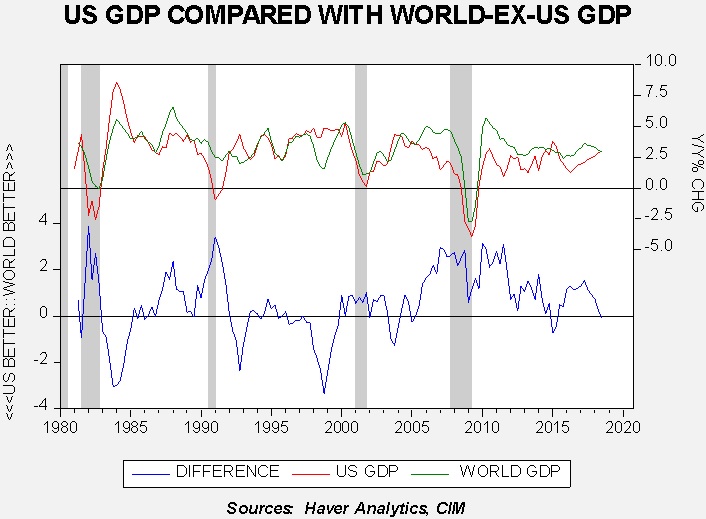

One of the important unknown factors for 2019 is whether slowing global growth will have a negative impact on the U.S. economy. Or, put another way, can the world lead the U.S. into recession? For the most part, history suggests the answer is no—the U.S. can bring down the world but the world can’t bring down the U.S.

The upper two lines show the yearly change in U.S. GDP and World ex-U.S. GDP. The lower line shows the difference. World and U.S. GDP are positively correlated at the 70% level, suggesting they are sensitive to each other. Since the U.S. provides the reserve currency it would make sense that a stronger U.S. economy would also support imports from abroad which would foster foreign economic growth. However, the U.S. doesn’t export as much relative to its size as other nations do, so it follows that stronger U.S. growth would support higher world growth but better growth in the rest of the world wouldn’t necessarily lead to better American growth.

A couple of examples show this pattern. In the late 1990s, world GDP growth fell sharply while the U.S. was unaffected. The Asian Economic Crisis and the Russian debt default did not derail the U.S. economy. In 2005, the U.S. economy began to slump due to the deflating housing bubble. World growth did hold up into 2008 but eventually succumbed to follow the U.S. into recession.

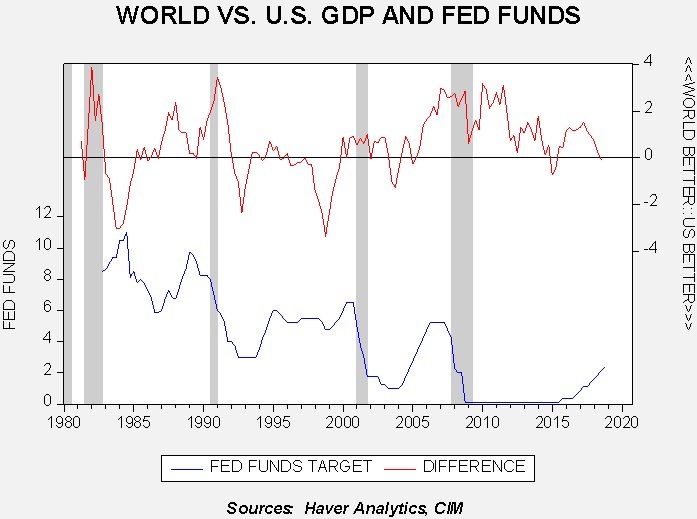

At the same time, this analysis doesn’t mean policymakers should ignore the world. In theory, the Federal Reserve’s mandate is full employment and low inflation. Since these goals can be mutually exclusive at times, the Fed has tended to leave both specifically undefined. That has changed; the Fed now has a semiformal[1] 2% core PCE goal, which means the full employment goal is even more amorphous. When asked about the world, Fed officials are usually circumspect but do say they will address the issue if overseas events affect the U.S. economy. The above research suggests this comment is something of a “fudge”; the world rarely affects the U.S. directly. But, there are times when the Fed does appear to move policy in light of world events.

A couple of events are notable, where the Fed appeared to have adjusted policy due to global events. In the early 1980s, the Fed was still managing interest rates by focusing on the money supply. However, the high level of interest rates led Mexico to default and caused cascading debt crises throughout the region. The Volcker and Greenspan Feds reacted by cutting interest rates from 11% to 6% and the spread between U.S. and global growth narrowed. The Greenspan Fed eventually cut rates during the Asian Economic Crisis and the Russian debt default in the late 1990s, although the Long-Term Capital Management debacle contributed to that move. We also note that the Fed continued to reduce rates into 2004 even though the recession had ended; while weak global growth may have contributed, as we discussed two weeks ago, high equity market volatility probably contributed as well.

If the FOMC is looking for an excuse to ease policy, it could certainly use concerns about global growth affecting the U.S. economy as a reason. Although we doubt that the weak global economy will bring down American growth, concerns about it could allow the Fed to lower rates and maintain credibility. So far, we have not seen any indication that this factor is affecting policy, but it would not be a stretch to see the reason pop up in comments and statements from the U.S. central bank to at least justify a sustained pause in rate hikes.

[Posted: 9:30 AM EDT] Equities are rallying around the world. Here is what we are watching this morning:

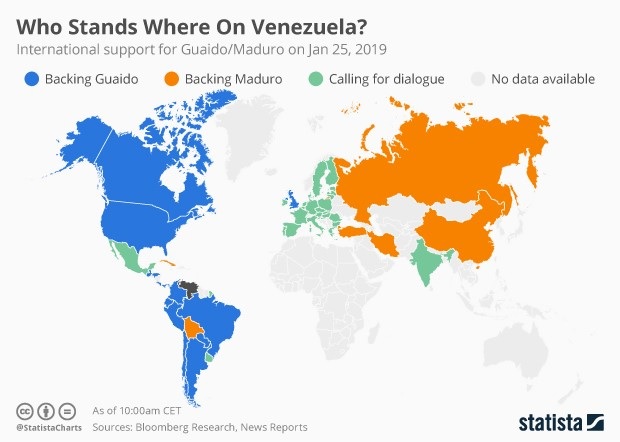

Venezuela: As we noted yesterday, China and Russia[1] would be on the hook for billions of bad debt that a new government could simply default on, arguing the debt was incurred by an illegitimate government.[2] China usually tries to avoid taking outright positions on international issues, a legacy from the Mao-Deng years. At the same time, if it doesn’t get involved, it could lose billions.[3] China is officially supporting Maduro but the endorsement is far from ringing. Senior military officials have signaled they continue to back Maduro.[4] However, it is unclear if the upper ranks can continue to control the sentiment and behavior of the lower ranks. There is also an impending concern about U.S. embassy staff. Maduro has ordered them to leave this weekend, but Pompeo indicated earlier that the diplomats will stay because the U.S. no longer recognizes Maduro as the legitimate ruler of Venezuela. Apparently prudence has partially overruled valor and the U.S. has ordered non-emergency staff out of the country and “advised” other Americans to leave.[5] But, senior diplomats will stay and the embassy will stay open, creating the potential for conflict. It is important to remember that Trump is a classic Jacksonian; an attack on the embassy would almost certainly trigger a military response.

