[Posted: 9:30 AM EDT] SOS Tillerson is in Moscow as tensions are rising. The White House is accusing the Kremlin of having prior knowledge of the sarin attack in Syria and attempting to cover up the attack. Putin is suggesting that the U.S. is being “duped” by rebels into attacking the Assad regime. It’s difficult to see how these talks have any hope of success. We did mention yesterday that Tillerson met with European members of the G-7 in Italy. The U.K., along with the U.S., called for Russia to abandon Assad; Italy and Germany, both facing refugee issues, were more cautious.

Yesterday, a tour bus carrying members of the Borussia Dortmund soccer team in Germany was attacked with three bombs. One member of the team was reportedly injured. The game was rescheduled for today. Borussia Dortmund is one of the most popular teams in Germany; it appears this may have been a terrorist attack.

Iran holds presidential elections on May 19. Registration for this office began yesterday and it seems the conservatives are running Ebrahim Raisi for the presidency. In the past, the conservatives have run a number of candidates that tend to dilute the vote, giving hope to centrists (liberals are pretty much excluded from the race). There is growing speculation tht Raisi was handpicked by Ayatollah Khamenei. If it is a two-man race, the current president, Hassan Rouhani, would face an uphill battle for reelection. If Raisi wins, we may see Iran retreat from foreign investment which would slow its development and may hamper oil production. We note that former president Ahmadinejad is making noise about running. Khamenei could probably prevent him from running by having the Guardian Council disqualify him, but such a move would be unpopular with the poor in Iran who remember the former president fondly. A more conservative Iranian president would be an unwelcome outcome for the U.S. and Sunni powers in the region.

In response to rising tensions between the U.S. and North Korea, Trump issued a stark warning via Twitter that the U.S. is prepared to act alone if China is unwilling to intervene in North Korea. Rodong Sinmun, a state-run newspaper in North Korea, stated that Pyongyang has its “nuclear sights” focused on U.S. military bases in South Korea and on the U.S. mainland. In our opinion, even though North Korea does have the capability to strike U.S. bases in South Korea, it is still unable to launch a missile that could land in the U.S. Nevertheless, China has issued a statement that it is committed to the denuclearization of the Korean Peninsula. In addition, the Global Times, a Chinese state-run newspaper, reported that Beijing is losing patience with North Korea and would consider cutting off oil exports if it continues to cause trouble. This Saturday could prove to be a test for both Kim Jong Un and President Trump as North Korea celebrates the birth of the country’s founder, Kim Il Sung. It is expected that Kim Jong Un will use the occasion to showcase the country’s military capabilities by launching another missile. If this were to happen, President Trump is likely to respond militarily, further escalating tensions between the two countries. We will continue to monitor this situation as it unfolds.

The Market

Since December, oil prices have been ranging between $48 and $55 per barrel.

(Source: Barchart.com)

Prices and Inventories

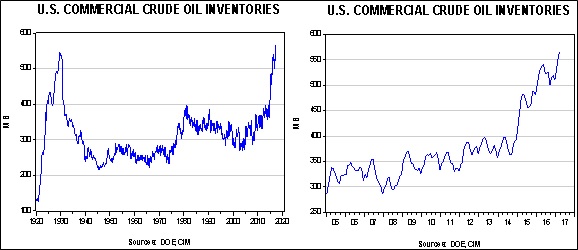

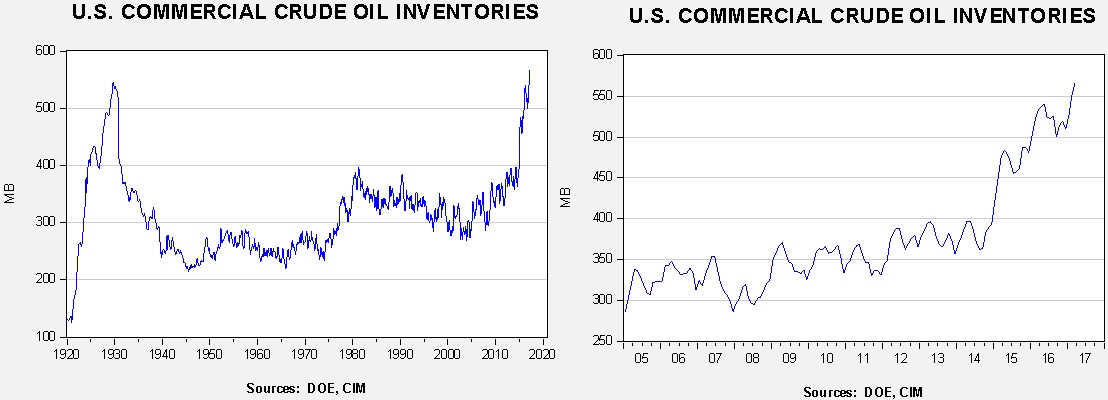

Inventory levels remain elevated, reaching historic highs.

In the above charts, the one on the left shows the long-term inventory situation, while the chart on the right shows a 12-year history. Normal inventories would be below 400 mb, so stockpiles remain elevated.

