Author: Amanda Ahne

Daily Comment (February 28, 2025)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Good morning! Markets are reacting to the latest inflation data. In sports, Steph Curry joined Wilt Chamberlain and Elgin Baylor as the only players with 45+ point games on the same date. Today’s Comment explores the factors behind the Fed’s aggressive policy shift, the strategic importance of a US-UK trade agreement, and other market-moving events. Plus, we’ll provide a comprehensive overview of today’s key economic data releases.

Close to Neutral? On Thursday, two Federal Reserve officials offered contrasting perspectives on the tightness of monetary policy, underscoring the persistent uncertainty surrounding the path to the neutral interest rate. Despite their differing views, both officials agreed that the Fed should maintain current interest rates for the time being.

- Cleveland Fed President Beth Hammack has indicated that the Fed’s policy rate is no longer meaningfully “restrictive,” suggesting that the central bank may be approaching its neutral rate — the level at which monetary policy neither stimulates nor constrains economic growth. Her comments mark one of the first signals that some Fed officials are growing comfortable with the idea of concluding the current easing cycle by the end of the year.

- On the same day, Philadelphia Fed President Patrick Harker noted that he believes the current policy rate remains sufficiently restrictive to maintain downward pressure on inflation over the long term. While these remarks do not indicate how many rate cuts he expects for the year, it does suggest that he may not agree that the Fed is close to finishing its easing cycle.

- Although both officials still support keeping rates steady at the upcoming meeting and neither has pushed for a near-term rate hike, the widening divergence in their views highlights a growing hawkish tilt among committee members in recent months. This shift signals that the Fed may be closer to ending its easing cycle than markets initially expected at the start of the year.

- Market expectations have shifted significantly. Before the latest inflation data, Fed futures contracts showed that many participants had largely dismissed the possibility of 50 bps of rate cuts this year. As of now, the likelihood of a rate hike has surpassed that of a cut. Current pricing suggests a 35% probability that rates will remain unchanged by the end of 2025, a 25.2% chance of a 25 bps increase, and a 23.1% chance of a 25 bps cut.

- As we have emphasized over the past few months, the Fed will be closely monitoring inflation data early in the year. The first few months present the best opportunity for the Fed to make progress toward its 2% target, given that inflation readings during this period have historically been elevated compared to their long-term average. While a sudden rate hike is not currently the base case scenario, it remains a potential unexpected headwind for risk assets.

UK Trade Deal: UK Prime Minister Keir Starmer visited Washington this week to discuss strengthening trade ties between the two nations. While no final agreement was announced, both sides expressed a commitment to maintaining positive relations. The potential US-UK trade deal is expected to serve as a benchmark for what allies can achieve when they align closely with US interests.

- Following the discussion, President Trump announced that his administration had begun working on a deal with the UK, which could help both nations avoid being swept into a trade war. The deal was a welcome development for Starmer, as his country has been seeking a breakthrough amid recent budget cuts and unpopular tax reforms. However, it appears that Trump may have a broader strategy in mind.

- The president’s decision to pursue a trade deal with the UK may signal to other countries considering breaking away from the EU that they, too, could negotiate their own agreements with the US. Under current EU rules, individual member states are not permitted to negotiate independent trade deals. Additionally, the president has mentioned that he prefers bilateral trade deals with countries as opposed to multilateral agreements.

- That said, this is not the first time the president has expressed interest in working on a trade deal with the UK. In 2019, his administration was actively negotiating an agreement, but progress stalled due to the pandemic. This time may differ slightly, as the administration appears to have a clearer vision of its objectives. However, it’s important to note that trade agreements typically require years of negotiation to finalize.

- One advantage the UK holds is that it currently runs a trade deficit with the US, meaning — by the President Trump’s metric — it is not exploiting the system. As a result, the UK may become an attractive destination for those seeking to avoid countries that could be negatively impacted by a trade war with the US.

Open AI Strikes Back: The latest version of Open AI’s model has been released, aiming to reassure investors that it remains on track following DeepSeek’s recent breakthrough. This new technology marks a significant shift for the company as it moves away from language learning models (LLMs) that rely on chain-of-reasoning approaches.

- The new GPT-4.5 is different from its predecessor models in that it is able to engage with users more naturally, therefore creating a more improved customer experience. The update is unlikely to create the same level of buzz as GPT-4 did when it was released in 2022, but it does show the focus of AI research has started to shift.

- When the technology was first introduced, it faced criticism for its capability to solve only straightforward problems while struggling with more complex ones. As a result, generative AI models have proven to be valuable tools for experts with a strong grasp of a subject, aiding them in completing tasks more efficiently. However, their unreliability in handling nuanced or intricate challenges has made them less suitable for beginners or those starting from scratch.