Here is a snapshot of global allegiances toward Maduro and Guaido.

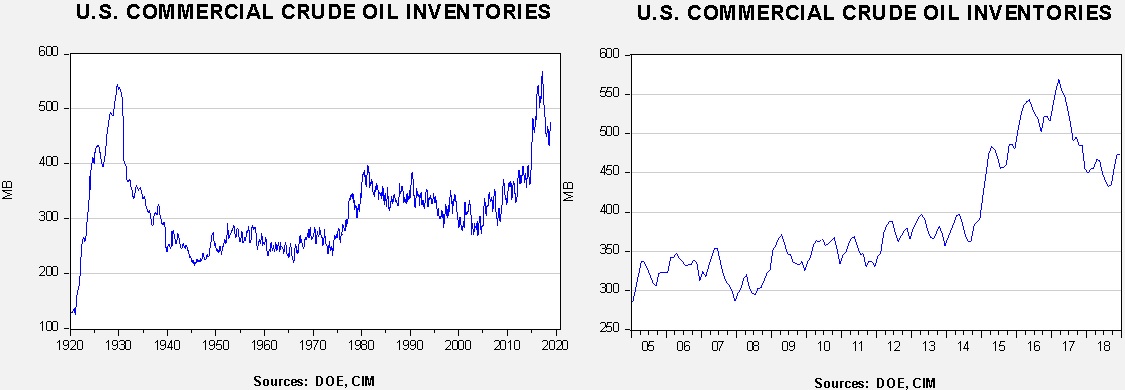

As we discuss below, this week’s DOE data was decidedly bearish as crude oil inventories rose sharply. We are seeing steady to higher oil prices this morning, in part due to the fact that oil and equities have been positively correlated recently (both are reflecting sentiment about economic growth), and probably also on expectations of at least a short-term disruption of oil flows from Venezuela. We also note that Venezuelan bonds, many of which are in default, are rallying on hopes that Maduro will go and the new regime will be willing to restructure and service the bonds.[6]

Fed policy: Two items of note. First, the FOMC is reconsidering its balance sheet normalization plan and may end its reduction much sooner than planned.[7] Our position on the balance sheet is that the actual impact is difficult to determine, but the primary value of QE was psychological; it showed the Fed still had policy tools available even after the fed funds target hit zero.[8] Although we doubt stopping the reduction of the balance sheet would have any “real” effects (other than to keep bank reserves excessive and keep the money multiplier and velocity depressed), there will almost certainly be a positive reaction in financial markets due to the psychological effects. Second, reflecting comments we have made recently about the two open governor positions, the administration signaled it is “looking for doves.”[9] This adjustment is very important because the appointment of two committed doves would weaken the Fed’s ability to hike rates. Although not set in stone, two persistent dissents from governors would tend to undermine Powell’s position and could lead to his resignation.[10]

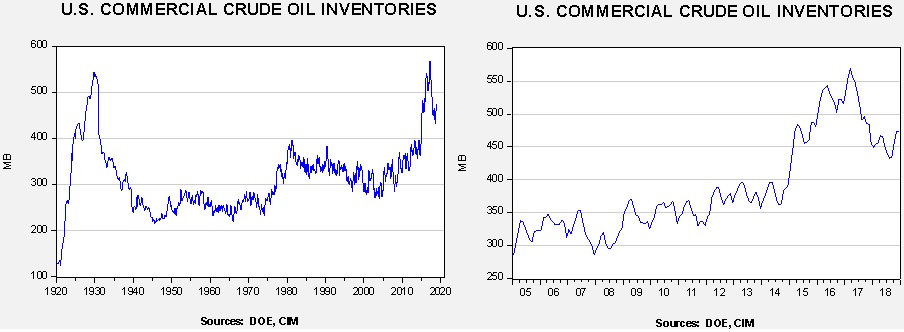

Energy update: Crude oil inventories rose 8.0 mb last week compared to the forecast decline of 0.5 mb.

In the details, estimated U.S. production was unchanged at 11.9 mbpd. Crude oil imports jumped 0.7 mbpd, while exports fell 0.9 mbpd. Refinery runs declined 1.7% and should continue to fall in Q1. Gasoline stocks continued to rise while distillates fell, likely reflecting increased demand for heating oil.

(Source: DOE, CIM)

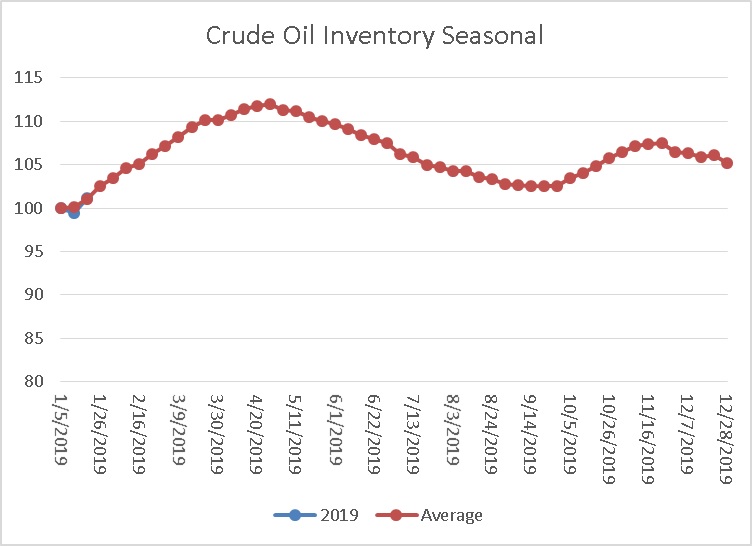

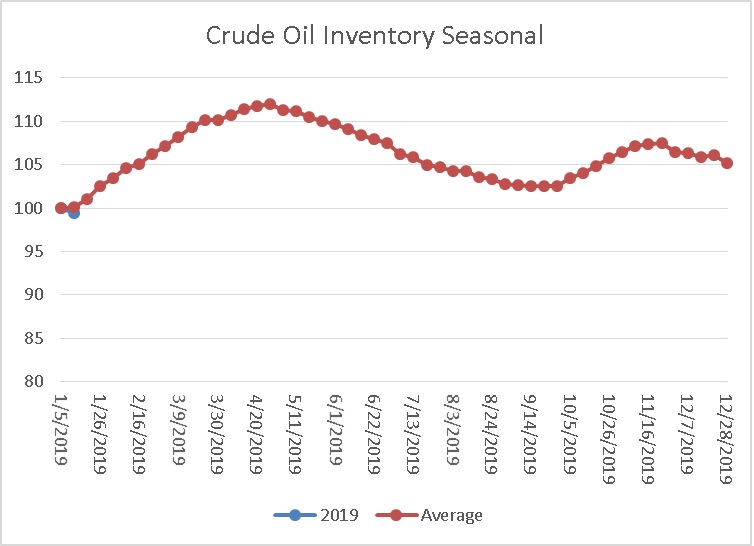

This is the seasonal pattern chart for commercial crude oil inventories. We would expect to see a steady increase in inventories that will peak in early May. This week’s increase, though well above expectations, was mostly in line with seasonal norms.

