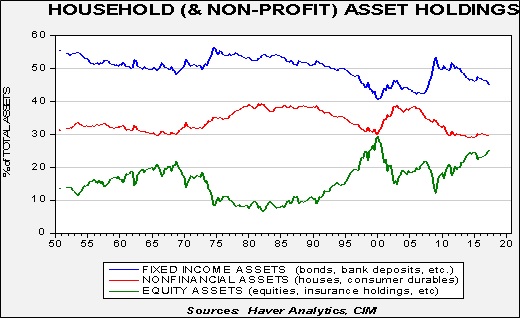

The Financial Accounts of the United States (formerly known as the Flow of Funds Report) is published by the Federal Reserve and provides data on the level of financial assets and liabilities by sector. Using this data, we can approximate the average asset allocation of American households over different periods. This accounting of assets is broad; for example, the equity portion includes equities held in defined benefit plans and insurance policies. In addition, the Federal Reserve includes non-profits in its data. In our view, non-profits are not material to the overall calculations.

The data goes back to the 1950s. On average, 50% of household assets are held in some sort of fixed income, while equity assets average 16% and non-financial assets average 34%. A casual observation of the data suggests that allocations to fixed income and non-financial assets (likely housing) are favored during periods of high levels of inflation and elevated nominal interest rates. On the other hand, equity allocations are higher during periods of low inflation and low nominal interest rates. The allocation to non-financial assets rose sharply after 2000 as part of the housing bubble. After the Great Financial Crisis, non-financial asset holdings declined; initially, fixed income rose and equities fell, but since 2010, that trend has steadily reversed as equities have taken a large share of assets.

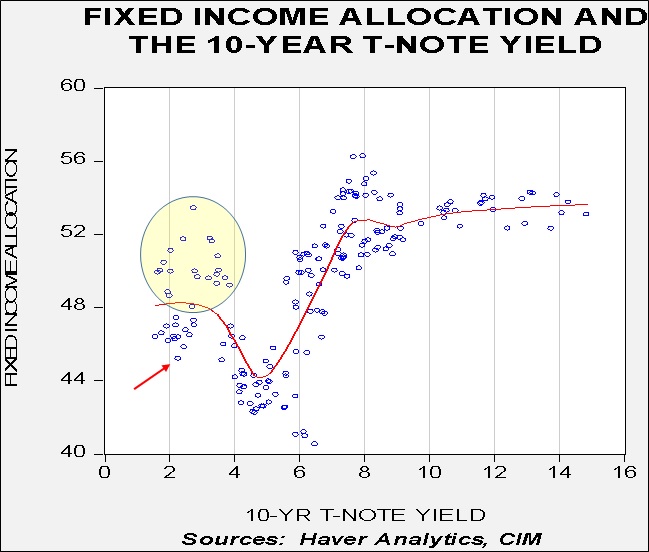

Some of the gains in the various asset classes have come from price appreciation and other parts from reallocation of assets. It isn’t completely obvious how much is coming from which part, although in future reports we will examine this issue more fully. However, the chart does suggest that equities have benefited from being “the only game in town.” Historically low interest rates and the aftermath of the housing crisis have undermined allocations to fixed income and housing. Historical patterns suggest that allocations to fixed income don’t increase until 10-year Treasury rates exceed 6%.

This chart shows a scatterplot of the percentage of total assets held in fixed income and the 10-year T-note yield. We have plotted a nearest neighbor fit study to the data. We have seen high fixed income levels along with low rates (shown in the circle), but these mostly occurred during the Great Financial Crisis. Although the current level of fixed income is low (shown by the arrow), a consistent rise above 50% generally has been seen with interest rates in excess of 6%. Thus, history suggests that it would take a more significant rise in interest rates to trigger a flight to fixed income.

Of course, recessions or geopolitical events could trigger a move out of equities. At 25%, the current allocation to equities is elevated. This level is similar to where it was in Q3 1999 and not far from the peak of 27% in Q1 2000. At the same time, the liquidity does need another place to go. After the 2000 tech crash, the primary beneficiary was housing. We don’t expect that pattern to repeat itself. Thus, without an event to scare households out of equities or a sizeable rise in interest rates, equities should maintain their favored status for the time being.

[Posted: 9:30 AM EDT] Risk-on returned to the financial markets this morning, with the dollar and equities higher and Treasuries and gold lower. The possibility that John Taylor could be the next Fed chair along with hopes of tax reform are boosting risk assets this morning.

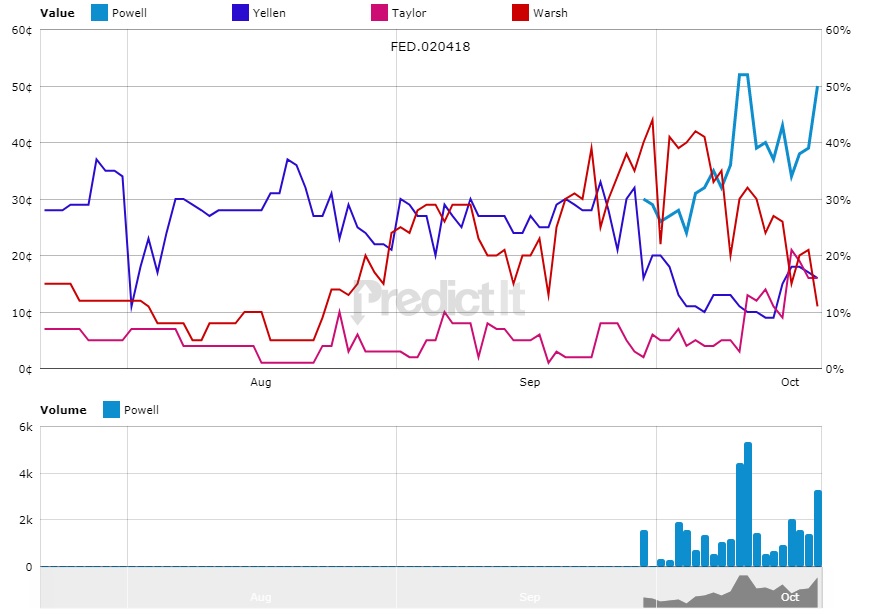

Chair talk: There are a series of dueling stories in the media this morning on who the president will select for the Fed chair position. The current conventional wisdom suggests that Powell is the front-runner, while John Taylor is running second. Below is the latest on the topic from PredictIt, the decision-betting site.

(Source: Predictit.org)

Warsh was the front-runner until about two weeks ago; since then, his star has fallen rather quickly. Powell makes sense as a chair. He favors deregulation and is considered a moderate on policy. However, he does not fit the “shake things up” framework of the president, so a surprise is possible.

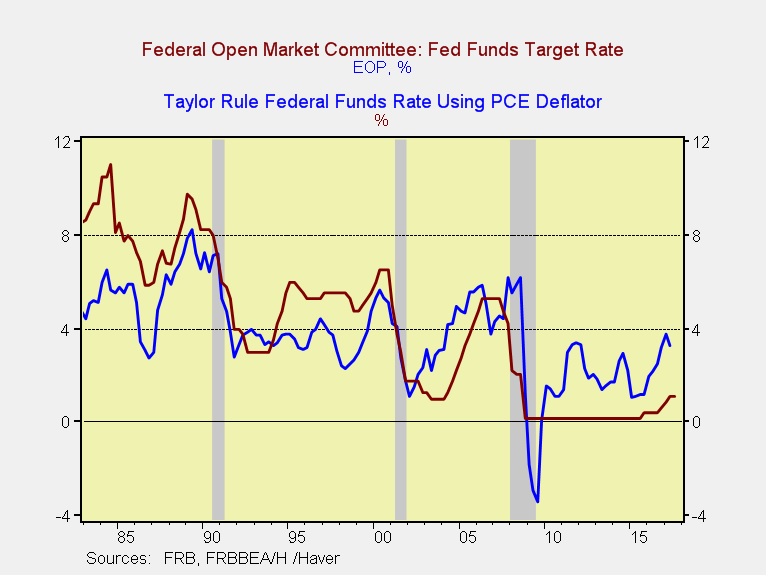

Here is the history of the target and the Taylor Rule, calculated using core PCE:

