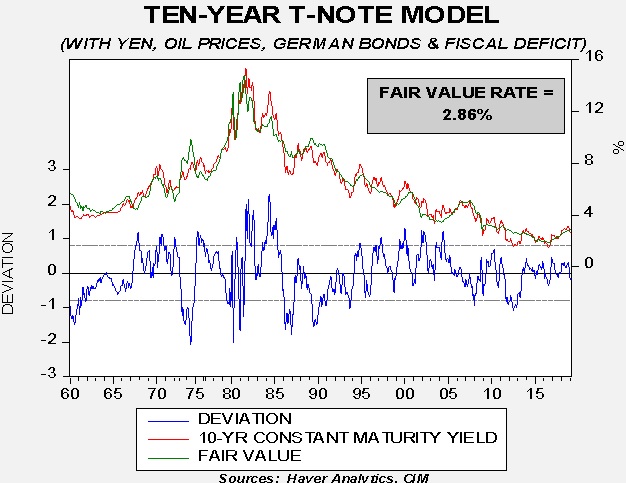

Long-dated Treasury bonds have enjoyed a strong rally in recent weeks. Fears about future U.S. economic growth, falling global economic growth and a reversal in monetary policy expectations have all conspired to lower yields. The question now is whether or not yields have fallen more than is justified by the fundamental factors.

This is our model of the 10-year T-note yield. Independent variables in the model include fed funds, an inflation proxy,[1] the yen/dollar exchange rate, German 10-year yields, WTI oil prices and the fiscal deficit as a percentage of GDP. The standard error line is 70 bps; thus, at current fair value, the 10-year T-note yield would be “rich” around 2.15%.

In general, the first two variables have the most explanatory power. The current yield is well below the fair value of 2.86%.[2] One way to account for the decline in yields would be if the market was projecting easier monetary policy. Leaving the rest of the independent variables unchanged, to reach a 2.40% 10-year T-note yield would require fed funds of about 1.50%, or a 100 bps reduction from current levels. Since such a cut is unlikely in the near term, it is arguable that the 10-year yield has overshot to the downside.

However, another possibility is that inflation expectations are falling. Inflation expectations have a powerful effect on long-dated debt yields. Our current inflation proxy puts inflation at 2.10%. To achieve current yields, inflation expectations would need to fall to 1.41%. Although inflation expectations are not directly observable, we assume such expectations are slow to change.[3] Thus, it would be unlikely that a drop in inflation expectations alone would account for the recent decline. However, inflation expectations falling to 1.8% and fed funds at 2.00% would bring yields close to 1.40%.

It is quite possible that falling inflation expectations and forecasts of easier monetary policy can justify the current 10-year yields. The risk is that the FOMC keeps policy steady and inflation eventually surprises to the upside. Thus, we would not see the current environment as conducive for extending duration.

[Posted: 9:30 AM EDT] Good morning, all! Equity markets are higher on progress being made in U.S./China trade talks. The overnight news was a bit quiet, but here are the stories we are following today:

Social media bias: On Thursday, Facebook (FB, $165.55) was accused of violating the Fair Housing Act by the Department of Housing and Urban Development. Allegedly, Facebook targeted real estate advertisements to people based on their race and color; Twitter (TWTR, $32.87) and Google (GOOGL, $1,172.27) are also being reviewed by HUD for similar violations.[1] The Trump administration has frequently criticized social media companies for being biased. Accordingly, we view this conflict as an escalation in tensions between the administration and the tech giants. Earlier this week, Facebook stated it would ban content from groups that are associated with “white nationalism” and Twitter announced it was considering labeling tweets from the president and other politicians if they violate its rules.[2],[3] Although we can’t say for certain that all these actions are related, the timing does seem to match up. Conservatives have long harangued social media platforms for promoting views that the platforms support while censoring views they don’t. If the contentious relationship between social media companies and this administration continues to escalate we would expect the president to become more vocal about breaking up some of these firms.

Guaido ineligible? The Maduro regime stepped up its war against the opposition by declaring Juan Guaido ineligible to take office for 15 years. The announcement came from state comptroller Elvis Amoroso, who claimed there were “inconsistencies” found in Guaido’s personal finances. We view the ruling as a way for the Maduro regime to undermine Guaido’s popularity in Venezuela and to delegitimize his claim as the leader of the country. Following a controversial election that saw Maduro win in a landslide, Juan Guaido was recognized by the U.S., Canada and several South American countries as Venezuela’s interim president. Since then, Guaido and his supporters have been trying to wrest power away from the Maduro regime. The move to delegitimize Guaido likely signals that Maduro believes he can wait out the opposition in order to maintain power, in much the same way Bashar Assad was able to do in Syria. If this is his plan, we do not expect the stalemate between Maduro and his opposition to end anytime in the near future.

