[Posted: 9:30 AM EDT] After a choppy week, financial and commodity markets are rather quiet this morning. There were a couple of news items of note. The BOJ, as anticipated, left policy unchanged. The vote was 7-2, with the two dissenters calling for tighter policy. However, the two outliers, Takahide Kiuchi and Takehiro Sato, will be leaving the BOJ board after this meeting and will be replaced by allies of Governor Kuroda. Thus, the governor will face less internal pressure to begin withdrawing stimulus. The news is modestly bearish for the JPY.

Greece has avoided default by reaching an agreement with its international creditors. The country will receive €8.5 bn in bailout aid, allowing it to make €7.0 bn in debt repayments. The primary sticking point was the IMF. The international lender wants European creditors to give Greece debt relief. German leaders are loath to do this, especially with elections looming in the fall. The IMF formally joined the agreement and will contribute €2.0 bn in new loans. However, the IMF won’t actually disburse the funds until the EU develops a plan for debt relief. Germany wants IMF participation for two reasons. First, the Merkel government fears that the EU won’t hold Greece to austerity, and second, the IMF gives the bailout/austerity package an international imprimatur.

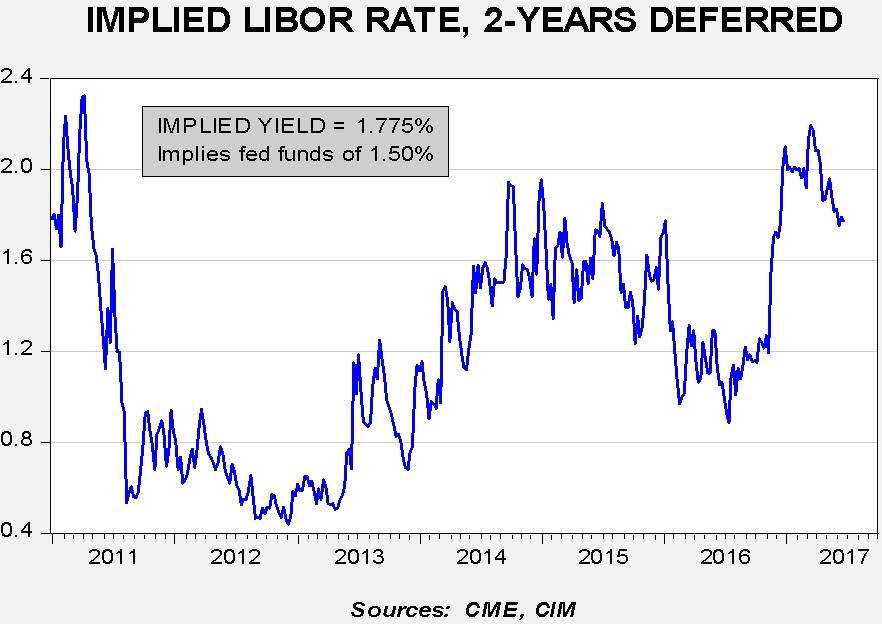

In the wake of the FOMC meeting, the deferred Eurodollar futures market was essentially unchanged. This chart below shows the current pricing for three-month LIBOR in two years. After the election, the implied rate jumped to levels not seen since 2011 on expectations of fiscal expansion. However, as those expectations erode, we are seeing expected yields decline. The fed funds rate implied from the Eurodollar futures suggests only one more rate hike. The dots plot clearly suggests that policymakers expect to raise rates more than the market expects so there is a danger that policy may become too tight and trigger a recession.

[Posted: 9:30 AM EDT] There were three items dominating the overnight news. First, the shooting at the GOP baseball practice yesterday continues to reverberate. We will have more to say about this event in the future but it is further evidence of deep divisions within American society that show no signs of improving. Second, the BOE followed script and held policy steady. However, the vote was 5-3, with the dissenters calling for rate hikes. The strength of dissent caught the markets by surprise; the GBP rallied off its lows (the dollar has been stronger today) and Gilt yields jumped. Financial markets in Britain have been leaning toward rate cuts. The high level of dissent suggests that cuts will be difficult. Third, we are seeing further fallout from yesterday’s FOMC meeting; the dollar is up, gold and equities are lower and Treasury yields, which fell yesterday, are recovering a bit this morning.

