[Posted: 9:30 AM EDT] Markets were mixed this morning as rising tensions in the Middle East have caused oil prices to increase, while a softening of rhetoric by the president has restored optimism for a possible trade deal between the U.S. and China. Here are the stories we are following this morning:

War in the Middle East? Earlier this morning, Saudi Arabia reported drone attacks on Saudi Aramco pumping stations, representing more escalation of tensions in the Middle East. Over the weekend, Saudi Arabia and United Arab Emirates vessels were attacked. No one has come forward to take responsibility for the attacks, but the U.S. has indicated it believes Iran was likely responsible for the latter.[1] There are also rising tensions surrounding the Strait of Hormuz, the body of water located between the Persian Gulf and the Gulf of Oman. The strait is crucial for oil and natural gas shipments, and Iran is strategically in place to control the body of water. Last month, Iran threatened to restrict trade within the strait following the White House’s decision to not renew sanction waivers for countries that still depend on Iranian oil.[2] Tensions between the two countries appear to have reached a boiling point. Although the U.S. has not fully concluded Iran was responsible, it appears the U.S. is already preparing its military for a possible response. And, the Pentagon has already drawn up a military plan in case American troops are attacked.[3] At this point, it is unclear whether war is imminent but Iran and the U.S. are walking a very delicate line and neither side wants to look weak. We will continue to monitor this situation.

Double trouble for Big Tech? Yesterday, big tech made headlines after the Supreme Court agreed to rule on a case involving Apple (AAPL, $185.72) and as more democrats are advocating for increased regulation.[4] The Supreme Court ruled that it would allow a lawsuit about whether the App Store violated anti-trust laws by banning iPhone users from purchasing apps outside of its store. The ruling overturned a 1977 ruling which argued that consumers could sue the owner, in this case the developer, if its prices were considered inflated. This move by the Supreme Court suggests they believe big tech firms have too much control over their platforms. This comes in light of online retailers like Amazon (AMZN, $1,822.68) being scrutinized for their anti-competitive practices.

The increased politicization of tech firms is further evidence that the country is shifting from an efficiency cycle back to an equality cycle. Although we don’t expect a change to happen overnight, we expect capital to lose some of its control over the political system as candidates find it harder to garner support without appealing to the extremes of the political spectrum. So far, three high-profile democratic candidates, Kamala Harris, Joe Biden and Elizabeth Warren, have stated they would support increased regulation of big tech. An escalation of rhetoric regarding big tech would likely weigh on equities.[5],[6],[7]

Carrot and stick: Following the release of a list of $300 billion of Chinese goods that could potentially be hit with a 25% tariff if trade negotiations continue to be prolonged, the White House gave markets a glimmer of hope by confirming that President Trump will meet with Chinese President Xi Jinping at the G-20 meeting next month. Markets have come under pressure as the U.S. and China continue their tit-for-tat tariff exchange. In addition, President Trump is likely feeling pressure from members of his own party as farmers continue to bear the brunt of this trade war.

On May 10, 2018, Nicolas Maduro was reelected as president of Venezuela. However, there were numerous irregularities during the vote and, as such, the U.S. and the Organization of American States (OAS) refused to view the election as legitimate. Shortly after Maduro was officially inaugurated on January 10, 2019, the National Assembly, which is controlled by Maduro’s opposition, declared Maduro’s election illegitimate and, following the Venezuelan constitution, installed Juan Guaido as the interim head of state until new elections are called. More than 50 nations have acknowledged that Guaido is the legitimate head of state; however, Maduro, supported by China, Nicaragua, Russia, Turkey and Cuba, remains in Miraflores Palace, the official residence of the Venezuelan president.

As a result, since late January, Venezuela has had two leaders. The U.S. has increased sanctions on Venezuela, including the overall economy and on individuals in the Maduro government. However, the impact of sanctions is somewhat limited given the terrible state of the Venezuelan economy. In addition, Venezuela has become something of a proxy conflict between the U.S. and Russia, with both sides allied with other nations. In a sense, Venezuelans have lost some degree of control over their destiny, complicating matters.

In Part I of this report, we will offer a short history of Venezuela to give readers some context to the current situation. In Part II, we will examine the opposition’s attempts to oust Maduro, the problems the opposition faces in removing the current leader and the interests of foreign players. As always, we will conclude with market ramifications.

[Posted: 9:30 AM EDT] Good morning, all! Equities are soft this morning due to rising tensions in trade and the Middle East. Here are the stories we are watching:

China responds: This morning, China decided to impose tariffs on $60 billion of U.S. goods starting June 1. The decision was expected after the U.S. raised tariffs on Chinese imports last week. The escalation in trade tensions will persist as President Trump continues to ratchet up pressure on China to secure a deal before he starts campaigning for reelection. The sides were rumored to be close to an agreement as recently as 10 days ago, but negotiations took a turn for the worse after the U.S. accused China of reneging on the deal. The trade tensions will likely weigh on exported goods such as soybeans.

