History seems to move in broad cycles. Beliefs come into and fall out of favor. Despite evidence of these cycles, people tend to “forecast with a straight edge.” In other words, we assume trends that are in place will remain in place forever. And, thus, it can come as a shock to society when trends shift.

One key reason why people tend to be surprised by inflection points is because we are mortal. Once we identify the trends in place there is an incentive to buy into those patterns. There are pundits who warn us that changes are in the offing but they are often warning us well in advance of the shift, and thus can either become like “Cassandras” who always signal calamity or like “stopped clocks that are right twice a day.”

In Part I of this report, we will offer some observations about inflection points—points in history when conditions change and a new regime of policy and thinking becomes dominant. These observations will lay the groundwork for Part II, where we will examine in detail what we believe are two coming inflection points. As always, we will conclude with market ramifications.

[Posted: 9:30 AM EDT] U.S. equity futures are flat this morning after a strong rally on Friday. Here is what we are watching this morning:

Powell the dove: Chair Powell participated in a panel discussion on Friday that included former Fed Chairs Bernanke and Yellen. He pretty much said everything the market wanted to hear. He indicated that there is “no preset path” for policy, including raising rates and adjusting the balance sheet. The financial markets interpreted these comments as an indication that the FOMC is taking financial market action seriously and that a pause is possible. As we noted last week, the implied LIBOR rate from the two-year deferred Eurodollar futures suggest the Fed should stop raising rates now. The Fed seems to have taken that news to heart.[1] We have been favorable to the idea that the Fed would manage a soft landing, a tightening that doesn’t bring a recession.[2] Our research suggests the Fed is now at the point where further tightening increases the risk of a policy error. Powell’s comments suggest he is aware of the risks.

The Syria withdrawal…nevermind:[3] After President Trump ordered the withdrawal of U.S. troops from Syria, Defense Secretary Mattis left the administration. Op-eds argued the move was leaving the field to Iran. However, the hawks in the administration, at least for now, appear to have reversed this move. National Security Advisor Bolton has placed conditions on fulfilling the action, which could delay the actual withdrawal for a long time.[4] The two primary conditions are that IS must be destroyed and the Kurds’ safety must be guaranteed.[5] Although American troop presence in the region is part of the U.S. superpower role, President Trump, consistent with his Jacksonian archetype, wants to reduce this role to only direct threats to the U.S. and any nation that besmirches American honor. Will Bolton (and, to some extent, Pompeo) be successful in reversing the president on Syria? We will be watching for two items; first, does the right-wing pundit class start criticizing the decision, and second, does Trump see Bolton’s actions as a direct refusal? With regard to the first, it should be noted that the president was prepared to avoid a government shutdown over the wall until the pundits began to criticize his decision. We doubt the Syria issue will raise the same degree of ire but, if it does, look for the president to push for withdrawal. Second, Bolton has been smart to not openly defy the president but to put conditions in place that essentially mean the troops will be there for a long time. Kurdish safety alone likely requires American troop presence. So, for now, the U.S. will be maintaining its role in Syria.

Another split in Ukraine: The Eastern Orthodox Church has formally split by recognizing the independence of the Orthodox Church of Ukraine as separate from the Russian Orthodox Church.[6] The church in Ukraine has been under the jurisdiction of the Russian church since 1686 when the Russian Church split from the Eastern Orthodox Church, which was centered in Constantinople. What will make its break difficult is that there are church members in Ukraine who maintain their allegiance to Moscow. This fact could further undermine Ukrainian unity. We would look for the Kremlin to use this dissention to further weaken the government in Kiev.

Trade talks: China and the U.S. will begin trade talks in Beijing today. Discussions will last two days and are designed to lead to further negotiations.[7] In the short run, we expect an agreement that will reduce trade tensions. China’s economy has been slumping and Xi needs to reduce trade pressure. The U.S. economy, though in much better shape than China’s, is showing some signs of weakness in the pivotal political year, the year before the election year. President Trump needs to avoid recession in 2019 at all costs or his reelection chances are doomed. However, the long-run situation remains difficult. The U.S. and China are strategic competitors, with China attempting to exclude the U.S. from its sphere of influence. This long-run condition means that, over time, the odds of a full-scale military confrontation are growing and the interconnectedness between the two economies will likely break down. Although that condition is not supportive for either economy, we expect a hiatus in 2019.

Hard Brexit looming? We have generally expected the U.K. and the EU to eventually reach a settlement that would not result in a sudden disruption of trade relations. However, as time passes, we are becoming increasingly concerned about the odds of a sudden break. PM May’s plan will go to a vote in Parliament on the 15th after a debate is held this week.[8] May is trying to sway MPs to her plan, but it doesn’t look like it has much chance of passage. May is hoping she can take this failure to the EU for concessions. However, here is the rub—the EU needs a unanimous vote to approve changes and the EU isn’t united on what it wants from Brexit. If Merkel were still powerful, she may have been able to bring enough influence to bear to give May some help. But, with Merkel on her way out, there really isn’t anyone on the EU side that could make concessions in short order.

If the EU can’t adjust, the U.K. could hold a second referendum. However, that option is fraught with risk. Structuring a vote that will reflect the will of the people will be hard. If the vote is between hard Brexit and remain, we would expect remain to narrowly win because the public won’t want the economic disruption that follows. But, that isn’t the only option. A different relationship with the EU is probably what most British voters want, but what exactly that entails is impossible to divine in a simple vote. It’s pretty clear that what May negotiated wasn’t it. The constant talk, even from the Labour Party, is that a different deal is wanted. Unfortunately, there isn’t any evidence that new negotiations would yield a deal better than what May got. If the referendum is simply hard Brexit or remain, and remain wins, then markets will rejoice but there will be a significant minority of U.K. voters who will believe their decision to exit the EU was stolen from them. The Tory party will likely split over this issue, ushering in Labour Party dominance for years. A Corbyn-led Labour government would have sharply negative connotations for U.K. financial markets. In general, the GBP has held up rather well throughout this turmoil, mostly because the dollar is overvalued versus the pound. Nevertheless, a hard Brexit and a Labour government would severely undermine investor confidence and send both the GBP and British equities lower. We are beginning to worry that we, and the markets, have been underestimating the odds of a bad outcome.

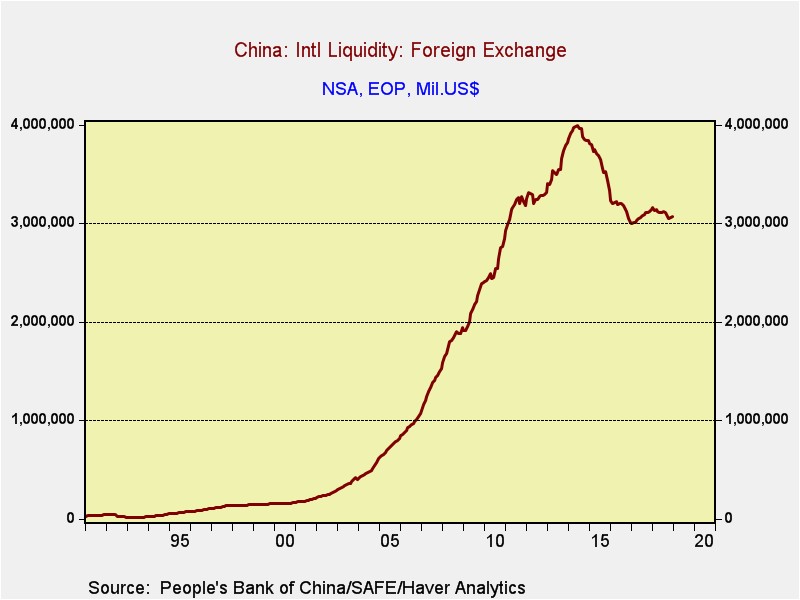

China’s reserves: China’s foreign reserves rose $11 bn in December, pretty much in line with expectations. The modest change suggests there was little selling pressure on the CNY in December.

