[Posted: 9:30 AM EDT] Yesterday saw a selloff in U.S. equities. We are not seeing much of a recovery this morning. Here is what we are watching today:

Barcelona: Using rented vans, a group of terrorists who claimed allegiance to ISIS tore through a tourist area of Barcelona, killing 14 (so far) and injuring over 100. One of the disturbing parts of this event is how far the drivers of the vehicle moved before stopping.[1] There was a second attempted attack in Cambrils, a city about 70 miles south of Barcelona. Police were able to thwart the second attack. A number of people have been arrested. Three vans were rented, so police are searching to find all the vehicles. Although this attack was horrific, there are signs it could have been much worse. The previous night, there was a gas explosion in Alcanar, a town south of Barcelona, that may have been a bomb-building facility for the terrorists. We note that the terrorists in Cambrils were wearing fake suicide vests; it is possible the group intended to use explosives in their van attacks and were left with using the vehicles as weapons when the bomb-making apparatus failed. Recent terrorist attacks in Europe are increasingly using vehicles as their weapon of choice. Guns can be traced and explosives, though effective, require some degree of expertise to build. But, most adults can drive cars. Thus, one of the most ubiquitous elements of modern life has become a threat. Market effects from terrorism tend to be short-lived; we are seeing some weakness in Eurozone equities but that is probably more due to yesterday’s U.S. selloff.

The “Cohn correction?” We think this is the first time in our memory that financial markets are concerned about whether or not a presidential advisor is staying. To a great extent, this is more about what Cohn represents. As we noted yesterday, the Trump administration has included both economic nationalists, who want a populist agenda, and globalists, who represent the GOP establishment and favor globalization and deregulation. The financial markets appear to have assumed that, in the end, the globalists would win out, bringing tax cuts, deregulation and continued open trade. In reality, the evidence is mixed. The president has made some steps toward impeding trade, although the moves have been more modest than the rhetoric. At the same time, there has been lots of talk about tax cuts, although there is no detailed plan for legislation. After the Monday press conference, speculation grew that Cohn might resign. Recent reports suggest he intends to stay. However, if he does leave, it might signal a broader exit of establishment figures in the administration and raise the odds that the nationalist agenda will dominate. This outcome is clearly not well liked by the financial markets. If the White House adopts a nationalist economic policy, it would create conditions of higher inflation. Of course, the White House can only do so much; the president can clearly affect trade with significant independence from Congress. On the other hand, tax policy and spending priorities need congressional approval.

Still, as we note below, there is no economic evidence of a recession which means that pullbacks will likely be short-lived. In addition, as we noted in last week’s Asset Allocation Weekly, there is ample liquidity in the economy which should support the equity market.

[Posted: 9:30 AM EDT] There is something of a negative tone to risk assets this morning but nothing that, so far, appears significant. Here is what we are watching today:

ECB minutes: The main takeaway from the ECB minutes is that the recent rise in the EUR has caught the attention of policymakers. The EUR is just off a 30-month high in part due to expectations of a slow reversal of the ECB’s ultra-accommodative monetary policy. Supporting EUR strength has been the realization that the FOMC (see next item) will be slow to raise rates. And, on a purchasing power parity basis, the dollar remains overvalued (EUR fair value is around $1.30 based on these models)[1] and thus is vulnerable to weakness. The ECB, unlike the Fed, has the exchange rate as part of its mandate and thus takes it into account when setting policy. The EUR’s strength may slow the pace of stimulus withdrawal but we don’t expect it to stop it completely because Germany really wants to see tighter policy. Eventually, the Merkel government will get its way. The EUR is weaker this morning on the concerns expressed in the minutes. However, we don’t expect that the ECB can engineer a reversal in recent currency trends, mostly because the European currency is still undervalued and U.S. monetary policy isn’t going to tighten all that much.

Fed minutes: Yesterday, the FOMC released the minutes of its July 25-26 meeting. The minutes are heavily summarized (and sanitized); after five years, the Fed releases transcripts of these meetings which are quite enlightening, revealing disagreements and snarky comments. In 2022, this meeting will probably have similar interesting commentary when the transcripts are released. The committee is clearly divided; some members are worried that inflation could rise as capacity becomes constrained, and it appears that nearly an equal number worry that not only will inflation remain low but it might fall further. Although the majority still adhere to the Phillips Curve framework, a significant minority are concluding that it is no longer useful in forecasting inflation. The committee warned against deregulating too quickly or creating conditions that led to the Great Financial Crisis. It does appear that the balance sheet reduction process could begin in September. The markets took the minutes as dovish and we concur with that judgement.

Watching Washington: Early on, we argued that President Trump had to manage two constituencies, the establishment wing and the populist wing of the GOP. The former want tax cuts, deregulation and continued globalization. The latter want immigration restrictions, trade impediments, health care reform and infrastructure spending. There are rather obvious policy conflicts between the two groups. The establishment, heavily represented by business leaders, do not want trade restrictions and favor open immigration. They are cool to infrastructure spending, although they are willing to bargain on that issue. Regarding health care, big business has generally worked within the Obamacare framework and has learned to live with it; thus, repeal isn’t a high agenda item. On the other hand, the populists, representing the working class and small business, are tired of globalization, have faced rising costs due to the Affordable Care Act and really don’t benefit directly from tax cuts. Appeasing each group is difficult as there are few overlapping policies. Managing this situation would be difficult for an accomplished political operator. It is a really hard task for a neophyte. Much of the president’s struggles are tied to managing this divide.

There are numerous cross-currents coming out of Washington over the past 48 hours. Steve Bannon dropped a bombshell with his interview with Robert Kuttner of the American Prospect.[2] Bannon indicated that there is no military solution to North Korea, essentially saying the president’s comments were bluster. He showed his contempt for the establishment members of the administration (Cohn, Mnuchin) and also suggested the U.S. is at economic war with China. Interestingly, he showed nothing but contempt for the white nationalists in Charlottesville. To quote, “Ethno-nationalism—it’s losers. It’s a fringe element. I think the media plays it up too much, and we gotta help crush it, you know, uh, help crush it more. These guys are a collection of clowns.” Bannon is making an important distinction here between the working class and the white separatist, white power movement, suggesting that restricting trade and immigration (and probably reregulating the economy) are worthy causes. Fighting over Civil War monuments isn’t a significant part of that policy goal; in fact, other than poking the mainstream media, this issue probably isn’t all that critical. This may or may not be the president’s position on this issue.

Bannon has attempted to walk back these comments by saying he didn’t think it was an interview. This is disingenuous. Bannon ran Breitbart. He should be acutely aware that unless clearly stated, journalists assume a discussion is on the record. We do media interviews all the time; there have been occasions where, for a variety of reasons, all or part of an interview is “off the record.” To signal this, we would tell the reporter up front that comments are not on the record and are only for background information. We suspect Bannon knew what he was doing.

So, the exodus of CEOs from the various advisory boards appears to be a win for Bannon. Attacking China on trade is a clear focus for him. Here is what the markets should be watching. If the establishment has failed to capture the president and he goes over to the populists, it probably won’t be good for financial markets. Tax cuts and further deregulation may not occur. Trade restrictions and immigration cuts are likely. These actions will crimp margins. The key to whether or not this trend develops rests on personnel; if establishment figures resign (Cohn, Mnuchin, et al.), the populists may gain access to the levels of power.

Energy Recap: U.S. crude oil inventories fell 8.9 mb compared to market expectations of a 2.5 mb draw.

