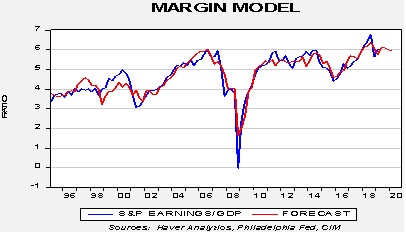

As wages and other costs rise and pricing power appears constrained, there are reasonable worries about the path of corporate earnings. We use purely top-down analysis to forecast earnings. Essentially, we forecast the percentage of total S&P company earnings relative to GDP. We use the nominal GDP forecast from the Philadelphia FRB’s Survey of Economists along with our earnings as a percentage of GDP forecast to arrive at our estimate; we do note that this estimate is for total earnings for all members of the S&P 500 and not the per share estimate.

We are currently expecting S&P earnings to equal around 6% of GDP.

There are a large number of components in the model but the most statistically significant are net exports as a percentage of GDP, credit spreads, the dollar and oil prices. The components suggest that margins will likely contract if the U.S. does move to reduce the trade deficit. A weaker dollar will help lift margins, and higher oil prices will tend to lift margins as well. Narrow credit spreads tend to support margins.

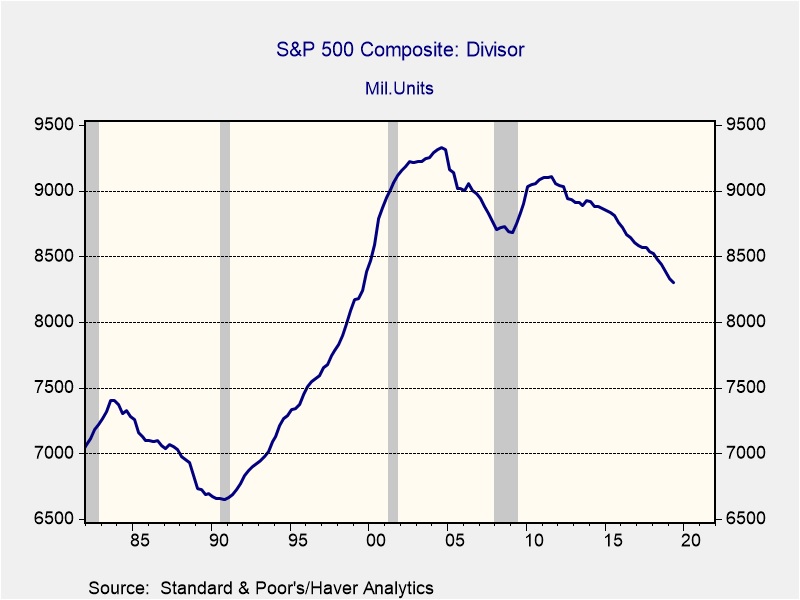

The process of getting to earnings per share is tied to the divisor of the index. And, that has been steadily falling, which is lifting earnings per share.

The divisor adjusts the index by accounting for mergers, the exchange of new companies into the index, and share issuance and buybacks. The persistence of share buybacks is clearly reducing the divisor which acts to boost earnings per share.

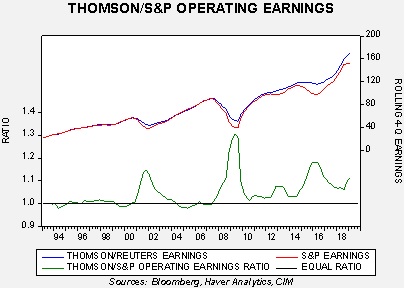

Adjusting for all these factors, our current forecast for earnings this year is $157.20, which is down from $160.93 at the beginning of the year. We do use Standard and Poor’s earnings data, which tends to be less than the more widely reported data from Thomson-Reuters; we use the former because we have a much longer history of that data. The current difference is significant. Thomson-Reuters data is about 11% higher than what is reported by Standard and Poor’s.

Our conversion model suggests a Thomson-Reuters earnings number of $168.92, which is well above the current consensus of $165.21. Given that we are working off a 3.8% nominal GDP growth rate (and so, 2% inflation would lead to a 1.8% GDP growth number), which seems achievable, the financial markets are probably too pessimistic on earnings for the rest of the year. If we are wrong, it’s probably due to margin contraction. Although there are worries about future policy causing margins to fall, the policy effect probably occurs next year, not in 2019.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EDT]

Happy Friday employment day! We cover the data in detail below but the snapshot is generally in line with expectations. Payrolls were 164k, nearly bang on forecasts of 165k, although revisions lowered payrolls by a net 32k. The unemployment rate was unchanged at 3.7% when a 3.6% report was expected. Wage growth was a bit stronger than expected (although the non-supervisory growth was steady) and the participation rate rose to 63.0%, a bit stronger than the 62.9% expected. Here is what we are watching this morning:

We doubt China will react well to this action. The Xi government has already indicated that a deal has to include the removal of all tariffs, which is unlikely. It’s important to note that Chairman Xi will be heading off to Beidaihe This seaside resort has been a long-time favorite of Chinese leaders going back to the Qing dynasty. CPC leaders, both current and former, mingle and discuss issues. We would expect Xi to find plenty of support to push back against the U.S. After all, no nation likes to be bullied. In addition, any criticism of Xi for poorly managing the relationship with the U.S. will likely be silent as Trump’s latest actions tend to confirm he is erratic and probably unmanageable.

