Author: Rebekah Stovall

Asset Allocation Weekly (April 16, 2021)

by Asset Allocation Committee | PDF

In the NBC mockumentary show The Office, the character Jim Halpert gets tricked into choosing his wife, Pam, as “Employee of the Month.” Perplexed and suspicious, coworkers begin to probe into how Jim’s wife was deserving of the award. Pam, who was also surprised, attempts to justify the result, saying, “I didn’t miss a day, I came in early, I stayed late, and I doubled my sales last month.” Not buying her answer, a coworker rebuts, “Oh, really! From what? Two to four?” In an aside to the camera, Pam replies, “Yup!” This example illustrates how an otherwise shocking statistic can be rendered meaningless when viewed in the proper context. In this report, we will discuss the importance of context when evaluating the Consumer Price Index (CPI) over the next few months and how an expected sharp rise in inflation may not be a cause for concern.

The CPI tracks the monthly price movements of consumer goods and services. The index is based on a weighted average in which services make up 60% of the index and goods make up the remaining 40%. To minimize distortions due to normal monthly variations, the index is adjusted to take seasonality into account as both demand and supply can be affected by seasons. For example, beef demand usually rises in the summer (the “grilling season”), so statisticians at the Bureau of Labor Statistics will adjust for the price effects of this seasonal demand through a seasonal adjustment process. However, these adjustments usually only deal with predictable yearly effects. Unusual weather events or one-off situations are not taken into account. As a result, outlier events such as supply disruptions, war, drought, and, most recently, pandemics aren’t part of the seasonal adjustment process. Thus, the frequently reported yearly change in CPI can sometimes be more reflective of changes in the comparison year rather than actual price pressures.

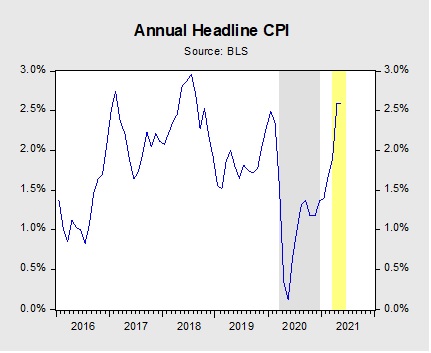

The chart above shows how the year-over-year change in the CPI will look if the index remains unchanged for the next three months. The grey region represents the start of the pandemic in March 2020 through the end of 2020. The yellow region shows annual inflation if the index remains unchanged from February. Using this assumption, headline CPI would show year-over-year increases of 1.9%, 2.6%, and 2.6%, respectively, over the next three months. The 2.6% figures would be near three-year highs. In other words, barring unforeseen deflation, the CPI report will likely show a steep rise in inflation.

The rise in the index over the next few months can be attributed to goods and services returning to their normal levels. Energy prices, particularly, are primed to be one of the key drivers pushing inflation higher. Fuel prices have risen 34.5% after hitting a 15-year low last May.[1] In general, prices for goods have outpaced services due to stronger demand from people forced to stay home. However, as vaccinations become more ubiquitous and restrictions on movement decline, this trend will likely reverse. Fares for travel and entertainment are expected to pick up as good weather sets in and more states begin to allow people to enjoy recreational activity.

It is also likely that stimulus checks could temporarily lift prices. Over the last few months, prices for durable goods such as used motor vehicles and major appliances have surged. White goods have done particularly well, with prices up 24.3% from February 2020. This suggests that households may have used their stimulus checks to purchase big-ticket items. That being said, this inflation will likely be limited as consumers are less likely to buy more of these goods over the next few years.

In summary, over the next few months, the CPI may not paint an accurate picture of inflation. Because the index does not make adjustments based on major outlier events such as pandemics, base-year comparisons can be distorted. As a result, the upcoming CPI report of annual inflation may reflect a combination of deflation in goods and services in the previous year and fiscal stimulus in the current year. Neither will result in the unfettered inflation that skeptics are warning about as both are one-time events. As a result, any adverse impact caused by these reports in the financial markets will likely be short-lived.

[1] In fact, last year, oil prices briefly fell below zero.

Weekly Geopolitical Report – The Geopolitics of Central Bank Digital Currencies (CBDC): Part IV (April 12, 2021)

by Bill O’Grady | PDF

This week, we conclude our series on CBDC with market ramifications.