There has been an interesting trend in the relationship of the rule to the policy rate. From 1983 to 2000, the policy rate target exceeded the Taylor Rule by an average of 178 bps. Since 2000, it has averaged -136 bps. The current Taylor Rule rate would be 3.25%, roughly the level of the Mankiw Rule using involuntary part-time employment. Greenspan mostly exceeded the Taylor Rule rate until the 2000 tech crash. He and Bernanke clearly lagged the rule rate during the last tightening cycle. Note that the FOMC moved much more quickly to lower rates during the last recession than did the Taylor Rule. In fact, it’s rather clear the FOMC performed better than the Taylor Rule during the downturn by acting faster to cut rates, recognizing the gravity of the situation. If one reads the meeting transcripts from 2008, there was a growing call to raise rates in August 2008. We suspect the Taylor Rule was one of the reasons why some hawks were leaning in that direction. In hindsight, that increase would have been toxic.

We are leaning toward Powell but it should be noted that the other open governor spots are important, too. If Taylor and Warsh are offered governor positions as a consolation prize, Powell’s ability to manage to a consensus will be significantly undermined.

A budget deal: By a 51-49 vote, the Senate passed a fiscal 2018 budget resolution and the House has agreed to accept. The vote was nearly by party line, with Rand Paul (R-KY) the only Republican voting against the measure. The resolution is important because now that one is in place Congress can consider tax law changes without fear of filibuster in the Senate. Although this is a first step toward tax reform, it is a rather small one; tax reform remains a difficult task.

More non-centrist political developments: If polls are accurate, the next PM of the Czech Republic will be Andrej Babis, a right-wing populist businessman. Although the overall economic data from the country is rather good, rising inequality and political corruption is lending support to Babis. He has run on an anti-corruption, anti-EU and anti-immigrant platform. If elections pan out as expected, another EU government will have moved to the political fringe. Meanwhile, in New Zealand, Jacinda Ardern, aged 37, will be the next PM; she is the leader of the hard-left Labour Party and another young figure at the helm of an important Western government. She was able to gain power after the New Zealand Party, a party dedicated to providing government funding to the elderly, joined Arden to form a majority coalition. Arden’s platform calls for social spending but is also anti-immigrant and wants to ban foreigners from buying property.[1] Like many nations in the region, New Zealand has been favored by foreign capital flight. In the election, the center-right (and former government leader) National Party received 56 seats, Labour won 46, the New Zealand Party won nine and the Greens eight. The Greens didn’t join the coalition but agreed to caucus with it, giving it a majority. The NZD dropped 2% yesterday on the news.

Merkel gives May a lifeline: Chancellor Merkel welcomed PM May’s initial offer of £20 bn and a transition deal on the EU’s terms to facilitate a smooth Brexit. Although the hardliners in the EU want something closer to £60 bn or more, Merkel’s reaction probably means that a less onerous package can be negotiated. The GBP rose on the news.

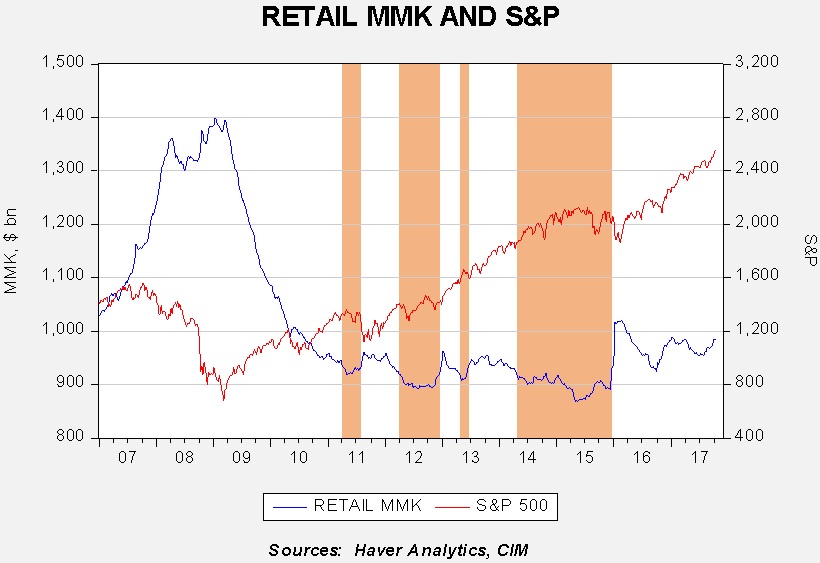

Retail MMK update: Yesterday’s market action in equities was consistent with recent patterns, which is that each pullback has been shallow and met with almost immediate buying. Thus, pullbacks have been consistently unsustainable. We attribute that characteristic to high levels of cash among investors waiting for the opportunity to invest. As a result, small market declines are seen as rare opportunities for purchasing. We have noted that the level of retail money market holdings has been a fairly good indicator of buying power.

This chart shows the weekly Friday close for the S&P 500 along with the level of retail money market funds. We have applied areas to the chart in orange—these represent periods when money market levels fell below $920 bn. In general, when money market funds held by retail fall to “low” levels, which we define as $920 bn, equity markets tend to decline or stall. We believe this occurs due to the lack of “fuel” for new buying. Current levels are near $985 bn, meaning there is ample cash for buying and thus, barring a geopolitical event, elevated levels of liquidity would be consistent with shallow pullbacks and a “buy the dip” mentality, exhibited yesterday.

