Part I of this report was a review of the reserve currency and the savings identity. In Part II, we showed how the Nixon and Reagan administrations used America’s hegemonic power to force some of the economic adjustment of U.S. policy onto foreign governments. This week, in the final segment of this report, we will look at the actions of the Trump administration, using the comparisons to the Nixon and Reagan administrations. We will conclude the report with market ramifications.

[Posted: 9:30 AM EDT] Happy Monday as we clear out the “tequila cobwebs” this morning! Cyclone Fani made landfall over the weekend.[1] Ramadan begins.[2] Trade turmoil returns. It’s a massive risk-off day so far. Here is what we are watching:

Trade turmoil: On Sunday afternoon, President Trump tweeted that, due to the slow progress of trade talks and reports that China was backtracking on some earlier agreements, he would increase the scale and scope of tariffs by Friday.[3] There has been a steady drumbeat of reports that President Trump was pressing his trade negotiators to make a deal;[4] it appears that his mood has changed. It is unclear what triggered the change. We have doubted that USTR Lighthizer would agree to a modest agreement, although Treasury Secretary Mnuchin has been seen as pushing for a less comprehensive deal. Perhaps the recent upturn in the economy emboldened the president or China may have crossed some sort of red line. At the same time, economic conditions in China have improved, which may have led Chinese negotiators to push back on some issues that appeared previously resolved. And, it’s quite possible the Chinese, again, misread President Trump and believed his desire for a deal would allow them to press for a more favorable agreement. China did announce cuts on reserve requirements for small business loans.[5] At the same time, in what might signal concern in the Xi government, China has lowered the daily limit on foreign currency withdrawals.[6] If there is a trade war, one would expect Chinese households to accumulate dollars on fears of CNY depreciation. The move by the PBOC to limit withdrawals could be in anticipation of rising concerns.

China has indicated it may cancel this week’s scheduled meetings in Washington, which were expected to start on Wednesday. It has backed away[7] from fully cancelling the meeting but may not send Vice Chair Liu[8] or could delay his arrival, which would almost certainly mean Trump’s tariffs will go into effect.

Financial markets reacted as one would expect. Equities around the world plunged.[9] The yen and dollar rallied and Treasury yields dipped. Most importantly, the CNY nosedived; it is possible that Beijing prevented the CNY from depreciating during trade negotiations. But, it should be noted that the textbook response to tariffs is depreciation. Gold lifted, but industrial metals fell. Another key market move occurred in grains. Even though the Midwest continues to deal with unrelenting rain, which is slowing planting progress and potentially constraining supply, grain prices fell hard on the prospects of a trade disruption.

Financial markets have mostly expected a deal to be made and for disruption to be avoided. The president’s policy reversal is important; we will be watching to see if there has been a significant rupture in relations or if the president is simply posturing. In other words, what we don’t know the answer to is if this is a bargaining tactic or an ultimatum. If it’s the former, financial markets will reverse today’s losses. If it’s the latter, a more serious pullback is in the offing. At this point, we don’t have much confidence in either outcome. It is possible President Trump is overly confident in the ability of the U.S. economy to overcome tariffs on China; the same overconfidence may be occurring in Beijing, too. Therefore, a mistake could be made. It is also possible that the president believes being tough on China will play well with his voters and that a trade war is a plus so long as recession is avoided. What we are concerned about, as noted above, is that financial markets have generally moved on from worrying about this issue and thus will need to recalibrate.

There have been a number of questions into our office about the impact of tariffs. In general, the best answer is “it depends.” At one extreme, the Chinese exporter cuts his price by the amount of the tariff and absorbs the tax (this is where currency depreciation helps); at the other, the tax simply passes through to the consumer.[10] So far, most studies have suggested that the incidence from metals tariffs have been borne by U.S. consumers. But, that might not be the case if tariffs broaden.

Iran: The U.S. is considering sanctions on other Iranian industries, although they have not been officially specified yet.[11] John Bolton, the National Security director, issued a press release indicating the U.S. was sending the CVN Abraham Lincoln to the Middle East.[12] He tied the move to increased tensions with Iran.[13] We do note that the carrier group has been in the area for a while (it’s currently in the Red Sea), so the announcement does appear to be stating what was already in place. In some respects, this carrier group in the region isn’t a big deal. The U.S. often has a carrier group in the Fifth Fleet’s area of operations; recently, it has had a lower presence in the region. If the U.S. was preparing for a conflict, it would have a minimum of two carrier strike groups and would prefer three, which would support 24-hour sorties. Meanwhile, the EU is continuing to support the Iran nuclear deal,[14] although business dealings with Iran have declined precipitously. Even with this news, we are seeing lower oil prices today. Oil has been trading as a risk asset, so lower equities are weighing on oil prices.

Gold: Although you wouldn’t necessarily notice it in terms of price, central banks have been increasing their gold reserves. Last quarter, central banks boosted their holdings by 145.5 tons over the same quarter a year ago.[15] Russia led the buying, likely in a bid to circumvent sanctions.

North Korea: As relations deteriorate, Pyongyang is returning to its old patterns of provocative actions. On Saturday, the regime launched a number of “projectiles” offshore. It is believed these were short-range missiles.[16] So far, the Trump administration has acted with restraint to these events, likely because they don’t include ICBM tests, which would directly threaten the lower 48.[17] We doubt Kim’s missile tests are sitting well with the hawks in the administration, namely Pompeo and Bolton. But, as long as Kim doesn’t test a missile that could hit the U.S., he will likely avoid a significant breakdown with Washington. To a great extent, Kim wants attention[18] and these short-range tests give him that without significant cost.

The Fed: With Herman Cain and Stephen Moore out of the picture, the administration returns to looking for two more candidates. Two names have emerged, Paul Winfree[19] and Judy Shelton.[20] Winfree’s economic work appears to be in fiscal policy, while Shelton seems to be a gold supporter. Winfree did complete an MA in economics; Shelton has a Ph.D. in management. What we find interesting is that Trump seems to really want a policy dove, but what he keeps getting are hard money types who promise to do the president’s bidding. But, once seated, will they keep their promise or will their hard money instincts kick in, especially since it’s hard to remove a sitting Fed governor?

Meanwhile, the Fed continues to examine the low inflation issue, building a case for keeping policy easy for longer. Chicago FRB President Evans,[21] St. Louis FRB President Bullard[22] and NY FRB President Williams[23] all indicated that rate cuts may be needed if inflation remains low.

