Author: Rebekah Stovall

Bi-Weekly Geopolitical Report – The 2023 Mid-Year Geopolitical Outlook: The Polycrisis (July 10, 2023)

Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA | PDF

As is our custom, we update our geopolitical outlook for the remainder of the year as the first half comes to a close. This report is less a series of predictions as it is a list of potential geopolitical issues that we believe will dominate the international landscape for the rest of the year.

We have subtitled this report “The Polycrisis” to reflect the complicated and multifaceted geopolitical world that is rapidly evolving. The number of issues we cover here is much greater than our usual mid-year update, but we felt that all these matters were important enough to mention. They are listed in order of importance.

Issue #1: Russian Political Instability

Issue #2: Ukraine’s Military Prospects

Issue #3: China Navigating Great Power Relations

Issue #4: China’s Youth Unemployment

Issue #5: China’s Debt Problem

Issue #6: U.S. Superpower Status and Fracturing Domestic Consensus

Issue #7: Re-Industrialization

Issue #8: Climate Change and Great Power Competition

Issue #9: The Problem with Mexico

Issue #10: Artificial Intelligence

Issue #11: EU vs. Poland and Hungary

Issue #12: Middle East Realignment

Issue #13: Iranian Nuclear Breakout

Issue #14: Emerging Market Debt

Don’t miss our accompanying podcasts, available on our website and most podcast platforms: Apple | Spotify | Google

The podcast episode for this particular edition is posted under the Confluence of Ideas series.

Weekly Energy Update (July 6, 2023)

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA | PDF

Despite OPEC+ promises to cut production, oil remains in a $67 to $74 per barrel trading range.

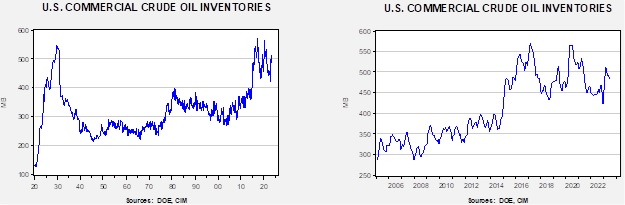

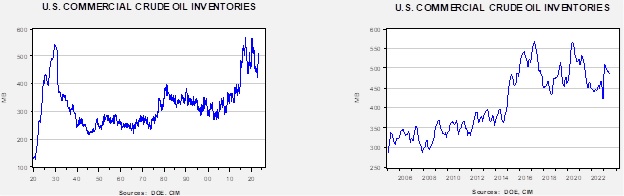

Commercial crude oil inventories fell 1.5 mb, which was on forecast. The SPR fell 1.5 mb, putting the total draw at 3.0 mb.

In the details, U.S. crude oil production rose 0.2 mbpd to 12.4 mbpd. Exports fell 1.4 mbpd, while imports rose 0.5 mbpd. Refining activity declined 1.1% to 91.1% of capacity.

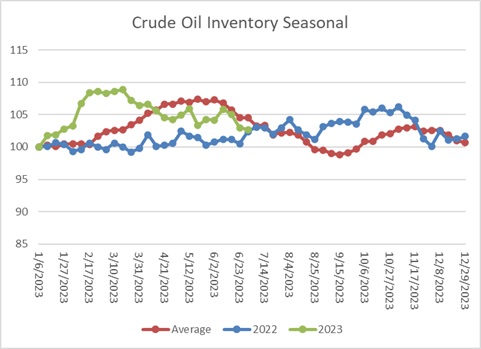

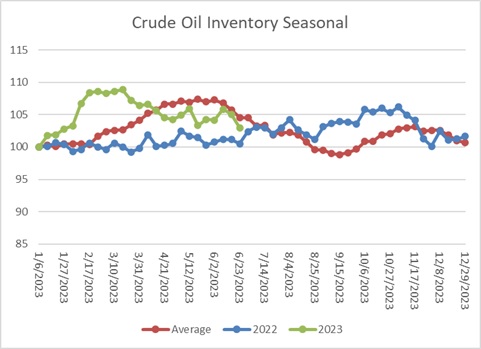

The above chart shows the seasonal pattern for crude oil inventories. After accumulating oil inventory at a rapid pace into mid-February, injections first slowed and then declined. This week’s draw is consistent with seasonal norms. The seasonal pattern would suggest that stocks should fall in the coming weeks, but this pattern has become less reliable due to export flows.