Oil tankers attacked: On Sunday, two oil tankers from Saudi Arabia were attacked as the vessels were approaching the Strait of Hormuz. It was also reported that four vessels from the United Arab Emirates (UAE) were sabotaged one day prior. Although no group has come forward to take responsibility for the attack, it is widely perceived that Iran may have had some involvement due to Saudi Arabia’s and the UAE’s relationship with President Trump. Iran has vehemently denied any involvement in either incident but has warned against “adventurism” within the region.

The rise of U.S. military presence within the Middle East may have added to mounting geopolitical risks in the markets. Last week, in response to intelligence gathered by allied forces, the U.S. deployed military forces into the region in order to counter an escalation in Iranian aggression. According to the intelligence, Iran has been mobilizing forces in Iraq and Syria in order to provoke the U.S. into military overreaction. Intelligence officials believe Iran wants to escalate tensions in order to boost domestic nationalism as sanctions continue to weigh heavily on the economy. Continued escalating tensions would be supportive of oil prices.

Car tariffs: On May 18, President Trump is expected to announce his decision on whether to impose tariffs on car imports and components. In February, Trump received a report from Commerce Secretary Wilbur Ross about the possibility that autos represent a national security risk. The president could use section 232 of the Trade Expansion Act to impose tariffs on cars in the same way he used it to impose tariffs on steel and aluminum. Thus far, the report has not been made public but it is speculated to have concluded that autos do represent a security risk. If true, this would be a serious escalation in trade tension with the U.S. and its allies, namely Europe, South Korea and Japan. In addition, this could hurt automakers domestically as tariffs could potentially disrupt global supply chains.

The threat of rising trade tensions have put U.S. allies on edge as they struggle to deal with growing American protectionism. South Korea, which has already renegotiated its trade deal with the U.S., is expected to ask for an exemption from the tariffs. The EU, on the other hand, is expected to respond with tariffs of its own. As global trade tensions continue to rise, we expect equities to suffer as uncertainty will deter business investment.

Fed news: Over the weekend, it was revealed that the White House is considering nominating Judy Shelton to the Federal Reserve Board. She was a former economic advisor to the president and is known for her support of a return to the gold standard. Her nomination would be unique due to the fact that people who support the gold standard are generally hawks and the president was believed to be looking for doves to fill the vacant board seats. That being said, a return to the gold standard would be supportive for a stable trade balance. We suspect Judy Shelton’s nomination could be a sign that the trade hawks, such as Wilbur Ross and Peter Navarro, now have the president’s ear. If Judy Shelton is nominated we expect her to be confirmed rather easily as she does not have the baggage of the previous two nominations.

In other Fed news, Minneapolis Fed President Neel Kashkari stated on Friday that the Fed should take income inequality into account when deciding whether its goal of maximum employment is being met. Income inequality has become a pressing issue following the financial crisis and Kashkari’s support for including it in rate decisions suggests that he favors holding rates at their current level or possibly easing.

While the financial industry is rife with performance comparisons to selected benchmarks, the most important investing goal for the majority of clients is a return above inflation that avoids catastrophic losses. Although beating the S&P 500 is a nice goal, solely focusing on that outcome may lead an investor to accept more risk than appropriate. This is an age-old issue where one confuses ends with means. Benchmarking is a means to an end. A benchmark gives investors some insight into how their investments are doing but should never be considered an end in itself. Sadly, measurement of performance seems to have eclipsed, and even replaced, the principal goals for clients. In other words, the benchmark has become the goal.

A good example of the problem with benchmarking is found in academia. Students have been told that the “4.0” is the clear marker of academic success. Now, getting all “As” is a good thing. But, anyone who has been to college knows that the GPA can be gamed. Students can fill their electives with easy courses. They can select the easiest professors in their major’s hardest courses. And, they can cheat. Or, perhaps equally as perverse, they can “know it for the test.” In other words, they can memorize the necessary information but fail to really understand it. Resolving this issue is part of hiring new graduates. There are ways to ferret out who knows their stuff and who gamed. Checking transcripts is a good way to look for clues—what were the electives and how did the candidate do in the hard classes? Another is to ask questions about the most basic components of a discipline but in a way that is rarely presented in class. An example for economists is, “Assume all drug users are addicts; what is the best way to reduce illicit drug consumption?”[1] However, how many positions are filled by candidates who are screened by GPA? In other words, how many good candidates never get an interview because their GPA fell below 3.5 because they took more challenging course work?

Let’s suppose that instead of attempting to help clients accumulate wealth within their acceptable risk tolerance, the goal was to outperform the S&P 500 Index and the criteria was what outperformed the index over the past seven calendar years. Out of the 34,468 U.S. dollar-based indices in Morningstar’s database, the sole index that met this criteria was the S&P HealthCare Equipment Select Industry Index. Naturally, exposure exclusively to this single index would be a poor investment strategy for the vast majority of clients, as it would expose them to very specific risks, yet it underscores the notion that simply striving to outperform the return of a particular index is fraught with the potential risk of a permanent impairment of capital.