Infrastructure? Forget it! The Congressional GOP has no interest.[24]

Elections: South Africa goes to the polls this week. Corruption appears to be the biggest issue.[25] Although the ANC is expected to maintain control, the margin of victory is likely to be less than the last election. Meanwhile, in North Macedonia, the incumbent party maintained power.[26]

Brexit: Although it’s still a long shot, there does appear to be some progress in building a cross-party coalition for a customs union with the EU.[27] However, while the leadership is close to an agreement, the backbenchers on both parties will likely howl and still scotch an agreement. And, it should be noted that the next PM could pull the U.K. out of the customs union anyway. Thus, we may see a bounce in British assets if an agreement is struck on a customs union, but it may not have legs.

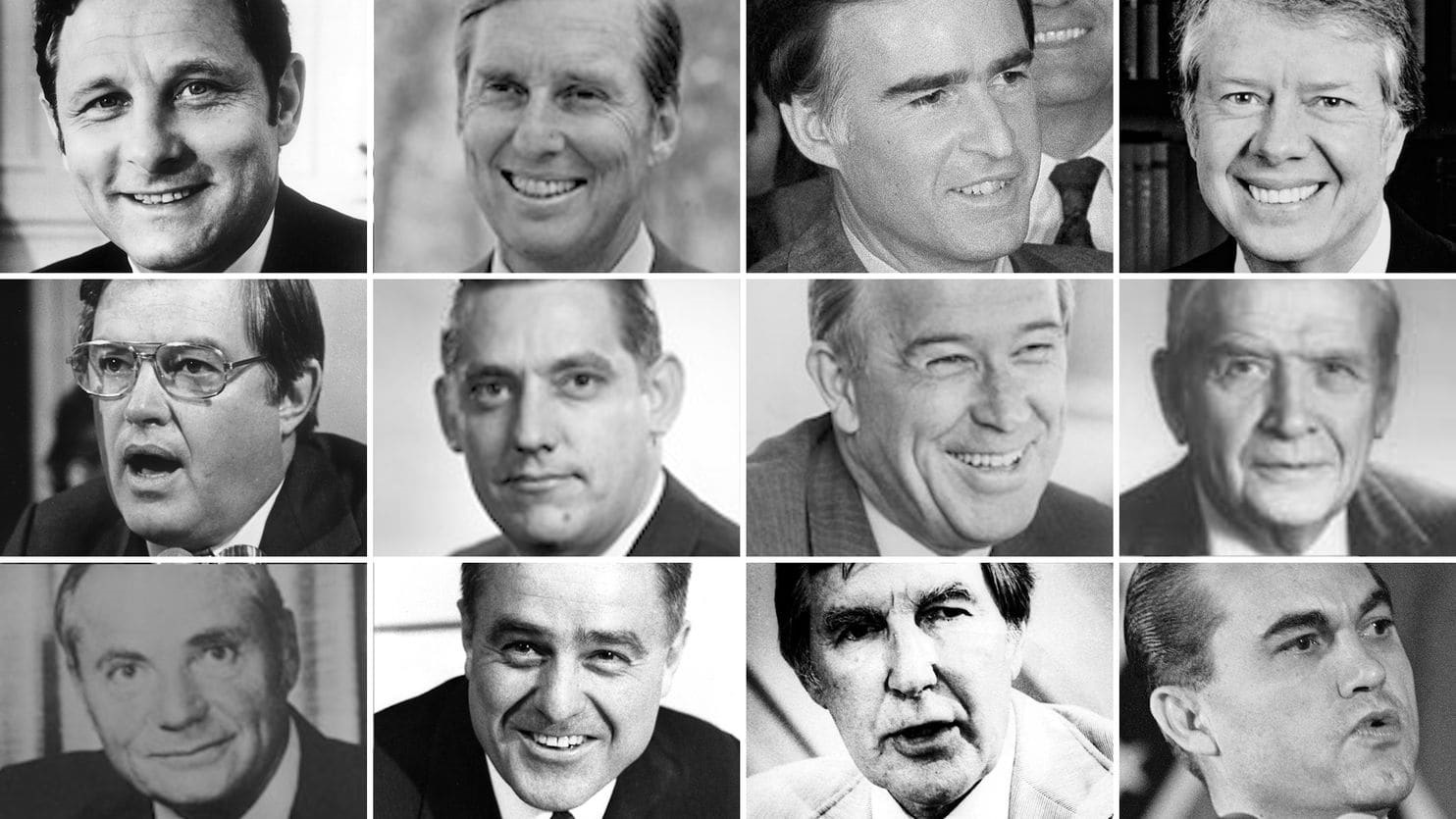

The 2020 elections: We are starting to get questions about the 2020 elections, especially given the large number of candidates vying for the Democratic Party nomination. We are not handicapping anything currently. And, to profile why we aren’t, try this quiz.

These were the 12 candidates running for the Democratic nomination in 1976; until this year, that was the highest number of Democratic Party candidates running for president. How many can you name?[28] Check the footnote to see how you did.

The point of this test is that a crowded field signals a high level of political turmoil, so much so that a plethora of candidates are willing to take the plunge (the winner was Jimmy Carter, top right). As the 2016 GOP primary showed, as did the 1976 primary, it’s anybody’s guess who will win. We are watching what is going on but, at this point, picking the Democrat from a field of 22 is an exercise in being wrong. After all, few pundits thought Trump would win in 2016 and Jimmy Carter wasn’t considered a strong candidate in 1976 either. Simply put, it’s too early to handicap the outcome and it probably isn’t affecting markets yet anyway.

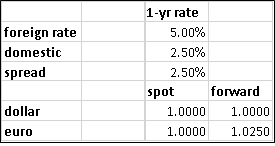

Covered interest rate parity is a basic concept that, at its heart, says all interest rates are equal after hedging exchange rate risk. It is one of the theories in finance that is beyond dispute—it works as long as capital markets are open (free of capital controls) and short-term money markets are liquid. In general, if foreign interest rates are higher than domestic rates, the forward exchange rate will trade at a premium high enough to absorb the interest rate difference. Here is a simple example:

In our example, one-year interest rates in the Eurozone are 5.00% compared to U.S. rates at 2.50%. If the forward rates were equal, a U.S. investor could exchange dollars for euros, invest at the 2.50% spread and hedge the currency risk, earning a risk-free extra 2.50% compared to dollar-based interest rates. However, in the process of doing so, the forward rate on euros would be bid up to 1.0250, which eliminates any arbitrage opportunities. A U.S investor should be indifferent to either investing in the U.S. at 2.5% or in the Eurozone at 5%, at 1.025 $/€ one-year forward exchange rate. In a year, if nothing changes, that euro purchased at 1.025 will be at 1.00, eliminating the entire interest rate spread.