[Posted: 9:30 AM EDT] U.S. equity markets continue to meander; hopes for fiscal support continue to buoy equities but there are growing worries that the administration will fail to deliver. Geopolitical issues are a concern as well. Sean Spicer, the administration’s press secretary, seemed to add barrel bombs to Syria’s prohibited weapons. Although this decision is clearly defensible, the persistent use of these bombs would almost certainly suggest that more U.S. strikes are in the offing. We doubt the president has made this change in policy but we will be watching. Anytime ordinance is in the air unexpected things can happen. If any further U.S. action leads to a Russian casualty, escalation is likely. In another part of the world, the Chinese media is reporting that the People’s Liberation Army has sent 150k troops to its border with North Korea. There are unconfirmed reports that these troops are training to handle a refugee situation. Given that Chairman Xi and President Trump have recently met, this buildup may be a signal that China is expecting some sort of military action against the Hermit Kingdom that, most likely, would lead to a flood of refugees heading into China.

Meanwhile, SOS Tillerson is on his way to Moscow after meeting with the G-7. The group suggested that more sanctions against Syria are being considered. We expect Tillerson to receive a rather chilly reception in Russia.

In Fed news, Chair Yellen suggested in a talk yesterday that the economy has exited crisis mode and her policy now is to protect the gains made. This suggests less support for the economy but doesn’t necessarily suggest tightening policy. Our most recent focus has been on inadvertent tightening; a rising dollar, increasing credit spreads, rising financial stress, etc. None of these appear to be a problem now. There are rumors that the administration may be close to nominating a FOMC governor, one to essentially replace the recently departed Daniel Tarullo. However, no names have emerged so there may be a surprise coming. The NY Post[1] is speculating that NY Fed President Dudley may have leaked non-public information to analysts, similar to behavior that led to the recent resignation of Jeffrey Lacker from his post as president of the Richmond FRB. If Dudley were forced out, it would remove a major dove from the board.

(Due to the Easter holiday, the next edition will be published April 24th.)

Last week, we began our retrospective on the EU. This week we will examine the post-Cold War expansion of the EU, including a discussion of the creation of the euro and the Eurozone. With this background, we will analyze the difficulties the EU has faced in dealing with the problems caused by the 2008 Financial Crisis. We will look at several proposals being floated in the wake of Brexit about reforming the EU and, as always, conclude with potential market effects.

[Posted: 9:30 AM EDT] Global markets are generally quiet this morning as investors try to discern how to handle President Trump’s new muscular exercise of foreign policy. After reading and reflecting over the weekend, we offer our take on the missile strike against Syria. First, this is a president that eschews consistency; although a number of analysts are trying to figure out if these attacks signal a “Trump Doctrine,” we suspect not. Instead, it shows that personal issues matter. It appears that the president was truly moved by video of the aftereffects of the sarin attack and reacted based on that feeling. This sort of behavior is consistent with a Jacksonian view of the world. Trump seemed to view the Assad gassing as a matter of honor and reacted accordingly. Second, the military appointees are clearly influencing policy. The strikes were designed to warn, not escalate. Military leaders try to avoid “mission creep,” where a military intervention keeps expanding as civilian leaders try to accomplish ever larger goals. The military prefers discrete events and this missile strike is a classic example.

We do note that the U.S. is sending a carrier group toward North Korea. We doubt this is little more than a signaling exercise but that doesn’t mean it won’t be effective. The U.S. doesn’t want war with North Korea but no president wants the Hermit Kingdom to acquire a nuke on their watch. Thus, sending a signal to the Kim regime that there could be costs to its current policy is prudent.

The Trump/Xi meetings ended with little drama. China did offer some modest concessions on finance and beef, and they set a plan to discuss trade over the next 100 days that may create conditions for a bilateral trade agreement. In the meantime, China will likely adjust higher its allowed percentage of foreign ownership of financial firms and lift the ban on U.S. beef imports. It also promised to buy more agricultural products. China will want to avoid a trade war until the October CPC meetings. After that, we will get a better look at China’s real trade policy.

The French polls have tightened, with the center-right Fillon and the hard-left Melenchon gaining ground. There is a high number of undecided voters going into the first round of elections later this month and the surge of these two candidates show how divided the French electorate has become. This election still holds the potential to upset Europe. We also note that Greece and the EU have reached an agreement on its bailout program. Now we will see if the Greek legislature will actually pass further unpopular reforms or bring down the government.

After the election, we argued that the fate of the Trump presidency rested on the poles of “Bannon v. Ryan.” That is morphing into “Bannon v. Kushner” but the battle is the same. The former represents the new isolationism, an attempt to return to a less globalized world. The latter in both cases represent a world that is globalized and deregulated. This is going to be a long war because even if the personalities are vanquished, the sides of the debate remain. At present, Bannon is losing power; the establishment is steadily marginalizing him. For investors, this is a good outcome because it means that inflation remains under control and margins should continue to be robust. However, the forces of populism remain and even if the right-wing version gets quashed by the right-wing establishment, the left-wing version remains in the background.

