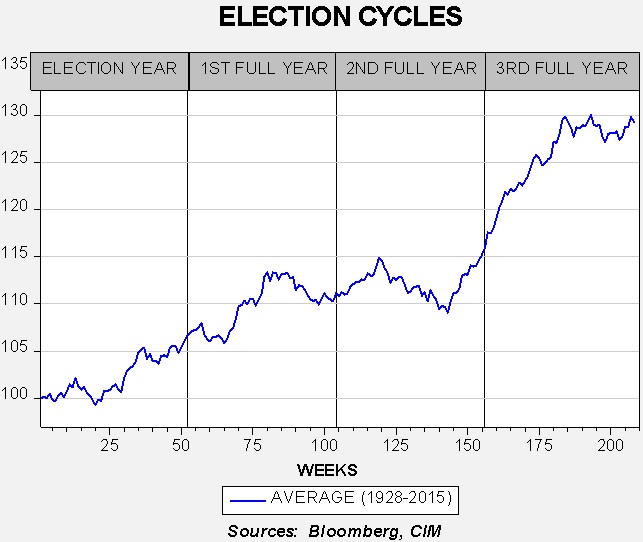

Traditionally, the election season kicks off with Labor Day so, with last Monday’s holiday, the election cycle is upon us. The midterm election year tends to be lackluster for equities until Q4, when a strong rally usually develops.

The data for this chart is developed by taking the weekly closes for the S&P 500, beginning with the first Friday close in 1928. We index the data over the next four years and then average each week across each four-year cycle. Thus, this graph represents 22 cycles. The election occurs around week 48 in the election year. On average, the euphoria surrounding the election lasts until week 80 (into the summer of the year after the election) when equities become range-bound. Some of this pattern is probably due to the inevitable disappointment that a new administration can’t implement all the changes it promised. By the midterm year (third full year), equities test the low end of the range into October then begin a multi-month rally that persists into the middle of the year after the midterms. Another range-bound pattern develops into the election year.

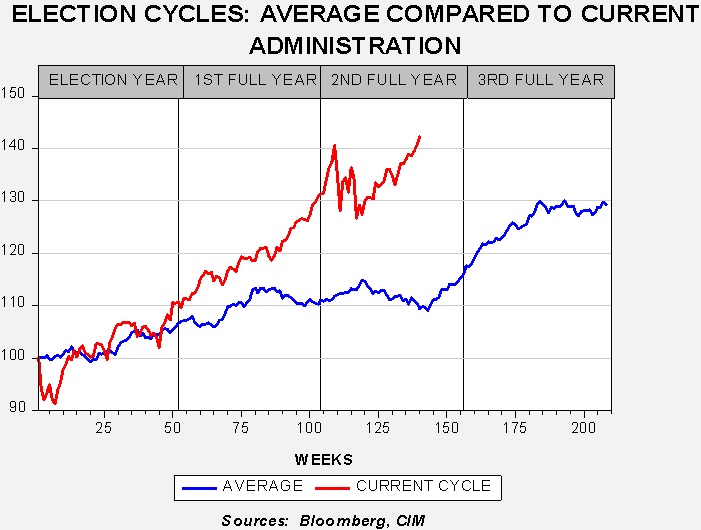

The following chart shows how the current administration compares to the average.

Clearly, the Trump administration has been popular with investors, especially during the first full year after the election. The tax cuts boosted equity prices into Q1 of this year. However, concerns about trade, tightening monetary policy and worries about the midterms have all likely conspired to bring a period of consolidation. Equities have improved recently, making new highs. The range-bound pattern that has emerged this year is consistent with the average election cycle pattern, albeit from a higher level.

The key question is whether we will see the typical midterm rally in Q4 through next summer. As we discussed last week, although there are worries about political turmoil in the wake of a potential change in power in Congress, the political situation, by itself, probably won’t derail the bull market. The primary threat to the bull market is recession and the most likely culprit would be overly tight monetary policy. Given the current pattern of tightening, we don’t expect that to be a problem until H2 2019. Thus, the pattern will probably hold but, given the recent strength in equities, we would not necessarily expect the usual 20% rise seen after the midterms. However, a more pedestrian rally of 5% to 10% would not be a surprise. To conclude, we do expect a post-midterm rally, perhaps less vigorous than average but a stronger equity market nonetheless.

[Posted: 9:30 AM EDT] It’s employment Friday. We cover the data in detail below, but the quick take is that labor markets are tightening. Although the unemployment rate rose, both the labor force and underemployment fell. August can have seasonal adjustment issues (it can be difficult to capture school/employment flows) and thus we will likely see revisions. The financial markets are taking the data as evidence of overheating, likely due to the faster than expected rise in wages. Interest rates are higher, the dollar is stronger and equity values have declined. Here are the other items we are watching today:

Brexit optimism: Comments suggesting some degree of thaw between the EU and the U.K. sent the GBP higher this morning. EU negotiators indicated that a modified border in Northern Ireland could be workable. Earlier in the week, Chancellor Merkel called for compromise and relaxing the border issue would be an important step in that direction. If there were a hard Brexit with no deal, border checks on the Ireland/Northern Ireland frontier would return and potentially increase tensions between Protestants and Catholics that have rocked the region for decades.

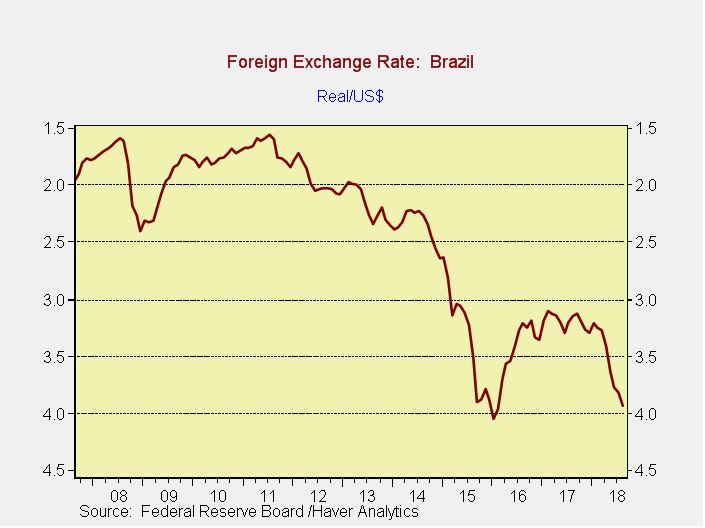

Brazilian elections: Brazil will hold its first round of presidential elections on October 7. On October 28, there will be a run-off to determine a majority for president. This election season has been quite unusual. For example, the leading candidate, former president Lula da Silva, cannot run…because he is incarcerated. Polls suggest he would capture around 35% of the first round’s vote. His replacement, Fernando Haddad, is only polling at around 6%. And, he has come under investigation on corruption charges.[1] In another twist, the current official front-runner, Jair Bolsonaro, a hard-right-wing candidate, was stabbed at a campaign rally yesterday.[2] Initial reports suggested that Bolsonaro, currently polling at around 22%, was not seriously injured. However, these reports turned out to be inaccurate. According to his family,[3] Bolsonaro was in critical condition and is now listed as “stable” but in serious condition[4] after treatment.[5] The Brazilian real has been under pressure recently, in part due to the disarray surrounding the upcoming election.

Trade: It doesn’t look like we will get a NAFTA deal before the weekend but talks continue. Optimism remains that the U.S., the EU, Canada and Japan will reconcile differences. However, there is no sign of peace with China. We are past the deadline for implementing another round of tariffs with China, this tranche reportedly on $200 bn of imports with a 25% rate. We do expect an announcement at any time, although no timetable is in place. Once announced, we expect China to retaliate in kind. We may be seeing an evolving trade policy that is designed to focus on China. Reports from China suggest that is Beijing’s take.