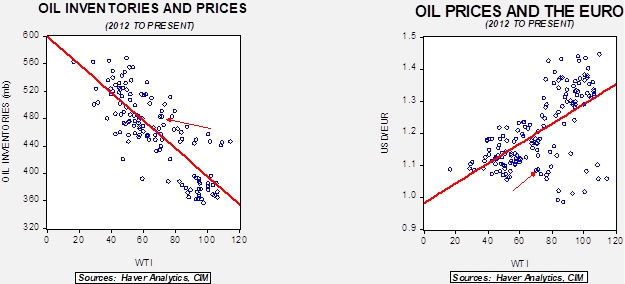

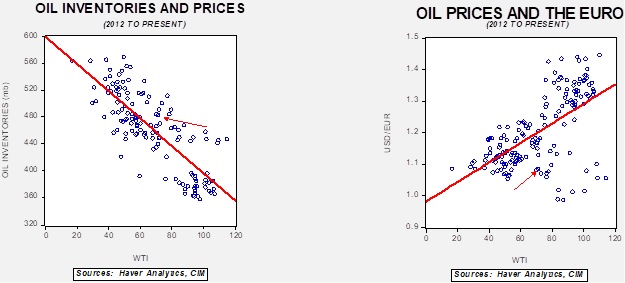

Fair value, using commercial inventories and the EUR for independent variables, yields a price of $61.81. Commercial inventory levels are a bearish factor for oil prices, but with the unprecedented withdrawal of SPR oil, we think that the total-stocks number is more relevant.

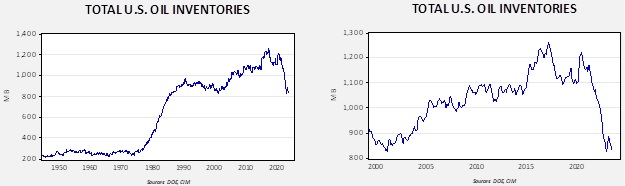

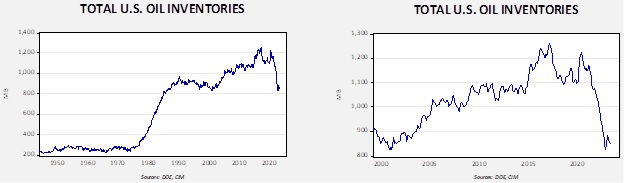

Since the SPR is being used, to some extent, as a buffer stock, we have constructed oil inventory charts incorporating both the SPR and commercial inventories. With another round of SPR sales set to happen, the combined storage data will again be important.

Total stockpiles peaked in 2017 and are now at levels last seen in 2002. Using total stocks since 2015, fair value is $94.69.

Market News:

- This week’s big news was the decision by OPEC+ to extend voluntary production cuts. The Kingdom of Saudi Arabia (KSA) agreed to extend its 1.0 mbpd cut another month and Russia promised to cut its production by 0.5 mbpd. The action by the cartel’s two largest oil producers did lift prices, but the rise has been rather modest given the size of the reduction. Why has the market mostly shrugged off the cuts? There are a few reasons to account for the lackluster response.

- It’s a simple fact that production cuts are usually seen as temporary. Production cuts mean that OPEC+ excess capacity rises. Bullish market positions are based on confidence that the cuts will be maintained. History shows there is always a risk that the cuts will either be violated or eventually reversed. Given that the dollar now tends to rise when oil prices rise, the temptation to cheat on announced cuts is even higher.

- World economic growth is cutting into oil demand. The forward curve for crude oil suggests traders don’t see a near-term supply issue.