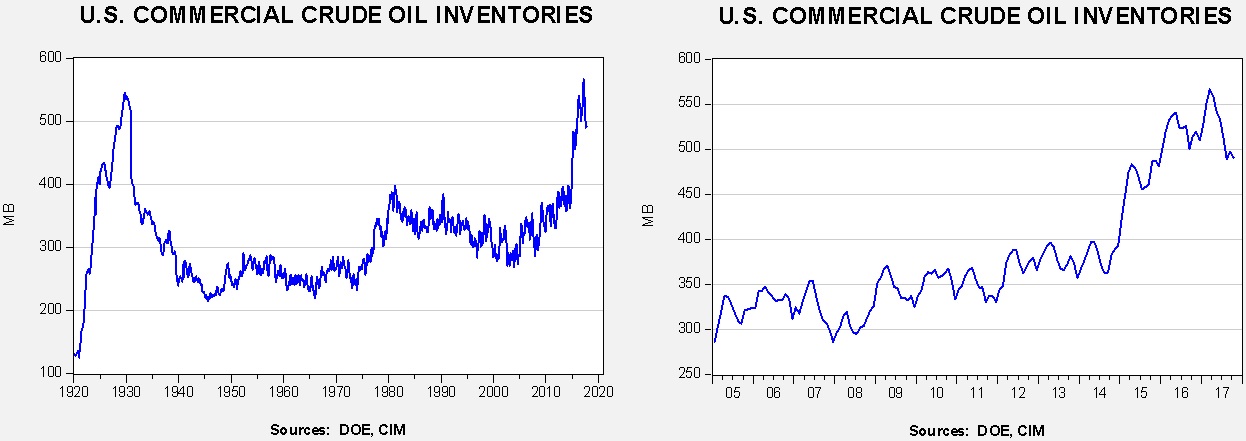

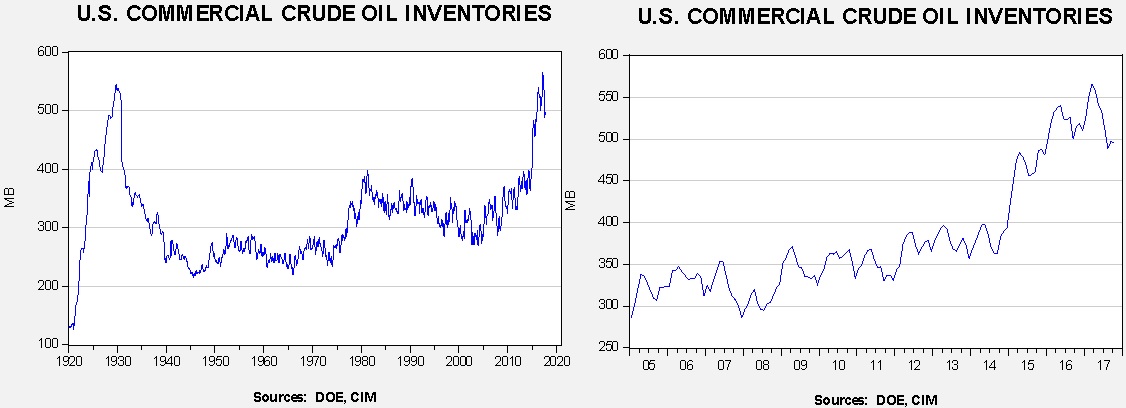

Energy recap: U.S. crude oil inventories fell 5.7 mb compared to market expectations of a 3.0 mb decline.

This chart shows current crude oil inventories, both over the long term and the last decade. We have added the estimated level of lease stocks to maintain the consistency of the data. As the chart shows, inventories remain historically high but have declined. The impact of Hurricane Harvey is diminishing as refinery operations recover. We also note the SPR fell by 0.7 mb, meaning the total draw was 6.4 mb.

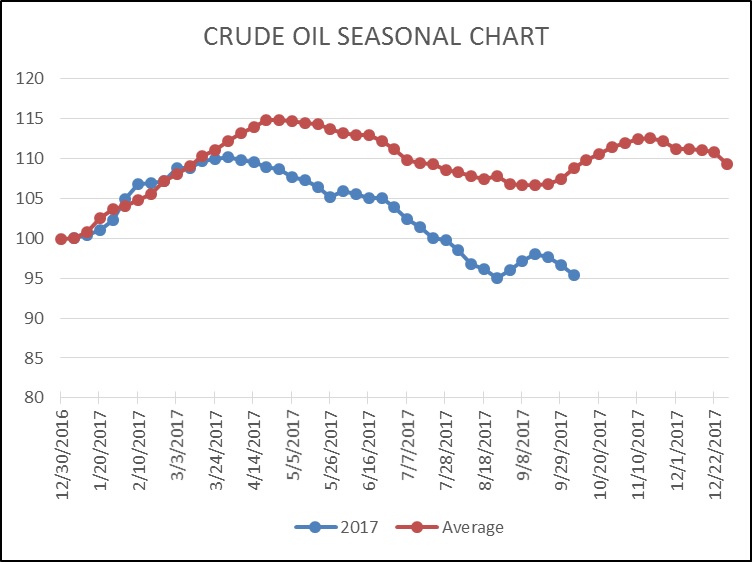

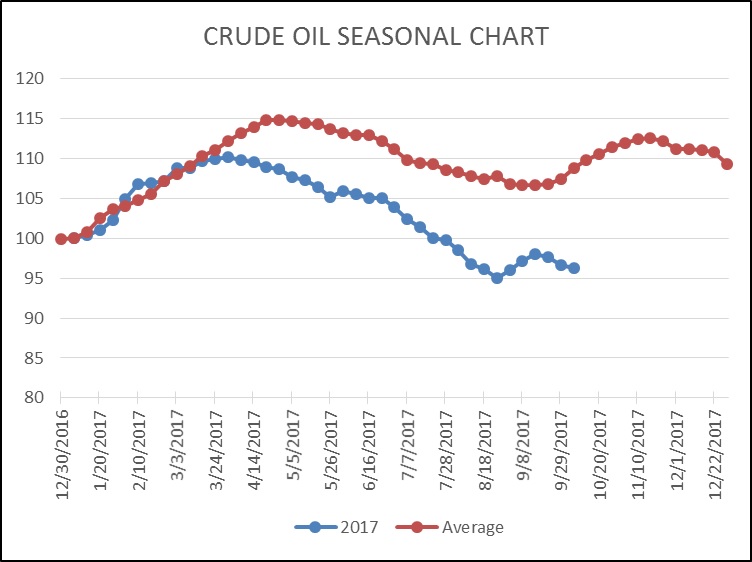

As the seasonal chart below shows, inventories fell this week. It appears we have started the inventory rebuild period sooner than normal this year due to the hurricanes. However, inventories have declined over the past three weeks, which is a surprise based on the seasonal pattern. Crude oil inventories usually rise into mid-November, so if this decline phase continues it should be supportive for crude oil prices.

(Source: DOE, CIM)(Source: DOE, CIM)

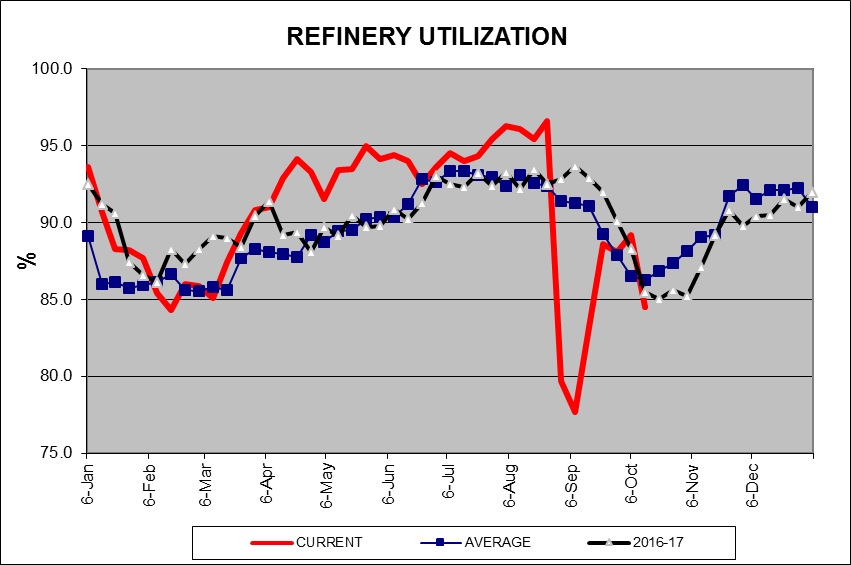

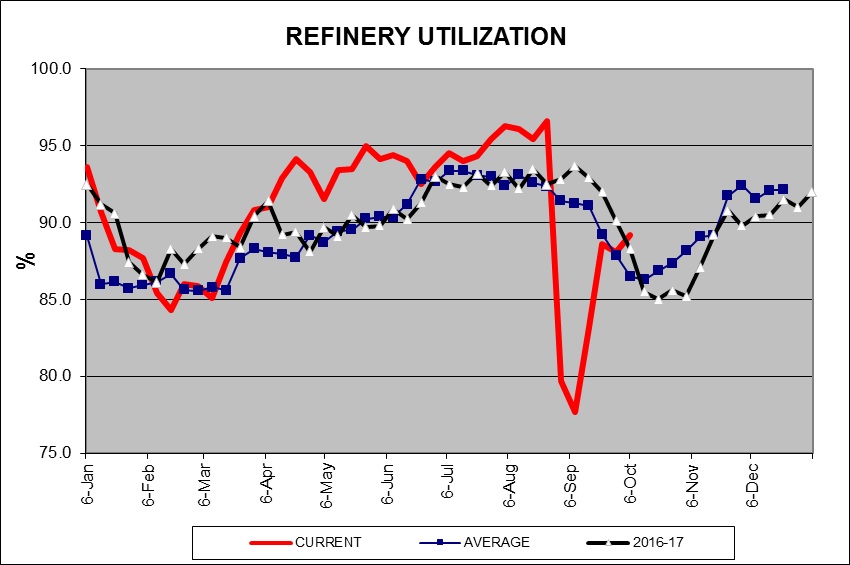

Refinery operations fell sharply last week in line with seasonal norms. This week usually represents the low in seasonal refinery activity, meaning that demand should rise on a seasonal basis going forward. What was interesting this week was that U.S. production appears to have declined by 1.1 mbpd. It isn’t obvious why this would have occurred and so we will be watching to see if this is a one-week event or part of a larger drop in oil production. If production remains low, it is also a bullish factor for prices.

