Author: Amanda Ahne

Daily Comment (July 7, 2026)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment today opens with news that Iranian forces have fired missiles at two commercial ships in the Strait of Hormuz, putting at risk the current US-Iran ceasefire and negotiations toward a permanent end to the war. We next review several other US and international developments that could affect the financial markets today, including a statement by Federal Reserve board member Christopher Waller on monetary policy and a French court decision allowing far-right leader Marine Le Pen to run in the country’s 2027 presidential election.

United States-Israel-Iran: US officials say Iran’s Islamic Revolutionary Guards Corps this morning fired missiles at two commercial ships passing through the Strait of Hormuz. The action shows how the IRGC continues trying to scuttle the current US-Iran ceasefire. However, it’s not yet clear whether the new attacks will put an end to the current recovery in shipping through the strait, which has been proceeding faster than expected. Global oil prices are little changed so far this morning.

US Monetary Policy: Fed board member Christopher Waller, whom President Trump had once considered elevating to the chairmanship, yesterday voiced support for Chair Warsh’s plan to cut back on “forward guidance” regarding the direction of monetary policy. According to Waller, the Fed’s forward guidance on keeping interest rates low during and right after the coronavirus pandemic had “tied the hands” of policymakers and helped spark the excessive price inflation that occurred from 2022 to 2024.

- Waller’s statement helps ensure that the Fed’s forward guidance will indeed be rolled back.

- Weaker forward guidance could well leave investors less sure about the future direction of monetary policy, so it may lead to increases in the policy risk premium in market interest rates. Along with the likelihood of higher and more volatile inflation in the future, that could mean higher interest rates going forward, which would likely weigh on fixed-income and equity valuations.

US Stock Market: SpaceX joins the Nasdaq index today, meaning investors holding mutual funds or exchange-traded funds linked to the index will have exposure to the stock whether they want it or not. However, because of the rules determining how the index is constructed, SpaceX will start out representing less than 1% of the index. Over time, the company’s weight will fluctuate not only as its share price changes but also as its free float changes.

US Artificial Intelligence Industry: The Wall Street Journal today carries an article describing how major AI firms are offering big discounts on compute resources to land and/or keep corporate customers. In some cases, customers have been able to play one AI firm against another to get huge price reductions on needed computing power. The article is likely to further raise concerns about tough competition and excess investment in the sector, which will increase the risk of another correction in AI stock prices.

Canada-Germany: Canadian Prime Minister Carney yesterday announced that his government has selected German shipbuilder TKMS as its preferred supplier for a fleet of 12 new diesel-powered submarines capable of operating in Arctic waters. The government’s second choice is South Korean defense firm Hanwha Ocean. Either way, the selection shows how Canada’s government is seeking to cut its reliance on US suppliers as relations between Washington and Ottawa continue to fray over a number of military, political, and economic disagreements.

Germany: The government of Chancellor Merz yesterday released new budget projections showing it plans to boost borrowing by 838 billion EUR ($958 billion) by 2030, largely to pay for big defense budget increases. The projections illustrate the extent to which even center-right parties in Germany now embrace the idea of borrowing to achieve high-priority public goals, after decades of insisting on fiscal austerity.

- As we’ve argued in the past, the boost in defense spending will likely help spur faster economic growth in Germany in the coming years.

- Coupled with rising orders from foreign governments, higher demand from the German government will likely provide an ongoing boost to the financial performance of Germany’s top defense firms.

France: An appeals court today confirmed the embezzlement conviction of Marine Le Pen, leader of the far-right National Rally party. However, the court also said she would not be banned from running in next year’s presidential election. Opinion polls currently show Le Pen would beat any expected first-round challenger, but she did not immediately say whether she will run. Later today, she is expected to make a statement clarifying whether she will run herself or allow 30-year-old party leader Jordan Bardella to compete in her place.

- If National Rally beats the established centrist parties in the election next year, the result would likely be a sea change in French foreign and domestic policy, including much less support for the European Union and the North Atlantic Treaty Organization.

- The associated political upheaval alone could unsettle European stock markets. If a National Rally-led government also adopted more populist economic policies, investors could also become concerned about a worsening fiscal deficit and higher debt.