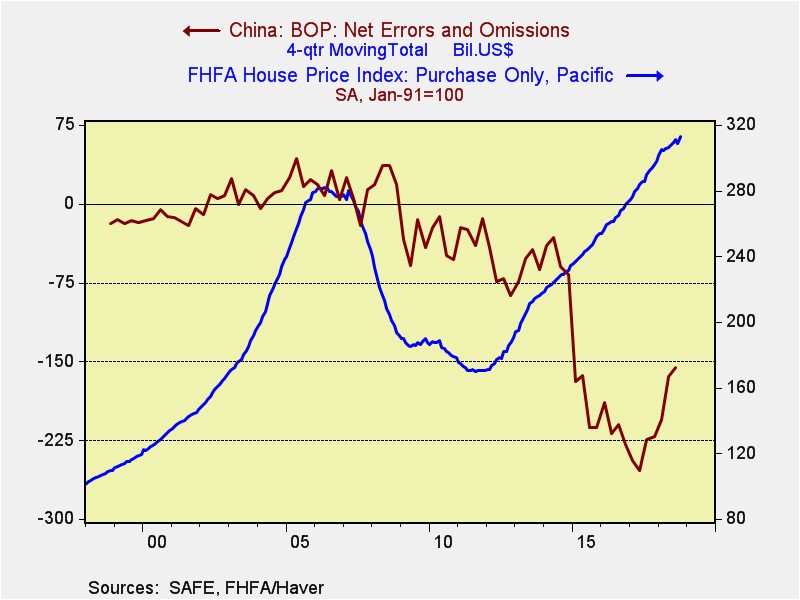

As this chart shows, China has managed reserve stability for the past few years. The lack of pressure on the CNY likely reflects success in restraining capital flight. Although capital flight is always difficult to track down (by design—if I am trying to secretly move my assets out of the country, it should be difficult to figure out what I am doing), the Net Errors and Omissions account in the balance of payments is probably the best measure available.

This chart shows the rolling four-quarter sum of the Errors and Omissions Account. Note that it declined rapidly in 2015, suggesting a rapid increase in capital flight. For illustration purposes, we have included the FHFA Home Price Index for the Pacific region. Although home prices began to recover in 2013 in this region, they accelerated rapidly in 2015 and have remained strong, rising about 7.5% per year. Anecdotal evidence has indicated for some time that at least some of Chinese capital flight was ending up in West Coast real estate markets. The home price data would tend to support this notion.[9]

[9] Although not shown, on a yearly change basis, Pacific region home prices rose faster than any other area of the country except the Mountain region, which may have also garnered some benefit from the capital flight.

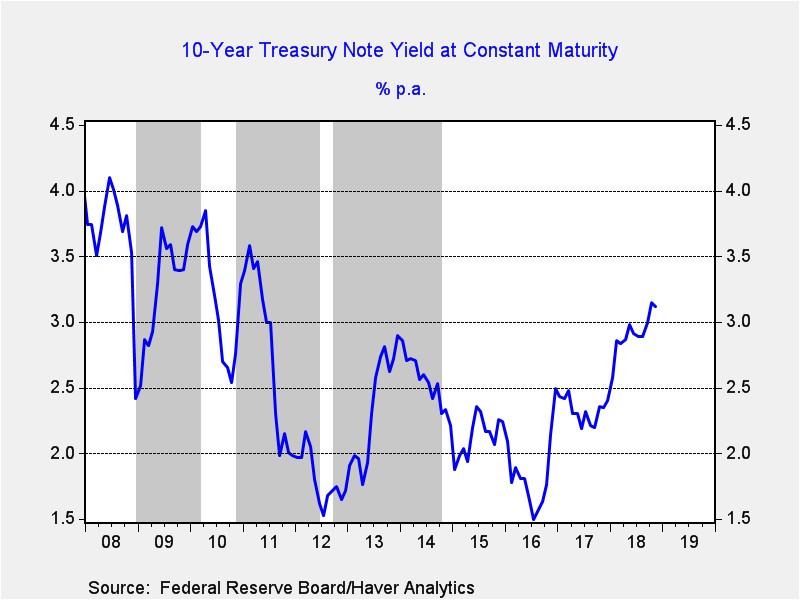

Quantitative easing (QE) was an element of unconventional monetary policy that emerged from the Great Financial Crisis. When the Federal Reserve lowered the fed funds target to zero (known as the “zero interest rate policy,” or ZIRP), policymakers decided that taking the policy rate below zero would not further stimulate the economy. Once interest rates fall below zero, idle cash generates a return and there was fear that negative interest rates would cause cash hoarding, which was exactly what the Fed wanted to avoid. However, policymakers also feared that signaling they lacked additional tools to support the economy could trigger a panic in financial markets. Thus, they created an additional tool, QE, which bought Treasuries and mortgages from the financial system and pushed additional cash into the economy.

The policy was controversial. Some feared it would trigger inflation as the high levels of cash would “inevitably” cause rising prices. Others argued that the process would distort financial markets. But, in the end, the effects of QE were difficult to parse. For example, one of the Fed’s arguments for QE was that it would lower long-term interest rates. In fact, at times, it seemed to have precisely the opposite effect.

This chart shows the 10-year T-note yield. The gray bars show periods of QE. In all three events, yields rose at the onset of the balance sheet expansion. Yields eventually fell during QE2, although that decline was probably more due to turmoil in Europe. Why did yields rise when the Fed was reducing the supply of bonds? Most likely, investors worried that QE would be successful in bringing about inflation and thus demand was adversely affected. Anticipation of the end of QE always led to a drop in yields.

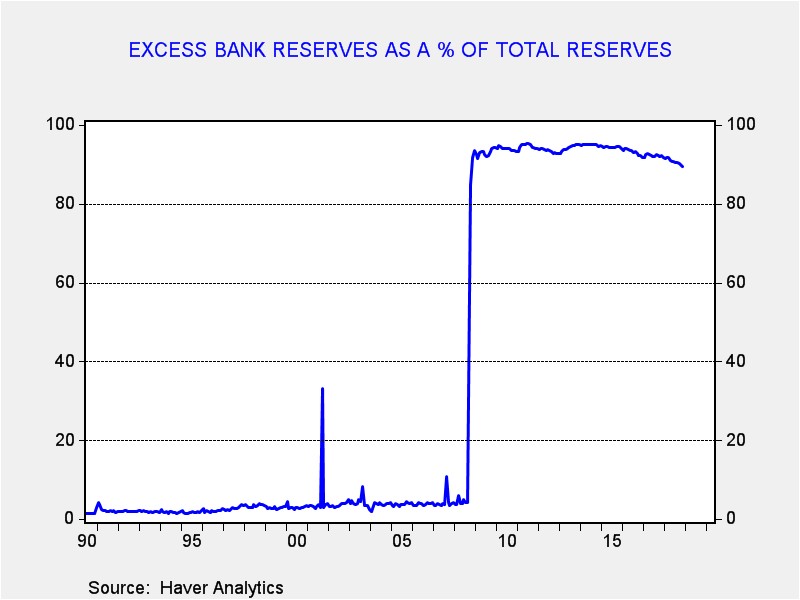

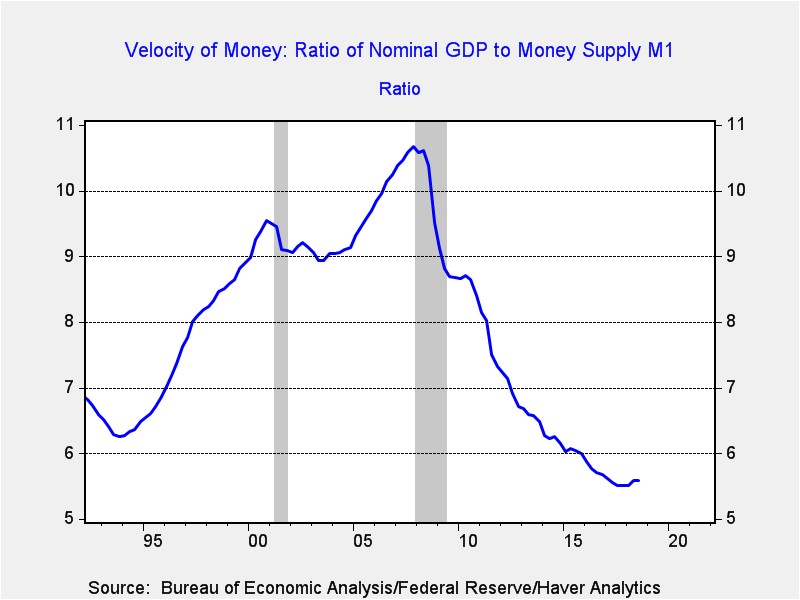

What about all that money that was injected into the system? Much of it remained on bank balance sheets in the form of excess reserves.

Using the equation of exchange (money supply x velocity = price x quantity), the increase in the money supply mostly led to a sharp drop in velocity, instead of boosting prices or quantity.