(Source: Morningstar)

Another problem that arises in making relative performance the principal objective is the potential for miscreants to juggle benchmarks in order to appear successful. As an example, the table below illustrates the divergence that is associated with popular small cap growth benchmarks. While all four of the benchmarks in the table are from highly reputable providers with well-documented methodologies for the U.S. small cap growth stocks included in their indices, the variance among these four in any given year can be profound. Note that even with indices from the same vendor the differences can be significant as evidenced by the MSCI U.S. Small Cap Growth Index varying from the MSCI U.S.A. Small Growth by 244 basis points in 2018.

(Source: Morningstar)

A further complication that may be encountered is the utilization of benchmarks that incorporate significant complexity in the myriad sub-asset classes that roll up to major asset classes. The resulting information will be a hash of statistics that are of little use to either investors or advisor supervision.

These potential pitfalls do not obviate the necessity of monitoring and evaluating relative performance as part of proper due diligence. The evaluation of a manager’s portfolio or asset allocation strategy against an appropriate benchmark is an essential tool for validation of an investment thesis, which can lead to the achievement of the client’s goals. However, this can be taken to extremes. Our industry’s all-consuming fascination with performance measurement has the potential to cause actions that are perpendicular to the goal of inflation-adjusted wealth creation, such as performance chasing.

What, then, is the correct approach to ensure a manager is properly positioned in a client’s portfolio or an asset allocation strategy is appropriate to help attain the client’s goal? The most straightforward means is to evaluate a manager or asset allocation strategy against a benchmark that is objective, possesses a sound methodology, recognizable, germane to the asset class represented and free of unnecessary complexity. For this last facet, the notion of Occam’s razor applies. This approach will naturally yield significant tracking error; however, tracking error should not only be expected, but embraced, for an active manager. While on a quarter-to-quarter basis investors may observe divergent returns relative to the benchmark, during discrete, representative periods and especially through a full market cycle, an uncomplicated and recognizable benchmark will represent a solid barometer against which to measure the risk-adjusted return of a manager or investment strategy. This will serve to evaluate whether the manager or strategy is contributing to the overarching client goal. But, ultimately, the key point to remember is that a benchmark is a means to an end, not an end in itself.

[1] If all users are addicts, then the demand curve is highly inelastic. Reducing supply merely drives up the price, but reducing demand (drug rehab, substitution) could reduce demand and have the biggest effect on reducing consumption.

[Posted: 9:30 AM EDT] The tariffs were applied at midnight. Here is what we are watching:

China trade: As the president promised, tariffs on trade with China were applied at midnight.[1] Interestingly enough, financial markets took the news in stride, with equities up across the world…until a series of early morning tweets from the president indicated a high level of comfort with tariffs, in general, and included a threat to apply tariffs on all goods from China.[2] The comments reversed equities, sending U.S. futures lower.

As we have watched this issue play out this week, here are some observations we have made:

It is becoming obvious that the president views tariffs as taxes that foreigners pay. And, it has become an article of faith in the mainstream media that consumers pay the tax.[3] The reality is far more complicated. In public finance, which is a branch of economics that studies government spending and taxing activity, who ultimately pays the tax is called the “incidence” of the tax. With tariffs, the incidence can fall on several parties.

In its simplest form, a good reaches our border, customs officials apply a tariff and collect the fee from the buyer and the buyer passes on the tax in the final goods price. In this case, the incidence is, indeed, on the consumer.

But, if a foreign seller faces competition for his product in the nation applying the tariff, the importer may take price action to protect market share. In this case, the importer may reduce the price to offset the tariff, thus the ultimate incidence of the tax falls to the exporter.

Under conditions of flexible exchange rates, the importer’s currency may weaken. This would lower the price of the imported good, offsetting some or all of the tariff, meaning the incidence of the tax falls on the consumers in the foreign nation (who now face higher prices for all imports) and on the domestic nation’s exporters (who face a markup on their exports due to the currency appreciation).

So, what is likely to occur? The most likely outcome is dollar appreciation. Although the dollar is overvalued on a parity basis, the trade war is an outlier event and therefore nearly impossible to model. Tariffs have become increasingly less common in the postwar era; U.S. hegemonic policy tended to support free trade and flexible exchange rates undermine the effectiveness of tariffs. Consequently, the more we see “saber rattling” on trade, the greater the odds are that the dollar becomes a one-way bet. We have covered currencies since 1986.[4] And, one observation we have about exchange rates is that markets tend to focus on one factor to the exclusion of all others and that factor drives trading until valuation levels become untenable. In the early 1980s, during the Volcker era, it was all about interest rate differentials. After the Plaza Accord, trade data drove exchange rates. Interest rates made a brief return in the early 1990s, only to be eclipsed by productivity differences into the turn of the century. Interest rate differentials returned into the financial crisis, when flight to safety dominated. And, since 2009, interest rates have mostly dominated exchange rate trends. We are becoming concerned that tariffs might dominate traders’ minds in the coming months and push the dollar to levels that will undercut U.S. exporters and pressure foreign stocks and large caps. It hasn’t happened yet and, if this doesn’t occur, it will be due to the Fed moving to cut rates.