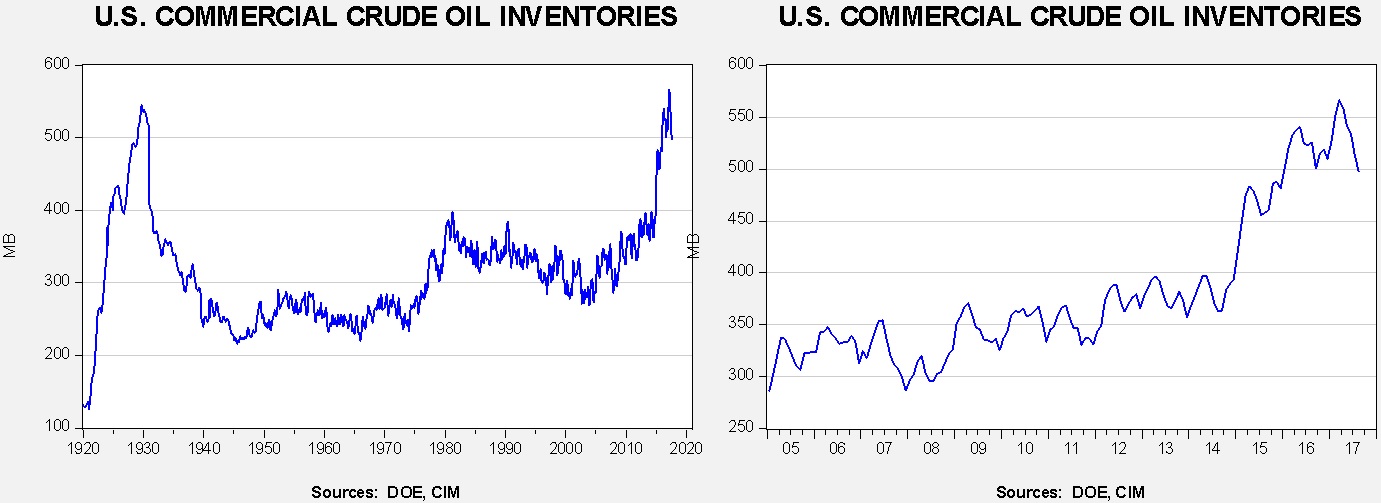

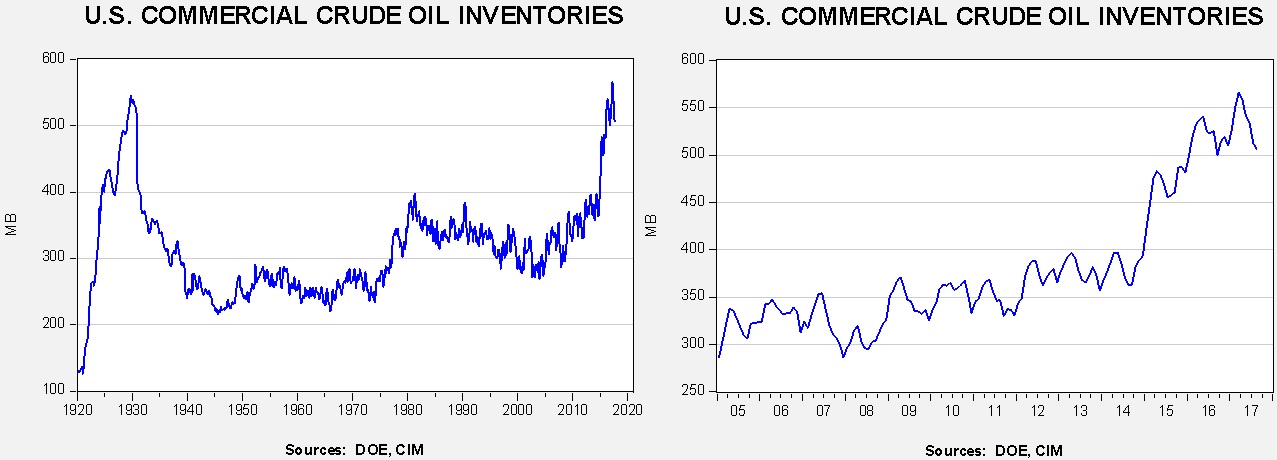

This chart shows current crude oil inventories, both over the long term and the last decade. We have added the estimated level of lease stocks to maintain the consistency of the data. As the chart shows, inventories remain historically high but they are declining. In fact, we have reached last year’s seasonal low, made in September; if seasonal patterns hold, we should see inventories fall to levels not seen since 2015. Again, this week, there was no oil sold out of the Strategic Petroleum Reserve (SPR). The authorized sale is nearly complete as 16.2 mb have been released out of an authorized 17.0 mb.

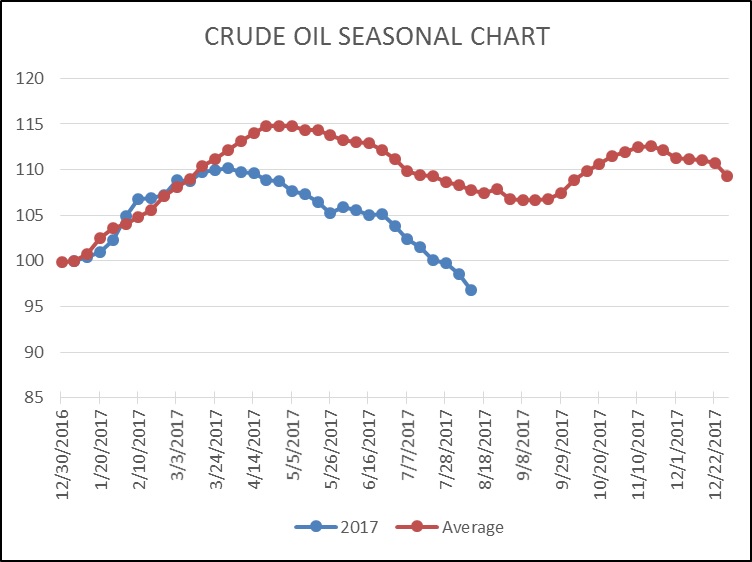

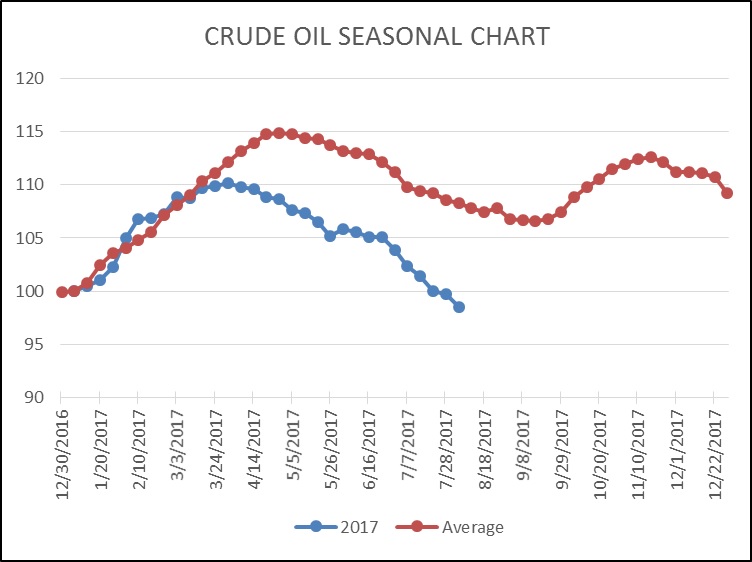

As the seasonal chart below shows, inventories are usually well into the seasonal withdrawal period. Even with the SPR sales, we have already seen a larger than normal seasonal decline; in fact, the drop is rather remarkable. It should be noted that the seasonal trough isn’t usually hit until mid-September. Thus, we should see further stock withdrawals over the next four weeks.