Brexit Day deal: Today, U.K. Prime Minister Theresa May will attempt, for a third time, to pass her Brexit deal through parliament. PM May has done everything possible to get this deal through parliament, even agreeing to resign following its passage, but it appears she still does not have enough support. The EU has shown little patience with the U.K. and has stated that if the deal fails to pass today then the U.K. will have until April 12 to secure another deal or risk leaving the EU with no deal. It is unlikely the EU would choose a no-deal Brexit if the sides were close to an agreement, but it seems the EU is getting a bit fed up.

[Posted: 9:30 AM EDT] Happy Opening Day! Even as cool temperatures linger in much of the country, major league baseball opens in the U.S. today, one of the official signs of summer. Here’s something to make you feel older: for the first time in the 21st century, there are no players on team rosters that have major league playing time in the 20th century.[1] Equities are modestly higher in a quiet news environment. There have been a number of Fed speakers in the past few days. The message remains consistent—the central bank is on pause, but not moving to ease. Here is what we are watching this morning:

Brexit: If ever there was a day that showed there is no consensus on a path forward, it was yesterday. All the indicative votes failed to reach a majority.[2] PM May offered to resign if her plan was accepted. Although that did sway some hardline Brexit supporters, the Northern Irish DUP rejected the offer.[3] This outcome probably means we will get a long extension of Article 50 and a new PM to guide the effort. The GBP is down a bit today but a long extension probably means the exchange rate will remain mired at roughly current levels.

Turkey: As we noted yesterday, in the run-up to elections Turkey has sent overnight interest rates to astounding levels, in excess of 1,000%, to punish currency shorts. Turkey has been struggling for the past year with rising inflation and recession. We would expect rates to fall after this weekend’s local elections.[4] While Erdogan is clearly safe in his position, this election has evolved into a referendum of sorts on the regime, so he is trying all kinds of actions to lift sentiment. Although conditions in Turkey remain difficult, we note that the exchange rate has fallen significantly, supporting a strong improvement in the current account. In other words, conditions are not good, but most of the bad news is already discounted.

Chinese trade: USTR Lighthizer is back in Beijing for talks; Chinese officials are expected in Washington next week. There are reports of progress[5] but nothing concrete ever emerges. This looks like a “stall” game. China is probably hoping that it can extend negotiations into early next year and expect election issues to dominate, allowing China to avoid making excessive concessions.[6] From a financial markets perspective, discussions won’t end suddenly, leading to tariffs and a drop in equity values.

A side note on China: Former colleagues of mine at Doane, an agricultural research service, inform me that the African Swine Fever[7] (ASF) is becoming a serious problem. The disease, so far, has affected Europe, Asia and South America. It poses no risk to humans but it is nearly 100% fatal to pigs. Thus, once a herd is affected, it essentially wipes out the group. The USDA and Customs continue to work hard to prevent the disease from entering the U.S.[8] ASF can be spread by pork products, so strict enforcement is vital. This event will almost certainly lead to higher pork prices in the U.S. as summer grilling season approaches; we would also expect China to “offer” to buy lots of U.S. pork as their supplies dwindle due to the epidemic in China.

Another side note on China: Taiwan’s President Tsai Ing-wen said today that the U.S. is open to the island’s request for new arms sales.[9] If the Trump administration does increase arms sales to Taipei, it will increase tensions with Beijing.

India joins another club: India has successfully shot down a satellite with a ground-based missile, becoming the fourth nation in the world to show it has this capacity.[10] Although there is speculation that this news is part of a pre-election plan to boost Modi’s reelection, the fact that India could “blind” its primary adversary, Pakistan, in a conflict raises the potential for escalation in a crisis.

Energy update: Crude oil inventories rose 2.8 mb last week compared to the forecast decline of 3.0 mb.

In the details, refining activity fell 2.3%, which was a surprise. Estimated U.S. production was unchanged at 12.1 mbpd. Crude oil imports and exports both fell 0.4 mbpd.