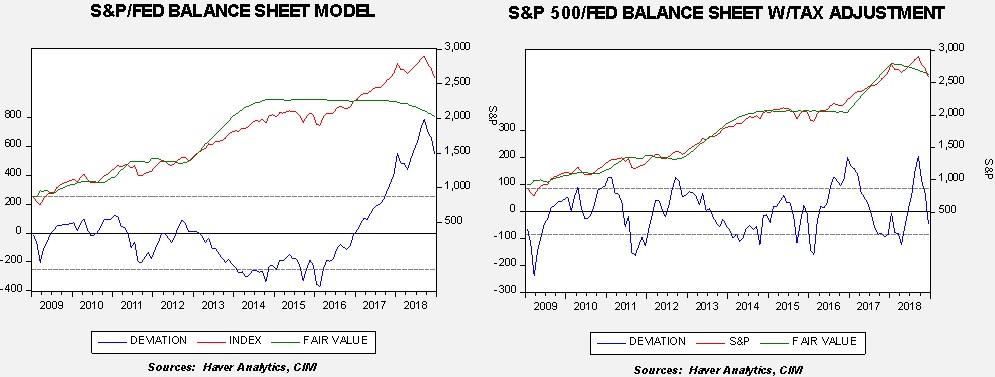

So, if QE mostly sat idle on bank balance sheets then the withdrawal of QE should not have had much of a real impact on the economy. And, that is likely true. However, this isn’t to say that QE had no effect. As we have noted in the past, there has been a close correlation between the S&P and the Fed’s balance sheet.

The chart on the left shows the original balance sheet model; note that after Trump’s election in 2016 the S&P rose much more than the model would have projected. To account for this move, we built a variable that adjusted for expectations surrounding corporate tax cuts. The additional variable improved the model dramatically; however, assuming no further reductions in corporate tax rates, the market is once again tracking the balance sheet.

Essentially, it appears that the impact of QE was mostly psychological; it signaled to investors that the Fed was supportive. Interestingly enough, the withdrawal appears to be adversely affecting investor sentiment. It is hard to determine how much, simply because there are other factors, such as trade conflicts and FOMC criticism, which are also affecting sentiment. However, this data suggests that a pause in the balance sheet reduction would likely improve investor sentiment.

[Posted: 9:30 AM EDT] After a hard sell-off in equities yesterday, we are seeing a bounce this morning. Boosting sentiment are hopes for a dovish tone from Chair Powell, a reserve rate cut in China and the opening of formal trade talks between the U.S. and China. We cover the employment data in detail below but the quick take is that the data came in “hot”—payrolls rose 312k, well above expectations, and wage growth was strong. We did see a rise in the unemployment rate, mostly because the labor force rose. Here is what we are watching this morning:

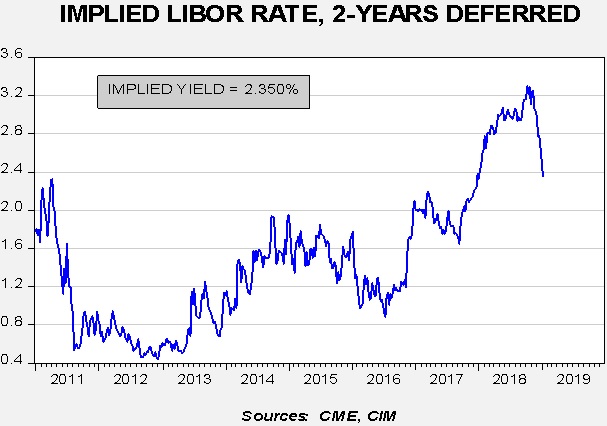

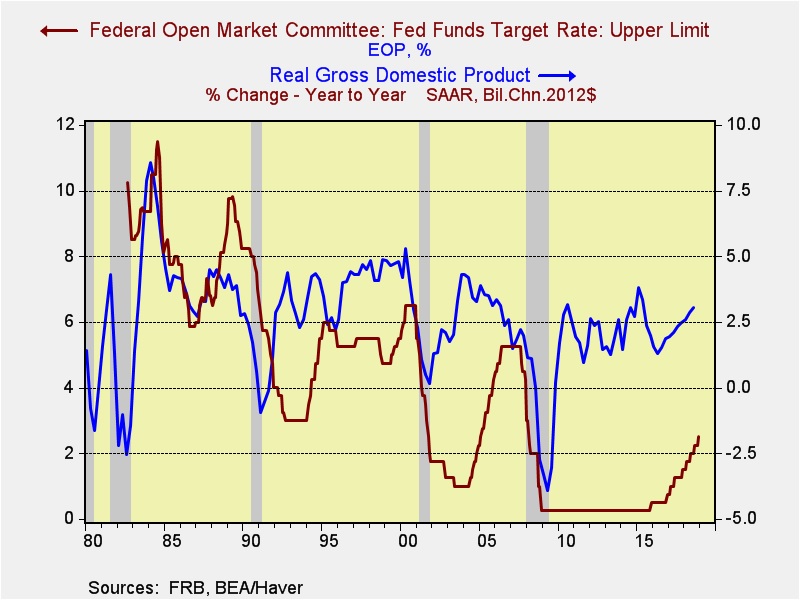

Signs the Fed needs to stop:[1] One of the key indicators we use for monetary policy is the two-year deferred Eurodollar futures. Essentially, it tells us what the market thinks three-month LIBOR will be in two years. It has an uncanny knack for signaling when policymakers should target policy rates.

First, the implied rate has fallen sharply in the last few weeks.

The implied LIBOR rate was 3.30% in late October. It has dropped almost 100 bps since then to 2.35%. As noted, this implied rate is closely tied to fed funds.

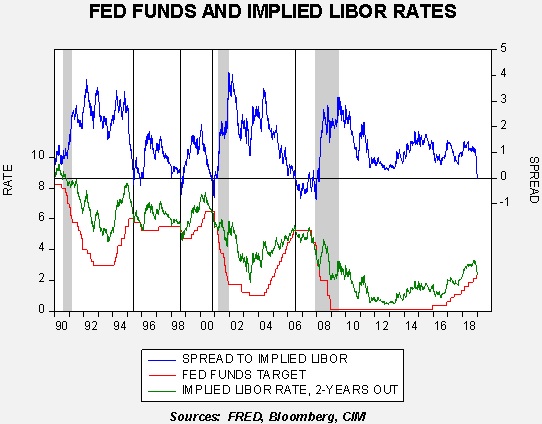

This chart shows the implied LIBOR rate along with the fed funds target on a weekly basis. The inflection points are shown by vertical lines. Recessions are in gray. Note that the Fed tends to stop raising rates when the upper line falls below zero. In fact, the Greenspan Fed tended to move rates based off this implied rate. We have seen a significant drop in the implied LIBOR rate to the level of the current mid-point of the policy rate range. Although the Fed may not necessarily need to lower rates, increasing rates at this point would be a serious policy mistake. Chair Powell is participating at a closed panel interview along with former Chairs Bernanke and Yellen at the American Economic Association in Atlanta today at 10:30 EST; we will be watching to see if he suggests any thoughts of a pause. We note that Dallas FRB President Kaplan told Bloomberg yesterday he supports a pause. The above data suggests the FOMC should take the advice seriously. At the same time, if Powell does lean toward further increases, he will likely cite today’s employment report.

Reserve rate cut: China cut its required reserve ratio[2] for banks by 50 bps on January 15 and an additional cut of the same magnitude will follow on January 25. That will take the reserve ratio for large banks down to 13.5%. Although this is good news, the action is modest at best. First, the PBOC’s Medium-Term Lending Facility will expire later this year and the ratio cut is designed to partially offset that loss. Second, the bank is anticipating the usual liquidity problems associated with the Chinese New Year (which is on February 5 this year; in the Chinese zodiac, it’s the year of the Pig). Although the financial markets appear to be treating the action as policy stimulus, in reality, there isn’t a lot here; in fact, the PBOC could offset any stimulus by raising the repo rate. However, we do expect to see rate cuts later this year to offset slowing growth.

Trade talks: The U.S. and China will begin formal trade talks on Monday.[3] Jeffrey Gerrish, the deputy U.S. trade representative, will lead the talks. Gerrish is closely aligned with Lighthizer, so we would expect him to hold to his boss’s hard line in negotiations. It is generally expected that these talks will lay the groundwork for higher level negotiations next month.

The U.S. and China: Apple’s (AAPL, 142.19) warning yesterday[4] highlights a problem in the geostrategic relationship between the U.S. and China. Both nations are now rivals, but unlike the U.S./Soviet rivalry during the Cold War the U.S. and Chinese economies are closely tied together. CEA Chair Hassett’s comment yesterday suggesting that U.S. companies with ties to China “are going to be watching their earnings be downgraded next year until we have a deal with China” sent tremors through the equity markets. We note the editorial boards of major papers are waking up to this problem.[5] China’s economy is clearly coming under pressure, in part due to the trade actions by the U.S.[6] But, the drop in the U.S. manufacturing PMI data yesterday shows that the American economy is also feeling a pinch from tightening monetary policy and issues with China.