In Sunday’s NYT,[1] Louis Hyman, a professor of economic history at Cornell, published an op-ed arguing that Main Street is mostly dead because it’s inefficient and so its return is not a likely outcome. Although he makes some good points, we believe he is being a bit naïve. Since the late 1970s, policymakers have bought into a “cult of efficiency” that Marx obliquely discussed. Marx’s assertion was that, at some point, capitalism becomes so efficient and income inequality so profound that there isn’t enough consumption to absorb all the productive capacity the efficient capitalists create. Marx thought that scenario would create a crisis for capitalism that would result in its collapse. So far, that hasn’t been the case. Nevertheless, that doesn’t mean that changes haven’t occurred. Both the Roosevelts took steps to retard the efficiency of capitalism through regulation. Hyman noted that we used to have “fair trade” laws that set minimum prices; a retailer could not put a price below a certain level meaning that the chain and the small independent business didn’t compete on price.[2]

Some of us represent capital, most labor, but all of us are consumers. The economic model that Hyman says can’t return was actually good for capital and labor but bad for consumers. The high inflation of the late 1960s and 1970s was a result of this model. As consumers, we cheer foreign trade because it keeps prices low, but foreign trade is mixed for capital and labor. We are less sure that Hyman is right; a return to a model that is less friendly for consumers is ultimately the goal of populism based on the idea that globalization and deregulation have been worse for labor. Although we could argue the case, that is the perception and thus a return to an earlier model cannot be so easily dismissed.

[2] This is one of the reasons Sears (SHLD, 11.34) developed in-house brands like Kenmore and Craftsman; because these weren’t national brands, it allowed Sears the ability to undercut the national branded competition.

In our 2017 Outlook, our earnings forecast for the S&P 500 was $119.45 per share, up from $106.25 in 2016.[1] Based on new data and other trends, we are raising this forecast to $126.44 for this year. There are three reasons for the change.

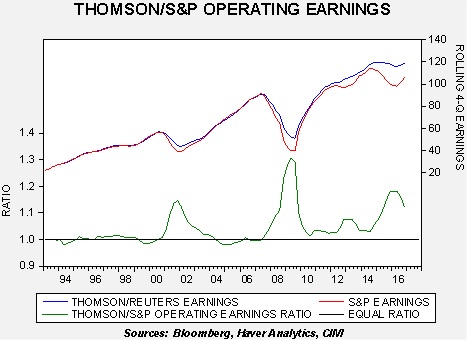

The spread between Thomson-Reuters and S&P operating earnings is narrowing. This is an issue we have discussed in the past. There are two primary sources of information for earnings, Standard and Poor’s and Thomson-Reuters. Most of the time, the two sources are consistent. However, since the Great Financial Crisis, the latter has tended to report higher operating earnings for the S&P 500 than the former. Explanations for this divergence vary. It does appear that Thompson-Reuters takes a more “relaxed” view on what costs are excluded compared to Standard and Poor’s. Here is the data through Q4 2016:

In 2001 and 2008, the spread between the two series coincided with recessions. Since the Great Recession, we have had two periods where the spread has widened; both are tied to declines in oil prices. As oil prices recover, the current spread should narrow.

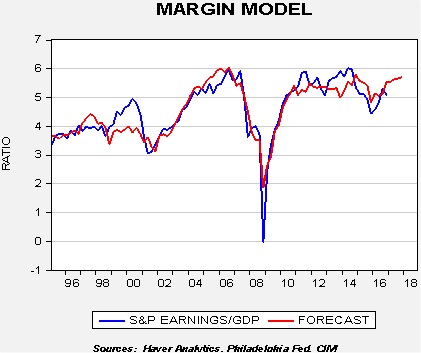

Margins are showing some improvement. We compare total S&P 500 earnings to GDP. Our model for this percentage is indicating that margins will improve this year.

The blue line on the chart shows the actual percentage of S&P 500 total operating earnings to nominal GDP. For most of this century, this percentage has been ranging between 5% and 6%. The drop in oil prices led to some margin compression. We also expect improving productivity and a modest widening of the trade deficit to boost margins, shown above as the red line, which is the model forecast.

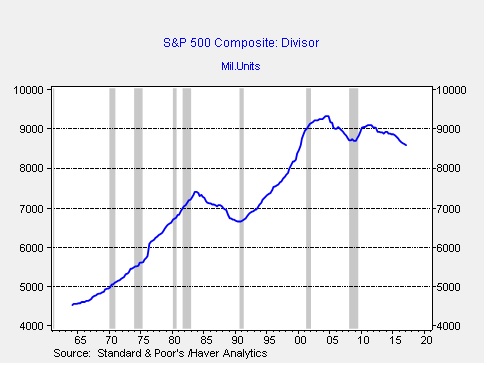

Finally, the per-share data will be supported by a steadily declining divisor. The below chart shows the S&P 500 divisor; it’s a scaling factor for the index.

To calculate the index, one takes the overall market capitalization and divides it by the divisor. The divisor adjusts to changes in the composition of the index, as well as new issuance, share repurchases and mergers. The rise in share buybacks has led to a steady drop in the divisor; we are now at levels last seen in early 2000. As the divisor declines, the per-share value rises.