Social media under the gun: High-ranking executives from some of the most prominent social media firms have been testifying in the Senate over competition and free speech issues. Now, the DoJ is considering an investigation into the free speech and competition issues with these companies. Public scrutiny has been building against these tech giants for some time.[6] However, the momentum against them does appear to be increasing.

Threats to U.S. troops in Syria? Russia has warned U.S. military officials that Russian forces, combined with Syrian troops, are preparing an attack in an area where U.S. military personnel are in place.[7] The region of concern is in southeastern Syria in an area called At Tanf. This is one of the two remaining strongholds of rebel troops in Syria, the other being Idlib (which will be the topic of next week’s WGR). Although we doubt Russian troops would directly attack American soldiers, it could create a major international crisis if they do.

Swedish elections:[8] The Swedes go to the polls on Sunday in what has been a very divisive election season. For most of the postwar era, Sweden has been dominated by a center-left coalition led by the Social Democrats. This party and its coalition partners are currently polling at 40.2%. Center-right parties, the traditional opposition, are polling at 37.7%. The major change has come from the Sweden Democrats, a populist, anti-immigration party, which is polling at 19% and was seeing support above 22% just a couple of weeks ago. The key issue appears to be immigration, which has been a critical issue in the West in recent years. Neither the center-right nor center-left has indicated it would allow the Sweden Democrats to join in a coalition but a strong showing by this populist party will make it difficult to put a majority coalition in place. If polls are accurate, Sweden will represent another example of the problem Western nations are facing in dealing with immigration.

Energy recap: U.S. crude oil inventories fell 4.3 mb compared to market expectations of a 2.8 mb draw.

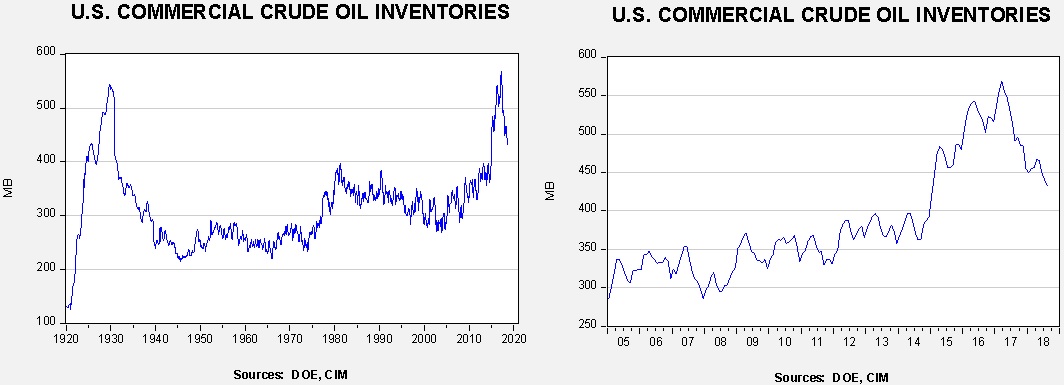

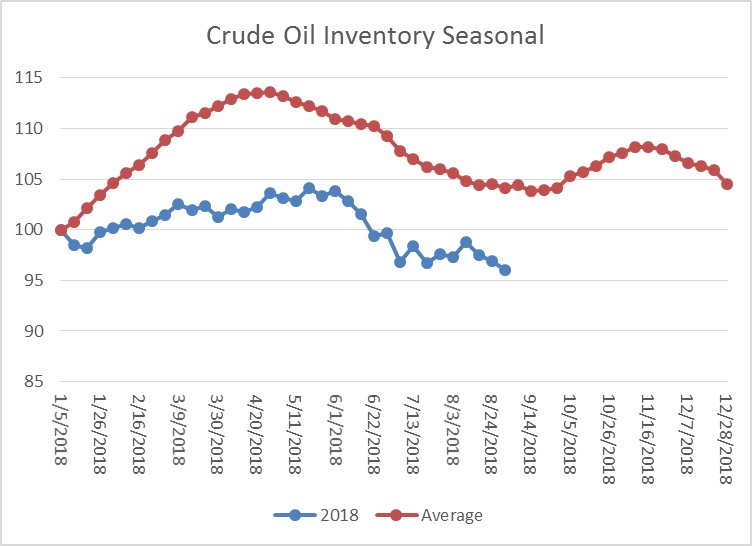

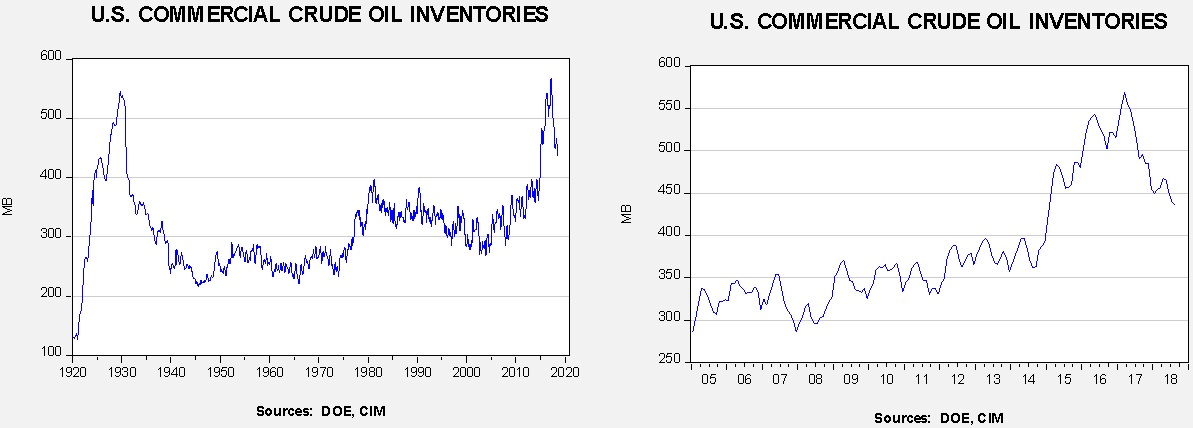

This chart shows current crude oil inventories, both over the long term and the last decade. We have added the estimated level of lease stocks to maintain the consistency of the data. As the chart shows, inventories remain historically high but have declined significantly since March 2017. We would consider the overhang closed if stocks fall under 400 mb. This week’s decline in inventories is in line with seasonal trends. Refinery utilization rose modestly to 96.6%, up 0.3% from last week. Oil production reached 11.0 mbpd.

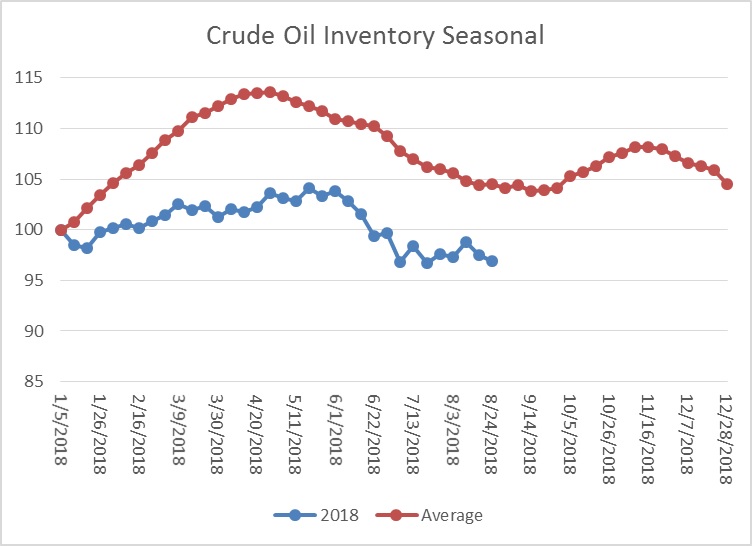

As the seasonal chart below shows, inventories are late in the seasonal withdrawal period. This week’s decline is normal but the size of the withdrawal was higher than usual. Over the next few weeks, we look for inventories to approach 400 mb, which would signal the end of the storage overhang that has developed over the past few years.