However, this doesn’t necessarily mean that hedging opportunities don’t exist. An investor could decide to buy into longer duration fixed income abroad and roll the hedge periodically. Using the above example, an investor could buy a foreign bond and hedge each year, selling the bond if the hedging costs become excessive.

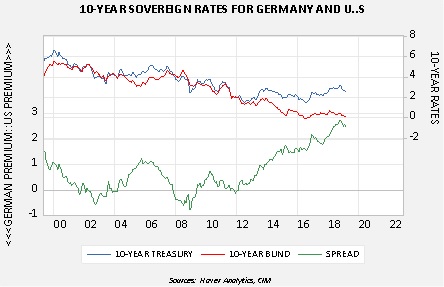

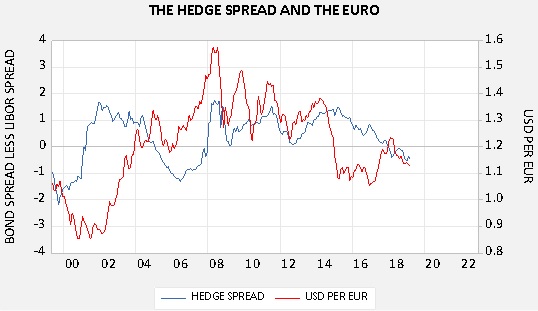

The current spread between U.S. and German 10-year sovereigns clearly favors the U.S. German yields are around zero and U.S. yields remain significantly higher even though U.S. yields have declined. Thus, it would seem that German investors would have an incentive to buy longer dated Treasuries.

However, for a German investor to make this investment, he would have to either accept the currency risk or attempt to hedge the risk. As shown above, the short-term rate spread determines the currency forward discount/premium relationship.

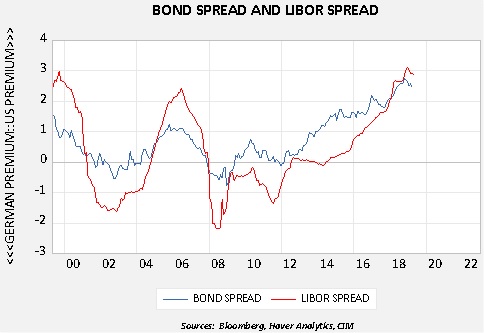

This chart shows the 10-year sovereign spread and the three-month LIBOR spread. When the bond spread exceeds the LIBOR spread, the bond spread exceeds the cost of hedging. Even with a very wide sovereign spread, a foreign investor cannot, under current conditions, profitably hedge the currency risk.

This has led foreign bond investors to (a) accept U.S. credit risk by purchasing corporate bonds and hedging the exchange rate risk, or (b) accept the currency risk by leaving the transaction unhedged. However, that situation is less than ideal and may discourage foreign investors from investing in U.S. fixed income markets.

Although the hedge relationship with regard to the euro isn’t overly strong, there is a modest tendency for the currency to strengthen against the dollar when the hedge spread is negative. Clearly, there are other factors that affect exchange rates beyond mere interest rate differences. Although the euro has been weakening recently, it hasn’t declined significantly despite unusually wide sovereign spreads; the likely culprit is the cost of hedging. If the U.S. yield curve were to steepen, perhaps with policy easing, the window for hedging might reopen and, paradoxically, could lead to a stronger dollar.

[Posted: 9:30 AM EDT] It’s employment Friday! We cover the data in detail below, but the quick take is that it was a blowout report. Payrolls were well above forecast and the unemployment rate fell to its lowest level since December 1969. Here is what we are watching:

Moore out: Stephen Moore is no longer in the running for a Fed governor seat. The official line is that he withdrew.[1] Moore has made a number of controversial statements that ended up dooming his chances.[2] To some extent, the president is pressing the boundaries of who he can nominate for these positions. What lesson may have been learned? Try to meet your goal with candidates that are less divisive. We still think Larry Kudlow will be the next to be “run up the flagpole.” His views are similar to Moore’s but Larry has the reputation of being a genuinely nice guy.[3] The president could also appoint a committed dove to the FOMC, such as Minneapolis FRB President Kashkari or St. Louis FRB President Bullard, and get the same policy outcome without the controversy. If the president continues to seek out difficult candidates, it suggests he sees some value in the battle and is less concerned about getting doves for the last two open spots.

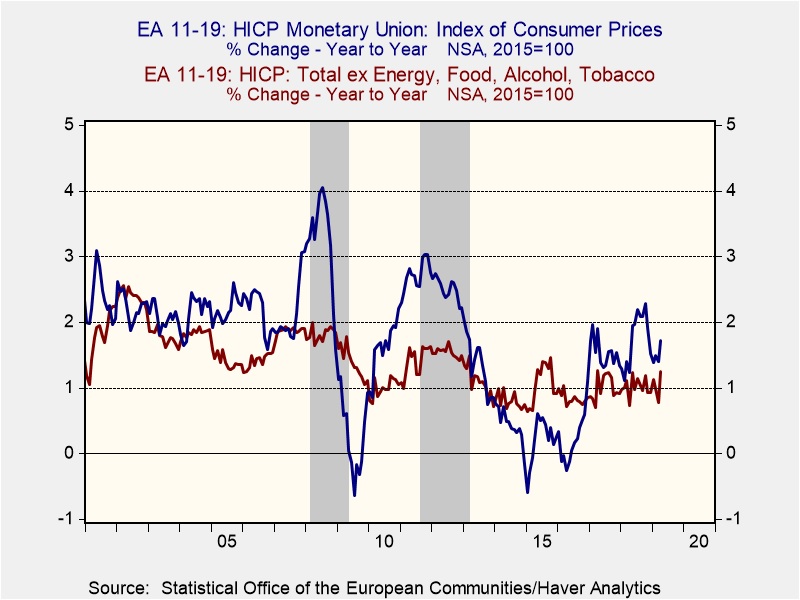

European inflation: Eurozone inflation rose more than forecast, up 1.7%, which was good news, although the data may have been distorted by the late Easter holiday. Core CPI also rose.[4]

Low inflation has weakened the ECB’s ability to stimulate the economy through rate cuts, so the central bank will welcome this rise.

