[Posted: 9:30 AM EDT] Happy employment day! The employment data is covered in detail below but the snapshot of the data is supportive. Payrolls rose 222k compared to forecasts of 178k; we also saw a 47k upward revision, making the report robust. The unemployment rate came in at 4.4% versus expectations of 4.3%, mostly due to a rise in the labor force and increased participation. Wage growth remains sluggish at 2.5%.

There is not much new to report on the G-20. We expect a contentious meeting where the differences between the emerging American policy of exiting the hegemonic role collide with the rest of the world’s terror at realizing the U.S. world order of the past 72 years is coming to a close. It should be noted that this retreat has been underway since 2008 and President Trump is merely making the case more clearly, but the American public, painfully aware of the costs of hegemony but inured to the benefits, has simply had enough of supporting the world. We note that Japan and the EU have apparently negotiated a new trade deal. This will be interesting to watch—how does a trade deal work between two parties that are running export-promoting policies? In addition, trade rests on the U.S. providing global security. Who will guarantee the sea lanes between Japan and Europe? China? Overall, we don’t expect much out of the G-20 other than clarity that the world is changing rapidly.

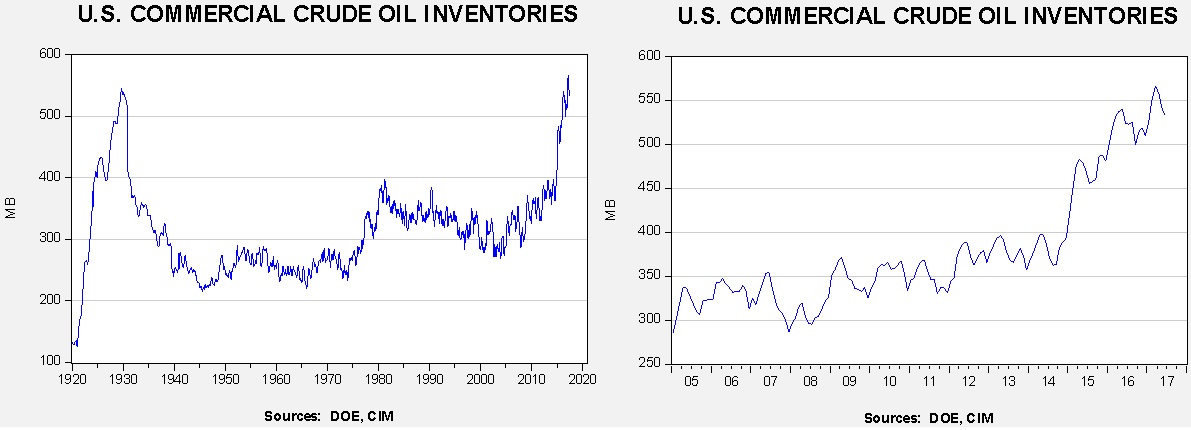

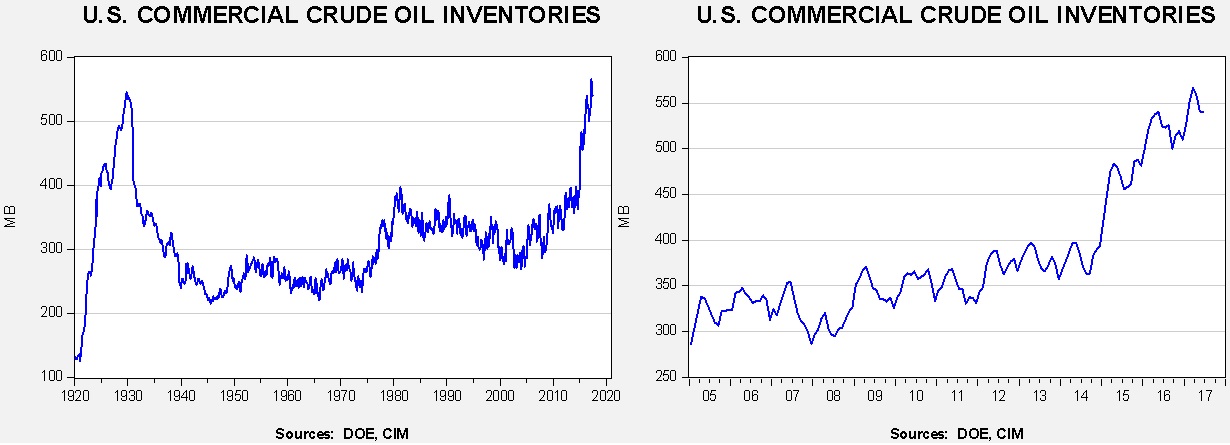

U.S. crude oil inventories fell 6.3 mb compared to market expectations of a 2.5 mb draw.