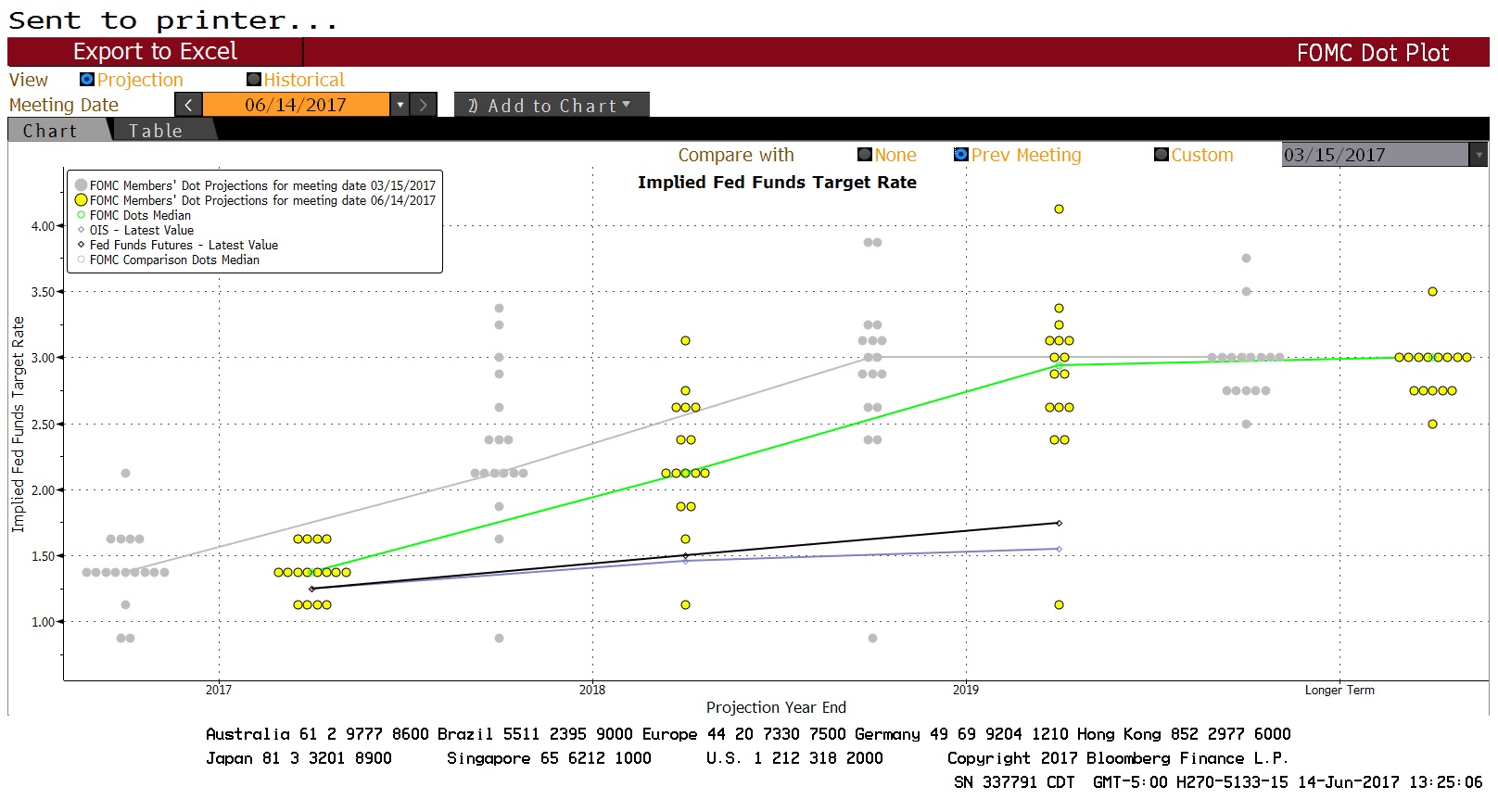

The FOMC did as expected, raising rates by 25 bps. The comments about the economy remain upbeat but the lack of inflation was noted. The big news was that the balance sheet reduction is expected to start later this year, perhaps as soon as September. At some point this year, which remains unspecified, the Fed will begin allowing the balance sheet to decline by $10 bn per month, increasing by the same amount every three months until it reaches a maximum decline rate of $50 bn per month within five quarters. There will be a 60/40 split on Treasury and mortgages, respectively. We do have concerns about the balance sheet; in theory, since most of QE has been sitting innocuously on commercial bank balance sheets, removing it shouldn’t be a big deal. In reality, we simply don’t know how the market will react. If the behavior is symmetrical, it should “double down” on the idea that the Fed is tightening policy. There was one dissenter, Minneapolis FRB President Kashkari, who wanted to maintain the current rate.

Here are some relevant charts:

(Source: Bloomberg)

This shows the dispersion of the dots chart. The green line plots the median from yesterday’s meeting, while the gray shows the previous meeting. There wasn’t any change for the next two years but a modest decline in 2019. The median does suggest a 2.25% peak rate for next year, with only one more hike forecast this year and at least three hikes would be scheduled for next year. The market doesn’t expect this pace of hikes.

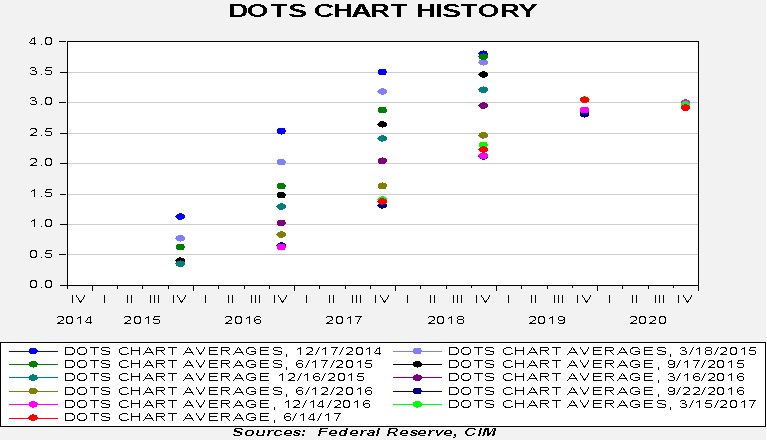

Here is our average dots chart:

The most recent dot is in red. The average suggests very little change in projections from the FOMC. The history of the dots chart is one of a steady decline in projections. However, for the past several quarters, there has been a stabilization of expectations, suggesting the FOMC is becoming comfortable with its policy path.

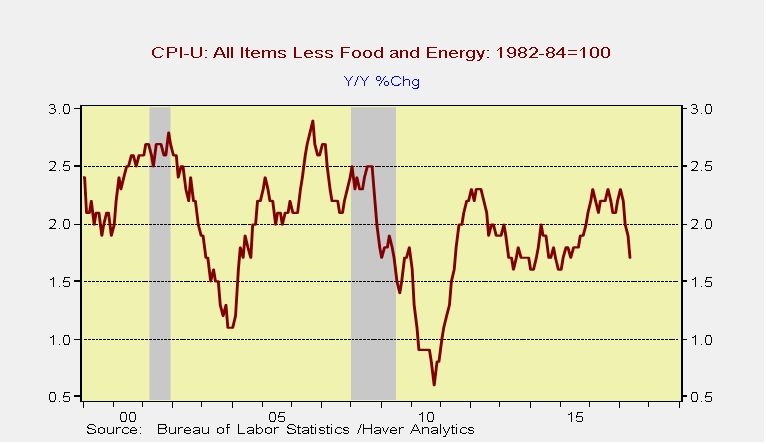

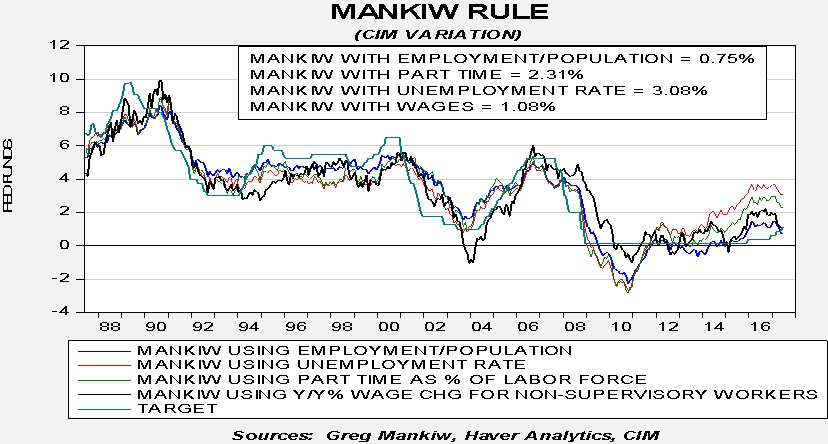

With the release of the CPI data and yesterday’s FOMC action, we can upgrade the Mankiw Rule models. The dip in the core CPI rate (see below) did affect the Mankiw Rule model results.

The Mankiw Rule models attempt to determine the neutral rate for fed funds, which is a rate that is neither accommodative nor stimulative. Mankiw’s model is a variation of the Taylor Rule. The latter measures the neutral rate using core CPI and the difference between GDP and potential GDP, which is an estimate of slack in the economy. Potential GDP cannot be directly observed, only estimated. To overcome this problem with potential GDP, Mankiw used the unemployment rate as a proxy for economic slack. We have created four versions of the rule, one that follows the original construction by using the unemployment rate as a measure of slack, a second that uses the employment/population ratio, a third using involuntary part-time workers as a percentage of the total labor force and a fourth using yearly wage growth for non-supervisory workers.