(Source: DOE, CIM)

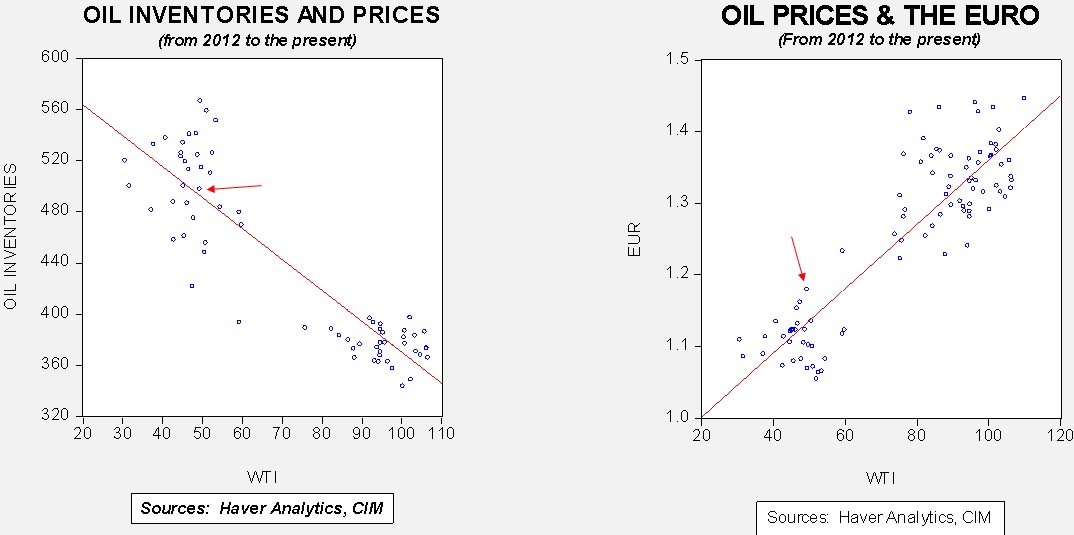

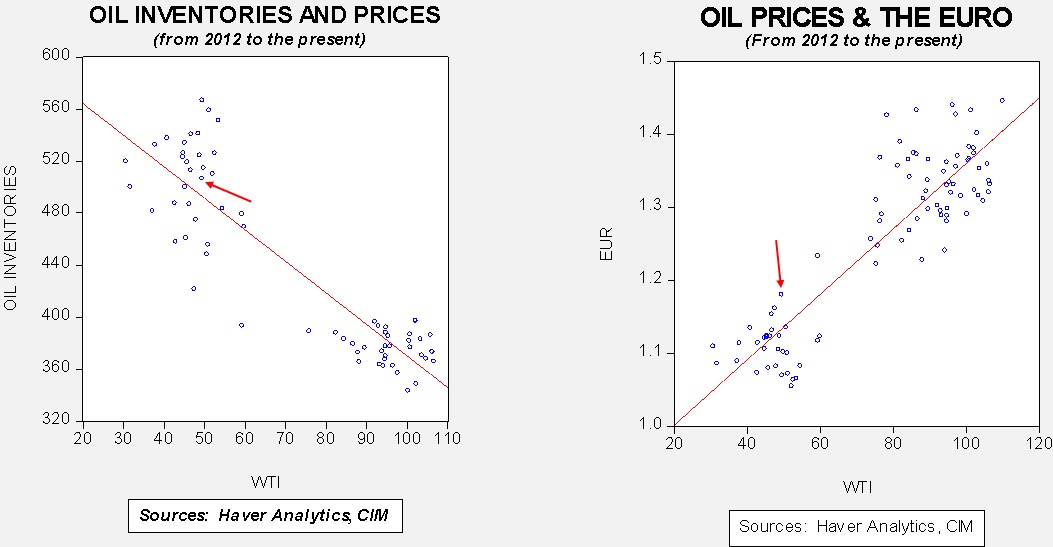

Based on inventories alone, oil prices are overvalued with the fair value price of $52.22. Meanwhile, the EUR/WTI model generates a fair value of $64.13. Together (which is a more sound methodology), fair value is $60.26, meaning that current prices are well below fair value. The most bullish factor for oil is currently dollar weakness, although the rapid decline in inventory levels is also supportive. Prices are well above fair value.

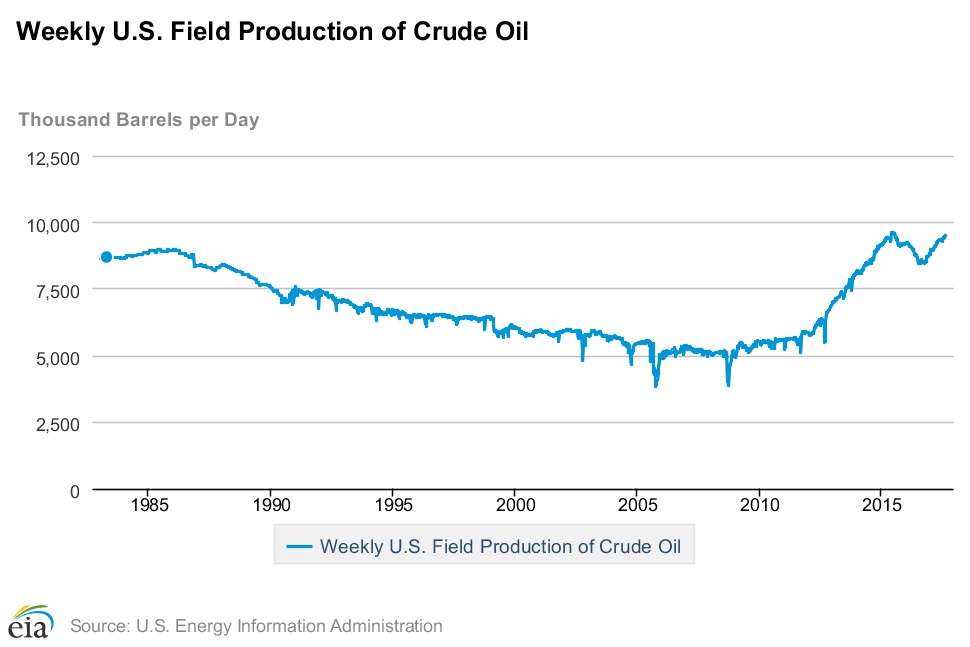

So, why are oil prices struggling? The mostly likely answer is that traders are focused on rising U.S. output. The chart below shows weekly U.S. oil production. It is near previous peaks. When seasonal demand falls, which will begin over the next month, inventories could rise rapidly if production continues to increase.

