution to allow a stronger military hit a roadblock, as parliament members agreed to cancel a discussion of a required change in Japan’s referendum law. With only two weeks left in the parliamentary session, the move basically prevents any movement on the issue for the rest of the year.

Canada: Prime Minister Trudeau has announced a significant shake-up to his cabinet. Most important, Foreign Affairs Minister Chrystia Freeland, who led the country’s negotiating team during the recent U.S.-Mexico-Canada trade deal, has been elevated to the role of deputy prime minister in charge of provincial and territorial affairs. That could help Trudeau overcome the nascent separatist sentiment in Alberta and Saskatchewan that has developed in response to his national carbon tax and other environmentalist policies. By developing Freeland’s expertise in domestic issues, it should also help set her up for a run at the prime minister’s role in the future.

Colombia: While political protests have burgeoned in Chile, Bolivia, and Ecuador, and as political and economic problems have intensified in Venezuela, Brazil, and Argentina, it seemed Colombia was a bastion of stability. Today, however, unions and anti-government protestors have launched a massive national strike to protest some of the same issues that have caused unrest elsewhere in South America, i.e., corruption, inequality, and political rigidity. The spread of the unrest to Colombia, and the potential for a violent government response will be negative for South American assets going forward.

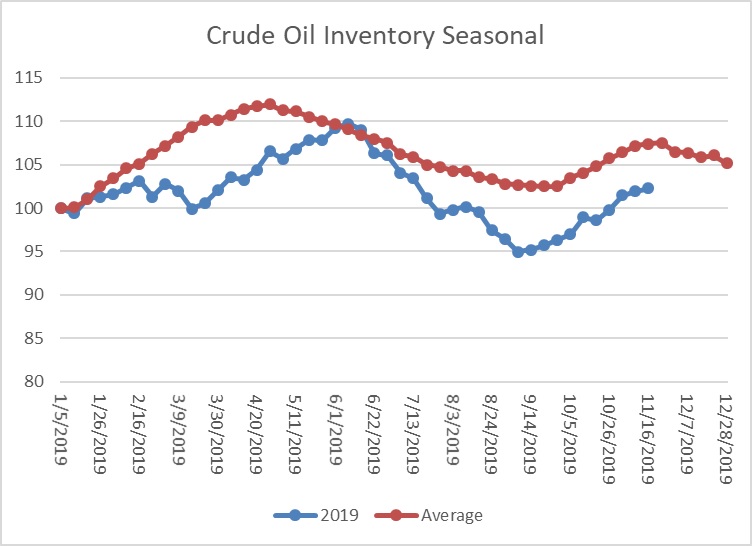

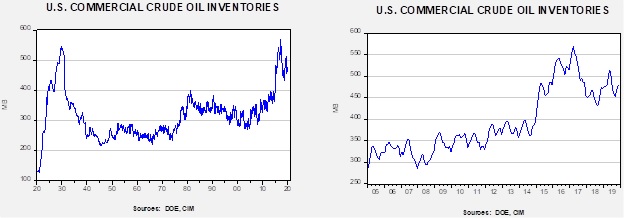

Energy update: Crude oil inventories rose 1.4 mb compared to an expected build of 1.5 mb.

In the details, U.S. crude oil production is unchanged at 12.8 mbpd. Exports rose 0.4 mbpd while imports rose 0.2 mbpd. The rise in stockpiles was mostly in line with expectations.

(Sources: DOE, CIM)

