The December employment data showed three interesting developments that are worth discussing. They are wage growth, hours worked and the level of “out of the workforce.”

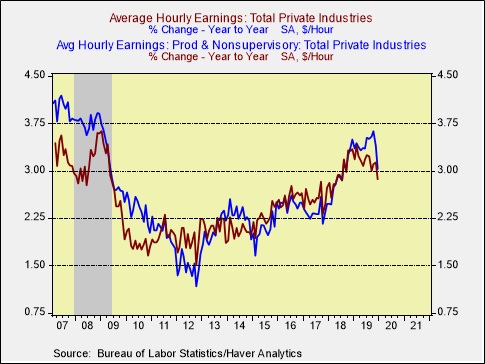

Wage growth: For most of last year, production and non-supervisory wage growth was outpacing that of overall workers. This development suggested that ordinary workers were finally benefiting from the long expansion. However, it was uncertain if the growth was due more to changes in state and local minimum wage laws or due to tight labor markets. It appears we have our answer. Many of the changes to local and state minimum wage laws occurred after the 2018 midterm elections. December’s data would be 13 months after many of these new laws came into effect, so if legislation was the primary cause of the rise in ordinary worker pay then we should have seen a drop in December’s wage growth.

In fact, that’s exactly what we saw. In November, wage growth for this class of worker rose 3.4%; it fell 40 bps to 3.0% in December. Thus, the divergence between total private wages and production and non-supervisory worker wages appears to be solely a function of minimum wage laws. Without additional measures, it seems unlikely that the divergence will continue.

Hours worked: The growth rate of hours worked by production and non-supervisory workers fell to its lowest level since June 2010.

The combination of fewer hours and falling wage growth will tend to further dampen available liquidity for the majority of households. The weekly hours data isn’t recessionary, but it is headed in that direction.

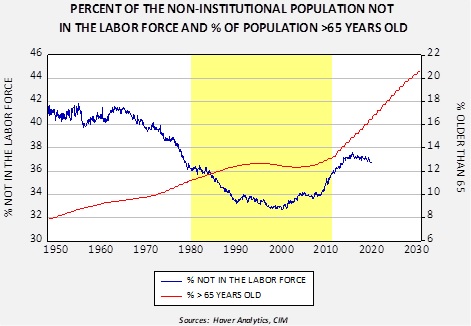

Out of the workforce: When the Bureau of Labor Statistics calculates the labor force, it includes those working and looking for work. Some citizens purposely decide to stay out of the labor force for a myriad of reasons, with age being the most likely. In other words, as the number of citizens reaching retirement age increases, the percentage of the population that can continue to work will tend to decline as will the potential labor force. Nevertheless, as the expansion continues, the potential pool of those out of the labor force tends to decrease until a point is reached where it becomes nearly impossible to draw down this group any further. At that point, wage growth is expected to rise; at the same time, the unemployment rate can’t decline any further because potential new workers become increasingly difficult to find.

The economy may be nearing that point.

The blue line shows the percentage of those not in the labor force relative to the non-institutional population over the age of 16. The red line is the percentage of the total U.S. population older than 65, with Census Bureau forecasts. The area in yellow represents the baby boom generation. The start of this area is when the last baby boomer turned 16, and the end is when the first baby boomer hit the age of 65. In the yellow area, the percentage not in the labor force fell and stabilized. As baby boomers headed into retirement age the percentage not in the labor force began to climb. However, this percentage has recently stalled, mostly due to the extended economic expansion. This trend will be difficult to sustain as the 65+ population continues to rise. Although we are seeing workers delay retirement, the recent trend should reverse over time. That factor will tend to keep the unemployment rate lower than it has been historically.

What is important about these three trends is that two of them are suggesting some softening in the labor market, whereas the last one might mask that weakness by showing a low unemployment rate. In other words, older workers, facing a weaker labor market, may simply opt for retirement and leave the labor force entirely. That will reduce the labor force and keep the unemployment rate low, suggesting the labor market is tighter than it really is. That factor could increase the potential for a policy error.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EST]

Happy Friday! Equity markets continue to grind steadily higher to new record levels. The White House officially nominated the two last open governor positions on the FOMC. An update on the Iran missile attack and other Iran issues. Germany is holding a summit on Libya; it is also in an uncomfortable position with China. The 20-year Treasury is coming back (call Youshi). Here is what we are watching this morning:

