by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment today opens with an update on the war in the Middle East. We next review several other international and US developments with the potential to affect the financial markets today, including a move by France to extend its nuclear weapons umbrella across Europe and reports that Kevin Warsh, the nominee to be the next chair of the Federal Reserve, does not intend to cut the central bank’s balance sheet as sharply as some have feared.

United States-Israel-Iran: The war against Iran not only continues today but shows signs of widening into a broader regional conflict that could increasingly impair the production and shipment of energy supplies. Iran continues to lash out at countries all over the Middle East, including a drone attack on the US Embassy in Saudi Arabia and missile attacks on key airports. We have also seen reports of rioting in Bahrain, raising the specter that Iran has pre-positioned civil unrest squads across the region.

- In support of Iran, Hezbollah militants in Lebanon launched attacks on Israel, prompting the Israeli military to stage attacks across that country and send troops over the border.

- Meanwhile, the US and its allies are becoming increasingly concerned that Iran’s unexpectedly large inventory of available missiles and drones could lead them to deplete their inventories of air-defense missiles.

- President Trump has tried to dismiss those concerns explicitly, saying the US has a “virtually unlimited supply” of most weapons, while acknowledging that the country is “not where we want to be” on the highest-end weapons. Nevertheless, the threat of a shortage illustrates how the US and its allies have failed to field Ukraine-style anti-drone units armed with less expensive but still relatively effective defenses against drones.

- In any case, the rapid depletion of US and allied air-defense assets likely increases the risk that other adversaries will take advantage of the situation. For example, it could tempt China to make a grab for Taiwan, while Russia could conceivably be tempted to stage attacks in Eastern Europe.

- As the conflict continues to expand, investors are becoming more concerned about the global economic impact. Energy prices continue to rise, with Brent crude oil today up another 7.5% to $83.53 per barrel. Natural gas prices are also surging. In contrast, gold and silver prices have pulled back a bit, perhaps reflecting both profit taking and concerns about an economic slowdown sparked by high energy prices. Indeed, stock index futures and copper prices are also down sharply so far this morning.

US Politics: President Trump has offered a range of justifications for launching the war against Iran now, angering the Republican Party’s influential “America First” wing, but the concerns were amplified yesterday by Secretary of State Rubio’s assertion that the US had to act because Israel was going to attack. The statement was interpreted by some as subordinating US interests to those of Israel. The growing controversy among Republicans could increase the odds of the Democrats taking control of the House in the November midterm elections.

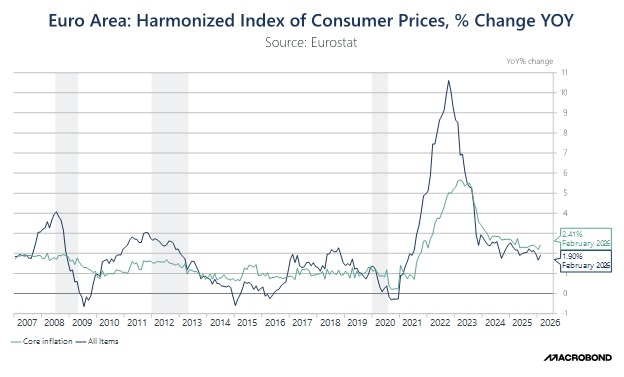

Eurozone: In an initial estimate, the February consumer price index was up 1.9% from the same month one year earlier, above expectations and up from 1.7% in the year to January. Excluding the volatile food and energy components, February core CPI was up 2.4% on the year, up from 2.2% in the year to January. The accelerating price hikes were driven in part by an uptick in energy prices as investors looked to the possibility of war against Iran. Now that the war has begun, price inflation in Europe is expected to accelerate further.

- Separately, the European Central Bank’s chief economist warned in an interview yesterday that a prolonged war in the Middle East and a persistent fall in oil and gas supplies from the region could cause a “substantial spike” in inflation and a “sharp drop in output” in the Eurozone.

- That would compound the economic challenges already faced by Europe since the Russian invasion of Ukraine disrupted its energy supplies starting in 2022.

France: President Macron yesterday said France is working on a plan under which it will boost its arsenal of nuclear weapons and forward-deploy them among eight other European nations including the UK, Belgium, the Netherlands, Sweden, Denmark, Germany, Poland, and Greece. The goal of the program would be to offer Europe a comprehensive nuclear deterrence with increased survivability in time of war. The announcement is consistent with our oft-stated belief that current geopolitical changes could well spark a new, global nuclear arms race.

- Importantly, if France becomes the linchpin for Europe’s nuclear deterrence, it would greatly increase the country’s influence over the rest of the Continent. At some point, that would likely become intolerable to Germany, given its centuries-old rivalry with France. Germany and other European countries, such as Poland, might then seek to develop their own independent nuclear forces.

- While the future prospects for uranium prices are rosy because of Chinese and Indian plans for more nuclear electricity in the coming years, we have long maintained that the added demand for nuclear weapons around the world will also tend to push up prices for the metal.

US Monetary Policy: According to the Financial Times, acquaintances of Kevin Warsh say the nominee to be the next Fed chair would reduce the central bank’s balance sheet over time, avoiding sudden moves that could destabilize the financial markets. The sources also said Warsh would only seek to shrink the balance sheet after extensive talks on its potential effects with banks and the broader public. If accurate, the report suggests that Warsh got the nomination by promising President Trump that he won’t tighten monetary policy too quickly.

US Private Credit Industry: The Financial Times reports that Blackstone’s $82 billion private credit fund, Bcred, suffered net outflows of $1.7 billion in the first quarter, equal to 7.9% of its assets. Coming shortly after Blue Owl halted redemptions from its private fund focused on the same asset class, the news illustrates how investors have become increasingly worried about “cockroaches” in exotic private debt and asset-backed lending markets. That will likely help tighten financial conditions, increasing the risk of an economic or financial market downturn.