Author: Rebekah Stovall

Bi-Weekly Geopolitical Podcast – #15 “The End of the World is Just the Beginning: A Book Review” (Posted 8/15/22)

Bi-Weekly Geopolitical Report – The End of the World is Just the Beginning: A Book Review (August 15, 2022)

by Bill O’Grady | PDF

Soon after founding Confluence Investment Management, we formulated a position that the U.S. was in the early stages of ending its hegemonic role. We postulated that this event would have a profound effect on the domestic and global economy, and, consequently, financial markets. In traveling around the country discussing this idea, we[1] were often asked, “When are you going to write a book about this?” It seemed like something we should do, although finding time while meeting a tight publication schedule and trying to run a business made it challenging. When Mark and I discussed the idea of a book, we wanted it to cover the material in an accessible manner.

And then the idea died…because Peter Zeihan beat us to it. His 2014 book The Accidental Superpower hit all the themes we wanted to cover and did so in a manner that we probably couldn’t improve upon. Zeihan has worked for the State Department and other think tanks. I saw his work with Stratfor when he was with that private intelligence firm, and he now runs his own consulting firm, Zeihan on Geopolitics. He frequently sends out short videos on various topics; you can join his mailing list here. Since The Accidental Superpower, he has written three books, the most recent of which was published in July and is the topic of this week’s report.

In this report, we will review Zeihan’s new book, The End of the World is Just the Beginning, briefly discussing its content, the major insights, and the overall strengths and weaknesses of his argument. We will conclude with market ramifications.

[1] Mark Keller (Confluence CEO/CIO) and me.

Don’t miss the accompanying Geopolitical Podcast, available on our website and most podcast platforms: Apple | Spotify | Google

Weekly Energy Update (August 11, 2022)

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA | PDF

Prices have broken support but appear to be basing around $88 per barrel.

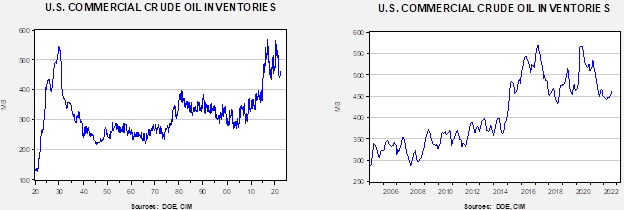

Crude oil inventories rose 5.5 mb compared to a 1.0 mb draw forecast. The SPR declined 5.3 mb, meaning the net build was 0.2 mb.

In the details, U.S. crude oil production rose 0.1 mbpd to 12.2 mbpd. Exports fell 1.4 mb, while imports declined 1.2 mbpd. Refining activity jumped 2.3% to 94.3% of capacity.

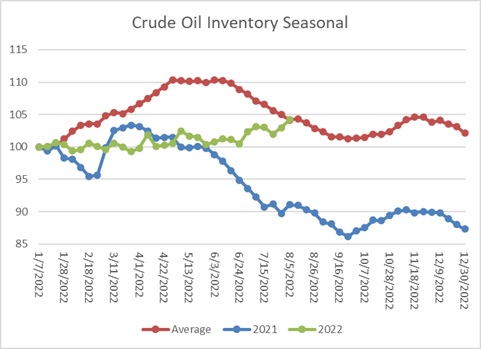

The above chart shows the seasonal pattern for crude oil inventories. Clearly, this year is deviating from the normal path of commercial inventory levels. The fact that we are not seeing the usual seasonal decline is a bearish factor for oil prices.

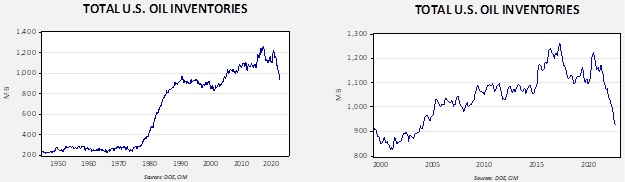

Since the SPR is being used, to some extent, as a buffer stock, we have constructed oil inventory charts incorporating both the SPR and commercial inventories.