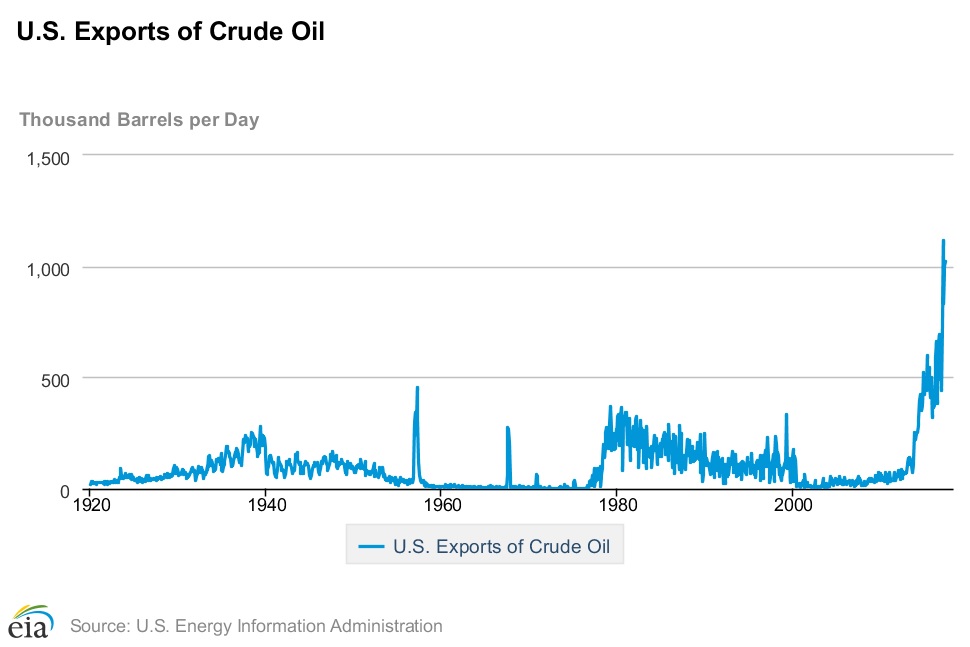

However, one factor traders might be missing is that U.S. oil exports are rising as well.

There are reports that the Louisiana Offshore Oil Port (LOOP) is considering retrofitting its facility to also export oil. Currently, it can only handle imports. Rising exports can allow for rising production and falling U.S. crude stockpiles…but it is also bearish for global prices.

[Posted: 9:30 AM EDT] Financial markets are quiet this morning, consistent with the late summer lull. However, there has been a lot of news flow. Here’s what we are watching this morning:

Fallout from the president’s press conference: President Trump’s press conference yesterday was highly controversial and has given the media much to talk about. However, what seems to have been lost in the comments is that he was expected to discuss infrastructure plans. Infrastructure spending was one of the policies designed to boost the working class by creating construction jobs for projects around the country. By shifting the focus to the events in Charlottesville, the president has muffled the infrastructure agenda and may have reduced any chances of getting a program through Congress.

GOP in disarray: The president’s comments have also put his party in a difficult position. In an upcoming WGR, we will discuss the philosophical roots of fascism and populism. Although often tied together, we will argue they come from different sources and ultimately have different agendas. GOP members of Congress can certainly support populism but want to avoid any hint of association with fascism. The president seems to be, perhaps inadvertently, equating the two movements and thus GOP members are being forced to either abandon the president or support a position that Americans fought against in WWII. The bottom line is that it will be difficult to implement legislation, such as tax changes, infrastructure, a debt ceiling, etc., when the leadership is divided.[1]

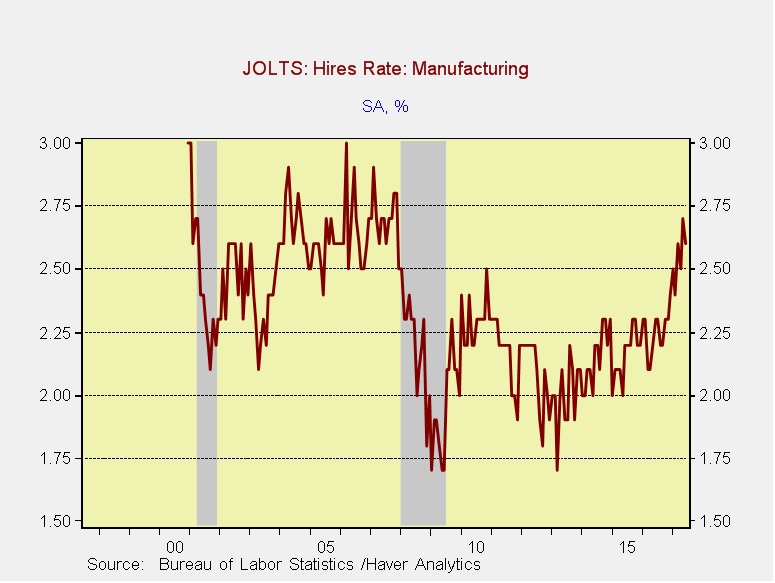

An interesting trend in manufacturing jobs: We were examining the recently released JOLTS report that surveys the labor market for open positions, hiring and separations. With the labor market tightening, we are seeing a rise in hiring.

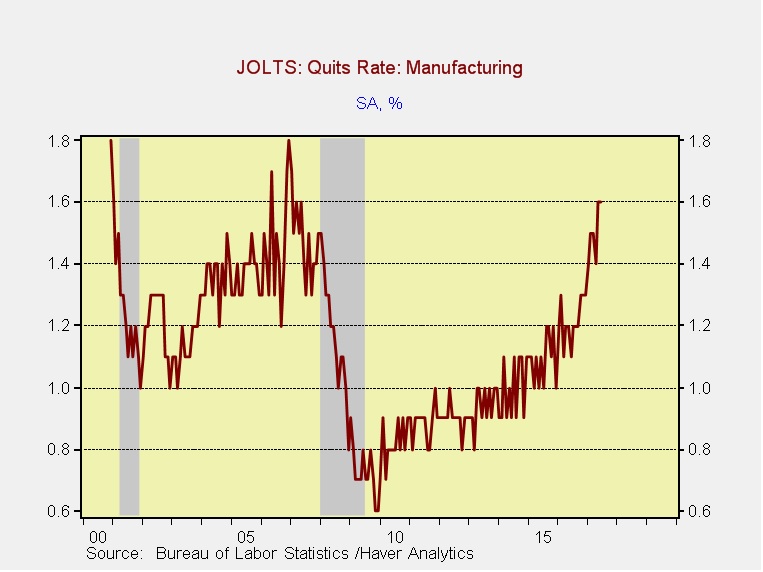

That’s not a huge surprise. What is a surprise is the jump in quit rates.

Usually, a rise in quit rates signals improving labor market confidence. Workers who believe they can easily find another job are more inclined to quit. Workers usually leave a job for one that has higher pay, so this is something we will be watching in the future. We note an article in the Washington Post[2] offering anecdotal evidence that some of the quits are due to baby boomers reaching the point where the physical demands of the job are making separation packages look attractive. Another factor mentioned is that the steady increase of automation has workers concluding that separation deals will become increasingly less attractive in the future and so taking one today is a better option. The proof will be in the pay; we will be watching for signs of rising manufacturing wages but, so far, there isn’t any evidence of that.

Jackson Hole may just be a vacation: Every year, the KC FRB holds a meeting in Jackson Hole, WY. If you haven’t ever visited the town, it is well worth it. Near the Grand Tetons, it is simply beautiful. The gathering, which will be held in late August this year, is often a forum for policymakers to unveil policy directions.[3] Chair Bernanke signaled QE3 at this meeting in 2012; in 2014, Draghi laid out the bank’s current QE program. There were expectations that ECB President Draghi would unveil his tapering program at Jackson Hole. Sources indicate that will not occur, although he will give remarks. No other policymakers are expected to signal anything significant.