The British faced a similar problem in the late 1800s as two rising nations, Germany and the U.S., threatened its global dominance. The U.K. managed the U.S. by essentially ceding the Western Hemisphere to America, quietly acknowledging it would be unable to defend Canada from a U.S. invasion. It turned its focus to Germany; sadly, that issue led to WWI. The U.S. needs to redefine its relationship with China. The idea that the Chinese would follow the path of Germany and Japan and align with U.S. geostrategic interests has been proven false. However, this redefinition will likely have an adverse impact on the economies of both nations. We also note the State Department has raised its warnings to Americans in China.[7]

Brexit: Our position has been that the May government or its successor will avoid a hard Brexit. However, the odds of such an outcome do appear to be increasing. One factor that appears to be driving the Tories to this outcome could best be described as “delusions of empire.”[8] There seems to be this belief that Britain, freed from the constraints of the EU, could “get the band back together” and recreate the Commonwealth.[9] We expected these ideas to fade as Brexit approached, but that doesn’t seem to be happening. In fact, polls suggest that 57% of Tories would rather have a no-deal Brexit than PM May’s plan.[10] The general consensus is that a no-deal Brexit would bring a nasty economic shock for the economy. However, the Tories simply don’t trust that narrative. For the rest of the population, 42% prefer to remain in the EU, 25% opted for no deal and 13% would accept May’s plan.

One potential outcome could be a split in the Conservatives between the leave and remain camp, which would lead to a position of dominance. A Corbyn-led government would be a major negative for British financial assets. Corbyn’s policy goals include renationalizing major industries and punitive taxes. This isn’t our base case but the country seems unable to come to a consensus about its position, and the longer indecision reigns the greater the chance of a crisis.

[Posted: 9:30 AM EDT] It was all about Apple (AAPL, 157.92), which is down around 8% in the pre-market trade, and the yen. Here is what’s going on:

AAPL: Apple[1] released a letter warning investors that the company would miss revenue estimates. Two reasons were given for the decline, weaker economic growth in China and disappointing upgrades. We won’t discuss the latter issue but the former is important. The trade conflict between the U.S. and China hit the Middle Kingdom at an inopportune time, just as China was trying (again!) to implement deleveraging. The act of reducing debt growth would, on its own, slow growth and cutting exports to the U.S. added to that issue. To some extent, the slowdown in Chinese growth isn’t a surprise; recent purchasing managers’ data already showed that the Chinese economy was slowing. However, the AAPL news suggests the trade war may be affecting U.S. equity earnings. There are already rising worries about 2019 earnings due to slowing economic growth. For a prominent company like Apple to confirm these concerns has led to a sharp decline in U.S. equity futures this morning.

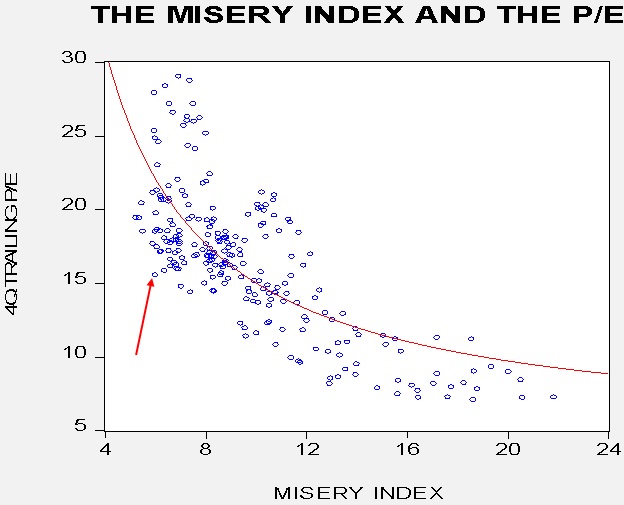

At the same time, as our P/E chart at the end of this report shows, much of this worry has probably already been discounted. The multiple has declined significantly and is unusually low given the level of economic activity.

This chart is a scatterplot of the four-quarter trailing P/E and the misery index, the sum of the unemployment rate and the yearly change in inflation. The arrow shows the current ordered pair of these variables. Essentially, this ordered pair usually indicates either a P/E in the low 20x or a misery index in the neighborhood of 10 (e.g., 6% unemployment with 4% inflation) instead of the current 5.9. Obviously, markets are forward-looking but this data suggests that the financial markets are discounting a plethora of economic weakness. So, to some extent, the Apple news should be seen as a confirmation rather than a new insight.

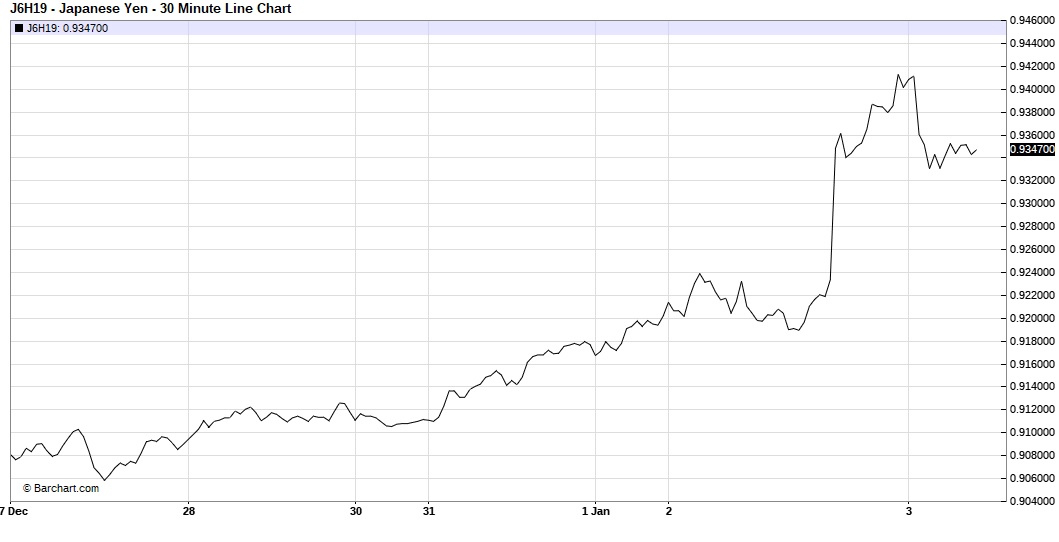

The yen: Overnight, the JPY soared in value.

(Source: Barchart)

This is a five-day chart of the yen futures (which are priced at 100 JPY per dollar). In cash terms, the yen jumped to 105. There is a lot of speculation about why this occurred,[2] ranging from an algorithm-driven event to perhaps related to the Apple news. The JPY is seen as a safety asset and if fear of a global recession is increasing then it makes sense that the JPY would rally. We note the AUD fell hard, which would tend to confirm the China story. We have been favorable to the yen for some time; on a purchasing power parity basis, the currency should be trading around 60 yen to the dollar. Because Japan has been a persistent current account surplus nation, it is forced to invest overseas. However, if Japanese domestic savers become fearful, they tend to repatriate, leading to a stronger yen. That happened last night, although some of it was likely exacerbated due to thin trading conditions. Still, the rise in the JPY is a warning that concerns are elevated.

Paygo: “Pay as you go” is a budget policy that requires the government to make all discretionary actions budget-neutral. Thus, if taxes are cut, spending must fall to offset the action. This is why there are discussions about “dynamic vs. static scoring” for budget actions. Supply side economists will argue that tax cuts stimulate the economy and boost revenue so the potential loss of revenue from a well-structured tax cut is less than the mere revenue loss measured with a static score. In its most extreme form, tax cuts are thought to not only be revenue-neutral but perhaps even revenue-increasing.

President G.H.W. Bush implemented this policy. It was a statutory requirement from 1990 to 2002. His son allowed the measure to expire which permitted the 2003 tax cuts and the Medicare prescription drug expansion to be enacted. Both widened the deficit. After taking back the House, the Democrats made Paygo the House rule from 2007 to 2010. However, in reality, the Paygo rules had loopholes for emergency spending and the like. Still, they acted as a brake on spending and revenue adjustments.

There is a major battle brewing between the Left-Wing Establishment (LWE) and Left-Wing Populists (LWP) on this issue.[3] Incoming speaker Pelosi wants to return to Paygo; her progressive wing opposes her on this measure. The LWE wants to be the responsible “adults in the room” and use Paygo to restrain the spending measures from the LWP and further tax cuts and extensions from the GOP. The LWP sees Paygo as an unnecessary restraint on environmental and social spending.

On its face, this is just a run of the mill fight over spending priorities. However, there is something much more important underlying this fight. The person to watch here is Stephanie Kelton, an economics professor at Stony Brook. Kelton is rapidly becoming the face of Modern Monetary Theory (MMT), a heterodox theory on money and the economy. She spent 17 years at the University of Missouri-Kansas City (UMKC) in the economics department and was the chair during her tenure. UMKC is the center for MMT with some of its seminal thinkers on the faculty. She was also the chief economist for the Senate Budget Committee and senior economic advisor to the Sanders campaign.[4]

We will have more to say about MMT later this year but, in a nutshell, the theory suggests that the government is the primary issuer of currency. We use and trust our currency because it is necessary to pay taxes. Taxes are designed, like monetary policy, to manage the economy. Taxes are not required to fund the government; the government can fund itself at any level simply by issuing currency. Instead, taxes, like interest rates, should be adjusted to constrain inflation and for other social goals. So, a deficit isn’t bad but normal, and should only be reduced when the economy is overheating. As long as slack exists in the economy and there are needs in society, the government should simply spend the money until inflation becomes a problem.

