by Bill O’Grady, Kaisa Stucke, and Thomas Wash

[Posted: 9:30 AM EDT]

Happy St. Patrick’s Day!

It’s a quiet morning in what has been a busy week. The only major news today is that Chancellor Merkel, who was due to visit earlier this week but was unable due to the snowstorm, is in Washington today. Merkel represents the established liberal order which Trump has vowed to upend. The meetings today could be interesting.

For the most part, economic expansions end for three reasons—inventory overhangs, overly tight monetary policy or a geopolitical event. Technology has mostly eliminated the first reason; firms have become so adept at managing inventory that overhangs are less common. The remaining two reasons have thus become more important. Geopolitical events were mostly to blame for the 1973-75 recession (the OPEC oil embargo was due, in part, to U.S. support for Israel in the Yom Kippur War) and the 1990-91 recession (the Gulf War was the culprit). The rest have been caused by overly tight monetary policy.

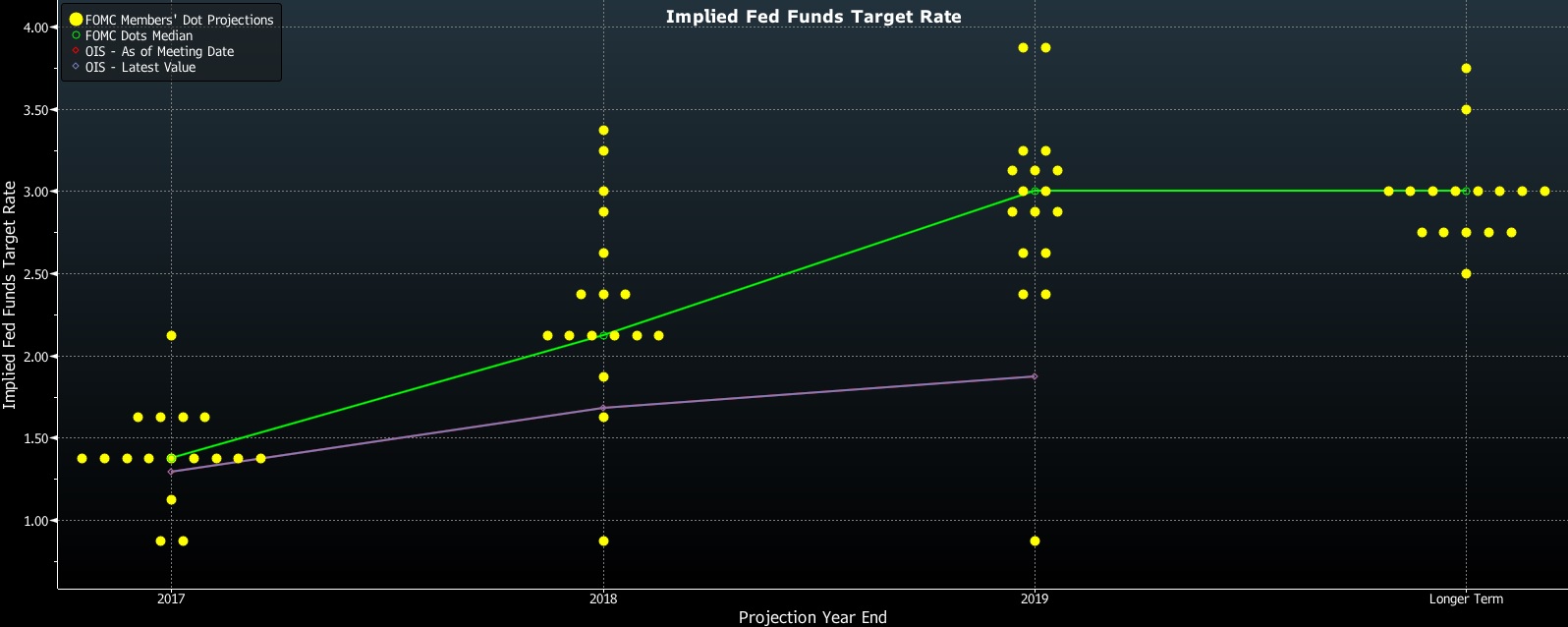

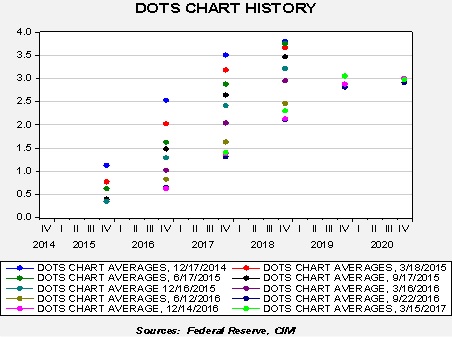

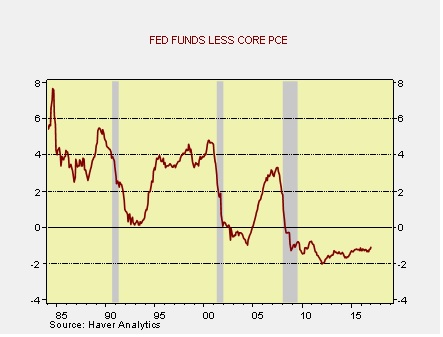

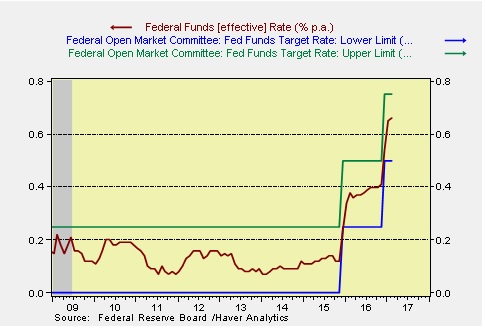

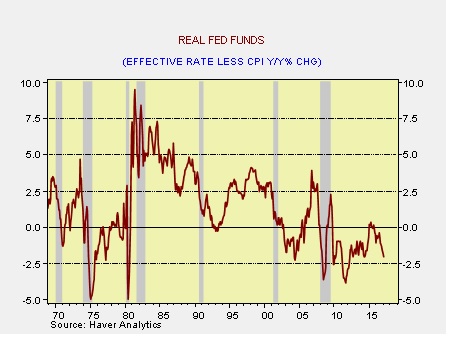

Currently, monetary policy appears accommodative—real fed funds remain negative and, by any measure of the Mankiw Rule (see today’s Asset Allocation Weekly below), policy is easy. Thus, paying attention to the other mentioned factor, geopolitics, makes some sense. And, when the lead headline in the FT says America’s “strategic patience” with North Korea has been exhausted, it makes us take notice. Secretary of State Tillerson said today that the U.S. considers the military option “on the table” if North Korea continues to ratchet up its military threats. We view this as a form of signaling. The military option should always be on the table. After all, if North Korea did something aggressive, like invade South Korea, the U.S. would almost certainly respond militarily. By saying the military option is available is to suggest that there is some sort of red line, or trigger, that would warrant military intervention. What might that be? Evidence that North Korea has a deliverable nuclear warhead might be enough.

