Author: Rebekah Stovall

Asset Allocation Bi-Weekly – Stopping the Bond Vigilante: How Fiscal Dominance Is Reshaping Global Markets (September 22, 2025)

by Thomas Wash | PDF

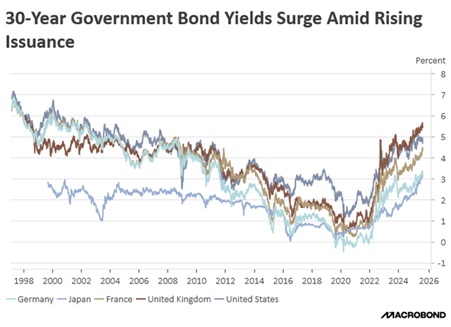

The bond bull market that began in the early 1980s lasted nearly four decades. Its longevity was largely built on the assumption that governments would always prioritize the health of their bond markets, even if it meant imposing economic pain on their own countries. This thinking fostered the legend of the “bond vigilante” — a mythical force that would supposedly punish irresponsible government spending by selling off bonds, thereby holding policymakers in check.

The bond market’s core assumption — that it would curb government overspending — has been severely tested since the pandemic. The initial, one-time surge in borrowing was necessary to prevent a global economic collapse. However, that precedent has been exploited. Many governments now use debt to finance a variety of pet projects, from infrastructure and green initiatives to energy subsidies and tax cuts. This increase in spending, detached from any corresponding increase in tax revenue or spending cuts, has been the primary driver behind the recent increase in bond yields around the world (see chart below).

A primary focus of attention is the potential for a supply/demand imbalance in the bond market. The concern is that rising bond issuance is occurring simultaneously, with a shift in investor preferences toward short-duration bonds driven by growing anxieties about inflation, economic growth, and central bank policy. As a result of this mismatch, yields on 30-year government bonds globally have risen to their highest level in over 20 years. This rise in sovereign bond yields is largely attributable to growing concerns over US credit quality, triggered by Moody’s Ratings’ decision to downgrade the US credit rating from Aaa to Aa1 on May 16. The agency justified its move by highlighting the US government’s perceived unwillingness to address deteriorating fiscal conditions, specifically citing structurally large annual deficits and escalating debt servicing costs.

These concerns were compounded by a poorly received 20-year Treasury auction on May 21, which served as an immediate test of market confidence. The auction results were weak, and yields rose above 5% for the first time since October 2023. Although not the sole driver, this weak auction amplified selling pressure across the yield curve, with the 30-year yield surpassing 5%.

Concerns about the US government’s credit quality have also raised fears about the creditworthiness of other developed countries. In the same month that the US had its weak bond auction, Japan also experienced poor demand for a 30-year bond offering. Furthermore, yields have risen across Europe and in the United Kingdom, driven by concerns that these countries may struggle to meet their own budget targets.

On the supply side, although interest rates remain elevated, governments are taking proactive measures to mitigate their impact on the broader economy. Notably, the US, Japan, and the UK have begun increasing their issuance of shorter-duration sovereign bonds. This strategy aims to reduce supply pressure on longer-dated bonds, which helps to curb the rise in long-term borrowing costs. Meanwhile, France is in a debt standoff as it looks to address its budget situation through a combination of spending cuts and tax increases.

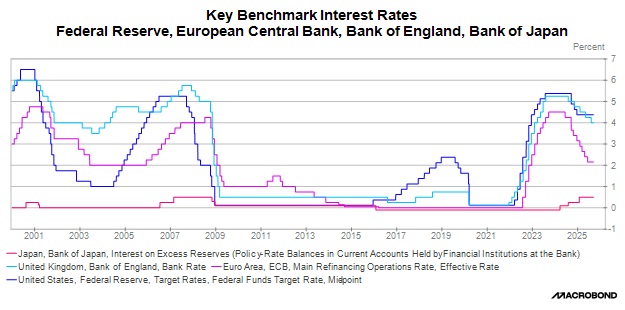

On the demand side, most central banks are actively adjusting their strategies to ensure liquidity in the bond market. The Federal Reserve, Bank of England, and Bank of Japan have all focused on modifying the pace of their balance sheet reduction to add liquidity back into the system. While the ECB has not formally stated its intention to use its tools to help bring down yields, particularly in France, it has expressed a willingness to do so through its Transmission Protection Instrument in case of a crisis.

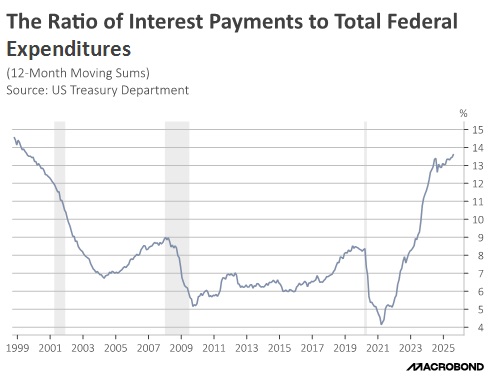

While rising government debt remains a problem, it appears that, at least in the short to medium term, governments have the ability to prevent yields from rising to very high levels. The trade-off is that governments worldwide may remain vulnerable to rollover risk when short-term bonds expire. This could force them to take more proactive measures to prevent rates from destabilizing the economy.