U.K. local elections: As expected, the Tories took a beating in local council elections.[5] Interestingly enough, so did Labour. The Liberal-Democrats, a center-left party, had the best showing. These elections have the tenor of a protest vote, which probably means they don’t really tell us much about the path of national politics.

Politics and money: A couple of articles caught our attention. First, Silicon Valley is finding the flow of cash impeded a bit by the Treasury department, which is vetting inflows from China and Saudi Arabia.[6] Second, the Chamber of Commerce, a bastion of the GOP establishment, is finding itself on the outs with the White House.[7] As the GOP becomes more populist, establishment bodies, like the Chamber and the Koch brothers’ Americans for Prosperity, have seen their influence wane.

A German at the ECB? Jens Weidmann has been a controversial candidate for the ECB. His nationality is an issue; the rest of Europe, but especially the southern nations, are worried that a German at the helm will turn the ECB into the Bundesbank. In addition, Weidmann has been a critic of the extraordinary measures adopted by Draghi. Over the past couple of years his star has risen and fallen, but it appears the Merkel government is pushing for Weidmann to get the nod. Today, European Commission President Juncker, who is near the end of his term, has signaled he would support Weidmann.[8] We would expect a more hawkish bank if Weidmann does become ECB president, which would be bullish for the EUR.

Japan and consumption taxes:Japan used an investment-led development model after WWII. The model generated domestic saving by suppressing household consumption. Part of that effort was national consumption taxes. This method of taxation was appropriate for Japan’s development period, but that ended in 1990 and the inability to adapt to the post-development era has led to over three decades of economic stagnation. The Abe government has been proposing to increase the consumption tax to 10% from 8% to address a huge fiscal deficit. However, it has delayed the move twice due to economic conditions, once in 2014 and again in 2016. Policymakers are indicating they will raise rates this year.[9] In the past, such increases have undermined Japan’s growth; we would expect a negative reaction again if the country makes good on an increase this year.

[3] A couple of observations. First, (Bill speaking here) I have been interviewed by Larry Kudlow on CNBC. Although I don’t necessarily share his views on the economy, he was a fair questioner and allowed my viewpoints to be expressed. Second, he usually goes on Bloomberg with Jonathan Ferro after the labor or GDP data are released. While they do spar, it is done with respect and Kudlow goes to great lengths to make his point but in a fair manner.

[Posted: 9:30 AM EDT] Some markets, notably China and Japan, remain closed for May Day. Here is what we are watching:

The Fed: As expected, the FOMC left rates unchanged. The statement acknowledged the pickup in economic growth but tempered that positive comment by indicating that household spending and business investment had weakened. It also noted low inflation. The Fed did act to lower the IOER rate from 2.40% to 2.35%, as expected, leaving the policy range unchanged at 2.25% to 2.50%.[1] The fed funds rate had moved above 2.45% so the IOER rate was lowered. Initially, the lowering of the IOER rate was taken as dovish. However, Chair Powell specified that this action wasn’t a policy move and described it as “technical,” and financial markets reversed the dovish take. Essentially, not much happened but the financial markets misread the IOER cut as a precursor for easing; Chair Powell put that idea to rest and the dovish position reversed. A second factor weighed on sentiment when the chair characterized recent low inflation as “transitory.” Low inflation was mentioned and has been discussed among some members of the FOMC as a potential problem that may require easing. Powell’s characterization of low inflation as transitory seemed to contradict those concerns.

Powell indicated that the Fed is on hold. He said the Fed could just as easily ease as tighten, which is a very good definition of neutral policy. Financial markets continue to signal that the next move should be a rate cut.

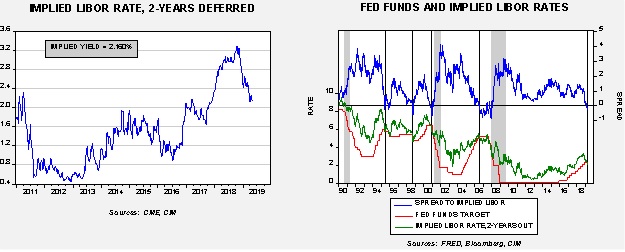

The chart on the left shows the implied three-month LIBOR rate from the Eurodollar futures for the contract two years in the future. Note that the rate has declined from over 3.30% last October to 2.16% now, a significant decline. The chart on the right compares this implied rate to the fed funds target. We have placed vertical lines when the two rates invert. When these two rates invert, it signals that the Fed needs to start easing to avoid a recession. With the rate inversion in February, which has persisted, these charts would argue for an “insurance” rate cut as recently discussed by Vice Chair Clarida. Thus, Powell’s description that policy is at neutral, meaning the FOMC could move rates in either direction, doesn’t fit the financial market’s position. Without a rate rise in the short end of the yield curve, the most likely next move is for lower rates, unless the Fed is determined to trigger a recession.

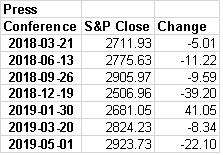

By the way, for those of you keeping score at home, here is the S&P on the dates of Chair Powell’s press conferences.

In seven meetings with press conferences, six had negative closes. We think the Fed’s policy transparency is a terrible mistake; policy functioned much better when little was said.

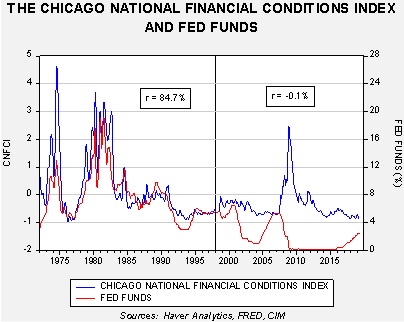

This chart shows the Chicago FRB National Financial Conditions Index, which is a reading of financial stress, and fed funds. From 1973 to mid-1998, the two series were highly correlated. Since then, they are virtually uncorrelated. The Fed began to slowly increase the level of transparency beginning in the mid-1990s. By mid-1998, we were getting statements and regular comments from FOMC members. During the period of relative opaqueness, financial stress was a force multiplier for the Fed, so raising or lowering rates had a dramatic impact on financial market behavior. Thus, tightening tended to reduce borrowing and raise the cost of risk, and lowering rates had the opposite effect. By increasing transparency, allowing market participants to accurately assess the direction of policy, the Fed’s ability to affect financial conditions has essentially been lost. So, when the Fed tightens it does little to inhibit risk activity, and easing does little to encourage risk-taking.