As we have noted in the past, trade wars, like kinetic ones, usually occur because both sides miscalculate the actions of their opponent. We suspect President Trump is overestimating how damaging tariffs are to China and underestimating the impact on the U.S. Chairman Xi is probably doing something similar. In addition, we think President Trump continues to hold the position that the incidence of tariffs is falling solely on Chinese exporters. Although it is occurring to some degree, a weaker CNY is offsetting some of the pain. Additionally, some of the tax is falling on U.S. consumers and, as we note below, that effect will likely increase. However, if the president believes the incidence isn’t affecting American buyers, he will tend to view tariffs as a “free tax” and have no compunction about continuing to apply them to China and others. It should also be noted that S. trade negotiators knew the president was considering additional tariff measures before their most recent meetings with Chinese trade officials.

“Blinking” will be difficult for both leaders. It is hard to see how either side backs down without losing face. If President Trump backs down, it will be a campaign issue. If Chairman Xi backs down, he will face criticism for caving into foreigners.

China clearly can’t retaliate 1:1 simply because of the trade imbalance. So, look for other retaliationmeasures, e.g., harassing American foreign investment in China, perhaps the arrest of Americans in China or other penalties for American firms (regulatory raids, etc.). We could also see European firms given preferential treatment to harm U.S. competitors. Look for the “unreliable entities list” to reemerge to pressure U.S. firms to show allegiance to China instead of the U.S. And, the most simple action is to weaken the CNY, which is already occurring.

There is another angle to the president’s surprise. In Chair Powell’s press conference on Wednesday, he mentioned international economic weakness repeatedly. The new tariffs will almost certainly increase pressure on the Fed to cut more aggressively. In a sense, the tariff announcement may have more to do with affecting monetary policy than trade policy.

And finally, there is one other issue to consider. The president could be following the Mexican playbook and decide not to implement the tariffs on September 1st if China buys grain and cuts narcotics exports. Since the tactic worked with Mexico, he may believe it will work with China as well. Thus, there is a chance that nothing happens.

The market effects were swift. The following are intraday charts of various U.S. markets.

(Source: Bloomberg)

The S&P 500 fell over 60 points.

(Source: Bloomberg)

The 10-year T-note yield fell over 15 bps to decline under 1.90%.

(Source: Bloomberg)

The dollar weakened on ideas that a trade conflict would likely force the Fed to cut rates more aggressively.

(Source: Bloomberg)

This chart shows the 2-year T-note yield. Like it’s longer duration “cousin” that yield fell sharply, confirming the comment on the EUR above. In fact, the yield curve modestly steepened.

(Source: Bloomberg)

On the other hand, oil prices plunged on fears that a trade war will harm global economic growth. We are seeing some recovery in oil prices this morning.

We also note that tensions between the U.S. and China remain high; SoS Pompeo criticized China at the ASEAN meetings in Bangkok, a clear indication of deteriorating relations.

Tories lose: In a by-election in Wales, the Liberal-Democrats won the seat, reducing the Tory-DUP coalition to a single seat. The loss increases the odds of snap elections. Labour continues to struggle, as it didn’t perform all that well. The Liberal-Democrats ran on a platform to Remain in a district that voted to leave. Perhaps the signal for this election is that the most important issue is the “should I stay or should I go” decision and not the traditional issues of fiscal policy, foreign policy, etc. The risk of new elections could be that there is a swift realignment of the parties, where Remainers in the Labour and Conservative Parties move to the Liberal-Democrats and the traditional parties fall to minority status.

United States-Russia: Today is the day that the United States has officially withdrawn from the Intermediate-Range Nuclear Forces Treaty of 1987, in which Washington and Moscow agreed not to develop, test, or deploy certain ground-based nuclear missiles that were seen as particularly dangerous and destabilizing. The move, announced in February, follows the Russian deployment of a ground-based cruise missile in violation of the accord. That violation was real enough, but we note that the immediate U.S. response didn’t have to be a complete withdrawal from the pact. The U.S. side is apparently gambling that in order to free its hands to develop its own new weapons to counter a rising China, it would be worthwhile to sacrifice stability in Europe. As we’ve already seen in the U.S.-China trade dispute, the Western Europeans are the main losers, at least in the immediate term. Separately, President Trump has belatedly imposed new financial sanctions against Russia for using the nerve agent novichok in its effort to assassinate former double agent Sergei Skripal in England during March 2018. Under law, the administration was required to impose those sanctions last year, but resisted until Congress recently raised pressure on it with a number of new Russia sanctions bills.

United States-European Union: As we mentioned yesterday, it’s important to remember that while the overall global trade picture continues to slide, there are smaller-scale improvements from time to time. Today, for example, the United States and the European Union will sign an agreement giving U.S. beef producers more access to the EU market. The deal is a direct result of the Rose Garden meeting last summer between President Trump and European Commission President Jean-Claude Juncker.