We believe the need to mitigate these fiscal risks could pressure governments into a regime of fiscal dominance, where monetary policy is subordinated to keep public debt servicing costs manageable. A key feature of this environment would be central banks tolerating higher inflation, effectively abandoning their strict price stability and leading to structurally elevated price pressures. In such a scenario, a barbell bond strategy — favoring both short-term and long-term bonds while avoiding the middle of the yield curve — could be advantageous in the near to medium term. Furthermore, peripheral European countries that have demonstrated a credible commitment to fiscal sustainability could become particularly attractive investment opportunities for those seeking international exposure.

Don’t miss our accompanying podcasts, available on our website and most podcast platforms: Apple | Spotify

Daily Comment (September 19, 2025)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment begins with an analysis of discrepancies in the weekly jobs data. We then examine the potential implications for US-China relations as the United States signals a desire to re-engage in the Middle East. Additional topics include a new fund for American manufacturing, the possibility of a government shutdown, and Germany’s reluctance to partner with a French defense firm. We also provide a summary of key recent global and domestic economic indicators.

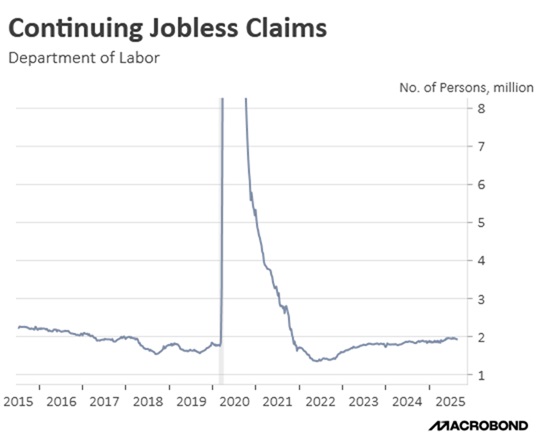

Low Hire, Low Fire? Expectations for Federal Reserve interest rate cuts rose on Thursday due to a data error that cast doubt on the labor market’s health. Although initial jobless claims fell significantly to 231,000, the reported drop in continuing claims to 1.92 million was largely an illusion. It was primarily caused by a major clerical error in North Carolina, which reported a mere 205 claims, a figure drastically lower than the 20,535 reported the previous week.

- This discrepancy in the data indicates that continuing claims may have actually experienced a slight increase from the previous week, despite the reported decline. This finding suggests that while companies are not yet accelerating layoffs, they are beginning to show hesitation in hiring, a trend that supports the narrative of a cooling labor market. Nevertheless, while continuing claims remain below the 3 million threshold often associated with a recession, the current level is nearing the peak for the expansion.

- The reporting error in continuing claims occurred shortly after a significant portion of the previous week’s spike in initial claims was attributed to an unemployment insurance fraud scheme in Texas, which is currently under investigation. It is noteworthy that this fraudulent activity did not prompt a downward revision of the prior week’s data; instead, the figure was revised upward from 263,000 to 264,000. This new error, therefore, calls the overall data quality into question.

- We continue to stress the importance of using multiple data sources to get a comprehensive view of the economy. Since the pandemic, we have seen significant data distortions that have made it difficult to pinpoint our position in the business cycle. We are concerned that the Federal Reserve’s over-reliance on this potentially flawed data may cause it to fall behind the curve. Therefore, we believe that implementing some portfolio protection may be a prudent measure at this time.

Back to Afghanistan? The US has signaled an interest in re-establishing a presence at Afghanistan’s Bagram Air Base, as indicated by a comment made by the president during a visit to the UK. While discussing plans to increase partnership, the president reportedly stated a desire to regain access to the base due to its strategic location. He specifically noted its proximity, describing it as “an hour away from where China makes its nuclear weapons,” suggesting the presence would be a form of deterrence.

- The US’s desire to position its forces near Chinese nuclear assets, coming just a day before the president’s meeting with his Chinese counterpart, Xi Jinping, suggests the two leaders will discuss more than just trade and technology. The agenda is likely to also include China’s allies, Russia and Iran, given their resistance to US efforts regarding Russia’s invasion of Ukraine and Iran’s nuclear ambitions.

- While officially maintaining a stance of neutrality, China is deepening its engagement in foreign affairs to align with US rivals. Its strategy involves capitalizing on the international isolation of Russia and Iran through discounted purchases of their energy resources. Furthermore, China is alleged to have supplied limited military assistance to both countries in the form of dual-use technology, enhancing their defensive capabilities.

- In the days leading up to the meeting with China, the White House has strongly hinted at its willingness to confront China’s foreign policy. The administration has urged allies, specifically the EU, to increase efforts to pressure China and India through sanctions, aiming to break their support for Russia’s invasion. While this strategy has not yet been effective, it demonstrates a clear desire to pressure China into changing course.

- The talks between US and Chinese leaders will likely set the tone for future relations as they try to navigate their differences. The US request to regain its former Afghan air base is likely a negotiating tactic; however, should the US follow through, it could lead to a significant escalation of tensions. While we do not believe a direct conflict is likely, the risks remain elevated.

American Manufacturing Fund: The White House is exploring how to use funds received from an investment deal that was struck with Japan. The plan is to use these funds for projects designed to support US ambitions in the chip and AI sectors. This strategy includes an expedited review process to allow for the rapid construction of factories and the development of mining operations, and it may also involve extending company leases to allow them to develop on public land.