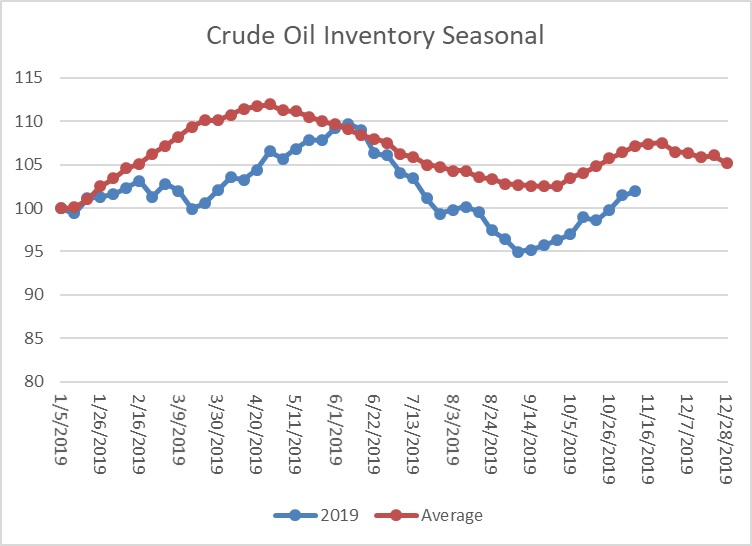

This chart shows the annual seasonal pattern for crude oil inventories. We are approaching the end of the autumn build season, which implies we will see a modest drop during the month of December before the usual seasonal rise in Q1.

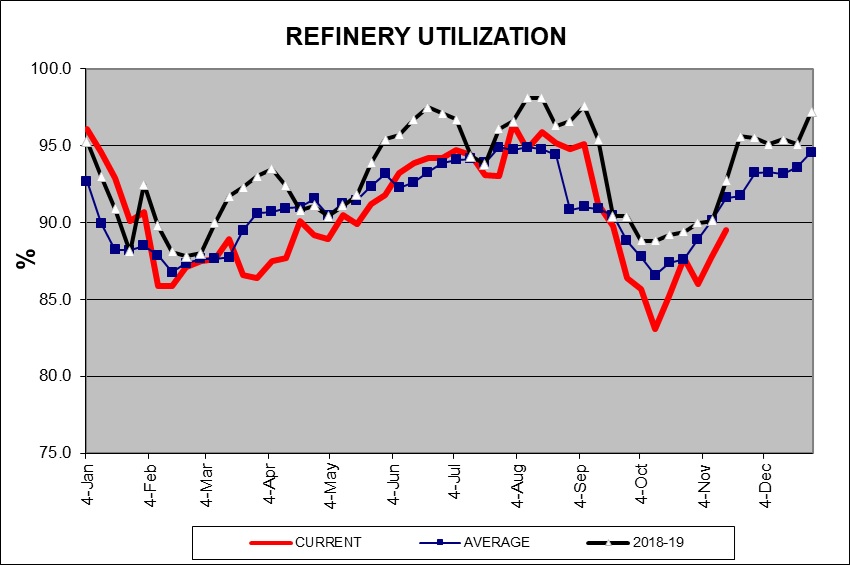

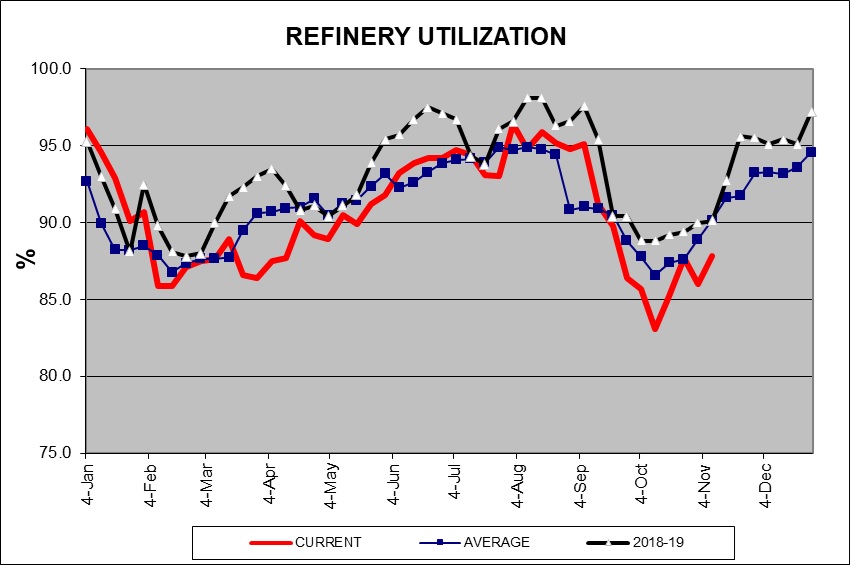

We continue to monitor the autumn refinery maintenance season.

(Sources: DOE, CIM)

This week’s rise is normal, but utilization remains below average. Run rates should continue to rise into the new year.

