by Asset Allocation Committee

Politics is usually an uncomfortable topic for financial market analysts. The subject is fraught with high emotion, and being overly concerned about a specific political outcome can sometimes cloud judgement. At the same time, political trends offer insight into future policy changes that can affect financial market performance. For example, we have documented the growing trend of populism and its potential impact on economic and market performance.[1]

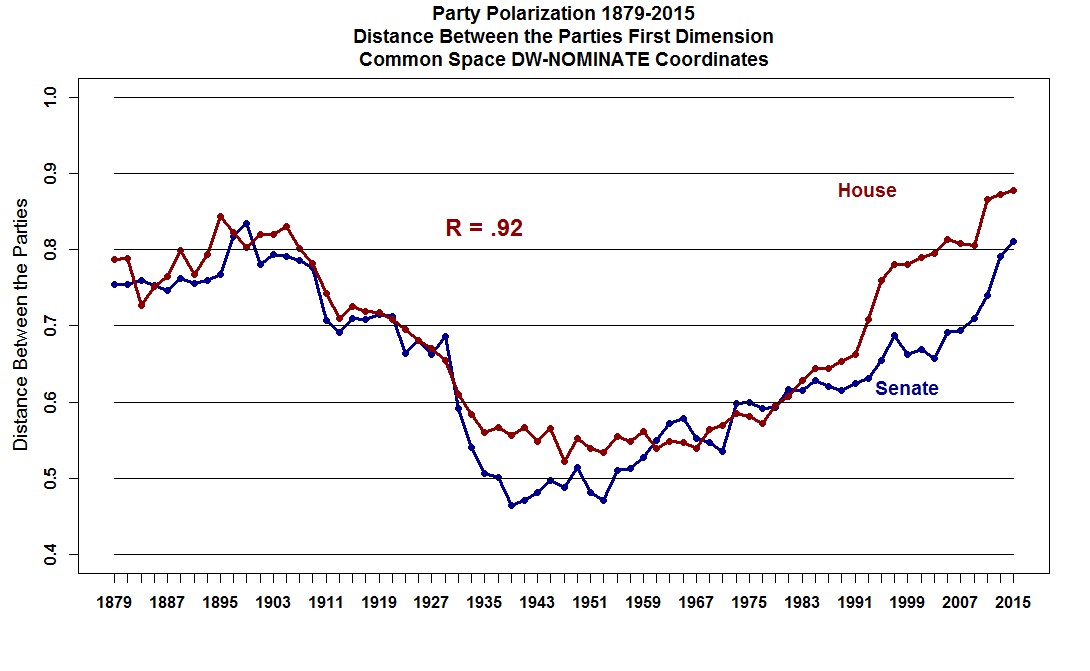

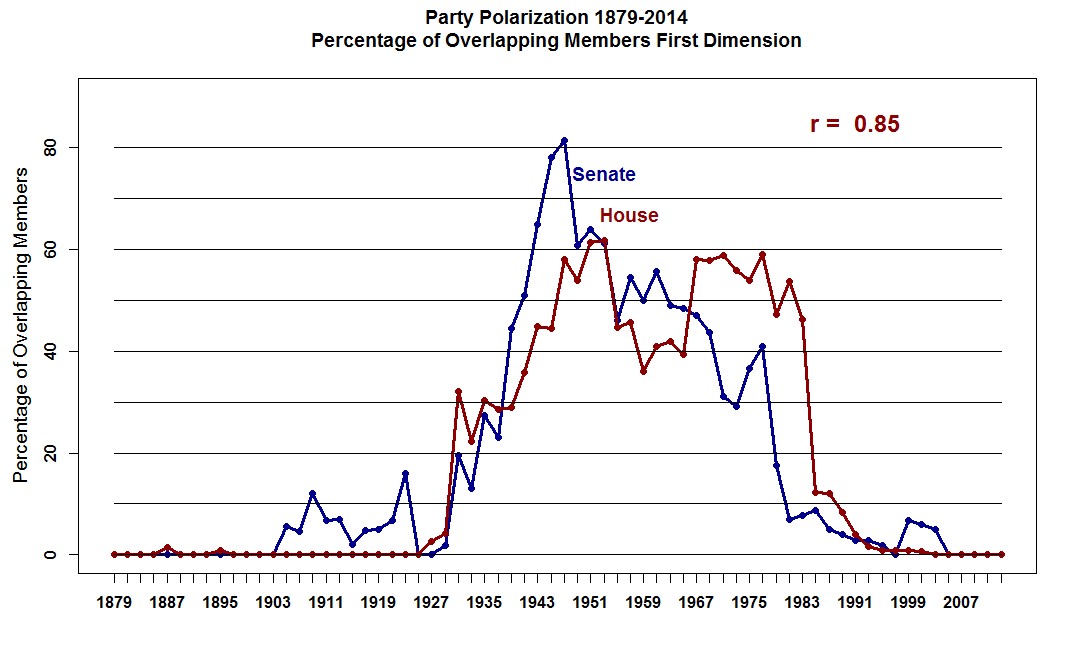

One of the more disturbing trends we have noted in recent years is the growing division among Americans that is being reflected in our political system. Race and gender concerns in marriage have become less of a concern, but marrying across political lines has become increasingly frowned upon.[2] The level of partisanship has increased steadily over the past two decades.

This data measures the difference between the party voting patterns in Congress. The higher the number, the greater the degree of difference, meaning a higher level of partisanship. A similar measure that estimates the percentage of overlapping members (likelihood of voting across party lines) has diminished as well.

This deepening polarization, coupled with the widespread use of social media, is leading to increasingly aggressive behavior and threats.[3] More American institutions are progressively being viewed under the lens of partisanship; the courts, regulatory agencies and law enforcement are all facing scrutiny for their decisions. Reaching an agreement on the impact of seemingly objective facts is becoming increasingly difficult.

The reasons for polarization are beyond the scope of this report. Our concern is the impact of polarization and partisanship on financial markets. So far, the Federal Reserve has mostly avoided the worst of this trend. However, it would seem naïve to believe that the U.S. central bank can remain above the partisan fray indefinitely. Already, President Trump has undermined protocol with regard to monetary