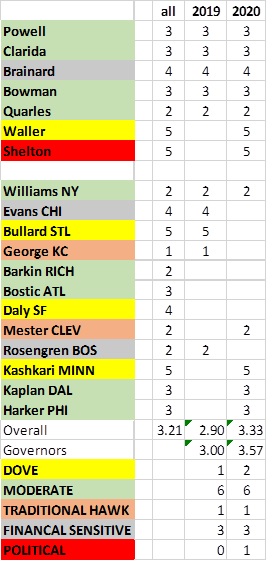

The Fed: Although the names have been circulating for some time, the White House has finished its background checks on Judy Shelton and Chris Waller. The latter is non-controversial. He is the research director at the St. Louis FRB and a conventional pick. That isn’t to say there is nothing interesting about the selection. We suspect the St. Louis Fed President, Jim Bullard, has designs on the Fed Chair job. There were rumors that Bullard was being considered for the open governor’s position. He quashed that rumor quickly but offered his research director instead. This serves two purposes: if Bullard does get the nod to replace Powell, he will have an immediate ally among the governors and, in the meantime, the composition of the board will become more dovish.

Shelton is another issue. She has argued that the Fed probably shouldn’t be in the business of setting interest rates. She has shown an affinity for the gold standard, but also seems to want to manage exchange rates in a manner to boost U.S. trade competitiveness. There were elements of the supply-side movement that wanted a gold standard, apparently, in part, to provide inflation-fighting credibility to address the fiscal expansion this group supported. This idea of “weaponizing” the dollar has been circulating recently; we addressed it in a WGR (Weaponizing the Dollar: The Nuclear Option, Part I and Part II). We expect opponents to Shelton to raise a rule that a Federal Reserve District cannot be overrepresented on the FOMC. Since Shelton and Brainard are both from Richmond, this could be raised as a problem. However, this rule has been ignored in the past, so if it is raised here it would suggest senators are looking for a reason to scuttle her nomination. Overall, we expect both to be nominated, although Shelton will be controversial.

The following table shows how the FOMC will change if they are nominated.

These are our estimates of policy leanings, with 1=most hawkish to 5=most dovish. We are assuming both of the new candidates are extreme doves (otherwise they wouldn’t have been nominated), with Waller being a traditional dove while Shelton is a political one. This means that if there is a change in administration, Shelton could become less dovish. The governors now are leaning dovish (going from 3.00 to 3.57) and the overall voting changing from 2.90 last year to 3.33 this year. This means that the hurdle for rate hikes has increased markedly. We would view these nominations as bullish for risk assets.

Libya: Chancellor Merkel is holding a meeting of the two warring groups in Libya in an attempt to reduce tensions in the divided nation. The two sides appear to be abiding by a ceasefire for now. Although we have little hope that the meetings will lead to a lasting peace (division into two nations is probably the best solution), the longer a ceasefire holds the greater the chance that Libyan oil production rises.

Germany and Huawei: The U.S. is pressuring Berlin to ban equipment from Huawei (002502, CNY 3.13). Germany has been reluctant to do so, in part, because China is threatening German car sales in China. China is the largest market for German automakers. In fact, Germany is facing a similar threat from the U.S.; the Trump administration has been considering tariffs on EU auto exports to the U.S. to address the trade deficit with the region.

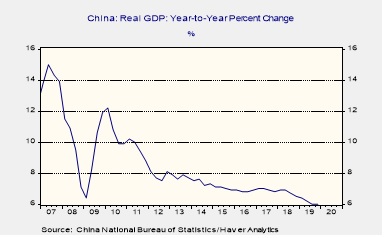

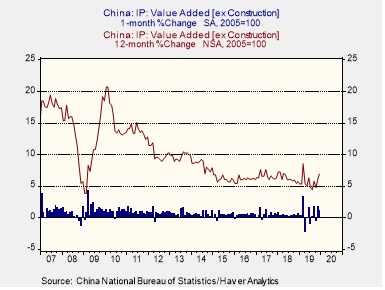

China’s GDP: The Chinese government said fourth-quarter GDP was up 6.0% from one year earlier, matching the annual growth in the third quarter but coming in short of expectations for a slight acceleration. GDP for all of 2019 rose 6.1% from 2018, marking the slowest full-year growth rate since 1990. On the other hand, other Chinese data today suggests the economy may have started to firm toward the end of the year. For example, December industrial production was up 6.9% year-over-year compared with a 6.2% gain in the year to November. December retail sales rose steadily by 8.0% from a year earlier. These figures suggest the economy may have gotten a bit of a boost as companies and consumers began to sense that the U.S.-China Phase One trade deal would really be signed. However, we doubt the economy is totally out of the woods. China is still struggling with longer term issues like poor demographics, high debt levels and general maturation. Moreover, implementing the new trade deal could be a challenge, and the Trump administration may well keep up its pressure for disruptive policy changes. That helps explain why the data only gave a slight boost to Chinese stocks and the renminbi today.