(Source: DOE, CIM)

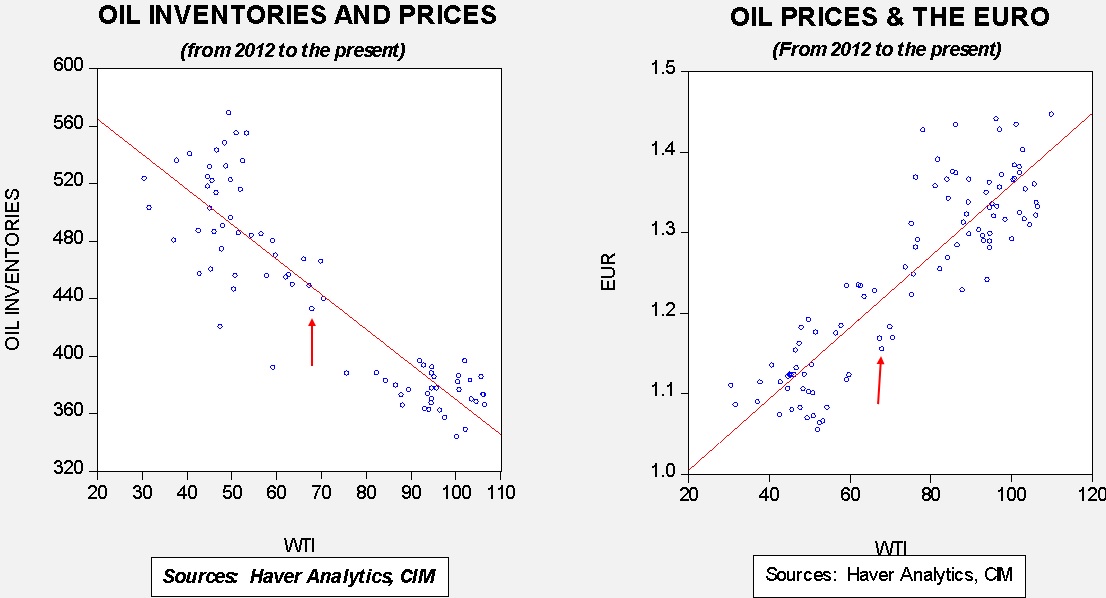

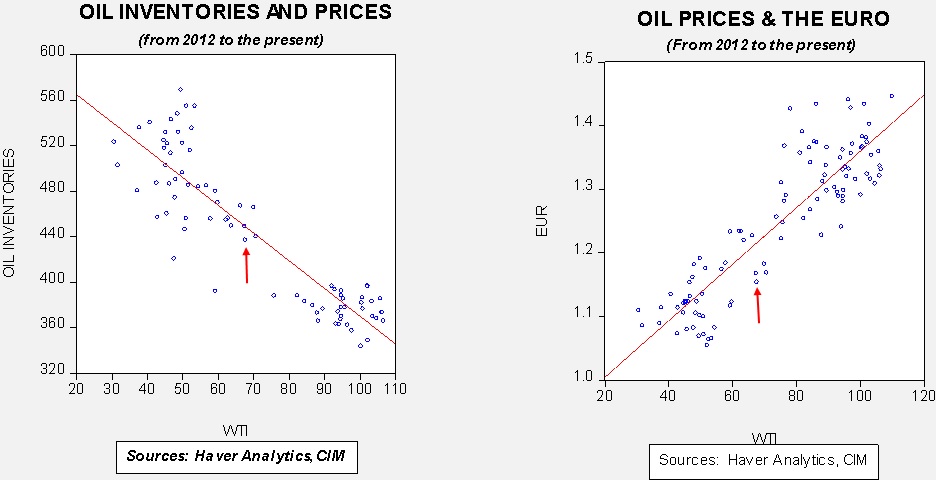

Based on inventories alone, oil prices are below fair value price at $73.62. Meanwhile, the EUR/WTI model generates a fair value of $58.13. Together (which is a more sound methodology), fair value is $63.12, meaning that current prices are well above fair value. However, the most bearish factor for oil is dollar strength. It will be difficult for oil prices to move higher without some reversal in the greenback.

A couple of items on the oil markets—first, Saudi Arabia is boosting its oil exports[9] to the U.S. in response to President Trump’s pressure to reduce oil prices. This decision could lead to an interesting situation. If the Saudis sell more oil to the U.S., it could widen the spread between WTI and Brent, encouraging U.S. producers to export more U.S. oil. If the U.S. had adequate infrastructure in place, the Saudis’ actions would certainly lead to a “merry-go-round” of oil flows. However, the U.S. doesn’t yet have the infrastructure in place to make U.S. exports seamless, so the likely outcome is weaker WTI but stronger Brent. Second, the U.S is warning[10] European firms not to break sanctions with Iran. Washington threatens that the U.S. will retaliate against Europeans, perhaps denying them access to the U.S. financial system, if sanctions are not honored.

[Posted: 9:30 AM EDT] For financial markets, it’s fairly quiet (especially compared to the political turmoil in Washington) with EM still coming under pressure. Here is what we are watching today:

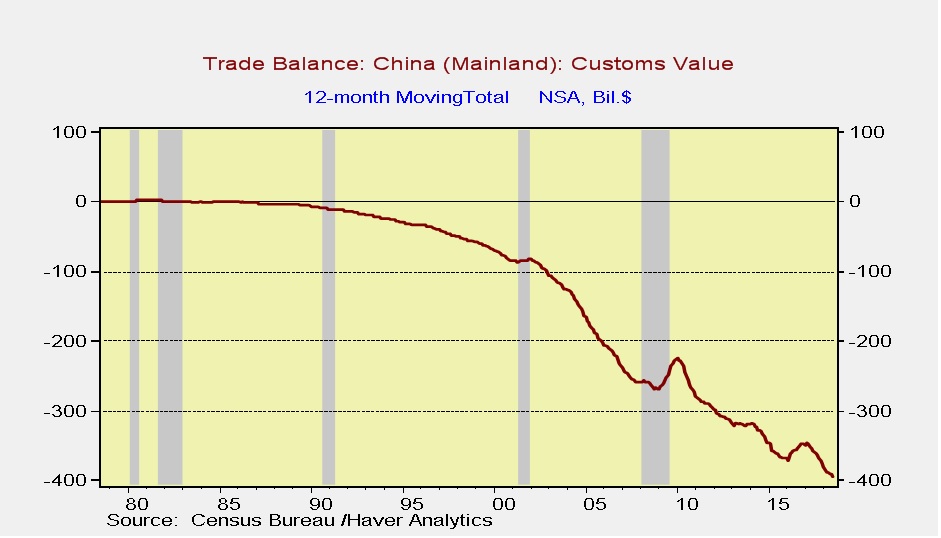

New Chinese tariffs? One of the effects of the Woodward book and yesterday’s anonymous editorial is that there appears to be some distraction on trade. Today is the deadline for deciding on new Chinese tariffs; these would be an additional $200 bn in size.[1] There doesn’t appear to be any talks of substance underway and we do expect some kind of announcement today. Anything less than $200 bn at 25% would likely be taken as bullish by equities. If a tariff announcement is made, we would expect China to retaliate, although China is starting to approach limits to what it can do because of the trade disparity. And, as yesterday’s data showed, the goods deficit with China continues to widen. On a rolling-12 month basis, the deficit is $393.5 bn.