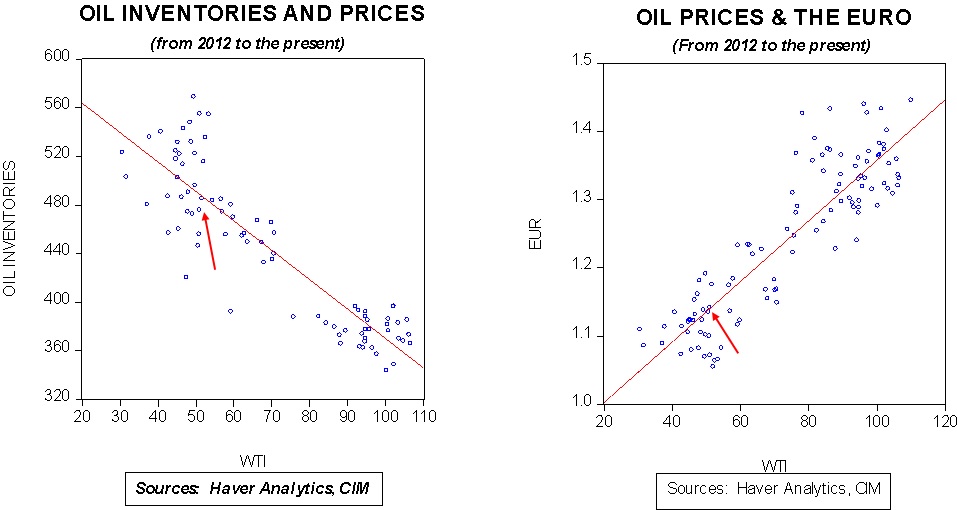

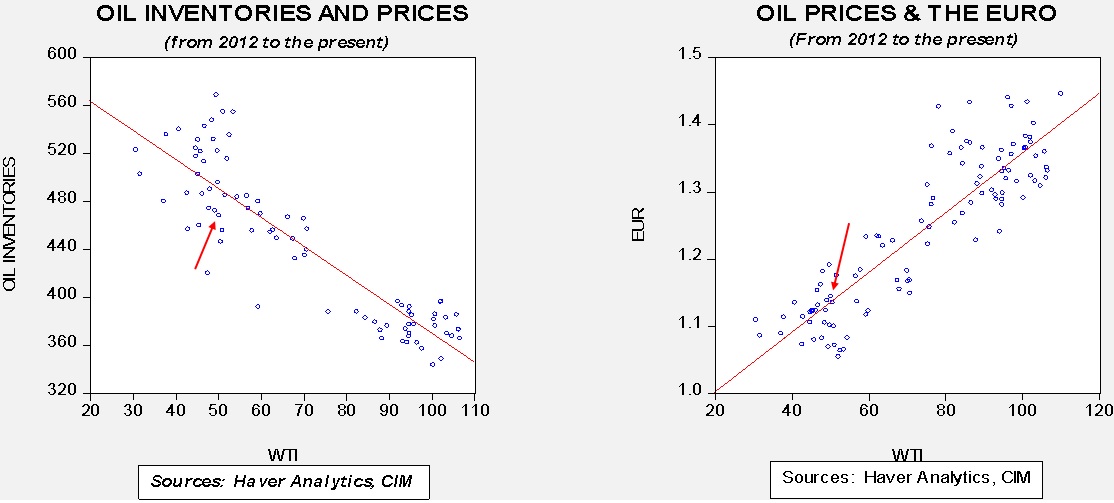

Based on oil inventories alone, fair value for crude oil is $59.05. Based on the EUR, fair value is $55.52. Using both independent variables, a more complete way of looking at the data, fair value is $56.03. By all these measures, current oil prices are generally in the neighborhood of fair value. However, we still expect prices to move toward $60 in the coming weeks, but rising oil inventories will tend to be a bearish factor for the market. Still, assuming the roughly current price of $53.00 per barrel and a steady EUR, the market has already discounted a 25 mb rise in inventory levels. A rise of that level, assuming we continue to track the usual seasonal pattern, would occur in early to mid-March. If inventories rise to their normal peak and the dollar remains stable, oil prices would be fairly valued around $50.50. Thus, the markets haven’t completely discounted the normal inventory build but have assumed part of it.

If you’re like most investors, you’re probably delighted to see 2018 in the rearview mirror. It was a year in which the stock market began on a euphoric note, in a January that proved to be the last month of a nearly two-year rising market. Indeed, from February 2016 to late January 2018 the S&P 500 rose 59% (bottom-tick to top), without even so much as a 5% pullback along the way. It was enough to turn even a confirmed old bear into a frolicking bull.

But after that high on January 26, the market spent the next nine months seesawing back and forth. There were three corrections of 12%, 9%, and 12 %, respectively, with nice little rallies in between. One of those rallies lasted six months, travelled 15%, and even took the market to a new high. As we noted in our October letter, that sort of volatility, though rare in recent years, is actually normal market behavior for those with a multi-decade point of view. But then came December…

From its intraday high on December 3 to its low on the morning of December 26, the market (basis the S&P 500) fell 16%. From the September 21 peak, this decline totaled 20%. This was a much greater than normal sell-off, and caused many investors (perhaps you) to wonder if a recession was upon us. Many conversations with both advisors and clients indicated to us that is exactly what many were worried about; in particular, many were (and, perhaps, still are) worried about a return to 2008. Is that likely?

In our opinion, no. Not only do we not see a recession on the near-term horizon, whatever its character, but it most likely will not look anything like 2008. That recession was triggered by a national decline in residential real estate prices, preceded by record household debt levels (as a percentage of income), and exacerbated by a lack of liquidity (i.e., cash) throughout the economy and financial system. What’s the situation today? Real estate prices are declining in several previously “hot” markets, but that’s not unusual and it’s certainly not a national problem. (Come to St. Louis!) Household debt as a percentage of disposable income is down more than 20% from its 2008 peak, and cash is “stacked high” as banks, corporations, and households hold large quantities of cash.

This state of affairs does not mean a recession is impossible, just that it’s most unlikely that a 2008-style liquidity crisis is upon us. The next recession will more than likely be similar to those of 1991 and 2002, when prior bad investments went sour on a broad scale (commercial real estate in the former, telecom/internet investment in the latter). These recessions hurt wealthy investors, but did not produce injury to average Americans on the scale of 2008-09. We worry about recessions (a lot!), but we really don’t see one in 2019.

As noted above, the sharp sell-off last month was unusual. In fact, it’s the only 20% sell-off of the S&P 500 in the absence of a recession since 1987. That was some year! In the space of two months, the market dropped 36%; in five days it dropped 31%. It dropped 20% in one day! What do I remember most about that sell-off (besides the knot in my stomach)? It was one of the best buying opportunities of my lifetime. Sharp, steep, emotion-laden sell-offs in the absence of recessions typically produce outstanding opportunities to buy high-quality, long-term investments at quite reasonable prices, which happens to be what we at Confluence enjoy doing most. It’s emotionally difficult to be a buyer in the face of such fear, but, historically, it’s the smart thing to do.