U.S.-India Trade: Officials in the U.S. and India are drafting a “limited” bilateral trade deal that could be unveiled during a visit by President Trump to New Delhi in the coming weeks. The deal would address some longstanding U.S. concerns about India’s market restrictions, while restoring India’s preferential trade status and ability to export to the U.S. duty-free. The news is probably bullish for Indian stocks.

U.S./China deal: Although the press has focused simply on the signing of the U.S.-China Phase One trade deal yesterday and the big import commitments China made in the agreement, our read of the text itself suggests the bigger story may be that the U.S. got the Chinese to make significant concessions in a number of important areas. The draft deal that China walked away from last May was apparently quite intrusive, with detailed changes to multiple areas of Chinese law. The text of the deal signed yesterday also includes many requirements that China change its legal and regulatory system to match U.S. standards, but without specifically enumerating each article, chapter and clause of Chinese law that has to be changed. Most of those changes relate to the protection of intellectual property, so there are many more issues in the U.S.-China relationship that still need to be addressed.

The agreement is being widely panned in the media. Although we always take the position of political neutrality, the tone is probably more negative than justified. There are two primary criticisms of the agreement. First, China’s practice of subsidizing firms that supports their export efforts wasn’t addressed. This charge is accurate. However, as we noted yesterday, USTR Lighthizer is working to use the WTO and team up with Japan and the EU to address this issue. In our view, Lighthizer is a grandmaster of trade negotiations; he appears to have decided that the subsidy issue is better dealt with in a broader context. Second, there is legitimate concern that China will not live up to its promises as it has in previous agreements. What is different this time is that the U.S. has shown it will implement tariffs if China doesn’t do what it says it will. We find it notable that the U.S. has kept the vast majority of tariffs in place even after this deal. That suggests the U.S. feels it won’t get compliance from Beijing without the persistent threat of a “stick.”

At least in our initial look, we have some worries too. There doesn’t appear to be a well-designed dispute mechanism; thus, the ultimate enforcement may come down to “I quit.” We are also concerned that China may not be able to fully meet the import targets; we note soybean prices fell yesterday on these worries.

However, overall, the trade war with China has clearly caught the attention of Chairman Xi. We suspect the USTR’s primary goal is to change the way the Chinese economy works, similar to what he helped engineer against Japan in the late 1980s. Simply put, he wants to change China’s economy from being investment and export driven, to consumption and import driven. Japan was never able to make the transition and thus has suffered 30+ years of economic stagnation. If China wants to avoid the same fate, it will need to make changes. Of course, history never repeats exactly the same way; China is big enough that it may try to create its own sphere of influence, something that Japan, who was dependent on the U.S. for its security, could never execute.

Putin: We once worked with a strategist who pretty much always had the same forecast, but the “show” was seeing how he would manage to create a path to that outcome. Vladimir Putin is similar in that respect. We know the outcome is always that Putin will remain in power. However, how he does it is interesting to watch. In his annual State of the Union address yesterday, President Putin launched a surprise constitutional revamp that could keep him in power past the end of his term in 2024. Under the proposal, which Putin said would be put to a referendum, the power to name the prime minister and his or her cabinet would be transferred from the president to the lower house of parliament (although the president would still be able to dismiss the prime minister and cabinet ministers). Parliament would also get greater power over the judiciary and the security services. Eligibility to become president would be tightened up so that anyone taking the post would need to first live 25 years in Russia and have no foreign citizenship or residency. Future presidents would also be limited to two terms in total. Meanwhile, the State Council, which Putin already heads, would be given increased power. To put the changes in motion, Putin replaced incumbent Prime Minister Medvedev with Mikhail Mishustin, the head of Russia’s tax office who is relatively unknown and has no appreciable political base. The move reflects a number of important principles: 1) Putin takes great pain to prolong the illusion of constitutional legitimacy, just as he did a decade and a half ago when he temporarily took the role of prime minister after reaching the term limit on his first presidency; 2) By neutering the presidency and installing a weak figure as prime minister, Putin is ensuring that he will maintain overwhelming control over the government from his position at the top of the State Council; and 3) Although the timing of the change seems early compared with the 2024 end of Putin’s current term, moving now may make sense given that Russia will hold parliamentary elections in 2021, and Putin could package the move to the advantage of his party in that balloting.

Turkey: Despite a recent rebound in inflation, the Turkish central bank today cut its benchmark short-term interest rate more sharply than expected, to 11.25% from 12.00% previously. The recent rate cuts, which have been driven largely by President Erdogan, appear to be spurring better economic activity even if they are spurring stronger price hikes. That may explain why the lira actually strengthened slightly after the rate cut was announced.