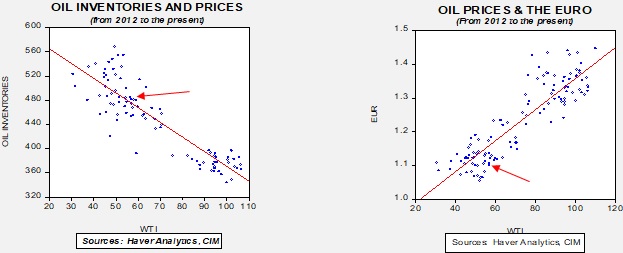

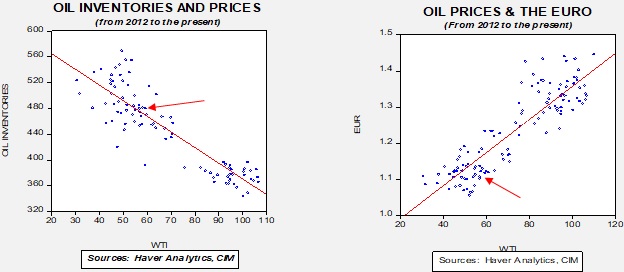

Based on our oil inventory/price model, fair value is $56.79; using the euro/price model, fair value is $49.14. The combined model, a broader analysis of the oil price, generates a fair value of $51.12. We are seeing the divergence between dollar and oil inventories narrow as the dollar weakens and oil stocks rise. We expect the Saudi IPO process to support oil and any positive news on the trade front would be supportive for oil prices as well.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EST] Episode #3 of our Confluence of Ideas podcast is now available.

It’s a risk-off morning at mid-week. There are three items of note in the overnight news. First, the Senate has passed the Hong Kong democracy bill. Second, the debate between Johnson and Corbyn was mostly a draw. Third, the Fed minutes are out today. Here are the details.

Gaming out the Hong Kong democracy bill: The Senate, in a rare example of bipartisanship, voted unanimously to pass its version of the Hong Kong democracy bill. The bill would require the secretary of state to annually certify that Hong Kong remained sufficiently independent to warrant its special status as a global financial hub. It would also allow the president to place sanctions on individuals who have been deemed to have suppressed human rights in Hong Kong. A similar set of legislation passed the House unanimously in October. There are some differences between the two versions, but with such strong support in the legislature, it is highly likely that a single version will emerge soon from the conference committee. China has already condemned the action and is urging the White House to veto the bill.

This legislation complicates the trade situation with China. Even with a veto, given the strong support in both houses, the president would be forced to spend prodigious levels of political capital to prevent an override. Although China might view a heroic but failed effort as good enough to maintain progress on trade, more likely the Xi regime will view the bill as an affront to its sovereignty and that would be enough to end negotiations. In addition, the president has to be careful with overt support for China. As we have noted before, Bill Clinton used the Bush administration’s reaction to Tiananmen Square against the president in the 1992 campaign. Protecting China would be used against the president in the 2020 campaign. On the other hand, if phase one of the trade deal fails, financial markets will not take it well and that will also be a negative for the upcoming election. President Trump reiterated that he will raise tariffs if China doesn’t make a deal with the U.S., suggesting he believes his bargaining position is stronger than Beijing’s. At the same time, China continues to press for a rollback in tariffs, which may signal that Beijing believes it holds the upper hand. Equities have made new highs, in part, based on expectations of a modest trade agreement. If the deal fails, it would be reasonable to expect at least a return to the low end of the channel the S&P has been trading in for nearly the past two years.

In other China news, Beijing is arguing that the recent Hong Kong court decision to overrule the government’s ban on protestor masks was illegal. Essentially, the PRC is arguing that such decisions are for Beijing to make. Such heavy handed responses make it difficult for the U.S. to argue that Hong Kong deserves its special status.

The Fed: The Fed will release the minutes of its most recent meeting. Although the notes are heavily sanitized, they should offer some insight into the level of dissention on the FOMC. In 2024, we will get the full transcripts of this year’s meetings. It will be fascinating to see just how divided this Fed is. The higher the level of dissention, the greater the hurdle to future easing.