We appreciate your confidence in us.

Gratefully,

Mark A. Keller, CFA CEO and Chief Investment Officer

[Posted: 9:30 AM EDT] Equities are rising modestly this morning. Here is what we are watching:

Venezuela heats up: Venezuela has been a problem for a while. Its economy and government have essentially stopped functioning. Hyperinflation has set in. There is a massive exodus of Venezuelans[1] to other parts of South and Central America (and, at some point, it is safe to assume they will come to the U.S. border). The state oil company, PDVSA, has been gutted by replacing competent workers with lackeys loyal to the regime; oil production has declined to 1970s levels. In fact, it is such a mess that the real mystery is why the current regime remains in power. It appears this mystery may be getting resolved. Protests in Venezuela have taken on a different tone. For years, the Chavez/Maduro leadership was able to control the country due to loyalty from the working class. Protests generally came from the middle and professional classes; the rich mostly live in Miami now. What is new is that the working classes are turning on the government. For a time, Chavez was able to funnel resources to the poor, which helped maintain support, but now the economy has become so weak that it can’t buy off the lower classes anymore.[2]

Juan Guaido, the president of the National Assembly, has declared himself interim president. The Trump administration has recognized him as the new president of Venezuela[3] and, more importantly, the military and security services are not moving against him. Regional governments have turned against Maduro, led by Brazil’s new leader, Jair Bolsonaro, but also with support from Argentina and Paraguay.[4] Maduro responded by giving U.S. diplomats 72 hours to leave Venezuela. SoS Pompeo, following the logic that Maduro is no longer president of Venezuela, indicated the diplomats would stay.[5] As we noted yesterday, the Trump administration is considering oil sanctions on Venezuela[6]; if implemented, they would remove the last prop keeping the Venezuelan economy functioning (as badly as it is). Meanwhile, Russia has warned the U.S. not to use military force against Maduro, which is, in a sense, an idle threat. There is no way Russia could maintain a major military effort over such a long distance. Instead, we would look for Russia to do its usual move in these sort of circumstances, which is to create pressure on U.S. interests where it can, e.g., Ukraine, Moldova, etc.[7] Besides Russia, Maduro’s dwindling international support comes from Turkey, Cuba, Nicaragua, Bolivia and South Ossetia (a state only in the mind of Putin).

We suspect Maduro is finished. What follows will be critical. The most pressing issue is to restart the economy, which means getting oil flowing again. The quickest way to accomplish this is to open the oil sector to foreign investment and allow foreign ownership of reserves. We doubt a new government would go quite that far, but generous production-sharing agreements would likely be a minimum. Still, it would probably take at least two or three years for output to return to the 3.0+ mbpd level it was before Chavez undermined PDVSA. The second major issue is debt; Venezuela needs to restructure its debt and will almost certainly require an IMF bailout. China and Russia, which have both become major creditors, are likely to be disadvantaged by a U.S.-supported regime.

Eventually, a renewed Venezuela will be bearish for oil prices; recovery would add 2.0 mbpd to global oil supplies. However, that recovery will take at least a couple of years. In the short run, turmoil could reduce Venezuela’s oil output even further and is thus supportive for crude.

ECB: The ECB, as expected, left policy rates unchanged. However, the press conference comments were decidedly dovish. The line from ECB President Draghi from H2 2018 was that prosperity was just around the corner. In these prepared comments, he has finally admitted that the Eurozone economy has slumped and he indicated the ECB will keep policy easy until growth and inflation rise. The EUR slumped on the news.

World growth: As we note below, flash PMI estimates from Asia and Europe were well below expectations. Eurozone PMI is now hovering just above the 50 expansion line at 50.5. Japan is sitting at 50.0, down from 52.6 in December. By its mandate, the Federal Reserve does not act as the central bank of the world but, in reality, it is because of the dollar’s reserve status. Thus, if the FOMC members are looking at a pause, world economic performance does offer an excuse for maintaining steady policy.

[Posted: 9:30 AM EDT] After a hard drop yesterday, equities are rising modestly this morning. Here is what we are watching:

The importance of trade: Equity market action on Friday and Tuesday made it abundantly clear how focused financial markets are on trade.

(Source: Barchart)

This is a five-day chart of the S&P futures. On Friday, reports that China was prepared to bring the bilateral trade deficit to zero over six years led to a strong rally, shown by the blue line. The red line shows the drop on reports that the U.S. rebuffed a Chinese offer to send officials for preparatory talks before the already scheduled meeting at the end of January.[1] However, in the afternoon, National Economic Council Director Kudlow did an interview where he indicated that trade meetings were still on, leading to the rally shown by the green line.[2]

What we suspect is happening is that the Mnuchin/Kudlow wing of the administration is battling for the “heart and mind” of the president against the Navarro/Lighthizer wing and are making dueling press statements that are affecting equity markets.[3] On the one hand, 2019 is critical to the 2020 elections; if a recession begins this year it would doom Trump’s re-election chances, and even if recovery occurs in 2020 it will likely be too late to offset the weakness that would have already occurred. This fact would suggest the president will take a deal with China that boosts optimism. On the other hand, China is now a strategic competitor. China is becoming a serious military threat to the Far East and is working to move up the value chain by dominating technology, an area that the U.S. has ruled for years. Thus, there are longer term issues of resetting Chinese relations to a hostile stance. The actions against Huawei (002502, Shenzhen, CNY 4.15) are part of that policy direction.[4] Our position is that Trump will make a short-term trade agreement with China and delay additional tariffs. However, in the long run, U.S. policy toward China will take a more aggressive turn which will disrupt global supply chains. If the president decides the long-term goal outweighs the short-term goal, then the potential for a recession and further economic weakness rises significantly.

Pressure on Venezuela: The U.S. has mostly stayed out of the turmoil hammering Venezuela. The Bush administration did make positive comments about the 2002 coup attempt that failed against Hugo Chavez but there was no evidence of active support. Subsequent administrations have applied various sanctions but avoided any that would seriously disrupt the Venezuelan oil industry (Chavez and Maduro accomplished that all on their own). Although the government has systematically undermined a divided opposition through arrests and domestic intelligence, conditions have deteriorated to the point where forces opposing the government are rising under new leadership.[5] More ominously for the government, there are increasing reports of military unrest.[6] Chavez did a good job of keeping the military aligned with the regime, playing on his veteran status, but Maduro does not have the same ties. Now, it appears the Trump administration is taking a more active role to undermine Maduro.[7] The most likely outcome is a military coup which would overthrow the regime. In the short run, if the takeover is “messy” it is a bullish factor for oil; although Venezuela’s oil production has plummeted to just over a million barrels per day (it once produced over three million per day), chaos would likely reduce output to zero. However, if Maduro is ousted and the next government is supportive of foreign investment, then an eventual rise in output is very likely.