Iraq: Caretaker Prime Minister Adel Abdul-Mahdi suggested in a cabinet meeting that he would leave the decision of whether to expel U.S. forces from the country to his successor. In spite of parliament’s recent call for such an expulsion and the Trump administration’s threat to impose sanctions if it does so, that means the issue may not come to a head in the near term. Any U.S. sanctions could very well be targeted against Iraqi oil exports, boosting oil prices, so pushing the issue off into the future could help keep the oil markets calmer than would otherwise be the case.

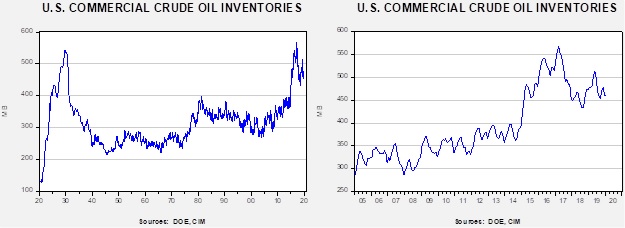

Energy update: Crude oil inventories fell 2.5 mb compared to expected no change in stockpiles.

In the details, U.S. crude oil production rose 0.1 mbpd to a new record of 13.0 mbpd. Exports fell 0.4 mbpd while imports fell 0.3 mbpd. The decline in stockpiles was unexpected but offset by large increases in product.

(Sources: DOE, CIM)

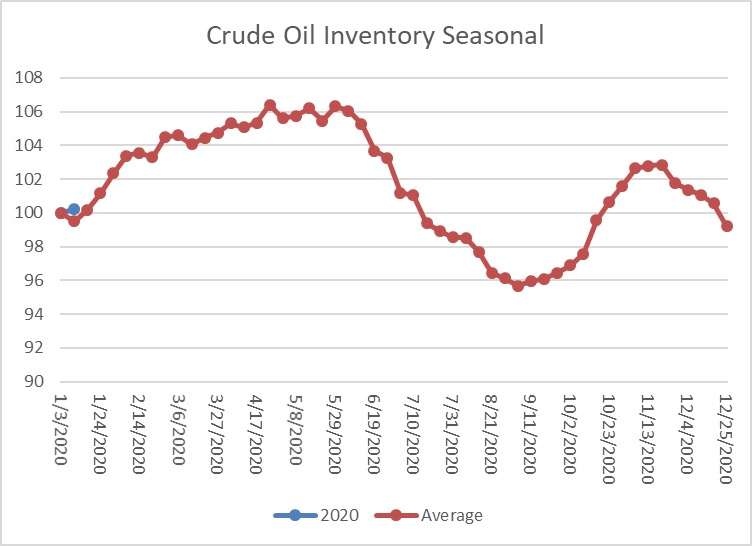

This chart shows the annual seasonal pattern for crude oil inventories. This week’s decline was a bit below normal. As the chart shows, oil inventories usually rise into late spring and then decline significantly into late summer. Last year, this pattern was disrupted to some extent because of exports.

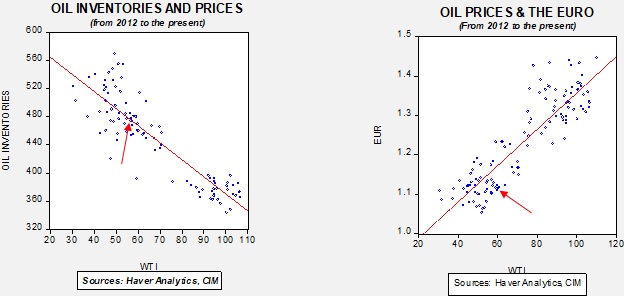

Based on our oil inventory/price model, fair value is $64.41; using the euro/price model, fair value is $51.35. The combined model, a broader analysis of the oil price, generates a fair value of $55.43. We are seeing the divergence between dollar and oil inventories narrow as dollar weakness persists. Given the level of geopolitical risk, prices have not moved significantly above the inventory fair value price, although the combined model would suggest a richly valued market. With inventories poised to rise seasonally and tensions seemingly easing, softer prices are more likely in the coming weeks.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EST] Good morning! It was a very quiet overnight session as markets await the signing of the Phase One deal with China. Here is what we are watching this morning:

BREAKING:Russian PM Medvedev resigned this morning along with the entire Russian government. This follows a speech from Putin in which he called on increasing the power of the PM and cabinet ministers. It is suspected that Putin, facing term limits in 2024, may opt to repeat his earlier job swap, where he accepts a newly empowered PM position and makes the presidency a ceremonial post.