Total stockpiles peaked in 2017 and are now at levels last seen in 2004. Using total stocks since 2015, fair value is $102.55.

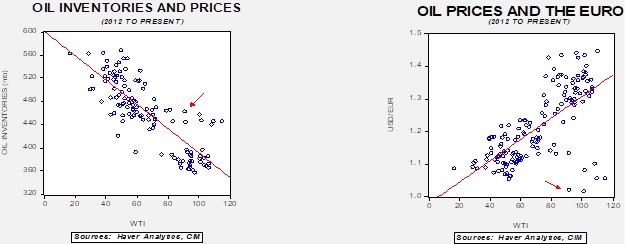

With so many crosscurrents in the oil markets, we are beginning to see some degree of normalization. The inventory/EUR model suggests oil prices should be around $64 per barrel, so we are seeing about $24 of risk premium in the market.

Market news:

- Oil prices rose this week as Russia halted shipments to central Europe over a dispute on payments. According to reports, Russia cut throughput after sanctions prevented Russia from accepting transit fees. However, the market failed to hold gains as a workaround was created.

- In last week’s report, we noted that OPEC+ increased production targets by 0.1 mbpd, a remarkably small adjustment. This had to be a disappointment for the White House. But beyond this news reveals a more troubling problem—the cartel may be near maximum output. For most of my career, we spoke of OPEC production “quotas” that were routinely violated. The usual excess production would tend to quell prices and, occasionally, lead the KSA to enforce discipline by flooding the market with oil. We now are in a world where we have production “targets” that are not met. The reason for the small increase appears to be less of a snub to President Biden and more because the producers just don’t have the capacity. Now, that doesn’t mean that they have no more oil to tap, but using that capacity would mean there is no additional buffer if something happens this winter. In any case, the price weakness we are seeing now is mostly a function of weakening demand.

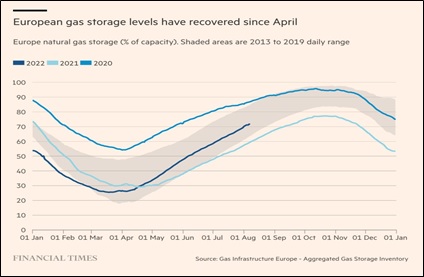

- Meanwhile, in Europe, countries are trying to figure out how to reduce demand to shore up inventories of natural gas without relying solely on price to ration demand. Such schemes have some usefulness, but there is a clear incentive to “free ride” the conservation of others. For example, Greek authorities are pressing for citizens to maintain an air conditioning temperature of 80o, but actually doing that is hard. So far, a weakening EU economy coupled with these measures is allowing inventories to accumulate, but at much higher costs. The other action we are seeing is fuel switching, which has mixed value. Still, research from the IMF suggests that with better coordination, the EU could offset some of the supply issues with better distribution.

- Although we have doubts that such demand “scolding” will work, EU storage levels are about normal.

- The negative effect on fertilizer and chemical plant operations in Europe could be significant if natural gas supplies remain constrained.

- After cutting off flows of natural gas to Latvia, supplies returned; it is not obvious why Russia restarted flows.

- Freeport LNG will resume partial operations in October. Although that is good news for Europe, it may result in higher U.S. natural gas prices. Various outages at gasification facilities have been very costly for natural gas firms.

- Reports suggest that Russian oil prices are starting to rise, which signals some degree of normalization of trade flows. Although bans on Russian oil in some markets will remain in place, nations open to buying Russian oil, namely, China and India, are likely creating a trading infrastructure to facilitate these sales.

- As Asia and Europe scramble to secure natural gas supplies, buyers are finding themselves competing for the same cargos. Meanwhile, as the U.K. steps up its LNG regasification, it is confronting a situation where some of the gas is tainted; if not rectified, this contamination could harm gas pipelines to the continent

- In Asia, a strike at an Australian LNG facility will delay maintenance and may reduce available supplies.