North Korea: Although tensions have eased in the near term, there are a few developments worth mentioning. First, the U.S. and South Korean militaries will conduct the annual Ulchi-Freedom Guardian military exercises, a 10-day event that will begin on Aug. 21. These war games infuriate the Kim regime and China has tried to set up a “freeze for freeze” scenario, in which the U.S. would suspend these games and North Korea would suspend its nuclear and missile program. So far, neither side has agreed. In what is a rare event, Gen. Joseph Dunford, Joint Chief of Staff, is visiting Chinese military facilities on the North Korean/Chinese frontier.[4] This visit is thought to be a signal to the “Young Marshal” that China is displeased with North Korea’s behavior.

[Posted: 9:30 AM EDT] Markets are calming down. Here’s what we are tracking this morning:

North Korea blinks: According to numerous reports, the military leadership of the Democratic People’s Republic of Korea (DPRK) offered plans to Kim Jong-un for a missile test around the U.S. territory of Guam. After reviewing the plans, the “young marshal” decided to postpone any attacks. There has been a definite cooling of tensions since rhetoric intensified last week. As noted before, the U.S. military has not mobilized for an extended attack. U.S. military leaders have been stressing the need for diplomacy. South Korea’s president indicated that “only the Republic of Korea (South Korea) can make the decision for military action on the Korean Peninsula.”[1] Although President Moon is partially correct in his assessment, in that the U.S. can’t dictate a ground war on the peninsula, an attack on Guam would lead to a U.S. response regardless of South Korea’s position. Still, as tensions ease, we are seeing a reversal of risk trades—the dollar is higher, gold and Treasury prices are falling and equities are improving (today’s retail sales data, shown below, have accelerated these trends).

The next North Korea? Iranian President Rouhani indicated today that his country could quit the nuclear deal “within hours” if new U.S. sanctions are imposed. Recently, the U.S. has applied unilateral sanctions on six Iranian companies for their work on Iran’s ballistic missile program. The Trump administration argues that Iran’s missile tests and development violate the 2015 nuclear deal; Iran denies that their conduct bars such activity. If relations between the U.S. and Iran continue to deteriorate and the nuclear deal ends, we expect Iran to rapidly move to build a deliverable weapon. This outcome would be quite negative. First, Israel will likely view this as an existential threat and could strike Iran with its own (so far undeclared) nuclear weapons. Second, even if military action doesn’t occur, a nuclear Iran will very likely create a nuclear arms race in the region and, given the instability of these regimes, the chances increase for either a nuclear accident or a rogue government with a nuke. The Iran nuclear deal probably was nothing more than “kicking the can down the road.” However, the end of “can kicking” has its own problems and it isn’t clear that the U.S. has the bandwidth to handle increasing problems in the Far East and the Middle East simultaneously. Additionally, we would fully expect the Putin regime to take advantage of American distraction if conditions in the Middle East deteriorate.

Germany signals to the ECB: German Finance Minister Schäuble indicated today that the European Central Bank’s ultra-loose monetary policy would come to an end in the “foreseeable future.” However, he also indicated that rates would remain low. Germany has not been comfortable with ECB monetary policy for some time and monetary policy is probably too loose given the strength of the economy. The EUR has been appreciating this year due to a combination of tighter ECB policy expectations, an overvalued dollar and disappointment that dollar bullish policies (e.g., border adjustment tax, infrastructure spending, etc.) expected when Trump was elected have failed to materialize. It should be noted that Schäuble’s comments were made at a campaign rally; Germany, a net saving nation, feels it is being unfairly penalized with low interest rates. So, his comments were well received.

Last week, we discussed a short history of Qatar and its geopolitical imperatives. This week, we will analyze the events precipitating the blockade, the blockade itself, the GCC’s demands and the impact thus far on Qatar. We will examine how the situation has reached a stalemate and, as always, we will conclude with market ramifications.

The Precipitating Events

As we discussed last week, a combination of conditions have allowed Qatar to avoid domination by Saudi Arabia, the generally recognized leader of the GCC. Qatar has powerful allies outside the region, friendly relations with Iran, is demographically unified and has an economy that isn’t dependent on oil, all of which have allowed Qatar to follow independent policies. This situation has persistently angered Saudi and UAE leaders. Beneath these national concerns are also long-standing tribal rivalries.

However, these differences have been in place for a long time. It appears that there were three events that led the GCC, Egypt, Yemen and Sudan to react and initiate the blockade.

[Posted: 9:30 AM EDT] There was a lot of news over the weekend. Here is what we see as important:

North Korea fears ease: Although worries remain about an escalation of tensions with North Korea, as we noted last week, there is no evidence of U.S. mobilization for an attack on the peninsula. There are no carriers near North Korea, there have been no evacuations of American civilians from South Korea and no overt preparations for war (e.g., confining troops to base, increased training activities). Although the president’s comments are clearly belligerent, his words are not a real signal of a march to war. We suspect this is a bargaining tactic, one that he has used in his private sector life. The problems with this sort of rhetoric are twofold. First, it creates the “boy crying wolf” problem. The more he makes statements that appear stronger than what the U.S. is ready to implement, the less foreign powers will pay attention. Second, a president must be careful in his threats because they can bolster the foreign power that is the target of ire. Think of President Bush’s “axis of evil.” One of these powers has collapsed, while the other two have either developed nuclear weapons or were at the brink before deals were brokered. Foreign governments must take threats from the superpower seriously. By threatening North Korea (and Venezuela, too), the leader can now legitimately argue that the country faces an existential threat and should back the person in office. It also supports building weapons of mass destruction to protect from regime change. Still, for now, an easing of tensions has led to a reversal in risk-off trades from last week—the dollar and equities are stronger, while bonds, gold and forex are weaker.

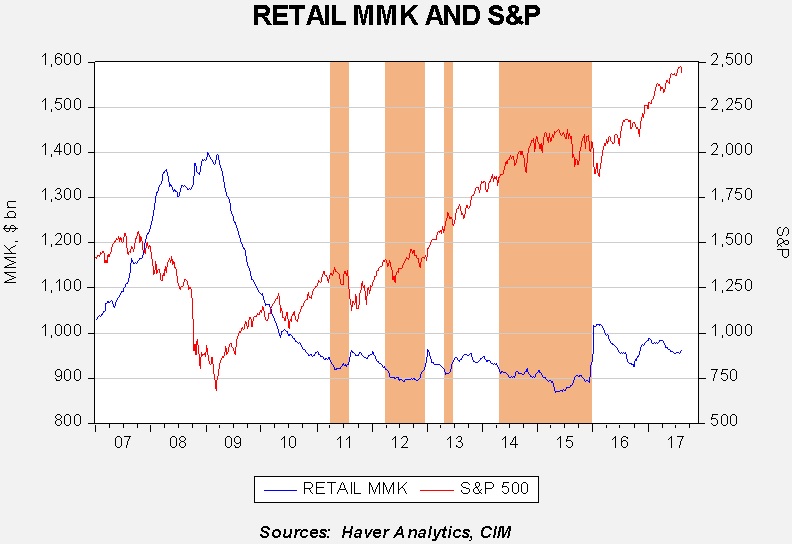

Not much of a correction: Last week we did see a pullback in equities. However, the major indices rose on Friday and are higher this morning. Although we remain concerned about the level of complacency in the financial markets, there appears to be simply too much available liquidity to investors to sustain a major correction. The chart below shows the level of retail money market funds along with the S&P 500. The orange bars show periods where retail money market funds approached $900 bn. These periods coincided with equity markets eventually losing momentum and correcting. Current levels are well above $900 bn, suggesting that there is ample cash available to buy equities. Until we approach $900 bn in money markets, we expect selloffs to remain shallow. Of course, events and recessions can overwhelm cash; the former is a worry, the latter much less so.

