Author: Rebekah Stovall

Weekly Energy Update (May 7, 2020)

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

Here is an updated crude oil price chart. The oil market is showing signs of recovery.

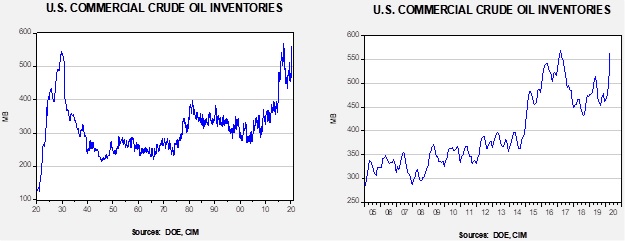

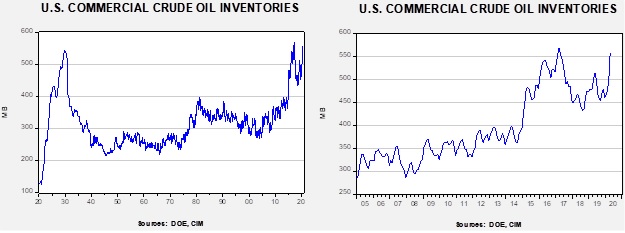

Crude oil inventories rose 4.6 mb compared to the forecast rise of 8.0 mb.

In the details, U.S. crude oil production fell 0.2 mbpd to 11.9 mbpd. Exports rose 0.4 mbpd, while imports rose 0.2 mbpd. Refining activity rose 0.9%, a bit more than the 0.8% rise forecast. The inventory build was mostly due to continued elevated U.S. production, although the pace of the rise is starting to slow.

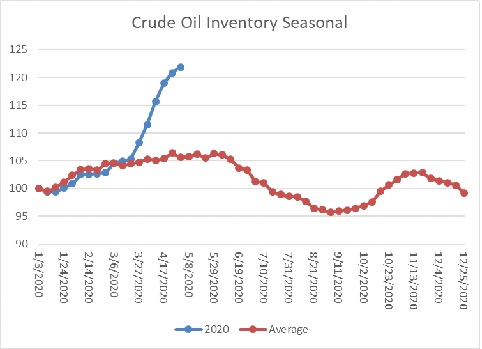

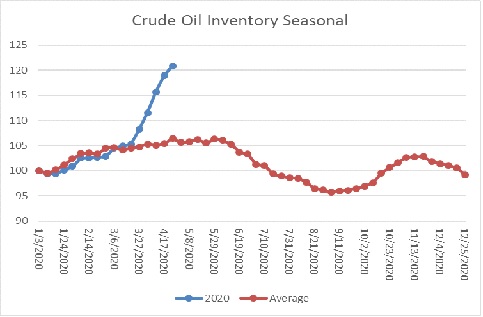

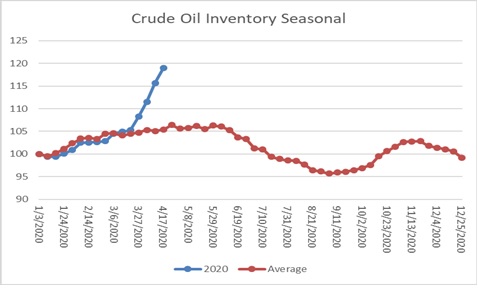

The above chart shows the annual seasonal pattern for crude oil inventories. The last six weeks have pushed stockpiles almost “off the charts,” although there is evidence to suggest the pace of inventory injections is starting to peak.

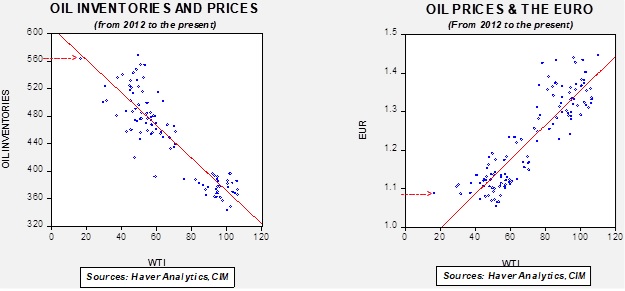

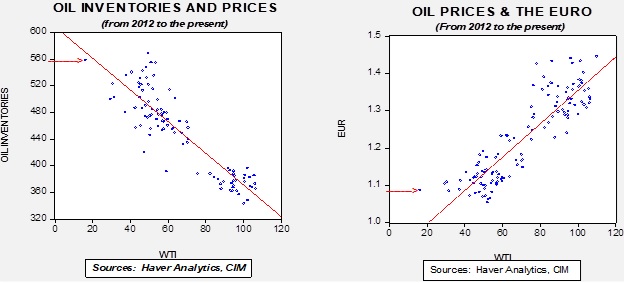

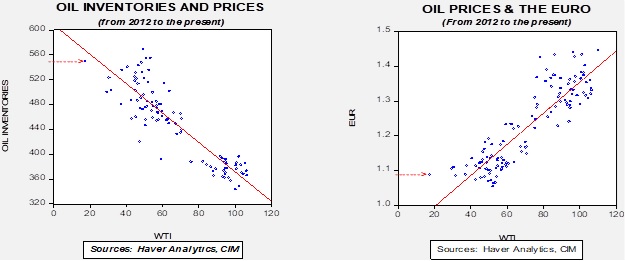

Based on our oil inventory/price model, fair value is $29.18; using the euro/price model, fair value is $44.58. The combined model, a broader analysis of the oil price, generates a fair value of $36.58. As we noted recently, the model output is less relevant as there is a non-linearity tied to the loss of storage capacity that cannot be fully captured with these models. At the same time, if storage remains available, the models would suggest upside for oil prices. We also note that the Eurozone could be roiled by German court decisions which could limit the flexibility of the ECB to support the Eurozone economy. This outcome would be bearish for the euro and may weaken it further, which would be bearish for oil prices.