Powell’s decision to increase the number of press conferences is a good example of this problem. As the above table shows, the chair seems to have a remarkable ability to bring lower equity values. Now, if this is his goal, he should be commended. But, we doubt that is the case; instead, we suspect he is trying to sound “reasonable,” which gives a muddled picture and leads to selloffs. If the FOMC position on low inflation is transitory, then why have a meeting in June to discuss changing inflation targeting? On Friday, NY FRB President Williams and Vice Chair Clarida will give speeches. We will be watching to see if these two essentially walk back Powell’s comments. If they do, it would suggest the chair misspoke.

U.K. elections and other things: The U.K. is holding local elections today. The Tories are expected to take a drubbing, although the U.K. Independence Party isn’t competing which may limit the damage.[2] Turmoil continues within May’s government; she sacked her defense minister overnight, blaming him for the leak around Huawei (CNY 4.02, +0.17).[3] It appears PM May is leaning toward a customs union with the EU, the position supported by Labour, as a way of avoiding a hard Brexit. If she can gather enough supporters in the opposition, she might be able to close a deal soon.[4] However, there is a wild card in this idea. There is a sizeable number of hard Brexit supporters within Labour that may put Corbyn’s leadership at risk if he supports such an arrangement. The downside of a customs union is that it would prevent the U.K. from making its own free trade agreements, at least on goods trade, with other nations. The Bank of England (BoE), as expected, left policy unchanged. However, its comments struck a decidedly hawkish position, indicating that rate hikes will be needed in the future to offset stronger economic growth. Although the tone was hawkish, it is clear the BoE is in no hurry to tighten policy.[5]

Venezuela: It still isn’t exactly clear what happened this week. It does appear that Guaido thought he had splintered the security forces enough to unseat Maduro. It also seems that administration officials thought so, too.[6] Clearly, that plan didn’t work out. But, if the action failed (we would not call it a coup because there is a case to be made that Guaido is the legitimate leader of Venezuela), then why didn’t Maduro arrest Guaido? It is possible Maduro has concluded that he doesn’t have the power or the skill to return Venezuela to prior prosperity. Therefore, he wants to leave but the Russians[7] and Cubans have “convinced” him to stay.[8] There are reports of negotiations between the opposition and the regime.[9] Meanwhile, Guaido is trying to maintain momentum after what appears to be a significant disappointment.[10] Protests continue with no end in sight.[11] If Maduro were to exit, we would likely see a correction in oil prices. For now, Maduro is hanging on but we wonder whether he actually wants to stay. One possible outcome—Russia, Cuba and China could remove Maduro and replace him with another member of the regime, perhaps a military figure, that would protect their position in the country and defuse the protests and the opposition. Such an outcome would put the U.S. in a difficult position—would the administration support the new government or take steps to oust it? Although there are elements in the administration and GOP who would support a military intervention, we think President Trump would be very reluctant to commit troops to Venezuela.

Chinese pork imports and ASF: As African Swine Fever (ASF) decimates the Chinese pork industry, Beijing has taken two actions that perhaps offset each other. Due to continued tensions between Ottawa and Beijing over the arrest of Meng Wanzhou of Huawei, China has been taking steps to punish Canada, including arresting Canadian nationals in China. Today, China announced it was suspending pork imports from two Canadian pork producers,[12] likely another step in its attempts to pressure Canada to release Meng. However, this action by China risks driving up pork prices further, so why target this industry? Perhaps because China has found alternative sources for pork in Argentina.[13]

Capital flight: One position we have held for some time is that if the U.S. does back away from its hegemonic role, world stability would suffer and the wealthy worldwide would be looking for an “escape portal” to protect their wealth and person. We have contended that the U.S. would be a prime destination for this capital flight. The U.S. has deep financial markets and a stable legal system, making it a good place to land if one’s homeland turns hostile. Recent data suggest an increase in “wealth migration” last year, with the U.S. seeing some of that flow.[14]

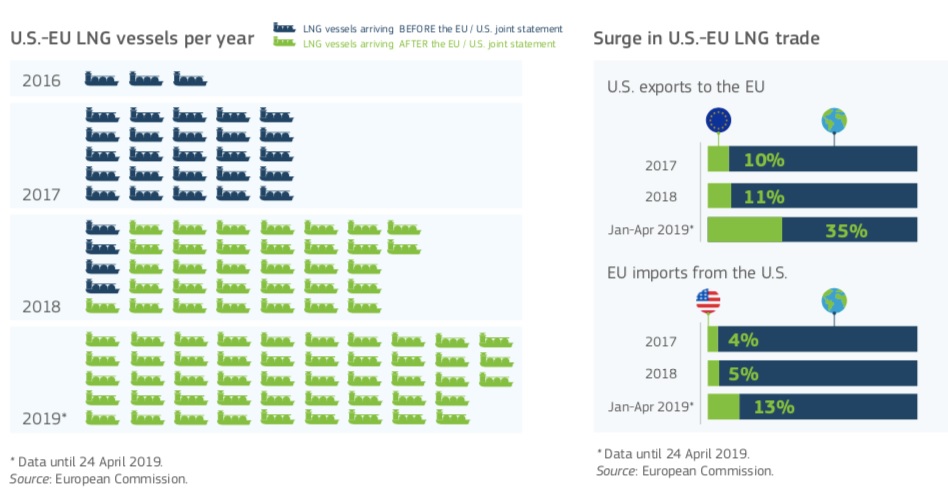

Europe and LNG: U.S. LNG exports to Europe are surging, up 272% over the past year.[15] The exports began to rise in the wake of meetings between President Trump and President Juncker last summer. The chart below shows how shipments have jumped after the meeting. It appears the EU may be using LNG as a potential bargaining chip in upcoming trade talks.[16]

U.S. natural gas prices have been depressed due to the high associated gas production tied to surging U.S. oil output. But, expanding LNG exports could reduce this supply overhang and eventually lift prices.