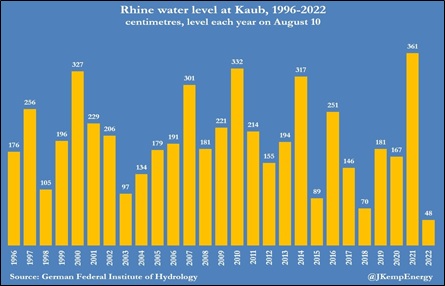

- As we noted last week, Rhine River water levels are declining due to unusually warm weather and the lack of rain. As levels decline, freight costs rise as ships can only be partially loaded.

- Factories in Bangladesh are planning for “holidays” to reduce energy demand.

- Gulf of Mexico oil production has been flat for the past two years. Most projects are longer term in nature and the investing environment is such that oil companies are being cautious, wanting to avoid stranded assets. In addition, production in the region is always at risk to tropical storm activity. That said, there are some projects coming on line which could lift production from this area in the coming months. Still, given where prices are, oil production has shown little growth, mostly because of capital discipline.

- The ESG movement has pressed financial firms to cut lending and investment to fossil fuels. As backlash has developed, banks and other financial firms are finding themselves caught between competing political trends.

- A Cuban tank farm caught fire after a lightening strike.

- Although the Biden administration hasn’t moved to restrict oil exports like President Nixon did in the 1970s, there is a risk that such policies might be considered again. However, given different grades of crude oil and their compatibility with the U.S. refining system, it is quite possible that the oil that isn’t exported would not be used domestically. This outcome would likely lower U.S. crude oil prices without lower product prices. In addition, such a ban would discourage U.S. production.

- High energy prices are translating into high food costs.

- China is producing oil and gas with ultra-deep drilling techniques.

Geopolitical news:

- According to reports, EU mediators negotiating between the U.S. and Iran have submitted their “final text.” Although Iran has returned to nuclear talks, the odds of success appear very low. For one thing, Tehran looks to be moving rapidly toward a nuclear weapon. For another, Tehran is trying to prevent the IAEA from investigating suspected weapons sites. We continue to expect that the talks will fail.

- Russia is launching a satellite for Iran to spy on the region.

- In Iraq, Muqtada al-Sadr is calling for new elections. Turmoil has been high in Iraq since al-Sadr’s supporters resigned from parliament.

- We have been reporting about high European temperatures this summer. One potential fallout is that hot weather could be contributing to geopolitical tensions in the Balkans.

Alternative energy/policy news:

- As the Inflation Reduction Act of 2022 careens toward passage, the climate change portions appear to be quite remarkable. Obviously, these projections are just that; it remains to be seen how this bill will work in practice. Nevertheless, it is notable that a political deal with a supporter of fossil fuels was open to signing off on such a measure.

- The bill does offer some political lessons. In a closely divided nation, carrots work better than sticks. This bill doesn’t have a carbon tax or items that will restrict demand; instead, there are subsidies and incentives.

- The parts of the bill that streamline permitting for pipelines is, in our opinion, a significant win for the oil and gas industry.

- One of the stranger elements of the bill is that to receive the EV tax credits, the supply chain has to exclude China. Since many of the EV elements come from China (batteries, some key metals in batteries, etc.), most EVs will be excluded. Although this rule does make sense, it also makes sense to buy your EV ASAP.

- As EVs become more popular, drawbacks are starting to emerge. First, EVs are expensive, even with generous subsidies. For widespread adoption, more affordable models will be required. Second, it will be difficult to source key inputs, such as lithium, nickel, and cobalt; there simply are not enough mines to meet the demand. Third, the charging infrastructure isn’t built out yet, and allocating the costs for that infrastructure will be partly absorbed by those not driving EVs.

- China’s CATL (300750, CNY, 505.65) intends to go ahead with its plans to build a battery facility in the U.S. With all the turmoil tied to Speaker Pelosi’s (D-CA) visit to Taiwan, there were doubts the investment would occur.

- Sanctions on imports from Xinjiang will likely reduce the availability of solar panels in the U.S.

- In some respects, hydrogen is the future of the energy industry and always will be. Hydrogen is not only ecologically friendly (using it in a fuel cell creates water as a byproduct), but it could conceivably use the existing filling station network and avoid the buildout of charging stations. Still, making hydrogen on a commercial scale has always been cost prohibitive. Fuel cells mostly use platinum, lifting costs as well. But, emerging research suggests that iron might be an acceptable catalyst, which could reduce costs significantly.