Despite this increase in earnings, we have not boosted our S&P 500 target forecast of 2400 for the year. We view the P/E as elevated at this point and so we expect the rise in earnings to mostly result in a weaker multiple. At the same time, this change will make equity markets less expensive and thus less vulnerable to disappointment. If the rise in business and consumer sentiment supports the multiple, we will make appropriate adjustments to our forecast.

[Posted: 9:30 AM EDT] Happy Employment Data Day! We cover the data in detail below but the payroll data, showing only a 98k rise, was quite disappointing. We suspect seasonal factors played a role as February weather was unusually mild while March was colder. It should also be noted that the unemployment rate fell to 4.5% (-0.2%), which is actually bullish. Initial market reaction has been bullish bonds and bearish equities and the dollar. However, we see lots of noise in the numbers so reversals throughout the day would not be a surprise.

At the same time, we have had heavy news flow over the past 24 hours. Here’s what we see going on:

The U.S. bombs Syria: President Trump ordered a moderately sized cruise missile strike on an airbase in Syria in response to the Assad government’s use of nerve gas against rebels with high levels of civilian casualties. Since the 2013 deal with Syria was thought to have ended Syria’s chemical weapons program, it is disappointing to see the regime use these weapons. It is unclear if they hid these weapons during the period when they were supposed to have eliminated them or if they have reconstituted their WMD industry. The U.S. response was limited but it is possible that escalation could follow.

Market reactions: Markets acted as one would expect—equities fell, gold and Treasuries rallied and oil prices jumped. Although Syria is a minor oil producer, the attack involves three major oil producers, the U.S., Russia and Iran. Thus, any escalation could affect oil prices; the most likely catalyst would have been if Iranian or Russian security personnel were killed in the attack. Given that Russia was warned of the strike, the odds were lessened that such an action would happen. We expect this attack to be limited and thus the overnight trends will likely reverse over time.

International and domestic reactions: European governments were supportive. China’s reaction was mostly neutral while Russia reacted harshly, as one would expect, calling the action a “significant blow” to U.S./Russian relations. However, if this is a one-off attack, which we believe it is, the Russians won’t escalate the situation. Russia can’t afford to go to war with the U.S. On the other hand, if the Kremlin thought it had its man on Pennsylvania Avenue, this attack undermines that position. Within the U.S., the reactions were interesting. Establishment figures across the aisle praised the attack; populists, especially on the right, were rather critical of the missile strikes.

Takeaways: We expect Trump to be mercurial and this action is clear evidence of this characteristic. It has been less than a week since the administration indicated that regime change in Syria was no longer a goal of the U.S. What it shows about Trump is consistent with the behavior of Jacksonians; besmirching honor guarantees a response.[1] It’s clear that Trump took the attacks personally. Assad engages in war atrocities often but usually with conventional weapons. Thus, indiscriminate bombing of civilians is tolerated but the use of chemical weapons isn’t. And, the fact that the images of gassed children were broadcast worldwide appears to be a major factor behind the response. So, the lesson to the world isn’t that attacks on civilians won’t be tolerated; it’s that high-profile attacks using banned weapons will not be allowed. We don’t see a change in U.S. policy in Syria. We seriously doubt we will see a large U.S. ground troop presence in the country anytime soon or an escalation of U.S. military activity in the region. For nations under threat, such as North Korea, this missile strike is a warning of sorts and may raise tensions even further. At the same time, Pyongyang should also note that it’s the public dishonor that gets one into trouble; acting badly in secret is probably ok.

The Mar-a-Lago meetings: Thus far, not too much has come out of the talks between Chairman Xi and President Trump. The Syrian attack will act as a distraction. North Korea, trade and the level of U.S. influence in the Far East are all issues but we doubt they will be solved in this meeting. Xi needs a smooth runway into CPC meetings in October that will allow him to pick his own team for his second term. Thus, low-key meetings are his goal.

The Senate goes nuclear: The Democrats are prepared to filibuster Neil Gorsuch and so the GOP will change the rules and allow Supreme Court justices to be appointed by a simple majority vote. Although legislation is still subject to filibuster, it’s just a matter of time in our opinion until this changes as well. The Senate has traditionally acted as a governor on policy, preventing it from moving too far or too fast in either direction. Once we go to simple majorities, there isn’t much use for having the Senate around. It probably should become like the House of Lords in the U.K.

Why is this happening? The nation has become deeply divided on partisan lines and thus sees anything the other side wants as prima fascia evil. Both will claim “the other side started it” and both are credible. At root, however, is that we get the government we send to Washington and when the country becomes partisan and divided, we want the other side vanquished. Since the divisions are more or less equal, it’s hard to get a large enough majority to force one’s will on the other.