There are some caveats. First, these rules only apply to governments that issue fiat currencies and borrow in their own currencies. So, state and local governments, which don’t issue their own currency to pay for stuff or service their debt, cannot run deficits. Thus, nations under a gold standard or nations with fixed exchange rates can’t use MMT. For example, the Eurozone nations cannot use MMT (as the Greeks discovered) because they don’t borrow in a currency they issue. Second, in practical terms, it is really hard for citizens to believe that their taxes aren’t necessary to fund the government. If they are not necessary, why pay them? Even if MMT is correct, the belief that taxes fund the government (which is true on a state and local level) may be a useful fiction.

However, during periods of economic stress, the government should run deficits but needs a theory that becomes the narrative to defend and explain the deficits. During the Great Depression, Keynes offered that narrative. In the early 1980s, when the U.S. was trying to quell inflation through high real interest rates, deregulation and globalization, there was a need for deficits to act as a safety valve for the economy. Supply side economics offered that narrative. Kelton’s MMT could very well be the theory that becomes the LWP’s narrative to explain how we can provide free college and health care to all without raising taxes to pay for it. Another thought is that high marginal tax rates are not necessary to fund the government but they can act to change the behavior of business leaders. If high salaries are mostly taxed away, CEO pay no longer acts as a “scorecard” for success and firms may be inclined to pay their workers more.

Our position has been, for some time, that the level of inequality in the U.S. was unsustainable and that a cycle of equality was coming. But, for that cycle to develop, a narrative is necessary; MMT will likely be that narrative. The key area to watch is the forex market. If the LWP is victorious and deficits soar, the exchange rate market will become the arena for how markets adjust. The first nation to go MMT will likely also have a weaker currency. In fact, the exchange rate may become the only constraint on deficits. As the past four decades have shown, a nation open to trade and technology disruption (which are not necessarily separable) can keep inflation under control. But, a decline in the currency might act as a constraint. Perhaps, under MMT, we could end up with something resembling a loose gold standard. However, this assumes that some nation doesn’t adopt MMT and become the standard bearer, much like gold did.

So, this fight is a big deal. If Pelosi loses it, watch Kelton and MMT. It could become the new narrative for the equality cycle.

Oil: OPEC output is declining[5] and there are growing worries that U.S. production cannot be maintained[6] without rising investment, which is unlikely with tighter financial conditions and low oil prices. Our position is that oil prices are well below fair value. We would look for a recovery in the coming months.

[Posted: 9:30 AM EDT] Back to the salt mines! The New Year, 2019 (hard to believe, isn’t it?), is starting out with a thud as weak Chinese data has sent equities into the red. Here is what we are watching this morning:

The Chinese data: The PMI data[1] from China came in soft, with the Caixin PMI dipping under the expansion line of 50 with a reading of 49.7 in December. This is the first time since May 2017 that the number has fallen below 50. The official PMI report, which came out on New Year’s Eve, was also under 50 at 49.4. Although the equity market mostly shrugged off the earlier report, the combination of both numbers under the expansion line has clearly raised fears that the Chinese economy is slumping. And, the usual response from policymakers, which would be strong stimulus, seems to be lacking this time. For example, the central government is warning local governments to avoid pushing property and real estate development to boost output.[2] Although the position of the central government makes sense (boosting apartment building would likely only bring further overcapacity and bad debt), China may be moving into the phase where it can no longer rely on investment for growth. In other words, China may now need to get serious about boosting consumption as its engine of growth. The problem is that (a) consumption would have to grow very fast to absorb the excess capacity, and (b) this path will have significant political consequences as it will upend the business model that has made important members of the CPC billionaires.

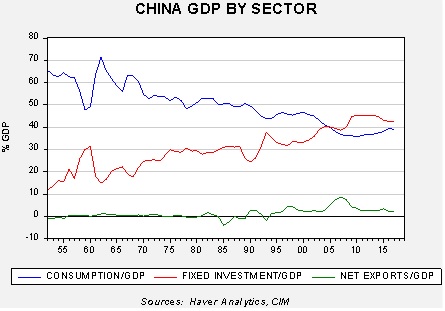

This chart shows China’s GDP by sector in percentage terms. A developed economy generally has consumption around 60% to 70% of GDP. China’s development model was based on investment and net exports, which were funded by household saving, mostly through suppression consumption. Although this model delivers strong growth, eventually excess capacity develops as investment becomes excessive and the “safety valve” of exports becomes stretched as foreign nations rebel against the loss of market share and unemployment. One way China could address this issue would be to shift ownership of state owned enterprises to households; the increased wealth would likely boost consumption (wealth effect) but it would deny ranking members of the CPC the avenue to power. This is why Beijing’s decision to signal to local governments that real estate development won’t be supported is important because it indicates that investment, at least for now, won’t be the path to support growth. Unfortunately, the Xi government hasn’t signaled how growth will be lifted.[3]

Washington unrest: There are two items of concern, the shutdown and the Right-Wing Establishment (RWE) rebellion.

Shutdown: The partial government closure has moved into 2019. Congressional leaders are meeting with the president today. The Democratic House leadership is preparing legislation to end the shutdown that will not include the $5.0 billion for border wall funding. It’s hard to see how the president won’t veto the bill and McConnell has already indicated he won’t approve a House bill that the president won’t sign. For now, the shutdown isn’t having much impact on the economy or, for that matter, the financial markets. But, it is causing individual hardship and we would not be surprised to see national park managers begin to close their facilities because they don’t have enough personnel to secure them. That outcome is bad publicity and will increase pressure for an agreement.

Rebellion: Before the break, we noted there was growing pushback against the president from the RWE. The situation with General Mattis was a key element in the criticism of the White House. The latest censure comes from the newly elected senator from Utah, Mitt Romney.[4] The op-ed, printed in the Washington Post, is a textbook response from the RWE. Romney applauds the president’s policy successes of cutting corporate taxes, reducing regulation, appointing conservative judges and attacking China’s unfair trade practices. What he slams the president on is character. As we have noted before, until January 2018, the president’s policy mix was establishment-supportive by cutting taxes and regulations. And, the financial markets rewarded the president with a strong rally. But, once the president moved to a serious attack on global trade, the equity markets began to stumble and are now in bear market territory. Although the RWE would like relief on technology transfers to China, it does not support tariffs or wants to see the loss of globalization, something the president favors. Trump has responded to Romney’s comments via Twitter[5]; as these responses usually go, this one was actually rather tame (no new nicknames for Mitt, for example). Romney is in a position to be critical of Trump; he is a senator, meaning he doesn’t face election for another six years, and he is nearly unassailable in his home state.

There are other new critics as well. Retired Gen. Stanley McChrystal sent a broadside against the president, calling him “dishonest, immoral.”[6] Trump’s response was more typical.[7] Retired Gen. David Petraeus indicated he wouldn’t serve in a Trump administration.[8] Probably the key issue that has led to the attacks from former generals is the sudden withdrawal from Syria. In response, the White House is slowing the withdrawal to about four months instead of weeks.[9]

The key question politically is whether Trump can win the 2020 presidential election with only the support of Right-Wing Populists (RWP). Much of that will be determined by who the Democrats nominate. Sen. Warren put her name on the list over the holiday. We would expect at least 19 more to participate in the nomination process. The conventional wisdom will be to run a Left-Wing Establishment (LWE) figure (e.g., Mayor Bloomberg, VP Biden) that would act as a “unifier.” This temptation will be strong; the GOP faced a similar situation in 2012 and lost by nominating Mitt Romney who failed to generate enthusiasm among the RWP. A similar move by the Democrats is possible, which would improve the odds of another term for President Trump. On the other hand, a Left-Wing Populist (LWP) would very well leave the financial markets with no favored candidate. That outcome would justify the current weakness in equities.

Trade with China: We think the odds favor a short-term deal with China that would offer relief to the equity markets. Trade Representative Lighthizer appears to oppose this outcome.[10] The problem for Trump is that if he orders Lighthizer to make a temporary agreement, the latter might walk. Although Lighthizer’s exit would be welcomed by the equity markets, it would seriously undermine the president’s efforts to change China’s trade behavior.

Taiwan: General Secretary Xi threatened to unify the island with the PRC.[11] Although we still view such comments as rhetoric and not a call to arms, if China decides it needs a “splendid little war” to assert its power in the region then a forcible unification of Taiwan with the mainland would be attractive. This issue did not reach a level to make our 2019 Geopolitical Outlook[12] list; however, it may reach this status by mid-year.