Ramifications

Money is a seminal good. As our metaphysical discussion examined, economics has tended to avoid forays into the being of money.[1] Accordingly, for the past 150 years, there have been steady changes to the use of money, from a gold standard, to a dollar standard, to full fiat currencies, and floating exchange rates. We have seen credit money dwarf state and commodity money. There have been discrete changes; the failure of the gold standard to hold in the interwar years was one, while Nixon’s closing of the gold window, effectively ending the Bretton Woods Agreement, was another. Most of the other changes were less dramatic. The development of the Eurodollar market undermined the Great Depression regulatory regime, as did the creation of the money market fund. The steady expansion of derivatives and the non-bank financial system played a role as well.

CBDC would also be a significant event on a global scale. And, any time there is a change in how money works, the potential for unexpected outcomes is high.

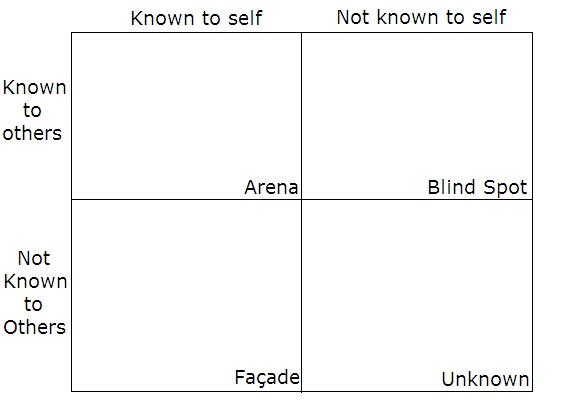

One way to develop a framework about CBDC and the challenges it brings is to use a Johari Window. A Johari Window is a psychological concept to compare what we know to what is known by others. We adapt it for our use by not having two “players” and instead use it to describe the risks of introducing CBDC.[2]

[1] For a deeper dive into this topic, we recommend: Bjerg, Ole. (2014). Making Money: The Philosophy of Crisis Capitalism. London, U.K.: Verso Publishers.

[2] The Johari Window is the basis for Donald Rumsfeld’s famous “known/unknown” comment.

Asset Allocation Weekly – #34 (Posted 4/9/21)

Asset Allocation Weekly (April 9, 2021)

by Asset Allocation Committee | PDF

One key worry for investors these days is whether massive fiscal stimulus, loose monetary policy, and accelerating economic growth will spark runaway inflation. That concern has been a major factor in driving down fixed income prices and boosting bond yields since the beginning of the year. However, we’ve been arguing that any acceleration in consumer prices this year is likely to be fleeting. Much of the expected rise in inflation will simply reflect “base effects” as current prices are compared to the extraordinarily weak prices at the beginning of the coronavirus pandemic one year ago. In spite of recent supply chain disruptions, such as the February freeze in Texas and the grounding of the Ever Given container ship in the Suez Canal, there’s also a lot of excess industrial capacity and unused labor in the U.S. and other major developed countries. The overall high availability of resources will likely help keep a lid on inflation for some time to come. In this report, we discuss yet another factor that will probably hamper inflation: population aging.

