Tag: pandemic

Asset Allocation Bi-Weekly – The Dip That Didn’t Bounce (March 2, 2026)

by Thomas Wash | PDF

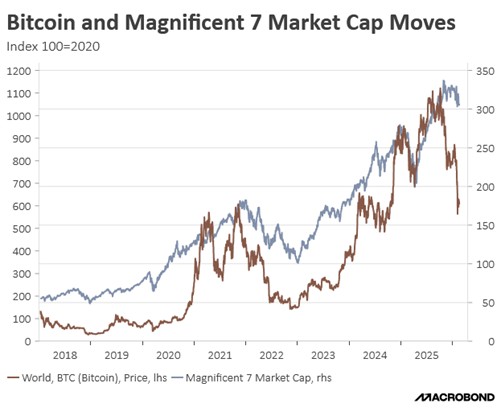

Retail investors have emerged as a crucial stabilizing force behind the ascent of the “Magnificent 7” in recent years. Rather than displacing institutional or ETF demand, their participation has added a new, resilient layer of support. This cohort’s propensity to buy and hold mega-cap tech stocks, even through periods of market anxiety, has helped sustain momentum and enthusiasm for these names, insulating them to some degree from the sharper sentiment swings affecting the broader market.

This distinct retail influence extends beyond equities, manifesting clearly in the behavior of Bitcoin. Estimates suggest that roughly two-thirds of Bitcoin’s supply remains in the hands of individual investors. Throughout 2024 and 2025, a notable correlation emerged, with Bitcoin and major tech and software names frequently moving in tandem. This parallel behavior reinforces the narrative that for many investors, particularly those with a higher risk appetite, mega-cap tech and crypto have effectively merged into a single, cohesive trade.

The sharp rise in Bitcoin and many tech-related stocks has coincided with a wave of new retail investors entering equity and crypto markets. This surge has been supported by pandemic-era stimulus payments, which boosted households’ risk-taking capacity, and by the rapid growth of easy-to-use, commission-free trading apps such as Robinhood, drawing many younger investors into markets for the first time. As a result of this new participation, the share of the daily trading volume of US equities attributable to individual investors went from the low single-digits pre-pandemic to nearly 20%.

This increased retail participation has pushed a larger share of market attention toward future growth potential and market themes, particularly in high‑growth technology and AI‑related names, rather than strictly traditional valuation metrics. Many retail investors have piled into rising tech stars, such as Nvidia, and into cryptocurrencies at the same time, often under the belief that prices would keep climbing, helping to cement a “buy‑the‑dip” mentality in which market pullbacks were frequently met with renewed retail buying.

This newer approach to investing has provided meaningful support to markets during periods of stress as it has been a source of incremental demand. Most notably, after President Trump’s “Liberation Day” tariff announcement sparked a sharp sell‑off, a strong wave of retail dip‑buying helped stabilize prices and fuel a powerful rebound. Also, brokerage and bank data indicate that retail investors’ returns around this episode and over 2025, as a whole, compared very favorably with many institutional strategies.

A major driver of this renewed wave of retail buying is the influx of younger investors into the market. Many of them have lived through a recession but have not experienced a deep, protracted equity downturn driven by widespread corporate failures. The only meaningful market pullback they recall is the 2022 episode, during which many of the hardest hit names later rebounded and went on to post extraordinary gains. As a result, many of these younger investors have held out hope that the equity market can help them accelerate their savings.

That said, retail investors — particularly younger cohorts — may prove to be a less reliable source of support for the market going forward. Using Bitcoin as a reference point, there are signs that individual traders have now become more risk‑averse, and this shift is starting to weigh on broader sentiment. This helps explain why the tech sector has seen limited upside so far this year, as investors continue to grapple with the true profitability of AI‑focused firms in light of their rising debt burdens and the threat they pose of triggering a broader “SaaS-pocalypse.”

While retail investors are likely to play a bigger role in markets over time, current uncertainty may prevent them from acting as buyers of last resort during future periods of stress. This growing risk aversion is especially likely to weigh on familiar large cap names in the technology sector. In our view, clients should pay closer attention to overlooked areas of the market as persistent pessimism toward mega‑cap tech could eventually drive a broader sector rotation as investors look to diversify into other industries.

The accompanying podcast for this report will be available later this week.