In our 2019 Outlook we focused on four potential risks to the market, with monetary policy and trade issues as the first two risks. Until recently, we felt rather confident that these two risks had mostly been addressed. The Fed had gone on hold and it looked like a trade war with China would likely be avoided. Perhaps the biggest risk to the markets now isn’t necessarily the trade issue as much as the Fed may see tariffs as inflationary and begin to make noise about raising rates. This is still a low probability event. The Fed remains data-sensitive and probably won’t move to lean hawkish without clear evidence of rising prices. And, if our expectation for a stronger dollar plays out, the chances of rising inflation diminish even further. But, if we are wrong, if the dollar doesn’t rally and the incidence of tariffs falls on consumers, then the risk to the expansion from monetary policy returns as a significant threat.

We have been paying close attention to the politics of the tariffs. This attention is mostly art and less science but we take note of local media reports, podcasts, commentary, etc. Our take, so far, is that China is being seen as a bad actor and the president has much more support for his tariff actions than is probably understood. Even in the farm belt, an area bearing the brunt of the trade conflict, the tariffs are seen as harmful but probably necessary. The only group that is consistently pro-trade is the right-wing establishment, who are committed to globalization (the left-wing establishment is also pro-trade but is a less vocal supporter). The U.S. has been steadily becoming anti-trade. Note that both TPP and TTIP failed to progress even though, from a geopolitical viewpoint, both would have led to U.S. trade dominance, at least in terms of setting rules. To some extent, this shift against trade makes sense. Trade becomes popular when inflation is considered a problem. With inflation being low and controlled for a long time, support for policies that reduce inflation would be expected to wane. The other factor we note is that, in a hyper-partisan era, there is a great deal of cross-party support for actions against China. The lack of political fallout for tariffs, even if it has some negative effects on the economy, will likely embolden the president further. Thus, it would be unwise to think the trade conflicts are going away anytime soon. If anything, the EU is next; we would expect something on auto tariffs with the EU next week[5] and increasing trade tensions with Europe.[6]

If our analysis of the politics is correct, at least initially, the negative impact from tariffs on equities may be limited. To some extent, multiples are a reflection of sentiment, and if there is a “rally ‘round the flag” moment with tariffs then equities may be able to offset the potential loss of margins from deglobalization by multiple expansion. Tariffs are, in isolation, bearish for stocks but the negative impact may not be extreme until a clear adverse impact on the economy becomes evident.

North Korea: As the Kim regime tests short-range “projectiles” the U.S. has seized a coal ship, which the administration says has been used to avoid sanctions.[7] We have no doubt that North Korea has been systematically working to evade sanctions, but the timing of this seizure will heighten tensions.

China and grain: China says it will have a bumper soybean crop this year.[8] If true, that would mitigate the price effects of tariffs on U.S. grain imports. However, the USDA reports that China could be facing a new foe, the armyworm, a pest that would affect all its crops.[9] If the pest spreads, it would have an adverse effect on China’s crop production and force it to import more corn and soybeans, just when it is restricting U.S. grain due to the trade conflict.

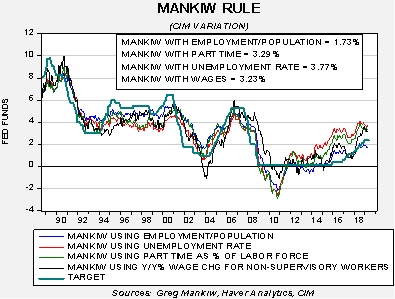

Mankiw Rule update: The Taylor Rule is designed to calculate the neutral policy rate given core inflation and the measure of slack in the economy. John Taylor measured slack using the difference between actual GDP and potential GDP. The Taylor Rule assumes that the Fed should have an inflation target in its policy and should try to generate enough economic activity to maintain an economy near full utilization. The rule will generate an estimate of the neutral policy rate; in theory, if the current fed funds target is below the calculated rate, then the central bank should raise rates. Greg Mankiw, a former chair of the Council of Economic Advisers in the Bush White House and current Harvard professor, developed a similar measure that substitutes the unemployment rate for the difficult-to-observe potential GDP measure.

We have taken the original Mankiw Rule and created three other variations. Specifically, our models use core CPI and either the unemployment rate, the employment/population ratio, involuntary part-time employment and yearly wage growth for non-supervisory workers. All four compare inflation and some measure of slack. Here is the most recent data:

This month, the estimated target rates were little changed. Three of the models would still suggest the FOMC is behind the curve and needs to be increasing the policy rate. However, the employment/population ratio suggests a rather high level of slack in the economy and would suggest the Fed has already lifted rates more than necessary. Given the uncertainty in the economy, coupled with political pressure, we expect the FOMC to remain on the sidelines.