NAFTA: According to reports, U.S. and Canadian negotiators made progress in NAFTA discussions.[2] If an agreement is reached, it would be bullish for equities.

Government shutdown? Although Congressional Republicans appear cool to the idea, President Trump seems open to shutting down the government to force funding for a border wall.[3] Government funding is set to lapse on September 30. A government shutdown could further undermine the GOP’s chances to retain the House. For financial markets, we would not expect too much of a reaction. Shutdowns in the past have been bullish for Treasuries and bearish for equities but, given that we have seen a few of these now, the financial markets will likely look beyond the initial event and assume a timely resolution.

Another North Korean thaw? Kim Jong-un was quoted as saying he wants to achieve Korean peninsula denuclearization by the end of President Trump’s first term.[4] President Trump responded positively. Our take on the overall negotiations is that Kim would like to improve relations with the U.S. in order to be less dependent on China. We note that China has openly flouted sanctions[5] in the aftermath of SoS Pompeo’s recent difficult talks with North Korean officials. Beijing does not want a thaw between the U.S. and North Korea; a potentially hostile power on its border would be an unwelcome development. At the same time, Pyongyang does not want to denuclearize without getting something substantial in return. Normalization of relations and the chance to see better economic growth are probably minimum requirements.

Italian populists blink: The leadership in Italy has indicated it will adhere to EU fiscal constraints.[6] Until these comments, Italy appeared ready to challenge the EU and expand beyond the 3% deficit/GDP limit. However, rising Italian yields appear to have sent a message to the government and this climb down is likely designed to reduce Italy’s borrowing costs.

India and Iranian oil: U.S. and Indian officials are in talks regarding Iranian oil imports.[7] The U.S. is implementing sanctions on Iran and is pressing all of Iran’s export customers to cease buying Iran’s oil. India has indicated it will likely continue to purchase Iran’s oil but is probably willing to make concessions to the U.S. and at least reduce imports from Iran. If the U.S. is successful in that effort, it will put further pressure on the Iranian regime.

[Posted: 9:30 AM EDT] It’s a risk-off day this morning as worries about global trade and emerging market contagion continue to mount. Here is what we are watching this morning:

BREAKING: There are reports that Germany is willing to make concessions to the U.K. The GBP jumped on the news. However, there are no details at this time.

NAFTA: After taking a five-day break, U.S. and Canadian negotiators are back to the bargaining table today. Here are the five major sticking points.[1] First, dairy. Canada has a milk board that allocates production. This leads to less supply and higher prices in Canada; to prevent the milk board from being overwhelmed by cheaper U.S. dairy, Canada restricts trade in this area. If the U.S. wins on this one, the Canadian dairy industry will be hammered. Protecting agriculture is common in many nations (people have a visceral reaction to food insecurity). On the other hand, Canadian consumers would greatly benefit. Second, the dispute management system is under threat. The current system for resolving disputes is a panel of representatives that determines if anti-dumping or countervailing duties should be implemented. The Trump administration opposes this body because it restricts U.S. sovereignty. Third, another part of the dispute management system allows firms to sue governments. The U.S. opposes this measure as well. Fourth is the steel and aluminum tariff issue. The U.S. implemented tariffs on these items and is threatening to do the same on autos. It’s hard to have a free trade zone when one nation can unilaterally apply tariffs. Lastly, culture protection is in question. The original agreement was made before the digitization of the economy. Patent and copyright protection need to be addressed but Canada has concerns about protecting the cultural integrity of French-speaking Quebec.

So, is a deal possible? Yes, but the Trump administration appears to be offering Canada the agreement already in place with Mexico or nothing. If PM Trudeau takes that deal, which is probably the best decision economically, the political ads for next year’s election almost write themselves. His opponents will run as leaders who will protect Canada. On the other hand, if Canada balks, the disruption to the Canadian economy will be massive. We suspect Canadian negotiators will try to get some modest changes to save face but will accept the bulk of the agreement the U.S. has in place with Mexico.

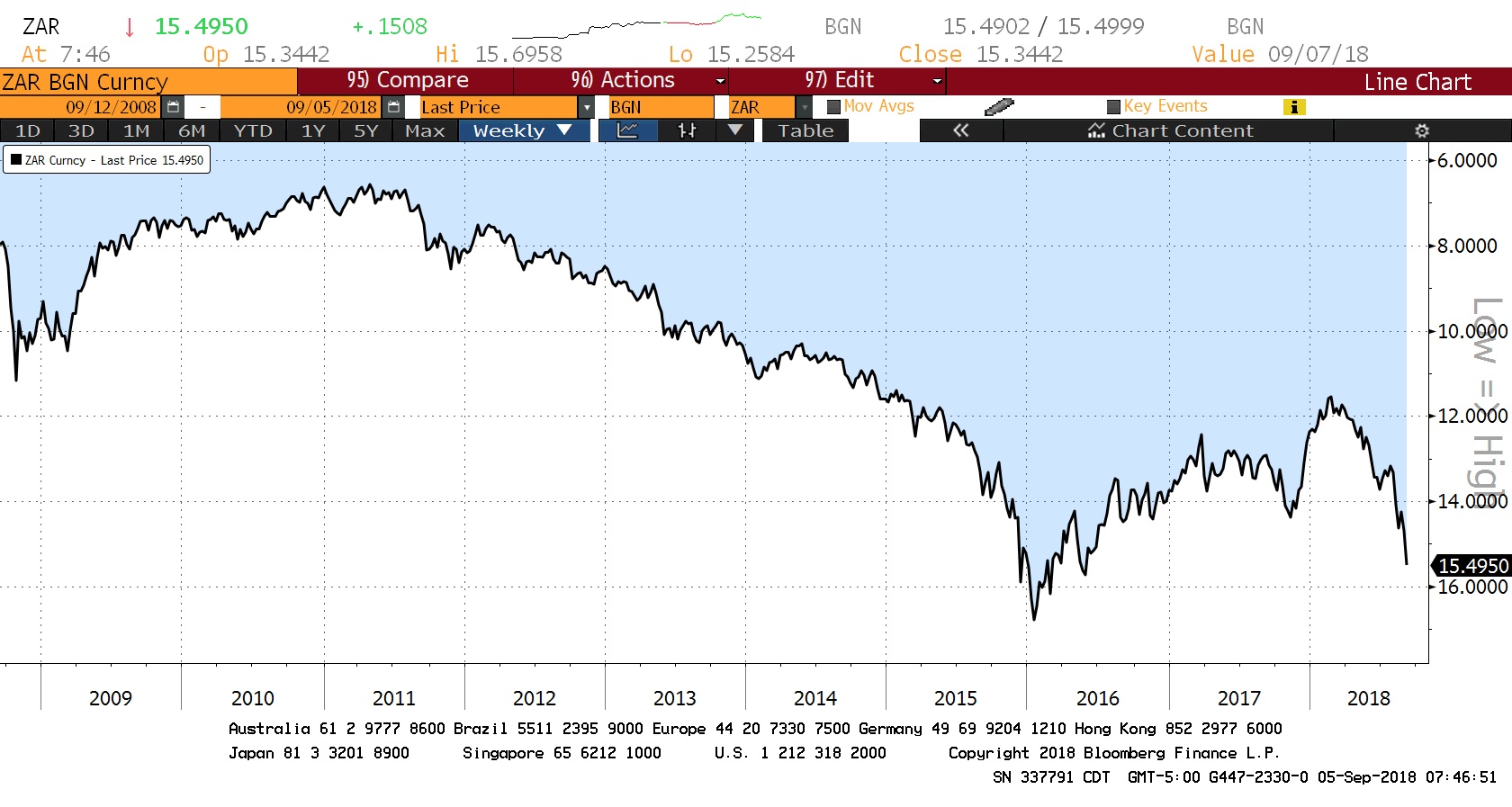

South Africa in the barrel: South Africa is the next EM country to see increasing pressure. Recent economic data indicate the country is in recession.[2] The ZAR continues to slide.

