by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez

[Posted: 9:30 AM EDT] U.S. equity markets are higher this morning on hopes of a trade deal at this weekend’s G-20 meeting. The second leg of the first Democratic debate was held last night. Vice President Biden had a tough night; there are concerns that if Biden falters the odds of a left-wing populist winning rise, which is potentially a negative for health care. Here is what we are watching today:

The G-20: We have covered our thoughts on the G-20 over the past few days and don’t have a whole lot more to add. The key meeting of the weekend occurs at 10:30 EDT tonight when Trump and Xi hold their meeting. Consensus is that there will be a ceasefire; no new tariffs and promises to continue talking will be the outcome. U.S. hardliners on China are worried that the president could negotiate away the stiff sanctions on Huawei (002502, CNY 3.44). So far, President Trump has struck an optimist tone, not only with China, but with other free trade talks currently underway. The U.S. and Japan have agreed to accelerate talks, for example. In addition, Trump and Chancellor Merkel (who has been having her own problems recently) seemed to get along rather well. At the same time, the G-20 is deeply fractured; it is possible they won’t be able to put together a joint communiqué at the end of the meeting. We also note that Peter Navarro was a late add to President Trump’s entourage. Navarro is arguably the most hawkish member of the president’s advisors on Chinese trade and having him at the meeting might signal a harder stance than the markets are currently discounting. We also note that the U.S. and Turkey will hold leader talks at this meeting. This may be the last chance for Erdogan to avoid losing access to the F-35 fighter and undermining NATO.

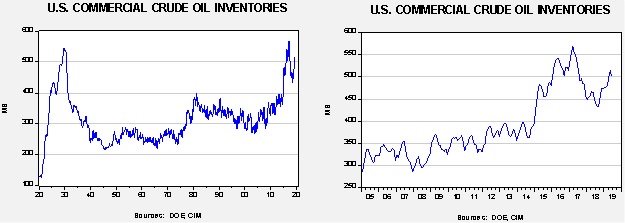

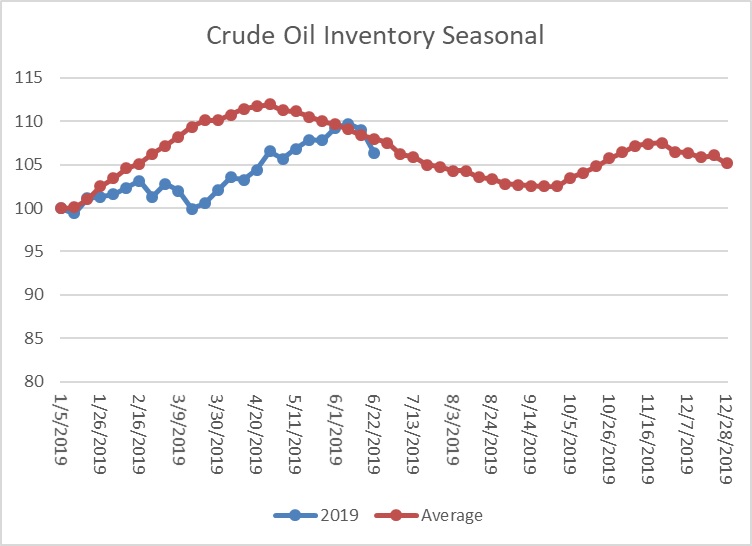

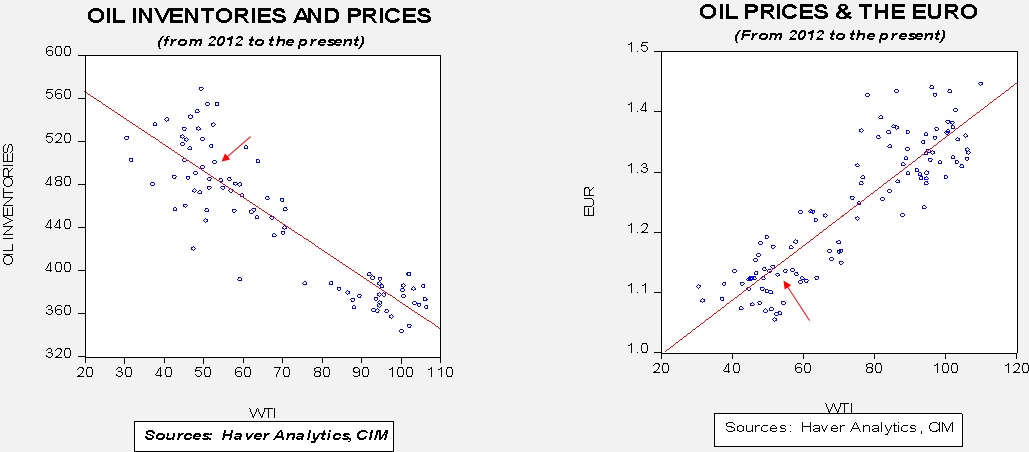

Iran: President Trump made some hawkish statements on Iran, suggesting that a military conflict would not last long. That notion is probably wishful thinking. It does appear the U.S. is considering tanker escorts and an expanded monitoring system, which makes sense. Meanwhile, the EU is preparing to launch its payments system that would allow Iran to trade with it. So far, it looks like it won’t lead to a significant improvement in Iran’s faltering economy. The EU is trying to bring about enough trade to keep Iran in compliance with the current Iran deal and avoid upsetting the U.S., a tough line to hew. Although nothing too significant is happening today, we would expect traders to cover shorts into the weekend, which could support oil prices.

Bank stress tests: The Fed held its bank stress tests. All got a participation trophy.

Trump and the dollar: President Trump said today that he wanted the Fed to ease in order to weaken the dollar. Chair Powell correctly noted that dollar policy isn’t the purview of the Fed. This discussion continues to frame a growing narrative that would support a “Plaza Accord II,” albeit a unilateral one, where the U.S. purposely depresses the dollar for trade advantage. We also note the BOJ is considering easing policy, which could lead to a weaker JPY and further anger the White House.

Capital gain cut? The Trump administration is apparently mulling the indexing of capital gains to inflation. Although this would infuriate the populists on both wings, it would be quietly cheered by the establishment.

Odds and ends: Tensions are rising in North Africa again. There have been terror attacks in Tunisia and simmering issues in Algeria. The U.S. is increasing its military investments in Iceland. Cocaine production is soaring. Russell indexes rebalance today; expect lots of equity action on today’s close.