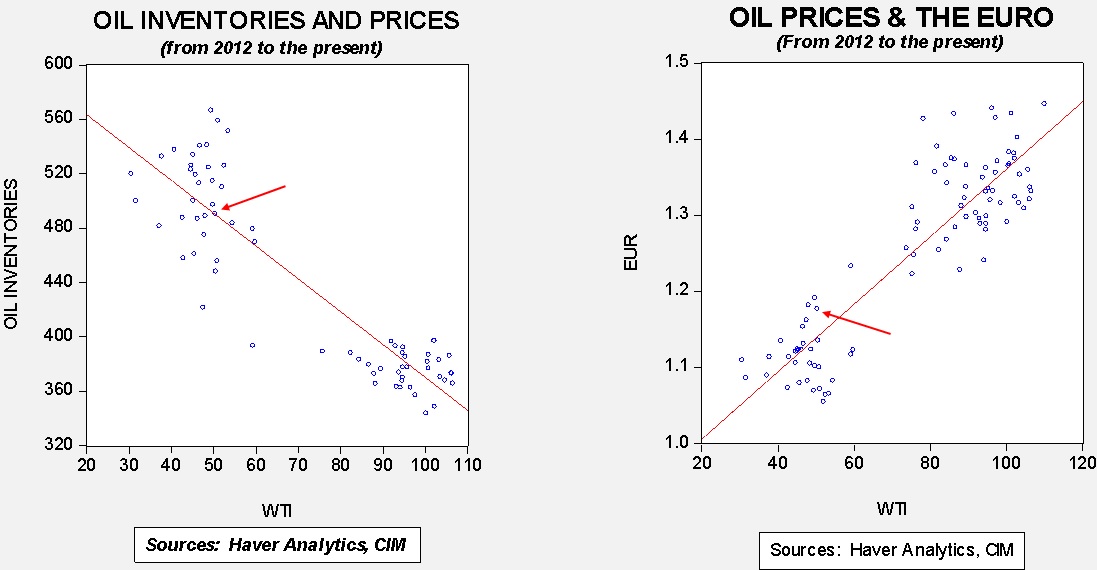

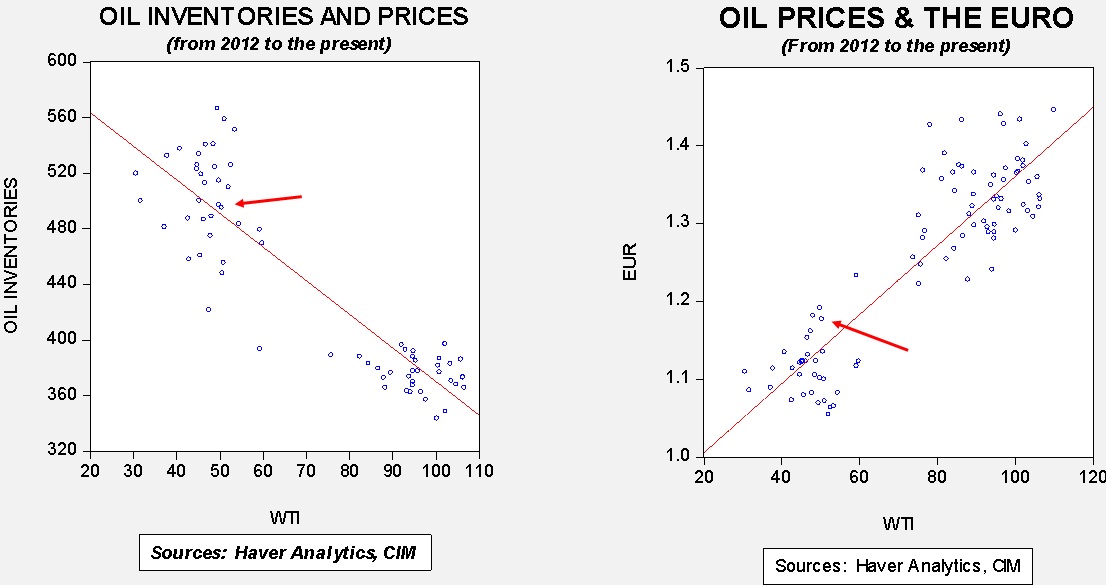

Based on inventories alone, oil prices are undervalued with the fair value price of $54.33. Meanwhile, the EUR/WTI model generates a fair value of $63.44. Together (which is a more sound methodology), fair value is $60.01, meaning that current prices remain below fair value. For the past few months, the oil market has not fully accounted for dollar weakness. However, now the markets are not even taking tightening inventories into account. In general, without the expected seasonal lift in crude oil inventories, oil prices at current levels are attractive.

[Posted: 9:30 AM EDT] Something unusual is happening this morning…equity futures are pointing to a lower opening. At the time of this writing, S&P futures are indicating about a 0.5% decline. In the sea of calm we have been operating in, such a modest decline does look rather different. We also note that other flight to safety assets are rising this morning—the JPY and EUR are higher, and Treasuries and gold are rising, too. Here is what we are watching today:

What’s behind this morning’s weakness? Although the proximate cause is the rising threat of state action by Spain against Catalonia, this probably isn’t it. The Catalonian government refuses to back down from independence and PM Rajoy appears ready to take steps to remove the provincial government from power and take control of the region. However, this isn’t really news as this action has been expected for some time. A good part of today’s weakness is probably just simply that we are due for some profit-taking. However, there are a few items that are worrying enough to remove some of the confidence in equities. Here is our list:

China and debt: Although Xi Jinping gave a long speech yesterday outlining his view of China as a rising power (long enough that a tea break was necessary), the other news out of China was far more sobering. The People’s Bank of China (PBOC) Governor, Zhou Xiaochuan, said in a talk today that excessive debt growth is raising the risk of a “Minsky moment” in China. Zhou may be replaced at the current party congress; if not, his term will end a year from December, so he is probably in the last 15 months of his career. He has been running China’s central bank since 2002, the longest serving governor of the PBOC in China’s history. So, what’s his concern about a “Minsky moment”? Hyman Minsky, who spent most of his career in St. Louis at Washington University, theorized that stability breeds instability, a condition known as the “financial instability hypothesis.” In other words, the longer an economy is stable, the more confident investors, firms and households become and the more likely they are to take on more risk and leverage. Zhou indicated this morning that, in his opinion, corporate debt is too high and household debt is rising rapidly. His worry is that leverage will magnify the cyclical variations in China’s economy in a pro-cyclical fashion, meaning that it will lead to stronger growth in expansions and deeper recessions in downturns. In a nation run by a communist authoritarian regime that desires stability, Zhou’s concerns are a significant concern. China needs to lower its debt; although it promises it can, history shows countries that have recently achieved development through debt investment have two paths to adjustment. They can either follow the U.S. depression model, which rapidly lowered U.S. private debt during the Great Depression through liquidation and foreclosure, or the Japanese model, which reduces private sector debt slowly by cutting growth to a sustainable level. Neither is pleasant but we don’t see a way for China to maintain stability, cut debt growth and maintain 6.5% GDP growth (as noted below, China grew 6.8% in Q3). We expect China to take the Japan option but try to get a bit better growth at 2.5% to 3.0% growth. That wasn’t the tenor of President Xi’’s speech. Thus, talking about China’s debt introduces a new risk to the global economy.