Italian banks:The ECB has appointed temporary administrators[13] to Banca Carige (CRG-IT, EUR .0015).[14] Although the Italian government mostly caved to EU demands on its budget, the problems with Italian banking have not been resolved and could still trigger a problem in the Eurozone.

(N.B. This is the last Asset Allocation Weekly for 2018. Have a Merry Christmas and Happy New Year. The next report will be published January 4, 2019.)

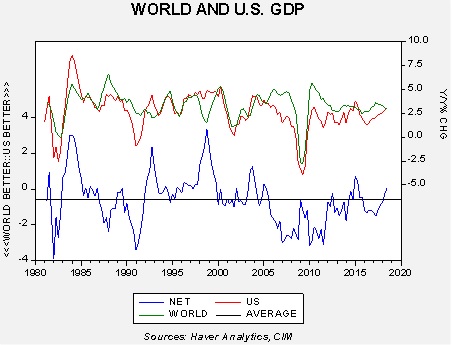

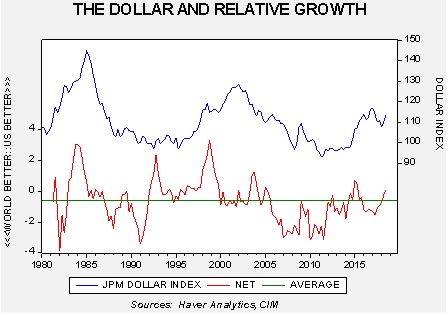

The U.S. economy is performing in line with the rest of the world.

This chart shows the yearly change in U.S. and world ex-U.S. GDP. The lower line on the chart shows the difference. On average, U.S. growth is usually 0.61% lower than world growth and the world exceeds U.S. growth 70% of the time (with data since 1981). This situation isn’t a huge surprise; the U.S. is the world’s largest economy and smaller economies can grow faster more easily. The lower line shows that U.S. growth has been gaining on world growth for the past two years.

The net number does coincide with dollar cycles.

When the growth differential is below average (implying stronger world growth relative to the U.S.), the JPM dollar index averages 107.21. When growth exceeds average, the index averages 113.14. We are projecting slower growth in the U.S. next year, around 2.7%, which is essentially average growth. If world growth also holds near average, around 3.3%, it would be reasonable to expect the dollar to weaken from current levels. The U.S. growth surge in 2015 led to a strengthening dollar and this year’s rally was partly due to the lift in U.S. growth due to fiscal stimulus. As that wanes, relative growth should favor the world, which will support a softer greenback. In general, a weaker dollar will tend to support commodities and foreign equities, especially emerging markets. We expect those assets to perform better in 2019.

[N.B. The Daily Comment will go on holiday from December 24 to January 2. From all of us at Confluence, but especially Thomas and me, thanks for reading and have a Merry Christmas and Happy New Year!]

On Friday, December 14, we published our 2019 Outlook: Red Sky at Morning report. If you missed it, you can find the report linked here or on our website.

Happy Winter Solstice! It’s another risk-off day—Washington unrest is the catalyst. Here is what we are watching this morning:

Washington unrest: Although spending any time watching cable news could lead one to think that Washington is always in crisis, what is going on now is actually chaotic. Here is the rundown:

Shutdown: It appeared the White House and Congress had a deal. In fact, a large number of senators headed home after voting for a spending bill, thinking the issue was resolved. The president, however, changed his mind and demanded border wall funding. The House did vote for the measure but it has no chance in the Senate. And so, we are heading into a partial shutdown. Usually, financial markets pay little mind when we have a shutdown outside of a debt ceiling issue. However, the sudden shift from an agreement to no deal has undermined investor confidence, which is already fragile. The president indicated that the shutdown could last a long time; that outcome could eventually start delaying data releases, which would further unsettle conditions (imagine no employment data for a month, or relying on the API for energy data).

Mattis: General Mattis was the last constituent of the “committee to save America,”[1] members of the administration representing the establishment who saw themselves as the primary barrier preventing the president’s populist instincts from running rampant. Since the president’s election, we have noted the continued battle between the establishment and the populists within his administration. The establishment pushes for business and market-friendly policies, such as tax cuts and deregulation. It opposes the populist goal of deglobalization, which includes trade impediments and immigration restrictions. The president has tended to straddle these divisions; the establishment has clearly benefited from tax cuts and deregulation, but the populists cheer the tariffs, tough talk on the border and anti-immigration stance of the White House.

In terms of foreign policy, populists want to reduce the American superpower role while the establishment supports continued American hegemony. That means continuing to freeze the three conflict zones,[2] which include the Middle East. This policy goal has been coming under pressure well before Trump took office. The Middle East became unstable after Bush removed Saddam Hussein from power and led Iraq into civil war. President Obama’s support for the Arab Spring led to civil conflict in Syria. The decision not to enforce the “red line” against Assad for using chemical weapons further weakened the U.S. position in the region. The power vacuum led to the rise of IS and prompted the U.S. to insert troops in the region to weaken this group. Russia has reasserted itself in the region. Iran is attempting to expand its influence. Saudi Arabia has been courting the U.S. to undermine the Obama-era policy of normalizing relations with Iran.

So, it’s not like President Trump inherited a well-functioning policy. However, removing U.S. troops from Syria ensures the U.S. will have even less influence in the region.[3] Secretary Mattis opposed removing the troops, but the president exercised his prerogative and ordered the withdrawal of the 2,000 American troops in the area. Mattis apparently saw this as his red line and resigned. And, he didn’t just resign—his exit letter lacked any of the usual expressions of gratitude to the president and instead offered a stinging rebuke.[4] In the letter, Mattis defended the Liberal World Order of free trade and support for allies—in other words, the policy the U.S. has followed since the end of WWII. Essentially, Mattis is indicating that, in his view, the president doesn’t support that policy, while Mattis does, and it is probably better for the president to have a defense secretary who has views consistent with his own.[5] Already, U.S. allies are viewing the resignation with trepidation.[6]

This exit isn’t just the normal flow in and out of an administration. Mattis is signaling to the GOP establishment that Trump is turning populist and the members of the establishment have to start considering their options. And, we are seeing some pushback. Sen. Ben Sasse, who has been critical of the president, was critical on this issue, too.[7] Sen. Lindsey Graham, who has had an on and off relationship with the president, is in a full-on Twitter feud with the White House.[8] However, perhaps the most unexpected response came from Sen. Mitch McConnell, who has generally been supportive of the president; he was actually rather critical of the decision that led Mattis to resign.[9] Mattis represented, to some degree, a member of the administration that the establishment could look to for comfort. That is now gone.

We will be watching how far this establishment rebellion goes. Already we are seeing Sen. Grassley push back on steel and aluminum tariffs as part of USMCA.[10] The shutdown will likely anger Senate Republicans. At the same time, the president seems to be moving into an increasingly populist stance this year. The trade conflict began in earnest in February. The removal of troops is classic Jacksonian policy, who like to fight wars with overwhelming force and clear endings. The president is planning on drawing down troops in Afghanistan,[11] likely opening up the country for the return of the Taliban.

Our view is that President Trump has been attempting to placate both the populists and the establishment but he is steadily being forced to choose. If he decides to go populist, he will lose support in the Senate which may hurt him if impeachment occurs. At the same time, his victory was mostly due to populist support. The president has a difficult political path to hew. It may be difficult to pull off. But, the more he leans populist the greater the risk to equity markets. It would make sense to delay this conflict as long as possible but it appears that option may not be available. Thus, we will continue to closely watch how this situation evolves.

China: The U.S. has accused two Chinese nationals of a series of cyberattacks on the U.S.[12] Other nations have made similar accusations. So far, the U.S. and China have kept trade talks separate from security issues. But, that condition may not last. China has announced further measures to boost the economy, which has slowed due to earlier deleveraging and trade issues.[13] Although China has been buying more American soybeans, thus far it has not purchased U.S. crude oil.[14] That fact has likely added to recent crude oil weakness.

Brexit: According to reports, PM May is building options in case her Brexit proposal fails. This may include delaying the exit,[15] a new referendum or new elections.[16] Given that deadlines didn’t improve the chances of her plan, it probably makes sense to consider other options. We still expect another referendum with the increased chance that Brexit may be rescinded.

[N.B. The Daily Comment will go on holiday from December 24 to January 2. From all of us at Confluence, but especially Thomas and me, thanks for reading and have a Merry Christmas and Happy New Year!]

On Friday, December 14, we published our 2019 Outlook: Red Sky at Morning report. If you missed it, you can find the report linked here or on our website.

