Author: Amanda Ahne

Bi-Weekly Geopolitical Report – What If Russia Wins in Ukraine? (January 16, 2024)

by Patrick Fearon-Hernandez, CFA | PDF

For the last two years, we’ve written a great deal about the evolving China-led geopolitical bloc and Beijing’s allies within it, including top partner Russia and other like-minded nations such as North Korea, Iran, Cuba, and Venezuela. We believe the geopolitical challenge to the United States and its allies from the China/Russia bloc will change the world’s political, military, economic, technological, social, and cultural landscapes for decades to come, with huge implications for investors.

Of course, Beijing doesn’t have total control over its bloc. We suspect Chinese leaders were discomfited when Russia launched its poorly conceived invasion of Ukraine in February 2022. By late 2023, however, the Russian military had improved its performance and stabilized its control over almost 20% of Ukrainian territory in the country’s east and south. At the same time, many politicians and voters in the U.S. and Europe had begun to resist providing more military aid to Ukraine. In this report, we examine the longer-term geopolitical, economic, and investment implications if U.S. and allied aid to Ukraine ends for good, with a focus on the implications for the top members of the China/Russia bloc and the U.S. bloc.

Don’t miss our accompanying podcasts, available on our website and most podcast platforms: Apple | Spotify | Google

Daily Comment (January 16, 2024)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM EST] | PDF

Our Comment today opens with some notes on the important voting in Iowa and Taiwan over the last few days. We next review a wide range of other international and U.S. developments with the potential to affect the financial markets today, including further Houthi attacks on commercial ships in the Red Sea and a Federal Reserve policymaker’s warning against cutting interest rates too soon.

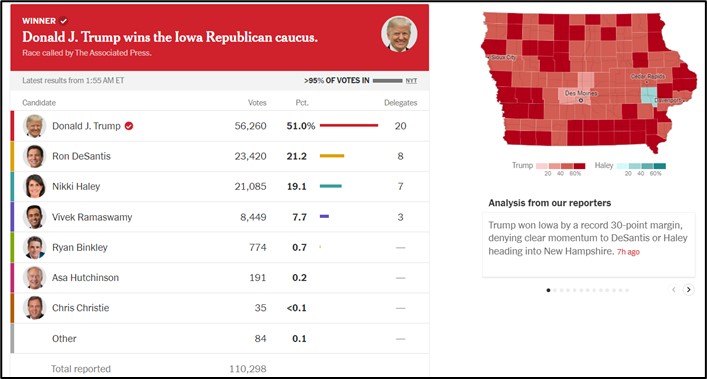

U.S. Elections: In the Republican Party’s Iowa caucuses yesterday, former President Trump overwhelmingly won, as expected, with about 51% of the vote. Florida Governor Ron DeSantis came in second with 21%. Former South Carolina Governor Nicki Haley only came in third with 19%, despite her recent surge in polling support. Entrepreneur Vivek Ramaswamy came in fourth with less than 8% and announced that he will end his long-shot bid for the nomination. Next stop for the remaining candidates is the New Hampshire primary next Tuesday.

- Although Trump’s margin of victory was a record for Iowa, it’s important to keep in mind that the state has had a poor record of choosing the ultimate Republican candidate in recent election cycles. Trump still looks like the likely candidate for the Republicans, but his position at the top of the ticket isn’t yet assured.

- Another thing to keep in mind is that it’s still unclear whether Trump’s candidacy should be treated as that of an incumbent or as an upstart. Over history, the political and financial market dynamics around an election have differed depending on the status of the ultimate winner. For example, if Trump were considered an incumbent, he would have been expected to take nearly all the vote in last night’s balloting.

- In any case, we’ll continue monitoring the election campaigns, with a key focus on the implications for issues such as:

- U.S. foreign policy, especially the U.S.’s tense relationship with China, the strength of its alliances, and approach to international trade, investment, and migration;

- Monetary policy, especially the independence of the Fed and likely nominations for key officials;

- Fiscal policy, including the fate of the Trump tax cuts due to expire in 2025, the outlook for the federal deficit and debt, and spending priorities in the budget; and

- Regulatory policy, including antitrust policies and the regulation of the energy industry and financial services.

(Source: Wall Street Journal)

(Source: Wall Street Journal)

Taiwan Elections: In Saturday’s election, independence-leaning Vice President Lai Ching-te of the ruling Democratic Progressive Party won the presidency with 40% of the vote. Lai’s win will anger Chinese leaders, as it means Taiwan’s government will continue to resist near-term reunification with the mainland. Still, Beijing may be partly appeased that the DPP lost control of the legislature to the China-friendly Kuomintang. Thus, the results may be the best possible outcome for peace in the Indo-Pacific and the security of Taiwan’s world-leading semiconductor industry, which produces 90% of the world’s most advanced computer and cellphone chips.

- Separately, the tiny Pacific Island nation of Nauru (pop. 11,000) yesterday recognized the People’s Republic of China, dumping its diplomatic recognition of Taiwan. In response, the Taiwanese foreign ministry accused Nauru of trying to extort large sums of money from Taipei to maintain its recognition of Taiwan.

- As a result, just 12 countries around the world now recognize Taiwan as the official representative of the Chinese nation.

South Korea: Although Taiwan’s election outcome probably boosts the near-term security of its chip industry, governments around the world still worry that the U.S.-China rivalry could threaten future semiconductor supplies. Reflecting that concern, the South Korean government yesterday announced a plan to develop the world’s largest semiconductor manufacturing hub by channeling $471 billion of private investment into the project over the next 25 years.

- Much of the investment will come from the country’s premier electronics firms, including Samsung (005930.KS, KRW, 73,900) and SK Hynix (000660.KS, KRW, 134,100).

- As with similar chipmaking plans in the U.S. and other countries, the aim of Seoul’s program is to develop its own domestic computer chip supplies.

North Korea-South Korea: North Korean paramount leader Kim Jong Un today ordered that his country’s constitution be changed to remove its language calling for eventual reunification with South Korea. Kim also ordered that all government agencies dedicated to reunification be dismantled and that North Koreans should now consider South Koreans to be their principal enemy. The aim of the move is apparently to give North Korea more political leeway for an eventual attack on South Korea, or at least to increase the credibility of threatening such an attack.

Philippines: After a meeting with President Ferdinand Marcos, Jr., yesterday, the chief of the Philippine military laid out an expansive plan to assert the country’ sovereignty over areas also claimed by China. The unexpectedly aggressive plan would include purchasing more military ships, radars, and aircraft, as well as building facilities to house troops on up to nine disputed islands. Given the U.S.-Philippine mutual defense treaty, Manila’s more assertive stance against China raises the risk of a potential U.S.-China conflict in the future.

China: In a speech to the World Economic Forum in Davos, Switzerland, Premier Li Qiang said Chinese gross domestic product grew by “an estimated” 5.3% in 2023. If confirmed when Beijing releases the official figures, that would mark an acceleration from the weak 3.0% growth in 2022, when the government was still imposing draconian lockdowns to battle the COVID-19 pandemic. Tellingly, Li bragged that the growth in 2023 was achieved without resorting to “massive stimulus,” which suggests investors shouldn’t hope for such policies in 2024.

