In our asset allocation process, we focus on cyclical trends; that doesn’t mean we pay no attention to secular trends but it isn’t our primary emphasis. The lack of clarity around what these terms mean can lead to confusion. And so, over the next few weeks, we will examine the difference between the two trends and how we address them in our asset allocation process.

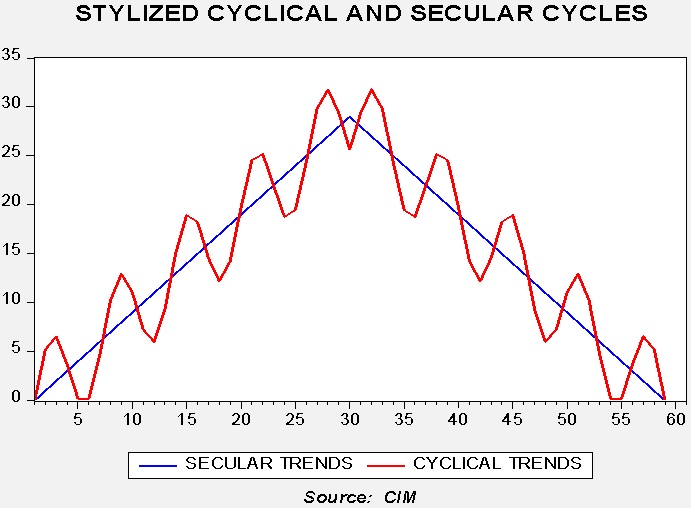

This chart shows a stylized example of cyclical and secular cycles. It’s simply for illustration purposes, but it does express the general view of how we view markets. In reality, cyclical trends are not this smooth or regular, but rather often exhibit varying length and amplitude. Secular trends are not necessarily constant either. But, in general, as we will look at in the coming weeks, financial and commodity markets exhibit both trends.

Depending on the market, cyclical trends tend to run three to 10 years. It is the most important trend in our asset allocation process. The business cycle is the primary factor in our analysis. The business cycle is the normal tendency for the economy to move from expansion to decline, recession, recovery and back to expansion. This cycle clearly affects financial and commodity markets. Financial market conditions, monetary and fiscal policy and geopolitical events are all important contributors to cyclical trends as well.

On the other hand, secular trends can last generations. These trends tend to be driven by societal factors. For example, public attitudes toward the balance between efficiency and equality are critical as these are affected by regulatory and tax policy. Long-term geopolitical stability is mostly a factor of hegemony; if a superpower vacuum is developing or a new hegemon is emerging, secular trends can adjust. What makes secular trends important is that because they last a long time, they become part of the background, leading investors to assume that these trends never change. And so, in the early part of a reversal in secular trends, actual market performance can vary widely from what is expected. The other factor that matters in secular trends is that, unlike our stylized model, they don’t always clearly shift, causing a degree of uncertainty as to whether the change actually occurred. Only with the hindsight of history can we definitively know when and if the secular change happened. Still, we pay attention to secular trends because, at inflection points, the impact on financial and commodity markets can be significant.

Therefore, over the next few weeks, we will examine the cyclical and secular trends in commodity, equity and debt markets. In general, this analysis will offer insights into our allocation process, discussing the important cyclical elements of each asset class along with the potential impact of a change in secular trends.

[Posted: 9:30 AM EDT] Happy Friday! Financial markets are mostly flat this morning. This is what we are watching:

Italy: The FT[1] is reporting that the Five-Star Movement and the League have reached a deal to form a government, although the prime minister post has not been settled. We would expect a compromise candidate, a figurehead, to emerge at some point for this role. The final deal does remove the talk of a return to “pre-Maastricht” and calls on the Italian bonds held by the ECB to not count against debt/GDP calculations. But, the agreement calls for both tax cuts and increased spending which will almost certainly lead to fiscal deficits that will run afoul of Eurozone rules.

What really caught our attention, however, was the government’s proposal to issue “mini-BoT,” which are short-term, small denomination sovereign bills. Denominated in euros, they are designed to be “tax anticipation notes.” Cash-strapped governments have issued such instruments; California did so eight years ago.[2]Still, previous notes were electronic entry; Italy plans to use its lottery presses to print these BoT, which makes them bearer bonds and potentially a parallel currency. Now, as one would expect, the coalition is downplaying this potential, indicating that no entity will be required to accept BoT. But, if the government follows through on this plan, it is a major threat to the Eurozone. It should be noted that the former Greek FM Yanis Varoufakis proposed similar instruments in 2015. In fact, the Five-Star and League negotiators consulted with Syriza on how to structure these instruments, yet even the radical Varoufakis wouldn’t go so far as to issue printed bearer bills. It isn’t hard to envision how these notes, issued at a discount to face value (say, €90 with a face value of €100), would fall to even deeper discounts as more are issued. Essentially, the BoT will potentially become a way for Italy to expand its fiscal debt in a quasi-currency. This coalition is turning into a significant threat to the Eurozone.

(Source: Bloomberg)