- Other producers within OPEC+ are still producing and could take market share. This is especially true of Iran; the sanctions regime is coming under pressure and thus more Iranian oil will likely be on the market.

- As interest rates around the world rise, the cost of storing oil also rises. If the oil market is in contango, the higher price for deferred barrels can offset the increases in interest rate costs. But the spread doesn’t currently compensate for higher borrowing costs. Overall, higher interest rates will tend to depress oil inventories, which could lead to higher prices if there is a disruption in flows.

- Argentina’s oil production is rising due to investment in shale fields at the Vaca Muerta project.

- Climate change policies are likely to lead to falling oil demand. This factor makes long-term production forecasting problematic for oil companies.

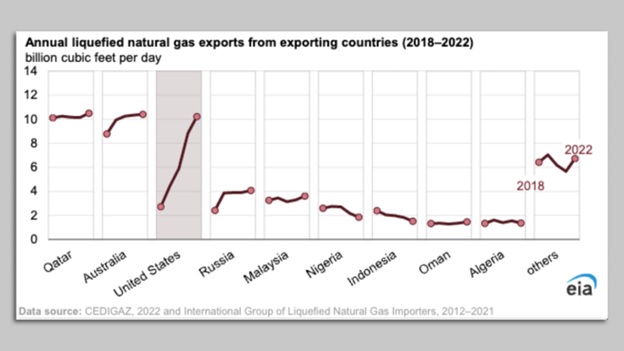

- The U.S. is rapidly building out its LNG export capacity, which has led to a sharp rise in exports. As this chart shows, this expansion has been rapid compared to the rest of the world. And, the U.S. number was adversely affected by the outage at Freeport. Despite the rapid increase, Europe and China are scrambling to secure U.S. LNG, which is adversely affecting smaller buyers in Asia.

Geopolitical News:

- The whole “decoupling/derisking” discussion with China is ongoing. The issue affects numerous industries, with technology and clean energy getting most of the attention. However, it should be noted that China imports significant levels of LNG from the U.S. So far, those flows have not been affected by the debate.

- The U.S. has released frozen funds to Iran in a bid to improve relations enough to make a modest nuclear deal and garner the release of Americans held by the regime. This thaw happened at the same time the U.S. Navy prevented Iran from seizing oil tankers near the Strait of Hormuz.

- Russia’s continued problems are prompting Central Asian oil producers to build new logistical channels to avoid the country. Increasingly, the war in Ukraine is causing Russia to lose its grip on its former near-abroad.

- Due to constraints within the Indian refinery system, we may be at the peak of Russian oil sales to New Delhi.

Alternative Energy/Policy News:

- Hot weather continues across the South and Midwest. According to researchers at the University of Maine, global temps may have set a record recently.

- In Texas, electricity demand hit a new record on June 27 due to high temperatures. It turns out that solar power in Texas has been a reliable source of power, helping Texas avoid service interruptions.

- These hot temperatures are not unique to the U.S. The world is seeing record temperatures.

- Solar panel production is creating tight supplies for silver.

- Electric vehicle (EV) news:

- As cobalt prices decline, China is stockpiling the metal. High prices last year led to higher production; as supply rose, prices fell. Cobalt is used in EV batteries. China is also the world’s primary source for finished nickel, which is also part of EV batteries. Meanwhile, Indonesia may be poised to further increase nickel output but perhaps at high environmental cost.

- Car companies around the world are taking an interest in acquiring key battery minerals. BYD (BYDDY, $67.21) announced a lithium processing project in Chile. As foreign interest rises, nations with the deposits are driving harder bargains to access these key resources. On a related note, the recent phosphate deposits discovered in Norway appear to be very large.

- China’s announcement of export licenses for rare earth metals is triggering a global scramble to secure these resources.

- In China, firms are creating subsidiaries to capture EV government funding.

- As we have been noting recently, China is targeting Europe for EV exports. China also announced groundbreaking on a new EV battery factory in Thailand and a lithium processing plant in Zimbabwe.