International Monetary Fund: The European Union’s finance ministers will vote today on their candidate to succeed Christine Lagarde as head of the IMF. The Europeans traditionally name the IMF chief, while the United States names the head of the World Bank. Frontrunners for the IMF job include former Dutch Finance Minister Dijsselbloem, Finnish Central Bank Governor Rehn, Spanish Finance Minister Calviño, and Bulgarian World Bank executive Georgieva. The unusual need for a vote reflects disagreement between Europe’s more affluent northern countries and the less developed southern nations.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EDT]

Good morning! Markets are dealing with the aftermath of the Fed meeting. China is slow-walking trade. The BOE met today. Osama bin Laden’s son is believed to have died. The MLB trade deadline big winner was Houston, with Atlanta coming in a close second. Here is what we are watching this morning:

The Fed: The FOMC generally did what was expected—the fed funds target was reduced by 25 bps and quantitative tightening has ended. However, beyond that, the financial markets view the Fed’s action as relatively hawkish. First, Chair Powell characterized the policy actions as “a mid-cycle adjustment.” This comment, coupled with confirmation later in the press conference, suggests that this rate cut doesn’t signal a new rate cutting cycle. Instead, to use a historical context, it is more like 1995. Essentially, the Fed has admitted it moved rates too high and is adjusting rates to a level better suited to current conditions. Powell did suggest that yesterday’s cut may not be enough for current conditions, but if the financial markets thought this was the beginning of 100 bps of easing into early next year, that probably isn’t the case.

Powell did note that the rate cut was also tied to the perceived decline in “neutral rate” which does indicate the Phillips Curve model still has some influence on members of the FOMC. He mentioned global concerns and the trade conflict as well. Although these issues do offer a potential path for future easing (e.g., weaker overseas growth could trigger additional rate cuts), these factors probably are less important than they appear. The dissents tend to undermine these other issues as having an effect on future rate moves.

Specifically, there were two dissents. KC FRB President George’s dissent was no surprise. She is a traditional hawk that would rely on the Phillips Curve for guidance. Given that labor markets remain tight, it is consistent that she would oppose the action. Boston FRB President Rosengren’s dissent is far more interesting. He is what we would characterize a “financially sensitive” voter; his opposition to a rate cut is based on the idea that it would lead to excessive risk taking in the financial markets. We examined this class of voter in an earlier AAW. In general, what we found was that when the 12-week moving average of the VIX was below 20, this class of voter tended to support rate hikes. And so, the recent drop in the VIX probably explains Rosengren’s dissent, which was telegraphed. With two dissents, the odds of further rate cuts will be challenging.

Financial markets reacted by treating the action as hawkish. Gold prices fell, the dollar jumped, the yield curve flattened and equities slid. To some extent, the reaction was probably a bit excessive but it is clear the financial markets wanted more and are now bringing back the risk of recession. President Trump was critical of the easing, suggesting it was inadequate.

Interestingly enough, the two-year deferred Eurodollar futures implied rate didn’t change. Although the spread compared to fed funds narrowed because of the cut, the projection of fed funds two years from now is still on pace for the 1.65% level (or a ceiling rate of 1.75%), meaning that three more rate cuts remain imbedded in financial markets.

In the final analysis, if Chair Powell wanted to move more than what we saw yesterday, he hasn’t convinced enough members of the committee to follow him. There were two significant clues for the Fed from the actions of the financial markets. The first is the yield curve. If the financial markets viewed the easing as stimulative, the yield curve would have steepened. The fact that it flattened is a clear indication the financial markets believe the Fed move and the consequent signaling was inadequate. The second is strengthening of the dollar. Given the dollar’s current high valuation, a policy change to easing should have led to a weaker greenback. The fact it rallied suggests the action was taken as non-stimulative. We should also note that the Fed’s modest action is occurring in a backdrop where the ECB is considering more aggressive actions and the BOJ is looking at allowing the JGB’s to fall into deeper negative territory.

The White House has been increasing its focus on the exchange rate markets, in our opinion, because the president has figured out that currency depreciation blunts the impact of tariffs. Although the Treasury has exchange rate policy in its mandate, it has limited tools to affect the rate.[1] As we have been discussing, the White House appears, at least to us, to be moving toward undermining Fed independence in order to fix the dollar’s exchange rate lower. Interestingly enough, now Congress is getting involved. Senators Baldwin (D-WI) and Hawley (R-MO) have introduced a bill that calls for a weaker dollar. It is starting to look a little like 1985 and the run-up to the Plaza Accord.

Iran: The U.S. has applied personal sanctions to Javad Zarif, Iran’s foreign minister. This action will make it more difficult to begin negotiations. However, the U.S. has also granted waivers to foreign nations participating in Iran’s civilian nuclear projects.

In what may be a new front in the U.S.-China trade dispute – or at least a new sore point – U.S. authorities have indicted a Chinese aluminum magnate on charges that he sidestepped anti-dumping duties on millions of pallets of aluminum brought into the United States from 2011 to 2014. The U.S. attorney for the central district of California said Liu Zhongtian’s “rampant criminality” not only posed a threat to U.S. industry, livelihoods, and investments, but also artificially inflated the value of his Hong Kong listed China Zhongwang Holdings (1333.HK, 3.44). More broadly, the U.S.-China trade dispute continues to weigh on manufacturing throughout the Asia-Pacific region. As shown below, the latest Markit purchasing managers’ indexes show factory activity continued to decline during July in Japan, South Korea and Taiwan.

Hong Kong: The commander of the Chinese military garrison in Hong Kong has warned that the city’s increasingly violent political protests are “absolutely impermissible.” In addition, the People’s Liberation Army released a video showing how the Hong Kong garrison is training to suppress mass protests. The speech and video are being taken as a warning to Hong Kong’s anti-Chinese protestors that the military is itching to clamp down on them. As a clamp down starts to look more and more likely, we would expect increasing economic disruption in Hong Kong and further headwinds for Chinese and Hong Kong assets.