Japan: As Prime Minister Kishida struggles with abysmally low ratings in opinion polls, compounded by his Liberal Democratic Party’s extensive illegal funding scandal, a recent poll shows that Foreign Minister Yōko Kamikawa is rising in popularity. Indeed, she is increasingly being seen as a viable candidate to replace Kishida, based largely on her reputation as an energetic and courageous leader.

Germany: Data released yesterday showed Germany’s gross domestic product fell by an inflation-adjusted 0.3% in 2023, making it the worst-performing major country last year. The decline reflected headwinds such as high energy costs, elevated inflation rates, and rising interest rates, all of which continue to weigh on Germany — and the broader European economy — so far in 2024.

Middle East Conflicts: Iran launched a series of ballistic missile strikes this morning against targets in Syria and northern Iraq, including what Iranian officials said was an Israeli “intelligence center.” According to the Iranians, the strikes were in response to recent Israeli attacks that killed an Iranian commander in Syria and members of Tehran-backed militant groups in the region. The strike against the Israeli facility, if true, could dramatically increase the risk of overt fighting between the Israelis and Iran.

- Separately, Iran-backed Houthi rebels in Yemen fired missiles at both a U.S. Navy ship and a U.S-owned commercial ship over the long weekend, hitting the commercial ship but only causing minimal damage. U.S. military officials said they are expecting more retaliatory attacks from the Houthis and are preparing to launch more punishing airstrikes in response.

- The Iranian and Houthi attacks are keeping alive the risk that the Israeli-Hamas conflict could broaden into a wider regional war that would draw in the U.S.

- A broader war in the region would threaten global trade and oil supplies, boosting prices and threatening to reverse the recent progress in bringing down inflation.

U.S. Monetary Policy: Atlanta FRB President Bostic warned on Sunday that cutting interest rates too soon could lead to a rebound in consumer price inflation. Indeed, Bostic also said that the recent fast progress in bringing down inflation will likely slow going forward. Bostic is a voting member of the policy-setting Federal Open Market Committee this year, so his warnings suggest he may help resist any move by the policymakers to cut rates as quickly as bond investors are expecting.

U.S. Fiscal Policy – Federal: Senate Majority Leader Schumer has submitted a new stopgap funding bill to keep the federal government open until early March, which would give lawmakers more time to agree on the appropriations bills needed to formally fund operations for the rest of the fiscal year. The bill is due to be taken up by the Senate today and would have to pass both houses and be signed into law by Friday to avoid a partial shutdown of the government, but opposition to the overall funding deal by some Republicans makes it unclear whether that will happen.

U.S. Fiscal Policy – State & Local: As New York Governor Hochul and New York City Mayor Adams today release their proposed budgets for the coming fiscal year, the plans are expected to encompass the state sending an additional $2 billion to the city to help cover the cost of providing housing, food, medical care, and other services to illegal immigrants sent their by border states. City officials expect the cost of caring for the immigrants will total $10 billion through mid-2025, likely helping create political pressure for tougher border policies.

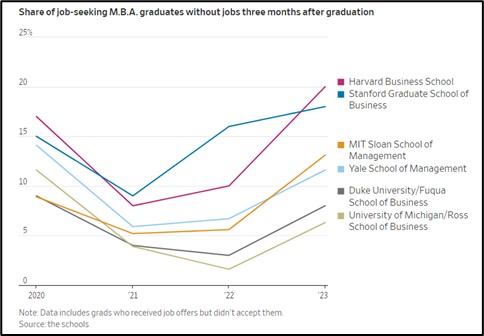

U.S. Labor Market: Although the overall demand for labor in the U.S. remains strong, data continue to show weak hiring for higher-paid, white collar jobs. The Wall Street Journal today carries an interesting story showing an unexpectedly high rate of joblessness for newly minted MBAs from top schools. For example, the report shows that 20% of students who received an MBA from Harvard Business School this spring were still unemployed three months later. Weak demand for white-collar labor could help explain some of the current crosswinds in the job market.

Daily Comment (January 12, 2024)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM EST] | PDF

Good morning! U.S. equities appear subdued ahead of the weekend, while Inter Miami’s new game plan is clear — feed Messi! Today’s Comment kicks off with an analysis of the potential risks of Western allies’ joint action against Houthi rebels, followed by a deep dive into why traders remain confident in a March Fed rate cut. We also unpack the latest Japanese monetary policy decisions and bring you up to speed on key domestic and international data releases.

Broadening Conflict: The U.S. and U.K. launched joint airstrikes against Houthi rebels in Yemen, heightening tensions in the Middle East.

- The U.S. and U.K. launched joint airstrikes against Houthi rebel targets in Yemen, responding to their recent attacks on commercial ships in the Red Sea. They were joined by Australia, Bahrain, Canada, and the Netherlands in this operation. The coalition used precision-guided missiles to hit more than 60 targets in 16 locations in Yemen. This coordinated effort comes days after the U.S. and its allies warned Houthi rebels that continued attacks on vessels would lead to a military response. The coordinated offensive raises the likelihood of a broader conflict in the Middle East. In response to the attack, the Houthis have vowed to retaliate.

- Fighting in the region is likely to lead to volatility in oil prices. The International Association of Independent Tank Owners, a trade group representing 70% of globally traded petrochemicals, has advised its members to stay away from the highly contested Bab-el-Mandab strait. The warning comes a day after Iran seized a ship with Iraqi crude that was headed for Turkey in the Gulf of Oman. Uncertainty regarding how the next few days will play out has led to a surge in oil prices, which have risen 4% over the past two days as traders price in the potential for supply disruptions. Despite the uncertainty, oil prices remain below the previous year’s levels.

- Red Sea tensions underscore the U.S.’s critical role in safeguarding economic stability through ensuring free passage in key shipping lanes. Though oil prices have been affected, swift containment of the situation should prevent long-term trade disruptions. Yet, a wider conflict which escalates military action could trigger a more sustained price shock and heighten recessionary risks, potentially sparking financial market panic due to geopolitical uncertainty. Although we remain optimistic that this will not turn into an all-out war in the Middle East, we acknowledge that risks remain elevated.

Traders Unconvinced: Market bets of rate cuts surprisingly increased even after hotter-than-expected inflation data and a reiterated commitment from Fed officials to maintaining restrictive policy.

- Central bank officials pushed back on speculation of March rate cuts but stopped short of ruling them out entirely. Hawk Loretta Mester, president of the Cleveland Fed, insisted it’s too early for such a move. However, she pointed out that December’s inflation uptick doesn’t mean that progress has stalled. Meanwhile, both Richmond and Chicago Fed Presidents Thomas Barkin and Austan Goolsbee, refused to rule out a March rate cut, adding to the uncertainty. The lack of clarity from Fed officials prompted markets to boost their March pivot prediction by five percentage points, raising the expectation of a rate cut next spring to 70%.