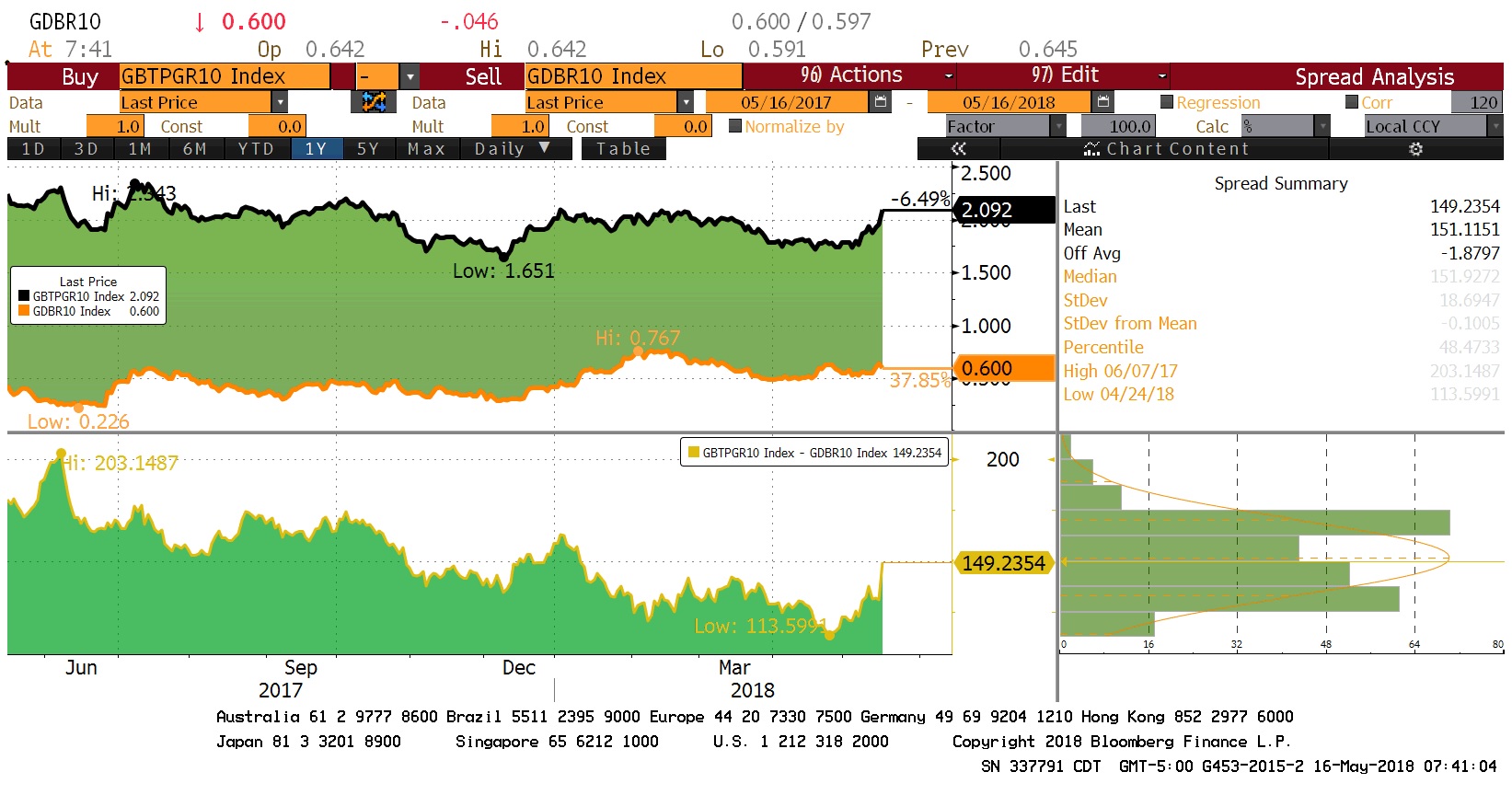

This chart shows the level and spread between German and Italian 10-year sovereigns. What is notable is that German yields have been steady to lower since the run up in Italian yields. We would expect Italian capital flight to develop and usually Germany is the first stop. We are also not seeing any unusual behavior in the Swiss franc. Perhaps investors are waiting for the PM to be appointed before deciding a populist threat in the Eurozone’s third largest economy is meaningful.

In the short run, the problems in Italy are bearish for the euro. But, if we get a north/south split, the euro becomes the new D-mark and a new southern euro becomes the new lira/drachma. The euro soars, while the southern euro depreciates. That may be the final outcome but getting there could easily mean a period of euro weakness.

Trade: There were two items on trade. First, there are reports that China will offer $200 bn in trade concessions.[3] Essentially, China will offer to increase its imports from the U.S. if the Trump administration relaxes the technology trade restrictions. Implied is the idea that Beijing will help in the negotiations with North Korea. The president now finds himself facing a problem often seen with his predecessors; the U.S. has multiple goals and has to “thread the needle” to meet all of them. And, in reality, it is usually impossible to get everything you want. China’s desire to expand and develop its tech industry seems paramount and it is willing to promise to buy grain,[4] natural gas and perhaps even oil to narrow the trade deficit if it will allow Beijing to maintain access to U.S. intellectual property. The problem is, of course, that this runs at cross-purposes to the U.S. goal to maintain tech supremacy. In addition, the buying China does with the U.S. means that other nations, e.g., Brazil, Argentina, Australia and perhaps Iran, will see their exports to China fall. Second, it appears that the NAFTA negotiations have failed. It isn’t clear if the administration will simply leave the treaty or if it will remain in limbo as talks drag on.

Venezuela: Elections will be held on Sunday; there is little doubt to the outcome.[5]President Maduro will likely win. Real opposition candidates have been prevented from running. Only two independent candidates share the ballot with Maduro and they won’t likely win more votes than Maduro unless powerful people in the ruling class have decided Maduro needs to go. If the expected occurs, most governments have already indicated they don’t recognize this election as legitimate which could mean new sanctions are imposed. If we get a surprise and Maduro is forced out, outside governments will have to decide whether this illegitimate election is now legitimate. Our expectation is that Maduro wins and Venezuelan oil supplies are further reduced.

[Posted: 9:30 AM EDT] Financial markets are quiet this morning. This is what we are watching:

More in Italy: Governments are powerful but not omnipotent. When financial markets turn on a country, it can force unwelcome policy changes. The populists in Italy are finding this out the hard way. As we noted yesterday, Italian sovereign yields rose sharply. Markets have offered little relief today as 10-year Italian sovereigns hit a high yield this morning of 2.15%; on May 4, the yield troughed at 1.71%. It should be noted that this 44 bps rise in rates has occurred without any tightening from the ECB. We did get some clarification on the debt write-down; the coalition doesn’t necessarily want the debt written off but wants any bonds held by the ECB as part of QE to not be counted in the debt/GDP calculation,[1] which, of course, is essentially the same thing. The leader of the League, Matteo Salvini, complained about market “blackmail.”[2] Although the populists have, to some extent, toned down their rhetoric about the Eurozone (they have dropped earlier calls for a referendum, for example), the coalition is proposing increases in fiscal spending that will break Eurozone rules. The coalition seems to be daring the Eurozone to sanction them; unlike Greece, Italy is a large economy and the populist leaders seem to be willing to force a showdown. If the coalition forms and does increase government spending, Germany’s reaction will be key. We doubt Germany will tolerate Italy’s actions and will press the Eurozone and the ECB to punish Italy. Although we have been bullish the EUR, for parity reasons, an internal fight will likely be bearish in the short to intermediate term.

Our long-term view has always been that the Eurozone was unsustainable; the single currency was not an economic policy but instead done for political goals, namely, to contain Germany. The real fight is whether Germany’s or some other European nation’s vision dominates. The story of Europe since 1870 has been all about the German problem. Germany is the strongest power in Europe but not strong enough to fully dominate it. In the long run, we expect the Eurozone to split into workable economic units, with the north and south creating their own currencies. As we noted yesterday, the “known/unknown” is which group France joins.

No NAFTA[3] today: Today is the deadline for NAFTA talks but it doesn’t look like a deal is in the offing. The deadline is somewhat artificial—negotiations can continue. However, in order to put the bill through under the complicated Fast Track Promotion Authority, which passes trade bills on an “up or down” vote without amendments, Speaker Ryan needs to put the bill into place today. In addition, exemptions for the steel and aluminum tariffs for Mexico and Canada end on June 1; it is hard to argue for an extension without a NAFTA deal. And, Mexican elections loom on July 1 and polls continue to show that Orbador still holds a dominating lead. He is a populist and negotiating a NAFTA deal under his government might not be possible. A breakup of NAFTA would be very disruptive to all three economies.

