by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EST]

It has been a very busy three days. We update the COVID-19 news. Risk assets reacted favorably to Friday’s press conference at the White House. However, we are not seeing any follow-through today; global equities are lower and bond yields are down across the board. Gold continues to sell off. The Fed moved aggressively, cutting the policy rate and opening QE4. Other central banks are following along. Here are the details:

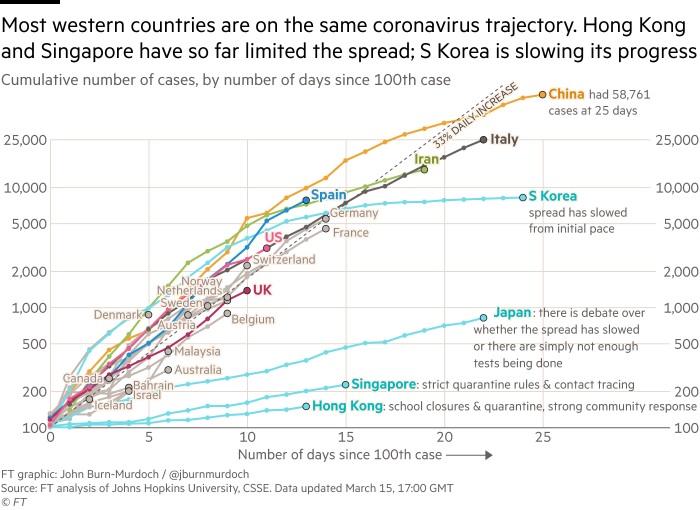

Assuming the U.S. continues to track Italy, cases will be up to 25k in a week or so. Here are some bullet points for today:

The U.K.’s natural experiment may be ending: The Johnson administration was bucking the trend of most Western nations by not ordering gathering places to close. The idea was that the virus can’t be contained anyway, so instead the government allowed movement to take place. As infections rose, a “herd immunity” would develop faster. For the population under the age of 50, this policy arguably makes sense. Most younger people are not threatened by the disease. However, for those over 60 it could be deadly. His government is rethinking the policy.

As economic data from China rolls out, the impact is stunning. Industrial output fell 13.5% for January and February compared to a year earlier. Retail sales plunged 20.5% for the same period and fixed asset investment dropped 24.5%.

We will have much more to say on the virus and other issues in the next day or so; an update to our 2020 Outlook is coming soon. Suffice it to say, the odds of recession have increased dramatically in recent days and may be unavoidable.

The Fed: In a surprise move, the FOMC decided to skip the formalities of Tuesday and Wednesday’s meeting and cut to the chase. It cut the policy rate of a range of 0% to 0.25% and announced QE4 by planning to purchase $700 billion of Treasury and mortgage paper. Specifically, it plans to buy $500 billion of Treasuries and $200 billion of mortgage-backed securities; this will take the balance sheet to over $5.0 trillion. In addition to these measures, the Fed reduced the discount rate to 25 bps and encouraged banks and primary dealers to use the window. Using the discount window mechanism would help support liquidity issues in the repo market. It also reduced the reserve requirement ratio to 0%. The FOMC also lowered prices on dollar swap rates with other central banks in a bid to reduce global liquidity issues. It is not clear in the statement how quickly the Fed intends to increase its balance sheet. There was one dissenter: Cleveland’s Loretta Mester opposed the rate cut but did support the other policy actions. The Fed did have “friends” as other central banks took action as well.

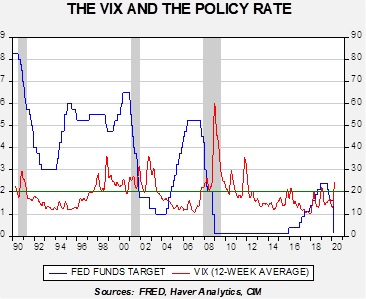

The Fed continues to guide policy based on financial risk. We note that the policy rate tends to be cut when the 12-week average of the VIX rises above 20.

The question now is, “what’s left?” There are two other directions the Fed could take. Currently, it cannot buy assets other than Treasuries or mortgages. It could ask Congress to buy other assets, e.g., corporate bonds, and perhaps equities. Or, it could consider buying foreign bonds, which would weaken the dollar. We do note the dollar fell on the move to ZIRP and a weaker dollar should support net exports. For the time being, monetary policy is mostly exhausted.

What about fiscal policy? This is the next line of defense. We are starting to see a consensus among both conservative and liberal-leaning economists on the wisdom of direct payments to households. Sending money directly was done in Hong Kong recently and tax rebates in the U.S. were implemented by the Carter administration. The worry is that political divisions will prevent actions from being taken. We suspect that direct action will likely occur but only after conditions deteriorate further.

Our baseline position has been that the COVID-19 virus would have a significant impact in terms of magnitude but be of limited duration and thus would probably not put the economy into recession. Over the past week, two events have occurred which put this position into question. The first is the oil market collapse triggered by a market share war between Russia and Saudi Arabia.[1] The second issue is that the financial system is exhibiting symptoms of liquidity problems.