- Mixed economic data fuels uncertainty around the Fed’s March policy stance. December inflation hit 3.4%, exceeding both forecasts and November’s reading, raising concerns about a potentiation return of price pressures. Conversely, a surprisingly strong December job market, which added 216,000 positions, suggests ongoing economic momentum. While headline figures mask nuanced trends, like a downward shift in monthly inflation and a steady increase in the number of unemployed workers throughout the year, the Fed’s muted reaction indicates they’re prioritizing different factors or possible embracing ambiguity. With conflicting signals and hidden depths, predicting their next move is like peering into a foggy crystal ball — a gamble fraught with uncertainty.

- Pent-up anticipation of a Fed pivot to easier policy has fueled risk appetite, with traders betting on six aggressive rate cuts this year. While this expectation reflects the perceived historical tendency of the Fed to cut rates faster than it raises them, we believe the actual easing cycle will be later and shallower than the market anticipates. If policymakers prove less dovish, the recent bond rally could face a sharp reversal. Nevertheless, even in that scenario, fixed-income securities should fare better than last year. The upcoming FOMC meeting will likely serve as the key turning point, testing market expectations and setting the tone for the year ahead.

What’s Next for BOJ? The Nikkei 225 continues to rally in 2024 as investors grow concerned that the Bank of Japan won’t be able to shift away from its aggressive monetary easing.

- The strength of Japan’s benchmark stock index comes amid signs that nominal wage growth slowed sharply in the final months of 2023. The annual change in nominal wage growth slowed to 0.2% in November, down considerably from the previous month’s rise of 1.5%. The slowdown raises concerns that BOJ Governor Ueda will see it as a sign of weak inflationary pressures, and will delay his planned pivot away from aggressive monetary easing. The wage slowdown points to firms’ continued reluctance to increase labor earnings, likely due to concerns about hurting profit margins if they cannot readily pass on the costs to consumers.

- While optimism has fueled a surge in popularity for Japanese equities since 2023, concerns linger about the sustainability of the rally. The Nikkei’s RSI climbed above the overbought threshold of 70, suggesting a potential loss of momentum in the coming months. Price pressures also provide a headwind. November’s CPI data showed a welcome decline in annual inflation to 2.5%, down from 3.2% in October. However, government forecasts predict inflation will struggle to fall below that threshold throughout 2024, exceeding the central bank’s 2% target.

- Many economists and market analysts anticipate that the Bank of Japan will eventually pivot away from its ultra-accommodative policy, but the timing largely hinges on the outcome of the annual wage negotiations in March, known as Shunto. If labor unions secure significant wage increases, the central bank may feel compelled to finally raise interest rates or adjust its yield curve control policy, potentially leading to a stronger yen (JPY). This may hurt Japanese businesses due to higher borrowing costs and a less competitive currency, but we suspect the fallout could spread into global financial markets due to the preponderance of yen carry trades that are outstanding.

Other news: Taiwan’s presidential elections take place this weekend, and China has issued another strong warning against any moves towards formal independence, raising concerns about a potential increase in regional tensions.

Daily Comment (January 11, 2024)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM EST] | PDF

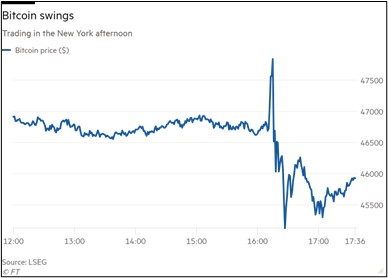

Good morning! Risk assets are off to a rough start as CPI failed to reinforce rate cut expectations. On the bright side, Real Madrid secured a nail-biting win over their city rivals Atlético Madrid in extra time, keeping their Supercopa dreams alive. Today’s Comment starts with our thoughts on the resurgence of demand for fixed-income securities. We then discuss the SEC’s approval of a bitcoin ETF and provide an update on the conflict in the Red Sea. As always, our report also includes an overview of the latest domestic and international data releases.

Bond Rush! Anticipation of central bank rate cuts has led investors to flock to fixed-income securities; however, policymakers continue to play their cards close to their chest.

- G-7 central bankers are hinting at the end of rate hikes, but they’re staying mum on potential cuts. While New York Fed President John Williams believes current rates can tame inflation, he emphasizes the need for continued evidence of a sustained cooldown before considering any easing. The European Central Bank’s Isabel Schnabel and Bank of England Governor Andrew Bailey both echoed this cautious stance by warning against premature speculation due to persistently high inflation exceeding their 2% target. Although inflation has eased notably over the past year, growing concerns from economists and analysts suggest that inflation may struggle to reach the 2% target within the year due to geopolitical and supply chain risks.

- Ignoring central bank warnings of steady rates, investors drove European bond sales to a record high of 118 billion EUR ($108 billion) this week. Supranational organizations and sovereign governments fueled the surge, seeking to lock in lower rates and fund annual expenditures. This borrowing spree wasn’t limited to Europe. Emerging market governments and corporations also jumped in, raising $50 billion in the first half of January to capitalize on the temporary dip in rates. This global borrowing spree reflects investor optimism in the wake of easing rate pressures, signaling potential financial relief across markets after a period of hawkish policy.

- While falling rate expectations eased borrowing costs and boosted liquidity, a long lasting ease in financial conditions will likely require actual policy changes from central banks. Despite isolated suggestions like Fed Governor Waller’s hint at a March cut, no clear evidence points to an imminent pivot. Thus, the risk remains real, similar to 2023, that the current bond rally may fizzle out before it gains firm footing, revealing more risk in long-duration bonds than current pricing suggests. We recommend that investors cautiously approach the prospect of rate cuts as a deceleration in inflationary pressure may prompt policymakers to maintain current rates beyond market expectations.

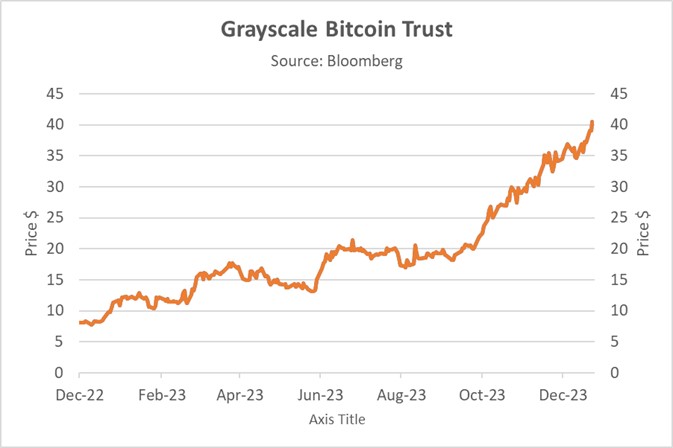

SEC Approves: Crypto traders achieved a crucial victory as the Security and Exchange Commission approved the first spot Bitcoin ETFs.