North Korea: The U.S.S. Ronald Reagan carrier group has moved to the Sea of Japan off Korea’s northeastern coast. According to reports, ships in this group have been given a warning order and prepared Tomahawk cruise missiles to fire on North Korean targets. There has been growing speculation that North Korea may either launch missile tests or detonate another nuclear device (or even both—an airborne test of a nuclear warhead over the open sea) during China’s 19th Party Congress. The U.S. is apparently prepared to retaliate if a test or a North Korean attack on American military assets in Japan, Guam or South Korea are part of North Korea’s actions to spoil Chairman Xi’s “party.” We note that the U.S.S. Theodore Roosevelt carrier group is near Hawaii and could move toward Korea, giving the U.S. two carrier groups if hostilities escalate. Although we don’t expect a conflict, tensions are high and the potential for a mishap is elevated.

Yellen and Trump today: Chair Yellen will meet with President Trump today. Although the president has indicated he likes Yellen’s low interest rate policy, he does favor looser regulation. Given the desire for less regulation and opposition to Yellen from Congressional Republicans, we doubt she will get another term. The best combination of easy policy and deregulation is probably Jerome Powell, who is favored for the chair position by Treasury Secretary Mnuchin. However, Trump may want a “name” and John Taylor would be the highest profile candidate among those mentioned. Taylor would probably be more hawkish on policy, which the president wouldn’t necessarily like, but he would also favor less regulation. We will be watching for post-meeting comments from the White House.

[Ed. note: we will update the energy recap in tomorrow’s report.]

Tax reform: Senate Republicans are moving closer to tax reform as 50 senators have agreed to begin debate on a budget resolution. In order for tax reform to happen, the Senate must first pass a budget appropriations bill. Currently, there appear to be a few holdouts that might prevent the budget resolution from passing through the Senate. Senator Rand Paul is the most vocal Republican holdout, stating that the bill fails to meet the budget cap requirement established in the 2011 Budget Control Act; Senator Bob Corker has also voiced similar concerns. In addition, there are still concerns about whether Senator Thad Cochran is healthy enough to vote as he has been recovering from an infection over the past few weeks. The GOP can only afford to lose two votes if they plan on passing a tax bill without help from the Democrats. That being said, there is growing speculation that tax reform will not get done by the end of the year. We continue to closely monitor this situation.

Return of the subsidies: Senators Lamar Alexander and Patty Murray reached a bipartisan deal that would fund healthcare subsidies for two years in exchange for giving states more regulatory flexibility with the law. Last week, Trump signed an executive order that would have ended subsidies that reimburse insurance companies for lowering deductibles, co-payments and other out-of-pocket costs for low income customers. At this moment, it is uncertain if it has enough support to become law; Senator McCain has expressed his support of the bill, while President Trump has backtracked on his initial support.[1] It is unclear whether Democrats are in favor of the bill, but it is widely perceived that Republicans will largely oppose it.

NAFTA stalemate: Renegotiations between the three-member trade alliance NAFTA ended at an impasse on Tuesday as Canada and Mexico were unwilling to give into U.S. trade demands. The countries will meet again next month for continued negotiations. During the negotiations, the U.S. asked for more flexibility to place import tariffs on certain goods such as automobiles, dairy and seasonal produce. The U.S. trade representative, Robert Lighthizer, told reporters that Canada and Mexico were being obstructionist and should be willing to “give up a little bit of candy” in order to secure a deal. We believe that this administration is possibly positioning itself for an eventual withdrawal from NAFTA. Furthermore, the Washington Post reported[2] that Peter Navarro, director of the White House Office of Trade and Manufacturing Policy, circulated a memo alleging that manufacturing jobs lost through trade contribute to increased abortions, divorces and spousal abuse; there was no data supporting the claim in the memo. A withdrawal from NAFTA could be bearish for U.S. equities.

Raqqa falls, what’s next? An American-backed militia, the Syrian Democratic Forces, claimed to have recaptured the northern Syrian city of Raqqa from the Islamic State. Raqqa is considered the capital for ISIS and its recapture represents a stunning blow to the dwindling group. The United States Central Command stopped short of claiming victory over ISIS, but has stated that the American-backed forces have wrested control away from ISIS. Despite the victory, there are concerns about how the U.S. plans to rebuild the areas formerly under ISIS control. Many fear that the defeat of ISIS could lead to a new power vacuum that could be filled by another militant group hostile to the U.S. As of right now, it appears that there are no detailed plans to rebuild the areas. President Trump’s insistence that the U.S. will no longer participate in nation-building further complicates the issue. We will continue to monitor this situation.

[Posted: 9:30 AM EDT] U.S. financial markets are quiet, but there is a lot going on again today. Here’s what we are watching this morning:

Taylor to the Chair? John Taylor, the creator of the “Taylor Rule,” visited President Trump yesterday and, according to news reports, the president was very impressed. Taylor is a well-respected economist with a good deal of government and academic experience. What makes him a bit of a surprise is that he is considered rather hawkish. When these reports emerged yesterday, the dollar rallied and Treasuries dipped. We would be surprised if Taylor gets the nod for chair, although it wouldn’t be a shock to see him appointed to the FOMC. In general, Trump favors lower interest rates; Taylor is on the record calling for a 2% real fed funds rate, or, assuming 2% CPI, a 4% nominal fed funds rate. Eurodollar futures are nowhere near that level and so we would view Taylor as a bearish event for equities and Treasuries, and bullish for the greenback.

Friends Again! Yesterday, Senate Majority Whip McConnell and President Trump stood side-by-side in the rose garden in a sign of unity as they prepare to pass tax reform. It has been reported that the two had a falling out after the Senate failed to repeal Obamacare. This display of friendship should be taken with a grain of salt as there have been reports that officials in Trump’s administration believe that Senate Republicans are an impediment to Trump’s legislative agenda. It is also worth noting that while speaking on their improved relationship Trump mentioned that he would talk Steve Bannon out of setting up primary challenges to Senate Republicans; earlier this month, Bannon stated that he is willing to go to war with establishment Republicans. We would interpret this gesture as a final olive branch before Trump gives up on the GOP and tries to pass legislation on his own. We will continue to monitor this situation.

More Headaches for the Catalan President: Yesterday, Spain’s high court sentenced the leaders of the Catalan National Assembly (ANC) and Omnium Cultural, Jordi Sanchez and Jordi Cuixart, to prison without bail pending an investigation of alleged sedition. The two men were accused of sedition due to their involvement in setting up massive protests to counter the Civil Guard’s crackdown on the October 1st referendum. As the two men were escorted from the courthouse, they were given a hero’s welcome from separatist supporters.

This event will likely put more pressure on Catalan President Carles Puigdemont to clarify his position on whether Catalonia has declared independence from Spain. Following the results of the referendum, Puigdemont stated that he has the mandate to declare independence but will suspend doing so in order to set up negotiations with the Spanish government. In response, the Spanish government has stated that it will not consider negotiating with Catalonia as long as it insists on becoming an independent state. In addition, Spain has given Puigdemont until Thursday to clarify his position or risk having his government dissolved. In rebuke of the Spanish government, the ANC sent a letter to Puigdemont urging him to immediately end the suspension of Catalan independence. Puigdeomnt appears to be in a lose-lose situation; if he formally declares independence he risks being removed from office, and if he does not declare independence he will likely lose the support of his base. Currently, Spanish equities are up but are trading slightly lower than last week.

So, you’re saying there’s a chance? Yesterday, CNN reported that a North Korean official stated that the region would only be willing to engage in diplomacy with the Trump administration if it has the capability to strike the East Coast of the U.S. Given all of its bluster, this statement represents a victory for SOS Rex Tillerson, who has maintained that sanctions will help bring North Korea to the negotiating table regarding its nuclear program. Over the past few weeks, SOS Tillerson and President Trump have offered differing strategies on how to deal with North Korea’s nuclear program. Tillerson would prefer to curb the program through diplomacy, while the president has advocated for ending the program militarily. These comments could be a prelude to possible negotiations but we are not prepared to rule out the likelihood of a U.S. preliminary strike. We will continue to monitor this situation.