Japan-South Korea: The Japanese government is preparing to take South Korea off its list of export destinations enjoying eased trade rules as early as tomorrow. The move is in retaliation to South Korea’s continued legal maneuvering to gain compensation for its treatment by Japan before and during World War II. The move would require Japanese exporters to obtain licenses before they export a wide range of chemicals and electronic goods to South Korea, compared with the controls that have already been imposed on just three chemicals. No licenses have been granted for exports of those three chemicals, seriously crimping South Korean computer chip manufacturers.

United States-Japan-Brazil: In spite of the overall global trend toward protectionism and trade disputes, there are some small signs of cooperation, too. For example, U.S. Trade Representative Lighthizer will meet today with Japanese Economic Revitalization Minister Toshimitsu Motegi to accelerate work on a U.S.-Japan free-trade deal. Separately, Brazilian Economy Minister Paulo Guedes said yesterday that Brazil and the United States are now officially in negotiations for a deal.

Where’s Boris? He was in Northern Ireland yesterday. Just like what we saw in Wales and Scotland, his reception was rather cool. Northern Ireland hasn’t had a local government because none of the parties can form a government so the area’s affairs are being run from Westminster. Although Johnson’s coalition is dependent on the DUP for support, Johnson argued he would be an impartial arbitrator in establishing local government. To a great extent, the Irish border is probably the most contentious issue with Brexit; if Ireland were unified, exiting the EU would be much easier. The Republic of Ireland is considering plans to establish border controls on its soil to protect the EU’s trading area.

Energy update: Crude oil inventories fell 8.5 mb, well more than the 2.5 mb expected.

In the details, U.S. crude oil production rose 0.9 mbpd, recovering from the hurricane induced curtailment. Exports fell 0.4 mbpd but import declined 0.7 mbpd. Refinery operations fell 0.1 mbpd.

(Sources: DOE, CIM)

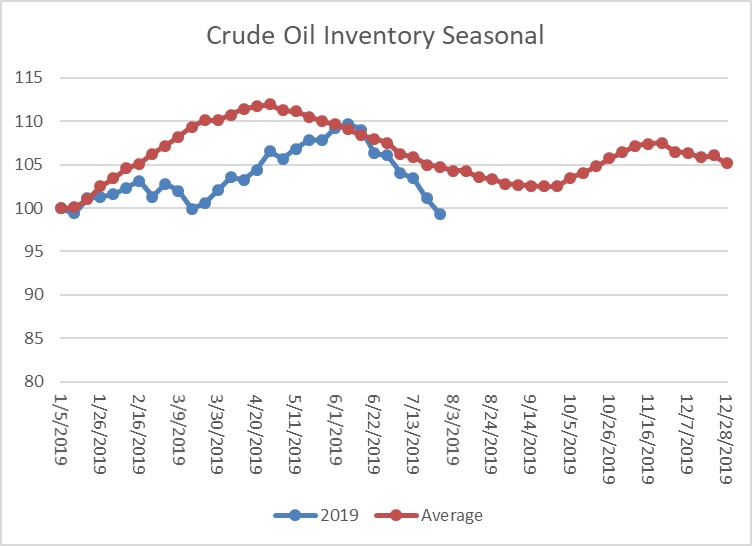

This chart shows the annual seasonal pattern for crude oil inventories. The decline seen over the past few weeks now puts the level below the usual seasonal trough in September. This decline in stockpiles is supportive for prices.

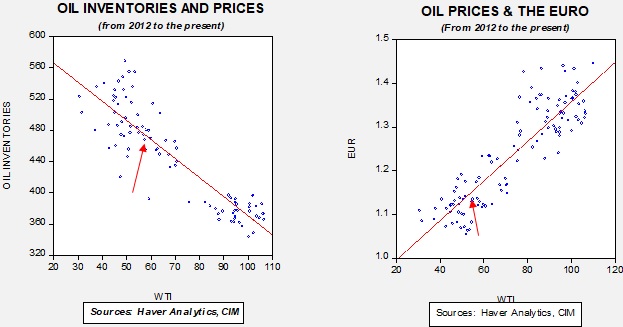

Based on our oil inventory/price model, fair value is $62.23; using the euro/price model, fair value is $51.84. The combined model, a broader analysis of the oil price, generates a fair value of $54.73. We are seeing a clear divergence between the impact of the dollar and oil inventories. If President Trump is successful in bringing the dollar lower, it would be bullish for oil prices.

[1] In reality, the Treasury’s mandate on forex is something of a holdover from the days of fixed exchange rates. In that period, the Treasury, working on behalf of the executive branch, would manage negotiations with other nations on the level of the exchange rate and instruct the Fed to take actions to maintain the peg (in an earlier period, against gold, later against other pegged rates). Under floating rates, the Treasury has limited tools to intervene to adjust the currency and can “jawbone.” However, monetary policy has a much larger impact.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EDT]

Good morning! The FOMC meeting ends today. North Korea continues to fire off missiles. The baseball trading deadline occurs at 4:00 EDT today. Here is what we are watching this morning:

The Fed: Yesterday, we noted the scenarios for today’s monetary policy. To repeat, there is almost no chance the Fed won’t cut by 25 bps today. Instead, there are two factors that could offer insights into future actions. First, Powell’s language, especially in the press conference, will be important. The key word is “patient.” If the statement includes the word “patience,” it will signal that this rate move is a recalibration, suggesting the policy rate overshot its equilibrium level and the move was an adjustment. However, it won’t indicate that this cut is the start of a rate reduction cycle. If this is the outcome, markets will be disappointed and we could see equities decline. Second, there could be action on the balance sheet. The Fed might announce that it will end its balance sheet reduction six weeks earlier than planned. Although modestly supportive, this action would be a dovish signal.