Odds and ends:Treasury Secretary Mnuchin has been more sensitive to the exchange rate issue than the rest of the administration. He clearly sees that foreigners could respond to tariffs with depreciation and has warned nations against it. Vietnam has been duly warned.[10] Canada has just noticed that the capital flight that has led to a real estate boom in select cities may have been with laundered money[11]…what a shocker![12]

[Posted: 9:30 AM EDT] Trade concerns remain, while tensions with Iran increase. Here is what we are watching:

China trade: Although Chinese negotiators are meeting with U.S. officials today, it appears we are heading toward tariffs at midnight EDT tonight. China has vowed to retaliate.[1] In a speech (granted, at a rally), President Trump accused China of “breaking the deal.”[2] We have been seeing more color around the decision-making process in both countries. When the written agreement went to Chinese officials, they realized it would require changes to the law; China apparently had assumed it could make adjustments through regulation, which would be easier to enact but also less difficult to reverse.[3] It’s likely that, from the Chinese perspective, this adjustment met the spirit of the deal without the difficult process of new legislation. From the American perspective, this was a deal breaker. In reality, this is rather classic diplomatic behavior, called “strategic ambiguity,” where two parties say the same thing but each interprets it as something different. USTR Lighthizer would be sensitive to such tactics and would likely see it as an attempt to circumvent monitoring and penalty (and he is probably correct in that assessment).

Another element that may have led to China’s behavior is the perception that the U.S. economy may be faltering, undermining the U.S. bargaining position. President Trump’s persistent attacks on the Fed may have created this impression.[4]

So far, the financial markets have reacted with caution but not panic. This may be due to what the NYT calls the “Trump put,” which means that every time equities run into trouble the president takes steps to lift confidence.[5] We don’t disagree with this observation. What one has to be careful with is the reason a Trump put might exist. If the president believes a bear market would weaken his chances at re-election, then relying on it makes sense. But, if the president concludes that playing tough with China is even better for his re-election, then the put might not be as reliable as the market seems to believe.

We note the president has suggested that China (and we believe the EU as well) may very well be playing a stall game,[6] where they try to push negotiations into 2020 with the idea that the White House will want to avoid the disruption of a trade conflict in an election year, or in hopes that a change in power might lead to a less confrontational trading partner. We think Trump has a point here, but not the one he is making. An establishment candidate would likely want to return to the pre-Trump multilateral trading system and would almost certainly not engage in the sort of tariff tactics deployed by the current administration. However, a populist Democrat might very well conduct policy in a fashion similar to Trump and may be even more aggressive. After all, we doubt a Sanders or Warren White House would have anyone resembling Steve Mnuchin in the cabinet. The key point here is that if it becomes a campaign strategy to make statements suggesting China and the EU want to negotiate with a “weak Democrat,”[7] then the Trump put may not be as certain as financial markets seem to believe.

To some extent, the tradeoff between the Trump put and the trade warrior stance may come down to the degree and distribution of pain that occurs from a trade war. The first element of risk is Chinese retaliation. China is nearly out of U.S. imports to apply tariffs, so its next step would be to deny investment and simply not buy certain (politically sensitive) goods. This is really bad news for the agriculture markets and probably a loser for companies with extended supply chains into China.[8] The second element of risk comes from the U.S. tariffs themselves. Up to now, most of the incidence of the tariffs has mostly affected primary and secondary goods, with less direct impact on consumer goods. But, as the tariffs widen, the impact on consumers will become more direct.[9] Winners could be foreign companies that directly compete with the U.S. for the Chinese market and foreign commodity suppliers, e.g., Brazil and Argentina.[10] At the same time, a trade war between the world’s two largest economies creates a good bit of collateral damage. World trade appears to have suffered.[11]

The bottom line in all of this is that the financial markets’ rather sanguine approach to the trade spat is probably based on the notion of a Trump put. Clearly, the president’s pattern of behavior fosters this idea. But, our fear is that the put is based on the president’s perception of political benefit, so things could get rocky if he concludes that a trade war brings him more benefit than an ebullient stock market. In addition, as we have stated before, wars occur due to miscalculation. We think China has misunderstood Trump. Although we doubt Beijing will hear us, they should really read about the archetypes of American foreign policy. Embarrassing a Jacksonian is a really bad idea.[12]

The Iran issue: Although the EU is trying to hold the nuclear deal together, we doubt it will work.[13] The EU is caught between Iran and the U.S. and has more to lose by not toeing the American line.[14] The U.S. has broadened sanctions on Iran,[15] further isolating the Iranian economy.[16] Meanwhile, Iran has indicated it will begin to enrich uranium again if the Europeans don’t support the Iranian economy, which would essentially scotch the deal. One other item of note—there are reports, so far not confirmed from mainstream sources, that an Islamic Revolutionary Guard Corps (IRGC) commander has defected.[17] Brigadier General Ali Nasiri ran the IRGC protection bureau, which performs some of the Secret Service protective functions for the Iranian regime. There are rumors that he carried “sensitive” documents to a Gulf state embassy when he defected. We will be watching to see if the report emerges in the Western media in the coming days.