(Source: Bloomberg)

Although there is hope that the new Ramaphosa government will overcome the scandal-ridden Zuma administration, unfortunately the government will be starting under weak economic conditions.

EM thoughts: We are seeing that nations with current account deficits are coming under pressure on fears they won’t be able to fund these shortfalls. Although it does feel a bit like the 1997-98 Asian Economic Crisis, there are some important differences. During that event, most nations were pegging their currencies which led to unsustainable foreign currency debt growth and “hard stops” when the pegs failed. This time around, currencies float, which means they can fall to a sustainable level quickly and signal to domestic borrowers in EM nations to slow or reverse debt growth. That doesn’t mean there won’t be austerity and pain but the path will likely be less jarring. On the other hand, the only way a current account deficit nation can pay back dollar debt is by running trade surpluses with the U.S. If the Trump administration continues to put up trade barriers, the ability of these EM nations to service their debt becomes questionable.

[Posted: 9:30 AM EDT] Back in session! Summer’s over. Today is all about the dollar, EM and oil. Here is what we are watching:

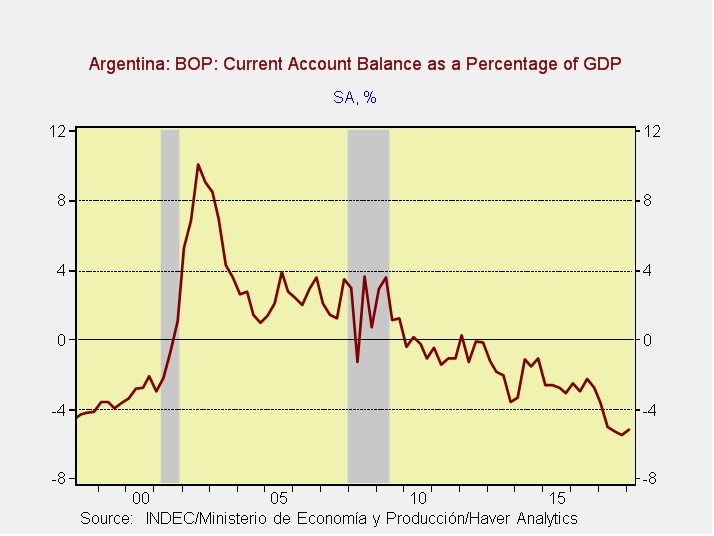

Emerging markets: Emerging equities were mixed overnight, with China doing well but others not so much. It’s looking like concerns are breaking into two broad categories. The first is the fragile group. These are nations that have borrowed in dollars and are vulnerable to dollar strength and rising U.S. interest rates. Argentina and Turkey are the prime examples of countries that will struggle to avoid default or restructuring. The second category includes those nations that are dependent on the U.S.-supported global trade structure; China and India are two examples of this group. The first group is most vulnerable to tightening monetary conditions in the U.S. The second group is being influenced by the Trump administration’s trade policies. If this analysis is correct, the first group will remain under pressure until we see signs that the FOMC is nearly finished with tightening. The second group may benefit if there is a change of control in Congress in November. For the time being, there doesn’t appear to be immediate relief on the horizon. The administration is poised to implement $200 bn of sanctions on Chinese goods by Thursday. Recent trade actions are already affecting global supply chains.[1] Argentina has released an austerity program.[2] We view it as a first step in stabilizing the currency. Turkey is also hinting at raising rates.[3]

The dollar: Continued trade friction and Fed tightening are boosting the dollar this morning.[4] The U.S. and Canada were unable to agree on a renegotiation of NAFTA last week but talks do continue.[5] President Trump, in an interview with Bloomberg, made off-the-record comments that made their way into Canadian media. Essentially, the president indicated that Canada would have no choice but to accept the agreement made with Mexico. As we noted last week, this puts PM Trudeau in an impossible position and, predictably, the Canadians balked. The problem for the White House is that NAFTA is a treaty and Congress has input. Already, we are hearing that Congress may force negotiators to keep Canada in the agreement. U.S. labor leaders are pushing to maintain the pact in its current form.[6] Simply put, Congress may trim the degree of changes the White House can make to the treaty and get it passed. Dollar strength is weighing on most commodities this morning, including gold. Oil, as noted below, has bucked the trend.

Oil and Gordon: As noted below, TS Gordon has formed and is moving into the Gulf of Mexico. Oil rigs have been evacuated,[7] although some production will be maintained as many of the facilities have automated systems that will keep oil flowing until wind speeds reach certain levels. Such storms will disrupt imports and thus could lead to a reduction in inventory levels over the next couple of weeks. In addition to Gordon, expectations of tightening sanctions are already affecting Iranian oil flows. Concerns over Iran have been supportive for oil prices and the tropical storm has simply added to supply concerns.

Pound down:Worries about a hard Brexit are hitting the GBP. PM May has tried to weave a policy that will meet the goals of the “leavers” but keep enough ties to the EU so as not to harm the economy. Unfortunately, this policy has managed to please neither side and is raising worries that the May government won’t be able to recommend a coherent policy for leaving.[8] If no plan emerges, we will likely see further weakness in the U.K. currency.

In light of the recent conviction of Paul Manafort and the guilty pleas by Michael Cohen, along with the upcoming midterm elections, we have been receiving questions about the political landscape going into winter. In this report, we will discuss our baseline expectations for political trends and their potential effect on financial markets.

Our expectations:

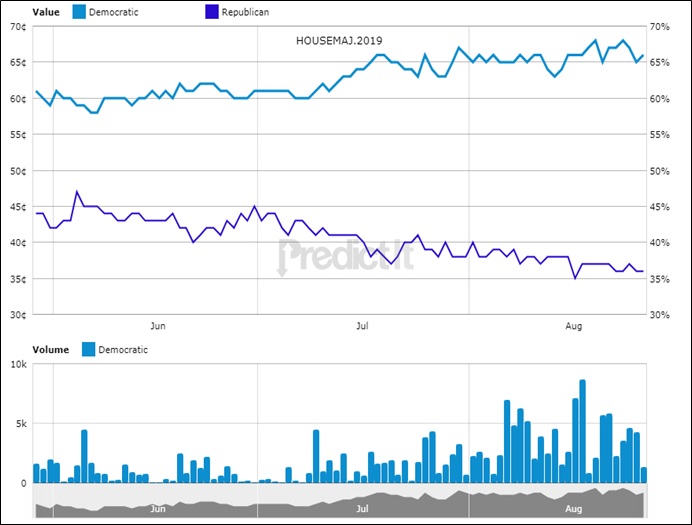

We expect the Democrats to win the House in November but the GOP will hold the Senate. Current prediction market wagers are the primary basis for this expectation.

(Source: PredictIt.com)

For the House, the prediction market has been consistently indicating a 65% likelihood that House control changes parties. At the same time, the same group shows the likelihood that the GOP retains control of the Senate is above 70%.[1]

A divided legislature will lead to gridlock. We expect a Democrat-controlled House to use its subpoena power to investigate any potential corruption in the Trump White House. According to Axios,[2] there will be a plethora of potential areas to examine. Because of this distraction, we doubt the White House will be able to muster any significant legislative achievements. This outcome isn’t all that unusual. Normally, the peak of a president’s power is in the first 18 months of his first term. Any political capital that isn’t spent in this period is lost. By summer of the second year in office, midterm elections are looming and Congress is distracted by the upcoming vote. Often, the president’s party loses seats in Congress after the midterms and legislative progress grinds to a halt. This usual pattern, coupled with the likelihood of perpetual investigations, probably means not much will get done.