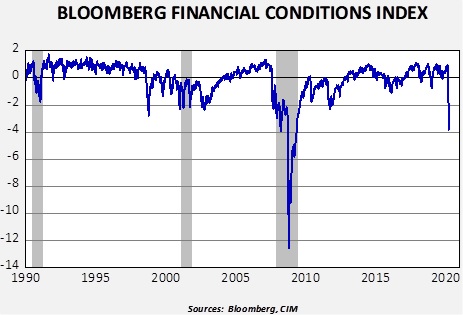

We have noted a sudden decline in financial conditions as measured by the Bloomberg Financial Conditions Index for the U.S.

Our data uses the Friday closes for the index. The index is composed of eight variables[2] which are standardized and totaled. The more negative the reading, the greater the level of financial stress. The index was positive until the last week of February. The current level of stress is about on par with March 2008 during the collapse of Bear Stearns.

This data suggests a serious level of financial problems in the financial system. We have noted difficulties in the funding markets since September. Although the Fed has consistently claimed there was nothing systemic in the rise of repo rates, the persistence of the funding shortages despite the expansion of the Fed’s balance sheet by $400 billion argues otherwise.

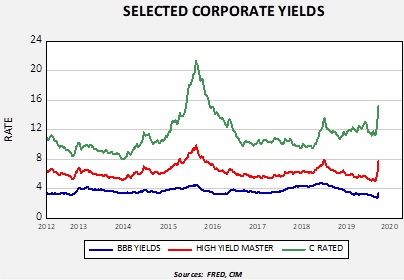

What is the nature of the financial stress? Its roots most likely lay with interest rates being too low for too long; investors had to extend their portfolio risk to find attractive yields. The financial services industry took steps to provide financial products with more attractive yields. Some of this product creation went to the non-bank financing system which funds itself in the repo markets. If repo markets are disrupted, they can no longer service the debt they used to own the higher yielding assets and liquidations occur. If no liquid market exists for these products, the owners may be forced to sell other assets (gold, Treasuries, equities, investment grade bonds) to find necessary liquidity. Recent weakness in “risk off” assets would tend to confirm rising levels of financial stress. A contributing factor is the plunge in oil prices, which raises default risk among energy companies.

The Federal Reserve should be able to corral this problem if it moves aggressively enough to force liquidity into the financial system. Unfortunately, as we saw in 2008, it may be difficult to pinpoint exactly where the funding problems lie. But, the key lesson from 2008 is that enforcing moral hazard is a bad idea; we doubt such a policy will be executed in this event. Although a few of our economic indicators have moved to signal recession, the preponderance have not. On the other hand, the yield curve did invert last year, and we have been on “recession watch” for some time.[3]

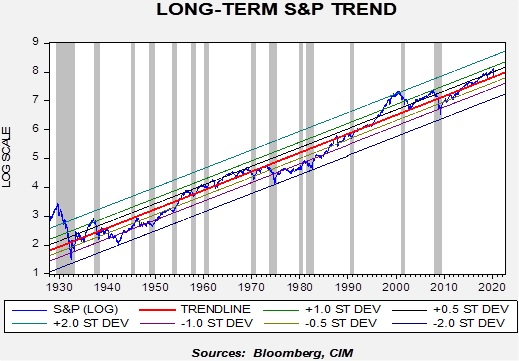

How does all this affect equity markets? The chart below can offer some guidance. This chart shows the weekly close of the S&P 500 going back to late 1927. We log-transform the index and regress a time trend through the data. The parallel lines represent various standard error levels from trend; the gray bars show recessions. It is obvious that, with the exception of 1945, every recession has led to some degree of stock market weakness.

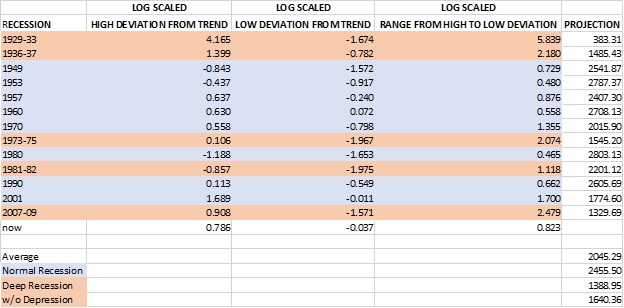

To compare recessions, we measured the high reached before the recession to the low in the index during the downturn in terms of movements in standard errors. Here is a table of the events.

Range represents the change in standard error from high to low. So, the Great Depression saw the market fall nearly six standard errors, a true “six-sigma” event. The current decline is consistent with a normal recession, so if policymakers can secure the financial system and absorb the quarantine effect of COVID-19, then equity markets should stabilize soon. A deep recession (but not including the Great Depression) would put the S&P 500 around 1640, a much more profound decline.

The postwar experience doesn’t support two consecutive deep recessions, which is why we have argued that another 2008 is unlikely. Of course, we did have consecutive deep recessions in the 1930s: the 1936-37 recession was caused by profoundly inept policy when the Roosevelt administration tightened fiscal policy while the Federal Reserve raised rates. The odds of a similar event occurring in the current situation is improbable; both fiscal and monetary policy are accommodative and will almost certainly become more so. About the only way we have a deep recession is if the policy response is strikingly underwhelming. Although possible, that is a low probability outcome.