Bi-Weekly Geopolitical Report – The Great COVID Labor Reform (May 20, 2024)

by Patrick Fearon-Hernandez, CFA | PDF

The COVID-19 pandemic of 2020 is now starting to fade from memory. Four years after the sudden outbreak of the disease sparked mass economic shutdowns, mask wearing, and millions of deaths, it’s tempting to think the crisis is becoming just another episode of history. However, the pandemic clearly led to changes in the global economy. For example, it helped usher in an era in which governments and companies worry a lot about potential supply chain disruptions.[1]

In this report, we discuss how the pandemic changed the United States labor supply. We focus on two key developments during the pandemic: 1) the mass excess retirements and deaths of baby boomers,[2] and 2) the generous income support programs implemented by the federal government. Considering these developments as a package, we show how they essentially amount to a labor market reform — perhaps the most significant US labor market reform in decades. We then examine how these labor market changes could help spur outsized US economic growth in the coming years, albeit with additional upward pressure on consumer price inflation and interest rates. We wrap up by examining the implications for investors.

[1] This would not be the first time a pandemic affected the labor markets. The “Black Death” in the 1300s killed so many workers that the lucky survivors saw a jump in real wages. After the Spanish Flu epidemic of 1918, something similar occurred.

[2] The baby boomer generation is conventionally considered to be all those born from 1946 to 1964.

There will be no accompanying podcast for this report.

Asset Allocation Weekly – #45 (Posted 7/16/21)

Confluence of Ideas – #19 “The 2021 Geopolitical Outlook” (Posted 2/9/21)

Weekly Geopolitical Report – Revisiting Scheidel’s Horsemen: Part III (May 4, 2020)

by Bill O’Grady

In Part I of this report, we discussed Scheidel’s thesis on the events that reverse the normal trend of inequality and used this analysis to frame the COVID-19 pandemic. In Part II, we introduced the equality/ efficiency cycle and discussed the first issue that would be affected by a shift to equality. In this final Part III of the report, we will address the other four issues, discuss inflation and conclude with market ramifications.

Weekly Geopolitical Report – Revisiting Scheidel’s Horsemen: Part II (April 27, 2020)

by Bill O’Grady

In Part I, we introduced Walter Scheidel’s four horsemen and examined the impact of COVID-19 using his framework.[1] This week, we introduce the equality/ efficiency cycle and discuss the first issue that would be affected by the reversal of this cycle.

COVID-19 and the Equality/Efficiency Cycle

We postulate that economies pass through cycles of equality and efficiency. We developed this concept based on the seminal work of three scholars. The first strand is the idea of the equality/efficiency tradeoff, which comes from Arthur Okun.[2] He argued that societies face a tradeoff between equality and efficiency. Efficiency is necessary for growth, while equality is required for political and social stability. However, there is no evidence that Okun saw this tradeoff as a cycle; instead, he saw it as two competing forces to be constantly balanced.