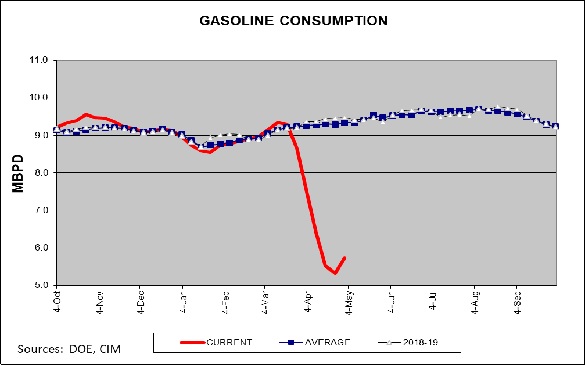

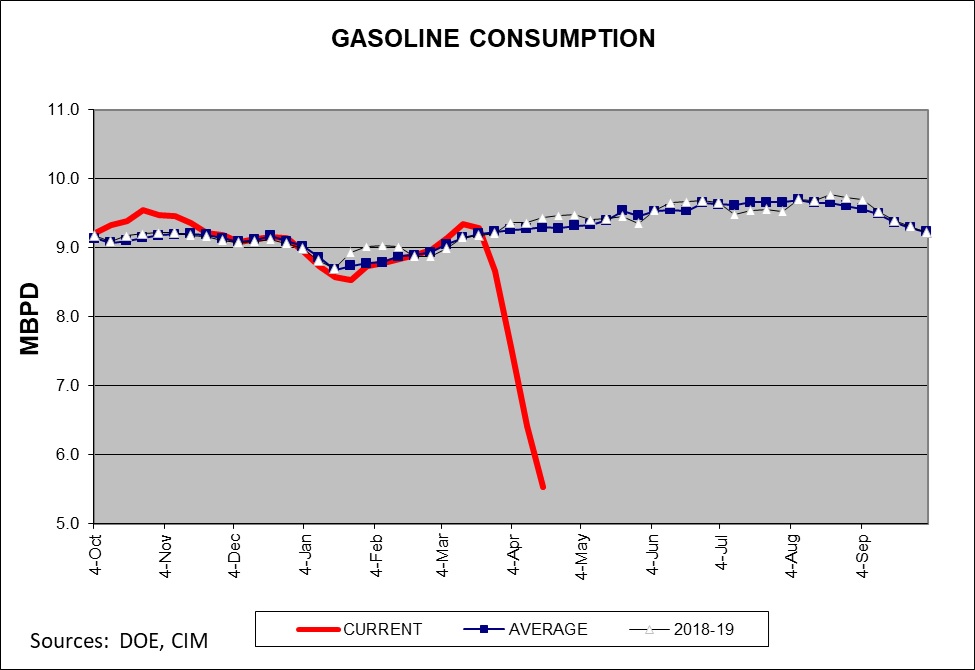

Although consumption remains depressed, gasoline data does show that a bottoming may be underway.

The weekly reporting is showing a steady decline in oil production. Media reporting is confirming this trend as well. The Fed has expanded its loan program to offer help to energy companies but there is little chance that it will be enough to protect smaller firms. Longer term, there is growing concern among oil companies that oil demand may never return to pre-COVID-19 levels. If that is the case, it will have profound effects on the energy industry. Between the slow recovery and climate change legislation, oil consumption may have already peaked. If so, higher cost reserves may not be recoverable. It isn’t just oil that is affected; coal is also affected because weak prices for oil and natural gas will further weaken demand for coal as well.

In international news, Iran’s OPEC governor suffered a severe brain hemorrhage. It is unlikely he will return to his post, but we doubt this will change Iran’s oil policy. Israeli sources suggest that Iran may be reducing its support for Syria. Recent bombing attacks by the IDF have brought little response from Tehran. Consequently, Israel has stepped up its attacks. We suspect two events have led to Iran’s pullback. The first is that the assassination of Qasem Soleimani has reduced Iran’s ability to manage the relationship with Hezbollah in Syria. Soleimani was a strong leader and his death may have created a leadership vacuum outside of Iran. Second, low oil prices and U.S. sanctions have damaged Iran’s economy to the point where it can no longer spend the funds necessary to maintain influence in Syria. If this trend continues, Russia and Turkey will vie for domination of Damascus. The Iraqi government has stopped payments to the Kurdistan Regional Government. Between the loss of these funds and lower oil prices, the Kurdistan government is near collapse. If it fails, we would not be surprised to see Turkey try to expand its influence. Most of the Gulf Cooperation Council states peg their currencies. This action brings stability and allows these nations, which often import nearly all their consumer goods, to maintain low prices. However, the decline in oil prices has raised fears that devaluations may be in the offing. If so, it could raise internal tensions in these countries.

Weekly Geopolitical Report – Revisiting Scheidel’s Horsemen: Part III (May 4, 2020)

by Bill O’Grady

In Part I of this report, we discussed Scheidel’s thesis on the events that reverse the normal trend of inequality and used this analysis to frame the COVID-19 pandemic. In Part II, we introduced the equality/ efficiency cycle and discussed the first issue that would be affected by a shift to equality. In this final Part III of the report, we will address the other four issues, discuss inflation and conclude with market ramifications.

