Economy grows at 1.5%; consumption has become the primary driver of growth.

Expansion continues to set new records for duration; no recession is our base case in 2020, although there are increasing risks of a downturn.

Core inflation max is 2.5% next year.

Dollar weakens, although the direction is mostly dependent on administration trade policy. We expect preparations for the 2020 elections will lead to a less aggressive trade policy.

S&P 500 earnings for 2020 will be $174.91 on a Thomson/Reuters basis (6.00% of GDP).

Assuming a P/E of 19.3x, using the S&P earnings projection, our expectation for the S&P 500 is 3375.76.

We expect some improvement in the lower capitalization areas of the equity markets, tempered by slower economic growth.

Growth has greatly outperformed value in recent years, a trend that has been mostly driven by multiple expansion. While we are expecting only a modest multiple expansion next year, continued outperformance by growth stocks is probable. This long period of outperformance, however, is likely nearing its end. Given the difficulty of timing such a transition, we recommend a balanced position in value/growth.

International will benefit if our assumption that the dollar weakens is correct.

We expect mostly steady monetary policy next year.

We expect the 10-year yield to peak at 2.25% next year, with a range of 1.70% to 2.25%.

Investment-grade bond spreads should stabilize; we believe high-yield bonds are overvalued and no more than a benchmark weighting is justified.

Despite a weaker dollar, commodities will likely struggle due to slow global growth.

Risks to the Forecast:

Primary risk – Recession: The Federal Reserve has lowered rates recently and this action may bring us a soft landing. However, recession risks are elevated. We provide market risk parameters below should a recession occur.

Secondary risk – Election: Election years add an element of uncertainty to investment. This year’s election is fraught with potential risk.

Secondary risk – Melt-up:Ample liquidity, accommodative monetary policy and fairly valued equity markets could trigger a sharp rise in equity prices, especially if the markets become comfortable with the idea that the Fed has engineered a soft landing. Under this scenario, we provide possible upside parameters below.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EST]

N.B. A couple of items. First, the Daily Comment will go on hiatus from Dec. 23, 2019 to Jan. 1, 2020. Publication will resume on Jan. 2, 2020. Second, the fifth episode of the Confluence of Ideas podcast has been posted. “Arriving at Decisions” examines the issues that surround making decisions under conditions of uncertainty.

Good morning, possibly at the dawn of a new era of non-negative interest rates . . . or at least that’s a possibility given today’s news out of the Swedish central bank, as discussed below. There’s also more evidence that any end to the world’s negative interest rates may be matched by a revival of fiscal stimulus. Here’s what we’re watching today:

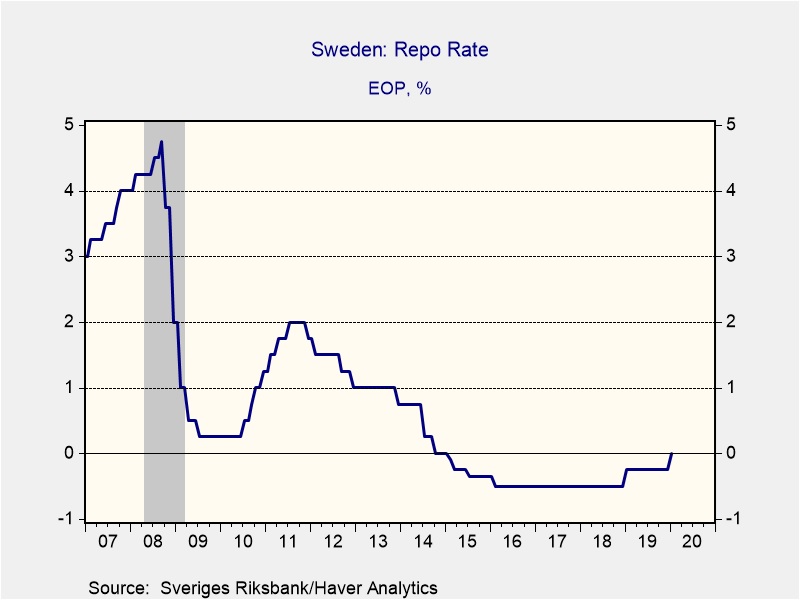

Sweden: In a sign that the era of negative interest rates may be ending, today the Swedish central bank raised its benchmark short-term interest rate to 0% from -0.25% previously. Even though Swedish economic activity has been cooling in recent quarters, the policymakers justified the rate hike by citing the widespread worry that negative rates, which have prevailed in Sweden since 2015, could be distorting the financial markets and might be encouraging undue risk-taking. The policymakers indicated they would be open to cutting rates again if necessary, but they said the more likely scenario would be for rates to stay at 0% for a long time, especially since inflation-adjusted rates remain sufficiently negative to support growth. European bonds are selling off and yields are rising on concerns that the Swedish move could be the beginning of a trend, even though the Bank of England today held its benchmark rate steady at 0.75%, and the Bank of Japan held its key rate at -0.1%.