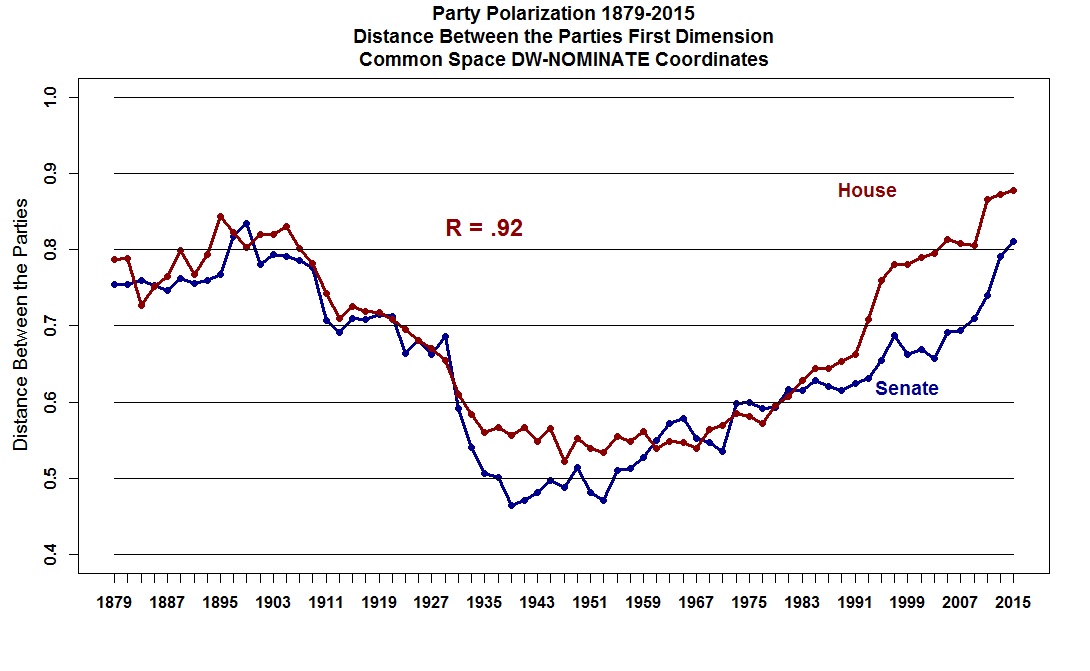

(Source: Voteviewblog.com, Rosenthal and Poole)

This chart shows the degree of partisanship in the House and Senate; the higher the number, the more partisan the body. The House is the most divided it’s been since the data series began in 1879; the Senate is approaching the highs it set in the late 1890s. We suspect partisanship was probably higher around the Civil War but that shouldn’t offer us comfort. This level of partisanship makes it difficult to govern and probably impossible to maintain the superpower role. It’s worth noting that the trend for bipartisanship began to accelerate after WWI when the U.S. was beginning to realize that it was going to have to take a more global role. We remained remarkably bipartisan through the Cold War, although the degree of agreement began to unwind as the Cold War ended. We don’t know how this will play out for sure but there are a couple of observations that can be made. First, if the Senate eventually ends the filibuster rule, policy shifts will become more pronounced and violent with new parties in power. Political risk for financial markets will escalate. Second, we are probably in an era of major coalition changes within the established parties. Third, America’s superpower status will almost certainly be unsustainable with this degree of domestic political division.

[Posted: 9:30 AM EDT] Most of the time, Fed minutes are snoozers. On the other hand, there is often real action within the FOMC. The full meeting transcripts are published with a five-year lag and they show verbal sniping and open disagreement. By contrast, the minutes are sanitized with code words like “some members” or “many members” to give hints at the degree of support or opposition. Most of the time, the minutes are nothing more than a longer version of the statement.

However, that was not the case yesterday. The FOMC made its clearest signal yet that it intends to shrink the balance sheet. The general expectation was that the Fed would allow the balance sheet to slowly unwind by not buying bonds when paper matures. However, that doesn’t seem to be what the FOMC is saying; instead, it appears to be looking to actively reduce the size of the balance sheet.

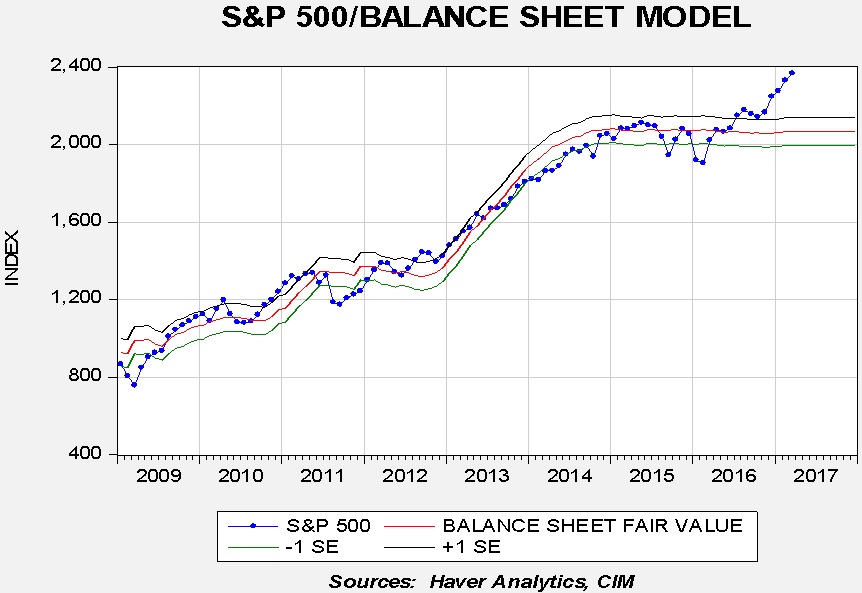

This is a big topic that will require deeper analysis. To be completely clear, no one knows for sure exactly how the balance sheet expansion affected the economy and the markets. We can look at market effects, but we can’t tell for sure why those factors worked the way they did. We can make a very good case that QE was good for stocks.

