by Bill O’Grady | PDF

On March 11, the International Energy Agency announced a coordinated draw of 400 million barrels from the Strategic Petroleum Reserve (SPR) System maintained by the organization’s member countries. Understanding the reasoning behind this decision requires an examination of the economics of inventory. This analysis will help the reader understand that SPRs are not just protective stockpiles but have a key psychological element as well.

In textbook economics, inventory doesn’t exist. Theory assumes a frictionless world, which means that production and consumption are continuous functions, and production meets consumption instantaneously. Obviously, this condition doesn’t reflect the real world. The classic example is agriculture: production is seasonal, so there are periods when supply is scarce (between harvests) and other periods when supply is abundant (right after the harvest). Inventory smooths out the supply to better meet demand.

Most goods markets have inventory, and many of them have inventory cycles driven either by production or consumption. Analysts usually attempt to determine what is a “normal” inventory for a given time of the year. Once this norm is established, inventory changes can signal the balance of supply and demand in a market. If inventory is below normal, it likely signals a tight market, which would be expected to bring higher prices. Higher prices encourage producers to make more and consumers to consume less, and the opposite is true when inventory is above normal. This pattern suggests that, under normal conditions, we would expect to see an inverse correlation between inventory and price. In general, high inventory levels should be bearish, while low inventory levels should be bullish.

If the correlation between inventory and price is positive, it suggests hoarding. Hoarding occurs when consumers fear that a good will become unavailable. In response, consumers attempt to build their personal inventory by purchasing more than they would usually hold. If markets are functioning normally, hoarding is irrational. Seeing higher prices, producers will boost output, which should provide enough product to ease shortage concerns. However, hoarding doesn’t usually occur in a vacuum. It typically happens in response to an exogenous shock, like a weather event, war, pandemic, etc. The problem with hoarding is that, at the micro level, it’s a perfectly reasonable response that can make the market situation worse at the macro level. Hoarding is a prime example of the “error of composition.”[1]

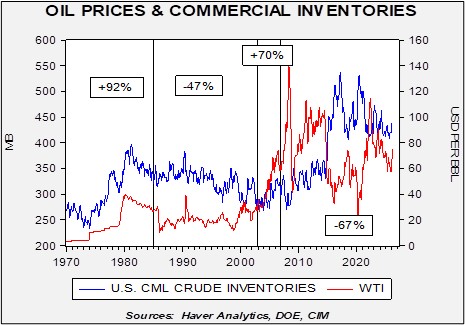

The chart below shows US commercial crude oil inventories and the West Texas Intermediate oil price. We have divided the graph into periods where the correlation between oil prices and inventories flipped. Note that in the 1970s, oil prices and inventories were highly positively correlated, reflecting hoarding. The correlation became positive again from 2003 through 2006 at the end of the China-driven commodity bull market early in this century. The rest of the time, the correlation has been negative, which is what one would expect under normal market conditions.

The thinking behind the creation of SPRs was to reduce the tendency to hoard. If a consumer is worried about physical scarcity (as opposed to high prices), then there is an incentive to stockpile. During the gas lines crisis of the 1970s in the US, it was not uncommon for drivers to wait in line to buy merely a gallon or two of gasoline “just in case.” Strategic reserves serve the purpose of ensuring the availability of supply, which should dampen the desire to hoard.

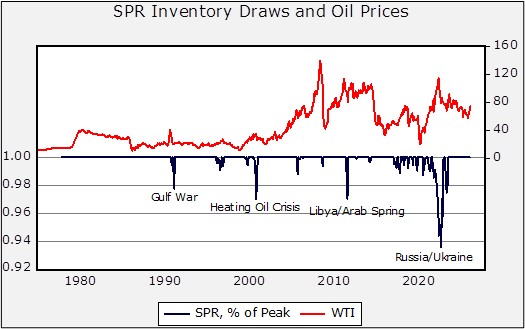

The chart below shows US SPR draws and oil prices. To measure draws, we compare oil prices to the previous month’s peak in the SPR. There are numerous small draws shown as Congress sometimes uses the SPR to fill budget gaps. Often, the SPR oil is “swapped” during supply outages and then usually replaced a month or two later. The major draws, which tend to bring down prices, are noted on the chart.

In our view, the recently announced draw should stabilize oil prices — at 400 million barrels, it’s the largest combined draw in history. However, it’s important to note that the Strait of Hormuz outage amounts to about 20 million barrels per day, meaning this draw could only offset about 20 days of losses. So, we view it as an action that should prevent spikes in oil prices, but it likely won’t be enough to bring down prices sharply without a reopening of the strait.

As our analysis on hoarding shows, if the nations releasing SPR oil keep it within their borders, prices may actually rise. To prevent that, the taxpayers who funded the strategic storage must be willing to “share” with nations that did not. For investors, this is the key factor to monitor. How will we know if the announced SPR release isn’t working? If we see commercial oil inventory and prices rise simultaneously.

[1] A logical fallacy that assumes what is true for an individual is also true for the whole.