European Union: Even as the era of negative interest rates may be ending, we’ve been noting a gradual shift in policymakers’ openness to looser fiscal policy, i.e., increased government spending, wider deficits and increased debt. The latest evidence of that came today in a speech by the EU’s new economics Commissioner Paolo Gentiloni. In the speech, Gentiloni warned that the EU’s strict budget rules, if they were fully enforced, would be inconsistent with the region’s current low-growth, low-inflation environment. According to Gentiloni, “it may not be a problem in a normal macroeconomic environment, but, as I have said, the conditions that we are living through are not normal.” Gentiloni also said he would begin a review of the EU’s deficit rules in early 2020. Coupled with Bundesbank President Weidmann’s recent warning against a balanced-budget “fetish” in Germany and the return to fiscal stimulus in Japan, this could well be a trend worth watching. Looser fiscal policy would likely help boost growth in developed countries in the near and medium terms, though with increased debt risk over the longer term.

France: Seeking to end the mass protests and strikes against his proposed pension reform, President Macron said he would be open to delay boosting the retirement age to 64 from the current 62 if another way can be found to balance the books. Government officials have been discussing the idea with union leaders yesterday and today. We view the proposal positively because even if the age provision has to be delayed in order to end the protests, the rest of the reform is focused on providing much-needed simplification and efficiency.

United Kingdom: Former shadow foreign secretary Emily Thornberry said she will be a candidate to replace Labour Party leader Corbyn. At least two other shadow ministers, Keir Starmer and Rebecca Long-Bailey, are expected to throw their hats into the ring in the coming days. While Labour will be in no position to exercise much influence in the new parliament, its focus now will be on how to rehabilitate itself for the future. The key question that party members are mulling over is whether to stick with Corbyn’s radical agenda or shift to the center.

Russia: President Putin today is holding his annual marathon news conference. In noteworthy statements so far, Putin refused to say whether he might try to stay in power beyond the official end of his term in 2024, and he defended the recent law that he signed to deem certain media outlets as “foreign agents.”

India: Protests against Prime Minister Modi’s new citizenship law continue, prompting the government to shut down communication services and prohibit public gatherings in locations around the country. Police have reportedly arrested hundreds of protestors, but it still looks like the pushback against the law is limited mostly to Muslims. The government’s clamp down on communications and public gatherings therefore has a good chance of keeping the tensions under control. As if to confirm that, Indian stocks rose to yet another record high today.

United States-South Korea: U.S. and South Korean negotiators failed to reach an agreement on cost sharing for the U.S. troops stationed in South Korea, but the U.S. side hinted it would no longer stick to President Trump’s demand that Seoul quintuple its contribution to $5 billion per year. If the U.S. side backs off that number when the negotiators next meet in January, it would likely help improve relations between the two countries, and allow them to focus more strongly on the reviving threats and provocations from North Korea.

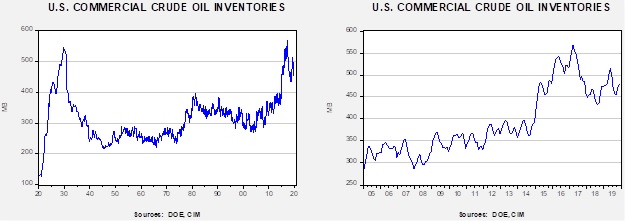

Energy update: Crude oil inventories fell 1.1 mb compared to an expected draw of 1.8 mb.

In the details, U.S. crude oil production was unchanged at 12.8 mbpd. Exports rose 0.2 mbpd while imports fell 0.3 mbpd. The decline in stockpiles is near expectations.