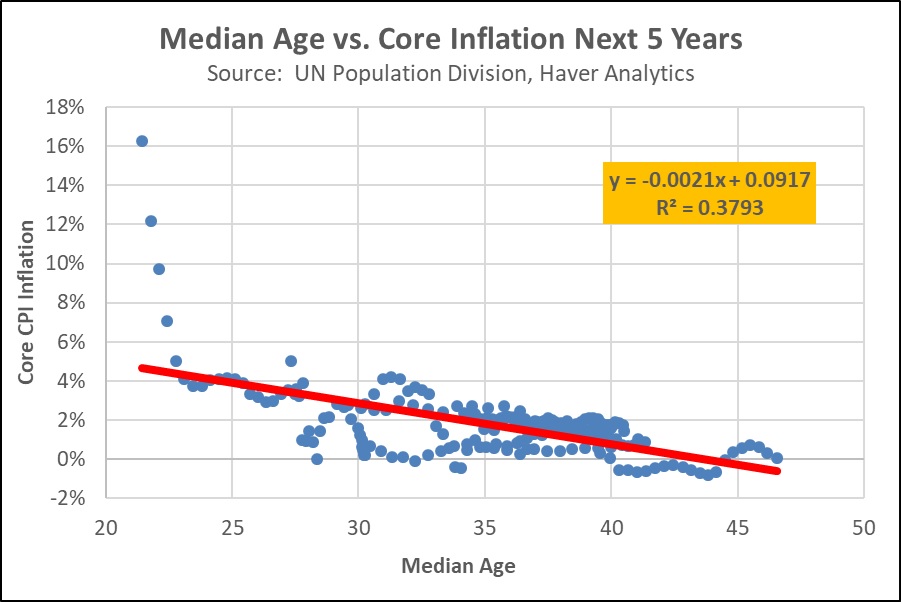

As shown in the chart below, a study we recently conducted suggests that when a country has a higher median age, it tends to have lower inflation in the coming years. Our study looked at the median ages and inflation experience over time for a sample of 10 major economies, each of which has a relatively comparable measure of “core” consumer inflation (consumer price changes excluding the volatile categories of food and energy). Countries in the sample ranged from developed nations like the U.S., Japan, and France to “emerging” or recently developed markets like Mexico, South Korea, and Israel. Across the sample, our study showed that for every additional year of median age, a country’s average annual inflation rate over the coming five years declined by approximately 0.2%. Similar inflation declines were noted for forward periods ranging from one to 15 years. For perspective, a one-year rise in median age is what the U.S. experienced when its median age increased from 37.3 years in 2013 to 38.3 years in 2020.

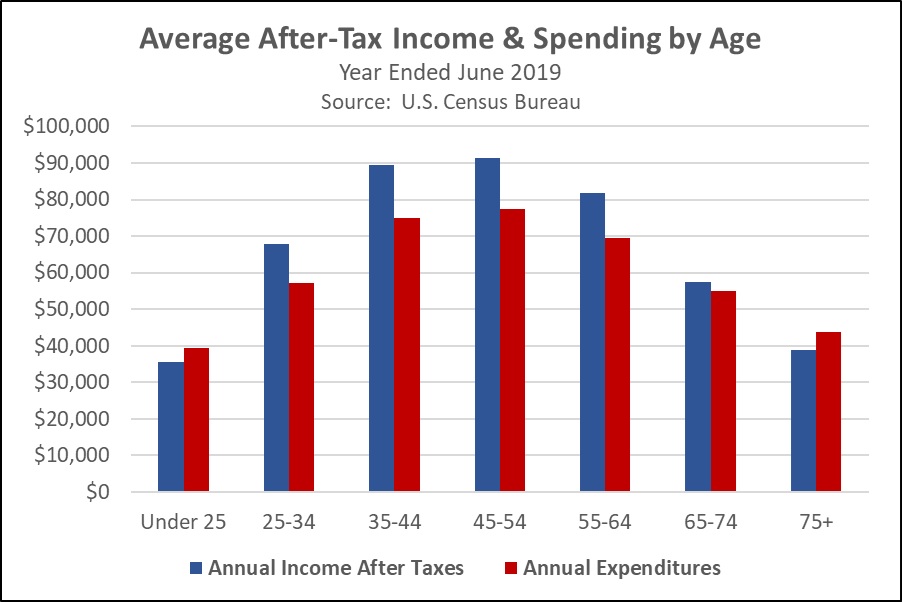

Our analysis suggests population aging holds down inflation primarily through the mechanism of weaker demand. A separate study that we’ve conducted shows that at least in large, developed countries such as the U.S., people tend to reduce their consumption spending as they approach and then enter retirement (see chart below). As birth rates fall, average ages increase, and a greater share of the country’s population enters pre-retirement or retirement. Overall consumption expenditures then grow more slowly than they otherwise would, and the weakening in demand makes it harder for companies to raise prices.

To be sure, plenty of factors can have a bigger impact on inflation in the near term, such as the base effects, fiscal stimulus, and supply disruptions mentioned above. That explains why the estimated equation in the first chart has a relatively low “R2” (a measure of how well the equation fits the relationship; an equation with a strong fit would have an R2 of 0.60 or more). Population aging is probably best thought of as an important background factor inhibiting inflation over the longer term, much like technological innovation or globalization. Population aging is to inflation what a big luggage carrier on the roof of your car is to your top speed: along with the size of your engine, your tire pressure, and other factors, it’s one of many things that can limit just how fast your car can go. That’s why we think falling birth rates and rising median ages in countries across the world should help convince investors that persistently high inflation probably won’t be a problem until further in the future.