The PBOC: China’s banks are following the PBOC’s lead; the latter cut the Loan Prime Rate earlier this week and banks are cutting lending rates by a similar amount. All indications are that the PBOC will become more aggressive in the coming months to offset a decelerating economy.

The rise of MMT: As we have hinted in the past, it appears Modern Monetary Theory (MMT) is becoming the most relevant alternative to orthodox economic thinking. Later today two expert witnesses, Randall Wray and Olivier Blanchard, are expected to testify before the House Budget Committee. The focus of the discussion will be on whether widening budget deficits have an adverse impact on the economy; in which MMT would argue only if it leads to inflation. The impact on these hearings reflects a growing desire to increase deficits to boost growth. Over the past ten years economic growth in the U.S. has averaged just a little over 2%. In addition, traditional theories that hold that widening deficits leads to higher inflation have been somewhat unfounded during this expansion. Currently, the fiscal deficit is approaching $1 trillion for the first time since the financial crisis, while inflation as determined by the Personal Consumption Expenditure (PCE) still remains well below the Federal Reserve’s inflation target of 2%. As plans such as Medicare-for-all and the Green New Deal become more prevalent in policy discussions, we expect MMTers to grow in prominence.[1]

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EST] Episode #3 of our Confluence of Ideas podcast is now available.

It’s rather quiet this morning with a modest risk-on tone to the markets. Yesterday, on the other hand, was active. Trump and Powell met. The government might shut down due to a lack of funding legislation. Hong Kong remains in turmoil. Bolivia is in turmoil too. Tory poll numbers improve. Trade news and other times from northeast Asia. Here are the details.

The president and the chair:President Trump and Chair Powell met at the White House yesterday. Meetings between these two officials are not historically all that unusual but have, at times, led to strong pressure from the White House. Both the president and the chair felt compelled to offer a public comment. The president continues to press the Fed for easier policy.[1] Chair Powell continues to protect the independence of the Federal Reserve. Of all the Fed related items out yesterday, the most intriguing, in our opinion, comes from Boston FRB Rosengren. He opposed the last rate cut; in fact, he has opposed all the most recent cuts. However, this isn’t because he is an inflation hawk. He is part of a small but growing faction of what we call “financial sensitives” who worry that rate cuts to lift price inflation are destabilizing the financial system. This stance is probably never going to dominate Fed thinking because it would put the bank in an impossible position; it would be setting policy based on financial conditions. Imagine a chair indicating rates were lifted because the P/E was too high. However, what makes the financial sensitives interesting is that they would take financial conditions into account when setting policy and if conditions are easy, they would be hawkish. In some respects, Rosengren, Brainard and Evans are perhaps the three FOMC members that would be the most difficult for markets to take. As a matter of record, neither Rosengren or Evans will be voters next year.

Government shutdown? With all the focus in Washington on impeachment, the need to fund the government is being lost in the noise. However, the potential for a shutdown in the next two weeks is rising.

China-Hong Kong:China’s parliamentary committee on law and labor issued a statement of “strong dissatisfaction” with Monday’s Hong Kong court decision overturning the city’s ban on protest masks. To make matters worse, a committee spokesman noted that under Hong Kong’s mini-constitution, China’s parliament has the final say on whether a municipal law is legal. By implying yet another trampling on Hong Kong’s autonomy, the statement is likely to further inflame the ongoing anti-China protests, which have already been weighing on the city’s economy and financial markets. Meanwhile, politicians and professors helped negotiate the evacuation of hundreds of protestors who had been holed up at the Hong Kong Polytechnic University. Under the deal, police said they wouldn’t immediately arrest anyone under 18, and would be lenient to any older protestors. However, approximately 100 protestors who don’t trust those assurances are reportedly still in the facility, and it isn’t clear what the police will do to get them out. We also note that Congress is getting increasingly active on condemning China. If a bill that condemns China’s actions in Hong Kong passes Congress, the president will almost be forced to veto it or see the trade talks fail.

Bolivia: Although Bolivia’s current (and self-proclaimed) interim President Jeanine Áñez said she would operate a caretaker government until the next elections, in fact, she has moved to unwind much of the nativist and populist policies of her predecessor, Evo Morales, currently enjoying exile in Mexico. Bolivians have noticed and are starting to express their opposition.