(Sources: DOE, CIM)

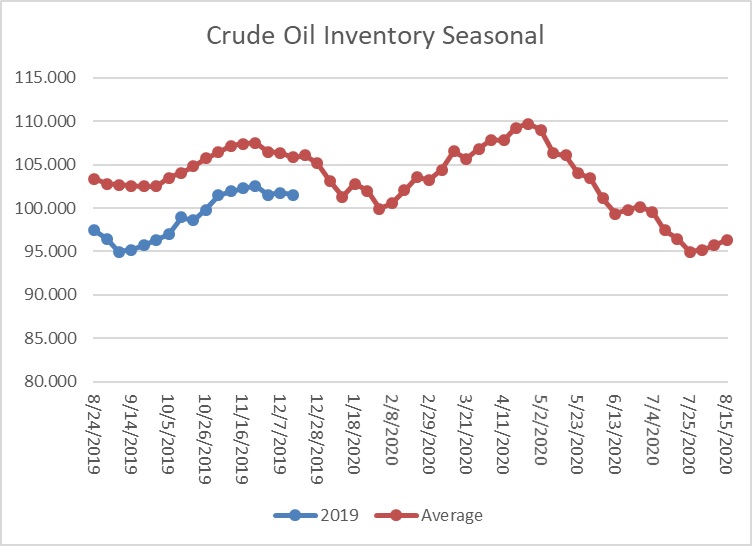

This chart shows the annual seasonal pattern for crude oil inventories. The early winter draw season is underway and will continue into early 2020.

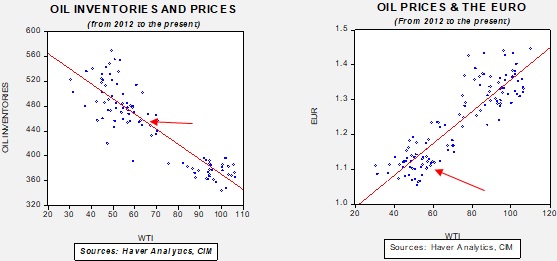

Based on our oil inventory/price model, fair value is $58.54; using the euro/price model, fair value is $50.23. The combined model, a broader analysis of the oil price, generates a fair value of $52.35. We are seeing the divergence between the dollar and oil inventories narrow as the dollar weakens.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EST]

Good morning, all. So far, the overnight news has been relatively mum as fears of an ongoing trade war appear to be dissipating. Meanwhile, rising concerns of a “hard” Brexit have weighed on the pound. Below are the stories we will be following today:

Weaker dollar in 2020: Following the agreement of the “phase one” trade deal, there has been a growing consensus that the U.S. dollar will likely weaken in the coming year. As we have written in previous reports, one of the setbacks of imposing tariffs is that it generally leads to currency strengthening. There are a few possible explanations for this:

Targeted countries may decide to weaken their currency through easy monetary policy, which would therefore soften the impact of the tariffs.

If tariffs are successful at getting countries to purchase more U.S. goods, it will lead to a boost in demand of the U.S. dollar and result in U.S. dollar appreciation.

When tariffs adversely hurt a country’s economy, it can lead to capital flight in which foreign investors seek refuge by purchasing assets in another country, thereby leading to currency depreciation in the host country.

That being said, a rollback of some tariffs should lead to a weakening of the dollar as investors attempt to move away from U.S. assets, which are generally considered havens. Furthermore, if this trend persists it will likely be bullish for foreign equities.