Will the Democrats impeach President Trump? Much of this will depend on what the House investigations unearth. Although articles of impeachment might be approved, there is very little chance that two-thirds of the Senate would vote to remove Trump from office.

How will financial markets react to these baseline forecasts?

Equity markets: There have only been two impeachment events during modern market conditions, in the early 1970s under Nixon and the late 1990s under Clinton. In the former event, equities declined but the Watergate scandal was probably nothing more than a minor contributing factor. The economy was in a deep recession in 1973-74, and the world economy was reeling from the end of Bretton Woods and the Arab Oil Embargo. Simply put, there was a lot going wrong and the Nixon resignation was only part of the overall turmoil. In the latter case, equity markets were in the midst of the great tech bubble and mostly ignored the political news.

In general, equity markets will be sensitive to the business cycle and policy. We don’t expect a recession over the next three to four quarters. If the Fed overtightens, which will be an increasing risk next year, a recession is possible. For now, we expect the FOMC to move slowly on rates and avoid a policy error. In terms of fiscal and regulatory policy, the equity markets have already received support in the form of corporate tax cuts, additional spending and deregulation. At the same time, we have seen some weakness develop on fears of a wider trade war. If congressional investigations slow the trade conflict, we could see the bull market in equities not only continue but gain strength.

Debt markets: If trade impediments don’t increase and the Fed continues to raise rates, the odds of higher interest rates will increase. Political turmoil may lead to some flight-to-safety buying for Treasuries, but credit spreads could widen as a result. Overall, we could see the 10-year Treasury yield move toward 3.15% but would not expect it to move much above that level.

Currencies: The dollar is probably the most vulnerable of all the asset classes. On a parity basis, the dollar is overvalued (our parity against the EUR is approximately $1.3050) and has been rallying mostly on trade worries. If the U.S. puts up broad trade barriers, we would expect foreign nations to depreciate their currencies in order to offset the price increases triggered by the tariffs. When President Trump appeared ready to apply trade restrictions globally, the dollar rallied. However, the recent deal on NAFTA and the détente with the EU suggests that the administration’s real goal may be to contain China. If so, the dollar could weaken; political turmoil might accelerate that trend. A weaker dollar would tend to benefit international investments, U.S. large caps and commodities.

The political situation will not be the only factor affecting market behavior. For equities, earnings and the overall economy will still be significant. Political peace coupled with a recession would still be bearish for stocks. The above discussion addresses the likely impact of the unfolding political situation. The bottom line is that our position, for now, is that the current political situation, by itself, probably won’t be a major market-moving event.

[Posted: 9:30 AM EDT] So, we have to say “goodbye” to summer…and have a great Labor Day! Here is what we are watching today:

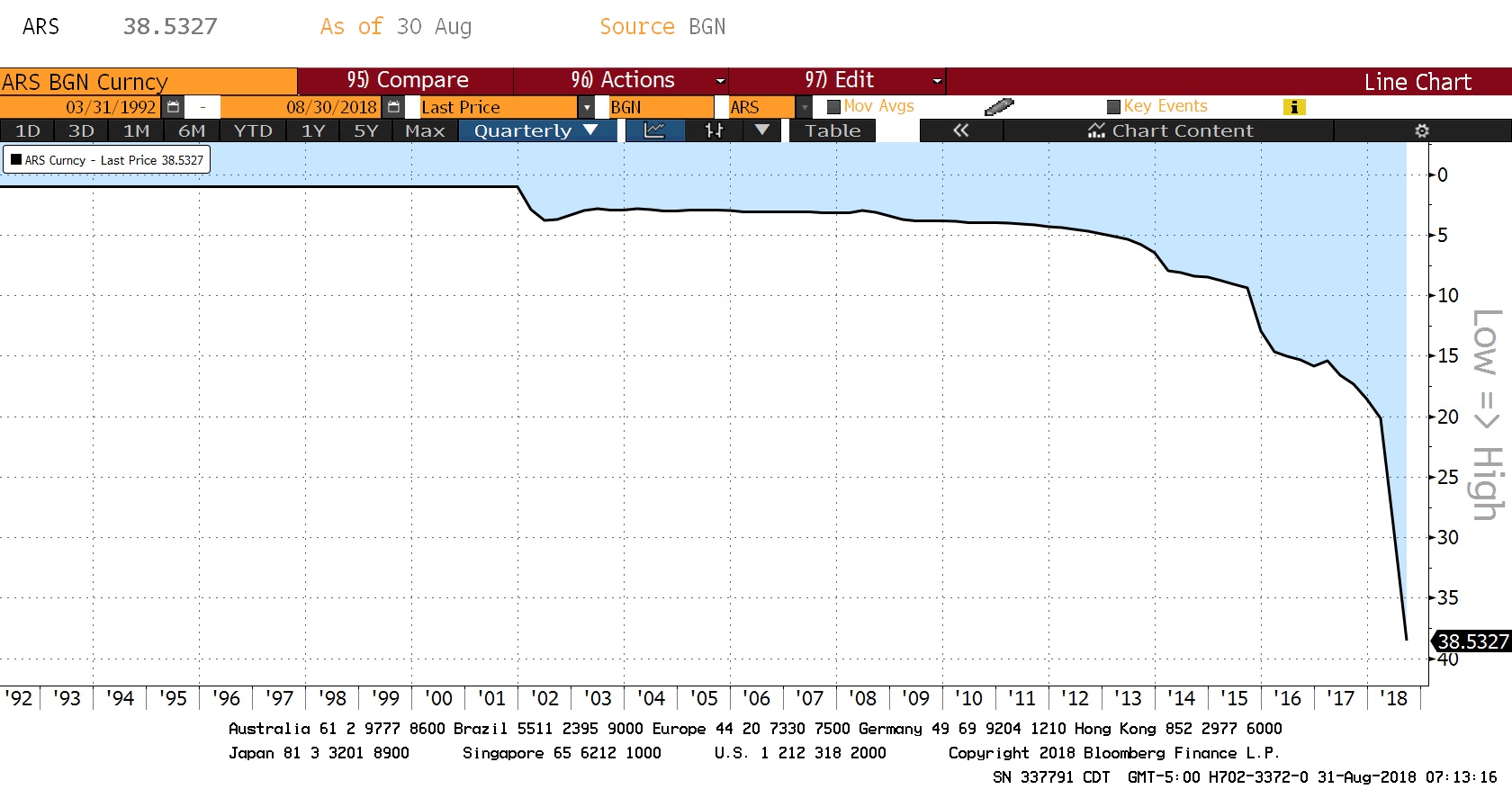

Emerging fears: The two problem nations, Argentina and Turkey, continue to struggle. Argentina has taken a beating; the currency is plunging to new depths and overnight interest rates have been ratcheted up to 60%.

(Source: Bloomberg)

This is a long-term chart of the ARS, starting in 1992. The currency is clearly in a freefall. For comparison purposes, note the chart below.