- After years of regulatory limbo, 10 crypto ETFs secured approval, marking a significant step forward for the industry. This green light follows a decade-long legal battle that culminated in the federal courts forcing the SEC to review Grayscale’s Bitcoin ETF application. Despite the SEC’s concerns about potential manipulation and fraud in digital assets, this decision clears the way for the first crypto ETFs to begin trading as soon as this morning. This opens the door for both retail and institutional investors to gain regulated exposure to digital assets for the first time, a move that could significantly boost adoption and legitimize the crypto market.

- Following the announcement, Bitcoin, the most widely traded currency, rose as high as 2% on the day and volume jumped to a 10-month high. This surge reflects investor excitement over the potential domino effect, paving the way for broader adoption of other digital assets. While crypto’s mainstream appeal remains debatable, its dedicated fanbase is undeniable. A recent Crypto Council for Innovation survey revealed that a whopping 83% of holders favor clear regulatory guidelines from the next president, hoping they will nurture the industry’s growth. Crypto may not swing elections, but its rising influence is becoming clearer.

- Although the ruling improves crypto’s attractiveness, the market remains rife with regulatory uncertainty and elevated volatility. Bitcoin’s $47,000 price tag faces a bumpy road ahead, with analysts predicting declines towards $28,000 by year-end, countered by some optimistic forecasts eyeing a climb above $100,000. This stark contrast underscores the inherent volatility of the asset. As a result, unless a divine power comes down to meet us at Mt. Sinai to tell us otherwise, we will remain steadfast in our belief that crypto is not a safe choice for risk-averse investors.

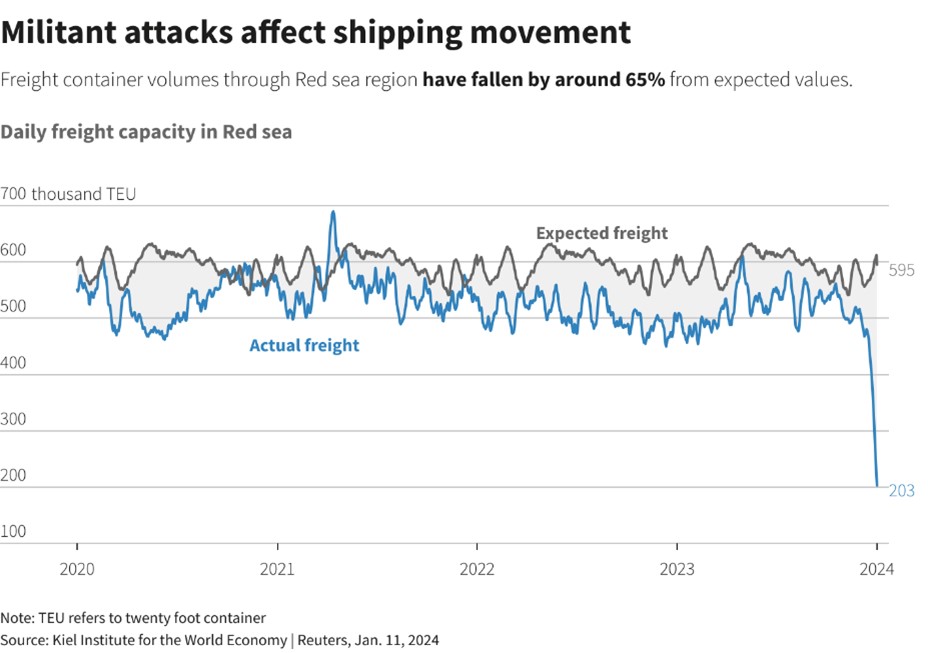

Conflict in the Red Sea: The Iranian-backed Houthis have continued to escalate tensions with the West by launching attacks on commercial ships entering the Red Sea.

- Frustration mounts as leaders from the United States and its allies issue stern warnings of military action in response to ongoing Houthi rebel attacks on shipping vessels in the Red Sea. This escalation comes after a recent barrage of attacks by the Houthis, which involved 18 drones, two anti-ship cruise missiles, and one anti-ship missile aimed at commercial ships traversing the crucial global trade route. The Houthis have linked their actions to the ongoing conflict between Israel and Hamas by vowing to continue their attacks until Israeli forces withdraw from Gaza. This raises concerns of a wider regional conflict.

- Houthi attacks on Red Sea shipping are worrying, but their inflationary impact remains elusive. Violence in the Red Sea has spiked freight costs, as shippers are forced to pay higher shipping costs through insurance and take longer shipping routes to transport their goods. That said, freight costs remain well below pandemic levels. Meanwhile, overall global trade dipped 1.3% in December suggesting that countries are still being impacted. The European Union, specifically, saw a sharp drop in trade with imports falling by 3% and exports declining by 2%. However, there are still no signs that the shipping problem will impact inflation.

- Weak confidence and elevated rates, which dampen demand, largely shield consumers from the conflict’s immediate sting. This trend is likely to hold in the next three to six months assuming that the conflict in the Middle East remains relatively contained. We foresee a broader conflict significantly impacting European inflation, more so than the U.S., while proving bullish for commodities like oil and metals. However, Western intervention remains a major headwind for financial markets as it could lead to a renewed war effort, but this remains a low probability.

Other News: With Chris Christie suspending his presidential bid, Donald Trump is now closer to facing a one-on-one fight for the Republican nomination. While he still appears to be the frontrunner, we can’t rule out an upset. China has gestured toward more cooperative U.S. ties days before Taiwan’s elections, potentially reducing the risk of miscalculation regarding an island takeover if its preferred candidate loses. Alphabet Inc.’s Google (GOOG, $143,80) plans to lay off hundreds, in a sign that tech may be trying to meet earnings expectations through a smaller workforce.

Daily Comment (January 10, 2024)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM EST] | PDF

Our Comment today opens with a warning about high government debt levels from the Institute of International Finance. We next review a wide range of other international and U.S. developments with the potential to affect the financial markets today, including a dramatic example of violence in Ecuador and the latest on fiscal policy negotiations in the U.S.

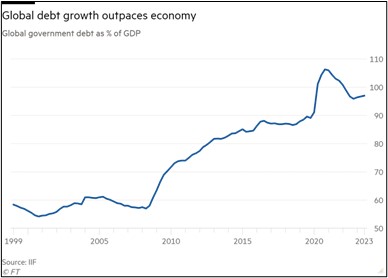

Global Government Debt: The Institute of International Finance has issued a report warning that the “unmoored” level of public debt around the world is raising the risk of a bond-market backlash. The report indicates that government debt isn’t just a problem in the U.S., the U.K., and other developed countries, but is also a problem in many emerging markets.

- Our analysis suggests much of the problem in the U.S. can be traced to the lingering effects of the COVID-19 pandemic, which pushed legions of baby boomers into retirement (replacing Social Security contributions with Social Security withdrawals), boosted price inflation, and prompted generous new entitlement benefits.

- In theory, policymakers could attack some of those issues, say by bringing down inflation and curtailing benefits. On the other hand, other issues will generate continued spending pressures, such as further population aging and new geopolitical tensions that will require higher defense budgets.