- Improvements in these models are expected to enhance AI’s ability to tackle more complex tasks, potentially boosting overall economic productivity. However, this advancement could, over time, undermine worker bargaining power as AI becomes increasingly capable of performing roles traditionally held by humans. Consequently, while the technology holds immense promise, it may also face significant political resistance as its broader societal and economic implications come to the forefront.

China Vows Response: Beijing has responded to President Trump’s threat to raise tariffs on Chinese goods, stating that it will take necessary measures if additional tariffs are imposed. This follows Trump’s announcement of a planned 10% tariff increase on Chinese imports, set to take effect on March 4.

- While Beijing has avoided detailing specific measures, its response signals a readiness to counter US threats. Export growth has been a bright spot for the Chinese economy, providing momentum as it seeks to break out of its current slowdown.

- That said, any response is likely to be measured, as both leaders are expected to meet soon to negotiate a trade agreement, making an aggressive reaction improbable.

Business Cycle Report (February 27, 2025)

by Thomas Wash | PDF

The business cycle has a major impact on financial markets; recessions usually accompany bear markets in equities. The intention of this report is to keep our readers apprised of the potential for recession, updated on a monthly basis. Although it isn’t the final word on our views about recession, it is part of our process in signaling the potential for a downturn.

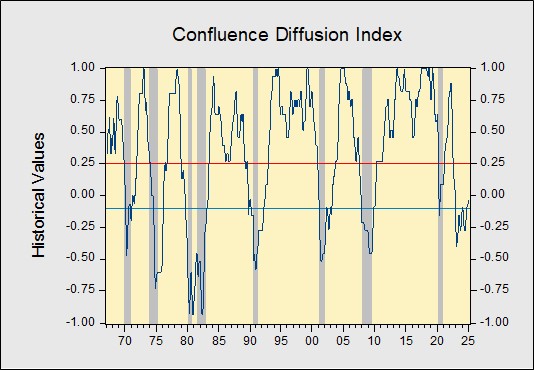

The Confluence Diffusion Index remained above the recovery indicator for the fifth consecutive month. However, the January report showed that five out of 11 benchmarks remain in contraction territory. For January, the diffusion index improved from -0.0909 to -0.0273 and is above the recovery signal of -0.1000.

- Interest rates rose due to renewed inflation fears.

- Manufacturing activity was relatively mixed.

- Labor market conditions showed signs of improvement.

The chart above shows the Confluence Diffusion Index. It uses a three-month moving average of 11 leading indicators to track the state of the business cycle. The red line signals when the business cycle is headed toward a contraction, while the blue line signals when the business cycle is in recovery. The diffusion index currently provides about six months of lead time for a contraction and five months of lead time for recovery. Continue reading for an in-depth understanding of how the indicators are performing. At the end of the report, the Glossary of Charts describes each chart and its measures. In addition, a chart title listed in red indicates that the index is signaling recession.

Daily Comment (February 27, 2025)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Good morning! The market is digesting the president’s recent tariff announcements. In sports news, Real Madrid secured a victory against Real Sociedad in the first leg of their Copa del Rey semifinal clash. Today’s Comment will explore why the trade deficit may not be the Trump administration’s sole concern, analyze the Magnificent 7’s weak start to the year, and cover other market-related developments. As usual, the report will also include a roundup of key international and domestic data releases.

Trump Tariffs: President Trump has pledged to proceed with tariffs on Mexico, Canada, and the European Union starting next week, though he left room for a potential extension that could delay them until April. The announcement sent shockwaves through markets, as uncertainty grows over how far his administration will escalate this global trade war.

- Originally, Trump planned to impose these levies on March 4, proposing a 25% tariff on goods from Mexico and Canada due to concerns that the countries were not taking sufficient actions to curb the flow of fentanyl into the United States. Simultaneously, the EU was targeted over allegations of unfair trade practices, which have placed the US agriculture and automotive industries at a competitive disadvantage.

- That said, his threats have caused some confusion, particularly for Mexico and Canada, as it remains unclear whether they will receive an extension. The president’s team has been evaluating various goods that could potentially be targeted by tariffs, which were also set to take effect on April 2. As a result, the president may consider imposing additional tariffs on Mexican and Canadian goods a month after implementing 25% tariffs, rather than extending the March deadline.