Brexit: PM May survived another leadership challenge, indicating that there really isn’t an obvious alternative to her in the Tory Party. She indicated that another Brexit vote will likely be held in a couple of weeks.[18]

Odds and ends: Cyril Ramaphosa won yesterday’s poll but the margin of victory was the lowest since the end of apartheid.[19] North Korea launched more “projectiles.”[20] Although Venezuela has defaulted on most of its bonds, it continues to pay on a portion of its debt, the bonds of Citgo and those held by Russia. The former is being paid to avoid creditors seizing its refining assets in the U.S., while the latter is to keep Russia as an ally.[21]

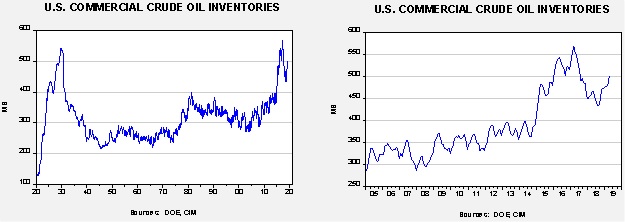

Energy update: Crude oil inventories fell 4.0 mb last week compared to the forecast rise of 2.5 mb. There was a 0.9 mb draw of the SPR, meaning the actual decline was closer to 4.9 mb.

In the details, refining activity fell 0.3% compared to the 0.9% decline forecast. Estimated U.S. production fell slightly by 0.1 mbpd to 12.2 mbpd. Crude oil imports fell 0.7 mbpd, while exports fell 0.3 mbpd.

(Sources: DOE, CIM)

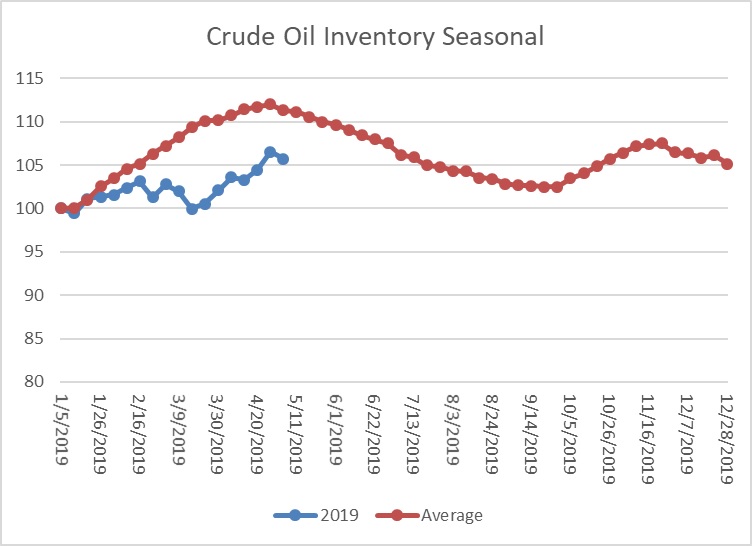

This is the seasonal pattern chart for commercial crude oil inventories. We are entering the spring/summer withdrawal season next week; this week’s decline is consistent with the normal seasonal pattern. If this trend continues, we will see weekly draws in stockpiles until the third week of September.

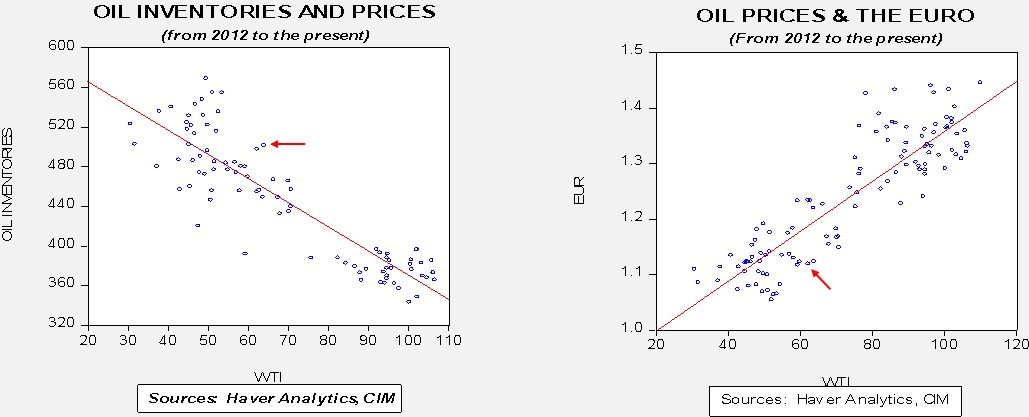

Based on oil inventories alone, fair value for crude oil is $52.34. Based on the EUR, fair value is $51.28. Using both independent variables, a more complete way of looking at the data, fair value is $50.67. This is one of those circumstances when the combined model fair value does not lie between the two single variable models. Current prices are running well above fair value. With this week’s focus on Iran, geopolitical risks are adding around $10 to $13 dollars per barrel to crude oil prices. Assuming we see usual seasonal declines and a stable dollar, fair value for the two-variable estimate rises to $54.05. Simply put, current prices have discounted a significant level of geopolitical risk and prices could see a sizable setback in the coming weeks if tensions don’t rise further. Another factor for oil—it has been acting as a “risk-on” asset and oil will likely fall too if equity values tumble due to trade tensions.