- Over the summer, we have been commenting on extreme temperatures and other weather events around the world. Iraq, for example, is reporting 120o temps this week. In the face of rising temperatures, cities are beginning to build and expand cooling centers to give people a place to cool off during the day. Drought conditions exist in 60% of the EU plus the U.K. The latter is bracing for another dangerous heat wave.

- The lack of rainfall is reducing Norway’s hydroelectricity supply; consequently, exports to the continent will be cut.

- U.S. power demand is set to make a new record this year.

- Thermal storage is increasingly becoming an alternative for absorbing excess electricity from wind and solar.

- One of the “dirty little secrets” of green energy is that it relies heavily on rare earths minerals. These tend to be mined in the developing world at terrible environmental costs.

- In a bid to clean up the plastics chain, investments in bioplastics are starting to ramp up.

- Although nuclear energy offers a path toward carbon-free energy, the U.S. is heavily dependent on Russia for uranium supplies.

- Solar and wind farms can take up space in farmlands. China is considering reducing such installations to ensure ample food supplies.

Confluence of Ideas – #26 “The 2022 Outlook: Update #2” (Posted 8/9/22)

Asset Allocation Bi-Weekly – #81 “The Devil Is in the Details” (Posted 8/8/22)

Bi-Weekly Geopolitical Podcast – #14 “Political Crises for Top U.S. Allies” (Posted 8/1/22)

Asset Allocation Bi-Weekly – #80 “The Puzzle of the Labor Force” (Posted 7/25/22)

Asset Allocation Quarterly (Third Quarter 2022)

by the Asset Allocation Committee | PDF

- Global growth is clearly slowing and the probability of a recession in the U.S. over the next year is significantly elevated.

- The Fed is continuing its aggressive attack on inflation through rapid increases in the fed funds rate and accelerating its balance sheet reduction.

- Economic data from overseas depicts difficulties, especially in Europe and China.

- The potential exists for defaults of selected emerging market sovereigns beyond Sri Lanka.

- Equity allocations are underweight and bond exposures were increased.

- BB-rated bonds are used as an equity proxy across the array of strategies.

- U.S. stock exposure remains heavily tilted toward value, with overweights to defensive sectors.

ECONOMIC VIEWPOINTS

In June, the World Bank cut its global GDP growth projection for this year from 4.1% to 2.9% owing to a spike in energy and food prices, which in no small part has been influenced by the Ukraine war and the resultant freezing of Russia’s foreign reserves. This has further curtailed supply and trade, which were already constrained by the global pandemic and altered by the general trend toward deglobalization. Deglobalization, coupled with an increase in regulation, could institutionalize a level of inflation above the Fed’s 2% target and lead to shorter business cycles than what we have become accustomed to since 1990.