The U.S. and North Korea have had a difficult history. The two countries were the primary combatants during the Korean War and still have not established a peace treaty. However, in the late 1970s, the Kim regime and the Carter administration considered normalizing relations. Carter’s national security team concluded there was little value in talking directly to North Korea[1] and, ever since, the U.S. has essentially “outsourced” North Korea to China.[2]

On its face, this decision makes sense. China is critically important to North Korea’s economy; more than 80% of North Korea’s foreign trade is with China. Mao described relations between the two countries as “close as lips and teeth.” However, relations are more than just economics. A review of historical relations between China and North Korea indicates a deep animosity that inhibits China’s ability to control the policies and decisions in Pyongyang.

In Part I of this report, we will begin our study of the historical relationship between North Korea and China, including a review of the Minsaengdan Incident and a broad examination of the Korean War. Part II will complete the analysis of the war, discuss the Kim regime’s autarkic policy of Juche and outline the impact of the Cultural Revolution on North Korean/Chinese relations. Part III will cover the controversy surrounding North Korea’s Dynastic Succession, the end of the Cold War and the ideological issues with Deng Xiaoping. Finally, we will recap this history and its impact on American policy toward the Democratic People’s Republic of Korea (DPRK) along with market ramifications.

[1] Carter was worried about being seen as weak by GOP critics. Creekmore, M., Jr. (2006). A Moment of Crisis: Jimmy Carter, The Power of a Peacemaker, and North Korea’s Nuclear Ambitions (chapter 7). New York, NY: Perseus Books Group.

[Posted: 9:30 AM EDT] Although U.S. financial markets are quiet, there is a lot going on. Here’s what we are watching this morning:

War in Iraq? Iraqi troops have taken a refinery and captured oil fields surrounding the city of Kirkuk. So far, only Iraqi regular army troops have been involved; the Iranian-dominated Iraqi Shiite militias have reportedly not been part of the action. Kurdish Peshmerga forces have withdrawn, avoiding a fight with Iraqi forces. Reuters[1] is reporting that General Qassem Soleimani, a key leader of the Iranian Republican Guard Corps (IRGC), has arrived in Kurdistan for talks. Soleimani is a somewhat shadowy figure in the IRGC but is considered to be the mastermind behind many of Iran’s tactics in the region. His presence there suggests Tehran is trying to contain the situation and prevent a wider war. To some extent, the tensions in Kurdistan are part of the collapse of IS. There is a power vacuum in western Iraq and eastern Syria; IS was the first to fill it, but it won’t be the last, and the process of determining who is in control will likely be difficult and lead to constant conflict. Oil prices lifted on the news.

A deadline for Catalonia: Catalan leaders are trying to support indigenous independence while avoiding a violent crackdown from Madrid. PM Rajoy has given Catalonia until Thursday to say, yes or no, whether independence was declared. If it was, look for a violent reaction from Spain. EU Commission President Juncker indicated today that he regrets that both parties in Spain didn’t heed his advice to talk sooner but said the EU would not mediate the crisis. Catalan leaders are stuck; if they back down from independence, they will likely lose their positions and more radical elements could replace them. If they declare independence, they will meet an ugly, aggressive response from Rajoy. So far, the EUR and Spanish debt have shown little signs of stress.

Austria moves right: As we noted last Friday, the Austrian vote went as expected, with the center-right People’s Party winning a plurality, making Sebastian Kurz the youngest leader of a major nation in the world. Kurz has moved the previously staid People’s Party into a more populist, right-wing party and has energized it with social media. He ran on an anti-immigration platform and will likely team up with the right-wing, populist Freedom Party. Although the general trend has been for populists to underperform in elections this year, as seen in France and the Netherlands, they have clearly done better in Germany and Austria. Populism remains a potent force in the West.

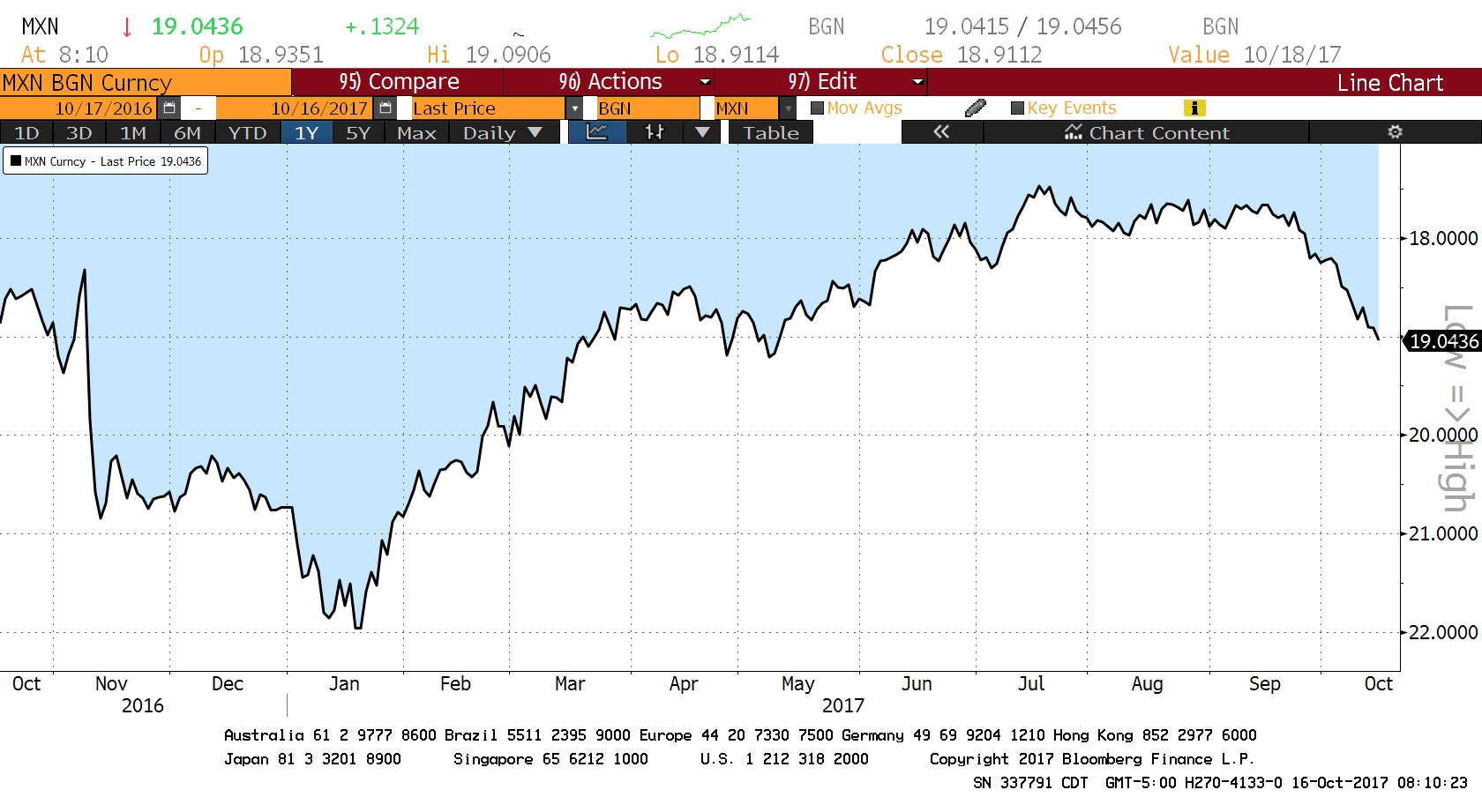

NAFTA worries: There are growing worries that the Trump administration will scuttle the agreement. There is talk of higher content rules for products (which would reduce imports of parts from Mexico and Canada) and sunset rules that would require renegotiation every five years. The former might be workable but the latter essentially kills the deal. Trade law changes business infrastructure; if it is open to major changes every five years then firms won’t make the investments into international supply chains and will simply produce more at home. Worries are starting to show up in the forex markets.

