Daily Comment (August 22, 2018)

by Bill O’Grady and Thomas Wash

[Posted: 9:30 AM EDT] We are seeing a bit of risk-off this morning on the big political stories from yesterday. However, the emphasis is on “bit”; equity weakness isn’t excessive, the dollar is modestly weaker, gold is higher but not by a lot and Treasury yields are down but no panic has ensued. So, let’s dig in:

The political news: As has been well documented, Paul Manafort[1] and Michael Cohen[2] were convicted yesterday. The former was by a jury, while the latter plead guilty. The basic charges were fraud. We have received market-related questions about these events. Here is our initial take:

- Equities: We expect the equity market to take the news in stride. Clearly, political turmoil affects sentiment and thus we could easily see further pressure on P/E multiples. However, earnings remain robust, the economy is strong and, in what may be the most important factor, the tax cut benefits are probably already in place. Although the likelihood of further initiatives being passed by this administration is low, those odds were already depressed. As we have noted before, the most powerful period for a new president is the first 18 months. After that, midterms loom and political capital has been exhausted. In addition, if the president faces mounting legal woes, the momentum on trade talks could wane which would be bullish for equities. As we have shown before, equities were on their way to “melt up” territory in January when the president turned his attention to trade and the P/E has declined since then. A lessening of trade tensions would likely be bullish for equities, especially large caps. Our expectation—neutral.

- Debt: Treasuries will benefit from any flight-to-safety buying. Legal distractions will likely reduce the White House’s focus on monetary policy tightening. Our expectation—bullish.

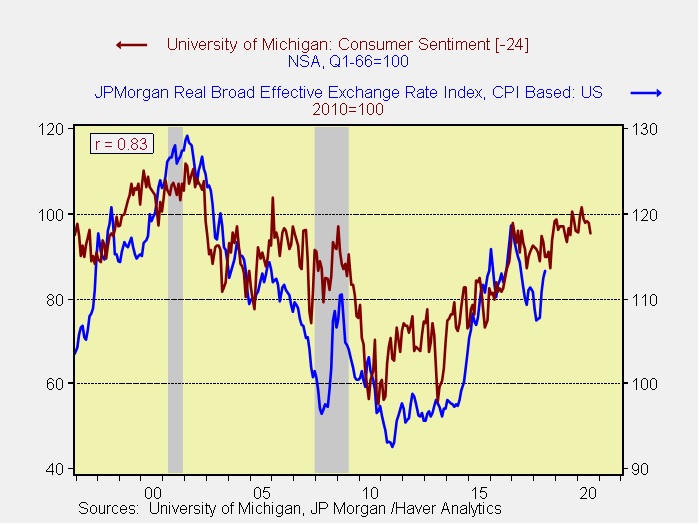

- Dollar: This is an area where the most impact is possible. The dollar, on a purchasing power parity basis, is overvalued. Tightening Fed policy has played a role in boosting the greenback but the potential for trade impediments is the primary reason for the bullish tone of the dollar. After all, if the reserve currency nation restricts trade, other nations must go to ever greater lengths to gain access to the U.S. market. The most likely way to do so is to support a weaker currency, boosting the dollar. Furthermore, exchange rates, in some ways, reflect sentiment. We note that the correlation between consumer sentiment and the dollar is very high since the late 1990s.

This chart shows the JP Morgan dollar index and the University of Michigan index of consumer sentiment. Since 1997, the two series are highly correlated with a two-year lag. Thus, if political turmoil begins to weigh on sentiment, it would probably put pressure on the dollar. Our expectation—dollar bearish, which would be bullish for commodities, gold and foreign equities.

The political outlook: Yesterday’s news is damaging for the president but it hasn’t reached the level of critical quite yet. The news highlights the importance of the midterm elections. If the Democrats take the House, we would expect a drive to bring articles of impeachment against Trump. As we saw with President Clinton in the late 1990s, that effort will likely fail in the Senate. Even if the Democrats experience a major wave and take control of the Senate, it seems highly improbable that the threshold of 67 votes to remove the president would be met.

However, as we have noted above, the distraction level will be elevated. That doesn’t mean that everything else would necessarily stop; President Nixon was able to come to the aid of Israel during the 1973 Yom Kippur War while in the midst of the Watergate investigation. Nevertheless, it will be hard to maintain focus on other issues. One subject we will be monitoring, especially if conditions deteriorate, is the power within the cabinet. For example, if the Mnuchin/Kudlow wing of the administration gains power during the turmoil and overshadows the Lighthizer/Navarro wing, then the tenor of the trade conflict would likely moderate. Our inclination is that Mnuchin will gain power and thus the trade conflict would be reduced. Overall, as noted above, we look for increased political distraction; by itself, that won’t be enough to derail equities but it could put downward pressure on the dollar.

Another factor worth noting is that despite talk of Russian collusion the administration and Congress continue to target Russia for additional sanctions. Earlier in the month, the administration applied additional sanctions on Russia over the U.K. poisoning.[3] Yesterday, the administration added new sanctions for violating sanctions on North Korea.[4] And, after we learned yesterday that Russia has hacked various right-wing think tanks, the Senate is preparing further sanctions.[5] So far, it would be difficult to make a strong case for Russian favoritism, at least given these actions.

Trade: Progress on NAFTA continues as reports suggest that a “handshake deal” could be struck with Mexico by tomorrow.[6] Talks on auto tariffs appear to be facing delays; as we noted earlier this month, the EU is expected to stall discussions into the midterms, likely hoping that more important issues will occupy the U.S. and thus allow the status quo to continue.[7] Meanwhile, China and U.S. negotiators continue to talk but neither side appears optimistic about an agreement.[8]

Monetary policy: The Fed minutes will be released later today (see below). We also note another report indicating that the BOJ is moving to end its aggressive easing stance.[9]

[1] https://www.ft.com/content/14dc40c4-a22d-11e8-85da-eeb7a9ce36e4?segmentId=a7371401-027d-d8bf-8a7f-2a746e767d56

[2] https://www.ft.com/content/5de0b3fc-a5a4-11e8-8ecf-a7ae1beff35b?segmentId=a7371401-027d-d8bf-8a7f-2a746e767d56

[3] https://www.ft.com/content/0d1d64dc-9b41-11e8-ab77-f854c65a4465?emailId=5b7cdea30b4eba00040e5254&segmentId=22011ee7-896a-8c4c-22a0-7603348b7f22

[4] https://www.nytimes.com/2018/08/21/us/politics/new-us-sanctions-target-russia-for-defying-rules-on-north-korea.html?emc=edit_mbe_20180822&nl=morning-briefing-europe&nlid=5677267mbe_20180822&rref=collection%2Fsectioncollection%2Fpolitics&te=1

[5] https://www.nytimes.com/2018/08/21/us/politics/russia-sanctions-microsoft-hacking.html?emc=edit_mbe_20180822&nl=morning-briefing-europe&nlid=567726720180822&te=1

[6] https://www.politico.com/story/2018/08/21/trump-nafta-mexico-746332

[7] https://www.wsj.com/articles/trump-auto-tariff-timetable-likely-to-slip-amid-europe-nafta-talks-1534853144

[8] https://www.ft.com/content/cea76a70-a510-11e8-8ecf-a7ae1beff35b

[9] https://www.reuters.com/article/us-japan-economy-boj/japan-central-bank-may-dial-back-stimulus-before-price-goal-met-ex-boj-ishida-idUSKCN1L707U