Asset Allocation Weekly (May 1, 2020)

by Asset Allocation Committee

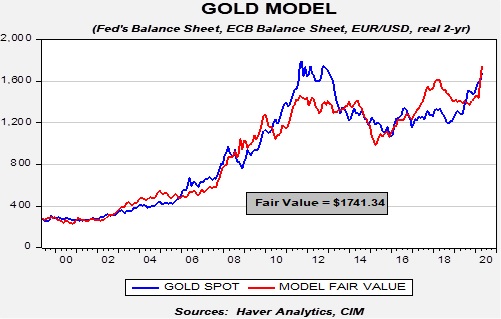

The policy response to COVID-19 has been mostly favorable for gold. Our gold model uses the balance sheets of the Federal Reserve and the European Central Bank, the EUR/USD exchange rate, and the real two-year T-note yield. The only variable that has been bearish for gold is the dollar, but the massive rise in central bank balance sheets and the drop in real yields has lifted the model’s fair value to 1,741.34.

In the coming months, we expect the fair value to rise; both the ECB and the Federal Reserve are likely to continue to expand their balance sheets, adding a broad spectrum of assets. We would also expect some modest declines in the real two-year T-note yield as inflation rises. Weakening the dollar may require direct action by the administration. Although this action may not occur this year, we would not be shocked to see it occur at some point in the future.

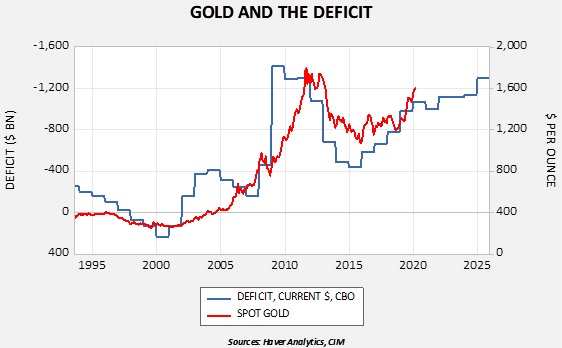

In addition, there is a long-term relationship between gold prices and the level of the fiscal deficit. Although the level of the current deficit does suggest that gold prices might be a bit overvalued currently, the likelihood of expanding deficits should offer underlying support for gold prices. The Congressional Budget Office recently increased its deficit forecasts; we still view them as conservative and would anticipate even higher deficits due to falling tax receipts and rising spending.

Therefore, our short- and long-term outlooks for gold remain positive.

Weekly Energy Update (April 30, 2020)

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

Here is an updated crude oil price chart. The oil market is showing signs of trying to consolidate in the mid-teens.

Oil prices continue to be affected by ETPs. The most popular ETP for crude oil, the United States Oil Fund, (USO, 17.91), has changed its investing procedures, now holding more contracts in the deferred calendar strip. The good news is that it is no longer so closely tied to the nearby contract and is thus less susceptible to price collapses and less affected by the roll yield issue. The bad news is that it is no longer a “play” on the nearby price of oil but is mostly now a position in the average price over several months. If this process continues, it should become less volatile in the future; on the other hand, if the market becomes backward at some point, it will underperform the nearby price. We also note it has engineered an 8:1 reverse stock split. U.S. investors are not the only parties to oil market turmoil. The Bank of China[1] (BACHY, 9.41) reports that its clients lost $1.0 billion on bullish oil positions. The Industrial and Commercial Bank of China (IDCBY, 13.43), the largest commercial bank in China by assets, has halted the sale of retail products in oil and gas.

Crude oil inventories rose 9.0 mb compared to the forecast rise of 12.7 mb.

In the details, U.S. crude oil production fell 0.1 mbpd to 12.1 mbpd. Exports rose 0.4 mbpd, while imports rose by the same amount. Refining activity rose 2.0%, a bit more than the 1.2% rise forecast. The inventory build was mostly due to continued elevated U.S. production.

The above chart shows the annual seasonal pattern for crude oil inventories. The last five weeks have pushed stockpiles almost “off the charts.” Although not totally unexpected, the current rise is at least consistent with the usual seasonal pattern; in early June, the divergence in seasonal patterns will become stark.[2]

Based on our oil inventory/price model, fair value is $30.66; using the euro/price model, fair value is $44.62. The combined model, a broader analysis of the oil price, generates a fair value of $37.26. As we noted recently, the model output is less relevant as there is a non-linearity tied to the loss of storage capacity that cannot be fully captured with these models, which has been clearly exhibited over the past week.

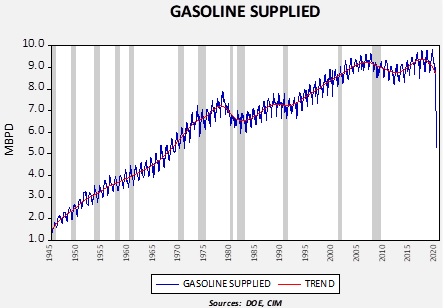

Here is a longer look at gasoline consumption.

This chart shows the amount of gasoline supplied to the U.S. since the end of WWII on a monthly basis. We have generated a trendline for the data. Until the 1979 Iran Crisis and the outbreak of the Iran-Iraq War, the trend in gasoline consumption moved relentlessly higher, even during recessions. There was a modest dip during the Gulf War in the 1990-91 recession and another decline in trend in the Great Financial Crisis. However, it is clear that what we are experiencing now has no historical comparison in the postwar era. We would expect a recovery to develop in the coming months, but the decline in consumption is extreme and will tend to weigh on the oil markets for months, at least.