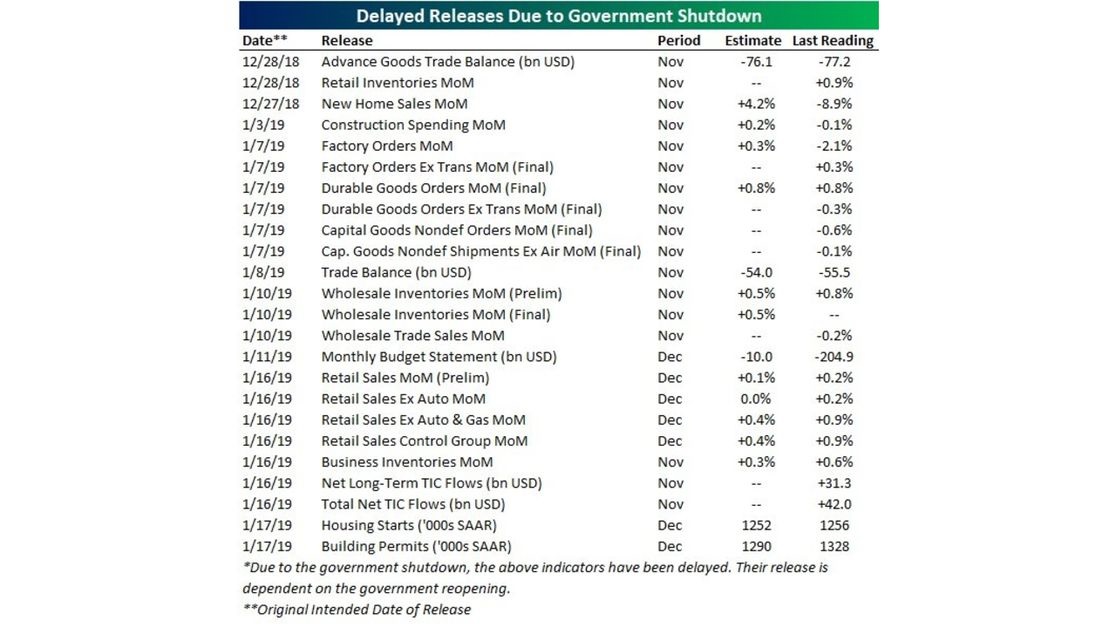

Shutdown: There is some movement on the government shutdown; the Senate is expected to vote on competing plans to temporarily fund operations.[8] We don’t expect either to pass the House or be signed into law but the fact that votes are taking place is some form of progress. There are widespread reports of government workers who are not being paid but are required to work who are not coming in. Especially critical are those working for the IRS; if they don’t go to work, tax refunds could be delayed.[9] Here are all the economic releases that have been delayed:

(Source: Axios)

Brexit: There’s not too much new to report. We are seeing tensions rise between Ireland and the EU on the border issue. Ireland wants to avoid a hard border with Northern Ireland on fears that a return to a hard border will lead to sectarian conflict. Ireland suggested it would not enforce a strict border even with a hard Brexit, while the EU indicated Ireland would need to put hard border controls in place if a hard Brexit occurs.[10] Hard Brexit supporters have argued that technology could allow for trade to be monitored without a hard border control. However, a soft border could become a headache for the U.K. as well because it could become a conduit for people to cross into the U.K. without papers being checked. Still, divisions within the EU increase the odds that the union may be more willing to adjust than it has been indicating. We are also noting softening opposition to May’s plan. Although the vote failed spectacularly last week, Brexiteers are beginning to fear that their desire for a hard break with the EU is not a majority position; in fact, the majority support avoiding hard Brexit at all costs. If the choice is to remain in the EU or May’s proposal, the latter is starting to look much better.[11] Although we fear a hard Brexit could occur because neither the EU nor the U.K. will budge, there is some evidence of movement that is raising hope for a more orderly outcome. That factor is why the GBP is doing better. Meanwhile, we continue to hear reports of firms leaving the U.K. on fears of a hard Brexit.[12]

[Posted: 9:30 AM EDT] Welcome back from the long weekend. Equities are in the red this morning mostly on worries about global growth. Here is what we are watching today:

The IMF, global growth and Davos: The IMF has reduced its world growth forecast to 3.5% for this year (down 0.2% from its October estimate) and 3.6% in 2020 (down 0.1% from October).[1] Noted concerns were widespread, including a hard Brexit, worries about Italy’s budget and global trade. The IMF noted that global direct investment fell 19% in 2018.[2] The Davos meetings are underway in Switzerland. The lineup is “lighter” than in previous years; of the G-7, only Germany, Italy and Japan are sending national leaders. The U.S. has no official representation due to the shutdown. PM May and President Macron are not at the forum due to domestic turmoil. Xi Jinping and India’s Modi are also taking a pass. Although climate change is the topic of this year’s meeting, concerns about global growth are the unofficial worry.[3]

China’s GDP: Over the holiday, China announced its weakest GDP growth since 1990[4] as reported growth fell to 6.4% in Q4. In general, GDP growth in China is often overstated; a better approximation is probably closer to 5.3%, which is still rather strong but also weakening. The details of the data are worrying. They confirm that real estate and retail sales slowed. China needs to reform its economic model away from investment and exports toward consumption; slowing retail sales is bad news.

(Source: Capital Economics)

Information technology remains very robust but is slowing.

(Source: Capital Economics)

As growth slows, there is evidence that China is “returning to the one that brought you,” or construction.

(Source: Capital Economics)

Essentially, China can achieve any growth level it wants by accumulating debt. But, the Xi government is trying to deleverage in an attempt to ease bad debt and excessive investment. Unfortunately for China, it can either reduce debt or grow fast, but it can’t do both.

Xi and the CPC: In a recent speech, Chairman Xi warned of the need to maintain stability under conditions of growing stress. Although such speeches are not exactly unusual for Xi, this one seemed to be a bit more strident that normal. For the most part, China abhors chaos; throughout its history, periods of weak governance have led to either foreign invasion or internal breakdowns that led to warlords dividing the country. History also shows that the coastal regions tend to have the strongest economic growth but only during periods when the coasts are exporting to the world. The divergence between the coasts and the interior can be sources of division that undermine governance. Mao unified China by turning the country inward; thus, China was united but poor. Deng was willing to risk that division for growth; now, China has a robust economy but also severe income and regional inequality. Xi is trying to address these issues.[5] The trick is that communism, for the most part, is a spent ideology. Xi often talks in terms of a dialectic, the familiar “thesis-antithesis-synthesis” language that Marx borrowed from Hegel. What makes that construct attractive is that it implies progress—an existing system or power structure faces a threat and the threat is absorbed by taking the best of both. Of course, after that, the new synthesis eventually becomes the next thesis and the process repeats. However, there is another alternative; there is no progress and history merely cycles between two polar positions and progress is often an illusion provided by better technology. Xi is worried. Since no one really buys into Marxism anymore, the legitimacy of the CPC is mostly derived from its ability to deliver growth and improve living standards. However, that growth has led to its own problems—pollution, income inequality, etc. The last two governments have tried to address both with mixed success. But, it has become difficult to address these other issues and maintain strong growth. To do so, the party has relied on debt growth, which is now becoming problematic.