The chart above shows the S&P 500 regressed against the Fed’s balance sheet. From 2009 until the middle of last year, the model did a good job of projecting the path of equities. Since the Trump election, equities have moved sharply higher. Our position was that the actual effect of QE was to boost equity market sentiment.

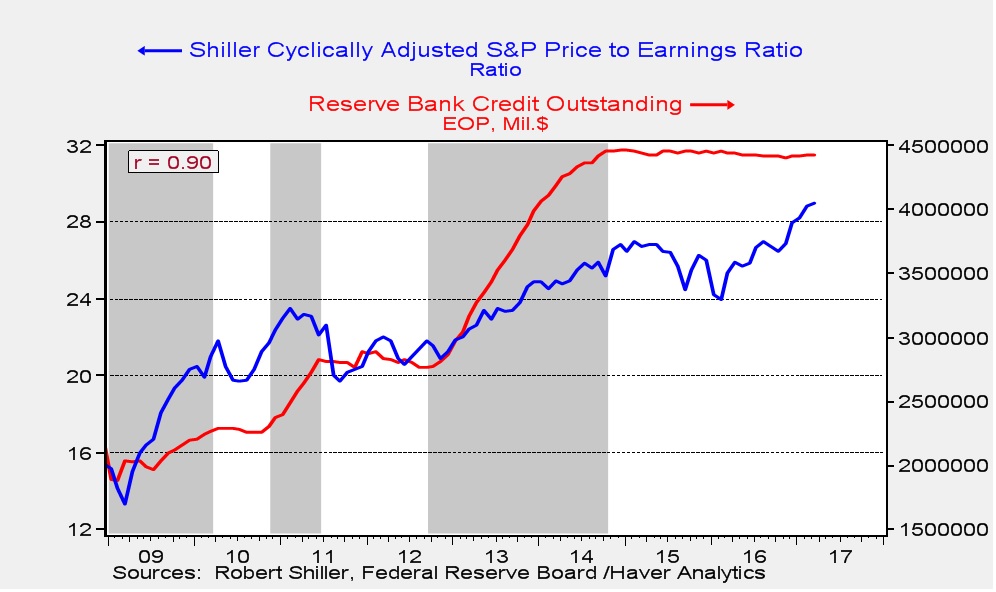

The chart above shows the Shiller CAPE and the balance sheet. Periods of QE are shown in gray. Note that the P/E tended to rise when the balance sheet expanded. Obviously, the most recent lift isn’t being caused by policy but by the election.

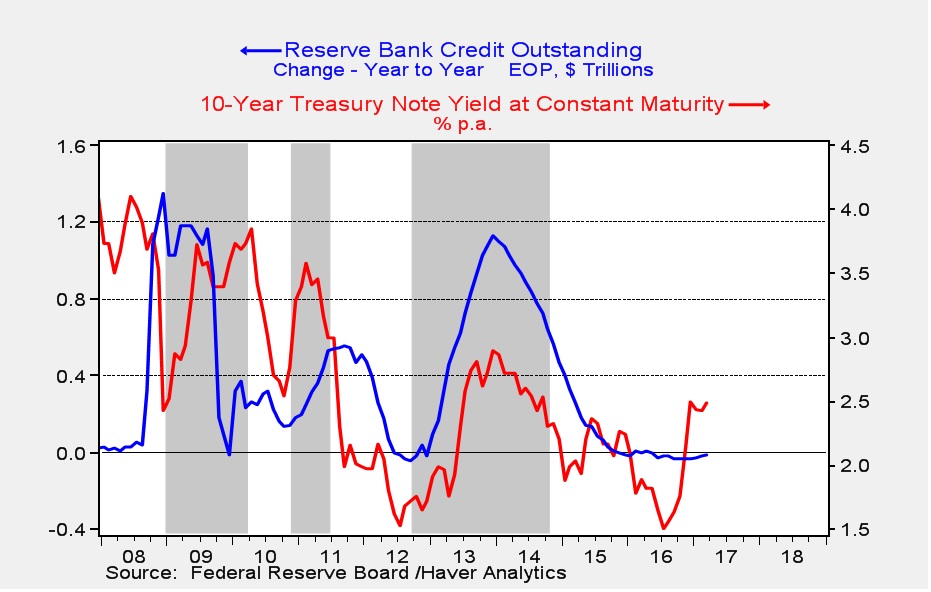

Perhaps the most underappreciated element of QE was the impact on long-duration interest rates. One of the reasons for implementing QE was to lower long-term interest rates. However, the evidence suggests the impact was just the opposite of what policymakers expected.

This chart shows the yearly change in the size of the balance sheet along with the yield on the 10-year Treasury. Note that, especially with QE2 and QE3, yields tended to rise during periods of balance sheet expansion. Although the common expectation is that yields will rise once the reversal begins, in fact, we would be more inclined to expect bond prices to rise. Why did bond yields rise during QE when the Fed was buying longer dated paper? Most likely, investors feared the goal of policy was reflation; rising inflation is always negative for bond prices and those fears overwhelmed the impact of reduced supply.