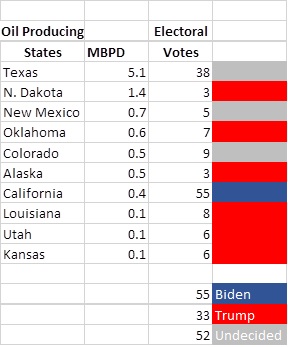

It is becoming clear that the federal government is probably not going to rescue the oil industry. The industry itself is divided, with the larger firms preferring to see smaller firms fail, allowing the larger firms to purchase their assets at depressed levels. Production levels are slowly falling. Although numerous proposals have been floated, opposition to the oil industry from the left, both establishment and populist, means passing support measures through Congress will be quite difficult. The best way to think about it is that political leaders, both at the White House and in Congress, have a limited amount of political capital. They want to spend it judiciously and get as much political support for the political capital they expend. It does look like the White House wants to support the oil industry but isn’t willing to use a lot of political influence (capital) to pay for that support. This table shows the top 10 oil-producing states along with their votes in the Electoral College and poll leanings from Real Clear Politics.

The last time Texas voted for a Democrat for president was Jimmy Carter in 1976. We would be surprised to see it flip this election, even if an oil bailout isn’t forthcoming.

Venezuela has a new oil minister. Tareck El Aissami has been appointed to the position by President Maduro. El Aissami replaces Gen. Manuel Quevedo, who has had the job for 28 months. Quevedo was also in charge of PDVSA, the state oil company; he lost that job too, being replaced by Asdrubal Chavez, the cousin of the late President Hugo Chavez. There is speculation that El Aissami, who is of Lebanese descent, may signal closer ties to Iran. It should also be noted that the U.S. has a $10 million reward for the arrest of El Aissami.

Although there are expectations that Saudi Arabia is preparing to cut output, Russia reported that its March oil exports to China rose 31% from last year, while Saudi imports fell 1.6%. Our thesis is that the two nations are fighting a market share war for the Chinese market; this news might reduce Riyadh’s ardor for cutting output.

It’s not just the oil industry that has been hit by low oil prices. Corn farmers are facing a drop in demand for ethanol, which will tend to undermine demand for the grain. The after-product of distilled corn, distillers grain, means that corn distilled into ethanol isn’t completely consumed by the industry. Thus, if cattle demand improves, farmers will still have a market for their corn; exports would also help. Still, the loss of ethanol demand is a problem for farmers.

Our current outlook is that oil prices will continue to hold in the teens for the next month or so and gradually improve in the coming months. The primary risk to oil remains the exhaustion of storage capacity, but we should see improving demand and supply curtailments eventually begin to allow prices to recover. The speed of the recovery will be partly dependent on reducing the current storage overhang, which will take months. Nevertheless, barring a situation where there is absolutely no storage to be utilized, another drop into single-digit prices is becoming less likely.

[1] Not the central bank of China, known as the People’s Bank of China, or PBOC

[2] Regular readers may notice the average is a bit different in this chart. We had a data issue which has been resolved. The overall pattern hasn’t changed, however.

Weekly Geopolitical Report – Revisiting Scheidel’s Horsemen: Part II (April 27, 2020)

by Bill O’Grady

In Part I, we introduced Walter Scheidel’s four horsemen and examined the impact of COVID-19 using his framework.[1] This week, we introduce the equality/ efficiency cycle and discuss the first issue that would be affected by the reversal of this cycle.

COVID-19 and the Equality/Efficiency Cycle

We postulate that economies pass through cycles of equality and efficiency. We developed this concept based on the seminal work of three scholars. The first strand is the idea of the equality/efficiency tradeoff, which comes from Arthur Okun.[2] He argued that societies face a tradeoff between equality and efficiency. Efficiency is necessary for growth, while equality is required for political and social stability. However, there is no evidence that Okun saw this tradeoff as a cycle; instead, he saw it as two competing forces to be constantly balanced.