We are starting to see more of monetary policy discussion being framed by exchange rate concerns. The ECB appears to be teeing up additional stimulus, including a deeper foray into negative interest rates and expanding QE. Some pundits are suggesting the Fed is being forced to move on rates to prevent further dollar appreciation. There is an element of truth to this charge. Central bankers and finance ministers have been careful not to couch their policy actions in terms of affecting exchange rates. In fact, in the unwritten rules of central banking, such discussions would be in bad form because they could open up a return to the 1930’s “beggar thy neighbor” devaluations that eventually led to a collapse in trade activity. However, in reality, much of the monetary stimulus came from currency weakness. After all, if you drive nominal rates below zero and you still can’t increase investment, what’s left? Export growth! Abenomics got most of this punch through a weaker yen, but because officials framed the actions as necessary for domestic growth, other central bankers essentially granted Japan a pass. President Trump doesn’t buy this ideology; he wants the Fed to cut rates by more than 25 bps to weaken the dollar.

At some point, this race to the bottom will end; one possibility is that we return to some sort of fixed exchange rate system but that might require central banks to focus solely on the exchange rate to set policy. But, before we get to some sort of resolution, continued attempts to weaken currencies is possible; the investor solutions are monetary assets, e.g. precious metals.

Trade: The first post G-20 meeting between U.S. and Chinese trade negotiators has come to a close. Not too much progress appears to have been made. China has agreed to buy some grain, but only to the extent consistent with “internal demand.” We also note that China is showing increasing interest in sourcing soybeans from South America. The U.S. will probably offer some tech relief but it is starting to look like both sides are digging in and awaiting the end of the next U.S. election cycle. This isn’t the worst outcome, which, specifically, would be a complete rupture of trade relations. In fact, the “slow walking” gives both sides a chance to adjust. The next round of face-to-face talks won’t take place until September.

North Korea: Kim doesn’t want to be ignored. As the U.S. and South Korea prepare for military exercises, for the second time in a week, Pyongyang has tested short-range missiles. North Korea has always been concerned about military exercises, fearing that they could be a pretext to invasion. Despite that fact that it hasn’t ever occurred, the worry is understandable. So far, the tests have not crossed any “red lines” such as entering Japan’s territorial waters or a long-range test that would threaten the U.S. We would not expect an overt threat to the U.S. from North Korea.

Hong Kong: U.S. officials are watching the buildup of Chinese forces on the Hong Kong border with interest. So far, Beijing has been content to allow local officials to handle the unrest but we doubt that the Xi regime has infinite patience on this issue. Perhaps the most important reason why China has been reluctant to crack down on the protestors is it knows Taiwan is watching. A harsh crackdown on Hong Kong will make it difficult for Beijing to convince Taiwan’s citizens that unification will preserve its democracy. Reports that China is restricting tourist visits to Taiwan did catch our attention. If Xi concludes he cannot tolerate continued unrest in Hong Kong and uses the military to restore order, it may mean that unification with Taiwan can only be accomplished by force. And if that decision is made, it comes down to timing.

A softening on Iran? The Trump administration is apparently going to reissue waivers that allow foreign nuclear projects in Iran to continue. Iran hawks argued against the extensions, including NSD Bolton and SoS Pompeo. At the same time, the U.S. has formally asked Germany to participate in maritime security operations in the Persian Gulf. This request will be difficult for Germany to manage; on the one hand, it believes the U.S. has caused this crisis by leaving the JCPOA, so why should it work to fix a problem it didn’t cause. On the other hand, if they don’t participate, it looks like Germany is continuing to “free ride” U.S. security. After all, it is clearly benefiting from U.S. protection of Persian Gulf shipping.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EDT]

Good morning! The FOMC meeting begins today. The GBP continues its slide. Here are the details:

The Fed: Although there is almost no chance the Fed won’t cut by 25 bps tomorrow, we are watching for two items. First, Powell’s language, especially in the press conference, will be important. The key word is “patient.” If the statement includes the word “patience,” it will signal that this rate move is a recalibration, suggesting the policy rate overshot its equilibrium level and the move was an adjustment. However, it won’t indicate that this cut is the start of a rate reduction cycle. If this is the outcome, markets will be disappointed and we could see equities decline. Second, there could be action on the balance sheet. The Fed might announce that it will end its balance sheet reduction six weeks earlier than planned. Although modestly supportive, the action would be a dovish signal.

Regardless of what happens tomorrow, we doubt the White House will be happy about it. The president wants a weaker dollar and he wants the Fed to engineer that outcome. If the reserve currency nation attempts to restrict trade, its currency will appreciate. This is because there is always demand for the reserve currency and the most effective way to acquire it is to run a trade surplus with the reserve currency nation. The best way to prevent the currency from appreciating is for the reserve currency nation’s central bank to peg an exchange rate and adjust its balance sheet to ensure the peg holds. This is what Switzerland’s central bank, the Swiss National Bank (SNB), has been doing relative to the EUR for the past few years. However, such a policy essentially ends central bank independence; the SNB’s policy is completely subsumed to exchange rate policy.