So, the bottom line is that we will likely see a few weeks of churning and perhaps a decline toward 2300, but the worst of this downturn is probably over. Liquidity injections and the natural waning of COVID-19 should improve sentiment over time. We are probably very close to the low in terms of price but not in terms of time. It will probably take a few weeks of basing before a durable recovery can develop.

[2] TED spread, LIBOR/OIS spread, commercial paper/T-bill spread, Baa/10-year T-Note spread, Muni/10-year T-Note spread, swap volatility, the S&P 500 and the VIX. There are other similar indices with a larger set of variables, but the Bloomberg variation is calculated daily, whereas the others are calculated weekly or monthly.

[3] Hence the title of our outlook for 2020, “Storm Watch.”

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EST]

Happy Friday the 13th! Let’s not bury the lede—equities are enjoying a strong recovery this morning after a historic decline yesterday. Europe is lifting as well. As is our usual practice, we update news on COVID-19. We also discuss how the virus crisis is rapidly revealing financial turmoil. Here are the details:

Relations between the U.S. and China are taking a dark turn. Chinese social media is swirling with rumors that COVID-19 came from the U.S. The reports came from China’s foreign ministry and have not been discouraged by Chairman Xi. In response, the White House and members of Congress are firing back. The notion that this virus started in the U.S. is patently silly; China is the fount of viruses such as coronavirus and influenza due to its geography. It lies in the temperate zone where migratory birds move. These viruses fester in wildlife and occasionally cross the species to become a problem for humans. The CPC’s propaganda machine is clearly trying to divert attention, but these attempts will weaken already frayed relations.

Overall, the virus continues to spread. The pattern that has emerged suggests the U.S. has a couple more weeks of rapidly rising cases before the growth rate begins to taper.

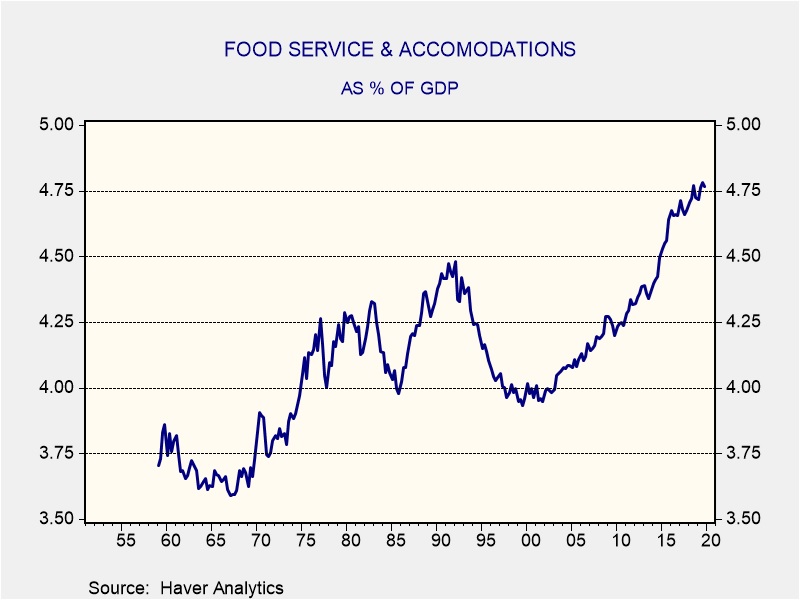

Financial concerns: In this week’s Asset Allocation Weekly (AAW; see section below, p.7), we make the case that the chances of recession have increased to probably 80%. We still haven’t seen confirmation from most of our data signals, but we expect the signals will be forthcoming. Thus, we aren’t certain, but it is probably safe to assume that there is at least a 4/5 chance of a downturn. What has happened here is that the economy has succumbed to three problems. First, the disruptions from COVID-19 will weaken consumption; as we noted in our Outlook 2020 report, GDP growth has become extraordinarily dependent on consumption so it will be hard to maintain positive GDP growth under measures being taken to isolate the virus. Second, the Saudi/Russia oil war will dampen demand in the oil patch and further weaken growth. The third head of this hydra that has emerged is what appears to be liquidity problems in the financial system. As the chart in the AAW shows, the Bloomberg Financial Conditions Index is at levels last seen when Bear Sterns collapsed. Evidence of stress has been surfacing in recent days. Spreads in the Treasury market have widened, suggesting that those holding the paper are not willing to lend it to those who need the collateral. Credit default swap rates have soared.

Central banks are responding to the immediate crisis. We had a brief respite to equity selling yesterday when the Fed announced a massive $1.5 trillion injection of liquidity to ease problems in the repo market. The ECB responded as well, although Legarde disappointed the market, which was hoping for a “whatever it takes” approach. Her comment of “I am not here to close rate gaps” was a rookie error. Other central banks have moved as well. The Bank of Canada expanded its bond-buying and repo operations. The BOJ added liquidity ($19 billion). The PBOC cut reserve requirements. The Bank of Norway cut rates, and the Riksbank injected liquidity. The BOE says it will continue to support markets. There is action on the fiscal front as well. The House leadership, working with Treasury Secretary Mnuchin, have put together a fiscal package. We will be watching to see how the Senate responds.