- Regardless of whether tariffs take effect in March or April, the uncertainty surrounding how events will unfold has already contributed to volatile equity markets. The US is expected to start with relatively low tariffs, with the possibility of increasing them if trading partners retaliate. Meanwhile, other countries have been preparing contingency plans in case their goods face tariffs, potentially targeting swing-state economies as part of their response.

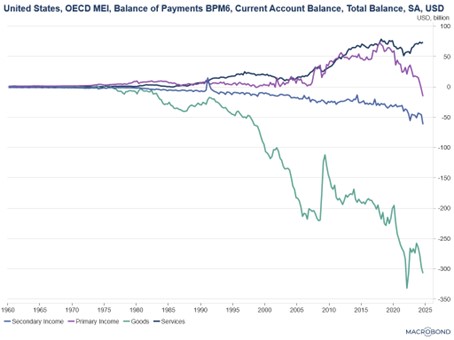

- One key area of focus in analyzing the trade war will be the current account balance. While the US trade deficit has been widely discussed in the media, far less attention has been given to the deficit in primary income. For the first time in recorded history, American residents are earning less on their overseas assets than foreigners are earning on their US assets. This suggests that the US is paying more to the rest of the world in dividend and interest than it is receiving from them in return.

- The concern with having both a trade deficit and a primary income deficit is that it indicates other countries are not only gaining an advantage in trade but also demanding higher returns on their investments. In the long run, this dynamic is unsustainable, as it could lead to a rapid increase in US debt or a currency crisis.

- It is important to note that the president may be using the current account as a scorecard to assess whether the US is being taken advantage of. As a result, the Trump administration’s pressure on the rest of the world could extend beyond trade and potentially into financial flows if these imbalances persist. This could introduce additional uncertainty into equity markets while simultaneously strengthening the case for gold as a safe-haven asset.

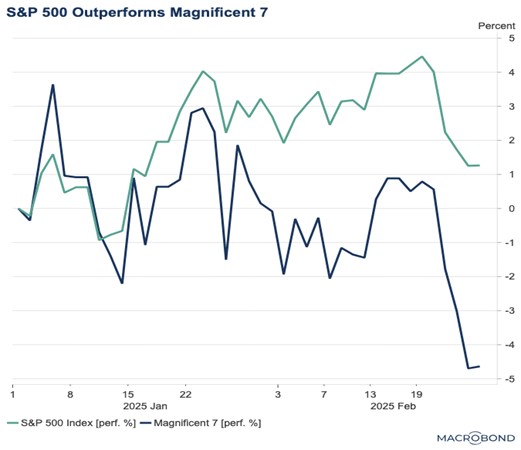

Magnificent 7: Nvidia was unable to provide a boost for the group of seven mega cap tech stocks, which have slipped into correction territory this week. Their collective weak start to the year comes as investors continue to assess the potential of AI and other emerging technologies.

- The chipmaker posted another strong earnings report in the fourth quarter of 2024. The company’s sales surged by 78% in the final three months of the year, reflecting robust demand for its chips. Additionally, it was able to counter concerns that demand for its products was under threat following the release of DeepSeek.

- That said, the strong earnings report failed to excite investors, as the company’s stock price remained relatively flat compared to the previous day, despite rising as much as 3.4% in the lead-up to the announcement. The muted reaction comes as investors have begun rotating away from the Magnificent 7 in favor of other large cap stocks.

- Following two exceptionally strong years in 2023 and 2024, during which the Magnificent 7’s collective stock price nearly tripled the performance of the S&P 500, investors appear to be seeking new leadership. While the Magnificent 7 is down 4.4% year-to-date, the rest of the S&P 500 has gained 4.5% over the same period.

- One of the key uncertainties is whether investors will continue to pressure the companies’ collective capital expenditure (capex) spending, particularly amid growing uncertainty surrounding US policy and geopolitical tensions. As a result, investors may adopt a wait-and-see approach for now, as they assess how these companies navigate emerging challenges.

Taiwan in Danger? Chinese military exercises around Taiwan are growing increasingly assertive, signaling that Beijing may be seriously considering the possibility of an invasion.

- A senior Chinese official responsible for Taiwan relations issued a strong call on Wednesday, urging the island to consider “the inevitable reunification of the motherland.” This bold statement indicates Beijing’s potential for increased action to maintain Taiwan within its orbit.

- This assertive stance, coupled with escalating Chinese military exercises near the island, has fueled concerns of a potential false flag invasion. Furthermore, the severing of undersea cables by Chinese entities has raised fears of hybrid warfare, suggesting a significant escalation in cross-strait tensions.

- While the US has consistently stated its support for Taiwan’s self-governance, President Trump has been reluctant to explicitly promise military defense of the region in the event of an attack by China.