Trade: Today, President Trump is expected to unveil an executive order investigating Chinese appropriation of U.S. technology which would prepare for trade restrictions if such a finding is made. The administration had delayed this action while the UNSC was negotiating sanctions on North Korea, but now, with sanctions in place, the president has decided to move forward. China is very concerned about trade restrictions; we expect China to react with promises to build productive capacity in the U.S. as a way to blunt trade impediments. The U.S. is also expected to begin formal NAFTA reform negotiations later this week.

Charlottesville: We won’t recap the weekend events because that is being done across the media. Here is the issue we are watching. The GOP establishment doesn’t want to be associated with the alt-right. Right-wing populists are less opposed to this group. The split in the GOP is becoming increasingly obvious and will be a threat to Republican elections over the next three years. There are rumors that Steve Bannon may be ousted from the White House.[1] If he goes, the influence of right-wing populists will be diminished, though not completely eliminated. On the other hand, the Democrat Party faces similar divisions.[2] We note that there were four major candidates in the 1860 presidential election. Although Lincoln won easily in the Electoral College, he took less than 40% of the popular vote. Current political divisions are deepening. How this affects financial markets remains to be seen, but a +20 P/E for the S&P seems inconsistent with volatile political divisions.

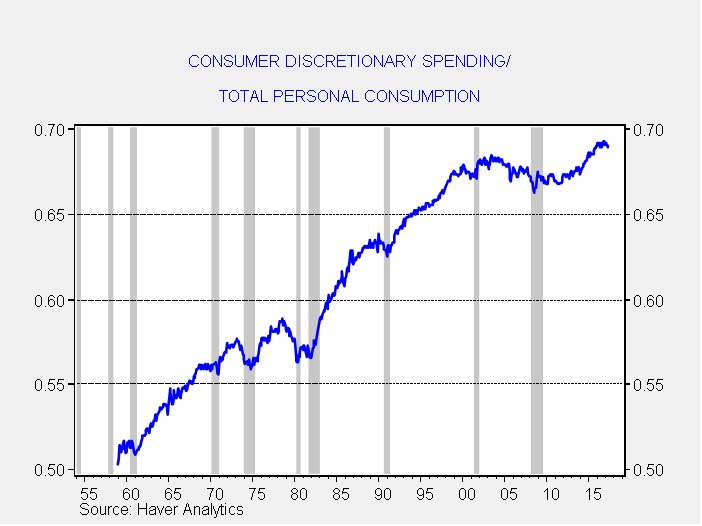

Although measuring “malaise” is more art than science, overall feelings of wellbeing or the lack thereof affect markets, politics, etc. One less common way to measure this is the ratio between discretionary spending compared to overall spending. Discretionary spending is defined as total spending less what is spent on food, clothing, energy and housing. In other words, if a household is able to spend more on other items besides these goods, one would expect “happier” people. Spending more on necessities, on the other hand, can make households feel as if they “can’t get ahead.”

This chart shows the ratio of consumer discretionary spending to total personal consumption. A higher ratio means that households are spending more on discretionary items and less on food, clothing, gas, heat and rent. Although the ratio has generally increased since the late 1950s, there have been two periods when the pace of improvement slowed, in the 1970s and since 2000.

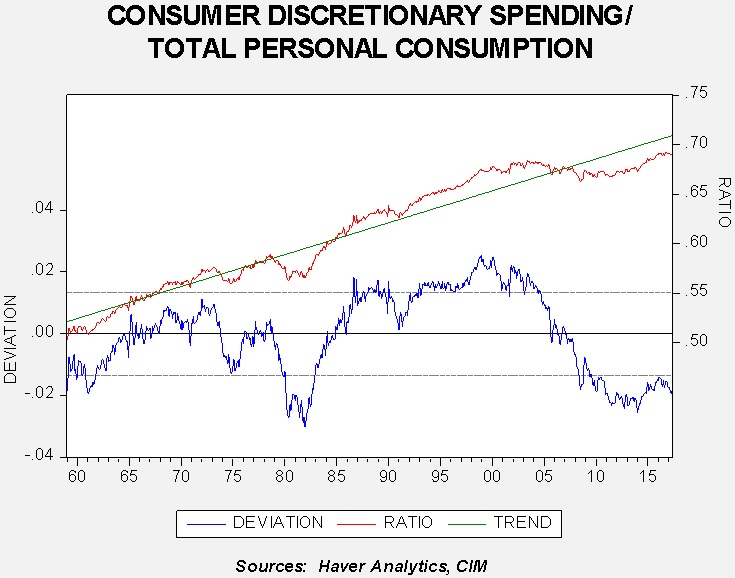

To better analyze the behavior of this ratio, we regressed the ratio against a time trend.

There have been four periods when this ratio was significantly below trend. The first was in the early 1960s. John F. Kennedy’s presidential campaign promised to get America moving again after the somnolent 1950s. The second occurred during the deep 1973-75 recession, which coincided with the first energy crisis. The third occurred during the late 1970s into the early 1980s; this period featured a “double dip” recession and another energy crisis. The 1970s also had major political problems, including the Nixon resignation and the difficult presidency of Jimmy Carter.

The most recent event has been the longest. The major recession of 2007-09 coupled with a slow recovery and stagnant income growth has led to a period where necessities are taking up a bigger share of spending relative to trend. It coincides with deep political divisions and a fear among many Americans that stagnation is never-ending.

To some extent, this is an imperfect measure of sentiment. After all, the trend will eventually reach 100%, which would mean that spending on the four necessities would need to fall to zero (either we stop eating, wearing clothes, driving and living in homes or apartments) or the cost of these goods would approach zero. Neither scenario is likely. Still, the fact that spending on necessities is higher than trend relative to other spending has proven, historically, to signal social and political problems. As one who lived through President Carter’s “malaise” speech, the feeling in the late 1970s was rather bleak. Ronald Reagan’s optimism was key to lifting the country out of this funk. The fall in inflation that allowed households to spend less on necessities did the rest.

So far, this period of below-trend spending on discretionary goods has not adversely affected financial markets. However, it is clearly having an impact on the current political situation and, at some point, it could affect market confidence. We monitor these conditions closely and are somewhat heartened by the recent improvement in this ratio. However, this time around, falling prices for energy and food probably won’t be enough to raise this ratio. Rising wages for the bulk of American households is probably the only way to lift this ratio back to trend.

[Posted: 9:30 AM EDT] Commentary from the White House remains belligerent, but U.S. equity futures appear to be stabilizing. Here is what we are watching:

U.S. v. North Korea: In a press event yesterday, President Trump doubled down on his bellicose rhetoric against North Korea. He added to it this morning, saying the U.S. has prepared “military solutions” that are “locked and loaded.” Although we are sure some plans are in place, we also note that there are no carrier groups in theater; the U.S.S. Carl Vinson and the U.S.S. Theodore Roosevelt are both in training exercises off the U.S. West Coast. The U.S.S. Nimitz, which was in the Far East in the spring, is now in the Persian Gulf. We estimate that two of these vessels could be near North Korea in two to three weeks. We also note that “non-essential diplomatic and military personnel” in South Korea have not been ordered to leave. If a major military operation is to be executed, we would expect two and preferably three carriers in the Far East and non-essential personnel to be evacuated. Thus, any military operations that could be executed now would be air attacks from Guam, Japan and South Korea. Although potent, attacks from these sources would be limited.