Brexit and Plan B: PM May revealed her “Plan B”; essentially,[6] it is “Plan A” with the hopes that the EU will give her some room on the Irish backstop issue. Her offer was mostly panned by the MPs.[7] However, divergences are starting to show. May has maintained all along that she cannot take hard Brexit off the table, but there is a growing rebellion among Tory MPs to do just that.[8] The official line from the EU is that there is no room to negotiate on “red lines,” which means the U.K. must stay in the customs union in order to avoid a hard border in Ireland. That position was reiterated by the lead EU negotiator, Michel Barnier.[9] However, the Polish foreign minister, Jacek Czaputowicz, suggested that May’s Brexit deal might pass Parliament if the backstop is temporary, for five years, perhaps.[10] On the one hand, it isn’t obvious that Poland is leading negotiations; on the other, the EU requires unanimity and if Poland is willing to allow a temporary backstop then there might be a crack in the EU negotiating strategy. Poland is quite interested in the Brexit negotiations as nearly one million of its citizens reside in the U.K. Poland would likely be willing to give a time limit on the backstop in return for protection for Poles in Britain. To some extent, this crack may be what May was hoping for all along.

At the same time, Labour’s Corbyn appears to be supporting a second referendum, something he has been reluctant to back. His concern is that there is some support for Brexit among the hard left (the Blair Labourites were solid on Remain) and, if a second referendum were to yield a reversal of Brexit, it might not only split the Tories but could also divide Labour.

The EU is also making it clear that it won’t extend the Article 50 deadline without good reason, and a disruptive hard Brexit isn’t a good enough reason. Only elections or a needed extension for additional Parliamentary votes will pass muster. We note that May’s widely panned Brexit strategy is getting a second look by some Brexit supporters, fearing that a rejection of May’s plan may lead to no Brexit at all.[11] Thus, the Polish offer might be enough to swing May’s coalition to her plan. Or, in the words of Monty Python, her plan’s “not dead yet.”[12]

At last, Sweden gets a government: It took 133 days from the last election but the Social Democrats have cobbled together a minority government. In the last election, the Sweden Democrats, a right-leaning, anti-immigrant populist party, won 62 out of 349 seats in the Swedish parliament. The Social Democrats bloc, a mostly center-left coalition, won 144, while the center-right coalition, led by the Moderate Party, won 143. That outcome meant the Sweden Democrats had the power to determine the next government. However, neither of the traditional coalition blocs wanted to form a government with the populist Sweden Democrats, meaning that the new government would either be a minority arrangement or the centrist blocs would need to form a grand coalition (like what happened in Germany to avoid a coalition with the AfD). The center-left formed a minority government but has gotten support from the Liberals and Center Party, who lean libertarian and are usually part of the center-right bloc. To form a government, the Social Democrats had to accept mandatory language testing for naturalized citizens, tax cuts and labor market deregulation. We doubt the government will survive a full four-year term. Both the left and right were critical of the deal but, at least for now, Sweden finally has a government.[13]

As we have seen elsewhere in Europe, centrist parties are trying to deal with the rise of populism. In France, the run-off system prevented the National Rally from winning the presidency. In Germany, it took a grand coalition that essentially emasculates the Social Democrats in order to govern. In Italy, the populists have won but both left- and right-wing populists share power, which may not survive. Although populists are not necessarily the majority, they are getting powerful enough to disrupt what has been the normal power arrangements. This is how populism has operated in proportional representation systems. In “first past the post” systems like the U.K. and U.S., populism is rapidly changing earlier arrangements. In Britain, it has led to Brexit; in the U.S., it has led the GOP to become the party of protectionism and is producing divisions in the Democrats on how to manage and regulate technology companies. Sweden is just the latest country to deal with this trend.

Equity markets struggled in 2018; although new highs were achieved twice during the year, volatility was elevated compared to 2017.

This is a chart of the CBOE VIX index, a measure of implied volatility from the equity options market. An elevated VIX means implied volatility is high, which implies a wider dispersion of expected outcomes for future equity index outcomes. As fear rises, it would make sense for investors to react. As the chart shows, for most of 2017, the VIX ranged between 10 and 15. Last year, the range was significantly wider. As fear rose, investors reacted by accumulating higher levels of cash.

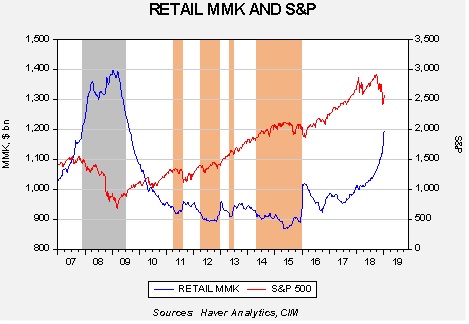

This chart shows the weekly close for the S&P 500 along with the level of retail money market funds. We have highlighted the 2007-09 recession in gray. The tan areas show periods when the level of money market funds fell below $920 bn. In this bull market, we have tended to see the upside momentum wane once money market funds fell below the aforementioned level. In other words, the market ran out of “dry powder.”

What is occurring now is completely different. Money market levels are nearly $1.2 trillion. They are rising in a manner closely resembling what we observed before the Great Recession. It appears that the level and rise of money market funds is consistent with the financial markets’ expectations of a recession. If a recession is avoided—if the trade conflict with China cools and the FOMC avoids overtightening—then odds likely favor a recovery in equities. The retail money market data suggests there is ample liquidity to support a significant rally. Of course, not all those money market funds will necessarily move back to equities. Given higher interest rates, some of it could stay in money markets. But, the key point is that financial markets appear to be in recession mode now. If recession is avoided in 2019, as we expect, the odds of a significant rally in equities is likely.

[Posted: 9:30 AM EDT] Happy Friday! Equities are moving higher this morning. Here is what we are watching today:

About those tariffs: Yesterday, equity prices were jolted higher on reports that the Trump administration was considering rolling back tariffs on China.

(Source: Barchart)

This chart shows March S&P futures; note the jump around 1:30, where the index rose 25 full points. The report came from the WSJ[1] and indicated that Treasury Secretary Mnuchin is spearheading a negotiating tactic to remove some or all of the Chinese tariffs to show good faith to Beijing and use this action to make a longer term deal. Needless to say, the Lighthizer/ Navarro wing of the party will reject this tactic out of hand. Instead, this report suggests that this story was a Mnuchin-led leak to show the president how positive equities would react to a significant reduction in trade tensions with China. If our take is correct, the real audience for the report was President Trump. The report was denied soon after and equities fell about as fast as they rose, which bolsters the case that the equity markets would look quite favorably on an easing of the trade front. At the same time, equities have been drifting higher, most likely on hopes of a trade thaw.

As we noted yesterday, there is a strong incentive on both sides for a short-term cessation of trade hostilities. China and the U.S. are dealing with slowing economic growth and President Trump is dealing with the run-up to elections in 2020. At the same time, the long-term outlook for relations between China and the U.S. is becoming a serious risk factor. Therefore, any short-term peace must be viewed in the context of problematic long-term relations.