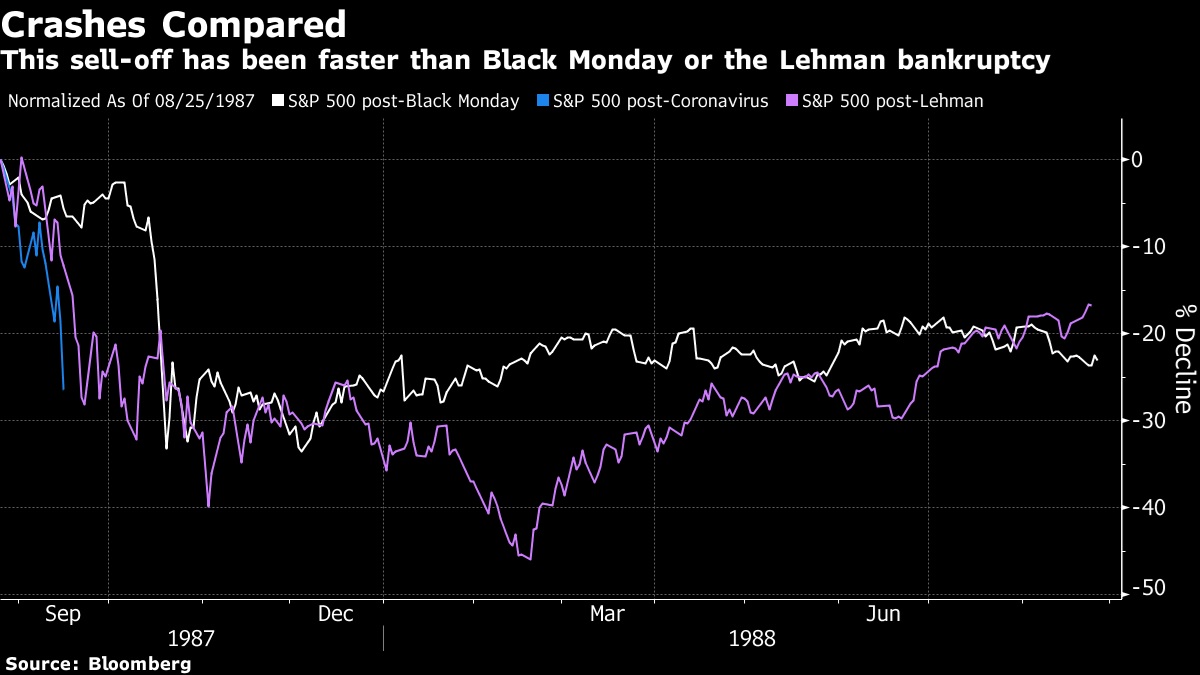

Although today’s recovery is obviously welcome, the most likely outcome for the next several weeks is a choppy basing process.

This chart shows how the S&P responded to 1987 and post-Lehman. It suggests a long period of basing. We discuss our views on the path of equities in this week’s AAW below.

So the bottom line is that this expansion has probably come to an end due to the combined impact of COVID-19, the oil market share war and financial fragility.

Conflict in the Middle East: On Thursday, the U.S. conducted airstrikes against an Iran-backed militia. The airstrike was in response to a rocket attack that killed two Americans soldiers and a British service member earlier this week. This was the first attack from the U.S. since the drone strike that killed Qassem Soleimani, and the Pentagon has warned of possible additional actions.

If we follow the general trend seen elsewhere, we will be at 8k to 10k cases by the third week of March. The U.S. currently has 1,323 cases. The experience seen overseas suggests exponential growth in infections in the coming days. We note that Dr. Brian Monahan, the attending physician for Congress, warned lawmakers that 70-150 million (yes, millions) of Americans will be infected. However, he didn’t give a time frame, so this headline may not be as dire as its seems. And, in behavior similar to bond rating agencies, the WHO has declared a pandemic.

Not what we were looking for: The president held a rare address to the nation to announce measures to counter COVID-19. The speech began at 8:00pm EDT. This chart of the overnight S&P 500 futures shows the reaction.

(Source: Barchart)

The financial markets were looking for “shock and awe.” They wanted to see payroll tax holidays, grants to households, loans and lots of spending. They got a travel ban from Europe, a tax deadline delay and talk that something might be coming. In fact, the speech initially suggested that air cargo trade with Europe would be halted; that had to be clarified. Needless to say, it didn’t go well. What we are experiencing is why Western democracies have shied away from fiscal policy and relied on monetary policy for the past 40 years; in a polarized political environment, getting fiscal policy done is nearly impossible. It is important to note that the first time TARP was put before the House it was voted down. It was only when conditions were spiraling into another Great Depression that Congress acted. The House Democrats have introduced a package of measures which mostly focus on households. The proposal includes food assistance and sick leave pay. There isn’t much help for businesses at this point, although industries being hit will likely, at some point, get relief. We do expect the White House and Congress to get something together in the coming weeks but, if history is any guide, it will only happen when conditions deteriorate further. Meanwhile, pressure on the Fed is mounting; there is increasing talk that the policy rate will fall to zero.