We were actually more interested in comments from SOD Mattis yesterday, who warned North Korea to “cease any consideration of actions that would lead to the end of its regime and destruction of its people.” Although Mattis is still pressing for a diplomatic solution to the current problems with North Korea, this warning should be taken seriously; attacking the U.S. will lead to an overwhelming response that will likely lead to the end of the Kim regime. Essentially, Mattis is suggesting that a military strike on the U.S. could trigger a devastating response.

We still think the odds of an actual conflict are low, but the risk is rising. It will be interesting to see how financial markets handle today’s market close. Does a trader want to go home for the weekend with a levered long position in equities?

The problem of positioning: As we have noted before, the Federal Reserve appears to be attempting to manage financial conditions as an unofficial third mandate. All the financial conditions indices we monitor remain at low levels (although they will tick up next week). We have serious doubts as to policymakers’ abilities to manage financial stress, but it does appear that low interest rates and perhaps an enlarged balance sheet have given investors comfort. In response to the third mandate, investors have been increasingly shorting volatility. The position has worked.

(Source: Bloomberg)

This chart overlays the VIX ETF (VXX, 13.29) and the inverse VIX ETF (XIV, 78.18). Over the past five years, holders of the VXX have suffered huge losses, while holders of the XIV have done well, especially since mid-2016. Obviously, yesterday we did see a spike in volatility and the XIV dropped sharply. Our concern is that investors have taken the “don’t fight the Fed” advice with regard to the third mandate and have increasingly shorted volatility. The problem is that the Fed doesn’t have direct control over financial stress. Thus, this positioning by investors aligns with the goals of policymakers; sadly, policymakers lack the tools to enforce their goals. Shorting volatility is a bit like “pocketing nickels in front of freight trains.” The position works well most of the time but, when it doesn’t, the reversals can be significant. Our worry is that if investors decide to abandon these short volatility positions, it could lead to selling pressure in the equity markets as money managers who target volatility will be forced to reduce share levels as volatility rises.

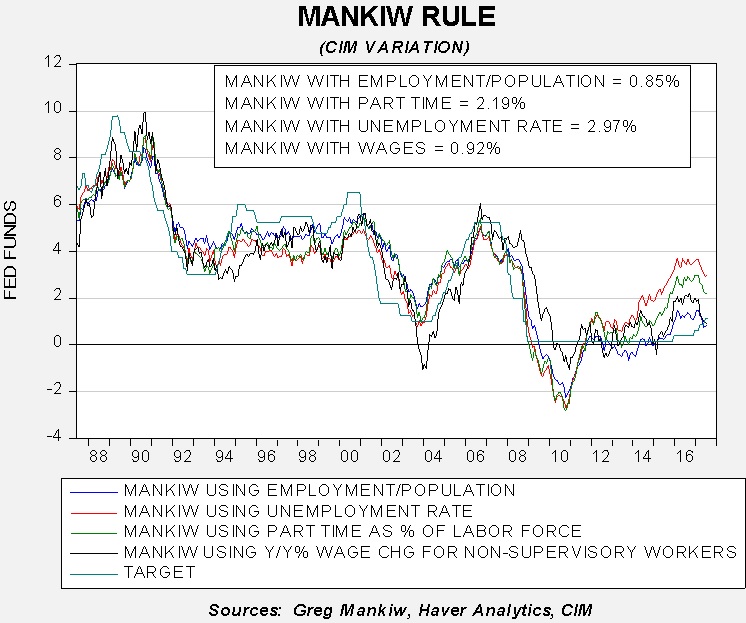

With the release of the CPI data and yesterday’s FOMC action, we can upgrade the Mankiw models. The dip in the core CPI rate (see below) did affect the Mankiw Rule model results.

The Mankiw rule models attempt to determine the neutral rate for fed funds, which is a rate that is neither accommodative nor stimulative. Mankiw’s model is a variation of the Taylor Rule. The latter measures the neutral rate using core CPI and the difference between GDP and potential GDP, which is an estimate of slack in the economy. Potential GDP cannot be directly observed, only estimated. To overcome this problem with potential GDP, Mankiw used the unemployment rate as a proxy for economic slack. We have created four versions of the rule, one that follows the original construction by using the unemployment rate as a measure of slack, a second that uses the employment/population ratio, a third using involuntary part-time workers as a percentage of the total labor force and a fourth using yearly wage growth for non-supervisory workers.

Using the unemployment rate, the neutral rate is now 2.97%. Using the employment/population ratio, the neutral rate is 0.85%. Using involuntary part-time employment, the neutral rate is 2.19%. Using wage growth for non-supervisory workers, the neutral rate is 0.92%. There wasn’t much change from last month; two of the models, the employment/population ratio and non-supervisory wage growth, are suggesting the Fed has achieved neutral policy. The other two remain elevated and indicate that 200 bps of tightening are necessary to achieve neutral.

To a great extent, the issue for policymakers remains the proper measure of slack. The danger for the financial markets is that the proper measure is either wage growth or the employment/population ratio but policymakers believe slack is best measured by either involuntary part-time employment or the unemployment rate. If one of the latter two is their measure, policymakers will likely overtighten and prompt a recession. Since inflation remains tame, it probably makes sense for the Fed to hold steady for a while to see if inflation does accelerate. That’s what we expect the FOMC to do; so does the market. Fed funds futures are not looking for another rate hike until mid-2018, which is why the dollar is weakening. As long as inflation remains tame, the pace of hikes will remain slow.