Rubio Russia Pivot: Secretary of State Marco Rubio has warned that the US should not allow Moscow to become a junior partner to China. This strategy, which some have dubbed the “reverse Nixon,” underscores the Trump administration’s willingness to pull Moscow away from Beijing’s influence.

- While the rhetoric may sound appealing, the practicality of this goal appears highly questionable, especially considering Russia’s already heavy economic reliance on China and the growing competition between the US and Moscow over energy markets in Europe.

- That said, the warming of ties between the US and Russia serves as another reminder to the EU that Washington no longer prioritizes its transatlantic relationships. This shift could potentially push Europe to seriously reconsider and accelerate its own defense buildup.

Daily Comment (February 26, 2025)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Good morning! Markets are closely watching the Republican budget bill, as the likelihood of extended tax cuts grows. In sports news, Alex Ovechkin made history by scoring 30 goals in a season for the 19th consecutive year, setting a new NHL record. Today’s commentary will delve into the sharp decline in consumer confidence, provide an update on the ambitious efforts by House Republicans to pass a new budget, and highlight other market-moving developments. As always, it will also include a roundup of key international and domestic data releases.

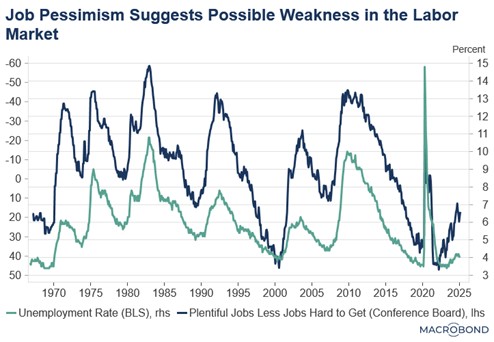

Consumer Sentiment Dips: A sharper-than-anticipated decline in the Conference Board’s Consumer Confidence Index has heightened concerns that the economy may be on the brink of a slowdown. The S&P 500 plunged below 6,000, and the 10-year Treasury yield dropped below 4.30%, as investors sought refuge in bonds.

- The February Consumer Confidence Index dropped sharply from 105.3 to 98.3, marking its largest decline since August 2021. The significant downturn in overall sentiment was primarily driven by growing concerns about the future, as the Expectations Index plunged 9.3 points to 72.9, falling below the critical recession threshold of 80 for the first time since June 2024. Additionally, consumer assessment of the current economic situation also weakened, with the Present Situation Index declining by 3.4 points to 136.5.

- The decline in sentiment was driven mostly by inflation fears. Rising egg prices and the perceived threat of tariffs are key contributors. The Conference Board survey revealed widespread unease about tariff impacts, with both businesses and households expressing heightened concern. Alarmingly, 12-month inflation expectations surged from 5.2% to 6.0%, signaling a growing belief in renewed inflationary pressures.

- Beyond inflation, respondents voiced growing unease about the labor market, particularly in light of recent federal government layoffs. The proportion of respondents saying jobs were “plentiful” dropped from 33.9% to 33.4%, while those reporting jobs as “hard to get” climbed from 14.5% to 16.3%. As a result, the net labor market reading, which measures the difference between “plentiful” and “hard to get” responses, narrowed to 17.1, the lowest level observed since October 2024.

- We believe the recent decline in confidence may partly reflect the initial shock effect of the Trump administration’s policies, particularly around tariffs and layoffs. As markets and consumers adjust to these changes, the negative sentiment could begin to ease in the coming months. However, continued monitoring of economic indicators will be essential to gauge whether this is a temporary dip or the start of a more sustained decline.

The Big Beautiful Bill: House Republicans successfully passed a budget blueprint on Tuesday that paves the way for extending the Trump tax cuts and raising the debt ceiling but is contingent on cuts to the social safety net. However, significant hurdles remain before the proposal can become law. Concerns over its impact on the deficit, coupled with potential revisions in the Senate, pose challenges to its passage.

- The bill passed by a razor-thin margin, 217-215, after last-minute presidential lobbying swayed several moderates. It now heads to the Senate, where it faces further amendments. Republicans aim to use budget reconciliation to extend the tax cuts with a simple majority once the bill is finalized.

- The overall cost of the bill continues to be a significant concern for the incoming administration, which aims to reduce the deficit as a strategy to lower long-term interest rates. According to estimates from the nonpartisan Committee for a Responsible Federal Budget, the new measure would add $2.8 trillion to the deficit by 2034. While this figure is substantial, it represents a notable reduction from the pre-election estimate of $7.5 trillion.