Trade: Although talks are underway, there is little movement toward a grand resolution. As we noted yesterday, China appears to be buying some U.S. grain. The U.S. is offering unspecified relief on tech exports. However, beyond these two actions, not much else is happening. As the U.S./China trade spat continues, companies have been moving supply chains out of China. They haven’t brought production back to the U.S. but are going to other low labor cost areas, e.g., Vietnam. This development has caught the attention of USTR Lighthizer who is now calling out Vietnam for its trade surplus with the U.S.

For those wondering if a new president would lead to a change in trade policy, we doubt it. In fact, it may become more protectionist. Elizabeth Warren’s recent comments on foreign policy are classic Jeffersonian (which leans isolationist) and her trade policy would probably be more protectionist than Trump’s. What this suggests is that the president’s foreign and trade policy may be less about him and more about the direction the country is headed.

A peek inside China’s foreign reserves: For the first time ever, China has released some details about its foreign exchange holdings. The data isn’t up-to-date (the last data available is 2014). But, it does show the State Administration of Foreign Exchange (SAFE) reduced its dollar holdings from 79% in 2005 to 58% by 2014. It shifted to EUR and other currencies, along with gold.

Health care transparency: Economists have debated the problem of health care costs for some time. Although measures to open the industry to competition should reduce costs, there are specific structures in the industry that defy standard market remedies. It is almost impossible to comparison shop for treatment because it is difficult for the average consumer to evaluate quality. And, even if one wanted to shop around, getting accurate price information is devilishly hard. The Trump administration has proposed measures to disclose price information; the fact the hospital industry is upset with the proposal suggests it probably would undermine its profit structure.

Japan: The Bank of Japan today held its monetary policy unchanged, with its benchmark short-term interest rate at -0.1%, its ceiling for 10-year bond yields at 0% and its pace of government bond buying at 80 trillion yen. However, in a sign that the BOJ is ready to join the other major central banks that have been loosening policy, the officials also vowed further monetary easing without hesitation “if the momentum towards our price stability objective is at risk.”

Hong Kong: The deputy leader of Hong Kong reportedly apologized for the way the city’s police force responded to last week’s incident in which thugs from criminal gangs beat anti-Chinese demonstrators. That sparked a protest by police officials, possibly pointing to cleavages within the municipal government regarding how to handle the ongoing political protests.

Venezuela: Although President Nicolás Maduro still publicly embraces socialism and castigates capitalism, the government is quietly embracing free markets in an apparent last-ditch effort to help the economy and stay in power. Private business owners say rules banning hard-currency transactions have not been enforced recently, importing has been freed, and many price controls have been dropped. The reporting says the economy is rapidly dollarizing, while inflation has fallen from more than 100,000% last year to an expected level of several thousand percent this year.

Last week, we referenced the basic philosophies of David Hume and Adam Smith and how their writings evolved into the economic theory of supply and demand. From there, we examined the weakness of supply and demand at the macro level and discussed an alternative model, the Economic Triangle, as a different means of explaining how various economic participants operate and the way in which political factors affect the triangle. This week, we will show how the Economic Triangle fits into the major economic systems, offer two contemporary examples and conclude with market ramifications.

The Theories

The history of economic thought and political economics has generated a plethora of theories and paradigms for balancing these interests. Here are some of the important ones:

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EDT]

Happy Monday! It’s Fed week. The MLB trading deadline is Wednesday. There was unrest around the globe. Here are the details:

The Fed: It is all but certain the FOMC will cut rates on Wednesday. Former Chair Janet Yellen came out in support. However, once this action occurs, there is great uncertainty as to what follows. There is growing doubt that this cut is the beginning of a cycle of reductions, even though it is obvious that this is what the market expects. If this week’s reduction is isolated, it would suggest the Fed overshot its rate hikes and is adjusting to correct the action. That would argue for a pause after this week’s reduction. In addition, it appears to us the FOMC is divided on how to move forward. We would not be surprised to see a dissent to the cut (KC FRB President George would be the most likely.) If the Fed stands pat for a couple of meetings, dovish dissents are likely. If we move into a period of “will they or won’t they” it is possible that equities will be rangebound for the next month or two.

China has used export promotion as a development model. In that model, policies to generate saving are implemented. China purposely has restrained household consumption with an undervalued exchange rate and low saving deposit rates. If the private saving balance is negative (investment < private saving) and the fiscal account is balanced, by definition, a trade surplus will occur. However, this is only if there is a ready buyer for the exports. The U.S. has played the role of “importer of last resort” for the world since the end of WWII but is pushing back against that policy. As the U.S. restricts imports, the excess production will show up in the national income accounts as unintended investment, better known as “inventory”. In other words, the private saving sector is forced into balance through unintended inventory accumulation. If China wants to continue to export, it must further constrain consumption and drive down export prices. Or, it can address the excess inventory by absorbing it with fiscal spending (which is a bit of what it is doing with infrastructure spending.) Of course, another alternative would be to abandon export promotion altogether and absorb the excess with domestic consumption. That doesn’t appear to be happening. What the above article indicates is the U.S. policy is having an impact.