South Korea: Memory chip giant SK Hynix late yesterday said American Depositary Receipts (ADR) representing its stock will begin trading in the US on Friday, making it significantly easier for US investors to invest in the surging equity. However, given that the underlying stock’s value has already jumped some 765% over the last year on higher memory-chip prices tied to the artificial intelligence boom, its high valuation likely presents the risk of a correction in the ADR price at some point.

Daily Comment (July 6, 2026)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment today opens with some interesting comments by a major Japanese defense industry leader warning that civilian industrial firms will not necessarily be able to exploit growing defense budgets around the world. We next review several other international and US developments that could affect the financial markets today, including the latest developments around the global oil market as the Strait of Hormuz reopens to shipping and the weekend launch of the “Trump Accounts” program.

Global Defense Industry: Amid a growing global trend of auto firms with underutilized factories trying to convert to green energy and defense products to take advantage of better prospects there, the head of a major Japanese defense contractor today has warned that auto factories probably can’t be used successfully to produce high-demand military drones. According to Eisaku Ito, chief executive of Mitsubishi Heavy Industries, the problem is that production issues between drones and autos are so dramatically different.

- As Ito explains it, factories geared toward automaking or producing other types of standardized, high-volume industrial products would not be able to handle the constant technological changes associated with drones.

- Ito’s statement is important because many struggling industrial firms around the world likely see a silver bullet in the world’s rising defense budgets, which we have discussed in detail. However, investors should probably be wary of whether such “conversion” efforts can work. Experienced defense contractors and closely related technology firms are likely to be more successful in exploiting the trend.

Global Oil Market: The Wall Street Journal today carries a useful article noting that oil tanker traffic through the Strait of Hormuz is starting to recover rapidly following the new US-Iran ceasefire and prices have fallen almost back to their pre-war levels. Near Brent crude futures are trading at about $71.94 per barrel this morning, and some analysts think they could fall to the mid-60s soon. However, the article notes that countries trying to rebuild their emergency stockpiles could help push prices higher again later in the year.

China: The People’s Liberation Army today said a PLA Navy submarine has test fired a long-range ballistic missile carrying a dummy warhead from the waters off northeast China. The missile apparently landed in the southern Pacific Ocean. Although the PLA notified neighboring countries of the launch ahead of time and publicly asserted that it was part of its normal training cycle, US allies in the region have condemned it as destabilizing.

- More broadly, the launch is further evidence that Beijing is trying to take advantage of the US administration’s preference to ease tensions and establish a kind of détente with China after years of escalating bilateral tensions.

- If Chinese officials really do believe that the US will now pull its punches, they could miscalculate, raising the risk of going too far and sparking an international crisis that could be unsettling for financial markets.

United States-Italy: Ahead of this week’s summit of the North Atlantic Treaty Organization, during which leaders from the US, Canada, and many European countries will meet, President Trump has posted a social media meme saying Italian Prime Minister Meloni needs a restraining order. The meme illustrates the rapid deterioration in relations between the erstwhile allies. It also comes as even many right-wing European leaders have begun to distance themselves politically from the US president, signaling continued tensions even as more right-wing parties gain power.

US Politics: In a speech commemorating Independence Day on Friday, President Trump warned that a “resurgence of the communist menace in our land” is currently the “greatest threat” to the US, on par with both world wars and the 9/11 terror attacks. The statement illustrates what is likely to be a key Republican attack line against the Democrats in this autumn’s midterm congressional elections, given that Democratic Socialists have recently won many Democratic primaries across the US.

- It’s not clear that the attack line will be successful.

- However, to the extent it is successful, it would offset other favorable trends that have buoyed Democratic hopes for taking control of at least the House of Representatives.

US Financial Markets: Over the weekend, the Treasury Department officially launched the new “Trump Accounts” program, which gives citizens born between 2025 and 2028 a government-funded, tax-deferred investment account of $1,000 that families can build on over time. Firms can also elect to match employee contributions to the funds. Initially, contributions will be invested in low-cost US stock index funds, such as the State Street SPDR Portfolio S&P 500 ETF (SPYM).