Supreme Court Battle: The White House has requested that the Supreme Court allow it to fire Federal Reserve Governor Lisa Cook while her legal challenge to her removal is ongoing. The move is a test of the president’s authority to reshape the Federal Reserve, which has reportedly resisted his push to significantly lower interest rates. If the court rules in the White House’s favor, it would set a major precedent that could weigh on the dollar and threaten the central bank’s independence.

US Government Shutdown: Growing concerns of a government shutdown are mounting as both sides remain unable to agree on a budget. Democrats plan to hold out for restored Medicaid funding and ACA subsidies. However, Republicans have started the process of passing continuing resolutions that would fund the government through November 21. This growing partisanship raises the likelihood of a prolonged shutdown, which could temporarily impact markets and the economy until an agreement is reached.

German-French Feud: German officials are looking for alternatives to their French partner, Dassault Aviation SA, for the development of a next-generation fighter jet. This comes as Dassault has reportedly pushed for a controlling role in the program. As a result, the Germans are looking for alternative suppliers from the UK, Sweden, or even Spain. While this decision to find new partners could lead to friction between the two countries, we continue to believe that EU defense companies should benefit from the increased spending.

BOJ Policy Normalization: The Bank of Japan voted to hold rates unchanged but signaled a shift by announcing it is considering offloading a portion of its massive ETF holdings. The central bank currently holds a portfolio valued at approximately ¥70 trillion ($475 billion), with plans to sell at a pace of about ¥620 billion annually. While this will not lead to a quick unwinding of its positions, the move is likely to weigh on domestic equities and push up the value of the yen. The policy shift is another signal that the US dollar may have more room to fall.

Daily Comment (September 18, 2025)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment opens with thoughts on the Fed’s latest rate decision. We then explore why Nvidia’s investment in Intel may reflect a broader US tech policy. Additional topics include progress in easing US-China trade tensions, a new EU sanctions proposal against Russia, and further evidence of China’s advances in chipmaking. We conclude with a summary of recent global and domestic economic data.

A Fed Divided: The Federal Reserve lowered its benchmark interest rate by 25 basis points, a move that was widely anticipated by markets. While the decision itself garnered broad consensus — with even the two previous dissenters siding with the majority — the future policy path remains uncertain. The sole dissenting vote came from the newest member, Stephen Miran. Furthermore, the updated “dots plot” signaled a more dovish shift, indicating expectations for an additional rate cut. Despite this, the overall trajectory of monetary policy appears far from settled.

- The Fed’s committee is in a near-perfect stalemate, with a deep divide underscoring the challenge of balancing short-term employment concerns against the long-term goal of controlling inflation. When you exclude the most dovish member’s forecast, likely from Governor Stephen Miran, the committee is split right down the middle: nine members favor, at most, one rate cut this year, while the other nine favor two.

- Fed communication failed to offer clear guidance on the future policy path. During his press conference, Fed Chair Powell framed the rate cut as a form of risk management. However, this dovish move was contradicted by the Summary of Economic Projections (SEP), which revealed that the Fed had grown more optimistic about economic growth and less confident that inflation would return to its 2% target.

- There’s growing concern over the Fed’s independence, stemming from Stephen Miran’s role as both a White House Economic Advisor and a newly appointed Fed governor. This conflict became evident in the latest “dots plot.” The projection attributed to Miran was 75 basis points below the next lowest dot, a stark outlier that suggests he’s deeply at odds with his colleagues. This wide gap likely indicates that other Fed officials are pushing back against potential White House influence.

- Poor communication from the Federal Reserve and concerns about central bank independence fueled significant market volatility on Thursday. This was evident in the dollar’s whipsaw action — initially dropping before rising — and in the S&P 500, which spiked following the announcement only to finish lower on the day. The reaction suggests deep market skepticism about the central bank’s ability to sustain its monetary easing cycle, given the current composition of the committee.

- The latest dots plot indicates that the FOMC is projecting additional rate cuts of 25 basis points over the last two meetings. The pace of this easing, however, will be highly dependent on incoming data. We believe a sustained cooling of the labor market is a prerequisite for more aggressive rate cuts. Conversely, if inflation remains stubbornly high, the Fed may be forced to postpone any rate cuts. While we do not see it as the most likely outcome, persistent inflationary pressure could even prompt discussions of a potential rate hike.

AI Race: Nvidia has announced plans to invest $5 billion in Intel as the two companies look to co-develop chips for PCs and data centers. The deal would allow Nvidia to purchase Intel shares at a steep discount, giving it a stake in its longtime rival. The move follows major US government funding and investment from SoftBank, highlighting the growing alignment among American tech firms to strengthen domestic capabilities and ensure the US remains competitive in the global AI race.

- We believe the continued collaboration between US tech firms and the government to expand AI capacity reflects a broader strategy: shifting from offering access to America’s vast consumer market to granting access to its technological ecosystem — a transition we call moving from free trade to free tech.

- This sentiment was reinforced by White House AI adviser Sriram Krishnan, who noted that the US is using global market share as a benchmark for success. His remarks suggest not only a massive expansion of domestic AI infrastructure, but also an effort to extend US technology abroad, positioning it as the global gold standard.

- We believe US tech companies collaborating to expand their global footprint could be a key driver of equity market returns in the coming years. However, failure to secure leadership in AI may trigger a significant pullback. As a result, while we remain optimistic on the tech sector, we also see merit in maintaining exposure to value stocks to help balance portfolios.