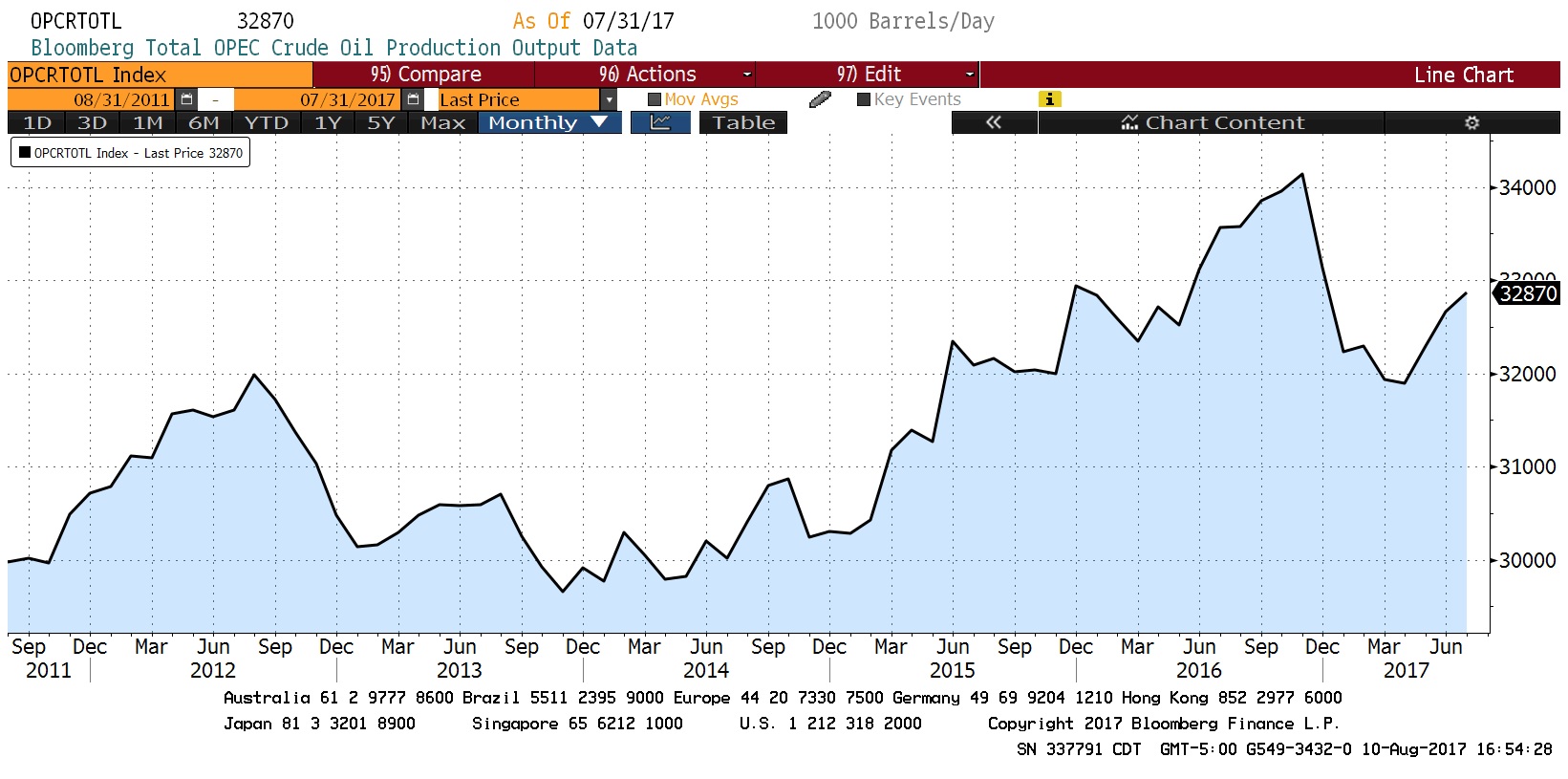

OPEC woes: As we noted yesterday, U.S. commercial crude inventories contracted sharply and have fallen rather impressively this summer. However, oil prices remain stalled on worries that OPEC output discipline is weakening. The data support that concern.

(Source: Bloomberg)

This chart shows the Bloomberg estimate of OPEC production, which is consistent with other sources of this data. Since March, OPEC output has jumped almost 0.9 mbpd, with much of that coming from states that were not given quotas, such as Nigeria and Libya. Saudi Arabia needs to press the other members to bring this production down if it wants oil prices to rise further.

Grain woes: Grain prices plunged yesterday after the USDA lifted production and ending inventory estimates for corn and soybeans. The government also lowered its estimates for prices and farm incomes. Higher inventories and lower prices will put economic pressure on the agriculture sector and give some leverage to China in trade talks. After all, the economic pressures in the farm belt would be exacerbated if China were to retaliate against American farm products due to trade restrictions it faces from the U.S.

[Posted: 9:30 AM EDT] Global equity markets are lower this morning as tensions surrounding North Korea rise. There is a growing chorus of commentators warning about a repeat of 1987 (maybe because we are approaching the 30-year anniversary?), which would be momentous because that crash was the last major one that was not associated with a recession. We have our doubts that a major correction is in the offing but, if it is, it should probably be treated as a buying opportunity. The softer than expected PPI data (see below) has put some downward pressure on the dollar and boosted Treasuries. It didn’t have much of an effect on equities. We get the CPI data tomorrow.

North Korea: The Kim regime has indicated it is drawing up plans to fire up to four missiles at Guam, which is a U.S. territory and the home of the Anderson AFB, a major base in the region. The symbolism of such a threat is high; Guam, although not a state, is close to being one. Persons born in Guam are American citizens. The territory has a non-voting delegate to the U.S. House. It has no electoral votes but it does participate in the primary process, so it has a modest effect on the presidential race. Thus, attacking Guam isn’t exactly like attacking an American state, but it’s close. We suspect the Kim government intends to land the missiles in the waters around Guam. This would represent the closest attack on what should be described as American soil so far by North Korea. It’s not clear how the U.S. will respond to such a launch if it transpires. NBC is reporting[1] that the U.S. is drawing up plans to attack North Korean missile sites pre-launch (so-called “left of launch”) that would likely be executed by B-1 bombers[2] currently located in Guam. Another alternative would be to use anti-missile defense systems to hit North Korea’s medium-range missiles after launch. Attacking North Korea left of launch risks escalating the situation; not attacking assumes the North Korean missiles will fall harmlessly into the sea and not actually hit Guam. We are treading into difficult territory here and the steady flight to safety in assets is warranted.

Mixed messages: The “fire and fury”[3] comments from President Trump, which were apparently his own, have been downplayed by his secretary of state and secretary of defense. We do know that Chief of Staff Kelly has actively worked to limit the reading material of the president to create a consistent message. Still, with the president’s use of social media and his personality, it will be nearly impossible to prevent such statements. The worry is how they are interpreted by the rest of the world. Already, Japan and South Korea are looking to boost their own defenses, in part on concerns that they can’t accurately predict how the U.S. will react to events. Although we believe this rearming is a natural consequence of the U.S. reducing its superpower role, this process may be accelerating as the world observes how the U.S. behaves in light of foreign policy crises.

Trump v. McConnell: A war of words has erupted between the president and the Senate majority leader. The latter, citing the lack of experience in the White House, has chastised the president for creating impossible deadlines that lead to the impression of failure on the part of Congress. The White House has pushed back, suggesting that McConnell is ineffective and should be working more diligently to get legislation passed. This spat is counterproductive. All presidents want things to happen fast; political capital is perishable and thus patience isn’t a virtue. On the other hand, senators only face a vote every six years and not all at once, so a more deliberate pace is part of the legislative structure. In our observation, the key to speed in the Senate is sequencing. Presidents should offer the easiest and most bipartisan legislation first to get bills passed quickly even if this legislation isn’t a high priority. Instead, administrations tend to pursue the most aspired legislative goals that are often partisan in nature and consume lots of political capital and take a lot of time to pass. If we are correct, President Trump should have started with infrastructure, which would have built his bipartisan credentials and would have passed easily. Bill Clinton often remarked that he should have started with welfare reform instead of his ill-fated health care changes. The president will need McConnell to create tax reform (or cuts) and so this argument isn’t helpful toward that goal.

Energy Recap: U.S. crude oil inventories fell 6.5 mb compared to market expectations of a 2.1 mb draw.

This chart shows current crude oil inventories, both over the long term and the last decade. We have added the estimated level of lease stocks to maintain the consistency of the data. As the chart shows, inventories remain historically high but they are declining. Again, there was no oil sold out of the Strategic Petroleum Reserve this week. The authorized sale is nearly complete as 16.2 mb have been released out of an authorized 17.0 mb.

As the seasonal chart below shows, inventories are usually well into the seasonal withdrawal period. Even with the SPR sales, we have already seen a larger than normal seasonal decline; in fact, the drop is rather remarkable. It should be noted that the seasonal trough isn’t usually hit until mid-September. Thus, we should see further stock withdrawals over the next five weeks.

(Source: DOE, CIM)

Based on inventories alone, oil prices are overvalued with the fair value price of $49.36. Meanwhile, the EUR/WTI model generates a fair value of $64.36. Together (which is a more sound methodology), fair value is $59.54, meaning that current prices are well below fair value. The most bullish factor for oil currently is dollar weakness, although the rapid decline in inventories is also supportive. Prices are essentially at fair value based on inventory levels but, thus far, oil prices have completely ignored the weaker dollar. We do expect that the dollar will begin to have a bullish impact on oil prices in the coming weeks.

[2] One of the reasons for using B-1s is that they are no longer fitted to carry nuclear weapons. Thus, there would be no confusion from North Korea misconstruing this as a nuclear attack.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.