Daily Comment (July 2, 2026)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment opens with our thoughts on the Warsh-led initiative to dismantle conventional forward guidance. Following that, we examine several key market-moving developments, including Meta’s strategic pivot, the encouraging inflation figures out of the EU, and the prospect of another government equity stake. We also touch on other notable headlines before closing, as always, with a comprehensive roundup of the latest domestic and international economic data.

Warsh Fed Takes Shape: Kevin Warsh recently offered clues into how Federal Reserve communications might evolve under his leadership. Speaking on Wednesday at a central banking forum in Sintra, Portugal, Warsh joined fellow central bank heads in articulating a unified stance on forward guidance, aiming to reset market expectations.

- Additionally, Warsh downplayed the idea of immediate changes to the central bank’s practices. However, he stated it was his “aspiration” to steer the Federal Reserve away from standard government data — which he labeled backward-looking — in favor of more real-time metrics. He also noted that the dots plot will remain in place for at least the short term while his task force conducts its review of Fed communications.

- That said, Warsh does not appear prepared to abandon forward guidance entirely. While he acknowledged that inflation has improved in recent weeks, he emphasized that readings above the Fed’s 2% target would not be tolerated, signaling a reluctance to support near-term rate cuts. He also reiterated his preference for continuing the balance sheet runoff, stressing that any policy adjustments would be clearly communicated in advance.

- However, Warsh does appear to be following through on his plan to establish a task force. On Wednesday, he announced that former Bank of England Governor Mervyn King will lead the initiative. King has previously criticized the Fed’s approach to forward guidance, arguing that policymakers should focus less on signaling specific near-term actions and more on outlining how policy would respond under different economic scenarios.

- King’s appointment suggests that Warsh may favor a shift away from rigid forward guidance, potentially aligning the Federal Reserve with a more flexible, data-dependent communication framework similar to that of the Bank of England. This broader move toward reduced reliance on explicit guidance has also been echoed by other policymakers, including ECB President Christine Lagarde at a recent forum and Bank of Canada Governor Tiff Macklem last week.

- Although there is growing interest in phasing out forward guidance, it doesn’t mean the transition will be a smooth one. In 2022, former Fed Chair Jerome Powell and Lagarde both moved away from forward guidance after being forced into more aggressive-than-expected tightening. Yet, both central banks ultimately reverted to the practice. Even recently, BOE Governor Andrew Bailey provided explicit guidance, noting that rate cuts are “off the table,” suggesting even the Bank of England hasn’t completely dropped the practice.

- Warsh’s appearance at the forum gave him a platform to signal how he intends to shape the Fed’s communication strategy. Market reaction so far has been muted, in part because the incoming data since he took over has largely matched expectations. In our view, as long as investors are confident that Warsh will respond decisively if inflation reaccelerates, they are likely to give him the benefit of the doubt. That goodwill could erode, however, if they begin to question his credibility.

Meta Compute: Meta wants to sell its excess computing power in a move that will likely put it in competition with its Magnificent 7 rivals Amazon, Google, and Microsoft. The move comes as Meta has been spending heavily on building its own data centers to develop its AI models. The plan involves selling access to its AI models hosted on its own infrastructure, as well as raw computing power. This shift reinforces our view that hyperscalers will eventually behave more like utilities as companies transition from growth to mature stages.

EU Inflation Eases: Preliminary data indicates that euro area inflation slowed more than expected in June. Headline inflation decelerated from 3.2% to 2.8%, undershooting consensus expectations of 3.0%. The moderation suggests that recent price pressures — partly driven by the Iran-related shock — are likely to prove transitory. In turn, the data reinforces the view that the ECB may not need to tighten further as inflation continues to move toward its 2% target.

OpenAI Stake: OpenAI, the developer of ChatGPT, is reportedly considering granting the Trump administration a 5% equity stake as part of its efforts to navigate regulatory hurdles ahead of a potential IPO. The move follows recent public remarks by the president expressing interest in securing ownership in the company. If executed, this arrangement could set a precedent for other firms pursuing public listings, particularly in sectors facing heightened regulatory scrutiny. The arrangement reflects a theme in our outlook of the growing government intervention in AI.

Russian Escalation: Moscow launched significant airstrikes on Kyiv and other major Ukrainian cities on Wednesday, killing at least 17 people and injuring around 70. The attacks come amid an intensifying exchange of strikes that have targeted urban centers and signal a potential shift toward broader escalation. This dynamic suggests the conflict may be moving beyond a more contained, military-focused phase toward a wider campaign with fewer constraints on civilian infrastructure.