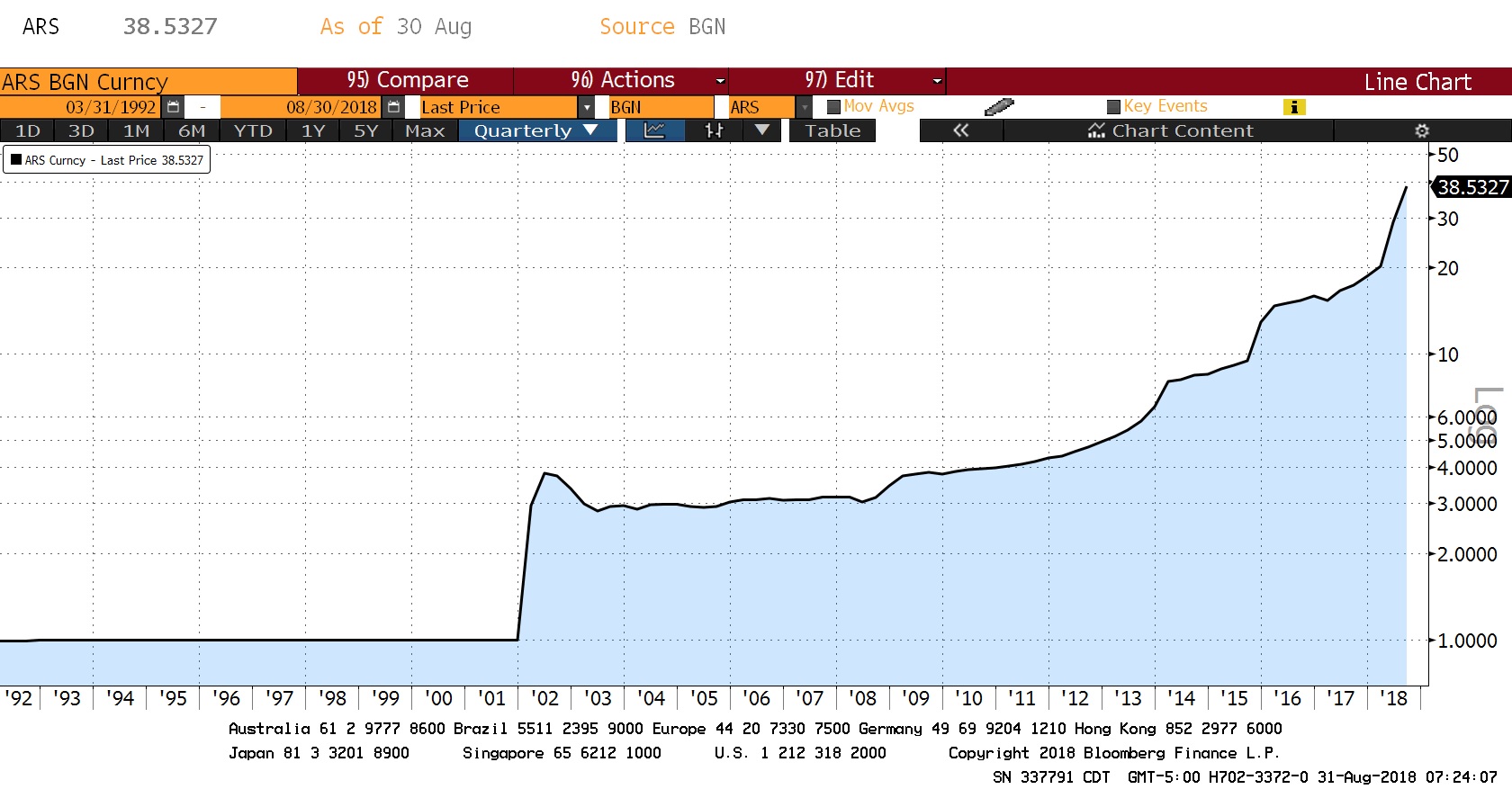

(Source: Bloomberg)

This chart shows the same chart above, but on a log scale (Bloomberg doesn’t have the capability to invert a log scale chart). Note that on a percentage basis, the 2002 depreciation was very large even relative to what we are seeing now. Thus, the decline, though historic in terms of level, is not out of the ordinary in terms of change.

How did Argentina address the problem in 2002? With fiscal austerity.

Argentina will likely receive help from the IMF in the form of accelerated payments. But, the IMF will demand fiscal austerity in return; history shows it will stabilize the situation. However, it won’t bring recovery and the political costs of austerity are high and unsustainable as we have seen from the country’s history. Thus, we don’t expect a long-term resolution to this problem.

Turkey was back in the news this morning as President Erdogan indicated his country would remain defiant in the face of U.S. financial pressure. The country did raise taxes on dollar deposits, which has helped stabilize the TRY this morning.[1]

The continued turmoil in Turkey and Argentina are putting downward pressure on emerging markets, in general. Adding to pressure are comments yesterday from the White House.

More from Trump on trade: In a wide-ranging interview yesterday with Bloomberg, President Trump indicated he wants to see an additional $200 bn of tariffs applied on Chinese goods. And, he suggested the WTO needs to “shape up” or the U.S. might withdraw from the body.[2] We have seen equities rally recently on optimism that the White House was moving in a direction to focus its trade actions on China. However, in yesterday’s interview, the president scotched those hopes and even piled onto them, criticizing the EU and rejecting the auto proposal made yesterday. European automaker equities reversed gains made yesterday morning on trade hopes.

Out of everything in the interview, the most concerning to us is the potential rejection of the WTO. The administration has been working to undermine the organization for some time, mostly by refusing to approve tribunal judges. Due to retirements, we are rapidly moving toward a situation where the WTO will not have enough judges to adjudicate claims. At that point, the trade body will essentially be unable to perform its functions. A U.S. withdrawal would pretty much overtly signal the end of the U.S.-built trade structure that was initially created after WWII.

We have noted that American actions are causing adjustments in the world order. For example, Japan and China, longtime adversaries, are meeting. Both nations are feeling pressure from Washington and so, even though they have areas of conflict, concerns over trade are encouraging discussions.[3] It has been our position for some time that the U.S. is reducing its global hegemony and the most likely outcome is a leaderless world where regional hegemons dominate security and trading arrangements. Japan may be concluding that the U.S. is no longer a reliable partner and thus is better off making arrangements with China to preserve its economy and security. Warmer relations between China and Japan would almost certainly lead the rest of the Asian powers to consider joining such a bloc (although India would try to hold out). We view such a world as unstable, although the U.S. will likely be able to avoid regional turmoil for some time.

NAFTA: Although negotiations continue, there is growing concern that a deal might not be reached. The CAD has dipped this morning on worries that negotiations may fail. We do think the odds favor an agreement.

[Posted: 9:30 AM EDT] So far, it’s a quiet morning with a bit of a “risk-off” tone. Here is what we are watching today:

An EU trade proposal? EU Commission President Juncker came to Washington this summer and convinced President Trump that the EU and the U.S. should negotiate on trade. Since then, not too much has happened. It is pretty clear that Juncker’s plan was to delay any agreement through the midterms and hope that a change of power in at least part of Congress would distract the White House and mostly maintain the status quo. At least, that’s what it looked like to us. However, to our surprise, the EU trade minister, Cecilia Malmström, has made a preliminary offer to end all tariffs on industrial products, including cars.[1] In the original discussions between Presidents Trump and Juncker, the scope of products discussed was only non-auto industrial goods. The EU currently applies a 10% tariff on imported U.S. vehicles compared to a 2.5% tariff on European cars imported to the U.S. However, the U.S. has a 25% tax on foreign light trucks. It will be interesting to see how the Trump administration responds. If the goal is to simply reduce tariffs, then this looks like an interesting offer. However, this deal would threaten U.S. automakers’ strength in light trucks. Although we don’t have year-to-date data since some of the automakers stopped reporting monthly sales, the latest data available through April show that U.S. automakers only hold a 25% share of the car market but a 55% share of light trucks. We would expect U.S. automakers to be cool to the change the EU is offering. In order to show that the U.S. really wants low tariffs but doesn’t want to hurt the U.S. automakers, the Trump administration could push to include agricultural products, which is a non-starter for the EU. European carmaker equities have risen on the news, but we would be surprised to see the U.S. accept this offer. However, we would not be surprised to see a tariff reduction on non-auto industrial goods.