Brexit and the EU: There really isn’t much more to say on this topic from the U.K. perspective. PM May and opposition leader Corbyn are at an impasse as the latter wants May to guarantee there won’t be a sudden exit on March 29, which she has no interesting in doing because it would remove most of her bargaining leverage.[2] Thus, British politics is in deadlock with no clear way forward.

Meanwhile, the EU is discovering Wilde’s observation.[3] The EU did not want to make the U.K. exit easy. Its leaders feared that a smooth exit would encourage others to leave the EU as well. The EU especially didn’t want to give the impression that a departing country could deal with the EU on an “a la carte” basis, picking the parts it wants and rejecting the rest. In the case of Britain, the EU has made it clear that the only way to have access to the free trade area is to accept the free movement of peoples within the EU. Given that goal, the EU plan has worked splendidly. The U.K. is in political chaos and the potential for a hard Brexit, which is only wanted by a minority, is rising.

However, the EU is discovering there are costs to it as well. The economic disruption from a hard break will hurt the U.K. significantly as 40% of its trade is with the EU, but that also means it will be disruptive to the EU. In addition, a U.K. out of the EU changes the balance of power within the union; France has been moving quickly to fill the void created by London’s exit. France has always viewed the EU as a force multiplier for its policy goals but the rise of Germany and the U.K.’s inclusion, along with the massive increase in the union with the addition of Eastern European nations, has diluted France’s impact. In addition, the U.K. is important to continental security as most of Europe has weak militaries. A U.K. separate from the EU makes Europe less safe.[4] Unfortunately for the EU, there really isn’t anyone to negotiate with in the U.K. PM May was politically damaged by the historic loss of her Brexit plan; if anyone else wanted to be PM, they surely should be able to win after that drubbing. However, Parliament also showed that Corbyn isn’t a popular replacement. Now, if the EU wants to avoid a U.K. exit, it isn’t clear who they would tell.

Financial markets are mostly convinced that both sides will agree to extend the March 29 deadline. For now, we agree that such an extension makes sense. However, it is important to note that EU Parliamentary elections will be held in May. It would be rather awkward for the U.K. to participate given that it wants to leave but, if the deadline is extended, it may be hard to prevent British voters from casting ballots for representatives who, at some point, will no longer be in the EU. In addition, the EU is facing its own demons. The European Parliament has backed a plan to make EU fund access conditional to nations that “back the rule of law.”[5] That is a direct swipe against Hungary but also other Eastern European nations, such as Poland. The EU is finding it difficult to integrate both Western and Eastern Europe; funding support is one lever the West can use against the East.

Goodfriend out? In November 2017, President Trump nominated Professor Marvin Goodfriend to the Federal Reserve Board of Governors. The choice always seemed odd to us. President Trump has made it abundantly clear he wants a dovish FOMC and Goodfriend is a hawk. Goodfriend’s positions were always controversial, but one policy he supported was a codified 2% inflation target; since there is no codified unemployment rate, a congressional mandate for 2% (or less) inflation would turn the Fed into the Bundesbank or its successor, the ECB. Again, one can make a perfectly reasonable argument for ending the dual mandate because it can put the Fed into a position where meeting one target necessarily requires violating the other. But, if one wants a perpetually dovish Fed, a codified 2% inflation mandate isn’t the way to accomplish this goal. So, we have been expecting the president to nominate someone else.[6]

One factor in the choice of filling open governor seats has been the evolution of the Trump presidency. All presidents tend to lean on experienced advisors early in their terms. Thus, the first cabinets and advisor groups tend to be “all-stars” from the major political parties. However, these all-stars also have their own policy agendas and use their White House positions to achieve these agendas.[7] Over time, presidents realize the goals of the all-stars can differ from those of the president. For example, President Obama’s foreign policy was spearheaded by Hillary Clinton in his first term; in his second term, Ben Rhodes was the leader. The Fed governor selections, thus far, appear to be centrists out of central casting, likely recommended by Treasury Secretary Mnuchin. Trump has two remaining vacancies; we expect the president to take control of these open positions and pick two doves. Although we have seen no indications, we would offer Minneapolis FRB President Kashkari and St. Louis FRB President Bullard as dovish candidates who would likely make it through the nomination process. Two doves would seriously undermine Chair Powell’s attempts to raise rates as two governor dissentions would make the chair look weak and likely lead to his resignation.

Oil talk: The potential for additional sanctions on Venezuela is leading some Gulf Coast refiners to scramble for heavy crude. Crude oil comes in grades based mostly on viscosity (heavy/light) and sulfur content (sour/sweet). Gulf Coast refineries invested heavily in equipment that would allow them to efficiently process heavy/sour crude oil, which is usually cheaper than light/sweet. However, fracked oil tends to be light/sweet, so the bulk of the new U.S. output isn’t ideal for these refiners. The two primary sources for heavy/sour have been Mexico and Venezuela. The former has seen production steadily decline, while the latter is not only facing falling output but sanctions could further reduce supplies.[8] This has led several oil companies to quietly inform the White House that further sanctions on Venezuela may be counterproductive. Meanwhile, the State Department is clarifying its positon on Iranian sanctions waivers. It looks like five nations will get further waivers, three will be cut off and Iranian oil exports will be capped at 1.1 mbpd.[9] If true, that would reduce the odds of a major supply disruption.

[Posted: 9:30 AM EDT] Equities are drifting lower this morning. Here is what we are watching:

Brexit: After facing the largest defeat in modern Parliamentary history, PM May survived a no-confidence vote but not by a great margin.[1] We have been discussing Brexit at length, so we don’t have much to add this morning. But, here are a few points:

To some extent, Brexit is probably signaling realignments within the major U.K. parties.[2] Although it’s still unclear what exactly the British want, we think there are majorities for two goals—leaving the EU for border protection and having as little trade disruption as possible. To achieve those goals, the U.K. political system needs to realign, with centrists in both Labour and the Conservatives banding across party lines to build a Brexit that people can live with. Perhaps the Liberal party makes a resurgence as the home for these potential defectors. But, it looks like neither Labour nor the Tories, as currently constituted, can come up with a workable solution.

The EU isn’t giving anything more to the U.K. They want the British to offer a new plan. And, the EU is starting to make active plans for a hard Brexit. Overall, a hard Brexit won’t be pleasant for the EU either.[3]

Given the uncertainty on both sides, it is reasonable to think that the March 29 exit date will be delayed.[4] However, that will require a change on the part of the EU, which has indicated it won’t give an extension without a good reason, e.g., new elections, new referendum, new plan. We suspect this is a bluff on the EU’s part, but it is possible that the lack of a Plan B from London and intransigence from Brussels will lead to a hard Brexit. The financial markets are probably underestimating the chances of this outcome.