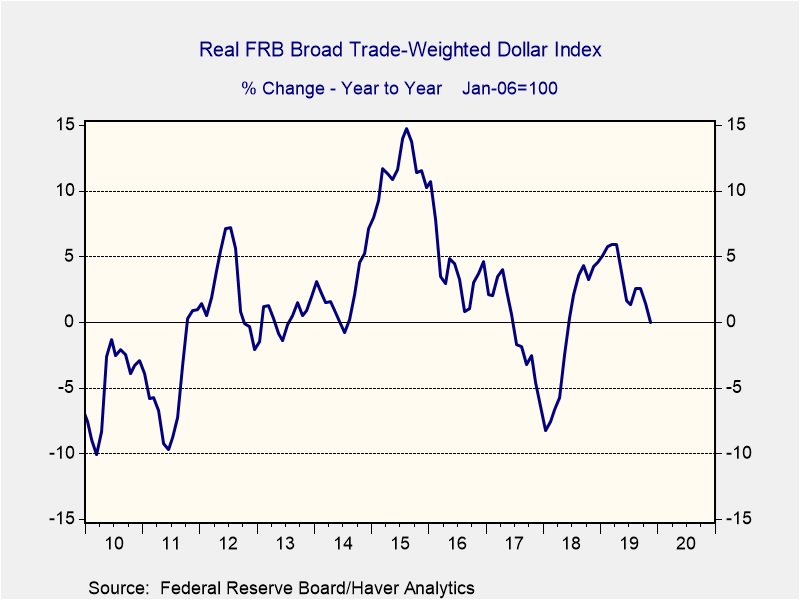

The chart above shows the year-over-year change in the Real FRB Broad Trade-Weighted Dollar Index. The index measures the strength of the U.S. dollar relative to the currencies from 26 of the country’s most important trading partners. The trend spiked in the beginning of the year but has been slowing down since April.

China agriculture purchases: There are growing concerns that the partial trade pact may not live up to expectations. In the trade pact, China has agreed to purchase at least $40 billion worth of agricultural products annually over the next two years; this would almost double its largest purchase order of nearly $25 billion in 2013 and 2014. The biggest concern about the deal is that it has not been formally put on paper; therefore, it is difficult to discern where China will make purchases. Despite the need for pork and soybeans, skeptics wonder whether China has a need for $40 billion worth of agricultural goods and may try to make up for it by purchasing non-agricultural products such as crude oil and natural gas. At this time, the formal written agreement is under review, so the commitment has yet to be finalized. Nevertheless, unless there is something in the agreement that leads investors to believe this deal will not hold, we expect the agreement to have little effect on equities.

Fears of manufacturing slowdown: Despite the reduction in global trade tensions, there are growing fears that manufacturing production will not pick up as fast as many would hope. On Tuesday, Boeing (BA, 327) announced that it will be halting its production in January of one of its flagship products, the Boeing 737 Max, as it undergoes regulatory reviews following crashes of two of its planes. Arguably the biggest U.S. manufacturing exporter, the company’s decision to halt production is expected to have an impact on the economy. Earlier this year, the company reduced its production of the plane from 52 per month to 42, resulting in a slowdown of durable goods orders. Accordingly, the halt is expected to result in a slowdown in inventory accumulation for Q1 2020 but will likely spike whenever the company decides to restore production.

The Oil Market

Since June, oil prices have held mostly within a range of $50 to $60 per barrel.

(Source: Barchart.com)

After a sharp decline in prices from late May into early June, due in part to a contra-seasonal build in inventories, inventories fell and oil prices rebounded. Rising tensions with Iran added to the lift in prices in September. Since then, we have seen a retest of the lower end of the range and a steady recovery. Soon after year-end, we usually see a seasonal rise in inventories, which tends to weigh on prices. However, with the advent of exports, that seasonal pattern has become suspect. For example, last year we didn’t see the usual increase in stockpiles.

Thoughts on Oil Demand

In general, forecasting demand is not usually a priority in commodity analysis. The shape of most short-run commodity demand curves is inelastic, which means that quantity isn’t very sensitive to price. Demand inelasticity means that a small change in supply can have outsized effects on price. It is because of that structure that commodity analysts tend to focus on supply. That being said, demand is important over the long term. For example, the effect of environmental regulations and consumer sentiment has adversely affected coal demand and severely depressed prices. The price of coal didn’t fall because supply expanded; it fell because demand declined.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EST]

Good morning from snowy St. Louis! It’s a relatively quiet morning, but there are some developments to note. It turns out the risk of a hard Brexit hasn’t entirely been eliminated, and French unions are threatening to play the Grinch for Christmas. Fortunately, fiscal policy and the financial markets look better here in North America. Here’s what we’re watching today:

United Kingdom: Reports say Prime Minister Johnson this week will propose legislation prohibiting any extension of the Brexit transition period beyond the end of 2020, even though the exit deal with the EU allows for such an extension if a new U.K.-EU trade deal isn’t finalized by then. Officials close to Johnson say the proposal merely encapsulates the prime minister’s promise to “get Brexit done.” However, it’s probably also aimed at boosting the U.K.’s leverage in its upcoming negotiations with the EU for a permanent trade deal – negotiations in which the much larger EU is likely to have the upper hand. The problem is that negotiating the new deal will be complex and time consuming. There’s no guarantee that a deal can be put into place by the end of 2020, so any law prohibiting an extension creates a new risk that U.K.-EU trade would suddenly revert to WTO rules, with the U.K. facing tariffs, quotas and other barriers to its Europe-bound exports. Both British stocks and sterling are therefore down sharply so far today.