Confluence of Ideas – #20 “The U.S.-China Balance of Power: Part I” (Posted 4/7/21)

Weekly Energy Update (April 1, 2021)

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA | PDF

After peaking in early March, prices have pulled back to pivot around $60 per barrel. Although recent builds in crude oil are bearish, expectations for stronger economic growth should be supportive for prices.

Crude oil inventories fell 0.9 mb compared to the 1.7 mb draw expected. There was no change in the SPR. Refinery operations have normalized to pre-Texas freeze levels.

In the details, U.S. crude oil production rose 0.1 mbpd to 11.1 mbpd. Exports rose 0.7 mbpd, while imports rose 0.5 mbpd. Refining activity rose 2.3%.

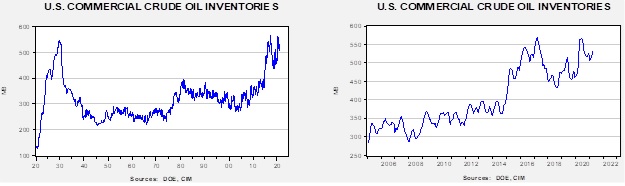

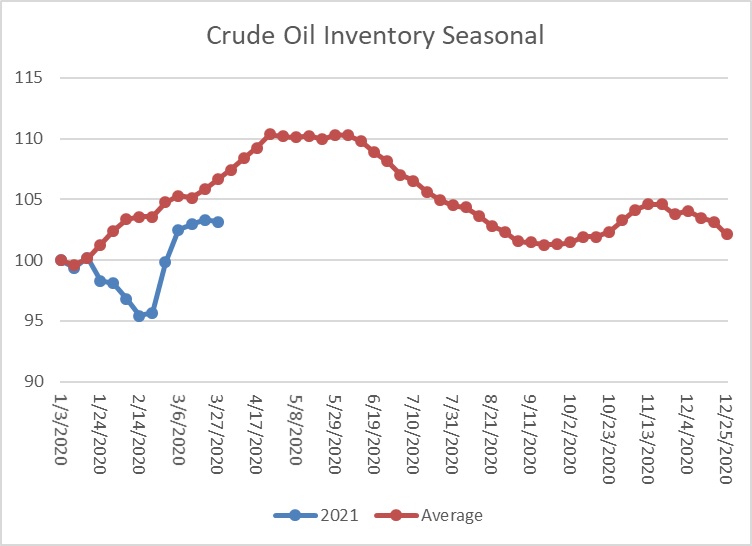

This chart shows the seasonal pattern for crude oil inventories. We are well into the winter/early spring build season. Until the Texas freeze, we were seeing a counterseasonal decline. This week, stockpiles declined modestly but usually don’t this time of year. We are currently at a seasonal deficit of 21.5 mb.

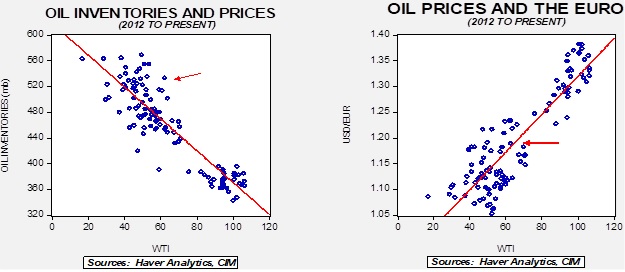

Based on our oil inventory/price model, fair value is $40.53; using the euro/price model, fair value is $64.67. The combined model, a broader analysis of the oil price, generates a fair value of $51.04. The divergence continues between the EUR and oil inventory models, although recent dollar strength has reduced the projected fair value generated from the euro/price model.

Market news:

- Abu Dhabi is unveiling a new futures contract based on its oil. If the contract becomes popular, it will put a market price on OPEC oil and could undermine efforts by the cartel to control the price of OPEC crude, especially from the Middle East.

- As vaccination efforts expand and the U.S. economy reopens, driving should rise which is bullish for corn.

Geopolitical news:

- The eventual transition to transportation electrification will dramatically reduce oil prices and revenues to oil producers. This development will likely have significant negative effects on oil-producing nations which are dependent on oil revenues. This is especially the case for less developed nations that produce oil; often, their marginal costs are high which means their oil will be the first to be priced out of the market.