Using the unemployment rate, the neutral rate is now 3.08%. Using the employment/population ratio, the neutral rate is 0.75%. Using involuntary part-time employment, the neutral rate is 2.31%. Using wage growth for non-supervisory workers, the neutral rate is 1.08%. The labor data is mixed, with the employment/population ratio falling and wage growth stagnant, while the unemployment rate fell and involuntary part-time employment was steady. The drop in core CPI has led to lower Mankiw neutral rate estimates across the board.

To a great extent, the issue for policymakers remains the proper measure of slack. The danger for the financial markets is if the proper measure is wage growth or the employment/population ratio but policymakers believe slack is best measured by involuntary part-time employment or the unemployment rate. If that is their measure, policymakers will likely overtighten and prompt a recession. For the past couple of years, this issue has been mostly academic. Regardless of the measurement of slack, policy was generally accommodative. Now, using either wage growth or the employment/population ratio, monetary policy has achieved neutrality. If rates are raised as projected by the dots chart, assuming no change in inflation, the policy rate will reach a level consistent with tight policy with another two rate increases. Thus, we are now entering a more dangerous period for the economy where a policy mistake will matter.

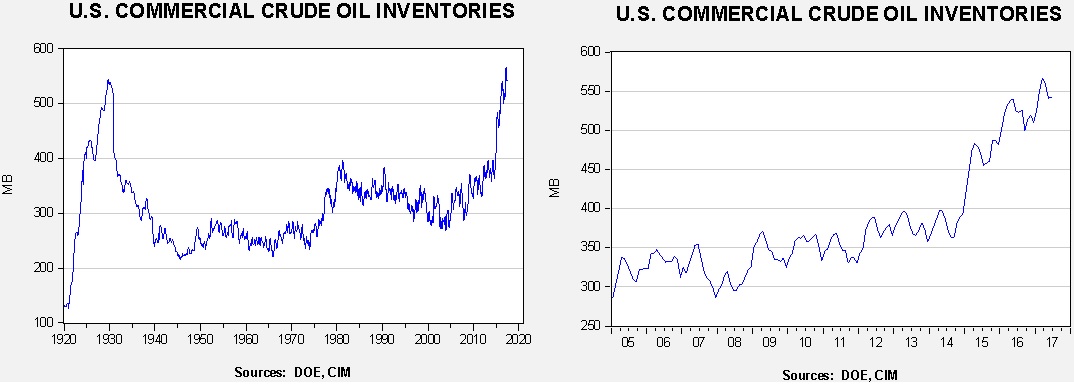

U.S. crude oil inventories fell 1.7 mb compared to market expectations of a 2.3 mb draw.

This chart shows current crude oil inventories, both over the long term and the last decade. We have added the estimated level of lease stocks to maintain the consistency of the data. As the chart shows, inventories remain historically high but they are declining. We also note that, as part of an Obama era agreement, there was a 0.4 mb sale of oil out of the Strategic Petroleum Reserve. This is part of a $375.4 mm sale (or 8.0 mb) done, in part, to pay for modernization of the SPR facilities. International agreements require that OECD nations hold 90 days of imports in storage. Due to falling imports, the current coverage is near 140 days. Taking that into account, the draw would have been 2.1 mb, which is near forecast.

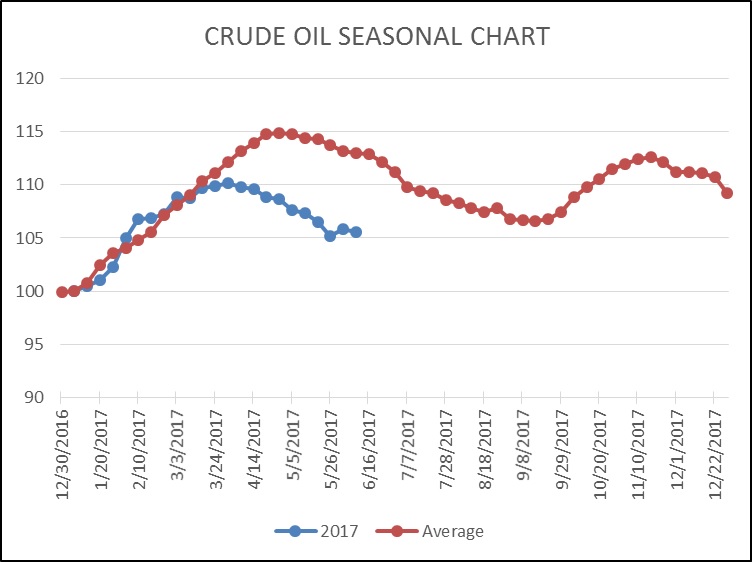

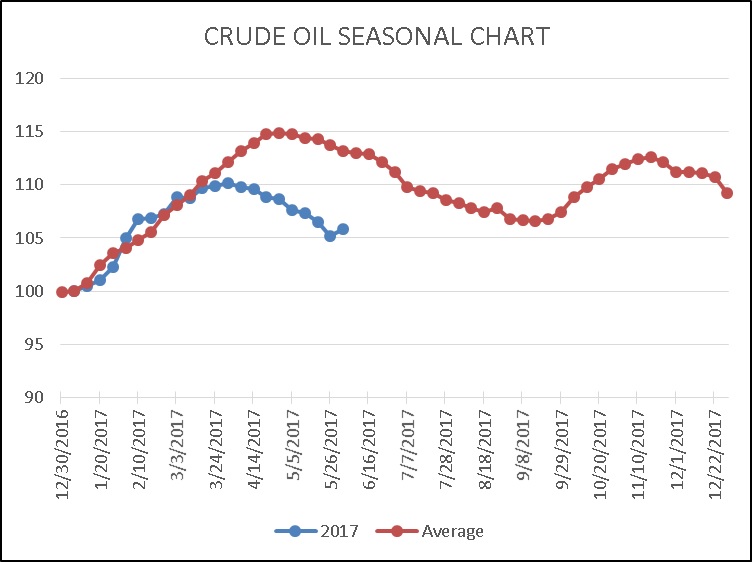

As the seasonal chart below shows, inventories are usually well into the seasonal withdrawal period. This year, that process began early. Although the actual level of stockpiles remains quite high, we have seen rather sharp stock declines until the past two weeks. We would expect the draws to increase as the recent rise in imports should fade.