U.S.-China Trade: Despite the euphoria over last week’s “phase one” U.S.-China trade deal, NAFTA update and U.K. election, it’s important to remember that we’re now in the period where people start focusing on the details and how things will actually play out. That will inevitably cause some second-guessing and reassessments, which will impact the markets. Today, for example, there are reports that one way China plans to show a boost in its U.S. imports is to lift its trade war tariff on fuels, and re-route some $10 billion in ethanol imports so they come directly to China, as opposed to being transshipped through Hong Kong.

U.S. Repo Market: In an important sign that the Fed may have gotten its hands around the issues in the short-term borrowing market, the overnight repo rate barely budged yesterday, even though it was the deadline for quarterly corporate tax payments, and settlement day for recent Treasury bond issues. When those issues last popped up in mid-September, overnight rates spiked to above 10%. The Fed responded by flooding the system with cash in the form of short-term loans, which has not only appeared to calm the market down, but will probably also provide a boost to the economy and the broader financial markets. Add that to the list of uncertainties that have been lifted in recent days (U.S.-China trade, the NAFTA update, and Brexit), and it should be no surprise that the equity markets performed so strongly yesterday.

Canadian Government Budget: Canadian Finance Minister Morneau issued updated economic and fiscal forecasts showing the government will tolerate much bigger deficits for the next four years. In part, the decision to loosen fiscal policy reflects the challenges of running a minority government that relies on the support of left-leaning parties. More broadly, the move provides additional evidence that governments around the world are warming to the idea of spending more to boost growth, especially now that loose fiscal policy is seen as becoming less effective. Bigger budgets may very well help goose growth and boost asset prices, though at the expense of higher debt levels later on.

United States-Mexico-Canada: In an effort to diffuse Mexico’s anger over a provision in the USMCA bill making its way through Congress, U.S. Trade Representative Lighthizer said labor disputes under the new trade deal will still be adjudicated by an independent panel, as agreed to by the United States, Mexico and Canada last week. According to Lighthizer, the U.S. labor attaches would merely offer “technical assistance” when disputes arise, rather than acting as independent inspectors. Mexican trade negotiator Jesús Seade said he was satisfied with the U.S. response. That should help ensure U.S. approval of the deal can happen this week, which should be positive for U.S., Mexican and Canadian equities.

Germany: Even though Chancellor Merkel’s open-door immigration policy at mid-decade generated intense popular pushback and helped spark the rise of populist leaders throughout Europe, continued economic growth and low unemployment could be reversing the tide. Against a backdrop of worsening labor shortages, even as growth slows, the Merkel government yesterday held a “skilled labor summit” to discuss ways to bring foreign workers to Germany from outside the EU. In spite of the political cost of the immigration policy in recent years, Merkel was sufficiently emboldened to say, “What is really important is that we are seen in third countries as a country that is open to the world and interested.” Just as notable, Finance Minister Scholz said, “We have accepted that we are a country of immigration.” It’s important to remember that Merkel is a lame duck, so such statements probably have limited political cost for her. All the same, it will be interesting to see if skilled worker shortages reduce anti-immigrant sentiment and the appeal of populists in Germany, or elsewhere.

India: Prime Minister Modi issued a strong defense of his new citizenship law, which has sparked mass protests across India because of its perceived tying of citizenship to religious affiliation, and discrimination against Muslims. The statement did nothing to diffuse the protests. If they continue and grow, the demonstrations could become a headwind for Indian assets.

(This is the last report for 2019; the next report will be published January 13, 2020.)

As is our custom, in mid-December, we publish our geopolitical outlook for the upcoming year. This report is less a series of predictions as it is a list of potential geopolitical issues that we believe will dominate the international landscape for 2020. It is not designed to be exhaustive; instead, it focuses on the “big picture” conditions that we believe will affect policy and markets going forward. They are listed in order of importance.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EST]

Happy Monday! Equities are lifting this morning on continued trade optimism, despite some creeping concerns. Economic data around the world was mixed; solid for China, weak for the Eurozone. More debt worries for China. Here are the details:

Trade: First, the Phase One deal with China. There is a lot of clutter to work through, but our bottom line is this—if China holds up its end of the bargain, Washington got the better of Beijing. Here’s why:

China has agreed to buy a lot more of U.S. goods. Although there are reports of certain levels of agricultural purchases, the key phase is that China will “import various U.S. goods and services over the next two years in a total amount that exceeds China’s annual level of imports for those goods and services in 2017 by no less than $200 billion.” Over the past two years, U.S. exports to China have run between $180 bn to $190 bn. Essentially, China has agreed to boost imports by $100 bn per year over those elevated levels. So, that would put exports around $280 bn.