(Sources: DOE, CIM)

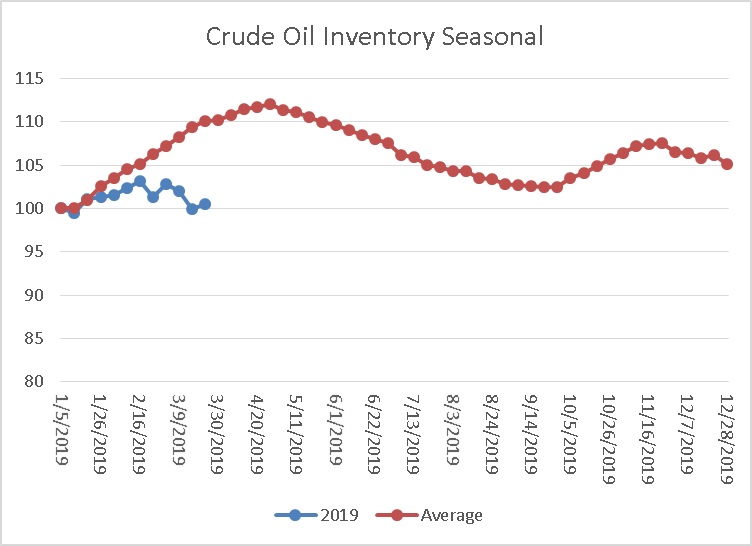

This is the seasonal pattern chart for commercial crude oil inventories. We would expect to see a steady increase in inventory levels that will peak in early May; the pattern coincides with refinery maintenance. Even with the build this week, the market is well behind normal which is supportive for prices.

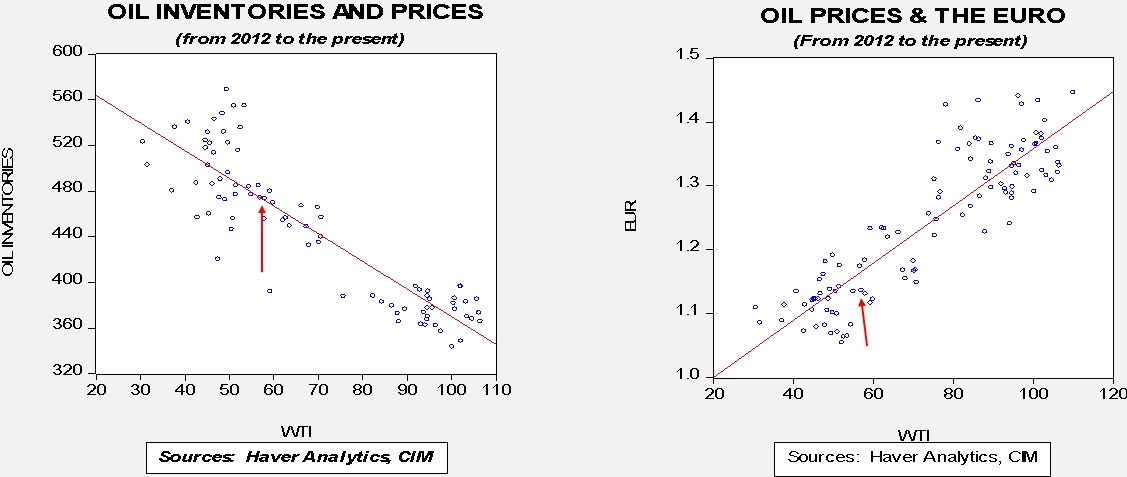

Based on oil inventories alone, fair value for crude oil is $59.87. Based on the EUR, fair value is $53.30. Using both independent variables, a more complete way of looking at the data, fair value is $54.86. We are seeing the two fair value levels widen, with oil stocks very supportive, while the dollar isn’t all that supportive for prices.

In other oil news, President Trump tweeted for lower oil prices this morning, sending markets lower. OPEC has consistently ignored the president on his calls for greater output. Saudi Aramco is coming to market with a $10 bn bond to partially fund its purchase of a Saudi petrochemical company.[11]

[Posted: 9:30 AM EDT] Equities are modestly lower in a quiet news environment. The big story remains in the long end of the yield curve as the 10-year T-note yield falls below 2.40%. Here is what we are watching this morning:

Why are bonds rallying? We suspect there are two factors sending yields lower. First, expectations toward monetary policy have flipped. The market expects the next move by the FOMC will be to lower rates. Stephen Moore, the president’s most recent nominee for Fed governor, is calling for an immediate rate cut of 50 bps. Although none of his future colleagues are supporting him (so far), assuming he is confirmed, he will be a consistent voice in favor of rate cuts. It should be noted there is an international element to this trend. ECB President Draghi indicated today that his bank is prepared to support the Eurozone economy by delaying policy tightening.[1] Second, there are growing fears that the economy is not only slowing but may be stumbling. With inflation low and economic data weak, there is an incentive for safety assets. To some extent, the rally in bonds is starting to look like a momentum trade, which probably means it’s getting overdone. Reversing the rally will require improved economic data.