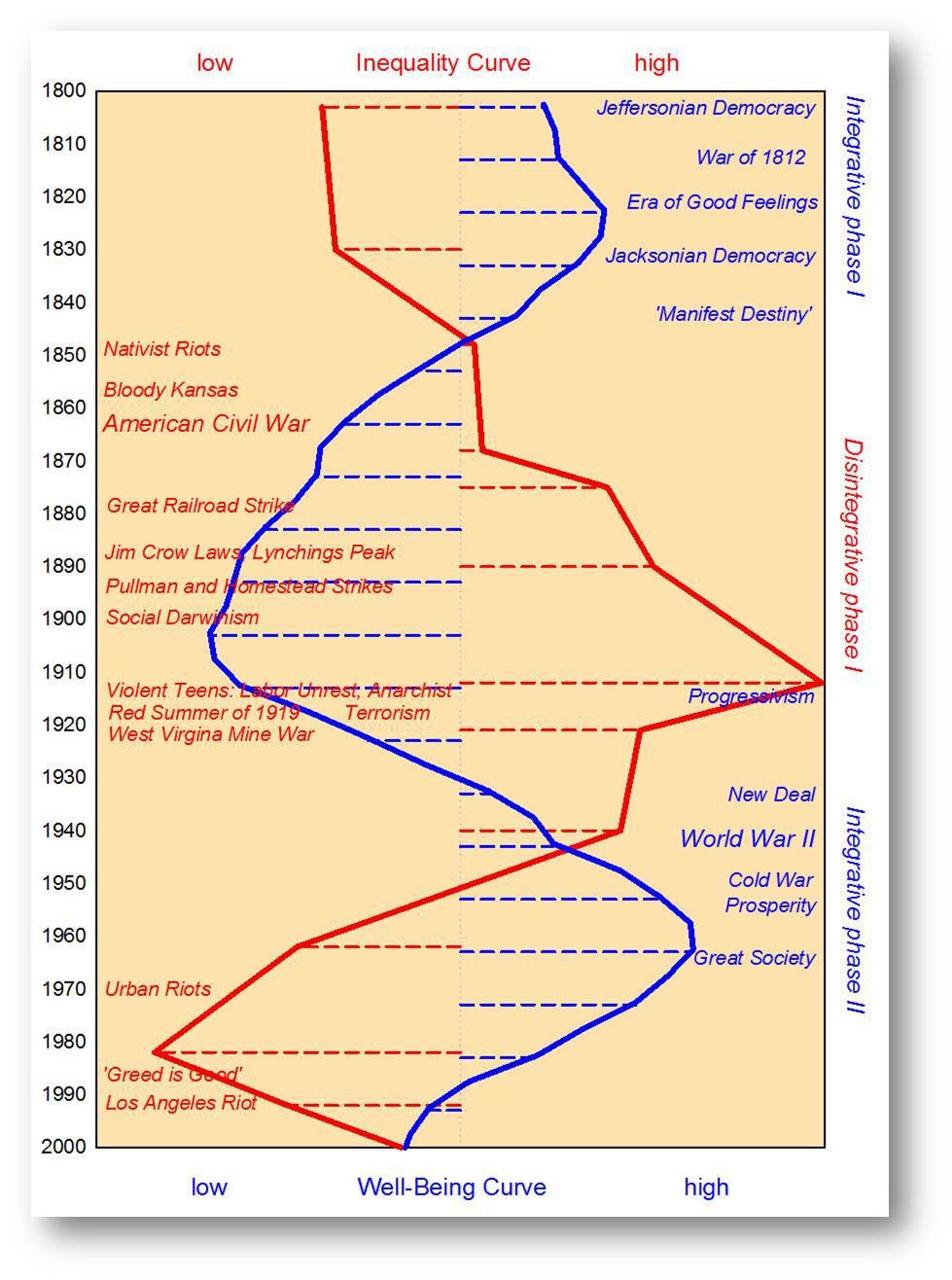

The second source of our postulate is from Peter Turchin, who suggested that countries cycle between periods of greater or lesser equality. In the following chart, Turchin shows this cycle in the U.S. from the early 1800s to 2000. Measuring inequality (red line) is a simple calculation that originated with Kevin Phillips. It is the ratio of the largest fortune in the U.S. relative to average household wealth. The well-being line (blue line) is the detrended and log-transformed level of social optimism, which is the average age of marriage, along with the wages of production workers divided by per-capita GDP, life expectancy and average height. The chart shows that well-being is inversely correlated to inequality.

The third source of our thesis comes from Walter Scheidel, who suggests that efficiency cycles are the norm due to the power of capital. Efficiency continues until it is stopped by one of four major disruptions: mass mobilization war, revolution, societal collapse or pandemic.

Therefore, our thesis is the following:

- Societies face a tradeoff between equality and efficiency.

- This tradeoff leads to cycles in which the goals of one or the other dominate.

- The natural course is for efficiency to dominate because capital tends to accumulate economic and political power over time.

- What reverses the dominant trend is a cataclysmic event, i.e., mass mobilization war, revolution, collapse of social order, pandemic.

- What reverses an equality cycle is persistent inflation, which is usually supported by equality policies of trade impediments, immigration control and regulation.

[1] Scheidel, Walter. (2017). The Great Leveler: Violence and the History of Inequality from the Stone Age to the Twenty-First Century. Princeton, NJ: Princeton University Press.

[2] Okun, Arthur. (1975). Equality and Efficiency: The Big Tradeoff. Washington, D.C.: Brookings Institution Press.

Asset Allocation Weekly (April 24, 2020)

by Asset Allocation Committee

As the COVID-19 pandemic continues to evolve, we are watching to see how the disease will affect the economy longer term. Of course, projections of this sort are highly probabilistic; factors could and will likely emerge that could render these projections irrelevant. At the same, ignoring potential long-term consequences of the virus could lead to improper decisions, failing to fully appreciate the changes the disease has caused.

In this week’s report, we will look at demographics. Demographic analysis is important because it is a “deep background” of what affects markets. Demographic change tends to occur slowly but can be rather easily forecast far into the future. Thus, if a variable is sensitive to changes in the population, it can be rather simple to forecast trends well into the future.

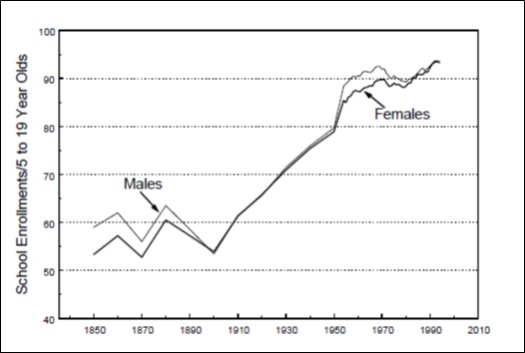

The baby boom, encompassing Americans born during 1946-64, has always been the “pig in the snake” for demographers. When this generation reached school age, the number of elementary enrollments jumped. Later, in the mid-1970s, enrollment fell and led to empty school buildings.