United States-South Korea: Negotiations on the financial burden sharing for U.S. military forces in South Korea broke down today, just six weeks before the current agreement expires. The U.S. side reportedly walked out of the talks after the South Koreans balked at quintupling their current annual contribution of almost $1 billion. He who pays the piper gets to call the tune, but the Trump administration finds little motivation in controlling the U.S. security environment around the globe. Rather, its motivation is in reducing the costs of global hegemony, even if that risks damaging relationships with allies like South Korea or Japan.

United States-North Korea: State media in Pyongyang claims the Trump administration proposed resuming the U.S.-North Korea nuclear talks in December, ahead of the year-end deadline for new ideas set by Kim Jong Un. However, the report didn’t say whether the North Koreans would accept the offer.

Iran: The Islamic Revolutionary Guard Corps have threatened to crack down on the continuing protests against a hike in fuel prices. The massive, violent protests suggest the renewed U.S. sanctions on Iran are creating social tensions as planned, though it isn’t clear whether the government will feel enough pressure to meet U.S. demands.

Eurozone Monetary Policy: Almost 60% of German banks are now charging negative interest rates on at least some large corporate deposits, while more than 20% are doing the same for large retail deposits, based on new data. The growing prevalence of negative rates in high-saving Germany is likely to generate stronger pushback against the ECB’s loose monetary policy, and help turn policymakers’ attention toward looser fiscal policy to stimulate economic growth.

Brexit and the elections: PM Johnson reversed himself on corporate tax cuts, citing costs. The Labor Party continues to strike a hard-left stance in its campaign for the December election, today releasing a hyper-intrusive, rigid plan for reining in business. This may account for recent polling action showing a surge for the Tories. Meanwhile the EU is warning Britain that a comprehensive trade deal by the end of next year is probably impossible, meaning that either a small deal is done, or hard Brexit occurs anyway.

(Due to the Thanksgiving holiday, the next report will be published on Dec. 2.)

In Part I of this report, we presented the first two of four ideas about the post-Cold War era and how well they fared. This week, we will cover the remaining two ideas and conclude with market ramifications.

Idea #3: The German Problem

Modern Germany sits in the center of Europe. It has few natural barriers, meaning it is nearly perfect for commerce and impossible to defend. The country was formed in the wake of the Franco-Prussian War of 1870. Germany was fashioned by Prussian leaders coalescing other independent regions in the area that were formerly part of the Holy Roman Empire. The decision to create a nation was due, in part, to prevent another military power from conquering the various principalities as Napoleon did and to take full advantage of the industrial revolution.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EST] Episode #3 of our Confluence of Ideas podcast is now available.

Happy Monday! U.S. equity futures are modestly higher this morning on hopeful trade talk. PBOC eases. Hong Kong unrest intensifies. Iran also facing unrest. Lebanon flirting with banking crisis. Here are all the details and more:

Trade talks:USTR Lighthizer and Treasury Secretary Mnuchin conducted a phone conversation with Vice-Premier Liu yesterday. We have seen a spate of positive comments recently. For example, the U.S. is expected to grant Huawei (002502, CNY 3.48) a 90-day license extension. However, one fact remains—China wants a tariff rollback and it isn’t clear that President Trump will agree. Equity markets continue to ride on optimism surrounding a trade agreement. If trade hopes are dashed, we could see a sharp reversal in the near term.

PBOC eases: It wasn’t much of an ease, a mere 5 bps; the PBOC cut its 7 day repo rate to 2.50% from 2.55%. However, it was the first cut in this easing cycle. This rate peaked in March 2018. Although the cut was small, it is expected that there is more to come. Reports suggesting problems for China’s smaller banks continue to circulate.

Iran unrest: As is common among OPEC nations, Iran heavily subsidies gasoline. An Iranian was paying 10k riyals, or about 32 cents per gallon; the new price is 15k riyals, or about 50% increase. In addition, if a household purchases more than 16 gallons in a month, the price doubles again. Consumers didn’t take the hike lightly. Supreme Leader Khamenei tried to ease fears, and at the same time warned demonstrators against violence. There is clear concern about the anger; Iran has blocked internet access which would be critical in organizing opposition. We have seen protests around the world over price increases, or reduced subsidies on government supplied goods. Iran does appear worried. Although U.S. sanctions have not led to new talks with Tehran, or stopped Iran’s meddling in the Middle East, the Iranian economy has clearly suffered. The decision to raise gasoline prices smacks of either desperation, or foolhardiness. We lean toward the former.