(Source: DOE, CIM)

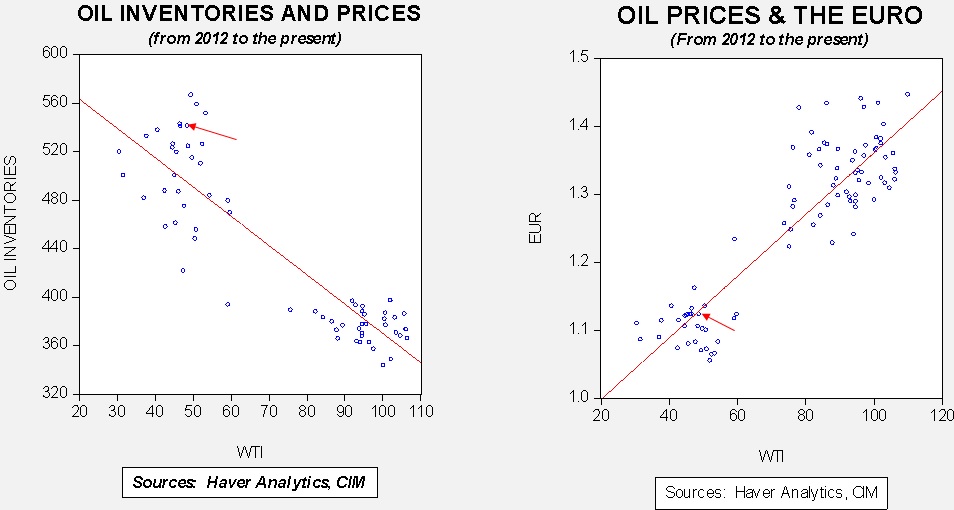

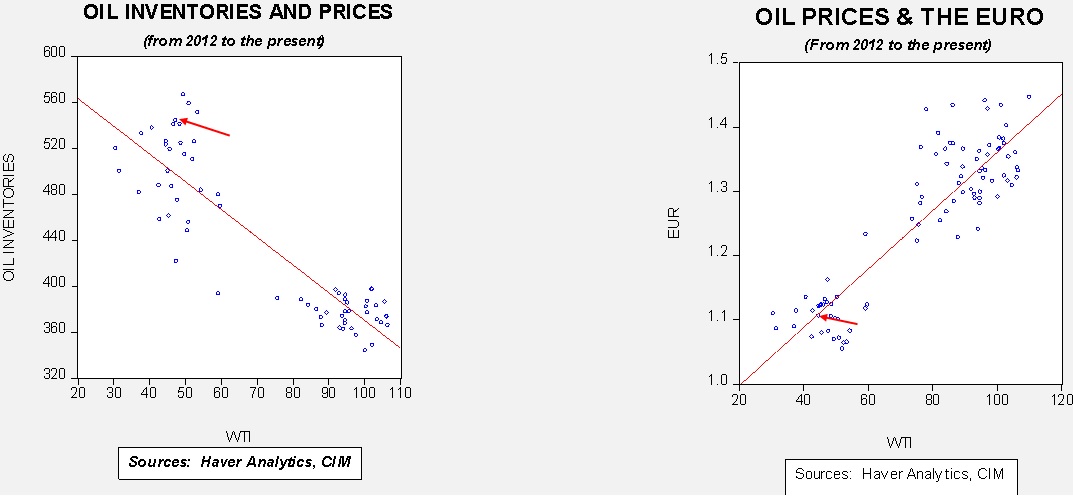

Based on inventories alone, oil prices are overvalued with the fair value price of $37.65. Meanwhile, the EUR/WTI model generates a fair value of $52.56. Together (which is a more sound methodology), fair value is $48.00, meaning that current prices are well below fair value. Currently, prices are below our expected trading range; we view oil prices as attractive on a short-term trading basis.

(Source: Bloomberg)

This chart shows the nearest WTI futures price. We have drawn a box between $45 and $55 per barrel. Note that since early October, nearly all prices fall within this range. This range has developed because OPEC’s cuts are being offset by rising U.S., Canadian and Brazilian output, leaving a mostly balanced market. As the chart shows, prices at this level have been attractive entry points. Of course, the risk is that we are seeing a downside breakout but we view further weakness as unlikely without strong evidence of OPEC cheating. Thus, a recovery should develop in the coming weeks.

[Posted: 9:30 AM EDT] There is breaking news at the time of this writing. A gunman shot at Congressional members and staffers at a baseball practice in suburban Virginia. The Congressional baseball game is one of the few bipartisan social events in Washington. Although the situation is evolving, early reports indicate at least five people were shot. The most notable is Steve Scalise (R-LA), the GOP House Whip, who was reportedly shot in the hip. Scalise is the third-highest ranking member of the House GOP leadership. His injuries are not considered life threatening. Although not confirmed at this time, there are reports the shooter was also shot and has been “neutralized” and is in custody.

Today is FOMC day. The Fed concludes its policy meeting with near certainty that the central bank will raise rates. This is a meeting with a press conference, new economic forecasts and a new dots plot. We don’t expect the Fed to change the dots plot too much; if so, the last plot implied one more hike this year, assuming a 25 bps hike today. Although we don’t expect details on shrinking the balance sheet today, we may hear more about that in the press conference. The FOMC is striving for transparency to preclude adverse market effects. Fed funds futures put the odds of a hike today at 92.7%. The odds of an additional hike in September are only 21.7% and, assuming no change until year’s end, a December move is currently priced at 34.3%. In fact, we don’t get a greater than 50% likelihood of a rate increase until the June 2018 meeting. Thus, anything suggesting a higher probability of a rate hike this year might be taken as hawkish.

CPI and retail sales for the U.S. came in soft (see below for details); the dollar rolled over on the news and interest rates declined. Gold prices also rose, but the yellow metal may also be reacting to the aforementioned shooting.

Oil prices are coming under pressure again this morning. The proximate cause was a report from the American Petroleum Institute (API) that crude oil inventories rose last week. The API report, based on a non-compulsory survey, comes out the evening before the official data from the DOE. The two series can disagree but inventory increases this time of year are unusual and thus bearish. However, on a longer term basis, the International Energy Agency (IEA), a division of the OECD, indicated today that the current inventory overhang will persist this year despite OPEC efforts to cut output. Rising production from Brazil, the U.S. and Canada are partially offsetting OPEC cuts. The IEA indicated that OECD stocks of oil rose 18.6 mb in April and are 292 mb above the five-year average. The IEA estimates that oil stocks won’t fall to their five-year average until March 2018 and this only occurs if OPEC maintains its production constraint. Industry reports suggest that U.S. production growth will stall the closer oil prices get to $40; although such a drop is possible, we expect a weaker dollar to mitigate downside risk in oil prices. We will have our usual recap of the oil data in tomorrow’s Daily Comment.

The debt ceiling is a looming threat; as we have noted in earlier reports, the Treasury is suggesting that the government will enter a partial shutdown by the first half of September without action taken to raise the debt ceiling. This issue has become an inter-party conflict within the GOP as the Freedom Caucus is proposing a $1.5 trillion increase in the ceiling, $1 trillion less than what the White House is requesting. The lower ceiling would lead to the exhaustion of borrowing capacity soon after the mid-terms. The White House would like to avoid further drama with a higher ceiling. We would expect a compromise, although the more entrenched positions become the longer we may go before a deal is reached. What is significant in this problem is that the battle is occurring within the GOP and highlights divisions within the party. The debt ceiling could be a further distraction from the president’s agenda and consume precious political capital.