However, it should be noted that trade relations are hardening outside this agreement. In what could be an important long-term move, USTR Lighthizer is pushing Japan and the EU to target China on corporate subsidies. This is a change in tenor; up until now, the U.S. has mostly engaged in bilateral actions. Lighthizer seems to recognize that “teaming up” with the rest of the industrialized world will probably have a stronger impact on the problematic issue of subsidies. This action won’t bear fruit for a long time; WTO actions are notoriously slow, which is part of the reason the Trump administration has mostly ignored the body. Nevertheless, it does create a framework for cooperation, and if this group can eventually include India it could force China to reduce or eliminate market-distorting subsidies.

Iran: We reported yesterday that Germany, France and the U.K. were planning to start the process of protesting Iran’s recent violations of the JCPOA. The three nations made it official. Iran warned that European soldiers in the region “could be in danger” after the move.

German slowdown: Germany expanded at its slowest pace in six years in 2019, expanding only 0.6%. As an export-promoter, Germany struggled to grow its economy as rising protectionism throughout the world led to a decrease in demand for exports. Additionally, auto-manufacturing, which represents a large part of the country’s exports, has also been hurt by changing regulations and a declining market. A reduction in the trade war may contribute to a more favorable environment for Germany, but it is worth noting that the president has the European Union in his sights as well.

Data: For years, the government’s data-releasing agencies (BLS, Commerce, USDA, etc.) would release its sensitive data to news organizations up to an hour before the official release. This allowed these news feeds to prepare stories and make the data available at the release time. There has always been a problem with this system; the government had to put elaborate security systems in place to prevent a journalist from leaking the reports.[1] The USDA even took to guarding the Venetian blinds in the reporter room to prevent signaling.

The Obama administration, in a bid to reduce costs, tried to end the embargo practice and make the news organizations wait like everyone else to get the data. However, the news bodies petitioned the administration and they retracted the decision. Now the Trump administration is apparently taking another swing at this action. If they follow through with this decision, government websites will be hammered with data requests as the release point nears. It isn’t hard to imagine their sites freezing up due to the demand. The bottom line is that if this path is taken there will invariably be some reports that won’t be disseminated in an orderly fashion. The pressure on government employees will also rise; traders who would benefit from an early look at the data (cue the Dukes) would likely be willing to bribe such employees. We will continue to monitor developments.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EST]

Markets are quiet this morning as earnings season begins. Trade is the biggest headline, as the U.S. and China are expected to sign a deal tomorrow. Here is what we are watching this morning:

Trade: First, the U.S. and China are expected to sign a deal tomorrow. The PRC will pledge $200 bn in new U.S. purchases; although the full details may not be released, it is generally expected that China promised to buy around $75 bn of manufactured goods, $50 bn of energy, $32 bn of agriculture and around $35 bn in services. These numbers represent purchases over two years. The U.S. won’t implement new tariffs that were signaled in September and has removed the currency manipulator label on China. Casual observation would suggest the U.S. won this round handily. It appears Beijing is sensitive to this idea; a well-connected blogger in China has taken great pains to suggest that we are early in the evolution of the trade relationship. The deal should reduce the bilateral trade deficit the U.S. has with China; however, since trade is ultimately the difference between public and private sector net saving, the deficit in these accounts invariably will lead to trade deficits with other nations. Austerity is the most effective way to reduce trade deficits; it is also the least popular.

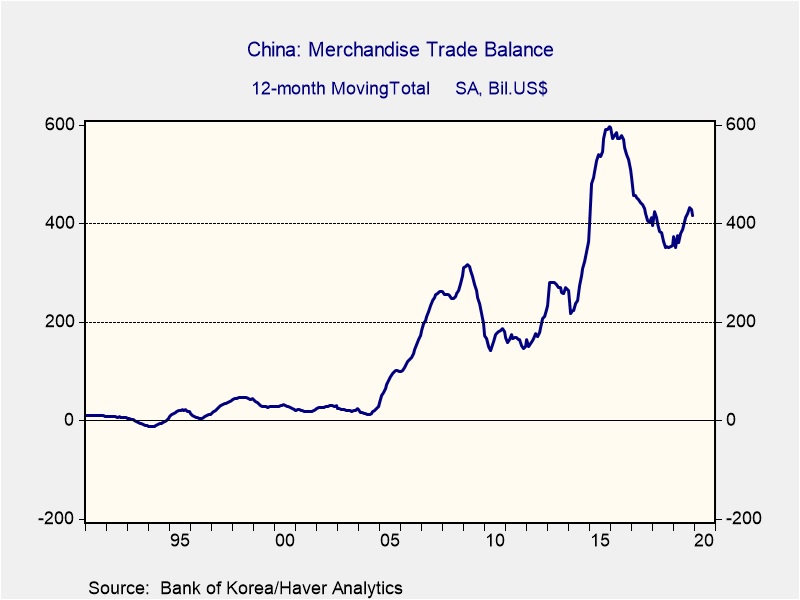

Second, China’s trade data improved in December, with exports up 7.6% and imports up 16.3% from the prior year. However, these eye-popping numbers are mostly due to base effects. Last year, trade was hurt by the early stages of the trade conflict. The overall balance was mostly flat.