Needless to say, that’s a lot. To hit that number, China should buy lots of U.S. grain and meat products. Energy too. For now, China has a clear incentive to buy our commodity products because its food inflation is really high. Additionally, because China has a two year window, it could be light next year with the promise of lifting purchases in 2021. So, retaliation on this issue probably isn’t immediate.

China agrees to not manipulate its currency. That isn’t a huge “give up” because a weaker CNY creates problems for China. Currency weakness increases capital flight and raises debt service costs for dollar-denominated debt. So, Beijing is probably more comfortable with a stable CNY.

There is vague language about intellectual property and technology transfer. The language in the agreement, on its face, is a huge win for the U.S. as China supposedly agrees to give up its practice of forcing foreign firms to transfer technology. However, the lack of details suggests this goal is aspirational and we would be shocked to see China meet U.S. demands on this issue. If Phase One is going to fail, this is an area of risk.

There is also vague language about dispute resolution. There were no details.

For all this, the U.S. did not implement tariffs on Dec. 15 and reduced tariffs on $150 bn of Chinese imports from 15% to 7.5%. To put a fine point on it, the U.S. tariff reduction will increase Chinese imports by $10 to $15 bn and in return, the U.S. will increase exports to China by $120 bn. If China abides by this deal, it is a huge win. Which means, of course, that the likelihood of compliance is low. The issue now becomes when does the Trump administration have enough evidence to say China is not meeting the terms of the deal and start putting tariffs back. The fact that the USTR remains at his post means that if our assumptions are correct, China has to be aware that when they fail to live up to their agreements, Lighthizer will inform the president. At the same time, we doubt President Trump will want to cause a tariff problem in an election year, so expect mostly trade peace in 2020. On the other hand, 2021 is a different matter.

One final thing on China. We do expect Beijing to make a show of compliance by purchasing lots of U.S. agricultural goods and energy. That will reduce buying from other nations. Thus, South America, Indonesia and Australia may be adversely affected by the deal.

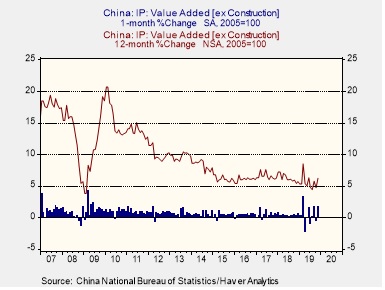

China: Adding to Friday’s positive news of a limited U.S.-China trade deal, Beijing released a trove of data suggesting its modest stimulus measures may have arrested, or even partially reversed its continuing economic slowdown. Perhaps most important, November industrial production was up a much better-than-expected 6.2% year-over-year, marking its best annual gain since June. November retail sales rose by a better-than-expected 8.0% on the year. Fixed asset investment in January through November matched its recent pace with a rise of 5.2% from the same period one year earlier. The figures should be positive for global equities today.

China debt: We have been watching China’s debt situation for some time and, as discussed in our 2020 Geopolitical Outlook (out this afternoon), it is one of our key concerns for next year. Over the weekend, an odd twist emerged. Beijing has decided to drop a huge number of criminal charges against firms in the private sector due to concerns that the arrest and prosecution of company leaders will only lead to the failure of their firms, unemployment, and of our concern, increase the odds of debt default.

We are not sure what to make of this development, other than it would seem to reflect an extraordinary level of concern among financial authorities. The signal it sends to business leaders is that any behavior, with the possible exception of criticizing the government, is acceptable.

The U.S. consumer: U.S. growth has become almost completely dependent on consumption. Although wage levels improved and confidence is elevated, we note that retailers are complaining that they are being forced to discount aggressively this Christmas to move merchandise. This development may not mean that households are struggling. It is possible that this problem may be more about excess capacity in retailing, or the impact of online shopping. In addition, shoppers have been “trained” to expect deep discounts and won’t shop if they don’t get them. However, what the report does indicate is that retail firms are likely facing margin compression from the discounting.