A leak: Yesterday, the NYT ran a long report of what appears to be leaked internal CPC documents regarding the crackdown in Xinjiang. The information does appear consistent with China’s actions in the region. To a great extent, the extensive leak gives more details on China’s suppression. At the same time, we saw few surprises in the report. The bigger story is who leaked it and why. It is possible that it is someone looking to undermine Chairman Xi; or perhaps a hardliner that wants to scuttle the trade deal.

Netherlands: Because of the country’s strict pension funding rules, exacerbated by the ECB’s ultra-low interest rates, some two million Dutch pensioners are facing benefit cuts beginning next year. Parliament is therefore set to start debating a solution this week, with unions threatening mass protests if relief isn’t provided. Given that the United States and many other countries face similar pension pressures as a result of population aging, longer life expectancies, and low interest rates, it could be especially instructive to see how the Dutch political process deals with the issue. Of key importance will be the relative weight put on higher required contributions, benefit cuts, or government support.

Lebanon banks: Lebanon’s financial system is essentially a dual currency system; USD and the Lebanese pound. Either specie is used in transactions. For this system to work the Bank of Lebanon has to maintain a stable exchange rate; most of the time, it trades around 1475 to 1525, pound to dollar. However, there is a problem with this system; the central bank can only print one of these currencies. So, to maintain the exchange rate, the central bank either needs to maintain a steady ratio of supply between the two currencies, or the country must have a steady inflow of dollars, mostly through tourism. Recently, banks have stopped allowing dollar depositors access to their money, leading to panic hoarding of dollars. To increase the supply of dollars, Lebanon must implement austerity to run a current account surplus; needless to say, the current level of unrest suggests this will be very difficult to manage.

Global Trade Flows: The WTO said its September leading indicator of global trade flows improved slightly but still pointed to below-average growth, as improvements in export orders, container shipping and auto shipments were offset by weaker air freight and shipments of raw materials and electronic components. The news is probably a slight positive for global stocks.

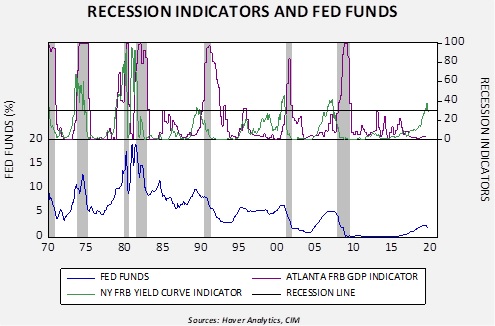

The yield curve has steepened since the FOMC started cutting rates, raising hope that a recession can be avoided. In this report, we will examine whether these hopes make sense.

The above chart shows two recession indicators from two different regional Federal Reserve banks, Atlanta and New York. The former is a GDP-based indicator and the latter is based on the yield curve. The New York indicator is designed to signal economic activity a year into the future. We like to combine the two indicators because the Atlanta indicator tends to give false positives. However, in the past, when the New York indicator has moved above 30 followed by an Atlanta indicator rising above 40, a recession has been unavoidable.

Fed funds show us that easing doesn’t necessarily protect the economy from a downturn. Even though the FOMC has usually cut rates as the New York FRB indicator penetrated 30, it was not enough to fend off a downturn. Thus, even with the recent rate cuts, the risk of recession remains elevated.

The good news is that the Atlanta indicator is at a level where a recession isn’t imminent. The bad news is that the New York indicator has signaled a downturn is coming. Since the 1969-70 recession, the average lead time from the New York recession indicator has been 10 months, with a range of five to 15 months. Thus, by next spring, we could see evidence of a downturn. However, if we use the Atlanta indicator as a signal-confirming device, we should have a better idea of when a recession is actually underway. So, for now, investors should not become overly cautious but, by the end of Q1, increased vigilance will likely be warranted.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EST] Episode #3 of our Confluence of Ideas podcast is now available.