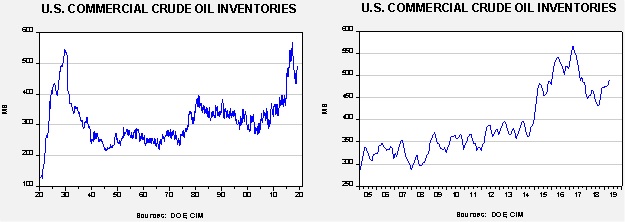

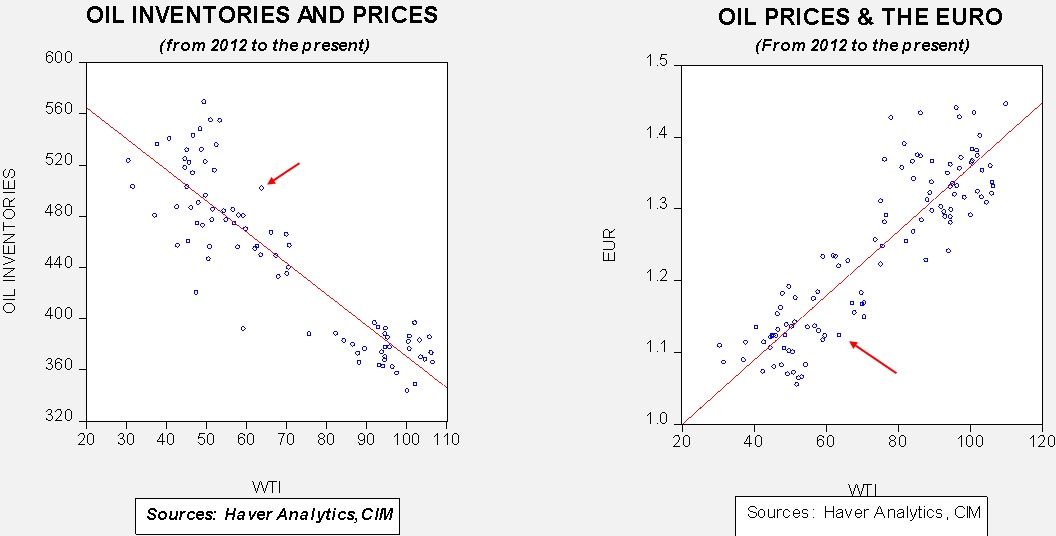

Energy update: Crude oil inventories rose 9.9 mb last week compared to the forecast rise of 1.8 mb.

In the details, refining activity expectedly fell 0.9% compared to the 0.5% increase forecast. Estimated U.S. production rose slightly by 0.1 mbpd to 12.3 mbpd, a new record. Crude oil imports rose 0.2 mbpd, while exports fell 0.1 mbpd.

(Sources: DOE, CIM)

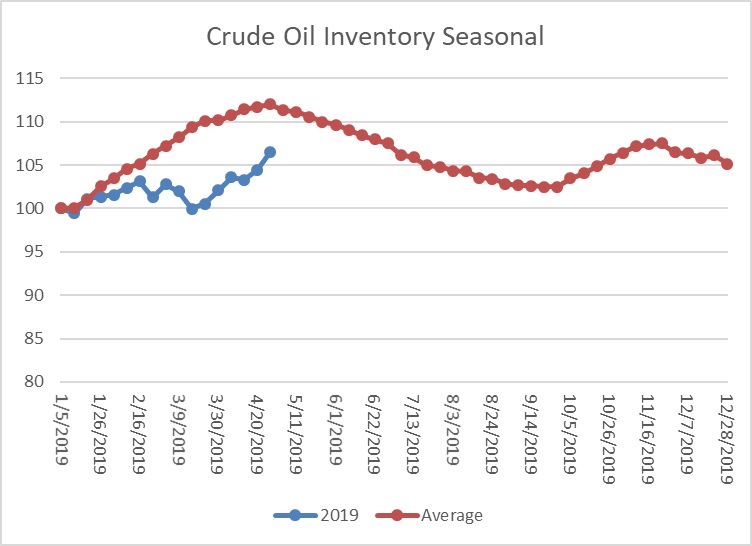

This is the seasonal pattern chart for commercial crude oil inventories. We are entering the spring/summer withdrawal season next week, so if inventories continue their rise it will become a significant bearish factor for prices. The recent upswing in inventories is remarkable; stockpiles have increased 30 mb over the past six weeks. Although we did not achieve seasonal parity with regard to inventories, the gap clearly narrowed.

Based on oil inventories alone, fair value for crude oil is $50.83. Based on the EUR, fair value is $51.96. Using both independent variables, a more complete way of looking at the data, fair value is $50.55. This is one of those circumstances when the combined model fair value does not lie between the two single-variable models. Current prices are running well above fair value. Geopolitical risks, including the turmoil in Libya, continued problems in Iraq, unrest in Venezuela and the end of Iranian oil export waivers, are all lifting prices. However, our data does suggest that the markets are getting a bit rich so any evidence that these situations are improving will likely lead to at least a period of consolidation, if not a pullback, in prices.

[Posted: 9:30 AM EDT] Happy May Day, the international Labor Day! It’s also Fed day. Here is what we are watching:

The Fed: The president continues to press the FOMC to cut rates.[1] So far, his demands have not had much effect, although we can make a cogent case that the financial markets are clearly signaling that a rate cut would be justified. It appears support for Stephen Moore is deteriorating in the Senate.[2] Although Moore is well-connected in the GOP, he has apparently made some enemies along the way and his comments about women are turning out to be rather damning to his support. Moore may fail to get nominated, but we still expect Trump to put doves in the two remaining governor positions. We still would not be surprised to see Larry Kudlow get the nod.

As far as today’s meeting goes, there is little chance of a rate move but we might see some technical adjustments to free up reserves in the banking system. We expect Powell to deal with questions about falling inflation in the press conference, but he should be able to deflect these to the early June meeting when policymakers are going to discuss changing the inflation target.