Iraq: A rocket attack at Camp Taji killed two U.S. soldiers and one U.K. soldier. It isn’t certain who was responsible for the attack; however, a similar attack in January led to the counterattack that killed Iranian Gen. Qassem Soleimani. Given the current situation, we are not sure we will see a similar level of retaliation to this attack.

Energy update: We are now updating our weekly energy recap from the DOE in a separate document published on our website, the Weekly Energy Update. Going forward, we will be linking to the report here after the data is released.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

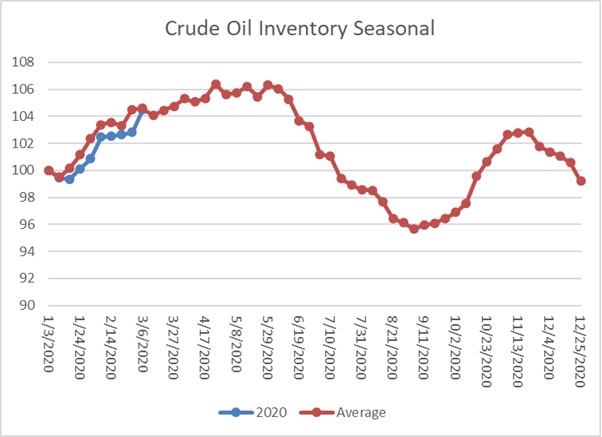

Crude oil inventories rose 7.7 mb compared to the forecast rise of 1.7 mb.

In the details, U.S. crude oil production fell 0.1 mbpd to 13.0 mbpd. Exports fell 0.7 mbpd, while imports rose 0.2 mbpd. The inventory build was more than forecast due to falling exports and rising imports.

(Sources: DOE, CIM)

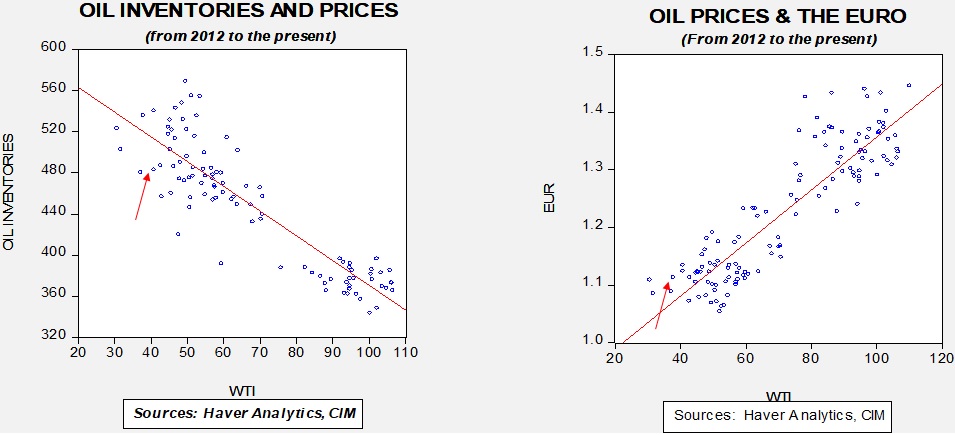

This chart shows the annual seasonal pattern for crude oil inventories. This week’s report rose to seasonal norms. Inventories will be expected to rise steady into late May. We will be watching the above chart closely in the coming weeks for signs that inventories are rising abnormally due to the market share war described below.

Based on our oil inventory/price model, fair value is $56.46; using the euro/price model, fair value is $53.22. The combined model, a broader analysis of the oil price, generates a fair value of $53.57. The model has lifted its fair value calculations due to dollar weakness; however, under current circumstances, the model output is less relevant unless Russia and the Kingdom of Saudi Arabia (KSA) come to an agreement on supply.

The big news in oil is the market share war that has emerged from the recent OPEC+Russia meeting. The KSA was unable to convince Russia to contribute to supply restrictions and Riyadh has announced an all-out supply war. Prices plunged this week in response.

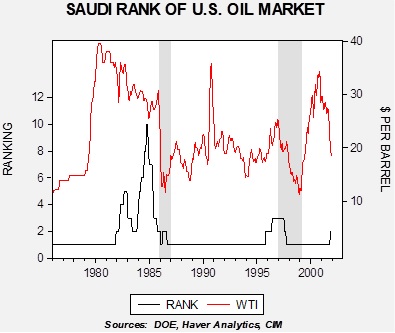

The following two charts show the KSA’s thinking. The Saudis have, in their history, had one market they keyed on where they wanted either to be the largest or second largest supplier. In the 1970s through the 1990s, that market was the U.S. There were two reasons for this. The U.S. was the largest importer of crude oil and provided security for the KSA. Thus, the kingdom did not want to lose share in the U.S. because (a) it was the most important market in the world, and (b) it feared the U.S. would view providing security as less critical if the KSA was seen as less important. During two previous market share wars, in 1986 and 1997-99, the loss of share was a triggering event. The chart below shows WTI along with the Saudi rank as foreign supplier to the U.S. market. The gray bars are designated as market share wars.