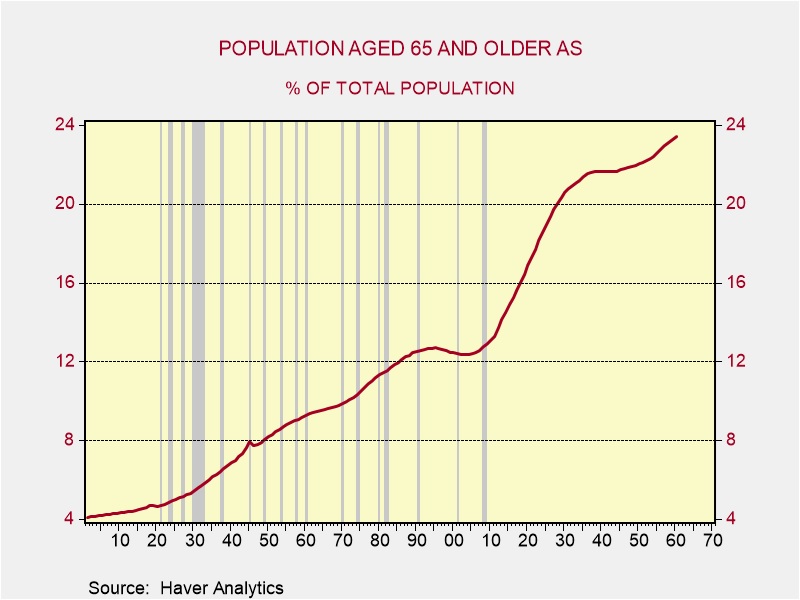

The current age range for the baby boom is 56 to 74. In another seven years, this entire generation will reach retirement age. The chart below shows that the population share 65 years and older is set to rise rapidly for the next two decades. Demographers for years have been warning that the mass retirement of this generation would cause problems in the labor market, predicting that employers would be scrambling to fill positions.

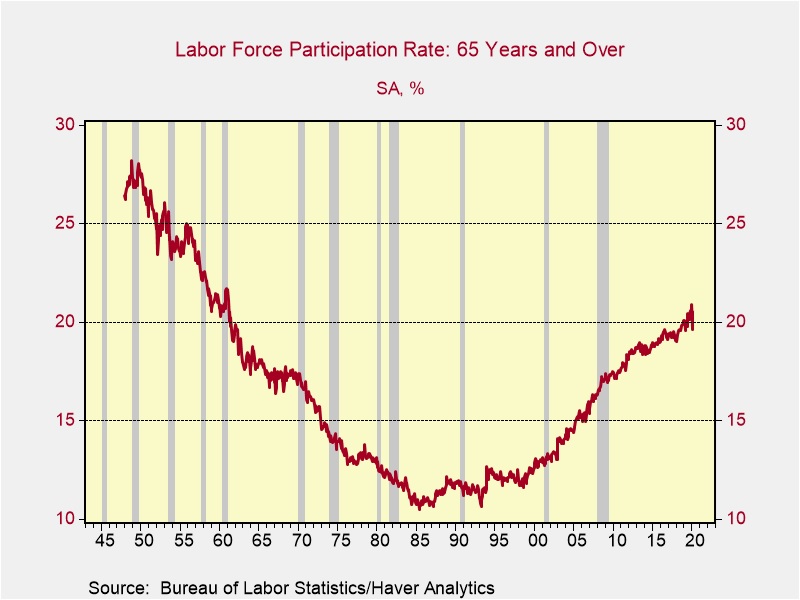

That hasn’t happened yet for a number of reasons—globalization has allowed firms to tap labor resources abroad, immigration has offset some of the retirement numbers, and baby boomers have continued to work longer.

At the turn of the century, the participation rate[1] was around 12.5%. It has steadily increased to over 20%, although it has recently declined. Essentially, baby boomers, which include nine years of this group, appear to have remained in the labor force. We suspect there are two reasons. First, as life expectancies have increased, wealthier boomers, who are probably healthy, likely wanted to remain working. Second, less affluent boomers probably needed to keep working as long as possible due to the lack of retirement saving.

COVID-19 could reverse this participation trend. The fatality rate of the virus tends to rise with age. Older workers who have stayed in the labor force may decide that the threat of infection is too high and thus opt to retire. If a broad-spectrum vaccine is developed, this potential trend could be thwarted, but if COVID-19 mutates like influenza and requires an annual vaccination of varying effectiveness, a vaccine might not be enough to prevent older workers from exiting the workforce. A decline in older worker participation would reduce the labor force; if that action occurs along with restrictions on immigration and trade impediments, all tenets of deglobalization, we would expect the labor share of national income to rise.

[1] The participation rate is the labor force (employed + unemployed seeking employment)/population eligible to be in the labor force.

Business Cycle Report (April 23, 2020)

by Thomas Wash

The business cycle has a major impact on financial markets; recessions usually accompany bear markets in equities. We have created this report to keep our readers apprised of the potential for recession, which we plan to update on a monthly basis. Although it isn’t the final word on our views about recession, it is part of our process in signaling the potential for a downturn.

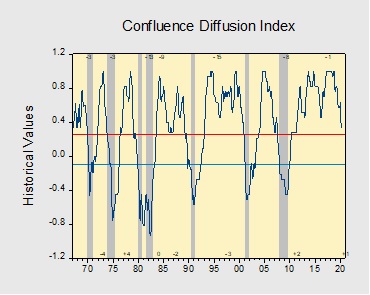

In March, the diffusion index nearly fell into recession territory. The weakness in the report was primarily due to the coronavirus pandemic, turmoil in the financial markets and the Saudi-Russia oil dispute. Last month, confirmed cases of COVID-19 in the U.S. rose from 74 at the start of the month and grew to over 180,000. Meanwhile, the oil price war between Saudi Arabia and Russia led oil prices to fall to a near-20-year low. As a result, equities dropped and Treasuries rallied. The interest rate on the 10-year T-note fell below 1.0% for the first time ever. Additionally, the manufacturing sector showed mixed signals as a slowdown in delivery times reflected positively in the report despite a drop in new durable goods orders. The employment numbers were abysmal and will likely be worse in next month’s report. In this report, six out of the 11 indicators were in recession territory. The reading for March fell to +0.333 from +0.57, a hair above the recession signal of +0.250.