Eurozone: Luis de Guindos, vice president of the European Central Bank, warned in a speech today that even though the eurozone economy is likely to enter another downturn this year, persistent inflation pressures could keep the monetary policymakers from cutting interest rates as aggressively as market participants expect. The statement illustrates how bond investors in Europe are probably too optimistic about near-term interest rate cuts, just as they are in the U.S.

United Kingdom: Former defense officials have gone public with complaints that the Ministry of Defense is trying to cover up data showing a serious shortfall in skilled personnel for the armed forces. The lack of skilled sailors has reportedly prompted the early retirement of at least two navy vessels. Meanwhile, The Telegraph reports that total U.K. armed forces personnel has fallen to 184,865, the lowest number since the end of the Napoleonic Wars in 1815.

Ecuador: Armed gang members yesterday staged attacks across the country, including breaking into a public television station and temporarily interrupting a live show while they brandished guns and grenades. The gang violence appeared to be a warning against President Noboa’s plan to crack down on the gangs and bring them under control. The violence highlights the growing power and violence of drug cartels, which threatens to destabilize governments, imped investment, and drive more migrants to the U.S.

United States-China: As more evidence that the U.S. military is preparing for a potential future conflict with China, an important Air Force intelligence unit is reportedly urging its Arabic- and Pashto-speaking cryptologic linguists to learn Mandarin. The move by the 70th Intelligence, Surveillance, and Reconnaissance Wing comes as the U.S. Marine Corp is completely restructuring to fight a war in the Indo-Pacific region, while the U.S. Army has reinstituted jungle warfare training, and the U.S. Navy is broadening its submarine efforts with Australia.

U.S. Fiscal Policy: Even though lawmakers have reached an agreement on the top-line budget parameters for the current fiscal year, Senate Minority Leader Mitchell yesterday advised that there won’t be enough time to pass all the specific appropriations bills needed to finance the government when the current stopgap funding law expires beginning in about two weeks. In other words, Congress may have to pass yet another stopgap to avoid a partial government shutdown until the appropriations bills are finished. Stay tuned for more budget chaos.

- Separately, lawmakers who are working on separate tax legislation are reportedly considering curbing the controversial pandemic-era Employee Retention Credit (ERC). That law, passed in 2020, gives employers a lucrative tax break for retaining employees during the pandemic shutdowns, but it has been wracked by fraud and an overly long availability until 2025.

- Curbing the eligibility for that credit or cracking down on spurious claims could help generate funds for other priorities the lawmakers are discussing, such as reversing the requirement in the Trump tax package of 2017 that corporate research deductions be spread out over five years instead of being expensed immediately.

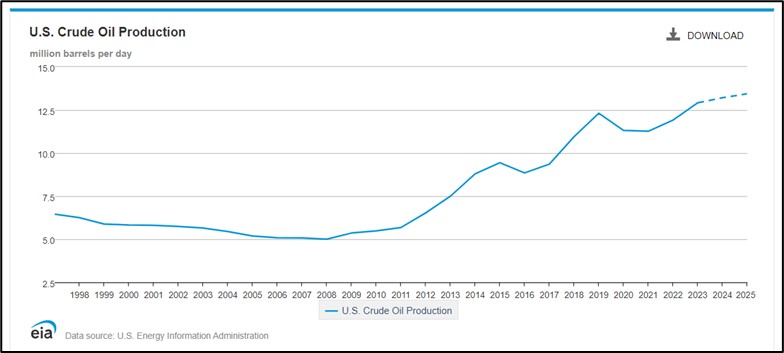

U.S. Energy Market: A new outlook from the Energy Information Administration forecasts that U.S. oil production will rise further from the record high of 12.9 million barrels per day in 2023 to further new record highs of 13.2 million bpd in 2024 and 13.4 million bpd in 2025. The agency also projects that U.S. output of natural gas will also rise to new records this year and next year. The figures underscore how the U.S. has become an energy powerhouse since the arrival of new technologies such as hydraulic fracturing and horizontal drilling.

- While “green” policies and investor demands for capital discipline did discourage new exploration and development for much of the last decade, drillers more recently have boosted output.

- Along with weakening demand growth in China and other markets, the surge in U.S. energy output has helped push down prices in recent months, helping bring down the overall rate of consumer price inflation.

- If the U.S. economy slows too much and slips into recession, the further loss of demand would likely weigh even more heavily on global oil and gas prices.

- Nevertheless, we think the hesitant drilling in recent years and increased geopolitical tension will buoy oil and gas prices again over the longer term.

U.S. Cryptocurrency Market: Bitcoin (BTC, $45,108.20) and other cryptocurrencies swung wildly in price yesterday after a hacker took control of the Securities and Exchange Commission’s social media account and falsely announced that the agency had approved the U.S.’s first-ever cryptocurrency ETFs. Crypto prices surged, only to fall sharply within minutes when the SEC disclaimed the report. Nevertheless, the SEC is widely expected to announce its official decision on crypto ETFs either today or tomorrow.

Daily Comment (January 9, 2024)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM EST] | PDF

Our Comment today opens with an observation from a high-profile investment manager about renewable energy as one element of energy security. We next review a wide range of other international and U.S. developments with the potential to affect the financial markets today, including a surprise fall in the eurozone’s unemployment rate and further indications that the Federal Reserve is pivoting toward looser monetary policy (although still probably not as fast as many investors think).

Global Energy Market: In a short interview carried by the Wall Street Journal yesterday, a managing partner at infrastructure investor Brookfield Asset Management (BAM, $38.84) argued that last year’s slump in many renewable energy stocks was “very overdone” and that investment and capacity growth in renewable energy continues to surprise on the upside. Importantly, the manager tied the outlook for renewables not only to a desire for clean energy and growing opposition to fossil fuels but also as a source of secure, domestic energy.

- The comment came from Jehangir Vevaina, a managing partner in Brookfield’s renewable power and transition group. Vevaina touches on a theme we’re seeing more often these days: With geopolitical tensions raising the risk of disruptions in global energy flows, one advantage of solar, wind, hydroelectric, and other renewables is that they can provide secure, domestically produced energy.

- Clearly, the current push for “Green Technology” has become very politicized and polarizing. The green technology push will likely lead to lots of malinvestment and underinvestment in fossil fuels. On the other hand, looking at renewables as one way to improve energy security suggests that the industry could still have a bright future even if today’s environmentally driven push for renewables comes to an end.

Eurozone: The November unemployment rate fell to a seasonally adjusted 6.4%, beating expectations that it would remain at October’s rate of 6.5%. With the decline in joblessness in November, the region’s unemployment rate is now once again at a record low, despite a recent slowdown in economic activity due to high interest rates and other factors. In turn, the continued strong demand for labor and rising wages could encourage the European Central Bank to keep interest rates high for longer than investors expect.

France: President Macron has named his recently appointed 34-year-old, charismatic education minister, Gabriel Attal, to be his new prime minister following the resignation of Élisabeth Borne on Monday. The popular Attal will be France’s youngest-ever prime minister, suggesting Macron was looking for a dramatic nominee who could breathe new life into his administration. Nevertheless, Macron’s lack of a majority in parliament means he will still struggle to push his agenda forward.

