by Bill O’Grady, Kaisa Stucke, and Thomas Wash

[Posted: 9:30 AM EST] The big news item over the weekend was the passing of Fidel Castro, the revolutionary leader of Cuba. The immediate impact of his death on markets will be rather small; as Fidel’s health weakened over the past decade he turned over the day-to-day running of the government to his younger brother, Raul. Still, Fidel was an important factor in the Cuban government. Raul, at 85 years old, is expected to retire in 2018. Thus, we will be seeing a change in power in Cuba. We don’t expect a wholesale reversal of socialism in Cuba but, without Fidel, we would expect to see a softening of what were often rigid socialist policies under Fidel.

Cuba’s geopolitical importance is that it is near the key U.S. port of New Orleans. For much of U.S. history, this city was the most critical port for the U.S. economy. This port was the terminal point for the massive American river system that includes the Mississippi, Missouri, Ohio, Illinois and Arkansas Rivers. If a foreign power could impinge on New Orleans, it would effectively bottle up the agricultural and material wealth of the U.S. Controlling Cuba was key to keeping New Orleans safe; that was part of the reason for the Spanish-American War. When Castro ousted Batista in the early 1950s, the importance of New Orleans had diminished as other forms of transportation were created. But, when Cuba fell under Soviet influence, Fidel became a significant threat. The 1962 Missile Crisis almost led to a nuclear exchange that may have been a disaster. Fidel survived 11 U.S. presidents and was a pain for almost all of them. Thus, his death will likely lead to an easing of tensions.

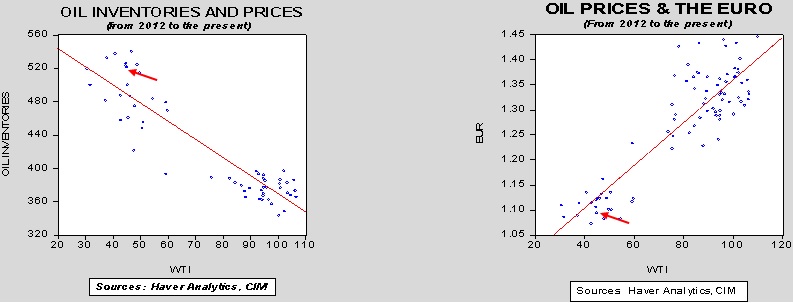

Of course, one of the reasons why Cuba might be more malleable is due to the economic collapse of one of its key supporters. The Saturday NYT had a long report about the newest refugee crisis as Venezuelans are taking small watercraft to island nations in the Caribbean and flooding across the Brazilian and Colombian borders. The Venezuelan economy is in near collapse and, according to this report, the lack of food is driving Venezuelans to leave their homeland. Venezuela needs higher oil prices to have any chance for economic recovery, although the distortions caused by the late Hugo Chavez are also a major handicap to the economy.

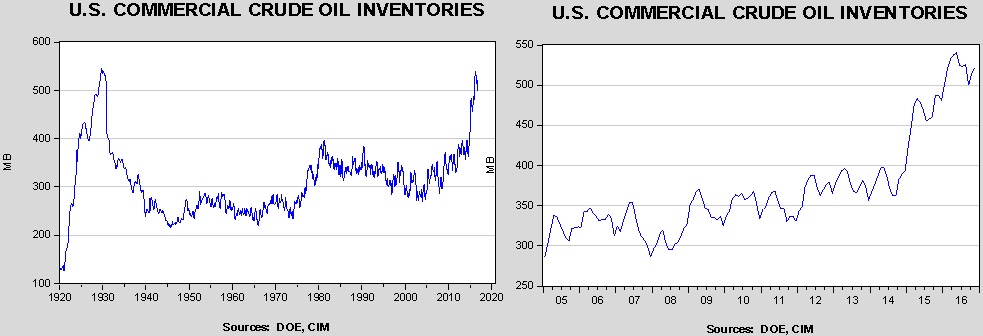

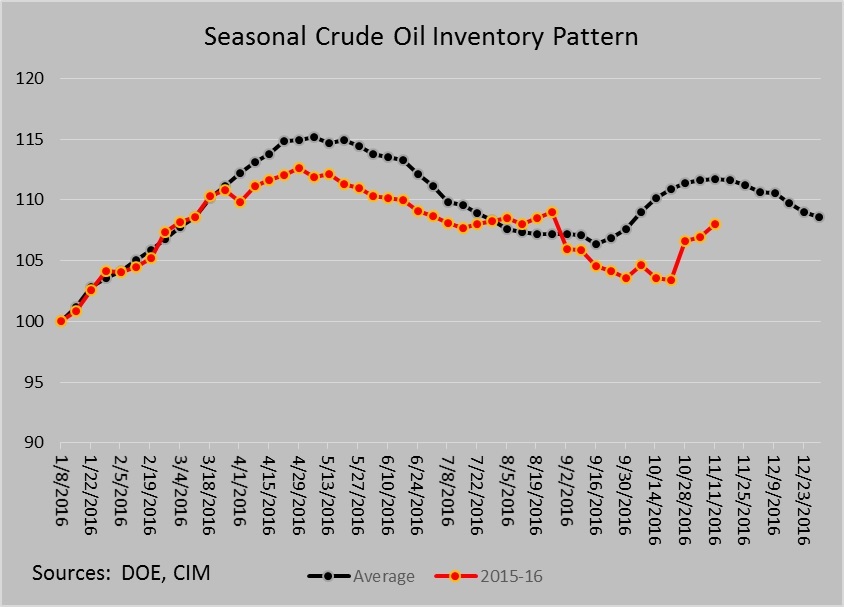

There has been great hopes for an OPEC deal, but the cartel is still struggling to allocate production cuts. The key sticking point remains between Saudi Arabia and Iran, although there is disappointment that Russia appears only willing to freeze production. What is especially galling about Russia’s behavior is that its production is at record levels, meaning OPEC cuts will boost Russia’s market share. At this point, an OPEC deal hinges on whether the Saudis can live with giving up market share to Iran, Iraq and Russia, which it is also essentially fighting in Syria. If the kingdom needs higher prices more than it needs geopolitical influence in the Middle East, it will be forced to make what are effectively unilateral cuts in output. That outcome may be more than the Saudis can stomach.

Finally, in case you missed it, one of our favorite China analysts, Michael Pettis, had an op-ed in the WSJ last week in which he discussed the key role of the U.S. in global trade. Most importantly, he discussed how the U.S. has been willing to run persistent trade deficits by providing the reserve currency. This has allowed the global economy to expand and has supported globalization. Pettis makes it clear, and we agree, that the Chinese economy is in no position to take over America’s role in the global economy. The last election has also made it clear that the U.S. citizenry is tired of the role of importer and consumer of last resort. Although Pettis holds out hope that some sort of restructuring is possible, a more likely outcome is a reversal of globalization.