US-China Trade Talks: China has dropped its antitrust probe into Google’s Android mobile platform, a move seen as a concession to the US as the two nations prepare for trade talks. The investigation was launched in February, the same day the White House imposed new tariffs on Chinese goods. This decision signals Beijing has learned that fostering a friendlier environment for US tech companies can lead to more favorable trade terms. It is a prime example of the growing linkage between global technology policy and trade diplomacy.

AI’s Competition: Earlier this month, two leading American AI models performed at a top-tier level against human competitors at the International Collegiate Programming Contest (ICPC) World Finals, often called the “coding Olympics.” OpenAI claimed its model would have secured first place, while DeepMind’s would have taken second. This breakthrough will likely accelerate the adoption of AI as an assistant or complement to computer programmers.

EU Sanctions: The EU is drafting a new Russia sanctions package for its members, targeting crypto, banking, and energy transactions to pressure an end to the war in Ukraine. This move comes after the US pushed the EU to enact 100% tariffs on India and China for backing Russia. Although the EU has not expressed openness to the tariff idea, it has pursued other restrictions against the Russian allies. Ultimately, while coordinated Western pressure could advance peace talks, it may also encourage Moscow to challenge NATO’s unity.

Farmer Bailout: The White House has announced a new plan to use revenue from tariffs to provide support to US farmers. This comes as the agricultural sector has seen a downturn in sales as a result of trade restrictions. The use of tariff funds for this purpose will likely lead to two key debates: first, the broader economic impact of these tariffs, and second, their long-term viability as a consistent source of government revenue to address fiscal needs, such as debt reduction.

The Chinese Nvidia? In a significant step toward technological self-reliance, Huawei Technologies has launched a new suite of semiconductors, including memory chips and AI accelerators. This announcement comes just one day after China prohibited its domestic companies from buying chips from Nvidia, highlighting a strategic push to control its supply chain. These events mark a major escalation in the US-China tech rivalry as both nations vie for dominance in the critical global semiconductor market.

Daily Comment (September 17, 2025)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment begins with what to expect from the FOMC meeting and its market implications. We then examine China’s ban on NVIDIA chips and its potential ripple effects across the global tech sector. Further topics include progress in US-UK trade talks, the evolving situation around a potential TikTok sale, and how Chinese trade restrictions are pressuring EU firms and even forcing some to consider shutdowns. We also include a summary of key recent economic data from both global and domestic sources.

Fed Primer: All eyes are on the imminent FOMC meeting minutes as investors seek to gauge the trajectory of interest rates and the Fed’s assessment of the economy. The market has overwhelmingly priced in a 25 basis point cut, with futures implying a 96% probability. However, mounting evidence of a softening labor market, coupled with lingering concerns over the economic outlook, suggests the central bank may ultimately decide on a more assertive path of rate cuts.

- Federal Reserve officials face a complex economic puzzle. While the labor market is showing clear signs of weakening — with firms slowing hiring due to tariff costs and AI adoption — consumer spending remains remarkably resilient as evidenced by strong retail sales data. This divergence between a softening jobs market and robust consumption is a major challenge for policymakers interpreting the economic environment.

- The confirmation of Stephen Miran, a White House advisor, to the Federal Reserve Board marks a pivotal shift. It breaks a nearly century-old precedent, making him the first sitting White House official on the board since the 1930s. This move is viewed as a notable assertion of executive influence over monetary policy and is expected to shape the Fed’s future decisions.

- Analysts will scrutinize the Fed’s “dots plot” for signs of the White House’s influence on interest rate projections. As the newest governor, Stephen Miran is expected to submit the most dovish dot, aligning with the administration’s previous statements. Furthermore, he will likely advocate for a policy focus that extends beyond the dual mandate of maximum employment and price stability, emphasizing a de facto “third mandate” of managing long-term interest rates.

- We anticipate the Fed meeting will serve as a significant catalyst for markets. In our base case, indications of an aggressive path for rate cuts would be interpreted as a substantial stimulus measure, providing a tailwind for equity assets. A key risk to this view is that the market’s positive reaction may be muted if the cuts are seen as politically influenced.

China Halts Sales: Beijing has ordered its companies to halt purchases of NVIDIA’s AI chips and cancel existing orders, significantly reducing reliance on foreign semiconductor technology. This directive follows recent accusations against the US chipmaker for violating anti-trust laws and comes just a month after regulators flagged its H20 chip as a national security risk. The company’s share fell pre-market following the report.

- China’s crackdown on NVIDIA chip purchases accelerates its push for semiconductor self-sufficiency, a key front in its rivalry with the US to develop superior AI technology. With domestic technology improving, Beijing is now urging firms to source more AI chips from local suppliers.

- Huawei is reportedly developing chips that rival those of NVIDIA in performance, signaling a major advancement in China’s semiconductor capabilities. This progress is complemented by breakthroughs in producing domestic chipmaking equipment comparable to that of leading US suppliers.

- China’s crackdown on US tech is a major market concern, particularly for growth companies in the S&P 500. These firms often rely heavily on foreign revenue, making them vulnerable to such restrictions. The impact is twofold: immediate earnings are threatened, and future growth is jeopardized by the loss of access to the critical Chinese market.

- While we maintain a positive outlook on the tech sector’s momentum, bolstered by supportive tax incentives for capital expenditure, we do believe a strategic allocation to value stocks offers crucial diversification and resilience during periods of market uncertainty.