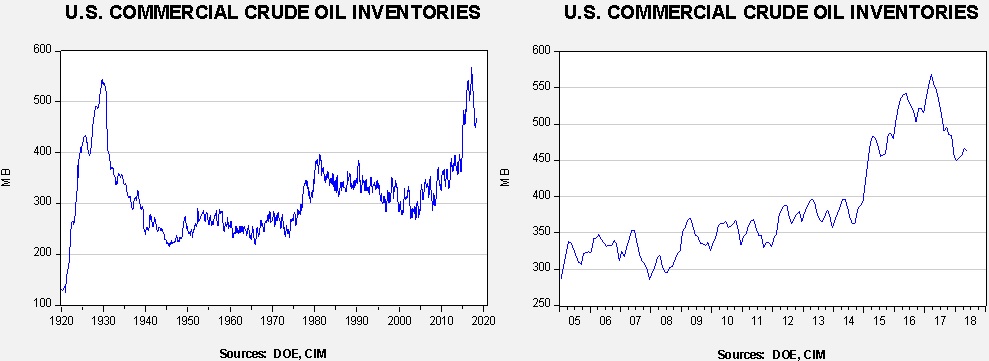

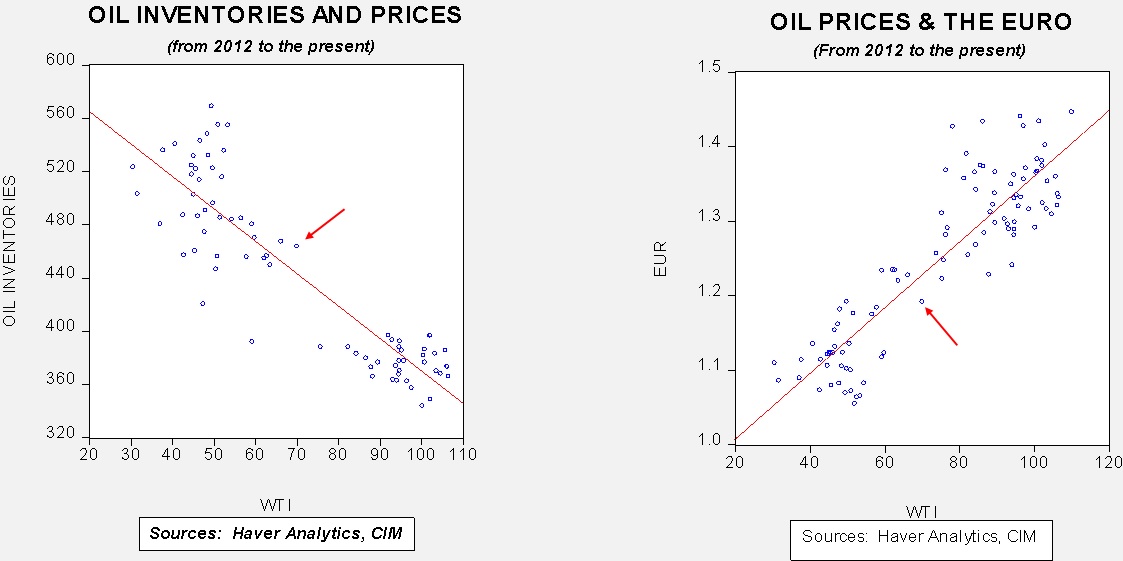

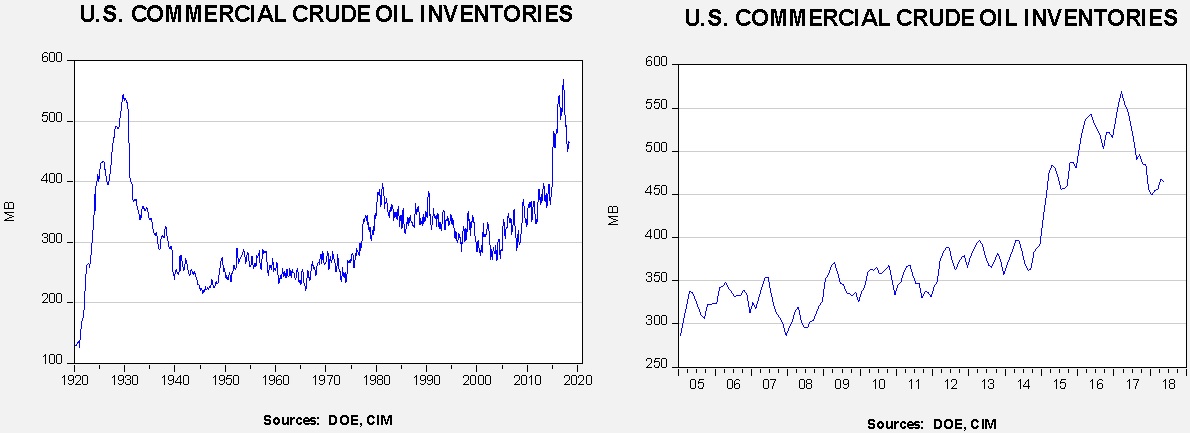

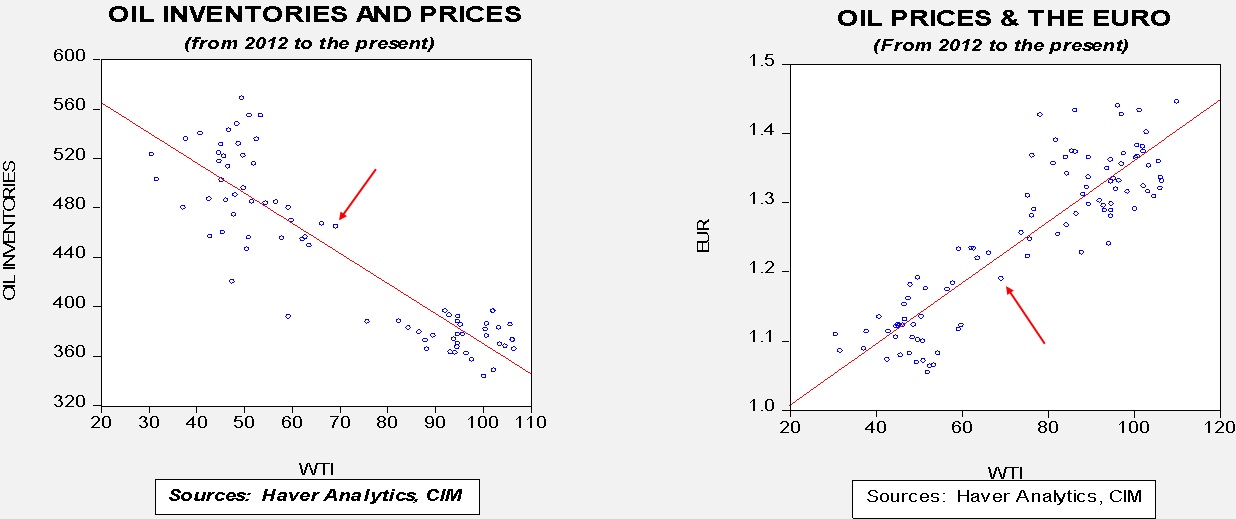

Energy recap: U.S. crude oil inventories fell 1.4 mb compared to market expectations of a 1.5 mb draw.

This chart shows current crude oil inventories, both over the long term and the last decade. We have added the estimated level of lease stocks to maintain the consistency of the data. As the chart shows, inventories remain historically high but have declined significantly since last March. We would consider the overhang closed if stocks fall under 400 mb.