German Tax Cuts: German Chancellor Friedrich Merz has unveiled a 10 billion EUR ($11.44 billion) tax cut package aimed at jump-starting the economy. The proposal targets middle- and lower-income households. For example, a family with two children earning 60,000 EUR ($68,600) annually would receive a tax reduction of approximately 600 EUR ($686). The plan would be partially funded by raising the top marginal tax rate from 45% to 47%. Politically, the measure appears designed to shore up support among more populist factions as the ruling coalition faces declining approval.

Note: Due to the holiday, there will not be a Comment published tomorrow. We hope everyone enjoys the celebrations for the 4th!

Daily Comment (July 1, 2026)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment opens with a discussion of the Bank of Japan and the evolving question of central bank independence. We then turn to equities, analyzing how the AI‑driven rally has created a new set of market leaders. Next, we briefly address the US decision to lift restrictions on Anthropic, NATO’s appeal for continued US commitment to the alliance, and the upcoming joint review of the USMCA. As always, we conclude with a summary of the latest domestic and international economic data releases.

BOJ in the Middle: Japan’s central bank is facing a growing threat to its independence. This shift comes amid efforts by the Japanese government to reshape the institution’s composition with an apparent preference for more dovish policymakers. While these changes are unlikely to alter the near-term trajectory of rate hikes, they have raised questions about the central bank’s longer-term commitment to policy normalization, particularly as the government seeks to stimulate the economy.

- The Bank of Japan’s independence appears to be coming into question. The decision to reshape the institution reflects broader efforts by the government to align the central bank more closely with the current administration’s priorities. Notably, the economic minister, who attended the June policy meeting, pressed BOJ officials to incorporate the government’s growth objectives into their policy discussions.

- While Japanese Prime Minister Sanae Takaichi has not openly criticized the central bank’s recent monetary decisions, her stance suggests support for reshaping its policy framework. An upcoming policy blueprint, expected to be finalized soon, is likely to emphasize closer coordination between the government and the BOJ to maximize policy effectiveness and stimulate private demand.

- Concerns over the Bank of Japan’s independence, particularly amid the recent rise in inflation, help explain the yen’s recent weakness. While the central bank’s independence is legally protected, statutory provisions require a degree of policy coordination with the government, creating potential tension between autonomy and alignment. As a result, investors increasingly question whether the BOJ will remain fully committed to its price stability mandate.

- Rising pressure on the BOJ to slow its tightening cycle, combined with government efforts to stimulate growth, will likely weigh on the yen. Historically, when the yen weakens, Japan has offloaded US Treasurys to fund currency interventions. While this strategy will likely face pushback from the White House, Tokyo has few other options if it wants to support its currency. Consequently, we could see either a coordinated US-Japan currency policy or a potential sell-off in US government securities.

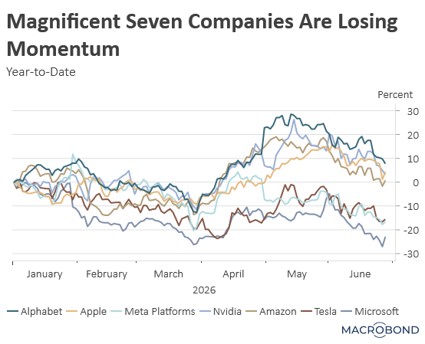

AI Trade: The S&P 500 delivered its strongest Q2 performance in six years, driven by a broadening AI rally that extended beyond technology into other sectors. This sharp uptick was fueled by easing geopolitical tensions and robust corporate earnings, which collectively bolstered market sentiment. The continued strength underscores the market’s underlying resilience amid persistent economic headwinds. However, beneath the surface of this broad-based advance, a notable compositional shift appears to be taking place.

- Hardware tech stocks were the primary drivers of the S&P 500’s rise last quarter, as firms continued to deliver strong earnings. The S&P 500 Hardware Select Industry Index surged more than 55% during the period, led largely by chipmakers. This robust performance comes as companies looking to expand their AI capacity have ramped up spending on equipment and inputs to build the infrastructure needed to meet surging demand.