Brexit: The “indicative voting” process begins today and will likely continue into tomorrow.[2] Sixteen different proposals are being considered. None are binding on the government; however, if any get overwhelming support (which isn’t likely) then PM May would be forced to either support the proposal or resign. Champions of Brexit are coming to the realization that May’s plan may be the best they can get, so there has been some talk of simply accepting the May plan.[3] Overall, we doubt anything definitive comes out of this process; if we are correct, the odds of a long delay are increasing.

Bouteflika out? The current president of Algeria appears to be losing support of the military. The army chief of staff, Gen. Ahmed Salah, is now openly calling for the president to be removed.[4] Bouteflika has suffered a series of strokes and is, by most accounts, incapacitated. So, if the military has decided that he is finished then it probably means the end is near. A peaceful transfer of power in Algeria is important; the country is a member of OPEC and a significant supplier of natural gas to Europe.

An update: Earlier this month, we reported that a shadowy dissident group had broken into North Korea’s embassy in Madrid as President Trump and Chairman Kim Jong-un were meeting in Hanoi. Apparently, the leader of the “operation,” a Mexican national living in the U.S., Adrian Hong Chang, fled to Portugal after the raid and flew back to the U.S. An American, Sam Ruy, was also involved. Spanish officials have issued international arrest warrants for both men. According to reports, the group has offered materials seized in the raid to the FBI. U.S. security officials have declined to comment.[5]

Turkey and the lira shorts: In the run-up to elections, Turkey has sent overnight interest rates to nosebleed levels, around 300%, to punish currency shorts. To short a currency, a trader essentially borrows in the currency he is shorting. The high interest rates are making shorting really expensive, reducing the attractiveness of such activity. Obviously, it will be impossible to continue such high interest rates indefinitely. At some point, those overnight rates will begin to affect other areas of the Turkish yield curve. But, in the short run, the move will stabilize the lira, which has been under pressure recently.[6]

The return of the exurbs:The WSJ reports that housing development away from urban centers has been showing signs of life, adding to evidence that the housing market is continuing to recover.[7] The article suggests that even younger buyers, who up until now have opted for urban rental property, are following the path of their parents and grandparents and moving out of the cities for cheaper housing after starting families.

[Posted: 9:30 AM EDT] Equities are higher in a quiet news environment. Here is what we are watching this morning:

Brexit: MPs voted 329/302 to take control of the House of Commons timetable, essentially removing the prime minister from running the process.[1] Although this is no huge shock, it isn’t obvious whether the MPs will have any better ideas. Parliament will begin holding a series of “indicative votes”[2] tomorrow to test out various ideas, which include combinations of May’s plan plus joining the customs union to a hard exit or another referendum. PM May remains defiant, suggesting she may not implement whatever Parliament decides. She can certainly threaten, but if she defies the will of Parliament she will almost certainly trigger a vote of no-confidence and an ouster. New elections cannot be ruled out. As it sits now, it looks to us like the most probable outcome is a long extension of the deadline. That’s about the only thing that likely has a majority of support. Such an outcome is modestly supportive for the GBP.

Bond bull market: Fears of recession and the lack of inflation have pushed the 10-year T-note yield below 2.50%. We are starting to see other effects from this rally in bond prices. First, the amount of global bonds with a negative yield hit $10 trillion, up from $6 trillion late last year.[3] The German 10-year Bund fell back into negative territory. Second, the BOJ is now talking about further monetary stimulus.[4] It is hard to see how taking rates below zero would stimulate growth; about the only factor that might boost the economy is a weaker yen, but that would get Japan in trouble with the Trump administration. Third, Fed policymakers are resurrecting the “operation twist” idea, where the Fed buys more short paper to steepen the yield curve.[5] Monetary policy is a spent force at this point, with the only remaining stimulative tool being fiscal spending.

Bolton v. Pompeo:Although both are considered Iran hawks, there is a split between them on implementing Iranian oil sanctions.[6] Pompeo wants to extend oil waivers to at least some of the eight nations that were initially granted waivers. In fact, China and India, which are currently receiving waivers, would probably continue to buy Iranian oil regardless of U.S. actions. On the other hand, not extending waivers would almost certainly weaken the terms for Iran on the oil it sells to India and China. Pompeo wants to extend waivers, while Bolton wants to end them. The other consideration is the price of oil; the Trump administration has made it clear it wants low oil prices and ending waivers would likely lift prices, at least initially. Saudi Arabia, in defiance of the U.S., continues to support $70 Brent prices.[7] Thus, if the waivers are ended, we would not expect OPEC to immediately step in to cover any shortages. However, history also shows that cartel discipline tends to weaken as prices rise.