- China and Iran have inked a deal for investment and security. Although we don’t expect Chinese warships and military to be engaged anytime soon, the pact will undermine U.S. efforts to force Iran to negotiate over its nuclear program and other issues.

- An Islamist insurgency is threatening a natural gas project in Mozambique.

- NGOs are calling on Chevron (CVX, USD, 105.03) to halt payments to Myanmar for projects the company has in the country. Myanmar recently had a coup and protests against the military have become increasingly violent.

- The Canadian Supreme Court has upheld the government’s carbon tax.

Alternative energy/policy news:

- The Biden administration is unveiling an infrastructure package with “green” tones to it. Proposals for greening the economy through public investment have been around for a while; it remains to be seen if this attempt will be more successful.

- As we have noted earlier, the government is considering various subsidies to farmers to compensate them for farming practices that capture and store carbon dioxide. However, to date, no concrete proposals have emerged.

- April Fool’s! Sources indicated that the U.S. division of Volkswagen (VOW, EUR, 307.20) was planning to change its name to “Voltswagen” to reflect the move to electrification. Turns out it was an April Fool’s joke a few days early.

- We continue to watch the rapid innovations in battery technology. The most recent changes are tied to lithium. It is well known that a pure lithium battery would be much more efficient, allowing for larger batteries, faster charges, and would last longer. One small problem is that lithium in its pure form is reactive and explodes when exposed to liquid. However, there are reports indicating that creating a liquid electrolyte eliminates the problem and ends the need for a solid-state battery. If this works, it would potentially revolutionize batteries and accelerate the transition.

- As we have discussed previously, hydrogen-powered fuel cells are a potential alternative to batteries. It may end up that hydrogen is more appropriate for fleets (where centralized fueling could take place) and aircraft (where batteries may weigh too much). Railroads in California are testing fuel cell locomotives.

- Wind power has been in place in the U.S. for some time, but it remains problematic. The windmills have been known to harm bird populations. Less populated areas tend to have the most persistent winds, but then require long transmission lines to deliver the “juice.” The long lines can be unpopular. The process of siting turbines can also be problematic as they are “hard to miss” once constructed. These issues have led to turbines being placed offshore, just over the horizon, to avoid these issues. In addition, winds tend to be very persistent offshore. Although such facilities are more common in Europe, the Biden administration is looking to construct them here in the U.S. as well.

- Soon after the election, the new administration suspended oil and gas leases on federal lands. It was unclear if this was a temporary measure or one destined to be permanent (or until a new government takes power). So far, the measures remain in place, but an outright ban hasn’t been announced either.

- A court in France recently declared that the government is responsible for climate mitigation. Although it is unclear how this decision will affect policy, protests against perceived government inaction have emerged recently.

- Congress has introduced new fees for methane emissions. Often, methane is released as part of the drilling process for oil and natural gas. In fact, recently, as drilling activity has accelerated, there has been a consequent increase in methane releases. Methane is a potent greenhouse gas and the fees are designed to reduce these emissions.

- Japan has been supporting coal-fired electricity plants across Asia. It has decided to end the practice, which would be a blow for coal demand.

- The American Petroleum Institute, the primary industry lobbyist, has decided to support carbon pricing. This decision suggests it sees carbon pricing as the most effective tool for carbon emissions management as opposed to cap and trade or regulatory restrictions. Now the issue will be the price applied.

View PDF

Weekly Geopolitical Report – The Geopolitics of Central Bank Digital Currencies (CBDC): Part III (March 29, 2021)

by Bill O’Grady | PDF

(Due to the Easter holiday, the next report will be published on April 12.)

This week, we continue our series with an examination of the geopolitics of CBDC.

The Geopolitics

As we noted in Part I, there has been strong interest among the central banks to introduce digital currencies. We would expect each country that decides to establish a CBDC regime will do so based on its domestic situation. But these new currencies won’t exist in a vacuum; the establishment of CBDC in one country will likely affect what occurs in other nations as well.

Therefore, this week’s report examines the likely structure of CBDC in the U.S., China, and the Eurozone. We will project what a CBDC will look like in each region by establishing the priorities of each one, a likely CBDC structure based on those priorities, and current progress. Obviously, the world is more than these three entities, but for our purposes, the introduction of CBDC by these three powers will tend to determine what other nations decide on this issue.