Until 1986, the KSA acted as “swing producer” for OPEC.[1] This led to a near-catastrophic loss of market share in the U.S. In December 1985, the KSA signaled it was abandoning the swing producer role and would retake market share. Oil prices fell from the low $30s to near $10 per barrel before the rest of OPEC capitulated and agreed to output cuts. In the mid-to-late 1990s, the KSA was losing market share in the U.S. to Venezuela, which had invited foreign company oil investment in order to boost output capacity. The KSA retaliated with supply increases into the Asian Financial Crisis. Prices fell from the mid-$20s to near $10. The war ended when Venezuelan President-elect Hugo Chavez signaled an end to the supply war, eventually ending the policy of using foreign investment to lift capacity. Prices rapidly recovered.

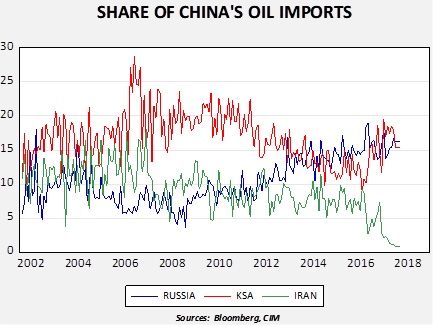

This time around, the U.S. is not the target of the KSA. The U.S. has made it clear that it is reducing its security footprint in the Middle East and, with the onset of shale production and a “captured” Canadian oil market,[2] the KSA can’t really defend its U.S. share. Instead, it has staked its future on rising Chinese oil demand, and likely hopes that, at some point, it will be able to receive security support from China as well.[3] Therefore, the KSA is committed to be the preeminent oil supplier to Beijing. Russia is threatening that position.

This chart shows the share of China’s oil imports from the KSA, Russia and Iran. From 2006 to 2012, the KSA held a dominant share. But, since 2014 (when the KSA reversed its policy on trying to drive down shale oil production via lower prices), Russia’s share has been competing with the KSA.

So, given this background, how do we expect this to play out? Most OPEC nations are rentier states; they use revenue from oil to support government spending. In addition, these nations tend to suffer from the “Dutch disease,” a condition where a commodity export tends to boost exchange rates, making domestic industries less competitive. This process tends to lift imports and consumers become used to low-priced goods from abroad. As a result, currency depreciation tends to be politically unpopular. When the KSA fought for market share in the past, its competitors tended to avoid currency depreciation, which is an effective buffer to the costs of the market share war. In other words, a foreign oil company sells its product for dollars but pays its workers in local currency. If the currency depreciates, then its production costs compared to output prices decline. Russia has shown a tendency to depreciate the RUB when oil prices decline. The next chart shows that tendency.

This chart shows Brent crude oil prices and the RUB/USD exchange rate (inverted scale). Note that as oil prices decline, the RUB falls with it. If Russia engages in similar behavior, it will give it more “staying power” in the share war.

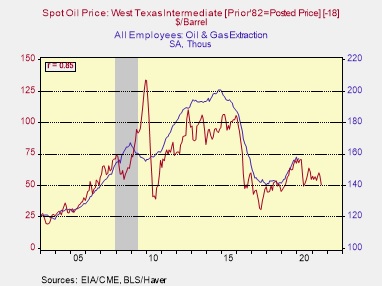

How much will this event affect employment? In the oil patch, it will be signficant.

Assuming we see $25 WTI, we will likely see nearly 40k jobs lost in oil and gas extraction. But, as the chart shows, it will take about 18 months to occur.

The bottom line is that this share war will likely get rather ugly. The KSA is pushing supply into the world market and it has no place to go. The U.S. oil industry will suffer greatly, but production probably won’t start to decline until autumn, when price hedges will likely roll off. Iran will also be crushed by this move; the little oil it is selling will fall dramatically in price. We look for prices to fall into the low $20s in the coming months.

[1] A swing producer adjusts output to fix a price.

[2] Canada’s pipeline system is limited, so most of its output ends up in the U.S. market. This means, at least in terms of the oil market, that Canadian production can be thought of as U.S. supply.

[3] This is a bit of a pipedream. Although China’s military is growing rapidly, it is still years away from being able to project power beyond its borders.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EST]

On this day in 1918, the first cases of Spanish influenza were reported in Ft. Riley, Kansas. How ironic it is that we’re now dealing with another big epidemic, though there is still no indication that it will be a mass killer like the Spanish flu. As always, below we provide an update on COVID-19, its economic impact and the evolving policy responses. We also discuss the escalating Saudi-Russia oil price war and the results of yesterday’s primary elections.