Third, as the U.S./China trade situation stabilizes, the administration is likely to shift its focus to the EU. In anticipation, the new EU trade negotiator, Phil Hogan is coming to Washington this week to attempt to get ahead of any conflict. He will have his work cut out for him. The U.S. is at odds with France’s new digital tax and President Trump has targeted Europe’s car industry as a problem.

Iran: Iranian leaders are trying to cope with protests and have announced arrests of those responsible for downing the Ukrainian airliner. EU leaders have put Tehran on notice that it will reimpose international sanctions on Iran if it doesn’t return to compliance with the JCPOA. Iran has been trying to create daylight between the U.S. and Europe, with the hope of cracking the sanctions bind that the Iranian economy faces. However, those hopes appear dashed as Europe is demanding a return to the nuclear deal and Iran will still face U.S. sanctions, which have effectively cratered the Iranian economy. We expect Iran to try and limp along and hope a new U.S. president in November might offer a way out of their current crisis. However, if President Trump is re-elected, they may have no choice but to renegotiate the nuclear deal.

Canada-Iran-United States: Responding to Iran’s airliner shootdown that killed dozens of Canadians last week, Canadian Prime Minister has laid the blame mostly on the Iranian government. However, in an interview yesterday, he obliquely blamed the U.S. as well, noting that “those Canadians would be, right now, home with their families” if not for the escalation of tensions in the region. There are some signs that other high-profile Canadians are also making that connection. Only time will tell how much the incident might damage U.S.-Canadian relations, but in any case, it does show how the administration’s “America First” strategy has the potential to isolate the U.S. even from its strongest historical allies.

Ireland: Confirming reports we noted yesterday, PM Varadkar has called a snap general election for February 8. The call scuttles a 2016 parliamentary voting deal under which the opposition Fianna Fáil Party propped up Varadkar’s center-right government to ensure political stability during the Brexit negotiations.

China economic news: A couple of Chinese economic anecdotes caught our eye. First, it is no secret that China’s corporate sector is generating a rising level of defaults. Anytime a loan is made, there is a certain chance that the borrower will default. Additionally, given that China only outlawed defaults in 2014, and restricted the use of defaults until 2018, the potential for a significant level of dodgy loans from non-financial corporations in China is very high. So, the real focus should be on workouts. If there are lots of bad loans, some sort of resolution is required. In other words, who gets “stuck” with the costs of resolution? Here is one item that got our attention. Dandong Port Group, a port operator on the border with North Korea, had its business adversely affected by sanctions on the Hermit Kingdom. However, it does appear that aggressive overexpansion is mostly to blame for its debt problems. In 2017, it defaulted on $150 mm in bonds. It continued to default on other issues, eventually stopping payment on $1.2 bn in debt. In April, the firm began formal bankruptcy proceedings. The bankruptcy court has rendered its verdict. The company will be divided into two firms, one controlled by the state and the other private. The best assets will go to the state firm, which will be controlled by a state-run company. The other firm will be controlled by the private creditors. Bondholders will get CNY 300k maximum compensation (roughly, $44k) and shares in the new company. Needless to say, private creditors are not happy. What is of concern is that if this settlement becomes the norm in China, it will become very difficult for non-state firms to borrow money and given the level of corporate debt in China, rollovers will likely be necessary to avoid bankruptcies. Of course, if the goal is to increase state control, the Dandong Port settlement might be a desirable model. Second, Chinese automakers are laying off workers as car sales continue to slump.

An economic puzzle: In theory, the world trade balance should be zero. Short of trading with Mars or the Moon, a trade deficit in one part of the world is a trade surplus in another part, and taken as a whole, there should not be a global trade surplus or deficit. In reality, due to reporting errors and other factors, the world does run a trade surplus with itself. However, a recent paper uncovered that nearly 80% of that global surplus comes from the EU. The paper makes the case that fraud related to the EU’s value added taxes (VAT) is the culprit. Exports are treated differently in the EU VAT calculations, so it appears there is a systemic fraud going on were domestic sales are being treated as exports to evade taxes. Public finance experts have suggested the U.S. could adopt a VAT to increase government revenues to improve confidence in public deficit financing. However, this paper does highlight that such a move isn’t without risks.

(Due to the Martin Luther King Jr. Day holiday, our next report will be published on January 27.)

On January 3rd, the U.S. launched a missile strike that killed Major General Qassem Soleimani, the leader of the Quds Force of the Islamic Revolutionary Guard Corps (IRGC). As a high-profile commander, his death rocked the region and raised fears of a broader confrontation.