- Most of the projected savings appear to stem from cuts to the social safety net. The budget directs the House Energy and Commerce Committee to identify $880 billion in spending reductions, raising concerns that lawmakers may target Medicaid as a primary area for cuts. Furthermore, the Agriculture Committee has been tasked with reducing $230 billion from food aid programs, specifically the Supplemental Nutrition Assistance Program (SNAP).

- Although the budget resolution offers a nonbinding framework, the combination of tax cuts and a lower-than-anticipated deficit may bolster investor confidence, signaling that the incoming administration is more fiscally disciplined than initially expected. Should lawmakers successfully enact these measures, the resulting stimulus could provide a moderate lift to equities.

Ukraine Agrees to Deal: Officials in Kyiv indicated that Ukraine is prepared to sign an agreement with the US, exchanging access to critical minerals for security assurances. The deal was finalized after Washington withdrew its initial demand for $500 billion worth of mineral resources. However, the agreement does not include any formal, written security guarantees, leaving the specifics of US support unclear.

- The new agreement stipulates that Ukraine will contribute 50% of the proceeds from the “future monetization” of state-owned mineral resources. These funds will also be allocated for investments within Ukraine. However, the agreement excludes mineral resources that directly contribute to the Ukrainian government’s budget, ensuring that the country’s gas and oil companies remain unaffected by the arrangement.

- Ukraine is a resource-rich nation, boasting critical minerals essential for defense technology and electric vehicle production, such as titanium, rare earth elements, cobalt, lithium, and graphite. Access to these resources provides the US with a strong incentive to ensure Ukraine is treated fairly during peace negotiations with Russia.

- The minerals deal will continue to be negotiated by both sides as they work to resolve any disagreements over the specifics of the arrangement. Once finalized, it will require approval from the Ukrainian Parliament before it can take effect. The US, however, does not intend to pursue a formal treaty, as that would necessitate a two-thirds Senate vote, making it politically challenging to achieve.

Joint European Bonds: There is increasing speculation that the EU may turn to the bond market to finance a significant increase in defense spending. This move reflects the region’s growing recognition that it can no longer depend solely on the US for its security.

- This sentiment stems from recent discussions among European leaders regarding the need to enhance the region’s military capabilities. The group of countries is expected to convene on March 6 to develop a bloc-wide defense package, estimated to cost around 500 billion EUR ($524 billion), with the potential for additional funding.

- Additionally, several countries are already planning to increase their defense expenditures. On Tuesday, Irish Finance Minister Paschal Donohoe advocated for higher defense spending at the national level. Meanwhile, in Germany, the likely ruling conservative CDU/CSU party is drafting a bill to approve a 200 billion EUR ($210 billion) special fund for defense spending.

- The decision by European countries to increase defense spending is expected to provide a boost to regional equities, as heightened investment in the sector could stimulate corporate earnings for defense firms. However, this fiscal expansion is also likely to exert upward pressure on bond yields, as governments continue to grapple with the challenge of curbing expenditures in the aftermath of the pandemic.

Daily Comment (February 25, 2025)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment today opens with more evidence of the Trump administration’s revolutionary realignment of US foreign policy, which could have big implications for the US economy and financial markets over the longer term. We next review several other international and US developments with the potential to affect the financial markets today, including news that Trump intends to let his big 25% tariffs against Canada and Mexico take effect next week and an important union vote at US ports today.

United States-Russia-Ukraine-Europe: In the United Nations Security Council yesterday, the US voted with China and Russia to approve a measure calling for a swift end to the war in Ukraine but failing to designate Russia as the aggressor. Earlier, in the UN General Assembly, the US voted with the likes of Russia, Belarus, North Korea, Hungary, and Nicaragua to oppose a resolution condemning Russia for its invasion of Ukraine. Finally, President Trump yesterday said he was negotiating an economic development deal with Russia.

- Yesterday’s moves are the latest examples of how the Trump administration appears to be trying to realign US foreign policy in favor of authoritarian powers long recognized as inimical to US interests, and away from the US’s traditional allies.

- One theory for this is that Trump is trying to pull a “reverse Kissinger,” replicating the former Secretary of State’s strategy in the Cold War to cozy up to China and isolate the Soviet Union. However, China and Russia are no longer at odds as they were in the 1960s and 1970s, so there is a risk that Russia will simply pocket any concessions it gets from the US, leaving the China/Russia bloc stronger and splitting the US bloc.

- In any case, any realignment of the US toward Russia and other authoritarian states would be a revolution in the country’s foreign policy. As we’ve noted before, another important risk is that the move could split the US from Western Europe and make the Continent vulnerable to Russian aggression, which would ultimately constrict US economic opportunities and probably undermine US financial markets in the longer term.