In Part II, we discussed the principles and consequences of Modern Monetary Theory (MMT). This week’s installment will be devoted to the importance of paradigms. Next week, we will conclude the series with a discussion on the potential flaws of MMT along with market ramifications.

The Importance of Paradigms

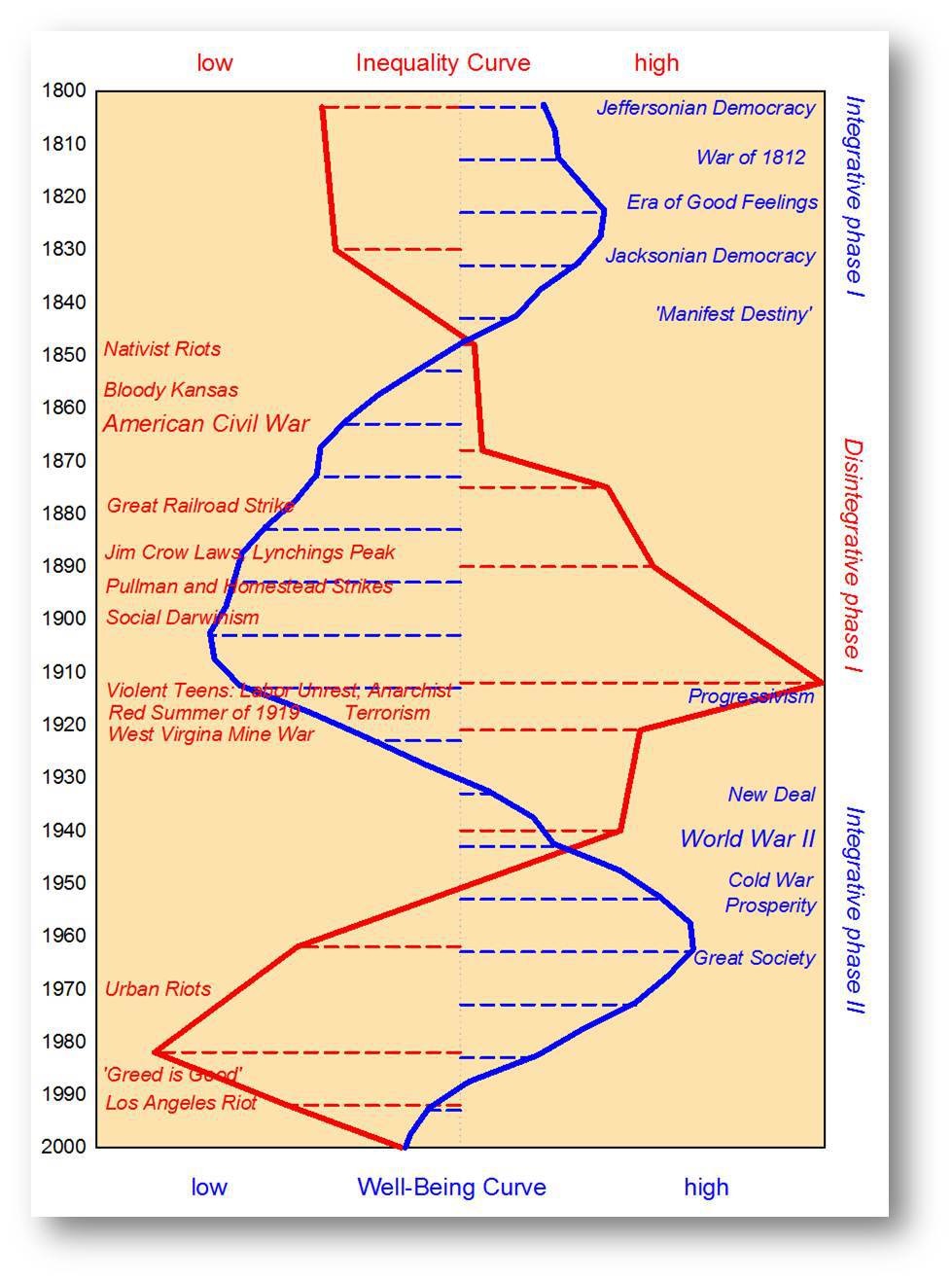

Every major shift in the efficiency/equality cycle has coincided with a favored economic theory to promote the change. The following chart from Peter Turchin shows his take on inequality and wellbeing cycles in U.S. history. Although Turchin doesn’t fit his pattern to Arthur Okun’s equality and efficiency tradeoff,[1] we see a strong match between this tradeoff and Turchin’s wellbeing and inequality cycles. During periods where Turchin’s wellbeing line is rising and inequality is falling, the economy is going through an equality cycle. Equality cycles are sometimes characterized by policies that favor labor (which may include high marginal tax rates, easy monetary policy, policies that favor unions and social mores that promote “the common man”[2]).