The mess in Venezuela: Yesterday, Juan Guaido called on the military to revolt against the Maduro regime.[3] It had the look of a staged event;[4] in other words, Guaido seemed to have gotten some assurances that there was support for an overthrow,[5] otherwise his actions bordered on treason. There are lots of reports in the media, which are difficult to substantiate, saying that a coup was indeed in place but Guaido may have moved prematurely.[6] In any case, as the dust clears, Maduro is still in office and Guaido’s position appears even shakier. Maduro supporters have violently pushed back against the opposition.[7] Although Guaido continues to call for protests, it looks like the bulk of the military are remaining loyal to the regime.[8] The situation remains fluid but Maduro seems to have more staying power than Washington expected. As long as turmoil continues, it will be a supportive factor for oil prices.

China trade deal:There are reports that the U.S. has watered down its demands for preventing Chinese cybertheft in order to get a deal finished.[9] We continue to closely watch USTR Lighthizer. His longstanding goal was to address China’s trade practices but we would expect him to resign if he is forced to negotiate a deal that he opposes. If he does, it might reduce the otherwise positive impact that an agreement would bring.

[Posted: 9:30 AM EDT] As we bid goodbye to April, there’s a new emperor in Japan and the IS leader re-emerges. China’s PMI data (see below) came in a bit light.[1] On the other hand, Europe’s GDP came in better than expected.[2] Here is what we are watching:

Spanish elections, some thoughts: The center-left has struggled in Europe recently, so the improved fortunes in Spain have raised some hopes of a recovery. Here is what we noticed. First, a key factor in the Socialists’ resurgence was a fracture on the right. The center-right lost votes to Vox, the hard-right anti-immigrant party.[3] Centrist parties have struggled with the rise of populism in recent years; for example, in Germany, the AfD has made strides against the CDU and has been pulling the CDU in a rightward direction. The Popular Party in Spain tried to hold on by moving to the right but the gambit failed. The Socialists were better able to maintain solidarity, mostly by suggesting that not voting for the center-left was implicit support for Vox.[4] The problem is that this outcome was probably unique to Spain and may have been an accident of timing and may not be repeatable. In other words, there doesn’t appear to be anything magical about what Sanchez did to win; he may have simply gotten lucky. Second, Sanchez did offer a more leftist platform, calling for a reversal of austerity and a higher minimum wage. So, in essence, his win was due to the right fracturing and a shift to more populist positions. Without the first, the second probably wouldn’t have mattered.

The return of Baghdadi: The leader of Islamic State (which, in reality, no longer exists) was seen in a video released by the group yesterday. This is the first time in five years that he has been seen in this format. Although there have been rumors of his demise, he appears to be on this side of the earthly pale.[5] IS has lost its caliphate, but it is rapidly becoming a global terrorist organization, similar to al Qaeda.[6] This will require different tactics compared to attacking a specific land target; look for the same strategies that were used against al Qaeda to be applied here, such as tracking money flows and counterterrorist activities.

Infrastructure? Senate Minority Leader Schumer and Speaker Pelosi are scheduled to meet with President Trump to discuss infrastructure.[7] Although infrastructure spending is attractive in the abstract, we haven’t seen much action on this issue because the two parties are divided on their methods of achieving public investment. Initially, the administration wanted public/private partnerships to fund infrastructure spending. Unfortunately, opportunities for large projects with such mechanisms are limited because a steady stream of revenue must be generated in order for them to work. Much of public investment does not generate direct cash flows. President Trump is said to favor direct public investment as do Pelosi and Schumer.[8] However, the latter want to force the president to raise taxes to fund the project, which is a non-starter as 2020 looms. In addition, Trump’s position is at odds with GOP legislators, who want to spend less, not more, especially with the debt ceiling looming in the fall.[9] So, we expect a lot of media coverage but see little chance of progress.

Oil bounce: Oil prices are lifting today on reports that Saudi Arabia wants to extend production cuts into year-end.[10] Meanwhile, Iran has indicated it will ignore U.S. sanctions and continue to export oil by evading such measures.[11]

A peace accord between Kosovo and Serbia: Two decades after a conflict that led to the separation of Kosovo from Serbia, the two sides are nearing an accord in which the latter will formally recognize the existence of the former.[12] If a deal can be reached, it would create conditions where Serbia could potentially join the EU. It would also mean Serbia no longer blocks Kosovo from joining the UN. Still, a deal isn’t certain. To make it work, there may need to be a swap of land, which is fraught with risk.[13] And, Russia would not be keen on Serbia joining the EU and perhaps being pulled from its orbit.

Equities and flows: Although equity markets continue to grind higher, flows from investors continue to move in the opposite direction. Lipper reports that both equity ETFs and mutual funds reported outflows last week, while fixed income enjoyed new flows.[14]

Reflections on serial defaulters:There are some nations that engage in sovereign defaults on a seemingly regular basis. Argentina is the most notable but isn’t alone. Early in my career,[15] I worked as a country risk analyst and had a front row seat to the latter stages of the Latin American debt workout. I was part of a massive debt/equity swap program that saw my commercial bank shed hundreds of millions of non-performing sovereign loans. As the process wound down, I remember thinking that these defaulters would be denied access to the credit markets for decades. Yet, in less than five years, most of them were borrowing again. Although I had chalked up that development to P.T. Barnum’s observation that “a sucker is born every minute,” it turns out there is good reason to invest in the “borrow, default, return” cycle. A recent paper by Josefin Meyer, Carmen Reinhart and Christoph Trebesch supports the idea that it is profitable to lend to serial defaulters.[16] However, as one would expect, such lending carries much higher risk.[17] The trick is to get a return commensurate with the risk, which usually means putting money in the country when it is in its most dire state.

Two weeks ago, we introduced this report with a review of the basics of the reserve currency and the savings identity. This week, we will examine two important historical analogs, the Nixon and Reagan administrations.