US-UK Talks: The US and UK will hold talks to discuss trade and investment, with US companies expected to announce billions in new technology infrastructure investments in the UK. This initiative aims to deepen the bilateral relationship and promote the adoption of US technology. As outlined in our latest geopolitical report, we suspect that the US is moving away from a traditional free trade policy toward a “free technology” policy, using tech access rather than consumer market access to cement alliances and keep partners aligned.

US Investments: The US is in talks to establish a fund, in partnership with investment firm Orion Resource Partners, to finance overseas mining projects. This initiative would target the extraction of critical minerals like copper and rare earths, which are essential for technology manufacturing. The move exemplifies the US government’s growing collaboration with the private sector to play a more active role in the economy.

TikTok Sale: The president signed a new order extending the deadline for Chinese companies to divest from the US, despite signs of progress in negotiations. Under a White House-brokered deal, TikTok would be acquired by a consortium including Oracle Corp., Andreessen Horowitz, and the private equity firm Silver Lake Management LLC. While it remains unclear whether Beijing will approve the deal, early indications suggest that China wants the app to keep its Chinese algorithm.

USMCA Talks: The US is set to hold trade discussions with its North American partners as they prepare for a review of the regional USMCA trade agreement next year. We suspect the conversations will primarily focus on ensuring the countries agree to create a united trade policy, particularly toward China, but possibly regarding other nations as well. Given how much trade is conducted between the three countries, any sign of trouble or disagreement could lead to renewed concerns of trade uncertainty.

China’s EU Crackdown: European firms face potential shutdowns due to a shortage of critical rare earth elements that are essential for production. This crisis follows China’s decision to restrict exports of these vital resources, a move triggered by global trade tensions and US tariffs. Although China and the EU reached an agreement to maintain Europe’s access, numerous member states have complained that significant supply issues persist. We believe this ongoing resource scarcity threatens to negatively impact market sentiment toward the global tech sector.

Daily Comment (September 16, 2025)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment today opens with news of a US-China deal that would allow Chinese social media app TikTok to keep operating in the US, although virtually no details have been released. We next review several other international and US developments with the potential to affect the financial markets today, including a report on weak production growth in the world’s oil and gas fields and a preview of this week’s Federal Reserve policy meeting.

United States-China: According to a social media post by President Trump last night, US and Chinese negotiators in Spain have reached a “framework” deal on US ownership and operating rights of Chinese social media firm TikTok. Although few details are available, it appears the basic deal will allow TikTok to keep operating in the US in return for concessions. Those concessions probably include selling the US operations of TikTok to a domestic company. If so, the US buyer could gain a lucrative social media asset with a huge usage base.

US Monetary Policy: The Fed today begins its latest policy-setting meeting, with its decision due tomorrow at 2:00 pm ET. Based on interest rate futures trading, investors are nearly unanimous in expecting the central bank to cut its benchmark fed funds interest rate by 25 basis points to a range of 4.00% to 4.25%. Investors also expect at least one more rate cut by the end of the year. The prospect of falling interest rates continues to buoy US stock prices despite clear signs that economic activity is slowing.

- Separately, a federal appeals court last night rejected an emergency Trump administration request to remove Fed Governor Lisa Cook ahead of the policy meeting. Despite allegations of mortgage fraud by Federal Housing Finance Agency Director Pulte, documents seen and reported by major media sources indicate Cook correctly listed her properties as owner-occupied or vacation-oriented. If Cook remains on the policymaking board, she seems likely to vote against an interest rate cut at this time.

- In another development yesterday, the US Senate voted to confirm White House economic advisor Stephen Miran to fill the current vacant seat on the Fed’s board of directors. Miran should therefore be able to participate in this week’s policy meeting, at which we suspect he will vote to cut interest rates as President Trump desires.

European Union: A year after publishing his influential report laying out the causes of Europe’s faltering economic competitiveness and offering recommendations, former European Central Bank Governor Mario Draghi today warned that slow adoption of the plan has led to further deterioration in the region’s ability to compete. Despite the warning, however, hurdles such as political resistance and high debt seem likely to limit long-term progress, even if new fiscal stimulus and higher defense spending spur faster growth and stronger markets in the near term.

Russia-Poland: In an interview, Poland’s deputy minister for digital affairs said Russian operatives are currently launching 20 to 50 cyberattacks against critical infrastructure every day. Most of the attacks have been thwarted, but a few have temporarily closed down facilities, including hospitals. The minister said the attacks have forced Warsaw to hike its cybersecurity budget to €1 billion this year from €600 million in 2024. The news is a reminder that Europe’s current defense spending hikes include opportunities for cybersecurity firms.

United States-Mexico: In a little-noticed report last week, Reuters revealed that the Central Intelligence Agency has been more deeply involved in helping Mexico’s security services than previously known. For example, the report said the CIA has leveraged its eavesdropping assets to help locate drug cartel members, while its analysts have helped develop target lists. Mexico has even relied on CIA polygraphs to vet members of its security services. The news suggests the US has more leverage than previously known in its trade negotiations with Mexico.

United States-Venezuela: President Trump yesterday said the US military has destroyed a second boat operated by Venezuela drug cartels in the Caribbean Sea. The administration provided no further details. Nevertheless, the incident illustrates the US’s strong new military focus on regional operations, including drug interdiction in the Caribbean. The new approach continues to raise concerns among Latin American countries about US interference in their internal affairs.