- Nations around the world have been subsidizing elements of their domestic EV industries. India announced subsidies for batteries this week.

- Toyota (TM, $161.99) announced a solid-state battery that would cut the weight of current batteries by 50% and reduce charging times to 10 minutes. The company hopes to commercialize the product by 2027. Solid-state batteries would likely tip the balance toward EVs because they would provide longer-range vehicles with recharging speeds near gasoline refills. However, it has been the promise for a long time.

- Recent surveys show that the public is open to EVs but only about 40% are in favor of totally eliminating ICE vehicles. Generally speaking, Republicans are less open to alternative energy than Democrats, although there is still some support for the transition even among the former.

- China is rapidly expanding its solar and wind energy capacity. In fact, it has hit its existing targets five years earlier than expected. However, progress has been slower than expected in rural regions.

- The Inflation Reduction Act is prompting European nations to build hydrogen production in the U.S.

- Siemens Energy (SMNEY, $16.46) wind turbines are developing cracks that are expected to cost at least €1.0 billion to address.

- Ocean shippers are experimenting with large kites to aid in propulsion. Using kites could reduce fuel consumption by up to 30%.

Asset Allocation Bi-Weekly – #101 “The Green Shoots of Re-Industrialization” (Posted 7/3/23)

Business Cycle Report (June 29, 2023)

by Thomas Wash | PDF

The business cycle has a major impact on financial markets; recessions usually accompany bear markets in equities. The intention of this report is to keep our readers apprised of the potential for recession, updated on a monthly basis. Although it isn’t the final word on our views about recession, it is part of our process in signaling the potential for a downturn.

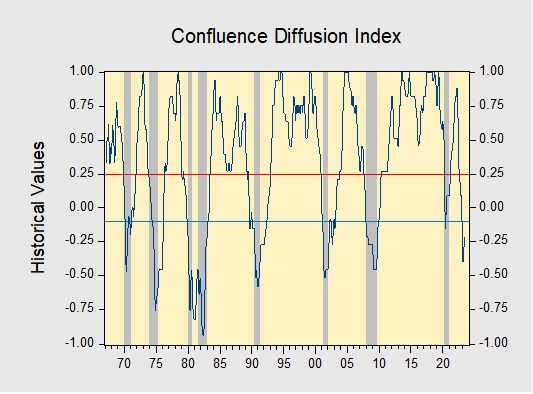

The Confluence Diffusion Index improved slightly in May but continues to signal that a recession is close. The latest report showed that six out of 11 benchmarks are in contraction territory. The diffusion index rose from -0.3333 to -0.2121 but still sits well below the contraction signal of +0.2500.

- Equities rebounded despite financial conditions remaining tight.

- Residential construction spiked but the goods-producing sector remains weak.

- Labor markets appear to be strong but the number of unemployed workers is starting to climb.

The chart above shows the Confluence Diffusion Index. It uses a three-month moving average of 11 leading indicators to track the state of the business cycle. The red line signals when the business cycle is headed toward a contraction, while the blue line signals when the business cycle is in recovery. The diffusion index currently provides about six months of lead time for a contraction and five months of lead time for recovery. Continue reading for an in-depth understanding of how the indicators are performing. At the end of the report, the Glossary of Charts describes each chart and its measures. In addition, a chart title listed in red indicates that the index is signaling recession.

Weekly Energy Update (June 29, 2023)

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA | PDF

Oil prices may be establishing a new trading range between $67 and $75 per barrel.

Commercial crude oil inventories fell 9.6 mb when compared to the forecast draw of 1.3 mb. The SPR fell 1.4 mb, putting the total draw at 11.0 mb.

In the details, U.S. crude oil production was steady at 12.2 mbpd. Exports rose 0.8 mbpd, while imports rose 0.4 mbpd. Refining activity declined 0.9% to 92.2% of capacity.