United States-North Korea: After yet another North Korean missile test on Friday, U.S. Special Envoy to North Korea Stephen Biegun criticized the provocations, but emphasized that the Trump administration is open to resuming denuclearization talks. Meanwhile, the U.S. Center for Strategic and International Studies released imagery suggesting that North Korea may be preparing for another test of a submarine-launched missile as we approach Kim Jong Un’s year-end deadline for new denuclearization talks.

India: The riots against India’s new religion-based citizenship law, which we described in our Friday comment, continues to spread and escalate. The protests have become especially strong on university campuses throughout the country, including Delhi, Mumbai and Hyderabad. As yet, there is no indication the protests will become a threat to Prime Minister Modi, or Indian assets, but we are watching the situation closely.

A pair of curious developments: Last month, two Chinese embassy officials drove onto a U.S. military base in Norfolk, VA. The base houses some Special Operations forces. The two “diplomats” claimed they were lost. They found their way back to China. This event is unusually brazen, and underscores tensions between China and the U.S. The other odd news item are reports from China that criminal gangs apparently became involved in the spread of the African Swine Virus in an attempt to boost hog prices. The gangs were smuggling potentially tainted pork across provincial boundaries for profit, and the virus was apparently good for business.

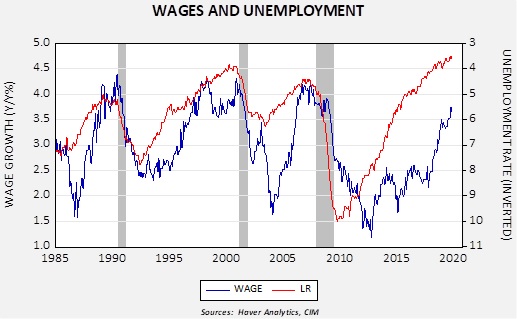

The recent employment report was very strong, with payroll growth rising more than forecast and the unemployment rate declining more than expected. One uncertainty that develops when labor markets tighten is the point at which wage growth begins to lift inflation.

This chart shows yearly wage growth and the unemployment rate (inverted scale). In the past three cycles, an unemployment rate at this level would have been consistent with wage growth in excess of 4.0%. Although wages have been increasing, the growth rate remains below the 4.0% level.

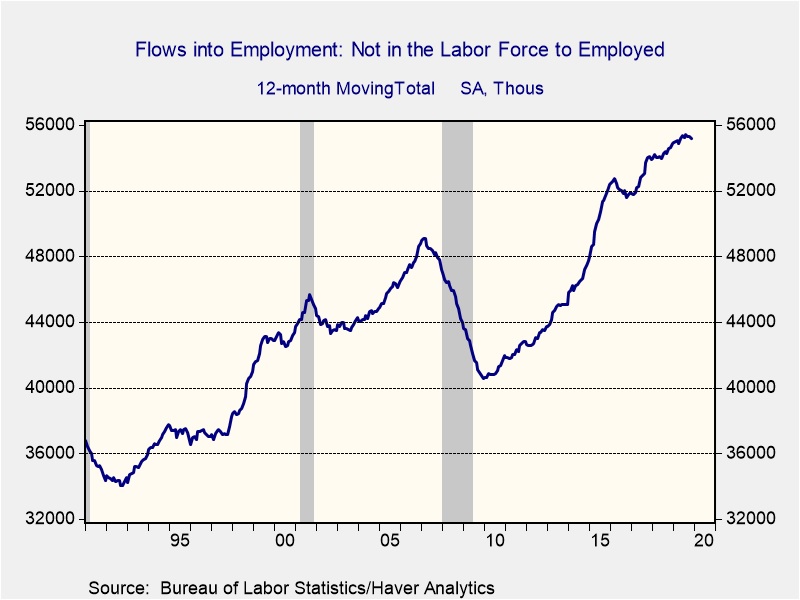

The reason wage growth remains modest is complicated, but a contributing factor is that the labor force continues to increase. A key function in that process has been that citizens who were not part of the labor force have been steadily finding jobs. The chart below shows the 12-month rolling total of those who have been out of the labor force and found employment. This number has been increasing in this expansion.

At the same time, the pace of these flows is beginning to slow. If this source of new employees declines, in theory, it would tend to lift wages at an increasing pace until employment growth slows. Nevertheless, for now, the labor market appears to be strong enough to attract new entrants into the labor force and employment, without excessive wage growth, which is a positive development for the economy.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.