[Posted: 9:30 AM EDT] After a two-day correction in tech stocks, equities are stabilizing this morning. Although the drop in the popular sector seemed to come out of nowhere, it looks to us like a fairly normal market correction, merely some profit taking. In a world of ultra-low volatility, such pullbacks are less common and thus receive a lot of media coverage. However, in the broader context, we haven’t seen anything so far in the decline that looks like it will have “legs.” That isn’t to say the group isn’t richly priced or a “good buy,” but it also doesn’t mean the recent pullback is the start of a larger market correction.

Bloomberg[1] is reporting that there is evidence of broad election interference by Russia in the 2016 presidential campaign. There have been scattered reports for weeks of Russian actions but this is the first time we have seen a reputable source indicating that there were Russian cyberattacks on election software in at least 39 states. Our view on this issue, which the article confirms, is that Russia’s goal wasn’t necessarily to sway the election in either direction but to undermine confidence in the electoral process. There were worries that these cyberattacks might corrupt voter rolls and lead to spoiled ballots or slow the counting process. What is particularly worrisome is that there is no unified electoral process in the U.S. Voting procedures are set at the state and local government levels and the degree of technical sophistication varies widely. On the other hand, having to attack some 7,000 county voting registration rolls would be a massive task and may not yield the desired results.

Partisan divisions have tended to undermine the legitimacy of presidents since the 2000 election. From hanging chads to controversies surrounding birth certificates, constant rumors of irregular voting and legislative attempts to increase the legal hurdles for voting, the voting process has become another battleground area in American politics. Now we can add Russian hacking to the list.

From Russia’s perspective, the goal is to support candidates who want to end the hegemonic role that America has played since WWII. In the last election, Hillary Clinton represented the establishment policies that would have maintained this role. President Trump’s campaign slogan made it clear he did not support this policy any longer. Thus, it would make sense that the Putin regime would support measures to help Trump. It is probably worth noting that Putin would have likely supported Bernie Sanders as well because his foreign policy positions were similar to Trump’s; neither candidate supported the two major trade deals and Sanders voted against the Iraq War. Thus, if the race would have been Sanders v. Rubio, for example, Russia would have probably tried to undermine the latter’s campaign.

Meanwhile, Putin is facing his own unrest as protests were held across Russia yesterday. Reports indicate that events were held in 145 cities across the country. Security forces in Russia moved quickly to quash the unrest. It has to be unsettling for the regime that it is mostly young Russians involved in the protests. We don’t think the regime is in any sort of immediate trouble as these events are not going to drive the Russian president from office. However, faith in the Russian government rests on the person of Putin; polls show that his approval ratings, which run around 80%, are well above the government’s approval ratings in the low 60%. To ensure the protests don’t gain momentum, the Kremlin is planning to tap one of its sovereign funds and there are rumors that Putin may sack his long time protégé Dmitry Medvedev, the current PM and former president. The government is also trying to revive its old patriotic youth movements in an attempt to control the uprising. Clearly, the regime is concerned about these protests. We note that the U.S. Senate is considering new sanctions on Russia.

Qatar is apparently running the blockade through Oman. The current blockade, which shows no signs of easing, continues to divide the region, with Iran and Turkey using the opportunity to support divisions within the Gulf Cooperation Council. In other Middle East news, the Saudi defense purchase deal is facing opposition in Congress.

The FOMC begins its meeting today, concluding tomorrow. This is a “presser” meeting so we will get a press conference, new economic forecasts and “dots.” It is a near certainty that the Fed will raise rates tomorrow. We will be watching for hints of future policy rates.

The Bank of Canada surprised the markets by signaling a rate hike is in the offing. The CAD rallied on the news.

Finally, the WSJ[2] is reporting the mortgage issuance industry is “re-learning” how to sell subprime mortgages. Early in my career (clearly, this is Bill writing), I was part of the process of winding down Latin America’s debt crisis, which ended by debt/equity swaps in the late 1980s. I remember at the time thinking, “It will be another generation before anyone lends to South America again.” It took about five years. The reason is that the previous lenders are usually swept away and find other jobs, and a new group enters without any experience of the pain suffered by the previous generation of lenders. This WSJ article describes well how this process works.

On March 10, Park Geun-hye was removed from her position as president of South Korea. Her ouster came on the heels of a scandal involving her close confidant who is accused of seeking bribes from chaebols, a group of family-owned multinational conglomerates that dominate the South Korean economy, to curry favor with the Park administration. Prior to the scandal, Park’s political party, Liberty Korea, had been accused of prioritizing the interests of the chaebols over the interests of the Korean people.

This controversy has paved the way for populist candidate Moon Jae-in, from the Democratic Party of Korea, to rise to the presidency. It is assumed that he will look to loosen government ties with chaebols. Recently, chaebols have come under scrutiny as many people feel that their overall size and dominance have constrained the economy. Currently, South Korea suffers from high youth unemployment, rising household debt and rising income inequality. Moon Jae-in has vowed to tackle each of these problems in addition to chaebol reform. This task may prove to be difficult as the chaebols have accumulated a lot of political clout over the years, thus he may find it difficult to pass serious reforms through parliament.

In this report, we offer a brief history on the origins of chaebols and their influence in lifting the country out of poverty. From there, we will focus on the role the Asian Financial Crisis played in changing public attitude toward chaebols and examine possible chaebol reforms. Finally, we will conclude with market ramifications.

[Posted: 9:30 AM EDT] The global political situation remains fluid. In France, President Macron won an apparent smashing victory in the first round of parliamentary elections, winning nearly 32% of the vote and faring much better than the conservative parties, which captured around 20%. The National Front picked up 14% of the vote and the Socialists polled in the single digits. The second round of elections will be held on June 18 when the En Marche Party is expected to capture 400 to 440 seats out of 577 seats. This is an impressive victory for a new party. The vote will give this new party and Macron a dominating hold on the legislature. Macron is promising to implement what can be best characterized as a neo-liberal policy, intending to lower taxes and end the 35-hour workweek. France never really adopted neo-liberal policies during the Reagan-Thatcher period so it would be a major change if they are implemented. On the other hand, Macron wants to create an EU fiscal mandate, which will surely be opposed by the Germans. All in all, Macron will have domestic political support.

While France appears to be moving to the right, the U.K. seems to be leaning toward unreconstructed socialism. Jeremy Corbyn pines to renationalize various industries that were privatized under Thatcher and initially nationalized by Labour after WWII. Although the Tories did win the majority of seats in the last election, they will struggle to form a government and the odds of another election soon are rising. After last week’s embarrassing loss, there is growing speculation that Theresa May will be forced to step down from her post as party leader while the Tories try to regather themselves. David Davis, the minister overseeing Brexit, has stated that Brexit negotiations will not start on June 19 as planned but will likely take place sometime next week.

We are seeing a penchant for newness as there are high levels of discord across Western societies. We have seen the rise of hard-left and hard-right parties, but what has been consistent across the West is a willingness by voters to try something new. Corbyn and Trump are calling for different policies but are clearly outside the mainstream. These persons become attractive because voters are desperate for something new, hence why France decided to go with a very young president and a new party promising neo-liberal, market-friendly policies. So far, financial markets are handling these divergences without major problems, although one could argue that currency and fixed income markets have moved while equities continue to mostly ignore political discord. We don’t know if this can last indefinitely, but it is clearly in place now.