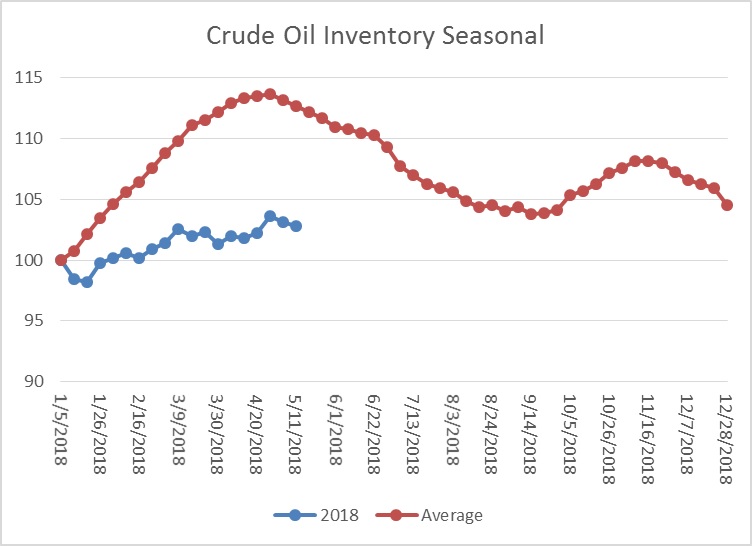

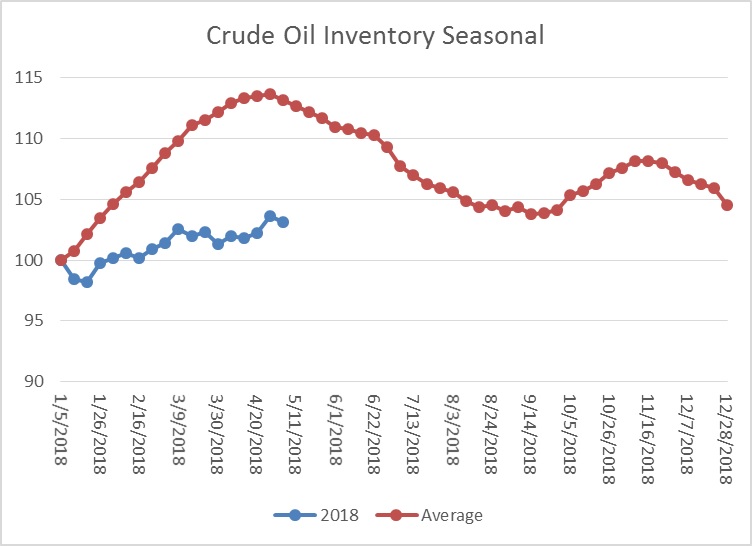

As the seasonal chart below shows, inventories are usually rising this time of year. This week’s decline is consistent with the onset of seasonal patterns. We expect steady stock withdrawals from now into mid-September. If we follow the normal seasonal draw in stockpiles, by September, crude oil inventories will decline to approximately 424 mb.

(Source: DOE, CIM)

Based on inventories alone, oil prices are overvalued with the fair value price of $63.55. Meanwhile, the EUR/WTI model generates a fair value of $65.68. Together (which is a more sound methodology), fair value is $64.68, meaning that current prices are above fair value. The combination of a stronger dollar and the peak of seasonal inventories has weakened our fair value calculations. However, we do expect the dollar to weaken in the coming months and oil inventories to decline based on seasonal factors. Using the oil inventory scatterplot, a reading of 424 on oil inventories would generate oil prices in the high $70s to low $80s range. At present, we have no reason to believe that inventories won’t follow their usual path so the case for higher oil prices remains, barring a seasonal divergence that increases supply or a sharp rise in the dollar. We note today that Total (TOT, (ADR) 63.21) warned it will likely pull out of Iran unless it can be guaranteed sanctions relief.[4] The French oil company is the largest foreign investor in Iran’s energy sector. If it does pull out, it would represent a significant blow to Iran and signal that, despite all the brave talk, Europe will be beholden to the American sanctions regime. Issues like this, plus the Venezuelan elections on Sunday, are a major reason why oil prices are running in front of where the dollar and inventories suggest they should be. In other words, the observed risk premium is reasonable.

[Posted: 9:30 AM EDT] It’s mid-week! Here is what we are watching this morning:

A DPRK snag? Yesterday afternoon, the Kim regime turned hostile, calling off talks with South Korea and threatening to cancel the summit meeting with President Trump. There is a lot of uncertainty around this sudden change in tone. However, here are some of our observations. First, the Kims are famous for erratic behavior. George Friedman of Geopolitical Futures used to call North Korean policy “ferocious, weak and crazy.” In other words, the regime projected itself as strong (better not mess with us), weak (we are small fry, why bother) and crazy (don’t provoke us, we might do anything). Kim’s actions are consistent with his father and grandfather’s behavior. Second, Kim gets more from this summit with Trump than anyone—he gets to put his nation on the world stage with the preeminent superpower. Thus, we doubt he will walk away. But, it makes sense that he would try to shape the talks before they begin. So, indicating that denuclearization ≠ unilateral nuclear disarmament is important for North Korea.[1] NSC Director Bolton has suggested that North Korea will follow the Libyan model, which is an unfortunate parallel, not one that Kim would adopt. North Korea wants “goodies” for each step in the denuclearization process. It does not want immediate denuclearization. Three, it’s important not to underestimate the impact of China; Beijing would prefer the status quo, so it may be giving Kim incentives to walk away from the summit. However, our take is that Kim and Moon are really trying to make the Koreas independent. If so, Kim wants to use the U.S. to distance himself from China. We suspect Xi understands this goal and is probably trying to thwart it. We will be looking for any change in China’s trade with North Korea.

For financial markets, there are two issues within this story. First, does a hot war develop? Second, how do the talks with North Korea affect U.S./Chinese trade relations? Unless these two issues are affected, the North Korean situation won’t have a dramatic impact on the financial markets.

Tensions at the FOMC? Reuters[2] is reporting that a dispute is developing over the issue of “R*Star,” which is otherwise known as the natural rate of interest. It also describes what we often refer to as the “neutral rate.” It’s the rate of interest that is neither stimulative nor restrictive. The concept was first described by Knut Wicksell and suggests that the economy could overheat if policymakers set a rate below the R*Star, while a rate set above could trigger a recession. R*Star is not directly observable; economists attempt to estimate it based on a number of methods. The Phillips Curve is one attempt to determine this rate. Others try to do it through combinations of long-term productivity and labor force growth. The dispute is over how to define R*Star. John Williams, recently appointed as president of the NY FRB, argues that slow productivity and labor force growth have led to a structural decline in R*Star, meaning the FOMC may be close to the peak of its rate cycle. Randy Quarles, a Fed governor, has postulated the economy has a much faster growth potential and thus should have a higher rate. In some respects, this is a normal “fight” within the Fed, one between hawks and doves. The difference here is the arena—economists are fighting over R*Star.

On a related note, those who prepared Richard Clarida and Michelle Bowman for their hearings likely raised a glass last evening because the take on their confirmation testimonies was “boring.” If one is preparing a nominee, boring is the goal. Although Clarida didn’t offer us much in his testimony, he did indicate discomfort with QE and seemed to suggest he might not have supported the later versions of the program. As we have noted in the past, we suspect a generation of young economists will write their dissertations on QE and its impact. Simply put, we really don’t know what it did. Our position is that the effect was mostly psychological. It convinced the public that the zero bound was not a barrier for further policy support. However, the liquidity injected seemed to sit harmlessly (and ineffectively) on bank balance sheets as excess reserves, so the real impact was probably limited. However, if the Fed forgoes QE, its only recourse at the zero bound is negative nominal interest rates.