Global Energy Market: The International Energy Agency today said production is declining faster than expected at oil and gas fields across the globe. According to the IEA, the fall in output largely reflects today’s greater reliance on shale resources, where production declines relatively quickly unless there is ongoing capital investment. The report says that since 2019, roughly 90% of global oil and gas investment, or $500 billion, was just to keep production steady. The report says the market has therefore become more precarious and at risk of price spikes.

Global Aluminum Market: According to the Financial Times, global aluminum prices have now risen 17% since their recent low in April, while regional prices within the US have jumped even more dramatically. The report says prices have climbed in response to factors such as a clampdown on production in China, limited smelting capacity elsewhere, the new US import tariffs, and rising demand for the product. Naturally, the jump in prices holds out the prospect of strong stock performance by aluminum producers.

Daily Comment (September 15, 2025)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment today opens with key news on the US-China and US-Russia relationships that could affect US technology companies and global energy supplies. We next review several other international and US developments with the potential to affect the financial markets today, including a further slowdown in Chinese economic growth and signs that the European Central Bank is close to ending its campaign of interest rate cuts.

United States-China: In a report on the first day of its pre-orders for the new Series 17 iPhone on Saturday, technology giant Apple said Chinese pre-orders were even stronger than for the Series 16 last year, even though its ultra-thin model is still unavailable because of regulatory issues. The strong Chinese orders came despite the worsening of US-Chinese geopolitical and economic tensions. They therefore highlight how top US brands retain significant loyalty in China, which may limit Beijing’s ability to target them as part of the US-China rivalry.

- On the other hand, Beijing today said US artificial intelligence giant Nvidia was found to have violated Chinese antitrust law. The announcement didn’t lay out any punishment for Nvidia, but it did say the company would be subject to further probes, which will likely weigh on the firm’s stock price. In pre-market trading, Nvidia’s stock was down 1.4%.

- Separately, Beijing on Saturday announced that it has opened an anti-dumping probe into US analog computer chips and initiated an anti-discrimination investigation over Washington’s handling of Chinese chips.

- The Chinese probes could well lead to tariffs or other trade barriers against US chips, so they could serve as a threat ahead of the new round of US-China trade talks in Spain this week. If such tariffs or trade barriers are eventually implemented, US chip firms could lose access to the large, important Chinese market, especially if they don’t enjoy strong brand loyalty like Apple does. That could lead to further bifurcation of the global tech industry and hurt the profits and value of US chip firms.

United States-Russia: Politico over the weekend said Sen. Lindsey Graham (R-SC) and Rep. Brian Fitzpatrick (R-PA) will try to attach their bill imposing major economic sanctions against Russia to the upcoming legislation to keep the US government funded. Senate Majority Leader Thune is reportedly supportive of the idea, and it seems consistent with President Trump’s pledge this weekend to level “major sanctions on Russia” when NATO countries stop buying Russian oil and levy tariffs on China.

- The effort by Graham and Fitzpatrick probably raises the possibility of major new US sanctions against Russia.

- The result could be new geopolitical tensions between the US and NATO versus China and Russia and possible disruptions in global energy markets. However, the moves may not be enough to convince Russia to stop its war against Ukraine.

US Monetary Policy: Mortgage-related documents seen by media sources appear to show that Fed board member Lisa Cook properly listed her Atlanta condominium as a vacation property, contradicting allegations of mortgage fraud by Federal Housing Finance Agency Director Bill Pulte. Those allegations, apparently based on other documents, were the basis for President Trump’s effort to fire Cook. The effort to fire Cook is now mired in judicial proceedings, but the new documentary evidence suggests she may have a fighting chance to stay in her position.

US Stock Market: President Trump this morning threw his support behind the idea of allowing companies listed in the US to issue their earnings reports every six months, rather than quarterly. In a social media post, Trump wrote that, “This will save money, and allow managers to focus on properly running their companies.” Such a change would require action by the Securities and Exchange Commission, which has required quarterly reporting since 1970.

Eurozone: In an interview with the Financial Times, Martin Kocher, the newly appointed governor of Austria’s central bank, said the European Central Bank’s monetary easing has now essentially ended, leaving the benchmark interest rate at 2.00% or slightly lower for the time being. If Kocher is right, the differential between US and eurozone interest rates could finally begin to narrow as the Fed re-starts its rate-cutting campaign this week.

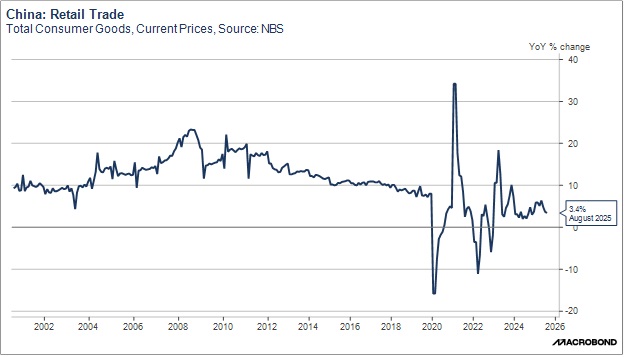

China: As a reminder that the US-China tensions are occurring against a backdrop of slowing economic growth, Beijing today said August retail sales were up just 3.4% from the same month one year earlier. That was much weaker than expected and significantly slower than the increase of 3.7% in the year to July. Other data showed slowing growth in fixed investment and industrial production as well, at least in part reflecting the government’s effort to rein in excess capacity and untenable price competition.