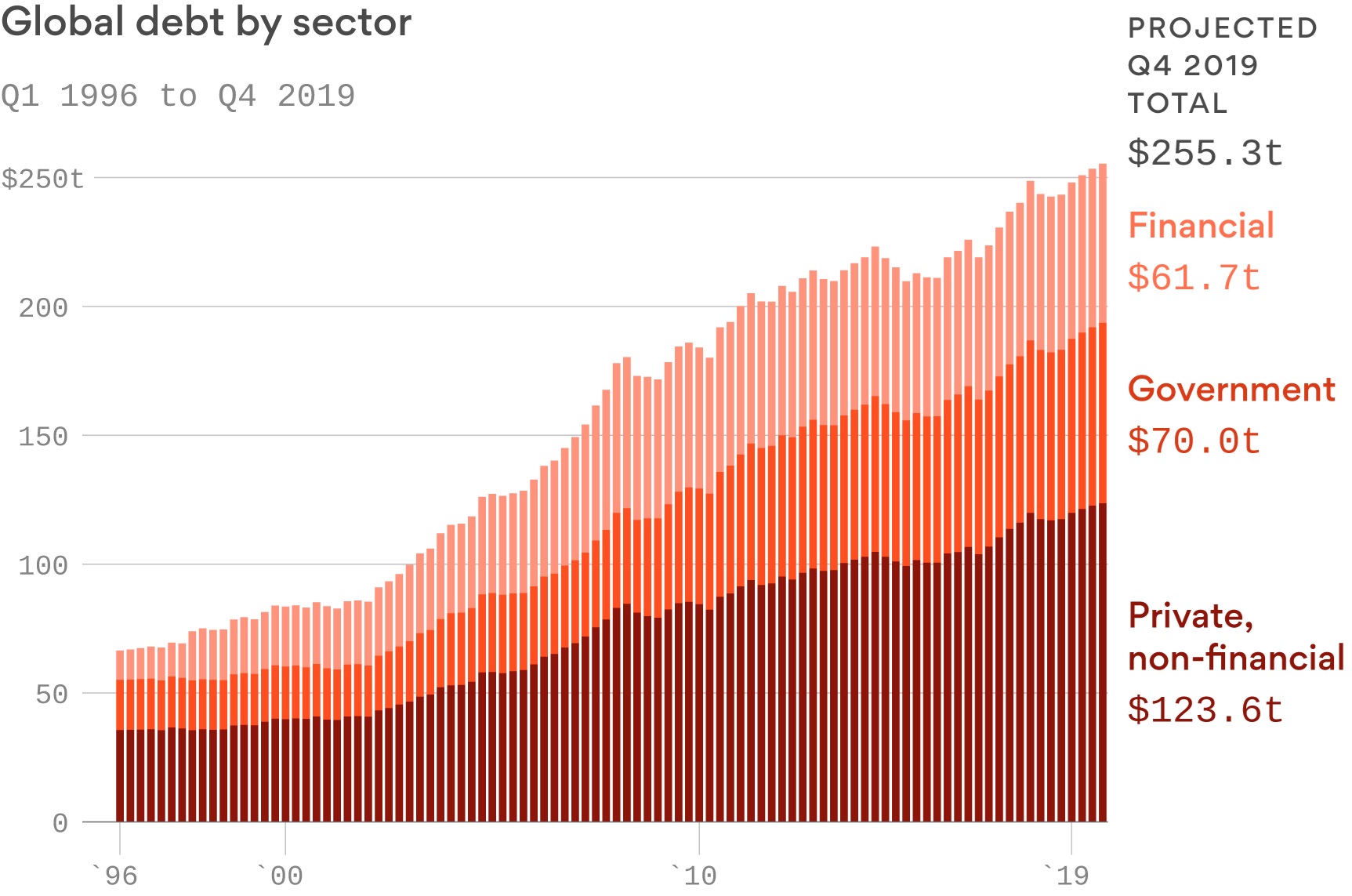

U.S. equity futures are modestly higher this morning. Lots of data today (see below). Some optimism on trade. Hong Kong is still very tense. Debt is on the rise. Here are all the details and more:

Trade: There are a couple positive news themes this morning. First, Larry Kudlow told the Council on Foreign Relations that a deal was “close,” but President Trump was not ready to sign off quite yet. Kudlow is part of the establishment wing of the administration and has repeatedly offered optimistic viewpoints on numerous issues including trade. Earlier this week, the talk on trade was much less favorable. Although Kudlow may be offering a valuable insight into the path of negotiations, it is also likely he is merely showing his bias. Second, Speaker Pelosi was optimistic that USMCA may be close to passage. With a number of distractions on Capitol Hill (impeachment, spending bills[1]), passage of the North American trade pact seems unlikely but moderate Democrats facing tough elections next year are pushing the Democratic caucus to pass the measure.