[Posted: 9:30 AM EDT] Risk-off continues. Tensions with Iran are increasing. South Africa holds elections today. Here is what we are watching:

The Iran issue: SoS Pompeo abruptly canceled a meeting with German Chancellor Merkel and made an unannounced visit to Baghdad.[1] According to reports, he made the detour due to renewed but unspecified threats from Tehran. The U.S. would likely want to base troops and other assets in Iraq if action against Iran is being considered. However, this might be difficult as Iran is deeply imbedded in Iraqi politics. Iran indicated that it may reduce its level of compliance on the nuclear deal due to U.S. actions unless Europe can guarantee that Tehran continues to have access to global markets.[2] France has indicated that if Iran does reduce its nuclear compliance and resumes nuclear enrichment activities then Europe would re-impose sanctions.[3] Tensions with Iran are clearly increasing; the sudden detour by Pompeo has the look of preparations for some sort of action. To some extent, this problem details dissonance within the Trump administration; on the one hand, the president’s instincts are to reduce American involvement in the world, including the Middle East. On the other, his Jacksonian tendencies lead him to react strongly to perceived threats. The concern is that he may be being led into a conflict by hawkish advisors.[4] Oil prices are steady this morning. Although the Iran news is supportive, U.S. inventory levels in the API data showed a build. Oil has been behaving as a risk-on asset and is likely following equities lower.

China trade: Apparently, China did reverse numerous positions that were previously established, leading to the administration’s response.[5] It seems highly probable that tariffs will be increased on Friday. The more hopeful outcome is that China returns to what was previously accepted and the U.S. pulls back on sanctions. However, doing that and saving face will be difficult. We suspect Lighthizer is pressing China hard on monitoring the agreement and building in further sanctions if the agreement’s terms are not met. This position is likely an anathema to China, which has a long history of accepting terms and then ignoring them.[6]

The chances of a significant trade rupture are increasing, mostly because both sides seem to underestimate the potential impact.[7] We believe China’s position is weaker than it perceives; we note defaults are increasing[8] and recent trade data showed weaker exports.[9] At the same time, tariffs would likely lead to rising inflation and may force the Fed into raising rates. Thus, risks are increasing.[10]

The Fed: Vice Chair Clarida appears to have reversed his comments suggesting a prophylactic cut in rates might be wise in the face of weaker inflation and, instead, adopted the language of Chair Powell, suggesting that low inflation was likely due to “temporary factors.”[11] Clarida is considered a top-flight economist and we would be somewhat surprised to see him toe the party line if he didn’t really believe it. Unfortunately, his recent comments seem to suggest a reversal from his earlier stance. One possibility? It may be that Powell is asserting the Fed’s independence and is intent on keeping policy steady to show the White House that it cannot be bullied into a rate cut. It is possible Clarida would be willing to accept that position even if his economic analysis suggests the Fed should cut rates.

Brexit: The May government has indicated that the U.K. will participate in the upcoming EU elections,[12] obliquely confirming that cross-party talks on Brexit have likely failed.[13] There are increasing risks that May will be forced to step down, triggering either general elections or a hard Brexit Tory PM to replace her.

Venezuela: The U.S. lifted individual sanctions against a Venezuelan general who changed his allegiance from Maduro to Guaido.[14] Caracas has ended a rigid program of tiered exchange rates, mostly because foreign reserves have reportedly dropped to $8.5 bn and most of this is in gold.[15] Meanwhile, SoS Pompeo and Russian Foreign Minister Lavrov are scheduled to talk in Sochi later this month in a likely bid to ease tensions over Venezuela.[16]

South Africa elections: Although Cyril Ramaphosa will almost certainly win today’s poll, his party, the ANC, is suffering from widespread corruption.[17] Ramaphosa is considered an honest candidate, but the bigger issue is increasing disillusionment with democracy itself. This condition increases the chances of a coup or a call for dictatorship. If unrest widens in South Africa, it could be bullish for precious metals, especially platinum.