(Source: Bloomberg)

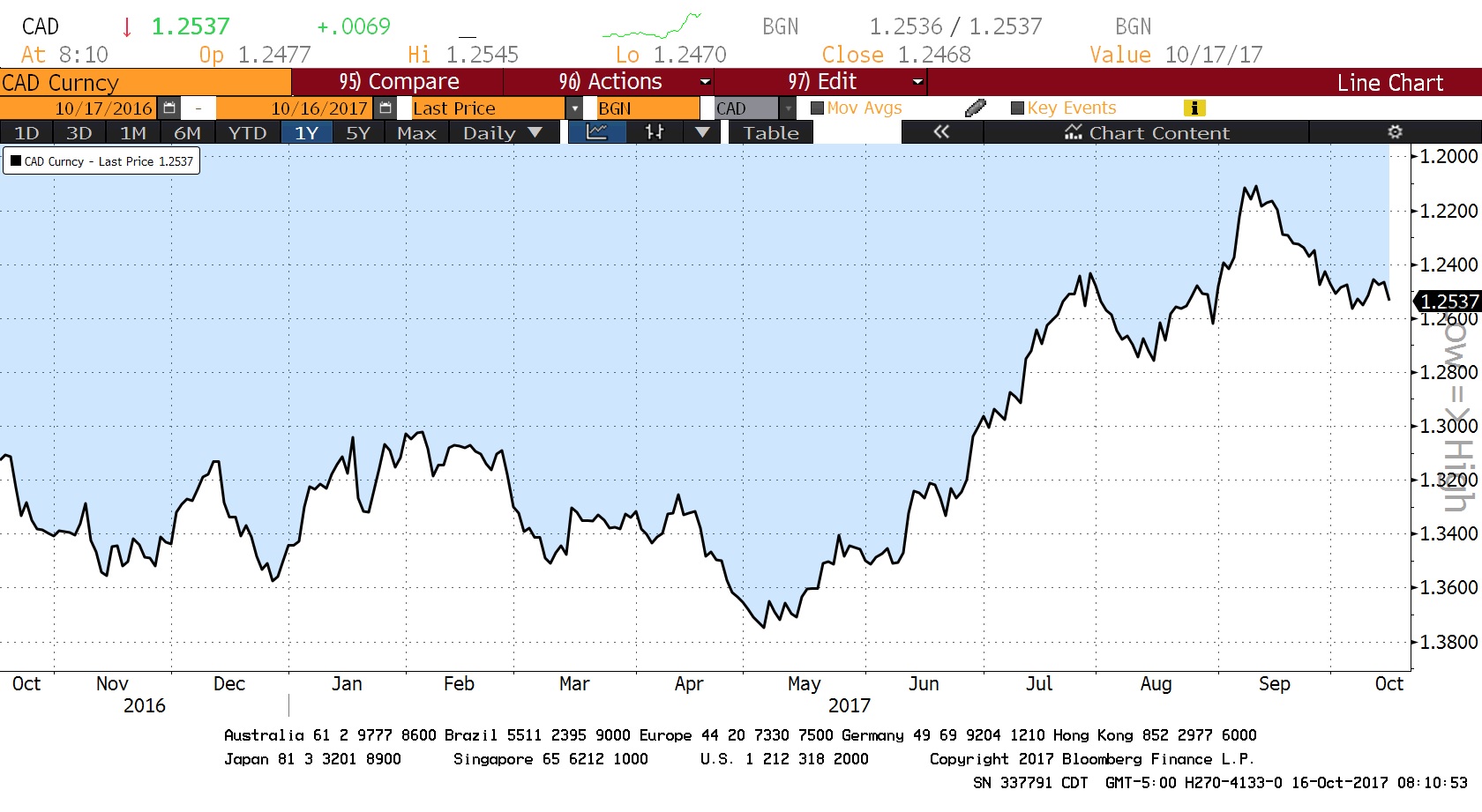

Concerns are clearly reflected in the MXN/USD (Mexican peso) exchange rate. This is the number of MXN per USD on an inverted scale. The MXN fell sharply after the election of President Trump but then the currency recovered on hopes that Trump, for all his rhetoric, would turn out to be a typical free-trade Republican. Note that the MXN has been weakening steadily since the middle of last month, reflecting worries about NAFTA. A somewhat less clear picture emerges on the CAD/USD (Canadian dollar) exchange rate.

(Source: Bloomberg)

Although the CAD didn’t weaken after the election (it was already quite weak), it rallied from May to September after the Bank of Canada raised rates. We have seen the currency weaken as NAFTA talks have deteriorated.

Yellen at the G-30: The G-30 is a group of finance officials from the industrialized nations. They met last weekend as part of the IMF meetings. Yellen reiterated her defense of the Phillips Curve and indicated that rates would continue to rise.

A worry for Turkey? A series of wiretaps suggests that PM (now President) Erdogan may have facilitated a violation of sanctions on Iran with gold for natural gas swaps in 2013.[2] The Turkish president has called the transcripts and tapes a fabrication but U.S. prosecutors think Turkey may have violated international sanctions on Iran. This case is damaging already strained relations with Turkey.

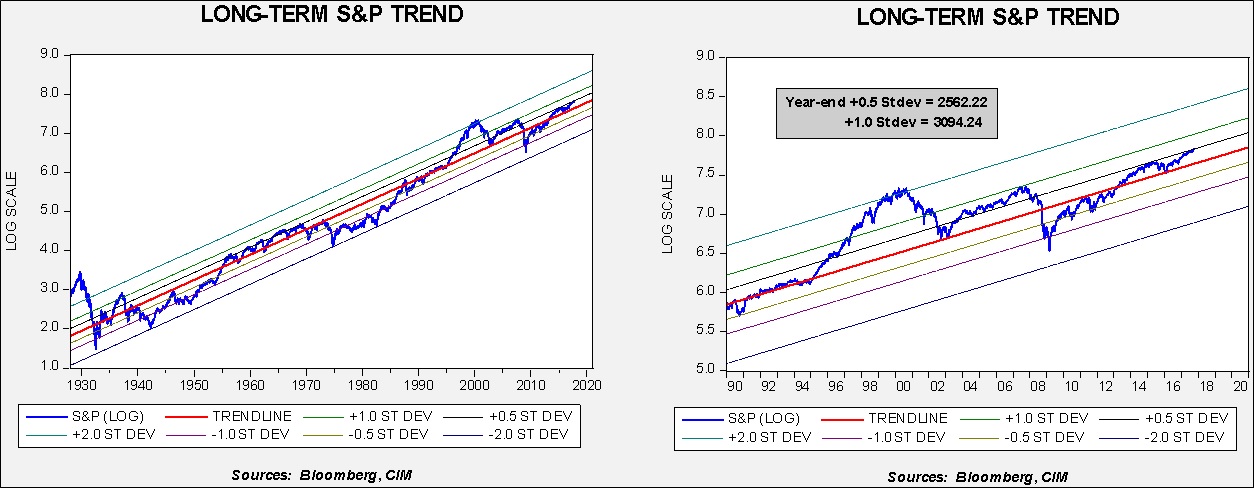

With the S&P making new highs almost daily, it is probably a good time to look at long-term trends to build some parameters.

This is a simple trend chart of the S&P 500 Index. We have log-transformed the weekly Friday closes of the index data and regressed it against a time trend. The chart on the left shows the index from 1929 while the chart on the right shows the index from 1990 (same regression trend lines for both charts).