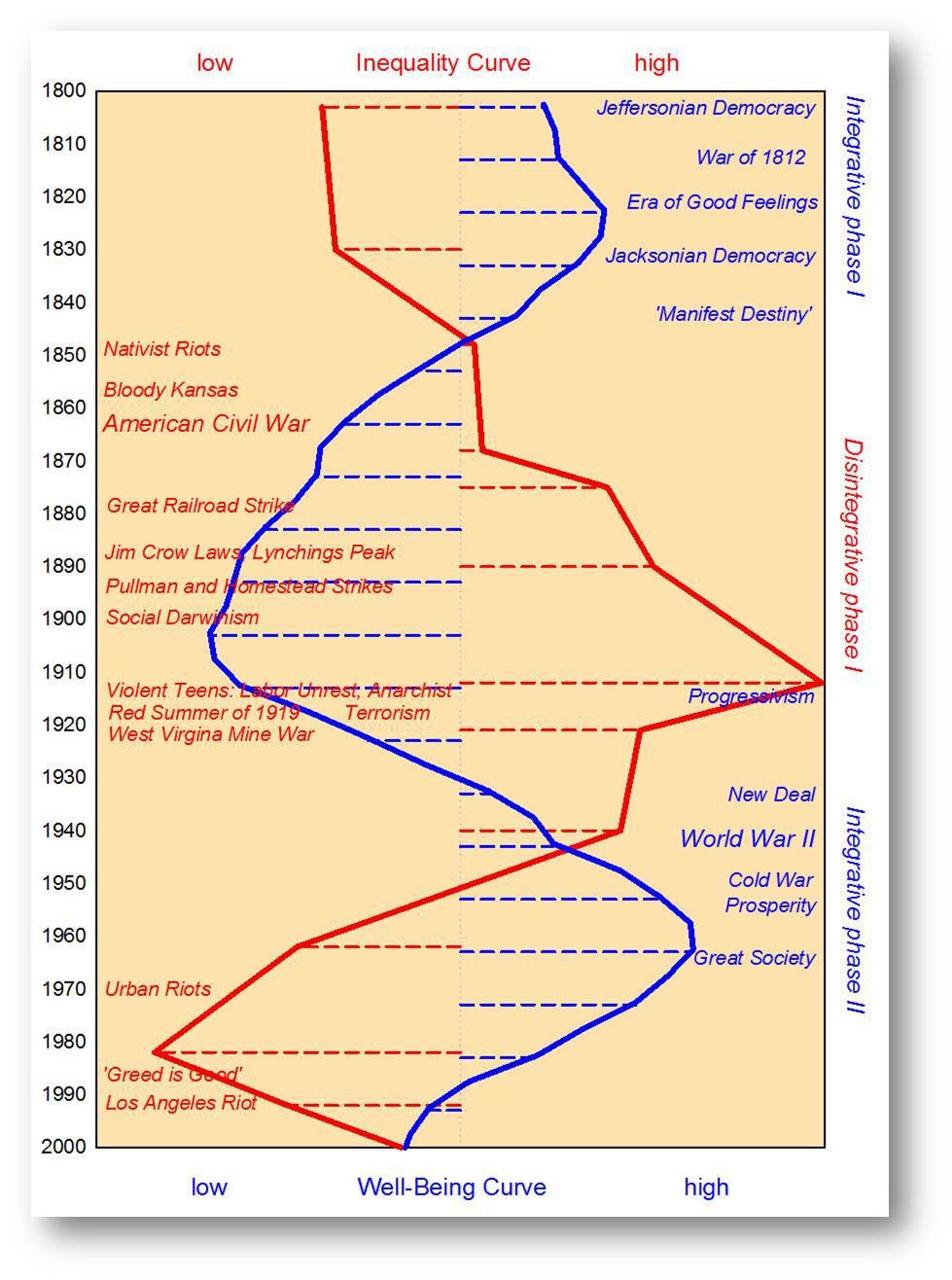

The second source of our postulate is from Peter Turchin, who suggested that countries cycle between periods of greater or lesser equality. In the following chart, Turchin shows this cycle in the U.S. from the early 1800s to 2000. Measuring inequality (red line) is a simple calculation that originated with Kevin Phillips. It is the ratio of the largest fortune in the U.S. relative to average household wealth. The well-being line (blue line) is the detrended and log-transformed level of social optimism, which is the average age of marriage, along with the wages of production workers divided by per-capita GDP, life expectancy and average height. The chart shows that well-being is inversely correlated to inequality.

The third source of our thesis comes from Walter Scheidel, who suggests that efficiency cycles are the norm due to the power of capital. Efficiency continues until it is stopped by one of four major disruptions: mass mobilization war, revolution, societal collapse or pandemic.

Therefore, our thesis is the following:

- Societies face a tradeoff between equality and efficiency.

- This tradeoff leads to cycles in which the goals of one or the other dominate.

- The natural course is for efficiency to dominate because capital tends to accumulate economic and political power over time.

- What reverses the dominant trend is a cataclysmic event, i.e., mass mobilization war, revolution, collapse of social order, pandemic.

- What reverses an equality cycle is persistent inflation, which is usually supported by equality policies of trade impediments, immigration control and regulation.

[1] Scheidel, Walter. (2017). The Great Leveler: Violence and the History of Inequality from the Stone Age to the Twenty-First Century. Princeton, NJ: Princeton University Press.

[2] Okun, Arthur. (1975). Equality and Efficiency: The Big Tradeoff. Washington, D.C.: Brookings Institution Press.

Weekly Geopolitical Report – Revisiting Scheidel’s Horsemen: Part I (April 20, 2020)

by Bill O’Grady

Although we do cover current events in the Weekly Geopolitical Report, we also try to anticipate changes that may be a consequence of current situations. The COVID-19 crisis is just such an occasion. We regularly update the current path of the virus in our Daily Comment, but we will consider the longer-term ramifications of COVID-19 in this report. We have recently discussed the pandemic, in general, in our weekly reports, and in the previous two installments we discussed how the virus has frayed relations in the EU.

This week, we frame the impact of the pandemic using Walter Scheidel’s book on inequality, The Great Leveler: Violence and the History of Inequality from the Stone Age to the Twenty-First Century.[1] We reviewed this book in a previous WGR published in 2017. In Part I, we will examine Scheidel’s thesis that says inequality tends to be resolved by violent or extreme events. Simply put, history shows little evidence that periods of high inequality are reversed without tragedy. Using this thesis, we will examine how the COVID-19 pandemic best fits into Scheidel’s framework. In Part II, we will discuss the equality/efficiency cycle and introduce one of five problems that could be resolved by the pandemic. In Part III, we will examine the other four problems, discuss the impact of inflation and conclude with market ramifications.

[1] Scheidel, Walter. (2017). The Great Leveler: Violence and the History of Inequality from the Stone Age to the Twenty-First Century. Princeton, NJ: Princeton University Press.