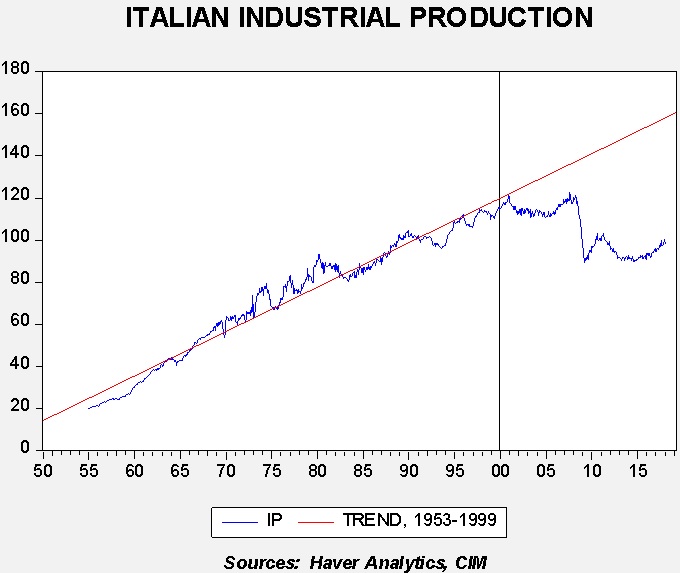

Italy: There were a couple of bombshells that emerged from the coalition talks. First, a draft version of the coalition agreement sketched out a plan that would effectively return Italy to the pre-Maastricht world of a steadily depreciating lira.[3] Although the plan does not call for Italy to leave the Eurozone, it wants to be freed from fiscal constraints. Before joining the Eurozone, Italy maintained its economic growth through steady depreciation of the lira and expansive fiscal spending. Joining the Eurozone did lead to lower interest rates but restricted fiscal flexibility; economic growth in Italy has suffered ever since.

This chart shows Italian industrial production from 1953 to the present. Note that production rose steadily until Italy officially joined the single currency in 2000. Since then, production has stagnated. We don’t disagree with the populist coalition—joining the Eurozone was a mistake. The question is how does Italy fix this issue? There are two paths. The first is a dramatic restructure of the Italian economy, similar to the labor market reforms in Germany (Hartz reforms) that occurred in the last decade. Politically, this is probably impossible. The second path is to leave the Eurozone. We have always suspected this would be the eventual outcome. The political trends suggest that exit is a growing possibility.

Another bombshell was that the potential coalition wants the ECB to cancel €250 bn of Italian government debt held on the ECB’s balance sheet. This would probably be illegal under Eurozone rules, which prevents direct fiscal funding by the ECB. This report has sent Italian yields rising.

(Source: Bloomberg)

This chart shows German and Italian 10-year sovereigns. Note the spike in the spread.

Italian polls still indicate the majority of citizens want to remain in the Eurozone.[4] However, it is tied with Greece with the most against the Eurozone and the lowest actual support. The coalition probably doesn’t have the support to exit the Eurozone yet. But, if Germany and the EU try to thwart Italy’s attempt to expand fiscally, we would not be surprised to see a swing toward favoring an exit (and we would also expect increasing capital flight to protect against just that outcome).

Would Italy’s departure from the Eurozone be the end of the single currency? Although losing Italy would be significant, we suspect that it would likely lead to a two-currency bloc. It would be easy to make the case that Spain, Greece, Portugal, Italy and perhaps some of the Eastern European nations could join a currency bloc, while the Northern Europeans keep the euro. That scenario would probably lead to a much stronger EUR, while the southern bloc, by design, would depreciate. The key nation in this scenario is France. France should probably be in the southern bloc but it would want to stay linked to Germany. This outcome isn’t imminent but, as history shows, a process like this can go quite quickly once it starts.

[Posted: 9:30 AM EDT] Risk markets are under some pressure this morning. Here is what we are watching this morning:

Clarida to the Hill: Richard Clarida, Columbia University economist and Global Strategic Advisor for PIMCO, testifies before the Senate Banking Committee on his way to a confirmation vote. Michelle Bowman, a Kansas banking regulator, will join him today in this endeavor. Clarida is up for the position of vice chair and, given Chair Powell’s lack of academic experience, the vice chair position will be of great importance. We view Clarida as a moderate on policy and expect him to be easily confirmed. Bowman will fill the role reserved for community banks; this position routinely votes with the leadership. Filling out the FOMC is important. Meanwhile, Marvin Goodfriend’s nomination remains in limbo; we doubt he can get confirmed and expect the administration to eventually find a replacement.

Today in trade: Every day seems to bring new information on trade. Today’s trends indicate that NAFTA talks, so far, are not progressing fast enough to meet the May 17th (Thursday) deadline. But, it’s probably too soon to declare negotiations “dead” because Washington seems to only accomplish things when deadlines loom. The president is trying to navigate the ZTE (ZTCOF, $2.26, delayed) issue. It appears the White House may be trading ZTE for grain tariffs, backing down on punishing ZTE in return for China not raising tariffs on grain.[1] There are suggestions that the China hawks may be losing influence[2]; specifically, it appears that Wilbur Ross may have acted rashly to punish ZTE. Although ZTE acted improperly, the punishment Ross approved was probably overly harsh and prompted the White House to walk it back. If this is the case, Treasury Secretary Mnuchin is likely becoming a more important influence on trade. If so, we could see a moderating tone on the trade war front.

Italian populists granted an extension: The Five-Star and League parties asked the Italian president for more time to form a government and the extension was granted. The policy platform does appear to be coming together but the sticking point is the prime minister. Neither party has enough power to press for its own party leader so they are trying to find a compromise candidate that both parties can live with. The possibility of a populist party is putting some pressure on the EUR.

Venezuelan woes: As the state oil company, PDVSA, defaults on bonds, creditors are taking steps to seize assets outside the country. In an especially crippling move, ConocoPhillips (COP, 69.59) has seized Caribbean tank farms and related export facilities owned by PDVSA.[3] ConocoPhillips won a court ruling against PDVSA for assets nationalized in Venezuela. There are reports of oil tankers owned by the company being seized by creditors.[4] The bottom line here is that PDVSA may find itself unable to export product and crude oil because creditors may seize the asset before it can reach its destination. Supply disruption from Venezuela may become a bigger issue than Iran for oil supplies.