Equities clearly trend higher over time. The yearly trend shows an average return for the S&P 500 Index of just over 6%. However, as the charts show, there is a fair degree of variation over time. The trend data shows that two standard errors above the trend is a dangerous area. One standard error above the trend is a concern. We are currently just below one-half standard error above the trend. That level by itself isn’t a big worry. In the 1950s into the early 1970s, we saw the index vacillate between the trend and one standard error above trend. These are not inconsequential market moves; in the current context, the trend line for the S&P 500 Index is 2090.26, meaning a pullback from current levels to the trend line would be a decline of about 17.6%.

Simply put, barring a recession or geopolitical event, equities are not seriously extended on a trend basis. We also note that the last two bear markets dropped a full two standard errors from peak to trough. The bear market that began in 2000 fell from two standard errors above the trend to the trend line (the bold red line on the chart), and the 2008 bear market ran from one standard error above the trend to one standard error below. Thus, a recession-triggered bear market would be a significant market event.

So, what does this tell us? Although there is a rather elevated sense of concern among investors, overall, the path of least resistance is to grind higher. Equities are not cheap but alternatives are even more expensive. The other insight this research offers is that a “melt-up” would take us well above 3000. If investors were to become “irrationally exuberant” we would expect a move to this level. At this point, there appears to be enough caution to prevent that from occurring. However, if a dovish Fed chair is nominated or a major tax cut appears likely to pass, a rise to these levels might be triggered. A recession is a clear worry; falling to one standard error below the trend line, which would be a drop of lesser magnitude than normal, would be to 1454.81 by year’s end. Obviously, because the trend line moves higher over time, the longer it takes to have a correction, the higher the expected bottom. For now, equities, based on this analysis, are not at levels that would usually signal a major bear market. At the same time, this doesn’t mean that there are no risks. It just means that, in terms of trend, we are not at extremes.

[Posted: 9:30 AM EDT] Markets are quiet again this morning; we are seeing the dollar weaken a bit and bonds rally on the weaker than forecast CPI data. On the other hand, retail sales were strong, although some of that is coming from hurricane distortion. Here is what we are following this morning:

ECB—less but longer: Reuters[1] is reporting that ECB policymakers have agreed on a plan to begin tapering. According to reports, the bank will extend the stimulus program by nine months but bond buying will be reduced to a range of €25 bn to €40 bn, down from the current €60 bn. The EUR eased modestly on the news. One of the problems is that the ECB is running out of eligible bonds to purchase so it needed to reduce its buying levels. At the same time, if this action is taken, the ECB is signaling its desire to remain accommodative. We view this action as modestly bearish for the EUR.

Tensions rise in Iraq: Iraqi forces are moving into the Kirkuk region, an area claimed by the Kurds. According to reports, Kurdish forces are withdrawing in front of the Iraqi deployment. Kirkuk is a key city in northern Iraq; both Kurds and Arabs see it as theirs (and both have controlled the town during various periods in history). It is also an important oil city. If open fighting develops, we would expect a disruption in oil flows and potentially higher prices.

Saudis buying Russian arms: Reuters[2] is reporting that Russia and Saudi Arabia are nearing a deal in which the latter will purchase the S-400 air defense system from Russia. This is a sophisticated air defense system, considered one of the best in the world. In fact, it seems odd the Saudis would need such a sophisticated air defense system because it isn’t obvious they face that sort of threat. We suspect this is a gesture of goodwill and a signal of deepening cooperation between Russia and the kingdom. Although the Trump administration has been working to improve relations with Saudi Arabia, it’s no secret that U.S. geopolitical interest in the region has lessened with the end of the Cold War and the advent of shale oil. We would expect continued cooperation between the two states as Saudi Arabia adjusts policy to emerging U.S. actions.

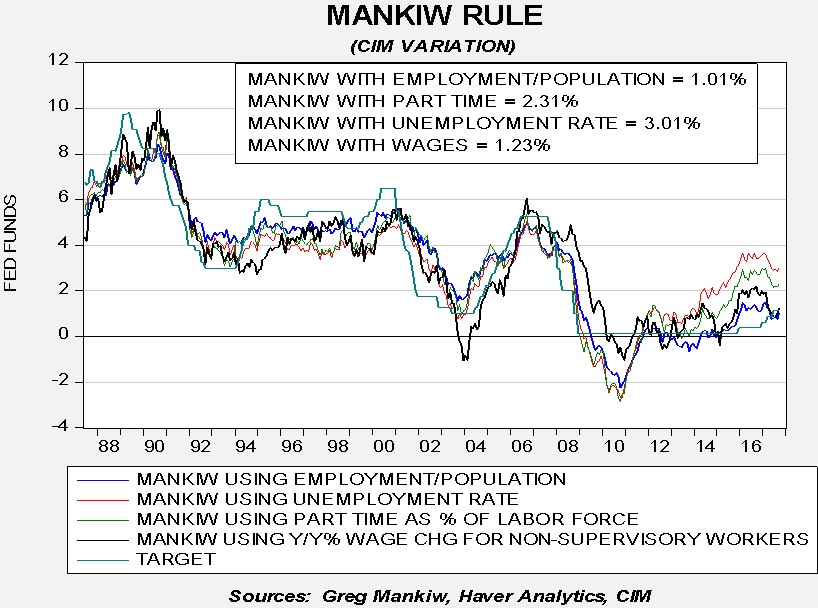

Fed policy: With the release of the CPI data we can update the Mankiw models. The Mankiw rule models attempt to determine the neutral rate for fed funds, which is a rate that is neither accommodative nor stimulative. Mankiw’s model is a variation of the Taylor Rule. The latter measures the neutral rate using core CPI and the difference between GDP and potential GDP, which is an estimate of slack in the economy. Potential GDP cannot be directly observed, only estimated. To overcome this problem, Mankiw used the unemployment rate as a proxy for economic slack. We have created four versions of the rule, one that follows the original construction by using the unemployment rate as a measure of slack, a second that uses the employment/population ratio, a third using involuntary part-time workers as a percentage of the total labor force and a fourth using yearly wage growth for non-supervisory workers.

Using the unemployment rate, the neutral rate is now 3.01%. Using the employment/population ratio, the neutral rate is 1.01%. Using involuntary part-time employment, the neutral rate is 2.31%. Using wage growth for non-supervisory workers, the neutral rate is 1.23%. The improved labor market data has lifted each model’s neutral rate calculation by 15 bps to 25 bps, putting all but the employment/population ratio variant below the current target.

Although the core rate rose less than forecast, we suspect there is enough support for a December hike to keep the likelihood of a move high. Fed funds futures still put the odds at 78% for an increase.

Energy recap: U.S. crude oil inventories fell 2.8 mb compared to market expectations of a 2.0 mb increase.

This chart shows current crude oil inventories, both over the long term and the last decade. We have added the estimated level of lease stocks to maintain the consistency of the data. As the chart shows, inventories remain historically high but have declined. The impact of Hurricane Harvey is diminishing as refinery operations recover. We also note the SPR fell by 1.8 mb, meaning the total draw was 4.6 mb.

As the seasonal chart below shows, inventories fell this week. It appears we have started the inventory rebuild period sooner than normal this year due to the hurricanes. However, over the past two weeks, inventories have declined, which is a modest surprise based on the seasonal pattern.

(Source: DOE, CIM)(Source: DOE, CIM)

Refinery operations unexpectedly rose last week, which is a divergence from seasonal norms. Strong product demand and attractive refining margins are supporting strong utilization. The seasonal trough usually occurs next week; this week’s activity suggests that the maintenance season may be concluding early, which is bullish for oil prices.

Based on inventories alone, oil prices are undervalued with the fair value price of $52.79. Meanwhile, the EUR/WTI model generates a fair value of $63.15. Together (which is a more sound methodology), fair value is $59.27, meaning that current prices are well below fair value. For the past few months, the oil market has not fully accounted for dollar weakness. If the oil market begins to recognize the dollar’s weakness, a broader rally in oil is possible.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.