In the Middle East, Qatar is still looking for a diplomatic solution to the blockade formed by Saudi Arabia. Qatar has been accused of funding terrorism, a claim that it has vehemently denied. SOS Tillerson has called for a de-escalation of the blockade, stating that it is hindering U.S. military operations within the region as well as being wrong on “humanitarian” grounds. It is worth noting that Qatar hosts the largest U.S. military base in the Middle East. As such, the Pentagon has also weighed in, stating that the blockade does not currently hinder its operations but rather its ability to plan for longer term military operations within the region. Alongside SOS Tillerson’s calls for de-escalation, Trump has issued a statement praising the blockade as possibly leading to the end of terrorism. Trump’s conflicting viewpoints from members of his administration have become somewhat routine. That being said, the Trump administration’s inability to formulate a coherent foreign policy could lead to the U.S. losing clout around the world.

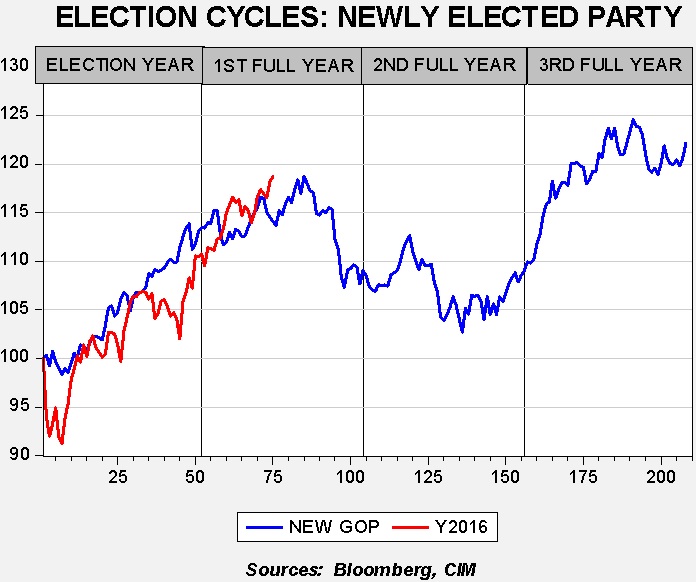

We have been monitoring the S&P 500 performance relative to new GOP administrations. Based on the historical pattern, the market has reached the average peak level a few weeks early.

This chart shows the performance of the S&P 500 on a weekly close basis, indexed to the first Friday of the first trading week in the year of the election. We have averaged the first four years of a new GOP president. So far, this cycle’s equity market has generally, though not perfectly, followed the average. Based on that pattern, the current level of the market is around the usual peak. Clearly, this election cycle could be different, but the average does suggest we could be poised for a period of weakness.

So, what might cause a pullback? Here are a few candidates:

A debt ceiling crisis: The Treasury indicates that the government may begin to shut down as early as August if the debt ceiling isn’t lifted. With the GOP controlling Congress and the White House, raising the debt limit should be perfunctory. However, there are rumblings that the Freedom Caucus will demand spending cuts to agree to any debt limit increases. The Democrats, after watching President Obama deal with two government shutdowns and the sequester over the debt limit, are in no mood to work with the administration and may force the congressional leadership to deal with the Freedom Caucus. If another debt limit crisis triggers a new government shutdown and raises fears of a potential downgrade of Treasury debt, a pullback in equities would likely result.

Winds of war on the Korean Peninsula: The U.S. will have three carrier groups in the East China Sea in the coming weeks. Although we doubt the Trump administration wants a war with North Korea, the U.S. is putting enough assets in the region to go to war if it so decides. A full-scale attack on North Korea would be a bloody affair; the Hermit Kingdom has been preparing for such an attack for years and even if its nuclear program isn’t ready to deliver a weapon, its conventional forces will wreak havoc on the South. Even a hint of a conflict will likely prompt a pullback in risk assets.

Monetary policy worries: The FOMC appears driven to raise the fed funds target rate. As we have noted before, there is a good deal of uncertainty surrounding the degree of slack that remains in the economy. The FOMC appears to be leaning toward the notion that the economy is getting close to capacity and further declines in unemployment will surely lead to inflation rising over target. Although financial markets didn’t react well to the rate hike in December 2015, the subsequent increases have occurred without incident. Telegraphing the increases has reduced the risk to rate hikes but the odds of overtightening will increase if the Federal Reserve has miscalculated the level of slack in the economy. This potential concern, coupled with plans to begin reducing the size of the balance sheet later this year, could begin to undermine market sentiment.

We want to note that the average decline shown on the above graph is not a numerical forecast; we tend to view the direction as a more important indicator than level. It suggests that a period of equity market weakness is a growing possibility later this summer. What we don’t see, at least so far, is evidence of anything more than a pullback. Recessions tend to be the primary factors that lead to bear markets. The economy is doing just fine; the yield curve hasn’t inverted, the ISM manufacturing index is comfortably above 50 and there hasn’t been any evidence in the labor markets to suggest a drop in economic growth. Thus, we may see a weak summer for stocks but nothing that would lead us to take a defensive position in the equity markets. Instead, a pullback will likely create an opportunity for investors.

[Posted: 9:30 AM EDT] In Britain, Theresa May’s decision to call a snap election in order to win a larger mandate backfired last night. The Tories, who were supposed to win more seats, lost their majority and barely squeaked out a plurality. Final results show that the Tories lost 12 seats, falling to 318 in Parliament, and their rivals in the Labour Party won 31 seats, increasing their total to 261. This outcome is seen as a stunning loss for the Tories who now need the help of a minority party in order to secure the additional eight seats needed to form a government. As of right now, the Democratic Unionist Party (DUP), a party from Northern Ireland that won 10 seats, is likely to help the Tories form a government but will not form a coalition. Despite the market’s negative reaction, there is growing sentiment that the election has possibly paved a way for a “soft” Brexit. The voting results suggest that May’s insistence that “no deal is better than a bad deal” may have hurt the Tories in anti-Brexit strongholds such as London. In the event that May fails to form a government, Jeremy Corbyn, leader of the Labour Party, will likely have to make concessions to the DUP (10 seats), Liberal Democrats (12 seats) and the Sottish National Party (35 seats) in order to form a government, all of whom are strongly in favor of a “soft” Brexit. That being said, May is expected to retain her role as prime minister as Brexit negotiations begin in 10 days, but it is unclear whether she will be able to retain her role as party leader in the long term. The GBP is currently down 147 bps relative to the dollar from the prior close.

Yesterday’s testimony by former FBI Director Comey is being spun furiously by both sides. Our take is that it’s damaging but not fatal. It doesn’t appear that there is a clear case of obstruction. Comey’s decision to leak is normal for Washington but it does taint his image. Former AG Lynch came off badly. For the financial markets, probably the best model to think about this issue is not Watergate, but Whitewater. There may not be much here, but the administration’s handling of the issue keeps leading to concern that “something” is being covered up. That means the special investigation will continue for months, if not years, and will be a distraction for the administration. If they are going to have any legislative success, they need to figure out how to manage this distraction.