#1: The Nixon Analog

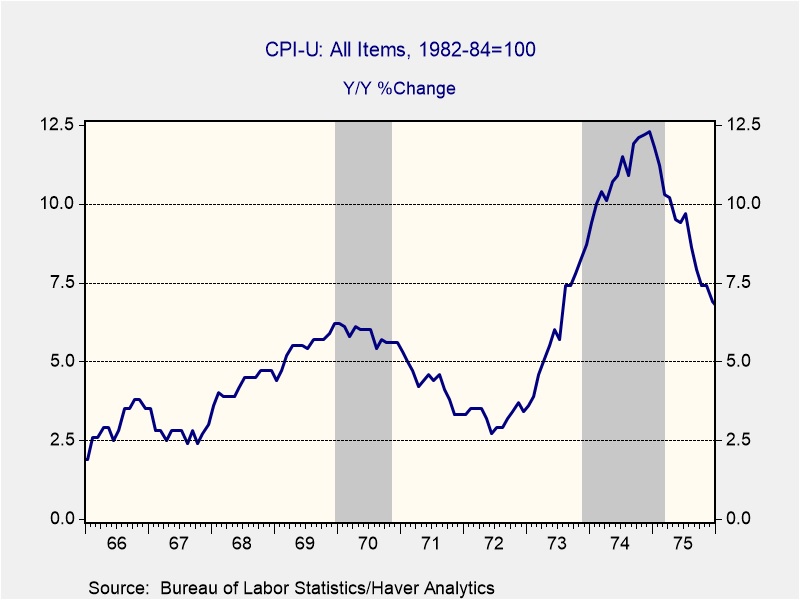

As President Nixon prepared for the 1972 presidential campaign, he faced a number of serious problems. First, inflation was increasing.

In 1967, inflation was 2.5%; by mid-1969, it was more than 5.0%. The Federal Reserve acted to quell inflation by raising the fed funds rate to nearly 9.2% by August 1969.

As the chart below shows, the increase in interest rates led to a recession, ending the long economic expansion that began in March 1961. The recession, which ran from December 1969 to November 1970, was not an especially harsh one, but Nixon knew that if he didn’t boost the economy in 1971 his reelection chances would be significantly diminished.

[Posted: 9:30 AM EDT] Happy Monday! It was a cold weekend in the Midwest, with a late April snow for the upper parts of the nation’s midsection. It’s going to be a busy week, with the FOMC meeting and Japan’s Emperor Akihito taking the rare step of abdication tomorrow.[1] Here is what we are watching:

Spanish elections: Pedro Sanchez’s Socialist Party had a good election, a rarity for center-left parties in the West. Although the Socialists will still need to build a coalition government, the party did take 123 of the 350 seats in the Spanish Parliament; that was up from 85 seats in the last government. The center-right opposition Popular Party took 66 seats. The centrist Ciudadanos won 57 seats, and the hard-left Podemos won 42 seats.[2] Vox, the right-wing populist party, took a surprising 24 seats, the best performance for a hard-right party in Spain since 1982.[3] It will still take weeks for Sanchez to form a government, but there isn’t another alternative to a return of his government. The election is supportive for the Eurozone and the EU as it shows that a centrist party can still win elections in the region.

Fed: The FOMC meets this week. There will be talk of an “insurance cut,” a rate reduction to “ensure” the expansion continues. This won’t happen on Wednesday but expect the chair to be noncommittal on this issue in the press conference. There are no dots or new forecasts at this meeting but, consistent with the Fed’s new policy, there will be a press conference. The key issue for the FOMC is falling inflation.[4] Chicago FRB President Evans suggested that inflation around 1.5% could trigger a rate cut.[5] Although the insurance cut and rate reductions due to inflation will likely dominate the discussion, we would not expect a move this week. In fact, with the early June summit on the inflation mandate, we probably won’t see a rate move before that meeting unless the economic data turns decidedly bad or a financial accident occurs.

China trade talks: Talks resume this week in Beijing as negotiators near an agreement.[6] Still, there are difficult issues that remain to be worked out,[7] with enforcement of the agreement one of the areas that remains unresolved.[8] It does appear President Trump and General Secretary Xi are planning a June signing ceremony in the U.S.[9] The financial markets have mostly discounted an agreement with China, although we would not be surprised to see further gains if a deal is completed.

Japan trade talks: Although President Trump has expressed some optimism that a Japan/U.S. trade deal may be coming soon, PM Abe has refused a key component of U.S. demands, an end to agricultural tariffs.[10] Abe faces local elections later this year and giving in on agriculture would put Abe’s party at risk. Paradoxically, Abe did consume a significant amount of political capital to reduce agricultural tariffs as part of TPP. Thus, the other nations in the agreement now have better access to Japan’s agricultural markets compared to the U.S., which refused to join the agreement.[11]

Growing tensions in the South China Sea: The U.S. has put China on notice that it will no longer tolerate aggressive actions at sea by China’s fishing fleet and its coast guard.[12] China has been expanding its power in the region by using these two factors to expand its influence. Traditionally, navies have less aggressive terms of engagement with non-military vessels. China has used this practice to its advantage, using the coast guard and fishing fleet to project power. By putting out this notice, the U.S. Navy is signaling to China that the U.S. will treat fishing vessels and coast guard ships with the same protocol as official Chinese naval vessels. We also note that the U.S. sent two warships through the Taiwan Strait yesterday as a show of force.[13]

Iran oil sanctions: The Trump administration is holding fast to its position on Iranian oil waivers, indicating that a hard stop will be enforced on May 1. In other words, there will be no grace period for winding down transactions with Iran.[14] Meanwhile, President Trump has renewed his call for OPEC to boost production to offset the loss of Iranian crude.[15]

African Swine Fever: There are reports that the deadly African Swine Fever[16] has moved into North Korea.[17] The virus, which does not directly affect humans, is deadly for pigs, with a very high fatality rate. It has already adversely affected China’s massive pork industry and reports indicate it may be in Eastern Europe as well.[18] It hasn’t been reported in the U.S. yet, but agriculture security officials are very concerned about the virus entering North America at some point. The virus is a bearish factor for grains but has sent pork prices soaring.

Is a sacred cow on the block? A decade ago, Germany implemented a fiscal rule that makes it nearly impossible for the country to run fiscal deficits. This decision, coupled with high private sector net saving, has led to Germany running a massive trade surplus. At long last, it appears there may be some cracks developing in support of the fiscal rule.[19] The rule has curtailed public investment and Germany’s infrastructure has suffered over the 10 years it has been in place. Germany needs to bend on this issue. Its economy has become very dependent on exports.

On the above chart, we have put a vertical line representing the onset of the fiscal law. Since implemented, the trade surplus has continued to increase.[20] Germany’s current account surplus represents about 7.5% of its GDP, one of the highest in the world. Expanding its fiscal deficit should reduce that surplus and boost growth for the rest of the Eurozone.

S&P on Italy:Standard and Poor’s left everything unchanged by maintaining the BBB rating on Italy’s sovereign debt along with the negative outlook. So, the good news is that a crisis was averted; the bad news is that nothing has been resolved.

[20] For reference, gross exports represent about 12% of U.S. GDP.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.