There isn’t a whole lot going on this morning; most of the market commentary is a post mortem on the Fed. We offer our views on the U.S. central bank below. Equity markets are trying to rally this morning but oil prices are testing recent lows. Here are the updates:

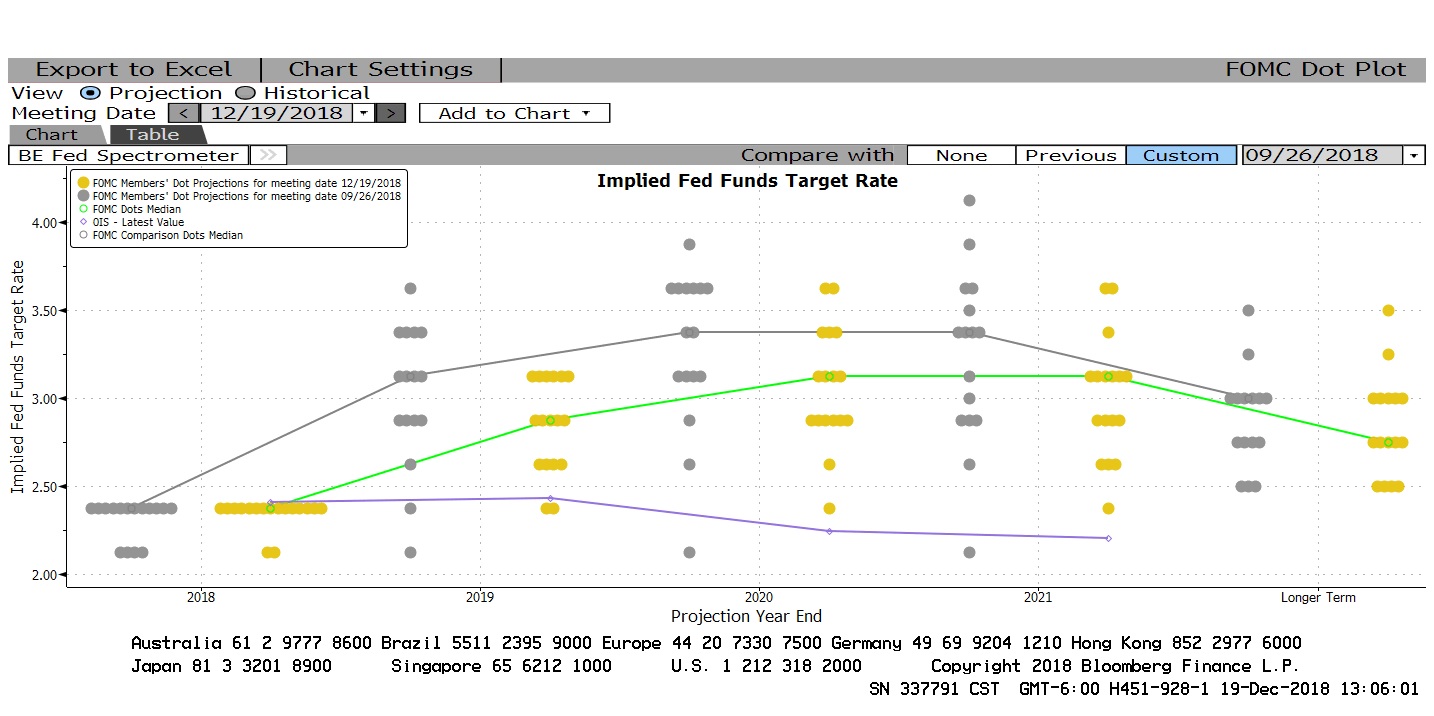

The Fed: Yesterday, we offered four outcomes from the Fed meeting. Essentially, the FOMC split the difference between outcomes #3 and #4. To recap, #3 was a hike with a clear signal of no further increases, while #4 was no change in the previous policy path. What we actually got was a hike with a reduction in the path forward.

(Source: Bloomberg)

The yellow dots show yesterday’s meeting, while the gray dots show the meeting from September, the last time we had a dots plot. The lines show the median rate path. Note that there has been a cut of about 25 bps in the path for next year and 2020. The statement had few changes, with the most significant being an acknowledgement of monitoring global and financial market conditions. The economic projections were mostly unchanged; there was a modest increase in forecast GDP growth for next year to 2.5% from September’s 2.3%, while core PCE is expected at 2.0%, down from 2.1% in September.

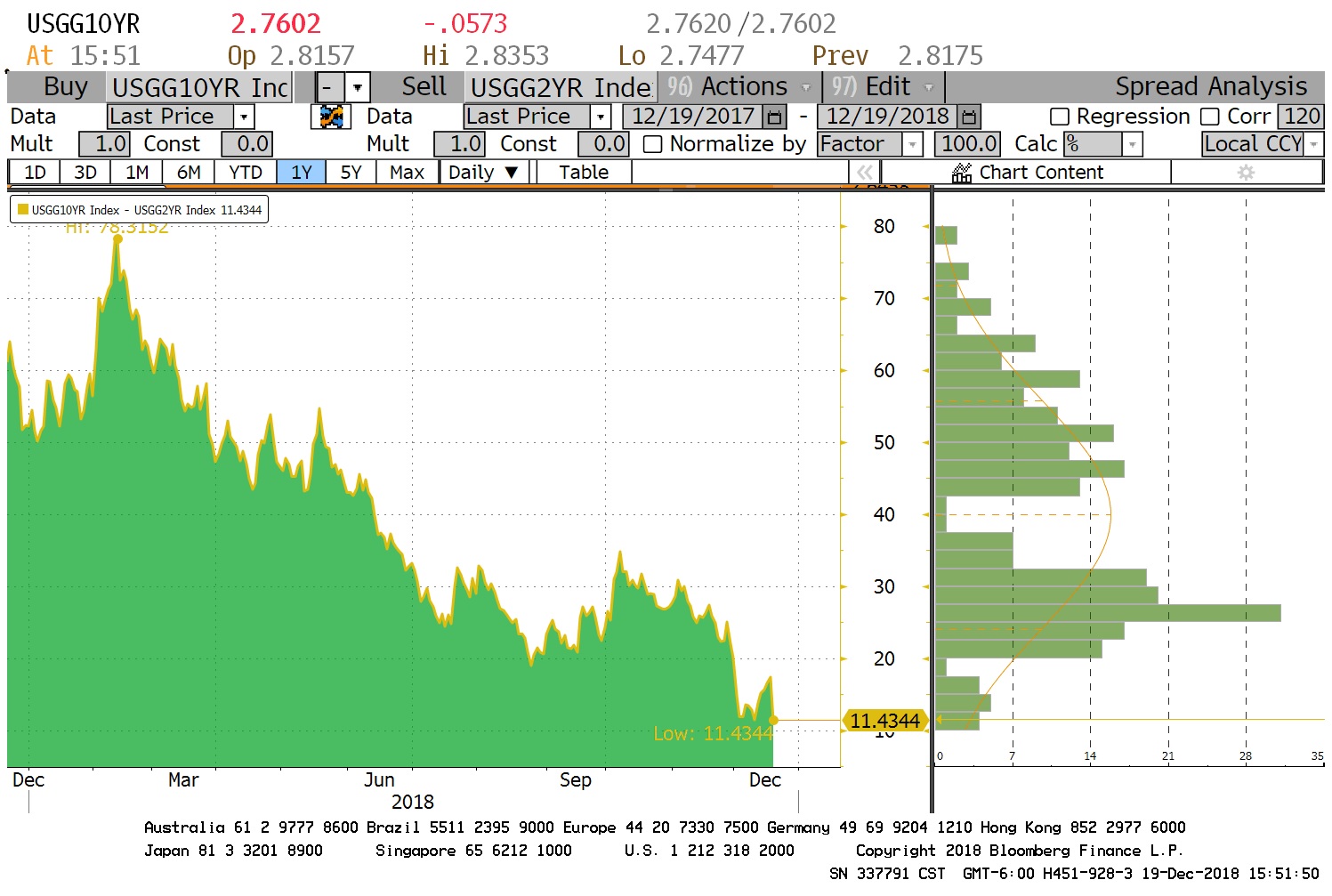

Clearly, financial markets were disappointed. The yield curve (2yr/10yr Treasury) flattened further.

(Source: Bloomberg)

The spread narrowed to just over 11 bps. Equity markets fell; the decline from peak to yesterday’s low has now reached about 15.4%. In general, a correction is 10% and a bear market occurs at 20%. The latter is usually associated with recession. Sentiment indicators are reaching levels that usually signal a washout. If recession is avoided, the chances are elevated for a rally in equities.