However, we are cautious about drawing too many conclusions from these patterns. We have no experience with cutting the size of a balance sheet this large. On the one hand, it shouldn’t make much difference. The rise in the balance sheet did nothing more than bloat the banking system with reserves that, for the most part, have not been lent. Reducing excess bank reserves shouldn’t be a big deal. On the other hand, QE and the balance sheet were symbols of Fed policy support. The psychological impact could be quite negative. We will have more to say on this going forward, but our initial read is that balance sheet reduction could be bearish for equities and bullish for bonds. Then again, the impact may not be large and could be overwhelmed by other issues, such as tax changes, geopolitical events, etc.

In other news, the China/U.S. summit begins later today. We would not expect much to happen here as the Chinese leader needs a “no drama” meeting. The Czech Republic ended its peg with the EUR; since mid-2015 the Czech central bank has pegged the koruna/euro rate at 27.0313. It has rallied about 0.5% on news that the Czech government will allow its currency to strengthen.

Stephen Bannon, special advisor to the president, was pulled off the National Security Council yesterday in a clear win for the establishment. Our read is that the key power broker is Jared Kushner and there have been rumors that Bannon and Kushner’s relationship has cooled in recent months. Some reports suggest Bannon was prepared to resign but the Mercers pressed him to stay. Gary Cohn, the White House economic advisor, apparently asked some senators about Glass-Steagall in a private meeting. According to Bloomberg,[1] Cohn expressed support for bringing the separation of investment and commercial banking back to the financial system. This is a bit of a shock coming from Cohn but it may be a trial balloon to see if Congress would support such a measure. Bannon’s fall from grace is a blow to the populists, while Glass-Steagall would be a win for this group.

Overall, in our establishment/populism “meter” the former is gaining strength. If the establishment gains power, financial markets will favor this outcome. However, populism isn’t going away and moving in this direction leaves President Trump vulnerable to a challenge from a leftish populist in 2020…if and only if the Democrat Party sees the opening.

U.S. crude oil inventories rose 1.6 mb compared to market expectations of a 1.5 mb draw.

This chart shows current crude oil inventories, both over the long term and the last decade. We have added the estimated level of lease stocks to maintain the consistency of the data. As the chart below shows, inventories remain elevated.

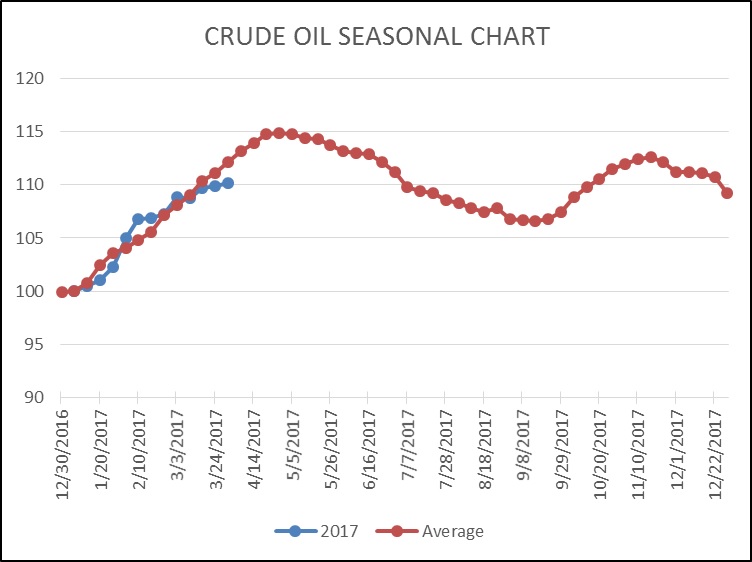

As the seasonal chart below shows, inventories usually increase for the next three weeks before rising refinery operations for the summer driving season lower stockpiles. This week’s smaller than seasonal rise puts us further below normal. Although inventories remain high, this seasonal level is consistent with early July, meaning that we may be on the way to an easing of the inventory overhang.

(Source: DOE, CIM)