United States-Canada-Mexico: President Trump today reportedly said that his 25% tariffs on Canadian and Mexican imports would be put into place as scheduled next week, although at least one administration insider has said the decision isn’t yet final. While the tariffs have been paused for the last month to allow for negotiations, we have seen no details on how the talks proceeded or if they in fact took place. In any case, the big tariffs will be a test case to see how broad duties against whole countries will affect the exporting economies and the US.

United States-Iran: As part of its renewed “maximum pressure” campaign to weaken Iran, the Trump administration yesterday imposed new, targeted sanctions on more than 30 individuals, entities, and ships associated with Iran’s “shadow fleet” for exporting oil. The aim of the new sanctions is reportedly to reduce China’s ability to import cheap Iranian crude. As background, our Bi-Weekly Geopolitical Report for February 24 provides an overview of US sanctions and the risks they create for investors.

Eurozone: Bundesbank President Joachim Nagel, who sits on the board of the European Central Bank, today said the ECB can continue to cut interest rates as consumer price inflation falls towards the policymakers’ 2% target, but since price pressures are proving stickier than expected, it should be cautious and not cut too fast. Separately, ECB executive board member Isabel Schnabel said in a speech that estimates for the neutral rate had moved up recently, and that higher rates were more likely in future.

- The statements by Nagel and Schnabel suggest the ECB’s rate cuts going forward may be slower than investors anticipate.

- The statements have given a modest boost to the euro (EUR) so far today, pushing it up 0.3% to $1.0495.

Germany: While Friedrich Merz, leader of the center-right CDU/CSU party, starts working to form a coalition government with the center-left SPD after Sunday’s elections, he reportedly is mulling a maneuver for the current parliament to ease the constitution’s “debt brake” before the resurgent far-right and far-left parties can be seated for the new parliament. Easing the debt limits is widely seen as necessary for Germany to ramp up its defense spending to counter potential Russian aggression and to boost public investment to support economic growth.

United Kingdom: Setting the stage for his trip to Washington to meet President Trump on Thursday, Prime Minister Starmer announced in parliament that his government will boost the UK’s defense budget from 2.3% of gross domestic product now to 2.5% in 2027 and 3.0% in the longer term. The hike in defense spending responds to both pressure from Trump and the growing threat from Russia. As such, the move exemplifies the rise in general European defense spending, which has ignited European defense stocks over the last couple of years.

China-Taiwan: The Taiwanese coast guard today caught a Chinese freighter in the act of dragging its anchor and cutting a subsea communications cable off the island’s west coast. The incident is the latest example of suspected Chinese and Russian “grey zone” warfare against US allies’ subsea infrastructure. The Taiwanese have reportedly detained the ship, risking increased tensions with Beijing.

South Korea: The Bank of Korea today cut its benchmark short-term interest rate by 25 basis points to 2.75%, as widely expected. The central bank also cut its forecast of 2025 gross domestic product growth to just 1.5% from 1.9% previously, as the economy softens amid uncertainty surrounding President Yoon’s impeachment trial. The country’s growth in recent quarters has also suffered from weak demand in China, but improved prospects there have strengthened the won (KRW) so far this year, including today.

Global Energy Market: In its annual outlook, energy giant Shell predicted that global demand for liquified natural gas in 2040 will be 60% higher than today, up from a 50% jump projected last year. The upward revision stems from expectations for faster economic growth in China and India, increased demand for energy-intensive computing, and continued corporate efforts to cut greenhouse emissions. If correct, the forecasts bode well for further development in the US energy sector, which has become a powerhouse LNG exporter.

US Labor Market: Unionized workers at ports on the East and West coasts will vote today on a new six-year labor contract that includes a total 62% pay hike and limits on automation. The contract is widely expected to be approved, precluding any further strikes or other labor actions at the ports until 2030. Despite the hefty pay hike and automation limits, reports say some port operators are comfortable with the automation investments that they will be allowed under the deal.

Bi-Weekly Geopolitical Report – Sanctions as an Investment Risk (February 24, 2025)

by Patrick Fearon-Hernandez, CFA | PDF

In the last two decades, the United States has dramatically increased its use of international economic and financial sanctions to stop or deter behaviors at odds with US national security or foreign policy. The Treasury Department has estimated that the US had such sanctions on over 9,400 individuals, entities, and countries as of 2021, and that number has surely grown since then.