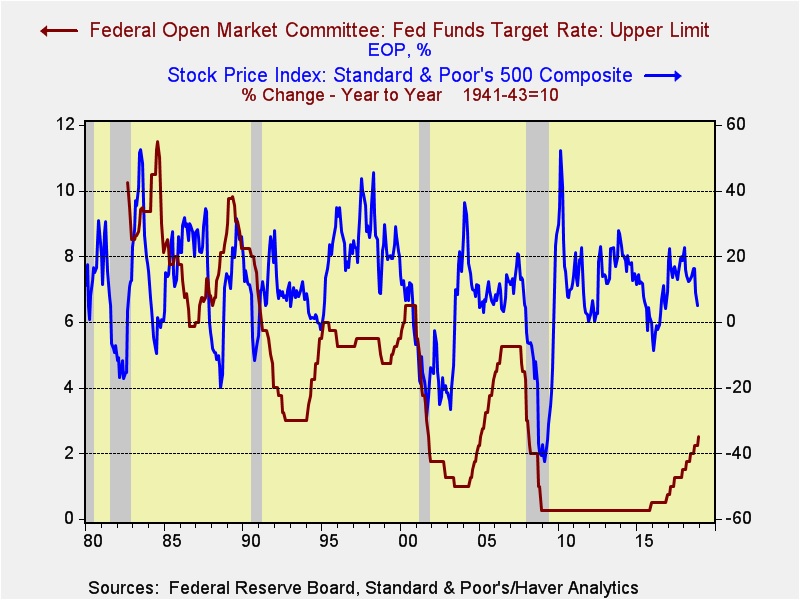

At the same time, financial markets were clearly disappointed. The Fed is dealing with what has been called the “Tinbergen dilemma,” named for the economist Jan Tinbergen, who first described it. The dilemma describes when a policymaker faces two policy problems but only has one policy tool. It is sometimes described as “trying to shoot two bad guys with one bullet.” The Tinbergen dilemma can only be resolved if the two policy problems can be fixed by the same solution. The Fed is facing an economy that is still rather strong (though momentum is clearly weakening), which supports tighter policy, and financial markets that are signaling increasing stress, which begs for easing. What has the financial markets so upset is that there is evidence that, in the past, the Fed has tended to placate the financial markets when facing a similar Tinbergen dilemma.

This chart shows the fed funds target with the yearly change in the S&P 500. When the yearly growth in the S&P becomes negative, the Fed has tended to take notice. Perhaps the clearest evidence of the Fed favoring financial markets was in 2000-04 when the Greenspan Fed kept cutting rates to what were historic lows at the time, even though the economy was recovering.

This chart shows the yearly change in real GDP. Greenspan didn’t start raising rates even with GDP growth exceeding 4% in 2003, most likely due to continued weakness in equities. In 2016, Yellen paused on rates as equities fell, but the economy has softened, too.

Essentially, financial markets have become accustomed to being favored when the aforementioned Tinbergen dilemma exists. Powell is trying to weave a path that addresses both but, in reality, it looks like the Fed is more concerned about the economy overheating than it is about a weak stock market or a flattening yield curve. This position increases the likelihood of a policy mistake, one of our four potential threats to the expansion we discussed in our 2019 Outlook.

So, what happens now? Equity market valuations are improving and sentiment is becoming increasingly negative. Both tend to favor a bounce at some point. The proverbial “Santa Claus Rally” probably won’t happen this year, but we would expect a January bounce.

U.S. out of Syria: President Trump announced that the 2,000 U.S. troops in Syria will be leaving very soon. The foreign policy and military establishment[1] is horrified at the prospect of having no influence in this part of the world. The winners in this decision are Iran, Russia, Turkey and Assad. The losers are Israel (due to the improvement in Iran’s position), Europe (will likely see a rise in refugees) and the Kurds. The Kurds are especially harmed; they have supported U.S. efforts in this part of the world since the early 1990s when the U.S. began protecting northern Iraq with a no-fly zone. However, now they will be subject to the tender mercies of President Erdogan. The reaction from Washington is actually rather interesting; populists are applauding the president. Even some former Obama officials are supporting Trump. Meanwhile, establishment figures on both sides of the aisle oppose the move.[2]

What are the ramifications? We will likely see the powers in the region turn on each other. Iran will try to maintain its “Shiite arc” from Tehran to Beirut, while Turkey will attempt to contain the Kurds. There will be conflict points between these two. Israel will try to prevent Iran from projecting power. Russia will likely try to manage the parties but we would not be surprised to see Moscow caught in a trap of maintaining peace. Meanwhile, the likely chaos will help Islamic State revive. Iraq will also be threatened by the ensuing conflict. The problem for the U.S. is that the commitment is never-ending. Trump, like a true Jacksonian, sees no reason why the U.S. should concern itself with the region. The consequence is that the region will likely descend into chaos.

At the same time, it is important to remember that the last three presidents have struggled to craft a working policy for the Middle East. President Bush made a critical error by removing Saddam Hussein from power without being able to replace him, creating a power vacuum in the region that still hasn’t been filled. President Obama tried to extricate the U.S. from the region by putting Iran in charge; although a defensible policy, it was far from ideal. President Trump reversed the Obama-era Iran policy but found that none of the other parties in the region can stabilize it. It appears that U.S. policy is now to allow the chips to fall where they may. This policy will allow one of the three frozen conflict zones to thaw; how this works out is anyone’s guess but we doubt it will be smooth. The primary market beneficiary will likely be oil.

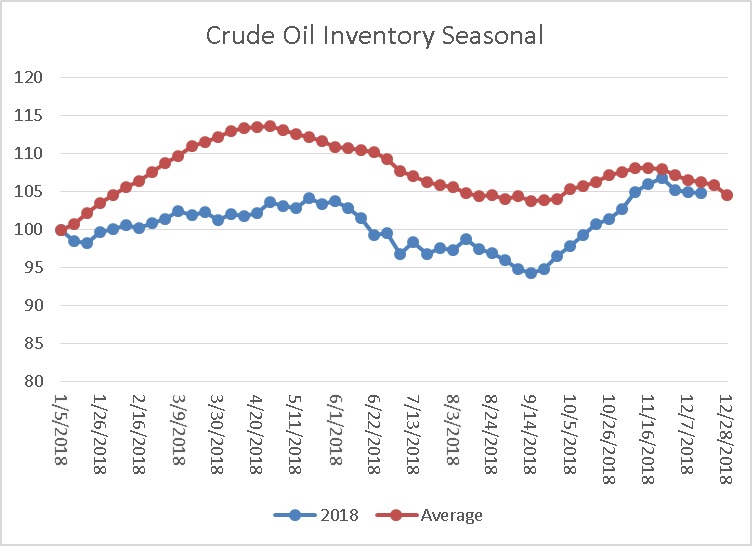

Energy update: Crude oil inventories fell 0.5 mb last week compared to the forecast decline of 3.3 mb.

In the details, estimated U.S. production was unchanged at 11.6 mbpd. Crude oil imports and exports were essentially unchanged, while refinery runs rose a modest 0.4 mbpd.

(Source: DOE, CIM)

The seasonal chart suggests the usual easing of inventory accumulation into year’s end is underway. Inventories usually decline into the new year.

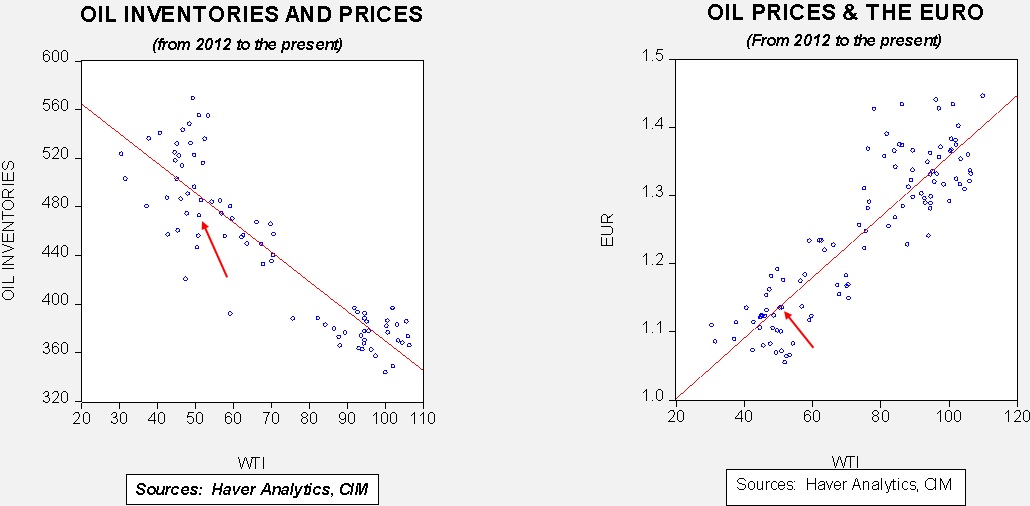

Based on oil inventories alone, fair value for crude oil is $60.35. Based on the EUR, fair value is $54.30. Using both independent variables, a more complete way of looking at the data, fair value is $55.70. By all measures, current oil prices are undervalued. Although fears of a weaker global economy do play a role in price weakness, it appears that even modest action by OPEC to restrict output should lift prices to the mid-$50s in the coming weeks.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.