COVID-19: Official data show confirmed cases have risen to 121,061 worldwide, with 4,368 deaths and 66,216 recoveries. New cases continue to slow in China, but the epidemic is accelerating elsewhere. In the United States, confirmed cases rose to 1,039, with 29 deaths and eight recoveries. In the hot spot around Seattle, authorities say COVID-19 has now spread to at least 11 elder care facilities; at least three have reported fatalities. Separately, New York Gov. Andrew Cuomo called out the national guard to help set up a “containment area” in a New York City suburb that has had a rash of cases. Residents will be free to walk around the three square mile area, but significant public gatherings will be banned for two weeks. Illustrating one important way the epidemic could impact the political process, former Vice President Biden and Vermont Sen. Bernie Sanders canceled campaign rallies yesterday on concerns about spreading the virus. Across the pond, even Britain’s junior Health Minister Nadine Dorries has been diagnosed with COVID-19, less than a week after she attended a reception with Prime Minister Johnson. In South Korea, a new cluster of infections discovered at a call center led to a surge in new cases that ended a four-day string of declines. Italy had its deadliest day of the crisis, with its death toll rising by 168 to a total of 631 dead.

Fiscal Policy Response. Precisely as we warned in our Comment yesterday, the administration’s Tuesday discussions with congressional leaders regarding an economic support package fell flat as both Republican and Democratic legislators apparently want to focus on smaller, more targeted measures instead of broad measures like a payroll tax cut. For Democrats, that may be because of a perception that the White House is overreaching. Reports say President Trump has privately floated ideas ranging from eliminating the payroll tax permanently to offering massive tax cuts to the oil and gas industry. For Republicans, the resistance seems to be rooted in ideological antipathy for big government programs to support the broad working class. In any case, we suspect the pushback against the program is a key reason for the weakness in stocks this morning. Still, we note that Democrats in the House reportedly are preparing to propose some targeted measures as early as Wednesday in order to start the ball rolling before Congress starts a one-week break on Thursday. In terms of administrative action, sources say the Treasury Department is also likely to extend this year’s April 15 tax filing deadline.

In a video call with EU leaders, ECB Chief Christine Lagarde urged a stronger, more coordinated fiscal response across the Eurozone. A prominent group of German economists also urged Chancellor Merkel’s government to abandon its commitment to a balanced budget in order to boost the COVID-19 fight.

Oil market: In a further escalation of the oil price war with Russia, the Saudi government said it would boost its crude production capacity to 13 million barrels per day from 12 million previously. The announcement has put additional significant downward pressure on oil prices so far today. However, as the threat of lower oil prices continues to suggest reduced U.S. shale drilling, investors are realizing that would likely also cut natural gas production (often a by-product of oil output). Natural gas prices have therefore surged in recent days.

Super Tuesday II: In yesterday’s Democratic primary elections, former Vice President Biden again put in a strong showing with convincing wins over Sen. Sanders in Michigan, Missouri, Mississippi and Idaho. The race in Washington State is too close to call at the moment. Based on current estimates of how many pledged delegates each candidate has won, we estimate Biden would only have to win 46.8% of the remaining delegates to lock up the party’s nomination on the first vote at the summer convention. That suggests Sen. Sanders could well drop out in the coming days. By removing the threat of Sanders-style “democratic socialism,” such a move would likely be positive for equities. Just as important, Biden seems to be forming a broad, durable coalition consisting primarily of African Americans, white suburbanites and older voters. That coalition would likely be potent in much of the Midwest and South. In other words, Biden is positioning himself to be a strong rival to President Trump in the November elections. If momentum keeps swinging toward Biden, we would look for many foreign leaders to push back stronger against Trump’s foreign and trade policies on hopes of waiting him out until January.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EST]

Happy Tuesday! The markets are looking better than yesterday, largely based on signs that the White House has swung behind the idea of significant fiscal measures to offset the negative impact of the COVID-19 panic. We update the latest news on the coronavirus and discuss prospects for the relief package. Separately, the oil price war between Saudi Arabia and Russia is intensifying, though crude is for now being swept up in the positive sentiment about the fiscal response to the coronavirus.

COVID-19: Official data show confirmed cases have risen to 115,855 worldwide, with 4,087 deaths and 64,046 recoveries. In the United States, confirmed cases rose to 755, with 26 deaths and 8 recoveries. However, the data continue to suggest the epidemic is peaking in China. The country reported only 19 new cases today, and President Xi finally visited the epicenter of the outbreak in Wuhan and claimed “victory is near.” That’s consistent with our view that the outbreak may follow a roughly two-to-three-month cycle when it hits a country. With the epidemic apparently peaking in China, attention will now focus on the accelerating outbreaks in other countries. The WHO now says the COVID-19 outbreak is “very close” to becoming a pandemic. All the same, the two-to-three-month cycle would suggest those outbreaks could slow dramatically by late April, even if the impact on the economy and economic data extends into early summer.