- The strong performance of hardware stocks has overshadowed the underperformance of the hyperscalers that provide the revenue base for hardware companies. Despite being viewed as the heart of the AI boom, the Magnificent 7, which include five of the six major hyperscalers, are not only underperforming the S&P 500 by roughly 10% but are also trading down year-to-date. The weakness stems from heavy infrastructure spending, which has come under scrutiny due to its sheer magnitude.

- While the S&P 500’s recent gains have once again been driven by technology, the internal shift from software to hardware stocks underscores the danger of concentration risk. As noted over the last few months, tech stocks carry significant upward momentum, yet signs of fragility are increasingly evident. To mitigate this volatility and reduce overall thematic exposure, diversifying into defensive sectors like aerospace and defense can provide valuable balance to investment portfolios.

Anthropic Freed? The White House has agreed to lift its export controls on Anthropic’s AI tools. The US Department of Commerce sent a letter to the firm granting permission for foreign nationals to use its Claude Fable 5 and Mythos 5 models. The move comes after Anthropic implemented new safeguards that addressed the government’s security concerns. While removing these restrictions paves the way for the company to re-release its models globally, it leaves open the question of just how much influence Washington intends to exert over frontier AI providers.

NATO Plea: The head of NATO has sought to dissuade a potential US exit from the security alliance by appealing directly to its economic benefits. NATO Secretary-General Mark Rutte argued that $300 billion in outstanding European arms orders from the US help sustain over 195,000 American defense jobs. While it remains unclear whether this transactional argument will successfully convince Washington to stay, the massive scale of these contracts underscores that European rearmament is a long-term reality.

USMCA Talks Begin: The six‑year joint review of the USMCA begins today under the treaty’s sunset clause. The United States has signaled reluctance to commit to a 16‑year extension at this stage, raising the risk that the pact will shift into an annual review process that could stretch over the next decade and, in a downside scenario, culminate in termination or US withdrawal by 2036. Canada and Mexico have indicated that they will formally seek renewal and remain publicly optimistic that an agreement can be reached.

Daily Comment (June 30, 2026)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment begins with an analysis of the growing political backlash Russian President Vladimir Putin faces over the war in Ukraine. We then examine recent Supreme Court rulings and their implications for executive authority. Next, we briefly cover a proposal to regulate AI agents, the continued weakening of the Japanese yen against the dollar, and a Swiss vote to ease restrictions on weapons exports. As always, we include a review of recent domestic and international economic data.

Putin in Trouble: President Vladimir Putin is facing his most significant political test in nearly two decades as the war in Ukraine drags on. On Monday, Putin was forced to acknowledge the impact of Ukrainian drone strikes on Russia’s energy infrastructure, a rare public admission of vulnerability. The acknowledgment comes amid growing domestic pressure on the ruling United Russia party as the economic and fiscal costs of the war continue to mount with no clear end in sight.

- The Kremlin has increasingly sought to bind Putin’s political fortunes to those of the ruling United Russia party in an effort to sustain his appeal with the public. According to a government-aligned poll, his popularity has fallen to 69%, its lowest level since the war began in 2022. The survey was conducted shortly after Ukraine’s drone attacks on Moscow and St. Petersburg, which forced Russian citizens to confront the war more directly and underscored growing public unease about the protracted conflict.

- Putin’s rare admission comes at a time when the country is forced to deal with rationing and intermittent internet blackouts. Ukrainian drone attacks have impacted Russia’s ability to produce oil, leading to domestic price spikes. To ease the supply burden, Russia has loosened its fuel quality regulations and permitted fuel import, a practice that was virtually non-existent prior to the conflict, given the country’s history as a major energy exporter.

- The growing domestic pushback Putin faces regarding the conflict will likely make it harder for him to ignore increasing calls for a ceasefire. Historically, Putin has been reluctant to accept any deal that falls short of an outright victory, fearing that compromise could undermine his political legitimacy. Consequently, a resolution to the conflict may ultimately require a change in Russian leadership.