Russia: According to British intelligence, the Kremlin has re-established the Stalinist counterintelligence organization known as SMERSH, an acronym for “death to spies.” Made famous in Ian Fleming’s James Bond spy novels, the unit aims to root out traitors and spies within the Russian government. Coming hot on the heels of increased counterintelligence efforts in China, the move may be a reaction to increased human intelligence successes by Western services that have unsettled President Putin and General Secretary Xi.

Israel-Hamas Conflict: In separate incidents yesterday, the Israeli military killed a senior figure of the Iran-backed Hezbollah militant group in southern Lebanon and another top Hamas commander in Syria. The increasingly brazen Israeli assassinations outside of the conflict zone in the Gaza Strip are keeping alive the risk that the war will broaden regionally.

China: The China Passenger Car Association today said the number of Chinese-made autos that were exported abroad rose to a record 5.26 million in 2023, putting China on track to be the world’s top vehicle exporter. When Japan, the previous top exporter, reports its data in the coming weeks, it is expected to have sold less than 4.50 million vehicles abroad.

- China’s surging auto exports reflect both its strong competitiveness in electric vehicles and its surging sales to Russia after that country was sanctioned by the West for its invasion of Ukraine.

- Since China’s rising auto exports will threaten domestic carmakers around the world, they are likely to spur further protectionist policies, especially in Europe. In turn, efforts to hold back the Chinese export tide will likely further exacerbate today’s tensions between China and the members of the U.S.-led geopolitical bloc.

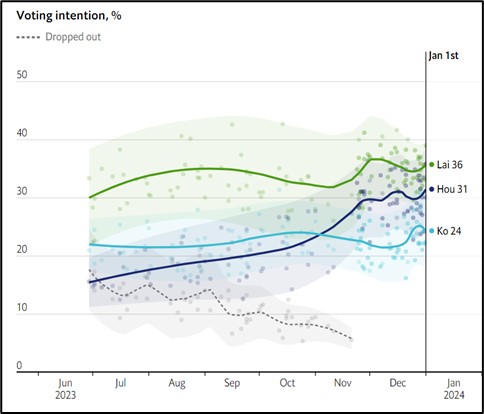

China-Taiwan: Just days before the presidential election on Saturday, independence-leaning frontrunner Lai Ching-te of the ruling Democratic Progressive Party has accused China of trying to undermine his campaign. According to Lai, Beijing has used the full gamut of interference tactics, from propaganda and military intimidation to “cognitive warfare” and fake news to scare voters into casting their ballot for his opponents, especially the China-friendly Kuomintang Party’s Hou Yu-ih.

- A victory by Lai could immediately raise tensions between China and Taiwan, potentially drawing in the U.S., Japan, and other Taiwan supporters.

- This portends rocky trading in the world’s financial markets early next week, assuming the current opinion polls are accurate (see the latest chart by the Economist below).

(Source: The Economist)

(Source: The Economist)

China-Argentina: The Chinese government yesterday said it would cut import tariffs or extend tariff reductions on 143 different products from Argentina, ranging from dried sweetcorn to infant formula and plywood. The move is being seen as an effort to curry favor with Argentina’s new, radical libertarian president, Javier Milei, who has vowed to shift his country’s orientation back to the U.S. and away from China.

- Our objective, quantitative methodology for predicting which geopolitical bloc a country will end up in currently places Argentina in the “Leaning China” camp, based in large part on Argentina’s strong commodity exports to China.

- Nevertheless, we think the U.S. and China will actively work to draw “Leaning” countries closer and away from their rival. With Milei threatening to reorient Argentina toward the U.S., it’s no surprise that Beijing has taken steps to curry favor with Milei.

- Going forward, many countries, especially those in the “Leaning” blocs, will likely be in a position to play the U.S. and China off against each other. To the extent that they can garner concessions from either of the big powers, those countries could see improved economic prospects and better stock returns.

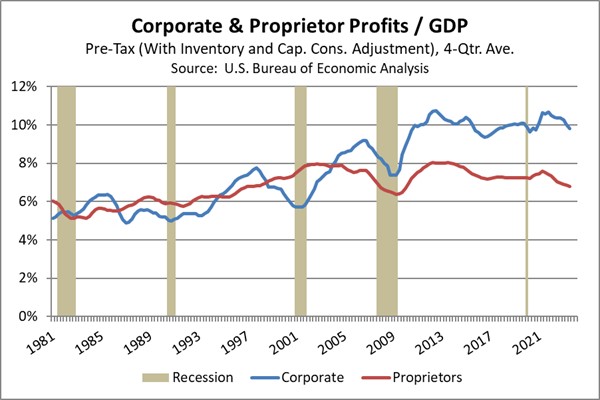

U.S. Economic Growth: New analysis cautions that the recent strong financial results at big companies may not be indicative of the overall corporate sector. Indeed, the analysis notes that while big firms’ earnings before interest, taxes, depreciation, and amortization (EBITDA) soared 18% from 2019 to the end of 2022, “middle market” companies with annual revenues between $100 million and $750 million saw their EBITDA fall 24% in the same period. That’s important because middle market companies account for a huge chunk of the U.S. economy and workforce.

- A range of other measures also reflect big advantages for big firms and tough challenges for smaller ones. For example, the advantages to size also show up in disparate EBITDA margins and differing trajectories for corporate profits versus sole proprietorships (see chart below).

- The tougher challenges for smaller firms could eventually prompt them to cool hiring, cap wage rates, and reduce investment, leading to stronger headwinds for the economy and financial markets.

U.S. Monetary Policy: In a further sign that the Fed has pivoted toward loosening monetary policy relatively soon, Dallas FRB President Logan in recent days delivered a speech calling for the Fed to slow its quantitative tightening program. We still think bond investors have gotten ahead of themselves in expecting sharply looser policy in the very near term, and we still think there is a risk that bond yields will rebound at least temporarily in the coming weeks and months. Nevertheless, the signs are starting to point more strongly to looser policy later in 2024.

Daily Comment (January 8, 2024)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM EST] | PDF

Our Comment today opens with a discussion of how the Houthi threat to shipping in the Red Sea is disrupting global supply chains and threatening to push up inflation again. We next review a wide range of other international and U.S. developments with the potential to affect the financial markets today, including a cut in Saudi Arabia’s oil export price and a budget agreement in the U.S. Congress that could avert another partial government shutdown or the need for another stopgap funding measure when the current one starts to run out later this month.