Although the situation remains fluid, Iran and the U.S. appear to have come to a point of stasis; in other words, the odds of further immediate escalation have declined. In this report, we will discuss recent events and examine the context surrounding these events. As always, we will conclude with market ramifications.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EST]

Happy Monday! Much of the U.S. is digging out of wintry weekend weather. Equities continue their grind higher. Tensions in Iran soar after the government admitted it accidently downed a Ukrainian airliner. The DPP wins big in Taiwan. The U.S./China trade deal is expected to be signed on Wednesday. Here are the details:

China trade: The U.S. and China are set to sign the Phase One trade agreement on Wednesday. Overall, there isn’t that much there. China has made promises to buy U.S. agricultural products but the numbers being discussed appear to be unworkable. China has agreed not to weaken the CNY. Although the PBOC did allow the currency to weaken last year, currency weakness runs the risk of triggering capital flight. Thus, this isn’t a major “give” by Beijing. At the same time, tariff levels on China remain elevated. We suspect the trade front will be quiet in 2020 through the election. Interestingly enough, the U.S. and China are planning to restart an Obama-era forum for regular meetings between the two countries.

Japan: With the government about to dispatch a navy unit to help patrol the Persian Gulf, a new Kyodo News poll shows 58.4% of Japanese voters are opposed to the move. Only 34.4% supported it. Not only do these numbers show how unpopular the dispatch is, but it also suggests Prime Minister Abe still hasn’t been able to swing the public toward his view that Japan should revise its pacifist constitution to allow greater military development.

Venezuela: New reporting explains an additional issue that played into the government’s ham-handed effort last week to regain control over the National Assembly by shutting out opposition leader Guaidó. To boost Venezuela’s plunging oil production and help revive the economy, President Maduro wants to turn oil operations over to foreign investors from countries such as Russia and China. To do so, however, he would need to overturn his predecessor’s law prohibiting such deals, and that requires the cooperation of the legislature. To date, it still isn’t clear whether Guaidó or Maduro’s loyalists will have final control over the National Assembly.

Austria: In an interview with the Financial Times, right-wing Chancellor Kurz said he remains committed to strict immigration controls despite needing to form a coalition with the left-wing Greens. He said the government’s top priorities would be immigration control and climate change, followed by tax cuts and efforts to spur the country’s competitiveness.

The Stormont returns: The Stormont is the capitol building of the Northern Ireland legislature. The body has been suspended for three years as Sinn Fein, which supports unification, left the government over a public spending scandal. Since then, Northern Ireland affairs have been run out of Westminster. The suspension likely hurt Northern Ireland’s interest in the Brexit process because it reduced its regional power. An agreement over the weekend will bring regional power back to Northern Ireland; a key element of the agreement was an injection of cash from London. Meanwhile, it appears that Irish voters will be heading to the polls next month as Taoiseach Varadkar had planned for new elections after Brexit. Varadkar’s government is a minority and was only able to govern due to an agreement among the parties to rule while Brexit negotiations were underway.

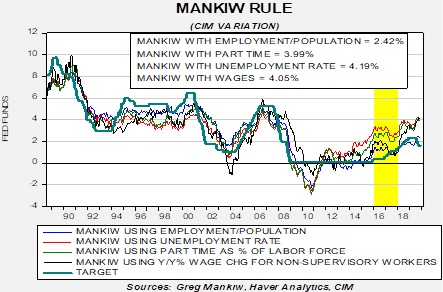

In our 2020 Outlook, we discussed three risks to the forecast, with one of them being a “melt-up” or a dramatic rise in stock prices. One of the key factors that could bolster higher prices for risk assets would be the idea that the FOMC has engineered a soft landing, which is best defined as a tightening cycle that doesn’t result in a recession.

In December 2015, the Fed raised the policy rate by 25 bps, lifting the rate from 0.125% to 0.375%. The conventional policy models, mostly based on the Taylor Rule, suggested that a series of rate hikes was likely.

This chart shows four variations of the Mankiw Rule, which is different from the Taylor Rule in how it measures slack in the economy. The former used the unemployment rate, while the latter uses the difference between actual and potential GDP. We prefer the Mankiw Rule because labor market measures are easily observable, whereas potential GDP is not. We have created four variations of the Mankiw Rule using various measures of the labor market. In the chart above, the area highlighted in yellow shows that all the Mankiw variations were suggesting the policy rate was too low and the Fed needed to raise rates aggressively. The financial markets feared tighter monetary policy but, as the chart shows, after an initial hike the Yellen Fed paused for a year before raising rates again.

Why did this pause occur? A contributing factor appears to be fragility in the financial markets.