policy established by Robert Rubin in the mid-1990s. That protocol meant the White House would refrain from commenting on monetary policy, with the concept being that the less political pressure the Federal Reserve faced, the more confidence investors would have in the central bank maintaining anchored inflation expectations. President Trump has been openly critical of monetary tightening. So far, we have not seen political pundits frame monetary policy in a partisan fashion. But, the risks of such events are rising. If monetary policy actions are increasingly viewed through the parameters of partisan politics, we would expect the following market effects:

- Long-duration interest rates will rise. These rates are sensitive to inflation expectations. Undermining Federal Reserve independence will tend to raise fears that policymakers won’t increase rates for fear of criticism, leading the central bank to tolerate higher inflation.

- The dollar will weaken. If the central bank won’t act against inflation impulses, then the attractiveness of the dollar will be diminished.

- Gold prices will rise. Gold will be seen as a store of value instrument, which will become more appealing in a rising inflation environment.

- Equity markets will suffer through falling multiples. Price/earnings multiples are partly a function of inflation expectations. If prices are rising, earnings become suspect and investors lower the price at which they will purchase those earnings.

To date, there is no evidence that monetary policy has been affected by White House criticism. However, that condition may not endure. We continue to closely monitor developments but we will take appropriate action if the Federal Reserve finds its independence compromised.

[1] See Weekly Geopolitical Reports, Reflections on Politics and Populism: Part I (7/16/18) and Part II (7/23/18); and European Populism (1/12/15).

[2] https://www.voanews.com/a/mixed-political-marriages-an-issue-on-rise/3705468.html

[3] https://thehill.com/homenews/administration/348014-threats-of-political-violence-rise-in-polarized-trump-era