Usually, equality cycles end when the economy needs to build productive capacity to reduce inflation and thus needs to increase efficiency. These are policies that favor capital, which may include low or non-existent tax rates, reduced regulation, anti-organized labor policies and social mores that lionize wealth.[3]

(Source: Peter Turchin[4])Our historical analysis suggests there have been four shifts in equality and efficiency and each has been supported by an economic theory that gave intellectual credence to the shift.

[Posted: 9:30 AM EDT] Equities have lifted from their overnight lows on a better than expected German IFO business sentiment index report. Although the Mueller news didn’t have any impact on financial markets, a finding of collusion would have been majorly negative, so that problem has been avoided. Here is what we are watching this morning:

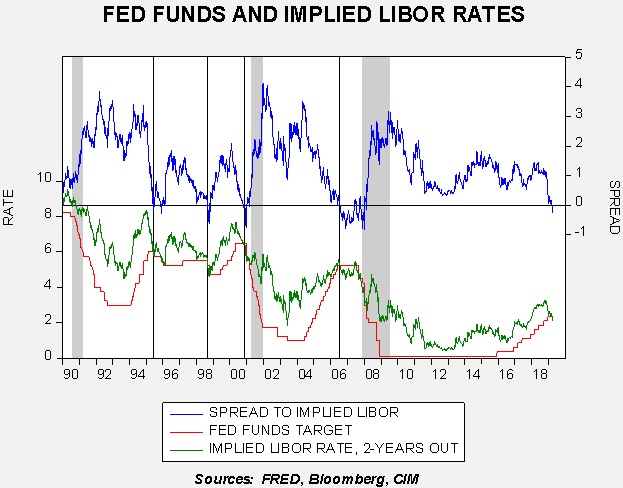

A signal for the Fed: We use the implied rate from the three-month Eurodollar futures, two years deferred. Essentially, it is the market’s projection for LIBOR two years from now. It has had an uncanny ability to signal what monetary policy “should” do. Over the past week, a clear signal has emerged—the Fed needs to cut rates now.

The green line shows the implied LIBOR rate, the red line is the policy rate and the blue line shows the spread. We have placed vertical lines at points of earlier inversions. The genius of the Greenspan Fed was that he tended to cut rates quickly when the blue line fell below zero. Although there is no record of the FOMC using the above chart signals for policy, it is essentially a yield curve analysis, which policymakers closely monitor. The Bernanke Fed stopped raising rates at the point of inversion but was slow to cut, which probably led to the 2007-09 recession. The Powell Fed is now facing a similar situation.

Given the state of flux in the underlying theories of policy, it might be possible for Powell to push the committee to cut rates. But, given how rapidly the Fed has moved from tightening in December to steadying by March, taking the next leg to cut might be too difficult for Powell to manage. Although this inversion doesn’t mean recession is imminent, it does suggest that the odds of a recession are significantly higher than they were just a few months ago.

Brexit: We are expecting a series of votes this week that probably won’t clear up anything. The problem is that there is no consensus in Parliament on a way forward. The situation in the legislature likely reflects conditions among the electorate. Over the weekend, there were large marches in London for a second referendum.[1] Meanwhile, Brexit fatigue has led to sentiment for a hard Brexit just to end the eternal drama.[2] PM May faced pressure to resign over the weekend, which she managed to fend off, but the chances of her ouster remain elevated.[3] The GBP is holding its own with the current delay in place, but there is still the potential for the U.K. to stumble into a sudden break with the EU, which, at least in the short run, would probably be devastating for the U.K. economy.

Chinese trade talks: Although negotiations continue, China is not bending on technology.[4] We do believe both President Trump and General Secretary Xi need a deal, but they may be misjudging who needs it more. If the talks break down, equities will not take it well.

Stephen Moore for Fed Governor: President Trump tweeted that he will nominate Stephen Moore for one of the open governor positions on the FOMC. There has been rather strong pushback from both the establishment right and left.[5] We view this announcement as further evidence that the president is becoming more comfortable with his office. He followed the advice of Treasury Secretary Mnuchin on Powell, Clarida and Liang. Trump has found all of them wanting because he doesn’t want a technocrat at the Fed; he wants a loyalist. Moore has pressed for Powell to cut rates; during the Obama administration, he argued the Fed should have raised rates to avoid hyperinflation. Although mainstream economists will oppose Moore’s appointment, we don’t expect the Senate to turn it down.