The chart above shows the Confluence Diffusion Index. It uses a three-month moving average of 11 leading indicators to track the state of the business cycle. The red line signals when the business cycle is headed toward a contraction, while the blue line signals when the business cycle is headed toward a recovery. On average, the diffusion index is currently providing about six months of lead time for a contraction and five months of lead time for a recovery. Continue reading for a more in-depth understanding of how the indicators are performing and refer to our Glossary of Charts at the back of this report for a description of each chart and what it measures. A chart title listed in red indicates that indicator is signaling recession.

Weekly Energy Update (April 23, 2020)

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

Given the remarkable events of the past week, we are adjusting the usual format of this report. We[1] have been covering energy for over three decades and never imagined that we would see prices for actively traded futures fall into negative territory.

The sharp drop in prices was mostly due to forced selling by exchange-traded products (ETPs).[2] As a reminder, there are no grantor trusts in oil, which would require the trust to hold actual barrels of oil; instead, oil ETPs usually create their products in the futures markets. Although there are various methodologies in operation, they all work, to a greater or lesser degree, by rolling contracts in different oil futures months. The most commonly used ETPs normally operate by holding the front month contract and, at some point near expiration, “rolling” into the next month. This gives an approximate constant long position in crude oil. The total return on these products come from three sources—the price of oil itself, the interest on margin,[3] and the “roll yield.” If the calendar curve for oil prices is backward (that is, the nearby futures trade at a premium to the deferred contracts), there is a positive roll yield. At each roll, under these conditions, the ETP will be purchasing a cheaper contract. If nothing changes, the cheaper contract will rise in value and benefit the ETP holder. The opposite condition, where the nearby futures trade at a discount to the deferred futures contracts, is known as contango. That is the current situation in the oil market. In this case, there would be a negative roll yield. Contango usually occurs when there is too much prompt supply relative to demand.

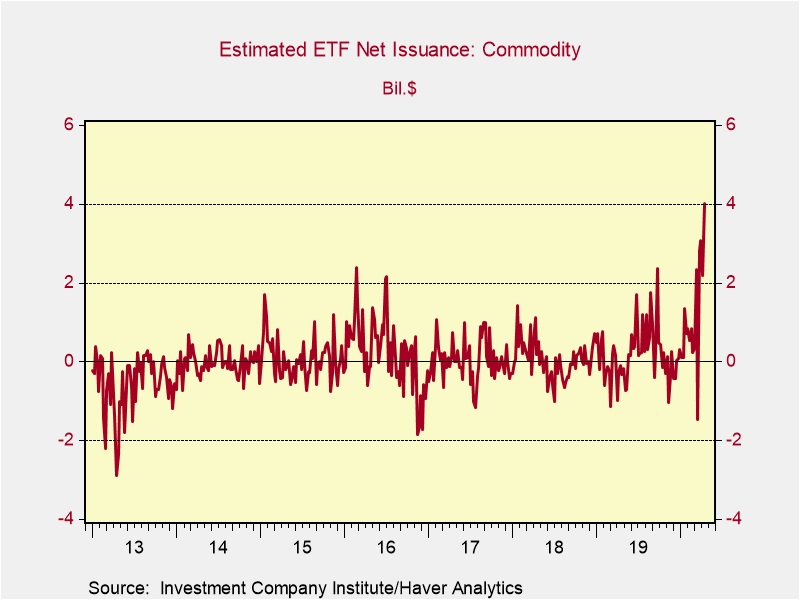

There have been reports of strong inflows into oil ETPs. Although we don’t have a breakdown by commodity, there has been a clear surge in flows. The chart below shows ETF net issuance for commodity ETPs on a weekly basis. The recent surge is notable and market commentary would suggest the lion’s share of these flows were likely into oil ETPs.

It is likely that retail investors viewed low oil prices as unsustainable and wanted to establish continual long positions for the eventual turn in prices. If not for the roll yield, this would be a reasonable strategy. But the roll yield under conditions of contango increases the cost of holding the position.

As the ETPs began the roll process, where they sold their long positions in the nearby futures and bought the next deferred contract, there was a large long position that needed to be liquidated. Unfortunately, there was little place to put the oil as the ETP doesn’t take delivery of the commodity. As of April 10, nearly 70% of storage at the Cushing, OK, delivery hub for the CME crude oil contract was utilized; it is likely that much of the rest of it was already leased. The ETPs were forced to sell to buyers that required the long to “pay” them for taking the oil off their hands, leading to the historic negative price for crude oil.

Some will ask, “is this a real price?” In one sense, no. We won’t see less than free gasoline anytime soon. The 2nd or 3rd next nearby futures contract is a better reflection of what is a normal price under current conditions. On the other hand, back in our futures days,[4] we remember a squawk box conference where a futures analyst suggested a price of a commodity had become “artificial”…to which a broker responded, “the margin calls, sir, are quite real.” There was damage to some investor accounts due to this debacle, to say nothing about participants in futures that made outsized gains and losses unexpectedly; imagine how it would be if a long equity position could see the stock price fall below zero. I am not sure this will ever happen again, but the continued squeeze on storage means that at every expiration there is a chance that something like this could be repeated.[5] If it does, the CME contract is in grave danger; we could see a shift to using Brent futures, which exhibited none of this behavior because it has wider storage options, including a cash settlement. The broader issue is that oil fundamentals are abysmal and until supply contracts and demand expands, prices will remain under pressure.

Crude oil inventories rose 15.0 mb compared to the forecast rise of 14.0 mb.