Russia-Romania: Bucharest over the weekend said one Russian drone had entered and exited Romanian airspace, marking the second time Russian drones have violated NATO territorial skies in the last week. The Romanian air force monitored the drone but didn’t take it down. The incidents suggest Russia is taunting NATO, testing its defenses, and gauging its willingness to respond to Russian aggression. The incidents point to a growing risk that the Kremlin will go too far and spark a kinetic conflict with NATO that would likely be negative for global financial markets.

Turkey: A judge today postponed a decision on ousting Özgür Özel as chair of the opposition Republican People’s Party over allegations of vote-rigging at a 2023 party congress. Since the effort to force out Özel has been seen as a ploy by President Erdogan to weaken the opposition and stay in power beyond the end of his current term in 2028, the postponement has raised hopes that the judiciary is pushing back against Erdogan’s authoritarian approach to governance. Turkish stock prices have therefore jumped about 4.5% today.

Global Critical Minerals Supply: New reporting by the Financial Times shows that global supplies of germanium, which is critical for high-technology military products such as thermal imaging systems, have practically dried up in response to a recent export ban by China. Although the US convinced China to quickly reverse a separate clampdown on rare earths earlier this year, it appears the restrictions on germanium and related minerals remain in place, driving global prices higher and threatening to disrupt high-tech manufacturing around the world.

Daily Comment (August 19, 2025)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment today opens with a recap of yesterday’s White House summit between President Trump, Ukrainian President Zelensky, and top European leaders. We next review several other international and US developments with the potential to affect the financial markets today, including US success in forcing the UK to backtrack on a proposed new regulation against Apple and a reiteration of the US sovereign debt rating by S&P.

United States-Ukraine-Europe: In yesterday’s summit between President Trump, Ukrainian President Zelensky, and top European leaders, it appears that Trump offered to have the US act as a backstop to any direct security guarantees given by the European countries to Ukraine to help stop Russia’s invasion of the country. Trump also said he is trying to arrange a bilateral summit between Zelensky and Russian President Putin, to be followed by a trilateral summit including Trump himself.

- It isn’t clear how the US’s backstop security guarantee might look. Nevertheless, as we noted in our Comment yesterday, the offer from Trump marks a notable evolution in his foreign-policy understanding and adjustment. Implementing such a backstop guarantee would tilt Trump’s foreign policy back toward the US’s traditional global engagement, despite his apparent shift toward Putin’s position in other war issues, such as the need for land swaps.

- According to the Financial Times last night, the Ukrainian government has offered to buy $100 billion of US weapons, financed by European countries, to help secure the US security guarantees. Kyiv has also offered to provide the US with $50 billion in military drones, leveraging the expertise it has gained in the new technology in the heat of war.

- Of course, Trump will likely face some pushback against the idea of any US security guarantees from the more isolationist wing of his political base.

United States-United Kingdom: Under pressure from the Trump administration, the UK has reportedly agreed to rescind its January directive requiring US tech giant Apple to provide a “back door” to encrypted customer data for investigatory purposes. The incident is the latest example of the administration’s strong focus on protecting US digital services firms from burdensome taxation and regulation in foreign markets — a stance that likely will help maintain the US firms’ global market dominance going forward.

United States-Brazil: Finance Minister Haddad yesterday said Washington and Brasilia have reached an impasse over the US’s new 50% tariff against Brazil, given that the constitution bars the government from trying to force the supreme court to end its prosecution of former right-wing President Bolsonaro, as the US demands. If Haddad’s statement is true, it would suggest that Brazil could continue to face debilitating US tariffs for an extended period, likely weighing on the economy and Brazilian asset prices.

Canada: The Canadian Union of Public Employees this morning said it has struck a tentative labor deal with Air Canada, ending the strike against the airline by 10,000 of its flight attendants. As we mentioned in our Comment yesterday, the strike had threatened to disrupt air travel and freight shipments across North America and beyond. Reports indicate the flight attendants’ main gripe against Air Canada was low wages, but it isn’t clear how their compensation would be adjusted under the new labor contract.

US Fiscal Policy: S&P Global Ratings today said it is keeping its US sovereign credit rating on hold at AA+/A-1+, midway between its second- and third-highest ratings, reflecting recent resilience of the US economy and “credible, effective” monetary policy. Importantly, S&P said it expects the US administration’s new tariff revenues to largely offset the tax cuts and spending hikes in this summer’s “big, beautiful” budget bill. The steady rating will help maintain demand for US Treasury obligations and help keep bond yields in their recent trading range.

US Labor Market: Fresh analysis shows new entrants to the labor force (mostly high school and college graduates with no prior work experience) now make up 13.4% of all unemployed workers, the highest rate since 1988. The jump in the new entrants’ share of jobless workers largely reflects the difficulty that Generation Z is having in finding work, as factors such as policy change and artificial intelligence make businesses reluctant to hire. High unemployment among the young is likely one reason for weak buying among lower-income consumers.

US Pharmaceutical Market: Danish drug giant Novo Nordisk yesterday said it will halve the US price of its Ozempic weight-loss drug for people who can’t buy it with health insurance. The firm also said it will offer the drug for home delivery. The moves likely aim to stave off tough US tariffs and/or other trade barriers that President Trump has threatened as punishment for high imported drug costs. In response, Novo Nordisk’s US-listed share price jumped 3.7% yesterday, ending at a three-week high of $53.75.