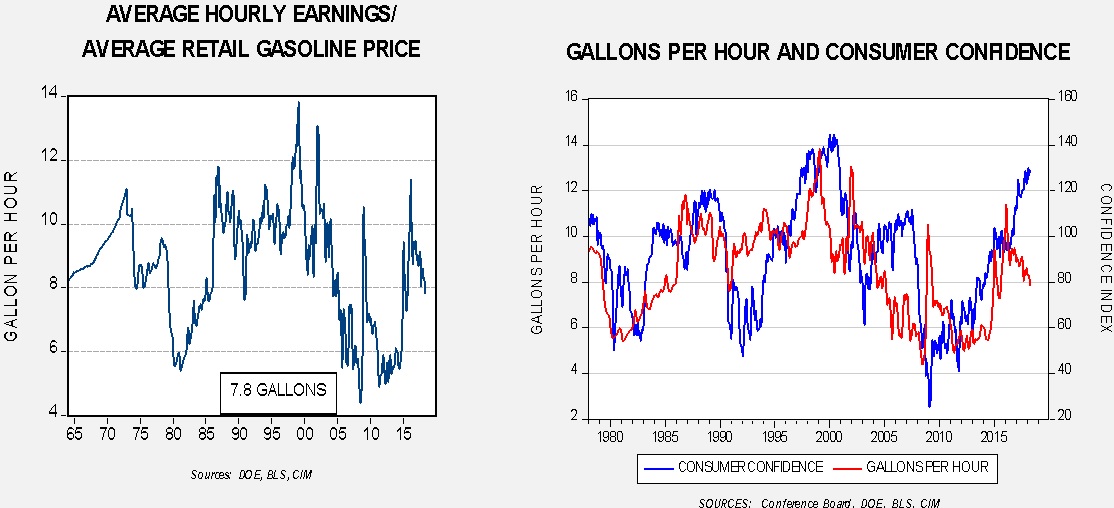

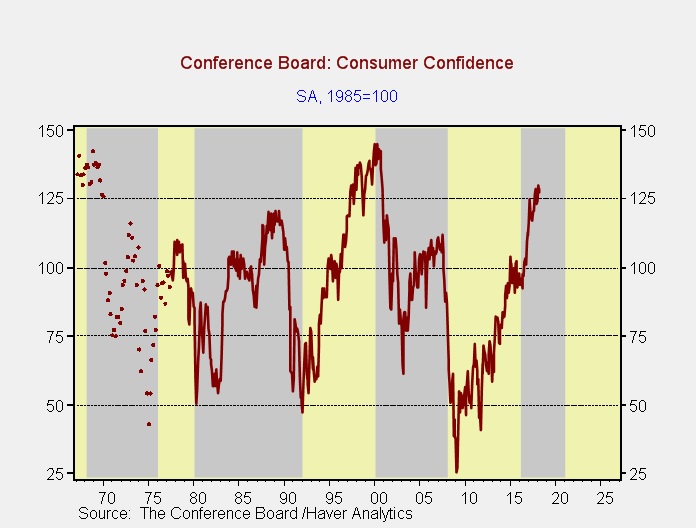

Summer and gasoline: One of the ways we measure the impact of the price of gasoline is to compare it to the average hourly wage for non-supervisory workers.

The chart on the left shows how many gallons of gasoline the average worker can purchase with an hour’s worth of work. Thus, the larger the number the more beneficial it is to the worker. The long-term average is about 8.6 gallons per hour. We recently fell below 8.0 gallons, suggesting gasoline prices are getting a bit lofty. The chart on the right compares the aforementioned ratio to consumer confidence. It’s not a perfect fit but, in general, a high ratio correlates with high consumer confidence. The recent decline in the ratio is diverging from the current high levels of consumer confidence. There was a similar pattern around the turn of the century that eventually led to a drop in confidence.

The impact of confidence on the economy is mixed. It sometimes coincides with stronger retail sales but other times diverges.[5] However, it does appear that confidence affects voting behavior. The chart below shows presidential parties, with gray showing Republican presidents. The relationship isn’t perfect, but we note that confidence declined in the early 1990s and in 2007, leading to changes in power. Interestingly enough, confidence was mostly elevated at the end of Clinton’s term as well as Obama’s, but neither saw his party hold onto power. We note recently that the president criticized OPEC for keeping oil prices high. He may be worried that rising summer gasoline prices might undermine his popularity and hurt the GOP in the midterms. If oil gets to $80 per barrel or higher, we would not be shocked to see a large SPR release in a bid to ease prices.

We occasionally run across a book that we deem important enough in the arena of geopolitics to warrant a full report dedicated to its review. Recently, we happened upon a book that fits this requirement, The Marshall Plan: Dawn of the Cold War by Benn Steil.[1] This book details the history of the Marshall Plan, discusses how the plan developed and identifies the major historical figures who created the strategy. Furthermore, more importantly for the present, it shows how this generation of policymakers addressed the geopolitical problems of Europe, issues that have resurfaced since the Cold War ended in 1991.

In this report, we will review the state of Europe after the war, focusing on U.S. and Soviet goals for the postwar era, and discuss the important figures of the era and the legacy they left behind.

Postwar Europe

Prior to the official end of WWII, Joseph Stalin, Franklin Roosevelt and Winston Churchill had begun negotiating how the postwar world would be managed. Roosevelt believed voters would not accept a permanent American military presence in Europe and thus intimated to Stalin that the U.S. would exit two years after the German surrender. Churchill was mostly focused on maintaining the British Empire, a position Roosevelt seemed determined to undermine. As the three drew up plans, Stalin sought to create a security buffer as far into Western Europe as he could press it.

[Posted: 9:30 AM EDT] Happy Monday! Here is what we are watching this morning:

ZTE relief? In a surprise announcement, President Trump tweeted that he is seeking some sort of relief for the embattled company. ZTE (ZTCOF, 2.26, delayed) is under a rather harsh penalty from the Commerce Department for breaking Iranian sanctions. Under U.S. rules, the company would not be able to access U.S. components for its devices. According to reports,[1] President Trump was contacted by Chairman Xi who asked for help on this issue. This action does appear contrary to the general direction of trade policy toward China but is probably also part of the administration’s broader negotiating stance. In other words, the president may be using ZTE relief to accomplish other parts of his trade agenda. We note that a high-level Chinese trade delegation is arriving in Washington on Friday, led by Vice Premier Liu He, a key member of Xi’s governing team.

This event highlights an element of this administration’s behavior. Simply put, the president’s negotiating style is personal and improvisational. He doesn’t over prepare and likes flexibility. This characteristic makes for great risk but also has the potential for breakthroughs. The North Korean negotiations are a case in point. It may turn out that the talks with Kim end up as a disaster, leading to war. At the same time, they might also lead to a new relationship and dramatic lessening of tensions. Previous administrations have been very cautious in their dealings with Pyongyang and have gotten nowhere. It is possible that Trump’s negotiating style is what is needed to move the discussion forward.

A similar trend may develop on trade. The bellicose tone may morph into a workable trade deal that improves the global financial system and extends this business cycle. It could also devolve into a trade war. It is clear that Trump has gotten the world’s attention. But, it is hard to know exactly what the result of these talks will be at their conclusion. For financial markets, this is really hard because part of the markets’ role to discount the future. The future is always uncertain but when a negotiator vacillates between war and peace, it increases the difficulty. However, if Trump is offering Xi an “olive branch” on ZTE and it reduces trade tensions, it will be bullish for risk assets. In order for Trump to do that, he will likely need a high-visibility “deliverable” to bolster his political fortunes.

Iran: Iranian officials are visiting nations that still remain in the nuclear deal.[2] For now, it looks like the non-U.S. participants will remain in the agreement, although they will likely face the threat of secondary sanctions from the U.S.; National Security Advisor Bolton suggested this in the Sunday talk shows.[3] For now, we expect the deal to hold but, eventually, Iranian hardliners will use the rupture to retake control of the government and at least threaten to restart uranium enrichment. In the short run, oil prices have benefited from the risk of a decline in Iranian supplies. Those supplies are probably not at risk for the moment. We do note that China has opened an oil futures contract denominated in CNY. Reports indicate that volume has increased in light of the sanctions.[4] Although transacting in CNY will reduce the risk of dollar-based sanctions, it also reduces the value of Iranian oil as the CNY isn’t broadly convertible and China limits foreign ownership of Chinese financial assets, a key element of the reserve currency system. Thus, Iran would be limited to buying Chinese goods and services. Still, one of the rules of sanctions is that the more nations that participate in the sanctions effort, the better they work and thus, if the U.S. stands alone, the impact of sanctions is lessened.

Italian government: According to reports, the two major populist blocs, the Five-Star Movement and the League, are making progress toward forming a government. Although the key sticking point, the prime minister position, hasn’t been resolved, they have put together a policy platform that includes a basic national income for the poor, a reversal of pension reforms and a flat tax of 15%. Although the fiscal plan may meet the technical constraints of the Eurozone, it clearly doesn’t meet the spirit of structural reforms that the Eurozone has been asking of Italy. A populist Italy will eventually threaten the fiscal rules of the Eurozone and, unlike Greece, Italy’s economy is large enough to threaten the integrity of the single currency bloc. European equities have eased on the news while probably supporting modest EUR appreciation this morning.