Odds and ends:The U.S. has decided to implement tariffs against Mexican tomatoes.[18] The U.S. had accused Mexico of dumping tomatoes on the U.S. market, beginning a formal investigation in 1996. The investigation was suspended on a regular basis ever since. Separately, China has begun construction on a third aircraft carrier, one that appears larger than the two it currently has, which are based on a Soviet platform.[19] This would be China’s first full-sized flattop. Lastly, we’re seeing more trouble for crypto currencies as a reported $41 mm was stolen from Biance, a crypto-exchange.[20]

[Posted: 9:30 AM EDT] Trade tensions remain. Parsing the Iran threat. Here is what we are watching:

Trade turmoil: So, is the tariff threat real or a bluff? Equity markets decided yesterday that it was more the latter than the former.[1] This morning, equity markets seem less convinced. This is what we know:

The U.S. is calling out China for reneging on previous agreements.[2] Lighthizer appears to have taken the lead in talks with China, edging out Treasury Secretary Mnuchin. Lighthizer, as we have noted before, is a hardliner on trade. He was instrumental in getting Japan to agree to “voluntary” auto export reductions in the late 1980s and is known as a relentless negotiator. Although President Trump seems to really want a deal, he trusts Lighthizer and the change in course likely reflects that the president agrees with his trade negotiator that China was trying to pull a fast one. It’s also important to remember that for Lighthizer these talks are perhaps his last chance to fundamentally change the U.S./China trade relationship to favor America, much like he did with the U.S./Japan relationship. Thus, he is less concerned about China’s “feelings” and the 2020 elections. It had appeared Trump was leaning toward Mnuchin and against Lighthizer so a deal could get done, but Lighthizer may have appealed to Trump’s “inner Jackson” and convinced the president that a hardline position was justified. But, come what may, Lighthizer’s goal doesn’t necessarily coincide with the president’s in all areas. If Trump decides to follow Lighthizer, a rupture in U.S./China trade relations is much more likely.

So far, China’s response has been measured. Vice Premier Liu will come to Washington, but not until Thursday and will leave the next day. He was originally scheduled to arrive on Wednesday and stay until Saturday.[3] Although the visit does avoid a complete rupture, it is hard to see how we can avoid the tariff increase.

Both sides may have overplayed their positions. The White House is basking in historically low interest rates and surprisingly strong GDP, while China is coming off a successful OBR meeting and better economic data.[4] Wars often start because the participants overestimate their own positions and underestimate their opponents.

China may have concluded that continuing to negotiate was a better outcome because elections in 2020 would likely force the U.S. to capitulate. Lighthizer likely sniffed out this position and may have recommended that the president renew the tariff threat.[5]

It is possible the White House believes that an increase in trade tensions might prompt the FOMC to cut rates. Although we are not sure that would occur, a breakdown in talks would likely weaken sentiment and may lead the Fed to ease. Thus, the president may think he has the Fed at his back if things go south.

Financial markets continue to expect a deal to be finalized. There is good reason to expect that outcome. But, it isn’t certain and there could be an equity correction looming if trade talks fail.[6]

Iran: According to reports, the U.S. received credible intelligence that Iran was planning to attack U.S. assets in the Middle East.[7] The U.S. response is something of a half measure. If the U.S. was really going to war with Iran, we would see three carrier groups in the region, not one. At the same time, the CVN Abraham Lincoln is a formidable asset and will get Iran’s attention. We suspect Iran has “fired up” Hamas and Islamic Jihad to attack Israel, leading to the recent missile strikes.[8] Iran’s problem is that the reduced U.S. exposure in the Middle East has led to a quiet alliance between the Arab states and Israel. Iran, under sanctions, is finding it difficult to respond to this pressure. Its “softest” target is Iraq, but it already has influence there anyway. Syria is a less reliable party because of Russian influence. Therefore, the desire to strike back at the Sunni Arab states makes sense. It should be noted that if Iran does “something” (e.g., cyberattack on Saudi Arabia, etc.), then the only real targets for U.S. warplanes are in Iran itself. Thus, the chances of escalation are probably increasing. However, it still is not obvious that Iran will act in such a way that makes it obvious Iran is the perpetrator. Iran is a master of the covert.

Turkey: President Erdogan’s party has forced a new municipal election in Istanbul.[9] The initial vote was allegedly corrupt. We have no doubt that, compared to Western standards, the election process was probably open to question. However, our reading of the process suggests there was nothing all that unusual in last month’s local elections. New elections will be held on June 23.[10] It appears Erdogan is unwilling to accept adverse results and that is unnerving foreign investors.[11] The TRY has weakened on the news; however, our position is that the currency has already discounted significant bad news.

Brexit: Although there is hope that May and Corbyn can put together a coalition to approve a customs union, this outcome may not have staying power. It appears that even if a deal is made we are probably still looking at either a new referendum[12] or new general elections.[13] It isn’t clear that a new referendum will offer any more clarity and the second outcome probably either leads to a Corbyn government (and market panic) or Johnson (panic, but less so). Stay tuned…

Fed governors:Senate GOP leaders are putting together a list of potential governor candidates for the White House to avoid a repeat of the Stephen Moore/Herman Cain situation.[14] Although this makes sense, the candidates offered will likely be hard money policy hawks, exactly the opposite of what the president wants. So, we expect no short-term resolution on this issue.

Part I of this report was a review of the reserve currency and the savings identity. In Part II, we showed how the Nixon and Reagan administrations used America’s hegemonic power to force some of the economic adjustment of U.S. policy onto foreign governments. This week, in the final segment of this report, we will look at the actions of the Trump administration, using the comparisons to the Nixon and Reagan administrations. We will conclude the report with market ramifications.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.