Asset Allocation Weekly (April 27, 2018)

by Asset Allocation Committee

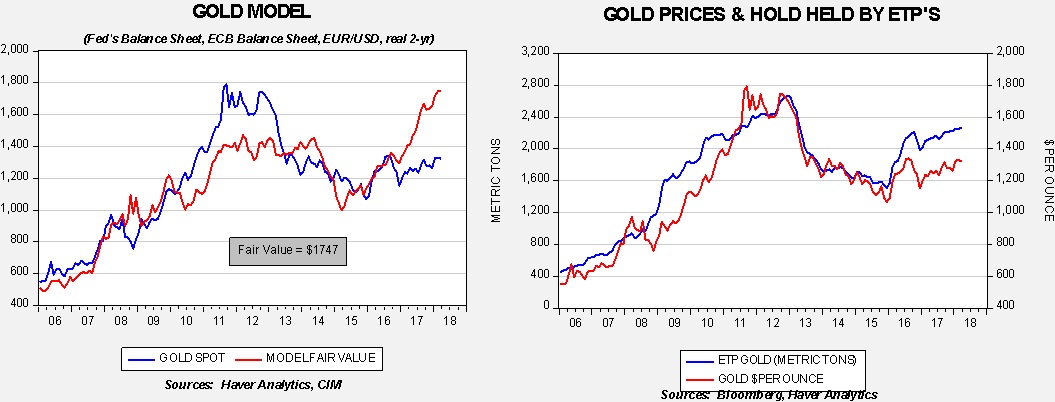

In our recent rebalance, the Asset Allocation Committee added a position in gold. There were two reasons behind the decision. First, we estimate that gold prices are undervalued compared to relevant fundamental factors.

The chart on the left is our gold valuation model. It uses the balance sheets of the Federal Reserve and the European Central Bank, the EUR/USD exchange rate and inflation-adjusted two-year Treasury yields. The model currently indicates gold prices are deeply undervalued. Much of this undervaluation is probably due to expectations of balance sheet contraction and higher real yields.[1] For example, if the Fed’s balance sheet was cut to $3.0 trillion from the current $4.4 trillion, the fair value would drop to 1585.73 (assuming the other variables remain unchanged). In other words, it appears the financial markets are discounting a more bearish turn in fundamentals than is probably likely.

The chart on the right shows the price of gold relative to the holdings of gold by exchange-traded products (ETPs). The price of gold tends to track the holdings of ETPs with two periods of divergence. Gold prices tended to track higher in both periods.

Second, gold is a flight-to-safety asset. During periods of turmoil, investors will often shift to safety assets. With the potential for a geopolitical event rising in the coming months, the committee has concluded that allocating some of the portfolio to gold is prudent. Here are some of the potential events:

- North Korea: If talks between Kim Jong-un and President Trump go awry, the chances for war in the Far East rise significantly. We view these talks as “make or break”; if they fail, it is hard to see a path forward that doesn’t result in conflict.

- Iran: The Trump administration’s policies toward Iran are hardening. If the Obama-era nuclear deal is scotched and new sanctions are imposed, we expect Iran to move toward a nuclear weapon which increases the odds of a conflict.

- China: Trade tensions with China are rising. A full blown trade war will tend to boost inflation and if the Federal Reserve is constrained in responding due to political pressure then gold will be an attractive response.

For these reasons, we have added gold to the portfolio. We will continue to monitor market conditions to address future risks.

[1] Note that from 2010 into 2012, the model indicated that gold was overvalued. This was likely due to the market overestimating the degree of balance sheet expansion.