We are in the very early stages of moving the Fed from an independent technocratic body to a more politicized one. This shift is probably inevitable due to the desire to reflate the economy. An independent Fed will tend to be more concerned about containing inflation, which is not what the populist uprising wants. Although reflation will take some time, the signs are all in place—trade wars, immigration opposition and now changes at the FOMC.

Italy joins the Belt and Road project: Italy welcomed President Xi and signed a MOU to join the Belt and Road project.[6] Although the actual impact probably isn’t going to be a big deal, the symbolism is huge. This is the first G-7 nation to join the project. Italy’s economy has struggled within the Eurozone and it would like to get support from the outside. China is undermining the U.S.-led order, in part, because the U.S. is less interested in the “care and feeding” of that order. It still isn’t obvious that China has the economic heft to generate a new world order, but it can clearly weaken the current one.

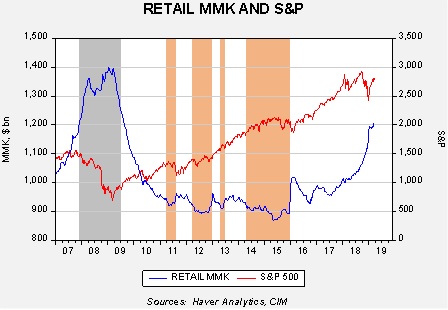

One factor we have been tracking is the recent behavior of retail money market funds. We have noted that households began building money market funds about the time that the equity market peaked and U.S. trade policy began to turn toward protectionism. In the coming months, money market funds continued to rise even as the S&P 500 made new highs. However, as equity markets fell in Q4, money market funds rose rapidly, with the pace of the increase rivaling what we saw in 2007-08.

This chart shows retail money market funds and the S&P 500. The gray shaded area shows the 2007-09 recession. The orange shaded areas show periods when money market funds fell below $920 bn. When money market funds fell to those levels, equities tended to stall. In recent weeks, the pace of increases in retail money market funds has slowed but still continues to rise, even with the market’s recovery. It may be difficult for equities to move much higher without retail participation.

In light of this analysis, which we have been discussing on a regular basis, another thought emerged—what is the role of cash in a portfolio? To examine this issue, we decided to look at cash instruments in the holdings of households.

It turns out that cash has a complicated history.

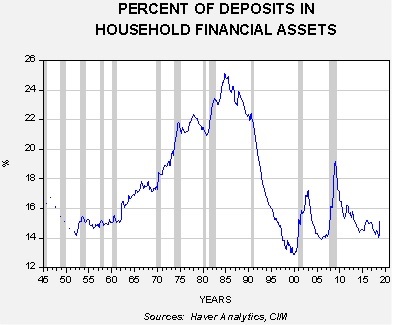

This chart shows the percentage of deposits in household financial assets. From the early 1950s into the early 1980s, the level of deposits generally rose. This rise was probably due to a number of factors. During this period, there was a steady rise in household income; at the same time, the financial system was heavily regulated. Regulations limited households’ flexibility in investing. However, by the mid-1980s, Regulation Q, which put caps on deposit rates, was removed. And, the financial services industry greatly expanded the products available and improved the logistics of investing. Financial deregulation increased the access to borrowing for households; thus, the need to save for purchases diminished. Income inequality also rose after 1979, which likely concentrated saving into fewer households. With more liquidity, these high income households were more likely to look for other investment opportunities. Essentially, the bull market in stocks that began in the early 1980s and ended in 2000 was supported by a more than 10% point decline in the share of deposits in household accounts.

Household deposits function as an investment, a way to smooth out spending and a flight to safety instrument. Thus, one would expect there to be a close relationship between consumption and deposits and a rise in deposits relative to consumption during periods of crisis. In fact, these features do exist, but there was a significant break in the relationship starting in 1990.

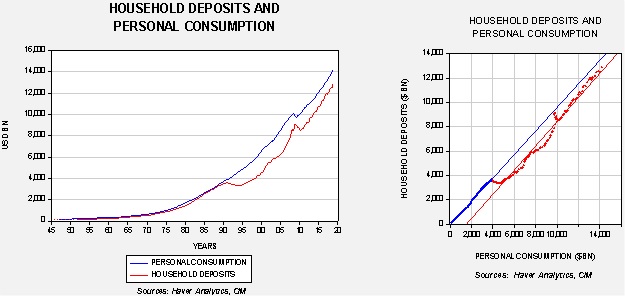

The chart on the left shows the time series of personal consumption and household deposits; the one on the right shows a scatterplot with regression lines. Note that after 1990, the relationship curve shifted to the right, meaning that fewer deposits were required to support consumption. Deposits rose sharply in 2005, even faster than consumption. That was when the housing crisis began and there was clearly a flight to safety.