(Reproduced from Institute of International Finance; Chart: Axios Visuals)

Financial debt is usually less of a concern because it includes some double-counting. Still the rise in private, non-financial (business and household) and government debt is significant. There are two issues to focus on. First, there is the sustainability problem. Debt by itself isn’t usually a problem; it’s the ability to service it that is the issue. High debt levels increase pressure on central banks to keep rates low because higher interest rates raise debt service costs. The implementation of negative interest rates is related, in part, to the issue of debt size. Second, there is the adjustment problem. If the debt does become unsustainable, the allocation of “pain” to debtors and creditors becomes the key part of the resolution process. The decision on the allocation of costs comes from the political system. It’s important to remember that one party’s debt is another’s asset. If debt values are going to fall, it’s either because asset values are going to decline, or borrowing is going to reverse (or both). Reducing debt values has led to historic events. The Great Depression was one such event. Japan over the last 30 years is another. Debt management may be the biggest issue the world faces now because a “sudden stop” in lending can lead to a cascade of defaults and in some nations, this debt may be denominated in some other nation’s currency, which makes resolution much more difficult. This is one of those “background” issues that always lurks, but occasionally pops up to cause problems.

North Korea: A day after North Korea threatened a “new path” if the United States and South Korea hold their planned joint military exercises next month, satellite images show dozens of military aircraft parked wing-to-wing at a North Korean civilian airport. The line-up could be in preparation for a visit by North Korean leader Kim Jong-un, but it could also signal some new kind of air power demonstration. In any case, it seems to confirm North Korea’s growing frustration with the denuclearization issue and the likelihood that it could soon revert to provocative military steps, which would likely unsettle the financial markets. Meanwhile, on a visit to South Korea, U.S. Defense Secretary Esper called on South Korea to cover more of the cost of stationing U.S. troops in the country. The Trump administration is pushing for the South Koreans to quintuple their contribution to $5 billion per year.

(Source: NPR)

France: As an antidote to all the news about global trade tensions and slowing factory activity, it’s important to keep in mind the power of economic reform, and not just in the so-called emerging markets. For example, French new business registrations in October were up 15.7% year-over-year, continuing the double-digit increases over the last two years. The continuing surge is driven by business-friendly reforms under President Macron, including the scrapping of a wealth tax on all assets other than property, a flat tax on capital gains and a special visa to attract start-ups.

Energy update: Crude oil inventories rose 2.2 mb compared to an expected build of 1.5 mb.

In the details, U.S. crude oil production rose 0.2 mbpd to 12.8 mbpd, a new record. Exports rose 0.3 mbpd, while imports declined 0.3 mbpd. The rise in stockpiles was mostly in line with expectations.

(Sources: DOE, CIM)

The above chart shows the annual seasonal pattern for crude oil inventories. We are approaching the end of the autumn build season, which implies we will see a modest drop during the month of December.

We continue to monitor the autumn refinery maintenance season.

(Sources: DOE, CIM)

This week’s rise is normal, but utilization remains below average. Run rates should continue to rise into the new year.

Based our oil inventory/price model, fair value is $57.82; using the euro/price model, fair value is $49.07. The combined model, a broader analysis of the oil price, generates a fair value of $51.25. We are seeing the divergence between dollar and oil inventories narrow as the dollar weakens and oil stocks rise. We expect the Saudi IPO process to support oil and any positive news on the trade front would be supportive for oil prices as well. At the same time, the IEA is warning of a potential supply glut next year due to rising non-OPEC output. Although we expect output discipline into the IPO, the Saudis may attempt to retake market share post-IPO. Historically, such events usually lead to much lower oil prices.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.