In the details, U.S. crude oil production fell 0.1 mbpd to 12.2 mbpd. Exports fell 0.5 mbpd, while imports declined 0.7 mbpd. Refining activity fell 1.5%, a bit less than the 2.0% decline forecast. The inventory build was mostly due to the continued collapse in refinery operations.

The above chart shows the annual seasonal pattern for crude oil inventories. The last four weeks have pushed stockpiles almost “off the charts.” Although not totally unexpected, the divergence in seasonal patterns could diverge in a bearish fashion in early June.

Based on our oil inventory/price model, fair value is $33.63; using the euro/price model, fair value is $44.77. The combined model, a broader analysis of the oil price, generates a fair value of $38.70. As we noted recently, the model output is less relevant as there is a non-linearity tied to the loss of storage capacity that cannot be fully captured with these models, which has been clearly exhibited over the past week.

As promised, here are a couple charts that look at U.S. oil demand. The chart below shows the four-week average of gasoline supplied to the distribution system. The combination of rising inventories and lower demand has pushed up the current days to cover to nearly 48 days; the average is 25 days.

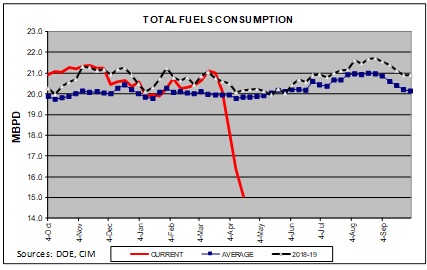

Total fuel consumption is plunging.

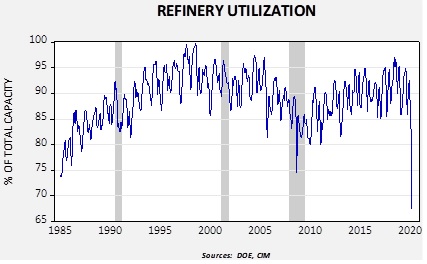

This is a longer-term view of refinery activity.

The last time we saw a drop of this magnitude was during the depths of the Great Financial Crisis. Over the past four weeks, refineries have reduced their oil consumption by 3.4 mbpd, far exceeding the drop of 0.6 mbpd in production.

So, now that oil prices have fallen precipitously, what happens now? There is a good chance that prices stay low for a rather long time. The market is building a major supply overhang that will take a long time to remove. This supply problem is being exacerbated by collapsing demand caused by the policies to reduce the spread of COVID-19. Thus, barring some event that reduces supply or boosts demand quickly, oil prices will likely languish at least into late summer. What sort of events could support a recovery in prices?

A geopolitical event in the Middle East. The potential for a disruption in oil flows is always possible. Lately, Iran has become more aggressive in harassing shipping in the Persian Gulf. The White House has warned Iran about this behavior. We doubt Iran wants a full-scale conflict with the U.S., and we doubt the U.S. wants a war either. There is the potential that both parties could stumble into a conflict, but it isn’t likely and would not be a reason to buy oil at this point.

Governments could absorb some of the overhang for strategic reserves. Such purchases would make sense. Oil prices are unusually cheap and buying emergency storage under such conditions is ideal. Australia has announced a plan to buy oil and store it in the U.S. Strategic Petroleum Reserve (SPR). It plans to purchase AUD 94.0 mm ($59 mm), roughly four million barrels of oil (at WTI $15 per barrel). China has announced purchases as well, although the actual level of injections into strategic reserves is unknown. The Trump administration has suggested SPR purchases but hasn’t been able to convince Congress to allocate funding. By itself, these purchases would not probably spark a recovery, but the buying would help.

Governments could take more aggressive actions to reduce supply. In addition to the government taking direct ownership stakes in oil companies to keep them afloat, there are reports that the administration is considering buying oil reserves from producers and simply not developing the purchased reserves, selling them at a later date when prices have recovered. This action would give cash-strapped producers cash for those assets and, at the same time, reduce future supply. There is no doubt energy-producing regions of the U.S. could use the relief. However, this plan is fraught with risk. It is not hard to imagine that a future administration could have a different policy on oil production and simply never sell or develop the purchased reserves. At the same time, this policy could have the same issues as adding oil to the SPR; it works in the short run but fashioning a policy to sell the reserves or sell oil out of the SPR has never really been done. Nevertheless, there is a chance that radical action may be taken.

Liquidate. Deep recessions and depressions reveal who is a marginal producer and who has staying power. Strong firms would likely prefer a wave of bankruptcies that would allow them to acquire assets cheaply. The fact that there is opposition to support from the oil industry suggests this sentiment remains strong. It would probably last until the strongest producers face bankruptcy; then support would be broadly welcomed. To some extent, this is the other side of the aggressive government action.

Overall, we have probably seen the lows in oil prices. It may be a few months before we see prices improve. The key factor for recovery will be a significant recovery in economic activity, which will likely come by autumn. Until then, prices will likely range in the teens into the summer.

In other news, the U.S. has ordered Chevron (84.44, +2.80) to halt operations in Venezuela by December and stop all production now. Although we doubt this will help reduce supplies all that much, it will disappoint the company, which had held on in the country to try to benefit from if or when the Maduro government finally leaves.

[1] Of course, this is Bill “talking” in the royal sense.

[2] This term encompasses exchange-traded funds, exchange-traded notes and grantor trusts.

[3] Margin on June futures is $6,400 per contract. There are 1k barrels per contract, and so, at $20 per barrel, the total value of a futures contract is $20k. The ETP fully funds the contract but is only required to maintain the margin. The rest is usually held in T-bills which generate some interest income.

[4] Again, Bill using the “imperial our.”

[5] BTW, if you were wondering if a retail client could buy and hold crude oil, here is a story about that.