The above chart shows the seasonal pattern for crude oil inventories. After accumulating oil inventory at a rapid pace into mid-February, injections first slowed and then declined. This week’s draw is consistent with seasonal norms. The seasonal pattern would suggest that stocks should fall in the coming weeks, but this pattern has become less reliable due to export flows.

Fair value, using commercial inventories and the EUR for independent variables, yields a price of $61.31. Commercial inventory levels are a bearish factor for oil prices, but with the unprecedented withdrawal of SPR oil, we think that the total-stocks number is more relevant.

Since the SPR is being used, to some extent, as a buffer stock, we have constructed oil inventory charts incorporating both the SPR and commercial inventories. With another round of SPR sales set to happen, the combined storage data will again be important.

Total stockpiles peaked in 2017 and are now at levels last seen in 2002. Using total stocks since 2015, fair value is $94.62.

Market News:

- The Dallas Fed data shows slowing activity in shale drilling. Rig counts have been falling and firms are reducing investment in production.

- OPEC+ is trying to woo Guyana into the cartel. So far, the South American nation has fended off the invitation. The government argues that with oil demand set to decline over time, the country needs to maximize revenue in the short run; thus, producing to a quota may harm that effort.

- From the 1970s into the late 1990s, the Kingdom of Saudi Arabia’s (KSA) rank as foreign supplier of oil to the U.S. was a reliable signal for the market. If the Saudis’ position fell below second place, within a few months, the Saudis would tend to flood the market with oil to maintain dominance of the U.S. oil market. The shale revolution ended that relationship, but we are watching closely to see if a similar pattern develops with the China market. It will be more difficult to establish the foreign rank given China’s tendency to control information, but we would not be surprised to see foreign oil producers try to become the largest supplier to China. Thus, we note with interest the reports that Russia is gaining share in China. This development could end the KSA’s recent thrust to raise oil prices via unilateral production cuts.

- As a heat wave develops in the Pacific Northwest, a county in Oregon is suing fossil fuel companies. Although we doubt this action will have any effect, it does suggest a vulnerability for energy producers.

- The DOE says that the majority of the lower 48 will be at risk of electricity disruptions due to high temperatures.

- China is aggressively expanding its petrochemical capacity, leading to a glut of product on global markets. Meanwhile, there is new investment in this industry in the KSA as well.

Geopolitical News:

- News of the Russian “coup” dominated last weekend, but for the oil markets, it’s not obvious if it will make much difference. Although there are many articles suggesting Putin is finished, we will wait and see. Chaos in Russia would be bullish for oil prices but, in the short run, not much has changed for oil flows.

- New research shows how geopolitical insecurity is leading China to stockpile oil and expand relations with oil and gas producers. The research suggests that insecurity of supply is driving policy.

- There is increasing evidence that the KSA is engaging in energy policies designed to harm the U.S. For example, the U.S. will see the largest export reductions tied to the KSA’s decision to cut oil production.

- The KSA is sending high-ranking officials to China’s “Summer Davos,” or formally, the Annual Meeting of New Champions. The decision highlights the Saudis’ close relations with Beijing.

- The latest on the Nord Stream sabotage is that Ukrainian operatives based this action in Poland. If true, it complicates inter-EU relations with Germany.

- Russian product sales are being facilitated by European trading firms.

Alternative Energy/Policy News:

- Ford (F, $14.12) has won a $9.2 billion DOE loan to build three EV battery factories. The UAW is unhappy with the development as the factories will be in non-union states and will likely not be manned with union labor.

- Synthetic fuels could replace traditional fossil fuels and, if created by nuclear power, they could be nearly carbon-free or carbon-negative if captured CO2 is used in the process.

- Oil and gas firms are expanding into lithium.

- China and Sweden have had political spats over the years, mostly over human rights issues. China has unofficially banned graphite sales to Sweden; the metal is a key component in EV batteries. Although it’s possible that China’s refusal to sell to Sweden is political, it’s more likely that Beijing wants to cripple Sweden’s battery industry.

- Sales of EVs continue to climb. China continues to dominate EV exports.