Protests in Moscow: There were also major political protests in Moscow this weekend, as people demonstrated against the effort to keep opposition candidates off the ballot for the upcoming municipal elections (see our Weekly Geopolitical Report for July 15.) The response from police was unexpectedly harsh, but even more ominous was what happened to opposition leader Alexei Navalny: After being arrested last Wednesday for fomenting the demonstrations, he was rushed from the local jail to the hospital after he suffered an “allergic reaction.” Given Moscow’s history, this sparked concerns that ruling officials may have poisoned Navalny in an effort to silence him. While the U.S. government traditionally would have pushed back against such authoritarian transgressions, the reaction so far has been relatively muted. It is possible the rather aggressive response suggests Putin is signaling to the factions within the Kremlin that he remains in power and that they shouldn’t consider siding with the protestors. There have been sporadic protests around the country this year over a myriad of issues, including overflowing garbage dumps and poor economic growth. The leaders of authoritarian governments are usually at greater risk to insiders abandoning the leader rather than to internal pressure.

Iran: The Iranian government has thrown cold water on expectations that the United Kingdom and Iran could agree on an exchange of oil tankers, each has seized from the other, over the last couple of weeks. Iran has decided to link the British seizure of an Iranian oil tanker to the nuclear deal, which will put that deal under further strain. Britain has sent a second Royal Navy vessel to the Persian Gulf to protect U.K. shipping. That should help keep alive some of the tensions in the Persia Gulf, buoying oil prices.

South Africa: Although President Cyril Ramaphosa has been planning a constitutional amendment to allow land seizures and redistribution to the black majority without compensation, a government advisory panel has urged him to set strict limits on any such seizures. The proposed law has soured investor sentiment on South Africa in recent months.

Japan: The Cabinet Office has cut its forecast of economic growth to just 0.9% in the fiscal year ending March 2020, compared with 1.3% in its forecast six months ago. The cut stemmed mostly from slowing export growth arising from weak demand in China and protectionist trade policies in the United States.

[1] Just a thought: We have noted rising concern about foreign interference in U.S. elections. Although such attempts are nothing new, the ability to use social media has become a significant force multiplier for all sorts of actions to sway public opinion. We could end up with a “free for all” in 2020, where Russia and Israel might prefer to keep Trump in office while China and Iran would rather see him ousted. Since all four nations have sophisticated cyber capabilities, social media could be flooded with conflicting campaigns, all trying for different outcomes.

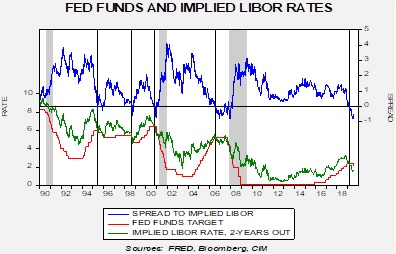

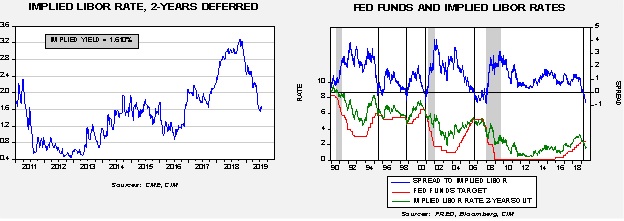

How much attention is the FOMC paying to international factors? It appears to be quite a lot. We have documented that the financial markets are clamoring for a rate cut. We have seen some of the more popular yield curves invert and the implied LIBOR rate from the Eurodollar futures market, two years deferred, has moved into easing territory.

The chart on the left shows the aforementioned implied LIBOR rate. In Q3 last year, the implied rate was 3.30%; it has fallen to just above 1.60%, a decline of 170 bps. The chart on the right compares the implied rate to the fed funds target. When this implied rate falls below the target, it is a signal to policymakers that monetary policy is too tight. The Bernanke Fed mostly ignored this indicator, unlike his predecessor, and Bernanke had to deal with the deep 2007-09 recession. This indicator is giving clear evidence that the Fed should be cutting rates aggressively.

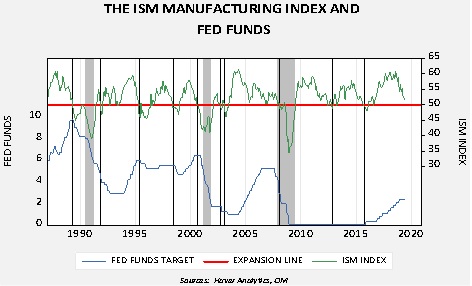

However, the signals from the domestic economy are not supporting a rate cut. The ISM Manufacturing Index is well above 50; since the Federal Reserve began confirming the policy rate, it is rare to see rate cuts when the index is above 50.

We have indicated when the ISM index falls below the 50-expansion line with vertical lines. The only time we saw significant rate cuts without the ISM index below 50 was in 2007, when financial markets were under clear stress. In May 2007, the Chicago FRB National Financial Conditions Index, an index of financial stress, was reading -0.67.[1] By August, it had risen to -0.13 and turned positive in November.