- While Ukraine’s leverage has grown in recent weeks due to its successful drone strikes, it is worth remembering that Russia has not yet deployed its full military capabilities. If Putin feels threatened by a potential coup, similar to the mutiny he faced earlier in the conflict, he could begin taking much greater risks. Consequently, while a ceasefire remains the most rational outcome on the table, the risk of further escalation cannot be ruled out.

Supreme Court Rules: Recent Supreme Court decisions have significantly reshaped presidential control over executive branch agencies. Most notably, the Court overturned a 90-year precedent that had restricted presidents from firing certain independent agency officials at will. Ultimately, these rulings underscore the Supreme Court’s expanding influence over executive authority.

- These rulings represent a major victory for the White House, which has consistently championed the unitary executive theory, the principle that the president should exert complete control over all agencies within the executive branch. Ultimately, the decisions are poised to significantly streamline the administration’s ability to direct federal regulators, paving the way for a more rapid rollback of key environmental, anti-trust, and financial regulations.

- While the Supreme Court backed the White House’s push for greater executive oversight elsewhere, it shielded the Federal Reserve’s traditional independence. In a 5-4 vote, the Court allowed Fed Governor Lisa Cook to retain her seat while her lawsuit over mortgage fraud allegations plays out. This critical exception honors the historical precedent of insulating the central bank’s monetary policymaking from direct presidential control.

- That said, the Supreme Court’s decision to grant a stay, thereby returning the case to the lower court, still leaves the question of the White House’s authority to remove Federal Reserve officials unanswered. The president has maintained that he still believes he has the power to reshape the Federal Reserve, suggesting that he may look to challenge the ruling further.

- The recent Supreme Court rulings will likely empower the Federal Reserve to carry out its policy agenda in the near term. However, the potential for shifts in leadership across future administrations could amplify the broader impact of these decisions. As a result, markets may face increased volatility going forward. In addition, the president’s continued push to reshape the Fed is likely to weigh on the dollar.

Growing AI Resistance: In a sign of growing momentum to regulate AI, Senator Mark Warner (D‑VA) has introduced legislation targeting AI agents. The proposal would establish new privacy safeguards and give users greater control over how their data is used and shared across platforms. Although the bill is unlikely to advance in Congress with midterms approaching, it underscores how AI governance is becoming an increasingly salient political issue that could shape the debate heading into the 2028 presidential election.

Yen Troubles: The Japanese currency has fallen to its weakest level against the dollar in nearly four decades, reflecting persistent pressure on the yen. The sharp depreciation is being driven in part by concerns over the economic fallout from the war involving Iran and Japan’s ongoing struggle to contain elevated inflation. The renewed weakness is likely to fuel speculation that the Bank of Japan could step in again to support the currency through market intervention.

European Defense: Switzerland has scheduled a vote on easing its neutrality rules to permit arms exports to select Western countries. The move underscores a broader shift across Europe toward strengthening domestic defense capabilities amid heightened security concerns tied to Russia and increasing strategic friction with the United States. If approved, the policy change would reinforce structural demand for European defense manufacturers.

Confluence of Ideas – #51 “The Mid-Year Geopolitical Outlook 2026” (Posted 6/29/26)

Daily Comment (June 29, 2026)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment begins with key takeaways from Apple’s push to ease restrictions on the purchase of Chinese semiconductors. We then turn to the US-Iran conflict, outlining our assessment of the ceasefire’s durability. Next, we briefly examine Volkswagen’s restructuring efforts, the policy agenda of the leading UK prime minister candidate, and President Putin’s recent and notable admission. As always, we conclude with a review of the latest domestic and international economic data.

Chip Shortage: The scale of the AI buildout is pushing firms to seek regulatory waivers to alleviate mounting supply constraints. Over the weekend, reports indicated that Apple is lobbying the US government for permission to source memory chips from a blacklisted Chinese supplier. The effort comes as Apple has already begun raising prices on key products in response to higher input costs, underscoring growing concerns that AI-related demand is beginning to exert upward pressure on inflation and may eventually weigh on earnings.

- Apple’s push to secure access to Chinese-made chips follows recent price increases across its MacBook and iPad lineup. The company attributed these hikes to constrained access to suitable components, ultimately passing higher input costs on to consumers. In the wake of the rare price increase, Apple’s stock recorded its second-largest single-day loss in company history.