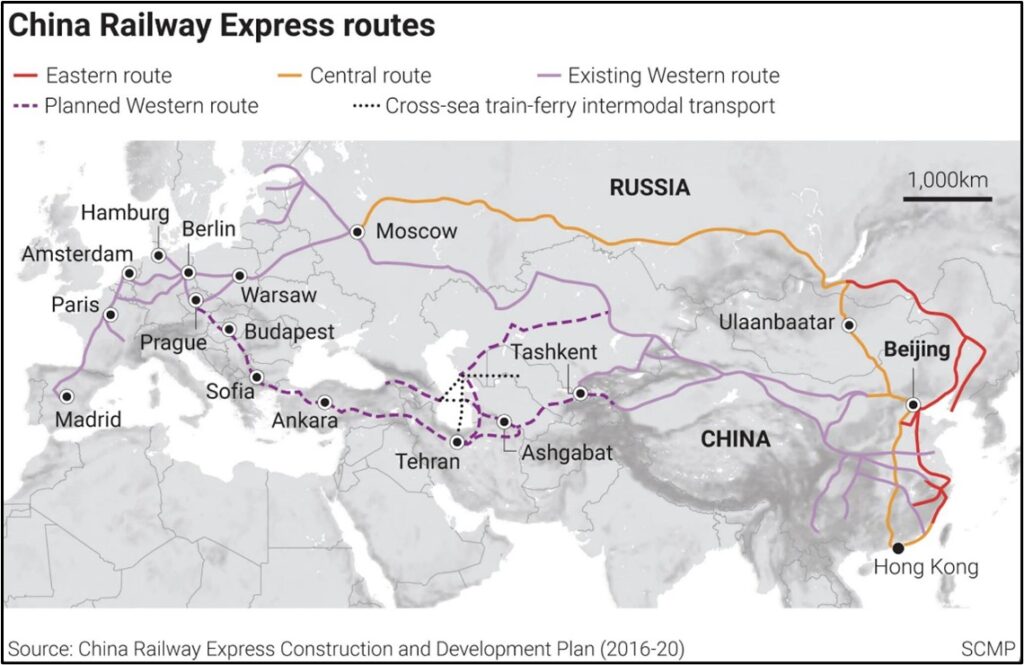

Global Supply Chains: As Houthi rebels in Yemen continue to attack commercial shipping in the Red Sea, shippers are increasingly worried that China won’t have enough shipping containers for its future exports. When firms carrying goods from China to Europe divert their ships away from the Red Sea and Suez Canal to the longer route around the Cape of Good Hope or shift to the overland China-Europe rail route (see map below), the delivery delay of up to two weeks means the return of half-empty containers to China will also be delayed.

- Any shortage of containers could stymie Chinese exports, further weighing on the country’s economic growth. Separately, Chinese electric vehicle makers are struggling to send their EVs to Europe because of an unrelated shortage of car-carrying ships.

- A surge of aggressively priced Chinese exports has been a key reason for the recent decline in consumer price inflation in the U.S. and the rest of the developed countries. Constricted Chinese exports and rising container leasing rates would therefore threaten to boost developed-country inflation again, complicating the major central banks’ calculus on when they could start cutting interest rates.

Global Oil Market: Today, Saudi Arabia cut the official selling price for its February oil exports. The cut reflects both rising U.S. oil production and slowing global energy demand because of factors such as China’s weak economic growth and high interest rates in many countries.

- We continue to believe that the outlook for oil is bullish over the longer term, but prices are likely to remain under pressure in the short term as global economic growth slows.

- In response to the Saudi price cut, oil prices have fallen approximately 3.3% so far this morning, with Brent currently trading at $76.19 per barrel.

Emerging Market Debt: In a new report, Fitch Ratings warns that higher global temperatures, rising sea levels, and increased flooding could lead to lower credit ratings for developing countries in the Asia-Pacific region that don’t adapt. The only country that Fitch identifies as safe is Singapore. The report warns that most other countries in Asia and South Asia will have trouble finding the resources to mitigate the risks.

Japan: Prosecutors have made their first arrests in the illegal political fundraising scandal that’s been dogging the administration of Prime Minister Kishida. Those arrested included Yoshitaka Ikeda of the ruling Liberal Democratic Party and one of his aides. Kishida announced that the party has expelled Ikeda, but the scandal nevertheless continues to weigh on the prime minister’s approval ratings and threatens his political power.

China: Now that Chinese home prices are no longer providing the strong investment returns that they used to, younger Chinese consumers are reportedly investing more in gold jewelry. Because of their enormous populations, India and China are already the world’s top consumers of gold jewelry. If Chinese demand accelerates further, it could conceivably give a further boost to global gold prices, just as recent purchasing by key central banks has done.

United Kingdom-China: The Chinese Ministry of State Security has accused the British secret intelligence service MI6 of recruiting a private-sector consultant from a third country to repeatedly enter the country, collect information, and try to recruit sources of information. The Chinese government has already cracked down on other Western data and due diligence firms, leading to some arrests. The new accusation is likely to further scare off Western professionals and prompt more Western companies to reconsider doing business in China.

United States-China: The top Republican and Democrat on the House Select Committee on the Chinese Communist Party have released a letter they sent to President Biden urging him to take stronger action to stem China’s growing dominance in the global market for older, less-advanced semiconductors, rather than just constraining China’s access to the most advanced chips, as the administration has already done. The lawmakers warn that the U.S. economy is becoming too dependent on workhorse chips from China.

- As we’ve discussed in the past, the worsening U.S.-China rivalry is driving a continued fracturing in global supply chains. Government and business leaders are likely to keep driving to cut dependence on critical, high-value goods from China, although many less important, low-value products are likely to continue being sourced from that country.

- The widening scope of the restrictions will continue to be a risk for companies that rely on Chinese inputs or sell to China.

U.S. Military: On Friday, the Pentagon announced that Defense Secretary Austin had been hospitalized in intensive care since New Year’s Day to deal with complications from an unspecified elective surgery. However, the incident created a scandal when it emerged that President Biden wasn’t informed about Austin’s hospitalization for three days, and that key members of Congress weren’t informed for four days.

- Deputy Defense Secretary Kathleen Hicks reportedly took on Austin’s duties while he was incapacitated, but only via secure communication links from her temporary location in Puerto Rico, rather than returning to Washington.

- The scandal is likely to raise pressure on Austin and lead to increased calls for his replacement. In any case, the scandal has the potential to disrupt the U.S. military’s on-going restructuring and adjustments to meet the rising challenge from China.

U.S. Fiscal Policy: Congressional leaders reached a deal yesterday on overall budget spending for the current fiscal year, potentially averting another partial government shutdown or stopgap spending bill when the current stopgap bill starts to run out later this month. The challenge now will be for Congress to pass the many individual appropriation bills that will turn the budget into law. Republican conservatives in particular are expected to oppose the spending total and demand riders that implement their preferred conservative policies.

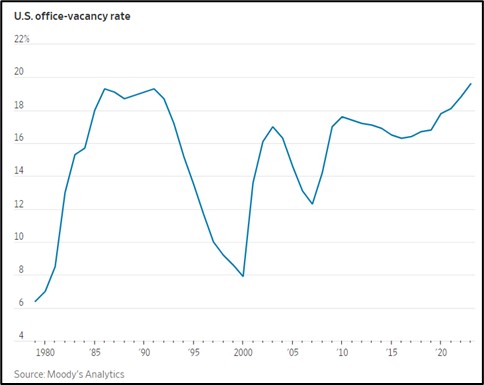

U.S. Commercial Real Estate Market: New data shows that a record 19.6% of office space in major markets was unleased in the fourth quarter, up from 18.8% one year earlier and slightly above the previous record of 19.3% in 1986 and 1991. The high vacancies reflect both previous overbuilding and the pandemic-inspired “work from home” movement. In any case, high vacancies coupled with high interest rates means the office sector remains an economic risk.