Indonesia terror attack: It appears a set of bombings in Indonesia was executed by a family that had recently returned from Syria, reportedly[5] with ties to an Islamic State group. Two Christian churches were targeted. There have been fears among counterterrorism experts that the demise of Islamic State would lead to its followers spreading into other parts of the world and carrying out attacks in their new countries. There was also an attack in Paris,[6] a knifing that may have been inspired by Islamic State, although the ties are not as clear as the Indonesian incident.

Iraqi elections: Although results are preliminary, it appears the radical cleric Moqtada al-Sadr was the winner of parliamentary elections over the weekend. Turnout was very low, around 45%, which may have contributed to his win. Results suggest his party won 54 out of 329 seats, which means he will need to build a coalition in order to govern. The expected winner, current PM Haider al-Abadi, came in third. Al-Sadr is an interesting candidate because he is considered an Iraqi nationalist—he opposes both the U.S. and Iran. Although a Shiite cleric, his relations with Iran are mixed and we suspect Tehran is not happy about his win as it will complicate relations between the two countries.

Hawkish Mester: Cleveland FRB President Mester indicated that better growth likely means she will support more rate hikes than she has in the past. She is a voter this year and this stance increases the odds of four hikes this year.

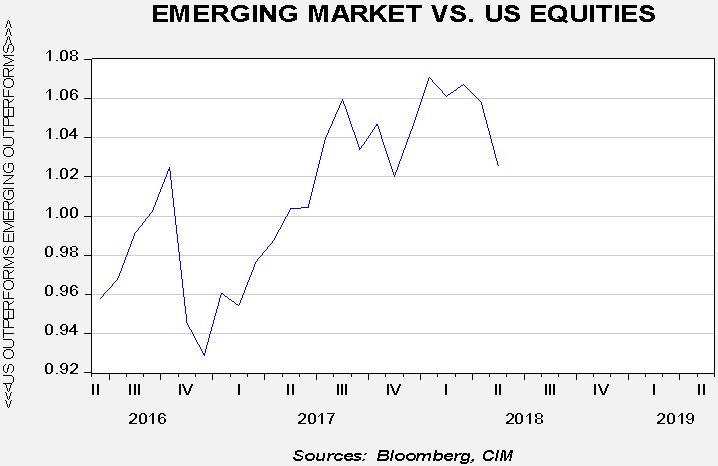

Recently, U.S. equities have outperformed emerging market equities.

The chart above shows the relative performance of emerging market equities against U.S. equities. A rising line indicates that foreign equities are outperforming. Questions are being raised as to whether this recent decline is the end of what has been a strong relative uptrend in emerging equities that began near the end of 2016.

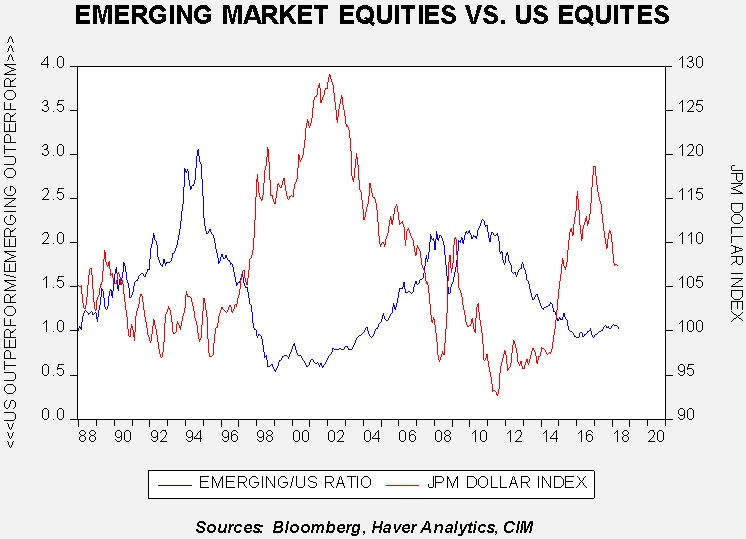

The above chart shows the same relative performance ratio along with the JPM dollar index. In general, emerging equities tend to trade opposite the dollar. In the past few weeks, the dollar has rallied after peaking in early 2017. We suspect this has mostly been a short-covering rally (surveys suggest market participants have been leaning heavily against the greenback), although there has been concern that interest rate differentials may be supporting the dollar as well.

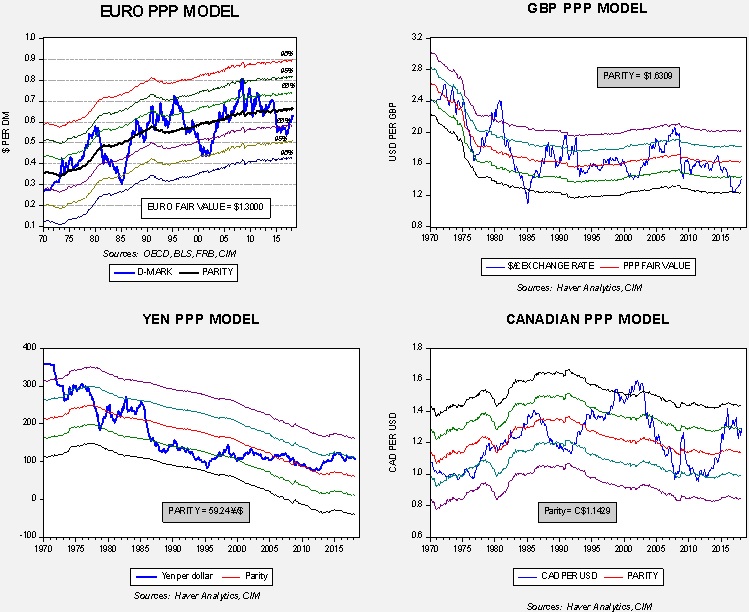

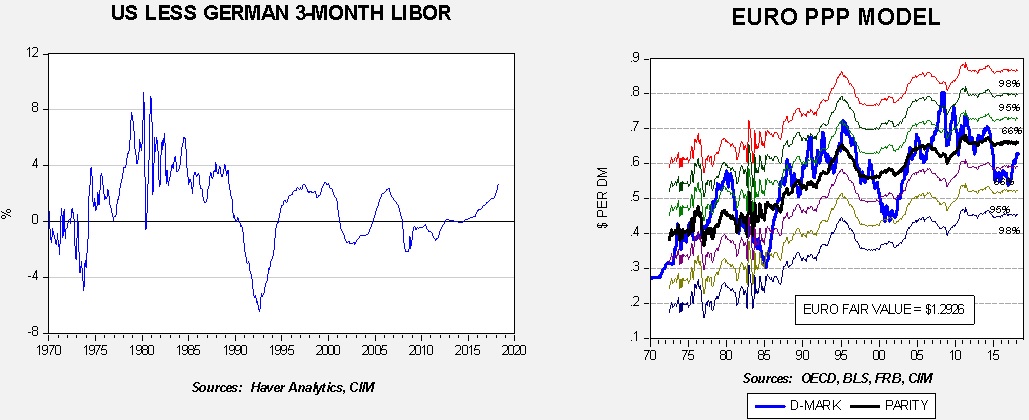

Our basic valuation model for exchange rates is purchasing power parity, which assumes that exchange rates offset price differences between countries. In general, nations with higher inflation tend to have weaker exchange rates to equalize prices. The model is not perfect; not all goods are tradeable and trade regulations can interfere with the ability of floating exchange rates to generate “the law of one price.” However, the historical record does suggest that when exchange rates deviate significantly from the fair value generated by the parity calculation, it is more probable that the trend will reverse over time. Currently the major exchange rates are running below parity.