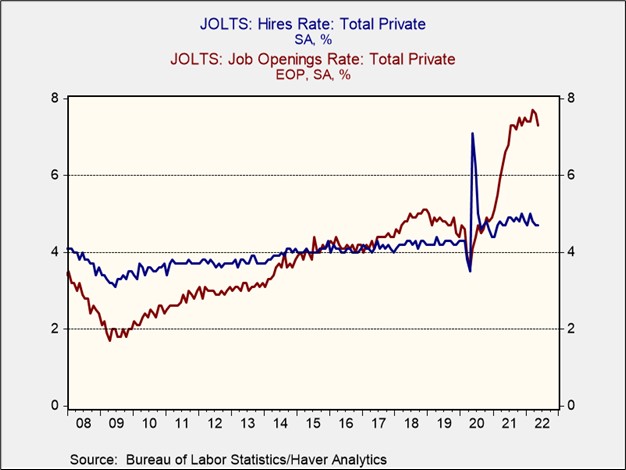

In the U.S., inflation has vaulted higher, with the CPI rising 9.1% year-over-year as of June, the largest annual increase since the end of 1981. At its recent meeting, the U.S. Federal Reserve increased the fed funds rate by 0.75%, the largest single hike since October 1994. In the conference following the meeting, Fed Chair Powell indicated that further rate hikes are in store for the balance of this year and into 2023 with the goal of pulling down inflation to the Fed’s 2% target range. Adding to the dynamic is the Fed’s reduction of its balance sheet, which began in June and is poised to accelerate in September to a monthly rate of $95 billion against the current balance of $8.36 trillion. The Fed’s articulated desire is to quell inflation and reduce the demand for labor without increasing unemployment. As the accompanying chart indicates, the JOLTS openings rate is well in excess of the hires rate. It is this froth that the Fed believes it can remove without aggravating unemployment, thereby accomplishing Powell’s goal of a “softish landing.”

The assertiveness of the Fed, combined with what we find are nascent signs that the spiking inflation is beginning to abate, create fertile ground for a recession in the U.S. The bond market’s inversion of two-year and 10-year Treasury yields underscores the market’s belief that the Fed will pursue its fight too aggressively and stall the economy. It also reflects the dissonance among Fed governors regarding the varying economic consequences of quantitative tightening in the form of balance sheet reduction, increasing the potential for a policy error. We expect inflation to ease within the next few months as the comparative base effects from last year take hold. In addition, we find improvements in supply chains and a satiating of demand from consumers as inventory/sales ratios of merchandise are rising.

Beyond the U.S., the European Central Bank (ECB) is similarly attempting to battle inflation but also trying to maintain tight spreads for rates among its member states. In combatting inflation, which reached a record 8.6% last month, the ECB is expected to raise its deposit rate at its July meeting and perhaps elevate it from negative rates for the first time in over a decade. However, it is simultaneously dealing with fragmentation risk, which is the possibility that yields on debt of some peripheral countries will spike versus German bunds. The ECB is wrestling with these items, while manufacturing data is indicating slower growth and economic sentiment is waning. On the other side of the globe, economic growth in China has slowed dramatically. The world’s second largest economy produced its lowest growth since data was first recorded in 1992 as lockdowns in major cities contributed to the stagnation. Though it is widely believed that the People’s Bank of China will enact stimulus measures to spur the economy, worries abound regarding capital outflows as the U.S. Fed aggressively raises short-term rates. Among other emerging market economies, the risk of default is garnering attention after the government of Sri Lanka defaulted for the first time. Credit default swap spreads across a number of smaller sovereigns that issue debt in hard currencies, such as the U.S. dollar or euro, have spiked significantly, indicating the potential for a contagion effect. As noted in connection with China, capital flows to emerging market economies are at risk under these circumstances.

STOCK MARKET OUTLOOK

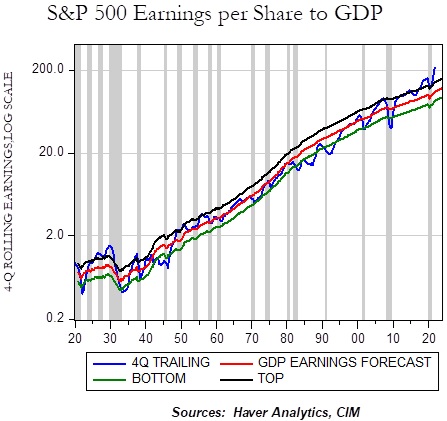

Equity markets have been in retreat for much of the year as investors have been struck by an array of worries including the Ukraine war, supply shortages, an aggressive Fed battle against inflation, and waning consumer and business confidence, among other concerns. Further pressure on U.S. stocks may come from a compression in earnings. As the chart indicates, four-quarter rolling EPS on the S&P 500 as compared to the earnings forecast based upon GDP is well above its historical standard error band. While the trailing figure relative to the GDP earnings forecast has been on a significant upswing recently, we expect this to decrease as financial conditions continue to deteriorate, the cost of labor increases, and prior inflation becomes fully incorporated. Relative to the cost of labor, larger companies may disproportionately contribute as they engage in elevated efforts to retain employees in a tight labor market. The escalating cost of hiring is encouraging firms to retain employees, despite growing wage levels. The result will likely be increased labor costs and lower margins, especially in service-oriented sectors that lack the ability to fully pass on increased costs to consumers. Beyond the effects of fragile global economies on corporate earnings, higher levels of inflation typically portend lower P/E ratios. Persistent inflation could continue to maintain pressure upon equity prices.