Daily Comment (January 5, 2024)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM EST] | PDF

Good morning! December jobs bury the bull market’s hopes, while Crosby and Bedard steal the NHL All-Star spotlight. In today’s Comment, we dive deep into the mysteries of the January Barometer, explore why the Magnificent Seven’s reign may be nearing its end, and analyze how Ukraine war fatigue might pave the way for de-escalation in Europe. As always, our comprehensive report encompasses the latest domestic and international data releases.

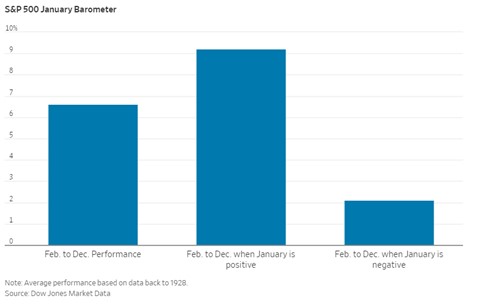

January Gloom: Equity prices are on track to finish the week down in a bad omen for financial markets.

- The weak start to January raises concerns about the rest of the year. Data from 1954 to 2023 reveals an unsettling pattern — in 11 out of the last 17 occurrences when January saw declines in both the first week and month as a whole, the S&P 500 finished the year lower. Rising interest rate concerns, fueled by mixed economic data, are driving this bearish sentiment. While the latest JOLTS report signaled that firms are slowing their hiring, both initial claims and ADP’s private payroll data suggest workers are having no trouble finding new work. Fueling anxieties further are the ongoing conflicts in the Middle East that threaten to disrupt energy supplies and exacerbate pre-existing inflationary pressures.

- This early-year phenomenon likely reflects investors’ tendencies to anchor expectations to limited data, seeking early signs for dominant themes. While the S&P 500 started 2023 with a decline in its first week, Microsoft’s (MSFT, $367.94) extended partnership with OpenAI, a leading artificial intelligence (AI) company, buoyed the index to a 6.3% gain by month’s end. Hopes for monetary easing have gripped investors since the last Fed meeting in December, where officials hinted at potential rate cuts in 2024, but these hopes have faced a sharp reality check. Investor expectations of a March rate reduction have drastically contracted, with the CME FedWatch Tool probability plummeting from 73.4% a week ago to 60.9% today.

- Just like in the lead-up to the climax of the classic romantic comedy When Harry Met Sally, investors will spend 2024 analyzing every move of the FOMC, trying to decipher the next step in their rate-cut tango. Will it be a graceful glide to lower rates or a clumsy stumble into recession? Prepare for a comedy full of “mumbling with great incoherence,” with investors caught between hope and frustration as the Fed navigates the economic tightrope. But remember, while monetary policy takes center stage, don’t forget the political circus happening backstage. Half of the world will be voting, and these elections could redraw the global economic map, which is also likely to have a major impact on financial markets.

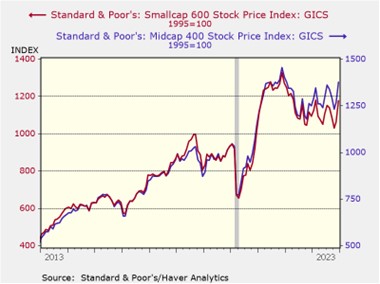

Tech Rally Over? Lower rates threaten the Magnificent Seven’s market dominance. Prepare for a changing of the guard.

- In an environment of high-interest rates and cautious investor sentiment, firms with significant growth potential and limited downside risk became particularly attractive investment targets. Large companies with exposure to AI technology, a field perceived to hold immense future potential, were among the most sought-after. Investors were drawn to these companies because the firms have the ability to grab market share in an industry that is expected to play a significant role in reshaping the economy. Consequently, the excitement over AI has led investors to neglect other sectors offering opportunities.

- The prospect of lower rates has helped shift investor attention toward stocks with a better value proposition. With a hefty P/E above 20, the S&P 500 looms large over its smaller rivals. Mid-cap companies, long overshadowed by big-name hype, finally saw their alluring P/E ratios attract renewed investor attention. Though initially buffeted by a 6.5% headwind in the first 10 months of 2023, the S&P 400 Mid Cap Index roared back with a vengeance, finishing the year an impressive 11.5% higher. At the same time, small-cap companies have had a similar performance, rising 13.9% to the end of the year.

- Market fundamentals favor a potential shift from large caps to smaller peers, but unforeseen headwinds like recession or rising rates could slam the brakes on the trend, dampening risk appetite and prompting caution. So far, all signs suggest that the Fed will be able to navigate a soft landing. The Atlanta GDPNow forecasts continued economic resilience with the economy expected to expand at a 2.5% annual rate in the fourth quarter. At the same time, Cleveland Fed data suggests the year-over-year change in core PCE inflation could dip below 3% this month, offering a glimmer of hope for risk-averse investors and potentially accelerating the shift towards smaller companies.

Fresh Ukraine Worries: The growing difficulty in supplying Ukraine with military equipment has fueled anxieties among Eastern European nations bordering Russia, who fear it could leave them more vulnerable to Russian aggression.

- Amidst the ongoing war in Ukraine, Latvian Foreign Minister Krišjānis Kariņš sounded the alarm, warning that Russia’s ambitions likely extend beyond Ukrainian borders and could pose a broader threat to Eastern European nations. He is pushing for the West to develop a longer-term strategy that will contain the ostracized country. His concerns come on the same day that the Pentagon stated that it had no funds left to replace weapons sent to Ukraine. Although there was $4.2 billion left for aid, it warned that the lack of additional funding may force the U.S. to pause its support

- With brutal new bombardments engulfing Ukrainian cities and Ukrainian counteroffensives pushing outwards, the need for further aid hangs precariously in the balance, shrouded in the uncertainty of allied agreement on a new spending package. The ongoing Congressional debate in the U.S., balancing domestic security concerns with foreign commitments, further clouds the picture. Meanwhile, Europe gropes anxiously for alternative solutions that don’t hinge on Hungarian approval, adding another layer of complexity to the already precarious situation. Ukraine’s stark assertion that no plan B exists beyond securing Western funding underscores the gravity of the situation and amplifies the pressure on allies to reach a decision.

- Though further Western aid for Ukraine does seem likely, its long-term sustainability remains on shaky ground, influenced by rising American anxieties about both securing their own borders and the escalating tensions in the Middle East. While America’s foreign policy focus is sharply rising, with four in 10 now saying it should be a top government priority — double the sentiment from a year ago — this change in attitude doesn’t translate directly to unwavering support for Ukraine. In fact, America’s focus on the war has dipped slightly from 6% to 5%. This shift in priorities could potentially make the West more receptive to a quicker peace deal.