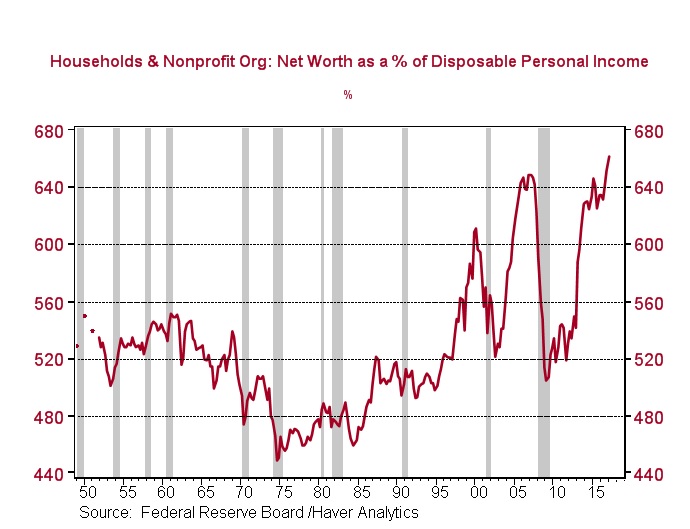

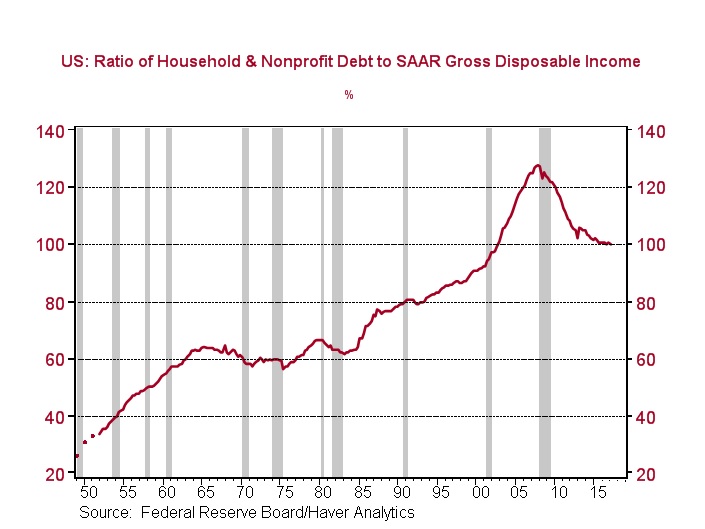

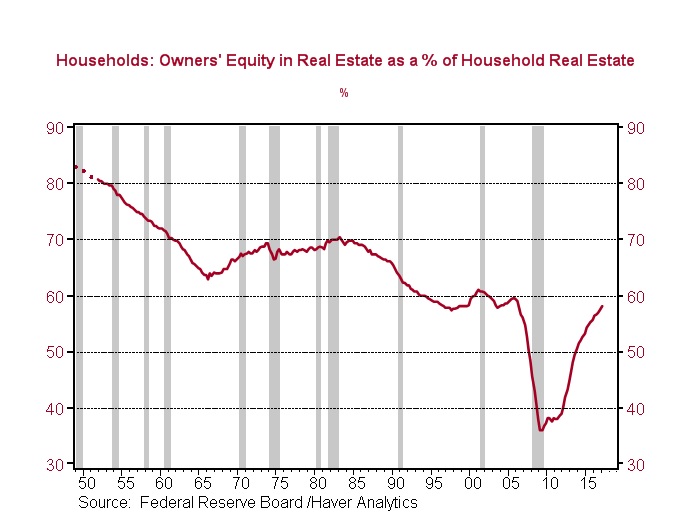

Yesterday, the Federal Reserve issued its Financial Accounts of the U.S. for Q1, otherwise known as the “Flow of Funds” report. It offers a plethora of useful and interesting data about the economy and the health of important sectors of the economy. The charts below show a few of our favorites.

The chart below shows net worth as a percentage of after-tax income. It has reached a new record high as financial assets rise and housing prices recover.

Deleveraging has slowed, but we are still seeing households lower their debt levels relative to after-tax income.

We are seeing a steady healing of the real estate sector. Owners’ equity in real estate continues to approach 60%, which history would suggest is “normal.” In other words, as we approach this level, we could see homeowners and potential buyers view home buying as a less risky activity. If so, we could see a boost in homebuilding that would help the economy.

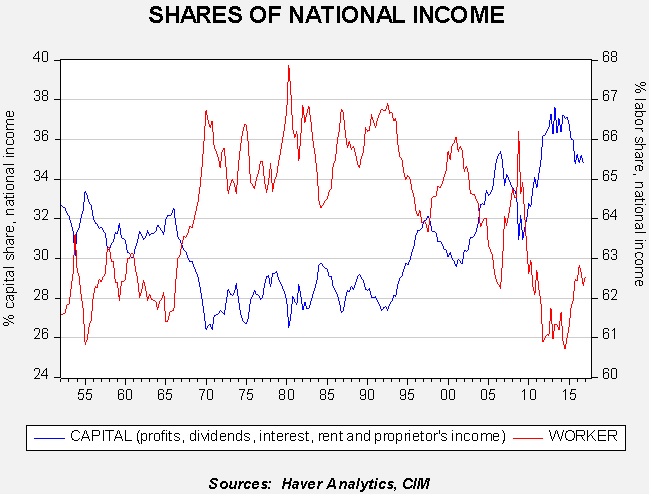

The Flow of Funds report also publishes national income data. Labor picked up modestly in Q1 but its share remains depressed. The steady loss of share is likely a factor in the rise of political populism.

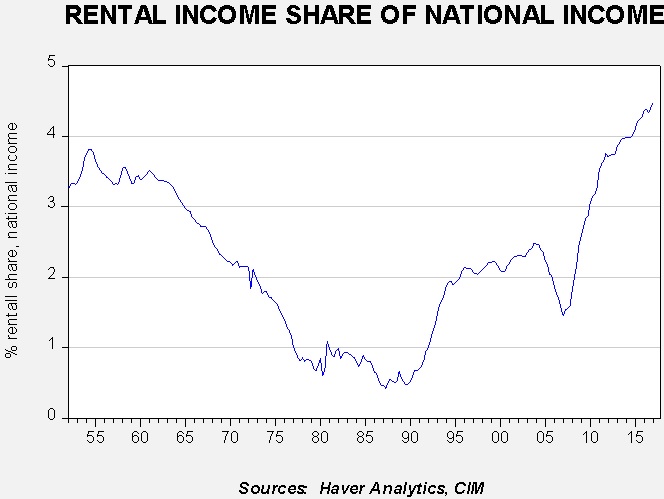

Rental income reached a new high, one of the factors that has made real estate investments attractive.