These four charts show the parity models for the D-mark (a proxy for the euro), the British pound, Japanese yen and Canadian dollar. All are, or have recently, been a standard error or more from fair value. This would suggest the dollar has more room to decline.

What about the widening interest rate differential? After all, the FOMC is tightening policy faster than the rest of the world. Although interest rate differentials affecting exchange rates makes intuitive sense, the small gains one can make from the differences in interest rates can be easily swamped by exchange rate moves. And, high interest rates alone are not necessarily signals of strength; recently, Argentina raised overnight rates to 40% to support the peso.[1] Such policy actions belie the notion that high interest rates automatically make a currency attractive. Still, between nations of similar credit characteristics, all else held equal, the nation with the higher interest rates would likely see a higher exchange rate.

Adding the interest rate differential with a 30-month lag suggests the impact of interest rates isn’t all that significant. Due to the lag, the differences in interest rates will tend to offer support to the dollar but, by far, the impact of relative inflation is more robust. Thus, if inflation in the U.S. does rise relative to German inflation, the impact of higher rates will be lessened.

In conclusion, the recent rally in the dollar and pullback in emerging markets does bear watching, but the underlying fundamentals still support the emerging market allocation. Thus, without ample evidence to suggest otherwise, we expect emerging market equities to recover from recent weakness.

BOE meeting: The BOE results were neutral to hawkish. Rates were left unchanged, as expected, but the vote was 7-2 with the dissenters voting for a hike. The press conference and the statement were rather dovish, belying the vote. Markets took the results as moderately dovish.

Israel v. Iran: Although we don’t think either side wants a full-blown conflict, Israel has launched a series of missile strikes against Iranian targets in Syria. These targets appear to be command and control centers for Iranian operatives and proxies in Syria. Iran has retaliated with similar strikes against military targets in the Golan Heights. The tempo of attacks has clearly escalated since the president withdrew from the Iran nuclear deal. Escalating tensions continue to support oil prices. At this point, we would characterize conditions as tense but not necessarily a prelude to an open conflict. However, the potential for escalation is rising.

Italian government: The Five-Star Movement and the Northern League are trying to form a government. It’s sort of a “damned if you do, damned if you don’t” issue for the markets. A government based on this coalition would be decidedly populist. Although all parties have moderated their stance on the Eurozone, the populists will push for fiscal stimulus and threaten the German-enforced order in the Eurozone. At the same time, if the move to form a government fails, summer elections are possible and the odds of an even stronger showing by the populist parties would be elevated. We have seen a modest rise in Italian sovereign yields; if conditions deteriorate, look for the spread between Italian sovereigns and Bunds to widen.

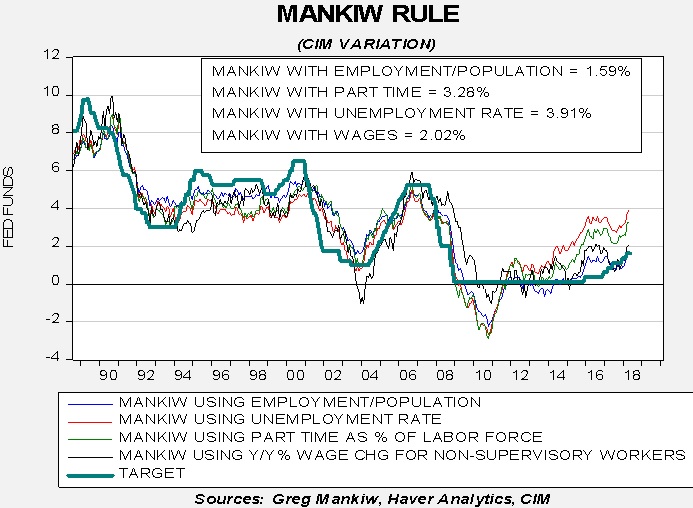

Fed policy: With the release of the CPI data we can update the Mankiw models. The Mankiw rule models attempt to determine the neutral rate for fed funds, which is a rate that is neither accommodative nor stimulative. Mankiw’s model is a variation of the Taylor Rule. The latter measures the neutral rate using core CPI and the difference between GDP and potential GDP, which is an estimate of slack in the economy. Potential GDP cannot be directly observed, only estimated. To overcome this problem with potential GDP, Mankiw used the unemployment rate as a proxy for economic slack. We have created four versions of the rule, one that follows the original construction by using the unemployment rate as a measure of slack, a second that uses the employment/population ratio, a third using involuntary part-time workers as a percentage of the total labor force and a fourth using yearly wage growth for non-supervisory workers.

Using the unemployment rate, the neutral rate is now 3.91%, up from 3.75%. The rise reflects the decline in the unemployment rate. Using the employment/population ratio, the neutral rate is 1.59%, down from 1.68%. Using involuntary part-time employment, the neutral rate is 3.28%, up from 3.22%. Using wage growth for non-supervisory workers, the neutral rate is 2.02%, up from 1.67%. The modest rise in core inflation (which was less than forecast) has lifted the forecast estimates for the neutral rate for all models. Although the divergence is wide between the models, three of the four do signal that the FOMC is still accommodative, with the target rate running below estimated neutral rates. Only the employment/population ratio version shows the neutral rate roughly equal to the current policy mid-point. In other words, if the FOMC is basing policy on the employment/population ratio, they would have already achieved policy neutrality and should refrain from further rate hikes. If anything, we suspect they lean toward the unemployment rate but, due to the high degree of uncertainty surrounding slack, the committee prefers to raise rates slowly in order to avoid a policy error.

Energy recap: U.S. crude oil inventories fell 2.2 mb compared to market expectations of a 1.3 mb build.

This chart shows current crude oil inventories, both over the long term and the last decade. We have added the estimated level of lease stocks to maintain the consistency of the data. As the chart shows, inventories remain historically high but have declined significantly since last March. We would consider the overhang closed if stocks fall under 400 mb.

As the seasonal chart below shows, inventories are usually rising this time of year. This week’s decline is consistent with the onset of seasonal patterns. We expect steady stock withdrawals from now until mid-September. If we follow the normal seasonal draw in stockpiles, crude oil inventories will decline to approximately 425 mb by September.

(Source: DOE, CIM)

Based on inventories alone, oil prices are overvalued with the fair value price of $64.09. Meanwhile, the EUR/WTI model generates a fair value of $65.38. Together (which is a more sound methodology), fair value is $64.31, meaning that current prices are above fair value. The combination of a stronger dollar and the peak of seasonal inventories has weakened our fair value calculations. However, we do expect the dollar to weaken in the coming months and oil inventories to decline based on seasonal factors. Using the oil inventory scatterplot, a reading of 425 on oil inventories would generate oil prices in the high $70s to low $80s range. At present, we have no reason to believe that inventories won’t follow their usual path, so barring a seasonal divergence that increases supply or a sharp rise in the dollar the case for higher oil prices remains. We should note that worries over the Iran nuclear deal are supporting oil prices and this factor will likely remain in place for the foreseeable future.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.