Fiscal Policy Response. In a statement yesterday, President Trump said administration officials will meet on Tuesday with Republican leaders in Congress to discuss coronavirus economic measures. He said a news conference on Tuesday afternoon will include the announcement of “major” steps like a cut in payroll taxes, financial support for hourly employees who can’t work and loans for small businesses. That news has given risk assets a strong boost so far this morning. However, since Trump didn’t discuss broader steps and some congressional Republicans previously pushed back against early action, we think there is a risk that the total package ultimately won’t satisfy the markets. Besides, if the Republicans can’t resist the temptation to pepper any required legislation with measures inimical to the Democratic majority in the House – such as draconian new regulations on immigration or immigrants – passage through Congress could be delayed or stopped. Another issue to watch is any risk that President Trump himself might be exposed to the virus. Trump was reportedly in contact with two congressmen who later went into self-quarantine because of previous contact with a coronavirus patient, and at a news conference following Trump’s statement, officials were either unwilling or unable to say whether Trump has been tested for infection. Separately:

Stock Market Action. Stock selling was brutal and merciless around the world yesterday, but in the key U.S. market it still wasn’t quite enough to produce a bear market in terms of the broad indices. At market close, the S&P 500 price index was down 18.9% from its record close in mid-February. All the same, if today’s nascent rebound doesn’t hold, the index could easily fall below the 2,708.92 level that would officially mark a bear market and put an end to the bull market that began back in early 2009.

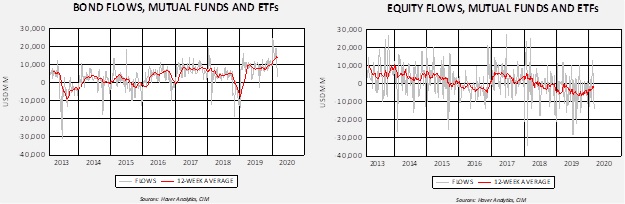

One saving grace is that retail investors have been cautious ever since the late-2018 correction. Although the data are volatile, the charts below show a net inflow of funds into bond mutual funds and ETFs during 2019, along with net outflows from stock funds. Since retail investors were already cautious going into the current downturn, the usual negative impact of a major decline in equities may not be as pronounced this time around.

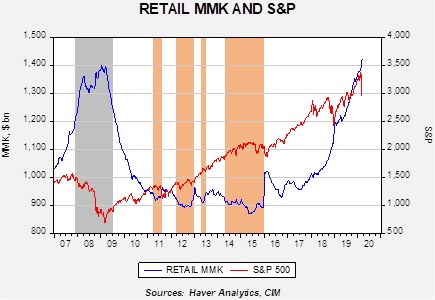

Another saving grace is that retail money market fund assets have now risen above $1.4 trillion, as shown in the chart below. There has also been a big rise in fund assets as a share of stock market capitalization (not shown). Either way you cut it, there seems to be sufficient fuel to support a strong recovery in equities if investors see the kind of fiscal shock and awe they’re looking for.

Bond Market Action. With equities looking set to enter a bear market, government bonds continue to surge. The yield on the benchmark 10-year Treasury dropped to a record low close of 0.50%. Market indicators continue to suggest investors are looking for the Fed to cut its benchmark fed funds rate by about 0.75% and for inflation pressures to crater for some time to come, giving a big bid to longer-term obligations.

Oil Market: In a dramatic escalation of its price war with Russia, the Saudi government said it will boost its oil supply to 12.3 million barrels per day (bpd) by next month. That would be 2.5 million bpd above its recent supply, and 300,000 bpd above its previously declared maximum production (suggesting the Saudis will release supply out of inventory). Russian Energy Minister Novak responded with a threat to boost Russia’s oil supply by 500,000 bpd. By itself, the Saudi effort to inflict maximum pain on Russia and force it to agree to production cuts would be bearish for oil prices. However, traders today are more focused on signs of fiscal measures to tackle the COVID-19 panic; thus, prices so far this morning are rebounding.

United States: In what’s being called “Super Tuesday II,” primary elections are being held in six states today. In the key Democratic Party contests, the largest number of convention delegates at stake are in Michigan and Washington. Also voting are Missouri, Mississippi, North Dakota and Idaho. If former Vice President Biden polls well against Vermont Sen. Bernie Sanders and his “democratic socialist” message, the results could be reassuring and positive for stocks tomorrow.

Since January, the world has been dealing with the COVID-19 virus, a new coronavirus that has been spreading around the world. Because this situation is still evolving, it is too early to determine the overall impact of this specific virus. We update our views on COVID-19 regularly in our Daily Comment report.

In this report, we will examine the general geopolitical consequences of pandemics. We will start with a broad description of pandemics. From there, we will discuss the key problem facing policymakers, how to create the proper response to such events. An analysis of the impact on social and economic conditions will follow. As always, we will conclude with market ramifications.

What is a Pandemic?

To define a pandemic, it makes sense to define the stages before a disease reaches that category.

Sporadic: This is a disease that occurs infrequently and irregularly. An occasional case of polio or measles that doesn’t spread would fall into this category. It usually doesn’t require a policy response.

Endemic: This is a disease that is constant or has usual prevalence within a specific geographic area. Annual influenza would be an example.

Epidemic: This is a disease that shows a sudden and large increase in infections within a specific area.

Pandemic: This is an epidemic disease that spreads to a wider geographic area.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.