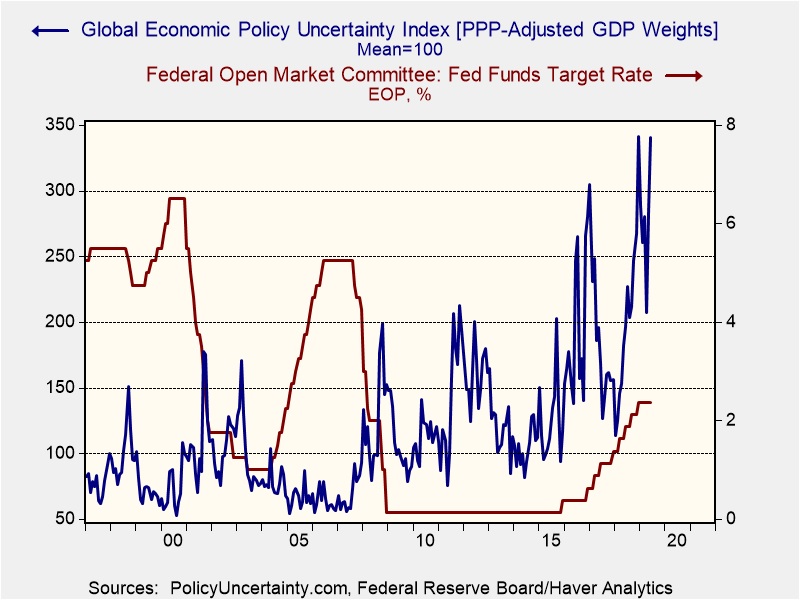

In this cycle, international pressures seem to be guiding policymakers to act.

This chart shows the fed funds target with the Global Economic Policy Index. This index measures mentions of economic or policy uncertainty in 20 nations; the index is weighted by GDP, adjusted for purchase power parity. A rising reading suggests increases in policy uncertainty. This chart supports Chair Powell’s continued references to overseas issues when calling for easing.

To some extent, there is a worry among market participants that the Fed is simply creating a narrative to allow it to ease, reducing pressure from the White House while maintaining some element of independence. The third chart suggests the Fed does have good reasons for acting to lower rates. With trade wars, the immigration crisis in Europe and the U.S., the potential for conflict in the Middle East and worries about a currency war, the level of global policy uncertainty is historically elevated. This factor, we believe, reflected in the financial markets, is what is prompting the desire to cut rates. We do expect a significant level of dissent among FOMC voters but, in the end, we look for two rate cuts this year, unless global stress levels unexpectedly diminish.

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EDT]

Happy Friday! As slow as the news is trickling in today, it’s clear that we’re deep into the dog days of summer. Nevertheless, we have seen a few interesting tidbits, like an initial estimate showing moderate economic growth and falling inflation here in the United States. Overseas, it looks like we’re in for another weekend of mass political protests in Hong Kong. Here’s what we are watching most closely:

U.S. economic performance: In the first of three regular estimates, U.S. gross domestic product (GDP) grew at an annualized rate of 2.1% in the second quarter, beating expectations but still marking a slowdown from the unrevised 3.1% rate in the first quarter (see additional details below). Compared with the same period one year earlier, GDP was up 2.3%. That means growth over the last year was slightly better than the average annual increase of 2.1% over the last two decades. As usual, most of the growth over the last year came from increased personal consumption spending. Finally, in a broad measure of inflation, the second quarter GDP price index rose at a rate of 2.4%, rebounding from its dip to 0.9% in the first quarter, which is still generally moderate. We don’t think these figures will change expectations for the Federal Reserve’s policy meeting next week. If anything, slowing growth coupled with moderate inflation should bolster expectations for a cut in the benchmark fed funds rate.

U.S. fiscal policy: The House of Representatives late yesterday approved the White House Democratic compromise bill to lift the federal government’s debt limit and establish high-level budget parameters through July 2021. If the bill now passes the Senate as expected, it would remove the risk of a debt default or new government shutdown until after the 2020 presidential elections. Separately, the White House announced additional aid to U.S. farmers hurt by the administration’s trade skirmishes. The new program will provide up to $16 billion for crop farmers based on the estimated impact of foreign tariffs across their county.

Hong Kong: Demonstrations against China’s influence in Hong Kong will continue this weekend, with protest leaders targeting the city’s airport in hopes of raising global awareness of their concerns. Separately, activists are also planning a protest against the police department’s lack of action when organized crime gangs known as “triads” attacked and beat dozens of anti-China protestors last weekend. As we’ve mentioned before, it looks like the city government, or perhaps Beijing’s liaison office, may have enlisted the triads to help control the weekslong protests. That’s reminiscent of how government officials in Russia and other rogue nations work hand-in-hand with criminals to achieve their goals (especially in cyberspace). If that’s really happening in Hong Kong, it would seem to reflect a new level of desperation for the government and a new low in its relationship with Hong Kong’s citizens.

North Korea: New imagery analysis from private sector researchers indicates that North Korea has continued to produce long-range missiles and nuclear weapons even as leader Kim Jong-un is negotiating a denuclearization deal with President Trump. In addition, analysts at the Defense Intelligence Agency say the North Koreans have probably produced about a dozen new nuclear bombs since Kim and Trump first met in Singapore last year. Separately, North Korean state media has explicitly tied yesterday’s short-range missile launches to its anger over upcoming U.S.-South Korean military exercises. We suspect President Trump will continue to look past such developments for now, but if North Korean provocations continue, they could eventually force Trump to break off the talks.

Russia: The Russian central bank today cut its benchmark short-term interest rate to 7.25% from 7.50%. Echoing the concerns driving many central banks to loosen policy, policymakers primarily based their decision on reduced inflation pressure and weakening growth prospects.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.