- The iPhone maker’s push to access Chinese-made chips comes as it seeks to navigate US policy constraints amid escalating competition with China over AI dominance. While US rules do not explicitly prohibit commercial purchases from blacklisted Chinese firms, companies that engage with these entities risk losing eligibility to do business with the Department of Defense, creating a meaningful compliance and reputational tradeoff.

- Apple is not alone in passing higher costs on to consumers. Electronics manufacturers including Hewlett-Packard, Dell, Microsoft, and Nintendo have either implemented price increases or signaled upcoming ones to protect margins. Beyond consumer electronics, industries such as automotive, retail, and medical devices have also lobbied the government for relief due to mounting pricing pressure tied to ongoing chip shortages.

- The AI buildout is reinforcing inflationary pressures from both directions. On the demand side, government incentives, particularly tax credits and subsidies, are draining inventories. On the supply side, trade restrictions and tariffs are boosting competition for inputs. These distortions are beginning to filter into consumer prices; while unlikely to trigger a sharp spike, they point to more persistent inflation and could weigh on margins, raising renewed questions around current valuations.

- Apple’s push to ease restrictions on sourcing Chinese chips underscores how the US drive for supply-chain resiliency is already impacting firm profitability. While firms have successfully raised prices to protect profit margins so far, mounting consumer pushback suggests this strategy cannot be sustained indefinitely. As a result of heightened policy and economic uncertainty, we continue to advocate for a balanced portfolio approach.

Ceasefire Tightrope: Tensions between the United States and Iran remain elevated as both sides contest control over the Strait of Hormuz while simultaneously engaging in longer-term diplomatic negotiations. Over the weekend, hostilities escalated, with both sides exchanging strikes after Iran moved to require shipping vessels to seek permission before transiting the strait. Although the two parties have agreed to continue talks and pause further strikes heading into the week, the episode underscores the fragility of the current ceasefire agreement.

- The dispute appears to center on whether Iran has the authority to impose fees on vessels transiting the Strait of Hormuz. Last week, Iran targeted ships operating along the Oman coast, including vessels involved in a UN-backed effort to assist stranded shipping vessels. In response, the United States launched two-day strikes on Iranian targets, while Iran retaliated by targeting US military bases in Bahrain and Kuwait.

- Although both sides agreed to a temporary halt in military strikes, the resumption of trade flows remains limited. Under the current framework, vessels are permitted to use the UN-backed maritime corridor off the coast of Oman; however, Muscat has reportedly informed European leaders that a transit toll may be imposed. This ongoing friction over potential fees is highly likely to spark another flare-up as both Washington and Tehran attempt to assert leverage in diplomatic talks.

- Washington and Tehran appear intent on continuing talks despite ongoing tensions. Both sides have shown a willingness to use force but also to pursue a longer-term deal, and we expect intermittent tit-for-tat activity as details are negotiated. Our base case is that an agreement is ultimately reached, allowing the conflict-related risk premium in commodity prices to gradually ease, though a breakdown in negotiations would sharply increase market volatility.

VW Overhaul: The German automaker’s proposed restructuring is weighing on sentiment across Europe. The company has proposed a layoff of over 100,000 workers and closure of four plants as profits are squeezed by Chinese competition, US tariffs, and softer European demand. Drawing comparisons to GM’s 2009 overhaul, the move would significantly reshape its operations; even if not yet final, it highlights how European firms must adapt to a changing global environment.

Burnham’s Plan: The prospective UK Prime Minister Andy Burnham is set to lay out his vision for the country on Monday. In his speech, he is expected to advocate devolving more power from London to the regions and to launch a 10‑year mission aimed at lifting living standards through re-industrialization, housing, infrastructure investment, and utility reform. Although he is currently the only declared candidate for the premiership, he is widely seen as the frontrunner in the leadership contest.

Russia Feels Pain: On Sunday, Russian President Vladimir Putin announced that Russia may begin importing energy resources following sustained damage from Ukrainian drone strikes. This rare admission marks one of the first times the Kremlin has publicly acknowledged the extent of the war’s impact on domestic energy infrastructure, potentially signaling a shift in battlefield dynamics away from Moscow’s favor. Despite this development, we continue to view a ceasefire between the parties as a plausible near-term outcome.