In the new Trump administration, it appears that tariffs and other trade measures may be the preferred tools of power, but we still think US investors should keep an eye on the risks they face if their stock or bond holdings become subject to sanctions by the US or some other country. In this report, we describe the key types of sanctions, identify which sanctions may be most problematic for US investors, and discuss the challenges in predicting whether sanctions might be imposed against a particular country, entity, or individual. To wrap up, we provide a sample tool to keep track of sanctions risks and discuss the implications for investment strategy.

Don’t miss our accompanying podcasts, available on our website and most podcast platforms: Apple | Spotify

Bi-Weekly Geopolitical Podcast – #61 “Sanctions as an Investment Risk” (Posted 2/24/25)

Daily Comment (February 24, 2025)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment today opens with yesterday’s parliamentary elections in Germany, which will make center-right politician Friedrich Merz the country’s new chancellor. We next review several other international and US developments with the potential to affect the financial markets today, including a US proposal to slap big new fees on Chinese shipping firms and Chinese-built ships accessing US ports and what appears to be a new effort by the Trump administration to cull the federal workforce.

Germany: In national elections yesterday, the center-right CDU/CSU party came in first with about 29% of the vote, putting leader Friedrich Merz in position to become chancellor if he can cobble together a coalition. The far-right Alternative for Germany came in second with about 21%, but because of its controversial positions, Merz is more likely to form a coalition with the outgoing center-left SPD, whose support fell below 17%. The environmentalist Greens garnered about 11%.

- Merz has vowed to reignite economic growth by rolling back Germany’s tough environmental and climate-stabilization regulations and cutting taxes, but the SPD may resist that effort. Even if Merz can cut Germany’s environmental regulations and taxes, the economy would still face challenges from issues such as high energy costs, poor demographics, tough competition from China, and legal limits to fiscal spending.

- More broadly, a Merz government is likely to be much more aggressive in European policymaking. As we will note below, Merz has also strongly pushed for Europeans to stop trusting the US to support their national security, arguing instead for Europe and Germany to build their own military capabilities (and this from a country whose militarism arguably led to two world wars).

United States-Germany: In a Friday interview ahead of Germany’s elections, Merz warned that Europeans shouldn’t trust President Trump to live up to the US’s mutual defense commitments under the North Atlantic Treaty Organization. Rather, Merz said European nations need to prepare to defend themselves against Russian aggression, perhaps by developing and broadening their own nuclear weapons strategy.

- The statement by Merz shows how the US’s new embrace of revanchist, authoritarian Russia, and its threats to abandon Western European democracies, have made the US geopolitical and economic bloc more fragile.

- The US’s new pro-Russia stance is often excused as a mere negotiating tactic to force the Europeans into taking greater responsibility for their own defense. However, the risk is that European leaders might lose so much trust in the US that they go their own way, potentially with countries such as Germany, Poland, and the Baltics developing their own nuclear weapons.

- The increased fragility of the US bloc can be seen using the scoring methodology we use to categorize countries into the US bloc, the China bloc, or several intermediate blocs. Based on 13 criteria ranging from trade relationships to military alliances, our method assigns each country a score ranging from +12 (for countries adhering to the US) to -12 (for countries adhering to China).

- If we eliminate all scoring for NATO membership (reflecting the alliance breaking up) and assume that tariffs and other protectionist moves eliminate all the US’s bilateral trade deficits, our method suggests only a handful of countries would leave the US bloc outright. However, the average score for the US bloc would fall from 4.70 to 3.75, suggesting weaker ties. (The average score for the China bloc would be little changed, going from -3.11 to -3.08.)

United States-Poland: After a meeting between President Trump and Polish President Duda on Saturday, the White House said it “reaffirmed” the US-Polish alliance and Duda said there was “no fear that the American presence in Poland will decrease.” However, given that the meeting was downgraded to just 10 minutes after Trump arrived late, and given that neither side detailed a firm US commitment to keeping troops in Poland, the positive comments may not ease European concerns that Trump will further reduce the US military presence in the region.

Russia-Ukraine War: Ahead of today’s three-year anniversary of the start of Russia’s invasion, Ukrainian President Zelensky yesterday offered to resign if necessary to secure Western security guarantees and ensure long-term peace for his country. The statement came as US officials claimed they were closing in on a deal in which the US would get a stake in Ukraine’s natural resources and infrastructure in return for its past support of Kyiv. However, Ukrainian officials were less positive, saying they still needed to see changes in the deal.

United Kingdom-India: The UK’s center-left Labour Party government today is launching a renewed effort to strike a free-trade deal with India. The two sides have already agreed on several key issues, but they are still at odds on a number of points, including reciprocal tariffs and short-term employment rights for Indians in the UK. If a deal is ultimately reached, it could boost trade and investment opportunities for both counties.