Trade and China: One the one hand, we are seeing talks progress. Vice Premier Liu has confirmed he will visit the U.S. for talks at the end of the month.[5] On the other hand, actions against Huawei (002502.sz, CNY 4.23) and other Chinese tech firms are accelerating. There is legislation in Congress designed to ban the sale of U.S. components to Chinese companies that violate U.S. sanctions or export control laws.[6] These laws would force the administration to reduce tech trade between China and the U.S. Meanwhile, the DOJ is investigating Huawei for stealing trade secrets.[7] Essentially, U.S. and Chinese negotiators are trying to make some sort of trade deal while there are active steps being taken to restrict technology trade between the two nations.[8] Although this would seem to doom current talks, we think both Presidents Trump and Xi are working on two time frames, short term and long term. In the long run, both leaders realize the relationship between China and the U.S. is fracturing into a classic established versus rising superpower clash, a factor that will dominate the next decade. However, in the short run, both need a deal that will boost confidence and economic activity. Xi can clearly see that the Chinese economy is slumping and needs trade relief. Trump can clearly see the U.S. economy is slumping and needs something to bolster confidence. Thus, we can have a short-term agreement in the midst of what may turn out to be the next major global conflict.

On a side note, President Trump’s obsession with trade tariffs remains unabated. He is expected to threaten car sanctions on the EU in order to open European agricultural trade.[9] The EU has opposed opening the European market to American agriculture because it would upset the delicate system of preferences and subsidies that maintains peace in the EU.[10]

A depressed Beige Book: The Federal Reserve released the Beige Book yesterday, which is an overall survey of economic activity at the regional district level. Although eight of the 12 district banks reported “modest to moderate” growth levels, and all reported tight labor markets, company sentiment is weakening on trade uncertainty and financial market volatility. We note that many of the regional Fed manufacturing reports have weakened recently as well. We suspect the Beige Book report reflects the recent shift of a pause in tightening.[11]

An important defense signal: Germany is nearing a decision on replacing the Luftwaffe’s 85 Tornado fighters, a mid-1970s air platform.[12] Berlin is considering either the Typhoon, an Airbus (EADSY, USD 26.37) plane built by a group of European nations, or one of three American platforms, the F-35, F/A-18E/F or the F-15E. Selecting a U.S.-built aircraft would be welcomed by the Trump administration and might ease trade tensions. However, shunning the Eurofighter will likely doom Airbus’s defense business to near irrelevance. To some extent, it all comes down to Germany’s perception of NATO and future relations with the U.S.[13] If Germany sees Trump as a “one-off,” a political accident that won’t be repeated, then it should select a U.S. airframe. The Typhoon can’t carry nuclear weapons and thus can’t fulfill its treaty obligations with the U.S. that state European nations must provide aircraft for U.S. pilots carrying American nuclear missiles to protect Europe. On the other hand, if Germany views Trump as a symptom of a deeper retreat from U.S. hegemony, a reflection of a trend rather than a fluke, then it will likely choose the Eurofighter, the Typhoon, because Europe will need its own indigenous airframe as the relationship with the U.S. becomes uncertain. We will be watching to see what Germany decides in the coming months.

Tsipras survives: Greek PM Tsipras survived a no-confidence vote following the name-change vote in Northern Macedonia. The margin was close, 151-148. It looks like Greece will be heading toward elections soon as Tsipras is now running a minority government.[14]

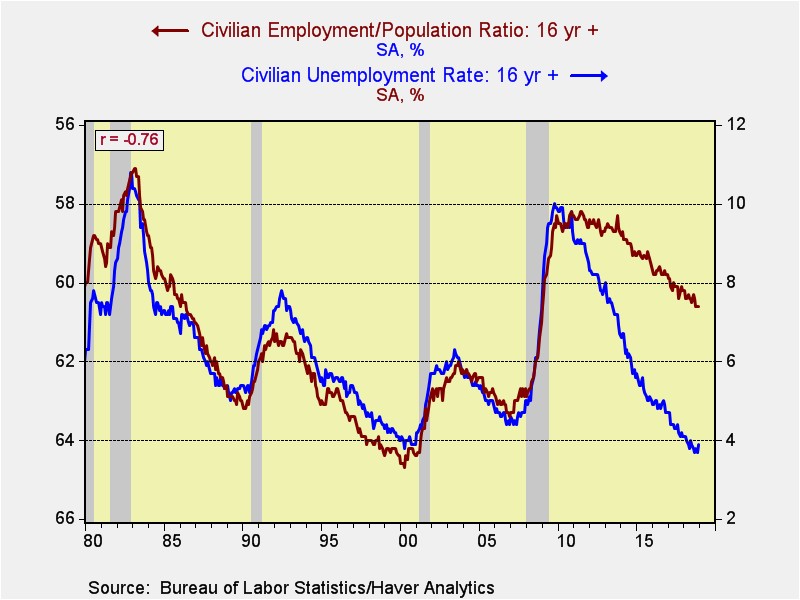

A take on the labor markets: One of our most iconic graphs in this recovery has been the divergence between the employment/population ratio and the unemployment rate.

From 1980 to 2010, the correlation between these two series was -95% (the employment/population ratio scale is inverted on the above graph). Adding the next eight years has reduced the correlation to the current level of -76%. This chart represents the biggest unknown for monetary policymakers. If the unemployment rate is the accurate representation of slack in the economy then the policy rate is too low and the Fed needs to tighten aggressively. If the employment/population ratio is actually the better measure of slack then the Fed has achieved policy neutrality.

Confirming data supports both sides of the argument, although the preponderance of data tends to favor the employment/population ratio. Until recently, wages have been stagnant and it is unclear whether the recent rise is due to demand or minimum wage legislation. The labor force has tended to rise even when the unemployment rate would suggest that additions to the labor force should be difficult. On the other hand, the JOLTS report shows that hires exceed job openings by a persistently wide margin.

A recent report from Axios[15] suggests that firms, facing a tight labor market, have taken unusual steps to draw the long-term unemployed back into the labor market with training and other forms of unconventional job support. These include helping homeless people find housing, reliable transportation and childcare as part of the hiring process. This population includes the recently incarcerated[16]or currently incarcerated.[17]

These reports suggest there is much more slack in the labor market than the unemployment rate indicates. It is true that reducing this slack will depress profit margins; firms are required to deploy measures to find and employ these workers, costing money that they otherwise wouldn’t have to spend. But, socially, this is a trend the Fed should support.

Energy update: Crude oil inventories fell 2.7 mb last week compared to the forecast decline of 2.5 mb.

In the details, estimated U.S. production rose 0.2 mbpd to a record 11.9 mbpd. Crude oil imports fell 0.3 mbpd, while exports rose 0.8 mbpd. Refinery runs declined 1.5% and should continue to fall in Q1. Product inventories rose significantly and the rise in product stockpiles will soon lead to a seasonal decline in refining activity.

(Source: DOE, CIM)

This is the seasonal pattern chart for commercial crude oil inventories. Starting next week, we would expect to see a rapid increase in inventories that will peak in early May. If we follow the usual pattern, oil inventories will peak at 489 mb (excluding pipeline oil; including this oil adds approximately 31 mb, putting the total estimate at 520 mb). Last year, inventories didn’t rise mostly due to oil exports. We will be watching to see if that pattern repeats this year.

Based on oil inventories alone, fair value for crude oil is $61.61. Based on the EUR, fair value is $56.08. Using both independent variables, a more complete way of looking at the data, fair value is $57.37. By all these measures, current oil prices are generally in the neighborhood of fair value. However, we still expect prices to move toward $60 in the coming weeks.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.