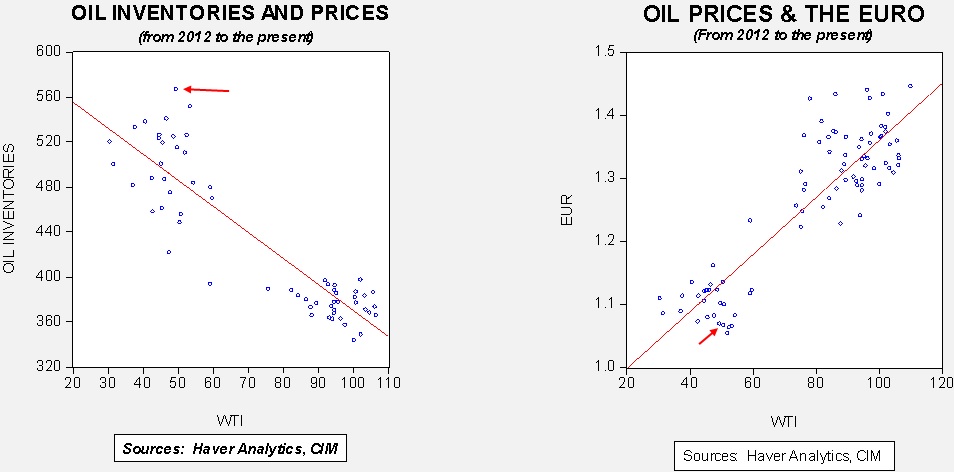

Based on inventories alone, oil prices are overvalued with the fair value price of $26.81. Meanwhile, the EUR/WTI model generates a fair value of $40.66. Together (which is a more sound methodology), fair value is $35.36, meaning that current prices are well above fair value. The data indicate that the bullish case for oil mostly rests on a weaker dollar. If the dollar continues to soften, coupled with the usual seasonal decline in oil inventories, our models will raise the fair value level. That isn’t necessarily bullish for oil prices but it does remove a potentially bearish factor. Simply put, current oil prices have already factored in a drop in inventories and likely a weaker dollar.

[Posted: 9:30 AM EDT] Yesterday, Richmond FRB President Lacker announced he was stepping down immediately after admitting he was involved in a leak of confidential information to an analyst with Medley Advisors, a well-connected Washington think tank. In October 2012, Medley published details of Fed deliberations that were non-public. In a conversation with that analyst, Lacker refused to comment on the information, which may have given the impression that he was confirming the report. We doubt that Lacker was the source of the leak; the public information we have suggests he was not but, perhaps inadvertently, confirmed it for Medley. Still, his abrupt resignation and acceptance of responsibility usually occurs as part of a deal to spare Lacker from further investigation. We suspect the leaker has still not been found.[1]

In the short run, his departure isn’t a big deal. First of all, he was leaving in October anyway. Second, he wasn’t a voter this year. The FOMC is losing one of its hawks; we rated Lacker as a one-star hawk, our most hawkish designation. Usually, regional FRBs replace presidents with similar characteristics. After all, it’s the bank board that appoints these presidents and there is some degree of continuity on these boards. However, given the whiff of scandal that surrounds Lacker, the Richmond FRB may decide to go a different direction which may lead to a more centrist replacement.

It looks as if Syrian President Assad’s forces used chemical weapons in an area controlled by rebel forces. We note that this attack closely follows comments from the administration’s ambassador to the U.N. suggesting that regime change is not the goal of the Trump government. Although that is the de facto policy of this administration, some things are better left unsaid. Confirming Assad’s position might have given him confidence that he could get away with using chemical weapons. However, in all fairness, U.S. Syrian policy has been a mess for some time. President Obama’s red line in Syria that was crossed and subsequently ignored was poorly managed. Allowing the Russians to participate in Syria was a mistake as well.

We think the best way to examine U.S. Middle East policy is to consider it as part of the postwar order. The U.S., in addition to containing communism, froze conflict zones in Europe and Asia by taking over the defense of Western Europe and Japan. This gave confidence to other parties in the region who would have normally been traditional enemies that they had nothing to fear. So, demilitarizing Germany (and, effectively, the rest of Europe) told Russia and the other European nations that the U.S. was the keeper of the peace and traditional regional rivalries were no longer a threat. In the Far East, by taking over Japan’s defense, China knew it was protected from Japanese attack. In the Middle East, the U.S. enforced the flawed existing borders, which meant living with the brutal autocrats in the region who were the only ones capable of maintaining order in states that were not created for natural stability but for the benefit of colonial powers. In the Middle East, we can safely say that American postwar policy is no longer in existence. By supporting the Arab Spring, the U.S. has unleashed tribalist and nationalist factors that will likely shape the region for the next three decades. Richard Haass has suggested that conditions in the Middle East closely resemble Europe in the 17th century during the bloody Thirty Years War. At this point, the Middle East is in turmoil and we don’t expect it to improve anytime soon. For markets, so far, the conflicts haven’t affected oil production and so the impact hasn’t been significant. However, continued conflict will raise the likelihood that, at some point, oil flows will be disrupted.

As Chairman Xi and President Trump gather together in Florida, the Young Marshal in Pyongyang launched an intermediate range ICBM. The response from the White House was, “the clock has now run out and all options are on the table.” It is unclear what exactly this means, but it does suggest that some options might include military activity. It doesn’t appear that the financial markets are expecting such action; if they did, we would expect equity values to be declining sharply, with Treasury prices and the dollar rising as well. We don’t expect military action by the U.S. either but our confidence in this position isn’t strong due to the nature of the Trump administration. We continue to monitor conditions closely.

By all accounts, the French debate wasn’t good for Le Pen; her opponents attacked her position on the Eurozone and her responses were deemed weak. European political systems tend to isolate populists as the establishment parties, who usually oppose each other, unite to prevent a populist victory. We expect a similar outcome in France. However, it will all come down to turnout. It doesn’t appear to us that the other candidates foster strong feelings among supporters; at the same time, Le Pen supporters seem to be committed. If voter participation is low, Le Pen has a better chance of winning than current polls suggest. However, even a low turnout may not be enough to grant her a victory.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.