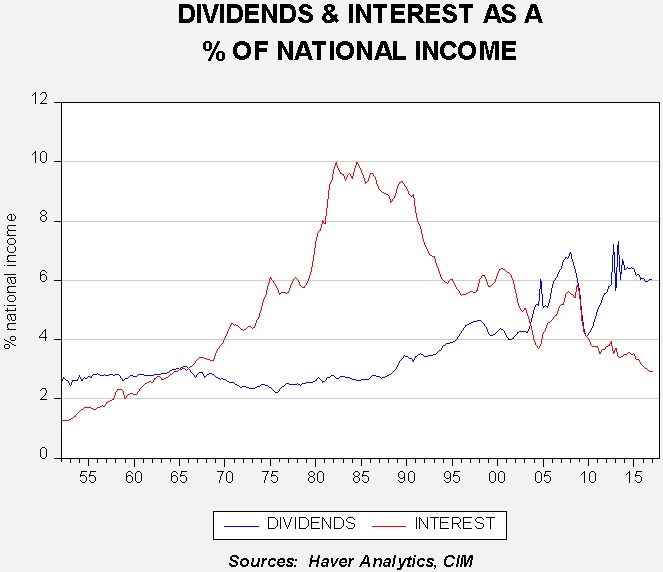

Our last chart examines the income from interest and dividends.

Dividends are currently about 6% of national income, with interest income under 3%. The last time we had dividends consistently exceeding interest income was in the 1950s and early 1960s, a period of financial repression. This chart portrays investor preference of income-producing equities.

Today, there is a slew of geopolitical events that may have an impact on global markets. In Europe, the ECB will hold a press conference about current and future policy decisions. In the U.S., former FBI Director James Comey testifies to the Senate Committee about Trump’s influence in the Russia investigation. In the U.K., there are parliamentary elections to decide the prime minister.

The ECB has decided to hold rates at their current levels and maintain the current level of quantitative easing. Prior to the press conference, the ECB released a statement that left out the mention of possibly lowering interest rates in the future. The market has interpreted this as a signal that the ECB is willing to exit the stimulus program. As mentioned yesterday, the ECB has cut its inflation forecast and revised its GDP forecast higher. During the press conference, Mario Draghi added that he expects monetary policy to remain the same for an extended period of time, even after the stimulus program ends. He went on to say that increased momentum in the Eurozone economy shows that risks to the global outlook were broadly balanced, but the momentum has not translated into stronger inflation dynamics. Draghi warned that global macroeconomic developments still present downside risk and that the ECB is prepared to increase asset purchases if the outlook were to become less favorable or financial conditions become inconsistent. After the press conference, the euro depreciated against the dollar.

With the release of former FBI Director Comey’s statement that Trump asked him to “lift the cloud” of the investigation by publically stating that Trump was not personally under investigation, Comey’s testimony today could prove to be a bit anti-climactic. The primary market worry would be that enough information will emerge to further distract the Trump administration from other goals. We do note that Senate GOP leaders are looking at a health care bill; reports suggest that McConnell will give it a few weeks and, if nothing is done, tax issues will be taken up. Tax cuts are what the market is mostly concerned over so if the Senate can move forward then it probably means equities will at least hold at current levels.

The other major item today is the British election. Polls are scattered, with some late polls showing a dead heat, while others show a 10% lead for the Tories. Our expectation is a Conservative win but no major pickup in seats and thus no expanded mandate. This isn’t a great outcome but it probably doesn’t move the financial markets.

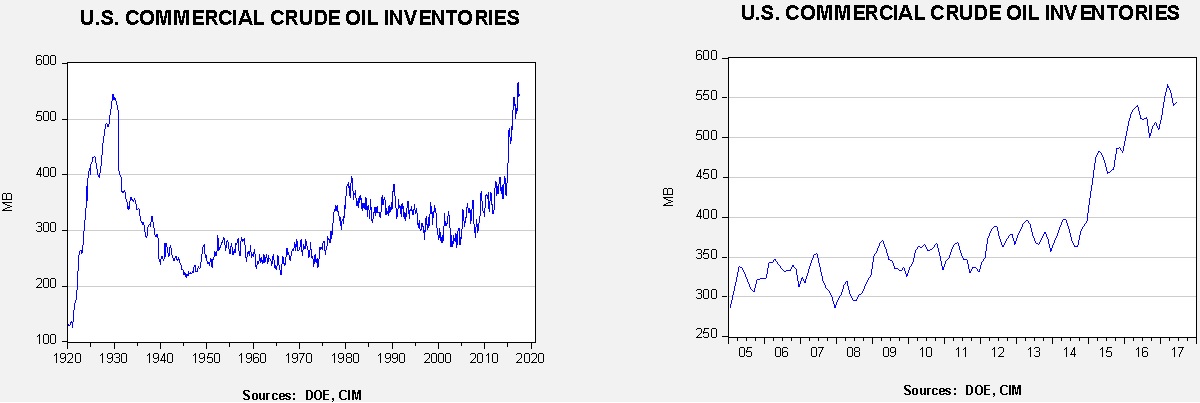

U.S. crude oil inventories unexpectedly rose 3.3 mb compared to market expectations of a 3.5 mb draw.

This chart shows current crude oil inventories, both over the long term and the last decade. We have added the estimated level of lease stocks to maintain the consistency of the data. As the chart shows, inventories remain historically high but have been declining. We note that, as part of an Obama era agreement, there was a 1.7 mb sale of oil out of the Strategic Petroleum Reserve. This is part of a $375.4 mm sale (or 8.0 mb) done, in part, to pay for modernization of the SPR facilities. International agreements require that OECD nations hold 90 days of imports in storage. Due to falling imports, the current coverage is near 140 days. Taking that into account, the build was a less ominous 1.7 mb.

As the seasonal chart below shows, inventories are usually well into the seasonal withdrawal period. This year, that process began early. Although the actual level of stockpiles remains quite high, we are seeing stock declines at a rather rapid pace. Assuming a similar drop from this year’s peak of 566.5 mb at the end of March, we will end up at 505 mb by late September. In fact, current inventory levels have already declined more than the seasonal trough, which is supportive. As a result, last week’s rise is something of an anomaly; we would not be surprised to see declines resume next week.

(Source: DOE, CIM)

Based on inventories alone, oil prices are overvalued with the fair value price of $37.17. Meanwhile, the EUR/WTI model generates a fair value of $53.24. Together (which is a more sound methodology), fair value is $47.34, meaning that current prices are below fair value. Inventory levels remain a drag on prices but the oil market seems to be ignoring the impact of dollar weakness. Our position has been that oil prices are in a range between $45 and $55 per barrel and, accordingly, oil is attractive at current levels. The worries about OPEC shattering over Qatar appear to us to be misplaced. The cartel has managed to maintain relations with members at war before. A bigger risk is that a conflict develops that disrupts flows. It’s not highly likely, but it is more likely than OPEC expanding output based on tensions with Qatar.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.