Since the end of WWII, nuclear weapons have evolved into more of a doomsday defense than an offensive weapon. Essentially, a nation with deliverable nukes cannot be forced to unconditionally surrender. If Hitler had had deliverable nukes, he probably could have forced the Allies to offer a peace deal or face the total destruction of Washington or Moscow. If Pyongyang had a deliverable nuclear weapon, the likelihood of an invasion to overthrow the regime would decline significantly. This is the lesson of Saddam Hussein and Muammar Gadhafi; without a doomsday weapon, your regime can be overthrown and you can face execution.

Threatening the North Korean regime will more likely than not spur Kim Jong Un to achieve a deliverable weapon. However, it is unknown how exactly the U.S. will act if North Korea goes nuclear. Two states have joined the nuclear club in recent years—India and Pakistan. These didn’t appear to be a threat to the U.S. because the weapons are mostly pointed at each other. Iran’s calculus was to have a program and get close to “break out” of getting a weapon without actually doing so. Iran was able to use this brinksmanship to get most international sanctions lifted. The reason Iran probably never moved to cross the nuclear line is that it wasn’t sure whether Israel or the U.S. would view this as an existential threat and attack its nuclear facilities.

North Korea’s “Young Marshall” is clearly trying to solidify his position; this is why he has been on a dramatic execution binge.[1] This activity would suggest he feels insecure and may do something rash. Managing this situation will require delicate diplomacy, which may not be forthcoming from this administration. That doesn’t necessarily mean we are on the brink of war but it does suggest that the risks are rising. Even if the conflict remains contained and conventional, it may lead to a recession if concerns rise enough. Thus, we are closely monitoring the situation with North Korea for signs of escalation.

______________________________________

[1] See WGR, 3/6/17, The Assassination of Kim Jong Nam.