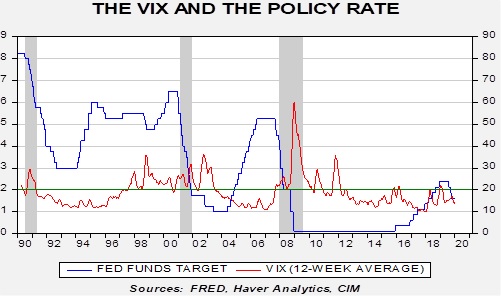

This chart shows the 12-week average of the VIX index of S&P 500 volatility and the fed funds target. Note that the VIX rose above 20 with the rate hike in December 2015. It is possible the FOMC worried about triggering broader financial problems by raising rates and thus paused to allow financial markets to “calm down” before raising rates further.

In the recent tightening cycle, the Powell Fed raised rates until the VIX broke 20; soon after, the Fed lowered rates even though the Mankiw Rules would suggest further tightening was in order. The Fed would be loath for the financial markets to conclude there is a “Fed put,” but, given how sensitive consumption has become to asset values, avoiding a recession may require guiding policy to prevent volatility from rising.

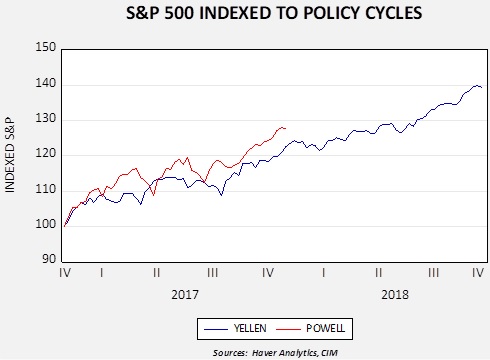

So, if this is what the Fed is doing, what does it mean for equities? We indexed the S&P 500 to early February 2016, when it became clear that Yellen would keep policy on hold, and January 2019, when Powell signaled at least a pause in tightening. The idea is that equities should benefit if the Fed avoids a “hard landing.”

The two periods are generally tracking each other; if this pattern continues, the current S&P 500 would end up at 3532.56 by late November. This analysis is clearly not foolproof as one episode of a soft landing won’t necessarily generate a repeat performance. Nevertheless, we are tracking relatively closely so further gains in stocks are possible if a recession is avoided. The trick is avoiding recession; accommodative monetary policy is probably a necessary, but not completely sufficient, condition for avoiding a downturn.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EST]

Happy employment day Friday! We cover the data in detail below, but the quick take is that the data is a bit soft as nonfarm payrolls rose by only 145k, less than the 165k forecast. The big news was a plunge in non-supervisory worker wages, mostly due to base effects from minimum wage laws enacted last year. In other news, it appears Iran shot down the Ukrainian airliner. Brexit passes. Strikes continue in France. Taiwan’s elections. Here are the details:

Ukraine airliner: Evidence is mounting that the downed Ukrainian airliner was hit by a surface-to-air missile launched from Iranian territory. The suspected weapon, SA-15, is a Russian-made system that uses a mobile launching platform. Simply put, this isn’t the kind of weapon that is used by proxy groups. In Iran, this system is managed by the Islamic Revolutionary Guard Corps (IRGC). Iran is disputing the evidence and has expressed willingness to turn over the black boxes to foreign governments for analysis. The current consensus of opinion is that Iran likely made a mistake; in the current environment, it is likely that Iranian air defense personnel were anxious about potential retaliation and thought the civilian aircraft had hostile intent. It is unclear how this incident will play out but, if the Malaysian Air Flight 17 offers any insight, not much will occur.

Brexit passes: In rather anticlimactic fashion, the Brexit bill passed the House of Commons 330-231; the bill now moves to the House of Lords where it will pass and become law. From this point, the focus will be on the trade negotiations. The early look from Michel Barnier is that talks will be difficult. The EU will do everything it can to prevent the U.K. from becoming a “Singapore on the Thames,” forcing Britain to accept EU regulations. We expect London to push back on this position. Our take is that the two sides will come up with a deal but not in 12 months; however, an extension won’t be a market-moving event.

Taiwan elections: Beijing will be watching this weekend’s elections in Taiwan closely; a big win for the DPP would suggest that tensions in Hong Kong have swayed opinions on the island that the PRC believes is a breakaway province. In fact, China is doing more than watching—it is actively trying to affect the outcome of the vote. We are watching to see how effective their measures are because we would not be surprised to see similar actions tried in the U.S. elections.

France: Transportation workers extended their strike into the sixth week, making it the longest labor action in French history. Workers are concerned about President Macron’s plans to reform the country’s convoluted pension system. Although it is generally acknowledged that reform is needed, workers don’t trust the president and fear that “reform” will mean longer working lives and less money for retirement.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.