US Semiconductor Industry: Semiconductor giant Intel late yesterday said it will sell a 2% stake in the company to Japanese technology investor SoftBank for $2 billion. Intel will sell new common stock to SoftBank at $23.00 per share, a slight discount to yesterday’s closing price of $23.66. The deal represents a vote of confidence in Intel as the Trump administration also mulls having the federal government buy a 10% stake in the struggling firm to bolster its domestic chip manufacturing. Indeed, SoftBank and the administration may have coordinated on the deal.

- In response, Intel share prices are up some 5.1% so far today, despite the risk that government ownership could eventually lead to political interference in company management.

- More broadly, the positive market response to the SoftBank deal and the potential federal stake highlight how investors have become comfortable with increasingly aggressive industrial policies, from subsidies under President Biden to outright government ownership under President Trump. One key question is whether investors will eventually get skittish about such policies and sell the associated stocks.

Daily Comment (August 18, 2025)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment today opens with a few words on the Trump-Putin summit in Alaska late Friday. We next review several other international and US developments with the potential to affect the financial markets today, including a new intra-day record high for Japanese stock prices and a short preview of the Federal Reserve’s annual symposium in Jackson Hole, Wyoming, which starts later this week.

United States-Russia-Ukraine: President Trump today will meet Ukrainian President Zelensky and top European leaders at the White House to hash out next steps to end Russia’s war against Ukraine, after Friday’s summit between Trump and Russian President Putin yielded meager results. Reports over the weekend suggested the main goal of the White House meeting will be to flesh out the US security guarantees for Ukraine that Trump seems to have embraced of late. The leaders are also expected to discuss possible land swaps as the basis for a peace deal.

- All presidents and their administrations continually learn as they conduct US foreign policy, even in their second term. Recent months have highlighted President Trump’s evolving awareness of the relative power and goals of China and Russia, the world’s other two “Great Powers.”

- Although Trump and his administration had rightly focused on China’s dependence on exports to the US as a source of leverage, the US-China trade war in recent months has shown that China also has an important source of leverage in its near-monopoly over critical mineral supplies. Putin’s intransigence in prosecuting his war against Ukraine has brought into high relief his maximalist geopolitical goals and duplicity.

- As US officials come to terms with these learnings about the other Great Powers and their relative leverage versus the US, it is possible they will partially back off their populist, isolationist inclinations. If Trump really has swung behind US security guarantees for Ukraine, we would have strong evidence of such a shift, even though his abandonment of a ceasefire goal and embrace of land swaps may look like he has embraced Putin’s perspective on the war.

- Any such shift back toward a more traditional US foreign policy focused on support for allies would likely help ensure the survival of the US geopolitical and economic bloc, which we have argued is an attractive investment space for US investors. However, such a shift would also likely generate plenty of pushback from much of the administration’s political base.

United States-European Union: A planned joint US-EU statement fleshing out the terms of the two sides’ July 27 trade deal continues to be delayed by disagreements over reforms to the EU’s Digital Services Act, which US officials claim is an unfair hinderance of US tech companies. The joint statement was originally expected to be issued within days of that trade deal.

Japan: The Nikkei 225 stock price index today reached its third all-time high in the last five trading days, illustrating how factors such as market momentum, a renewed weakening of the yen, decent economic growth, and optimism over the war in Ukraine have been boosting Japanese stock values.

China: As Chinese economic officials seek new resources to fund fiscal stimulus measures, they are reportedly starting to crack down on domestic investors’ foreign investment income. Chinese residents investing onshore are currently exempt from tax. However, foreign investment income is subject to a 20% tax, and many individuals fail to report their gains. A new crackdown could theoretically limit Chinese demand for a range of investments around the world, hurting returns.

Bolivia: In the first round of the presidential election yesterday, centrist Senator Rodrigo Paz came in first with about 32% of the vote, and conservative former President Jorge Quiroga came in second with 27%. Paz and Quiroga will now compete in the October run-off, ensuring that Bolivia will once again be led by a pro-US, market-friendly president after 20 years of almost uninterrupted rule by the leftist Movement Toward Socialism party. The prospect of better economic policies has given a further boost to Bolivian bond values and other assets.

Canada: The Canadian Union of Public Employees, which represents 10,000 of Air Canada’s flight attendants, launched a strike against the airline over the weekend, ignoring a government order for binding arbitration and grounding hundreds of flights. The main issue for the union is compensation. Since Air Canada is tightly integrated with the Star Alliance (which also includes United Airlines, Lufthansa, Turkish Airlines, and Singapore Airlines), the strike threatens to disrupt air travel and freight shipments across North America and beyond.

US Monetary Policy: The Fed’s annual symposium in Jackson Hole, Wyoming, starts this Thursday, with the official theme of “Labor Markets in Transition: Demographics, Productivity, and Macroeconomic Policy.” Chair Powell will give his keynote speech on Friday, and investors will be looking for confirmation that the central bank will cut its benchmark fed funds interest rate in September as expected. Investors will also be hoping that Powell will provide guidance on future rate cuts through the end of the year.

US Corporate Bond Market: Little noticed amid the recent rally in stock prices, surging prices for company bonds have driven the corporate yield spread over 10-year Treasurys to a 27-year low of just 0.75%. The ultra-low credit spread appears to reflect investors’ continued strong optimism about the US economy, even as they also expect slowing economic growth and cooler inflation to allow the Fed to cut interest rates multiple times before the end of the year.