China: The government earlier this month said it would allow 10 of the country’s top insurers to invest up to 1% of their assets in gold as a way to improve their portfolio diversification. The move could create a significant new source of demand for the yellow metal, on top of today’s strong buying by central banks and the recent safe-haven buying related to US policy changes. We remain positive on the outlook for gold prices even as they stand near record highs.

US-China Investment: President Trump on Saturday signed a new executive order directing the federal government to “use all necessary legal instruments” to block Chinese investments in US “technology, critical infrastructure, healthcare, agriculture, energy, raw materials or other strategic sectors.” The order also called for applying new legal tools to stop US citizens from investing in China’s defense industrial sector. The Chinese government quickly vowed retaliatory measures “to defend its legitimate rights and interests.”

- The new order expands the investing bans already put in place by Trump in his first term and by President Biden in his.

- The previous bans focused on cross-border investments related to technology and defense. By broadening the bans far beyond those sectors, the new order has the potential to sharply accelerate the decoupling of the US and Chinese economies.

US-China Trade: The US Trade Representative on Friday proposed massive new fees on Chinese shipping firms and Chinese-built ships accessing US ports. The proposal is open to public comments until a March 24 hearing, when the Trump administration will decide whether to go ahead with the fees.

- The proposed fees are the result of a US probe launched last year that found China engages in unfair trade practices in the maritime, logistics, and shipbuilding sectors.

- Together with the new US-China investment restrictions mentioned above, the shipping fees suggest the administration is ratcheting up its pressure on China despite initially seeming to be softer than expected on Beijing.

United States-Japan-South Korea-Taiwan: New reports say the Trump administration is pushing Japan, South Korea, and Taiwan to ramp up their purchases of liquified natural gas from the US. According to the sources, the administration is also pushing the Asian allies to invest in new LNG export facilities on the US West Coast, including a $44-billion project in Alaska that some observers believe is uneconomic because of high costs. The administration is reportedly using its tariff threats as a cudgel to push the allies toward a deal.

- As we’ve noted before, the administration’s evolving trade policy is largely geared toward eliminating the US trade deficit, if not to generate large trade surpluses. Energy and other commodity exports are expected to be a big part of any such rebalancing.

- The reports say the administration is arguing to the allies that greater reliance on LNG from the US would help insulate them from Chinese and Russian geopolitical pressure. According to the reports, the administration also hopes that making the allies more dependent on the US will force them to bow to Washington’s policy goals.

- However, as we noted in our Bi-Weekly Geopolitical Report from January 27 and in our discussion above, there is a risk in employing sharp threats and saddling the allies with big, new economic burdens, such as potentially uneconomic energy purchases or investments. Even if the tactics make the allies more dependent on US energy, resentment over the cudgeling to get there and the high costs involved may make the alliances more fragile.

US Fiscal Policy: At the apparent urging of Elon Musk, the Office of Personnel Management over the weekend sent an email to legions of federal workers directing them to reply with approximately five bullet points saying what they accomplished over the previous week. Even though the emails didn’t include Musk’s warning on X that anyone who didn’t reply would be out of a job, and even though some agency chiefs told their employees not to respond, the move has reportedly further rattled federal workers.

- Since many federal workers have already been laid off, and since Musk has aggressively pressed several other tactics to push employees out of their jobs, the new move is nearly certain to prompt more federal contractors, workers, and those who depend on them to rein in their spending and prepare for the worst.

- Incoming analyses suggest the $55 billion or more in spending cuts that Musk has claimed for his Department of Government Efficiency, so far, are highly inflated. Nevertheless, substantial cuts have occurred, and given that federal workers are distributed widely throughout the country, consumer spending and investment could be affected nationwide, raising the risk of an economic slowdown.

US Industrial Policy: Apple today said that it will invest more than $500 billion in the US over the next four years to expand its domestic footprint in research and development, engineering, software development, and manufacturing. According to Apple, the investment will create about 20,000 new jobs, including a major new factory for artificial-intelligence servers in Houston. The news suggests that the cajoling of President Trump is accelerating US re-industrialization, building on the industrial policies of the Biden administration and his own first administration.

US Stock Market: In his annual letter to shareholders on Saturday, famed Berkshire Hathaway CEO Warren Buffet assured investors that the firm hasn’t changed its management approach and is still looking to use its $321-billion cash pile to buy equities. However, he suggested that rich valuations are the main obstacle to doing so, saying, “Often, nothing looks very compelling.” The statement is consistent with the high valuations we see in the market, but we note that momentum could still drive stock prices higher.