by Bill O’Grady, Kaisa Stucke, and Thomas Wash

[Posted: 9:30 AM EDT] In a wide-ranging interview, President Trump roiled the markets late yesterday by admitting that (a) China is not a currency manipulator; (b) the dollar is too strong; and (c) Chair Yellen might be invited to stay at the FOMC. Point (b) was the market-moving news; since Bob Rubin was Treasury Secretary during the Clinton administration, the White House has hewed to a “strong dollar” policy. Essentially, this policy was designed to end the practice of currency manipulation by the government. For the most part, the U.S. has allowed the dollar’s level to be set by market forces.[1] Earlier, the Trump administration signaled that the Rubin dollar policy was coming to an end and active discussion of the dollar’s level was possible. The president’s position that the dollar is “too strong” suggests the administration would like to see it weaken.

This policy of “oral intervention” is often effective in the short run. Whether it has a long-term effect depends on two factors. First, is the jawboning followed up with policies that change the fundamentals for the exchange rate? And second, what is the valuation of the currency when the jawboning takes place? Currently, on a relative inflation basis, the dollar is expensive relative to the JPY and EUR. For the most part, the dollar’s strength since 2014 has been a function of tighter monetary policy. In fact, based upon the current level of the two-year T-note, the EUR/USD rate should be closer to parity. It appears to us that the exchange rate markets are waiting to see how much more U.S. monetary policy tightens and whether other central banks are coming close to ending their overly easy policies. A president suggesting that he wants a weaker dollar does, at least in the near term, signal the potential for a weaker currency. However, we would also note that most presidents prefer dollar weakness on hopes it might boost growth. Even President Reagan, who supported dollar strength initially, reversed course on currency policy in his second term.

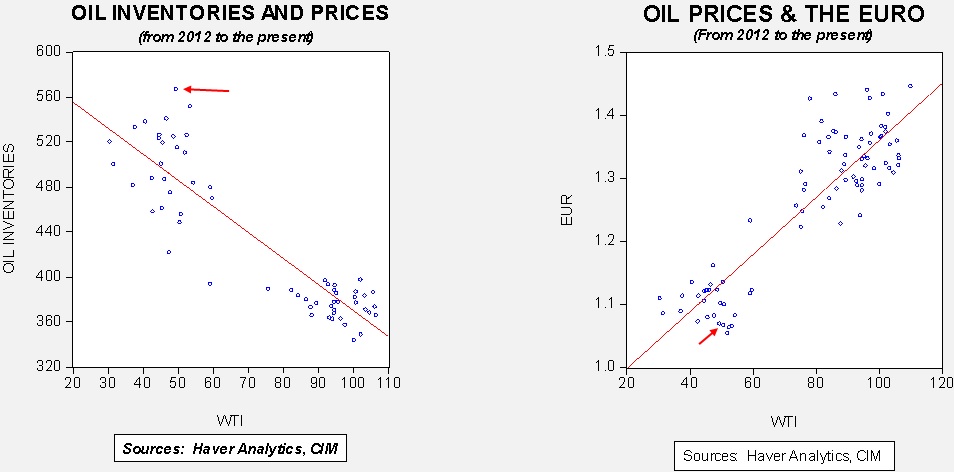

If the dollar is poised to fall, it would change our outlook for some markets. Emerging markets have been unusually strong relative to the dollar, which may suggest that investors in these markets anticipated a reversal in the greenback. Although dollar weakness is usually bullish for emerging markets, we would argue that much of that has already been discounted. Commodities usually benefit as well. As we note below, oil prices arguably have discounted some dollar weakness, too. A weaker dollar tends to support large caps relative to small caps and that trade may have some room to move further. But, it is too early to tell if yesterday’s weakness will stick. After all, the FOMC is still expected to make at least two more hikes and the balance sheet will likely be trimmed, so a weaker dollar has to occur with tightening policy. That might be a struggle.

The interesting issue surrounding the decision not to name China a currency manipulator is that Trump actually has already received the key response to naming a nation a currency manipulator, namely, bilateral negotiations designed to reduce the trade imbalance. China does, in fact, manipulate its currency but in a way that is positive for U.S. trade; left to its own devices, the CNY would be much weaker. By getting trade talks without naming China a manipulator, which would have been difficult based on the Treasury Department’s criteria, Trump has managed to get what he wanted anyway.

On the Yellen comment, we think it’s best to frame it relative to what we see going on in the White House. Since the election, we have discussed this presidency as “Bannon v. Ryan.” Bannon is losing ground fast. Jared Kushner appears to be the president’s most trusted advisor, and he is steering Trump toward a conventional GOP establishment position. This not only excludes the populists but also the Freedom Caucus, which is pre-Rooseveltian. In other words, this is becoming a country club GOP administration. That being said, the other characteristic of this administration is that it consists of mostly tactics with little clear strategy. When the president cites “flexibility” we see the lack of clear goals.

If we are correct, it is good news for financial markets. The inflation-generating policies that the populists want would weigh on stocks and bonds. Instead, we will likely see “middle of the fairway” policies—the ACA mostly stays intact, modest tax cuts occur, trade impediments are mostly for show and the superpower role will remain intact. On the other hand, the populists aren’t going away. If this is the correct assessment of the trend, it will open the door for either a right-wing populist to mount a GOP primary challenge or, more likely, a “Bernie-crat” challenge from the left. The latter assumes that the Democrat Party understands the populist-establishment dynamic, which is questionable. So, we will continue to watch this development closely, but this is what we are seeing.

______________________________________

[1] U.S. dollar policy has always been an odd configuration; the Treasury has the mandate for policy but the most effective tools for short-term exchange rate management are interest rates, which are the purview of the Fed. The Treasury was mostly left with jawboning the markets, which isn’t a good long-term strategy. Rubin decided that it made the most sense to say the U.S. wanted a strong dollar without defining what that meant. That decision has left subsequent Treasury Secretaries to maintain the language without content.