The key to this proposal is that the U.S. does appear to be isolating China. If the EU and U.S. can ease trade tensions and, as we note below, NAFTA is renegotiated, then China will be left out. As we have noted before, this was the aim of TPP/TTIP.

So, you’re saying there’s a chance? Both President Trump and Canadian PM Trudeau[2] said yesterday that there is a chance a deal could be reached by Friday. Canadian dairy subsidies remain a sticking point but it does appear that Canada realizes the value of NAFTA to its economy. The PM will lose a lot of political capital to make this deal; politically, it never looks good for a nation to accept a fait accompli. We will be watching to see how the Canadians “spin” the agreement if one is reached.

Argentina’s woes: Despite central bank intervention, the Argentine peso plunged yesterday after President Macri asked the IMF to accelerate its aid disbursements.[3] The IMF indicated it would examine Macri’s request.

(Source: Bloomberg)

As this chart shows, the ARS has declined to new lows. A deepening current account and concerns about debt repayment have raised fears among investors.

The famous “century bond,” issued last year, is now trading at 70.5 cents on the dollar. Argentina will need to pay $50 bn in debt service this year and apparently needs the IMF’s support to ensure it can meet its obligations. Crises like what we are seeing in Turkey and Argentina have weighed on emerging markets in general.

China in Afghanistan: China is building training camps in the Wakhan Corridor, a small land strip that connects China and Afghanistan.[4] This is the first time in modern history that China has had a military presence in Afghanistan. However, as China attempts to build out its “one belt, one road” system for trade and infrastructure, Afghanistan’s role as a potential land bridge makes China’s influence there increasingly important. China is likely worried that Uyghur separatists in the Xinjiang region of western China could use the area around China to base operations. Thus, the move into Afghanistan makes sense. At the same time, as the U.S. is learning, Afghanistan’s moniker as the “graveyard of empires” should raise concerns in Beijing that becoming involved in Afghanistan can become a persistent drain on resources.

Energy recap: U.S. crude oil inventories fell 2.6 mb compared to market expectations of a 1.5 mb draw.

This chart shows current crude oil inventories, both over the long term and the last decade. We have added the estimated level of lease stocks to maintain the consistency of the data. As the chart shows, inventories remain historically high but have declined significantly since March 2017. We would consider the overhang closed if stocks fall under 400 mb. This week’s decline in inventories was in line with seasonal trends. Refinery utilization did decline, falling 1.8% to 96.3%. Oil imports were steady but a rise in oil exports helped reduce stockpiles more than forecast.

As the seasonal chart below shows, inventories are late into the seasonal withdrawal period. This week’s decline in stocks was consistent with seasonal patterns. If the usual seasonal pattern plays out, mid-September inventories will be 399 mb. We do note that we are approaching the end of the summer withdrawal season for crude oil inventories. By mid-September, we will start to see a rebuild in stockpiles; the impact of oil exports will rise in importance in autumn because we may not see the full extent of the usual seasonal build if exports rise.

(Source: DOE, CIM)

Based on inventories alone, oil prices are below fair value price at $72.22. Meanwhile, the EUR/WTI model generates a fair value of $57.96. Together (which is a more sound methodology), fair value is $62.48, meaning that current prices are well above fair value. However, the most bearish factor for oil is dollar strength. It will be difficult for oil prices to move higher without some reversal in the greenback.

[Posted: 9:30 AM EDT] It’s a quiet Wednesday, very typical of late summer. Here is what we are watching today:

Ottawa to Washington: The U.S. has given Canadian negotiators a deadline of Friday to accept the deal negotiated by the U.S. and Mexico. In response, Canada’s foreign minister, Chrystia Freeland,[1] is in Washington to conduct talks. It seems almost impossible that Canada would accept terms on such short notice. If the Canadians join, it would suggest the changes agreed to by Mexico and the U.S. are not different enough to matter. At the same time, not signing off on the pact could be very damaging to the Canadian economy. Politically, it will be hard for the Trudeau government to spin that it didn’t cave to the Trump administration if they accept the deal on such a short deadline. There is also increased grumbling about the deal among U.S. senators.[2] It isn’t completely clear that this agreement could pass Congress. So, yesterday’s declaration of victory may be premature. If the deal fails, it will raise fears surrounding trade and would be bearish for equities and bullish for the dollar.

About last night: A number of primaries were held last night as the primary season winds down for November’s main event. The key takeaway is that the current political coalition continues to fray and the populist insurgency is still growing. We are especially taking notice of the choice Florida voters will be facing, which is between a left- and right-wing populist.[3] The other interesting item of note was the heavy GOP turnout in Florida, which does suggest a higher degree of enthusiasm[4] than would be indicated if a “blue wave” is coming in November.

China and influenza: A new strain of the influenza virus has emerged in China. This is nothing unusual; nearly every year, a new strain mutates and often originates in China, which has a natural reservoir of swine and fowl that propagate new strains. The new virus, called H7N9, has been circulating for over a year. The U.S. would like to get a sample of it to start creating new vaccines for the upcoming flu season. However, China is refusing to share samples of the virus. According to reports,[5] some U.S. laboratories have received samples from Hong Kong and Taiwan, but it is unclear if enough material is available to build ample vaccine reserves. Although neither government is saying much officially, this lack of cooperation appears to be due, in part, to deteriorating relations between China and the U.S.

Russian war games: Russia is conducting the Vostok-2018 war games[6] next month. Beginning on September 11, the games will be the largest conducted since the fall of the Soviet Union. China has agreed to participate. The exercises, held in eastern Russia, used to be designed to prepare for a conflict with China. Thus, the participation of Chinese military units is unprecedented. This show of force coincides with a flotilla of Russian Navy vessels that have moved into the Mediterranean. These ships may be part of a build-up to support Syria in operations against rebel positions in Idlib, Syria.

U.S. war games return: As part of the agreement at the recent U.S./North Korean summit, the U.S. agreed to suspend military exercises with South Korea. Secretary of Defense Mattis[7] announced yesterday that this suspension would be lifted going forward, most likely due to the lack of denuclearization from Pyongyang. It is interesting to note that South Korea has been reluctant to say it would also resume war games.

India boosts defense spending: India has approved the acquisition of $6.5 bn of military hardware, including 111 naval helicopters. There has been an arms race escalation across Asia; current spending is $450 bn, with 44% coming from China alone.[8] This spending is due, in part, to fears that the U.S. is withdrawing from its postwar role of protecting the region. This spending is really not a surprise, but the mounting increase in spending and the arms build-up could lead regional powers to use this military hardware to either project power or resist incursions. What we are seeing in Asia will likely be seen in Europe over time.

A German bailout of Turkey? There are reports that the Merkel government is considering providing emergency economic aid to Turkey, fearful that an economic collapse could destabilize the Middle East and Europe.[9] In our most recent WGR,[10] we speculated that Ankara might use the threat of a migrant overflow into Europe to encourage support from EU leaders. These recent reports may indicate that Turkey is using backchannels to warn Germany and the EU that it might make good on this negative outcome. If so, the odds that Turkey stabilizes would improve, to some degree.

Richard Clarida to the FOMC: At long last, Richard Clarida made it over the final hurdle and will join the FOMC for the September meeting. We expect Clarida to vote as a moderate governor.

[10] See WGRs, The Turkey Crisis: Part I (8/20/18) and Part II (8/27/18).

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.