Since 2005, there has been a steady increase in deposits relative to consumption, which would suggest a generalized increase in fear relative to the period from 1995 to 2005.

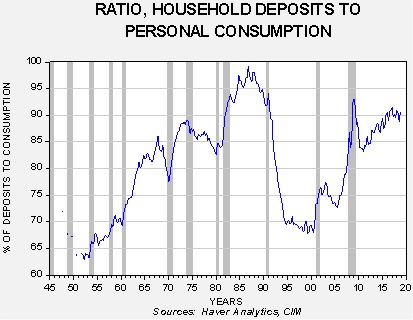

This chart shows the ratio of deposits to consumption. In 2000, deposits fell below 70% of consumption. The ratio rose after that and has currently reached 90%. Note how fast the ratio rose after housing peaked in 2005—there was a clear flight to cash that culminated in the Great Financial Crisis. That level of fear has persisted, shown by the high level of deposits relative to consumption.

In conclusion, as the first chart shows, we have seen a lift in money market funds. This does suggest an elevated level of fear in financial markets. However, the recent rise should be viewed within the context of overall cash holdings in households. Essentially, households are holding high levels of deposits relative to consumption, suggesting rather high levels of caution already. We still believe that retail money market funds need to decline in order to see equities rise this year; however, it also seems that households are not as complacent as they were in 2005 and therefore the likelihood of a financial crisis is probably not very high.

[Posted: 9:30 AM EDT] Good morning! Equity markets are mixed today following weak manufacturing data in Europe and the president’s hints that a trade deal with China is close to fruition. Below are the stories we are currently monitoring:

Brexit extension: On Thursday, the Financial Times reported that the EU is preparing to offer the UK an extension on Brexit on the condition that MPs approve a withdrawal agreement next week. According to reports, the EU would agree to an extension of May 22, the day before the European Parliamentary elections, on the condition that May is able to gain parliamentary support. However, if the U.K. Parliament rejects May’s offer then the EU would consider an extension of nine months. If this longer extension occurs, then the UK will be required to participate in the EU elections. Brexiteers are furious at the prospect of the U.K. participating in EU elections following the country’s decision to withdraw from the EU. As a result, we would not be surprised if more Brexiteers end up supporting PM May’s deal.

Venezuela’s “big stake”? The Trump administration hinted at possible retaliation against President Nicolas Maduro following the arrest of Robert Marrero, the Chief of Staff of opposition leader Juan Guaido. This move by Maduro will likely escalate tensions between the U.S .and Venezuela as Maduro grapples with staying in power in light of crippling U.S. sanctions. Tensions have been running high between the two countries following the U.S. decision to recognize Juan Guaido as the legitimate leader of Venezuela. Following this decision, the U.S. has maintained that there will be severe consequences for the Maduro regime if Guaido or anyone in his inner circle is harmed. At this point, the administration has been ambiguous about what its response will be, but has vowed that Maduro’s actions “will not go unanswered.”

Flood season: The National Oceanic and Atmospheric Association stated in its Spring Outlook report that the U.S. is likely to see “historic and widespread flooding” in May. If this occurs, it will be bad news for farmers who have been stockpiling crops in anticipation of a possible trade deal with China and are still recovering from the bomb-cyclone that hit two weeks ago. Federal regulations prevent the selling of crops that have been tainted by flood waters, which will likely result in farmers absorbing losses of some of their excess inventories. As a result, we expect the price of crops to be relatively high over the summer as poor weather conditions will have a negative impact on supply.

North Korea:Following months of progress, it appears that denuclearization talks between the U.S. and North Korea may be on the brink of breaking down. Last week, it was reported that North Korea was considering walking away from negotiations following the summit in Hanoi that saw both sides leave without an agreement. Speculation was further stoked today after North Korea decided to withdraw from a shared liaison office with South Korea following the U.S. decision to sanction two Chinese shipping companies. The sticking point in negotiations appears to be North Korea’s insistence that sanctions be removed before it decides to completely denuclearize, while the U.S. maintains that sanctions will only be removed once there is proof the country has completely denuclearized. Furthermore, there are reports that North Korea has been able to avoid sanctions with the help of China. At this point, it is unclear what the next steps are but we will be closely monitoring the situation.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.