Although our base case is a troubled outlook for the stock market over the next several quarters, various fundamental forces could aid prices over our three-year forecast period. A satisfactory resolution of the Ukraine war would be a significant positive for global equities. In addition, a staggering amount of cash remains on the sidelines, both individual and institutional. If the Fed is able to engineer a softish landing or decides that it has fought the inflation battle too aggressively and/or too late and becomes more accommodative, a modest deployment of cash available for investment could prove to be a propellant for equity prices. Finally, a bottoming in the economy followed by a solid uptick created by full digestion of supply imbalances and improving consumer and business sentiment could buoy equity prices. While we acknowledge the potential advantages for U.S. stocks over our forecast period, we don’t necessarily share the sentiment for some international developed or emerging market stocks. Difficulties faced by some European companies as the ECB practices its version of inflation therapy, and the likelihood of reduced foreign direct investment in emerging economies during a period of elevated sovereign risk, may crimp the shorter-term advantages for international equities in these strategies, especially with a surging U.S. dollar.

Given our expectations for the economy and outlook for stocks, we are further constraining our exposure to risk-based assets. Accordingly, the stock allocations in our strategies are lower, and in some cases the lowest since inception. Within these reduced equity exposures, we maintain a significant bias of 65% to value stocks as they tend to outperform as economic growth retreats. There is also less concentration among the top names, where the top five companies in the S&P 500 Growth Index account for 45.2% versus 11.7% in the S&P 500 Value Index. To complement the value skew, we continue the overweight to defensive segments of Health Care and Consumer Staples, as well as Energy. In addition, we believe the Ukraine war has advanced an increase in defense expenditures among developed countries, thus we retain a position in the aerospace and defense industry. Our efforts to reduce risk also apply to international allocations, where the only exposure is in a Japanese equity position that carries a currency hedge back to the U.S. dollar. The thesis leading to this overweight included the relative pricing advantage of Japanese stocks compared to U.S. counterparts complemented by continued policies from the Bank of Japan that are contributing to a depreciating yen. Emerging markets remain absent from all strategies.

BOND MARKET OUTLOOK

Rampant inflation and a motivated Fed would normally imply caution regarding the bond market. Typically, as the Fed is raising rates and emptying its balance sheet, the fundamental forces it unleashes would cause yields to increase and thereby prices on bonds to retreat. Based upon the impact on bond prices thus far in 2022, we believe much of the punishment to bond investors has already been wrought this year. Moreover, the inversion of the yield curve for two-year/10-year Treasuries indicates market participants are becoming convinced that fed funds increases are going to be limited to this year. Accordingly, we hold a positive outlook for the short- and intermediate-term segments of the Treasury curve. However, the sanguine outlook does not completely extend to credit. With the increasing prospect for a recessionary environment in the U.S., we expect spreads to widen for investment-grade corporate bonds closer to historic averages. While we expect these instruments to produce positive returns over our three-year forecast period, the returns will be restrained by the spread widening. We expect a similar dynamic to unfold in the BB-rated space within high yields. However, in lower rated speculative bonds we find the inherent risks outweigh any advantage at this point in the economic cycle. Consequently, the exposure to speculative-grade bonds in all strategies are confined to bonds rated BB, which are used as a lower volatility equity proxy.

OTHER MARKETS

Due to the Fed’s aggressive fight against inflation and the increased potential for a recession, REITs are absent from the strategies. We retain exposure to commodities in all strategies given the utility they offer as portfolio stabilizers as the potential for risk increases. Gold is utilized given its appeal as a haven from heightened geopolitical risk, and a broad basket of commodities, with an emphasis on energy, is also employed across all strategies. The global thirst for energy, especially in Europe as they adjust to sanctions on Russian exports, produces certain advantages for this positioning.