This chart shows current crude oil inventories, both over the long term and the last decade. We have added the estimated level of lease stocks to maintain the consistency of the data. As the chart shows, inventories remain historically high but they are declining. We also note that, as part of an Obama era agreement, there was a 1.4 mb sale of oil out of the Strategic Petroleum Reserve. This is part of a $375.4 mm sale (or 17.0 mb) done, in part, to pay for modernization of the SPR facilities. We note that sales have reached 13.1 mb this year, which likely means we should see these sales end in the coming weeks. International agreements require that OECD nations hold 90 days of imports in storage. Due to falling imports, the current coverage is near 140 days. Taking that into account, the draw would have been 6.7 mb, which is an even more impressive draw.

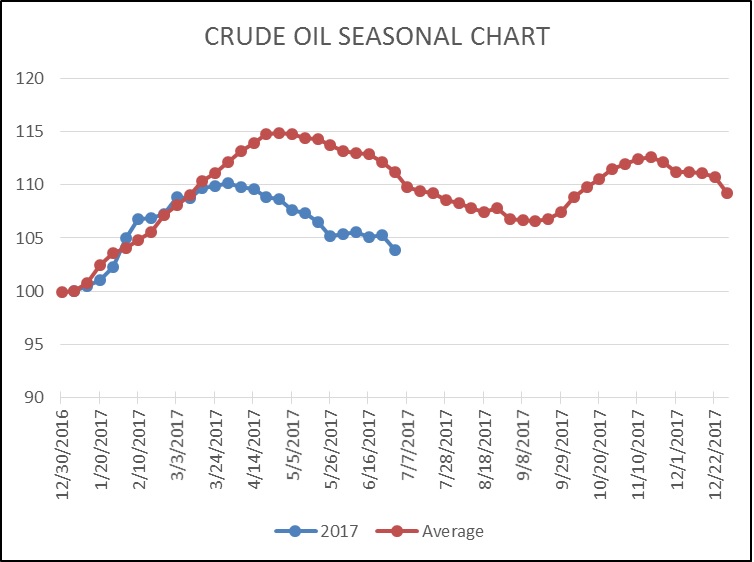

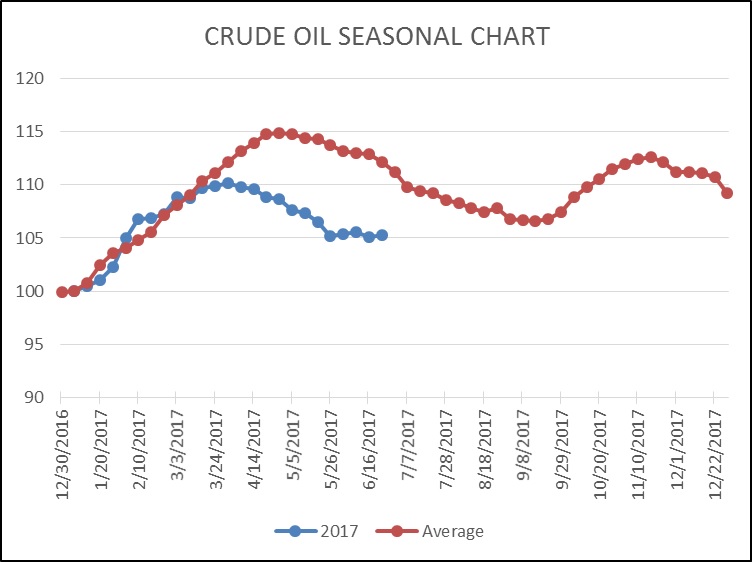

As the seasonal chart below shows, inventories are usually well into the seasonal withdrawal period. This week we saw an acceleration in the decline. Some of this was likely due to weather disruptions caused by Hurricane Cindy. Still, we have already seen a larger than normal seasonal decline and the seasonal trough isn’t usually hit until mid-September. Thus, we should see further stock withdrawals over the next couple of months.

(Source: DOE, CIM)

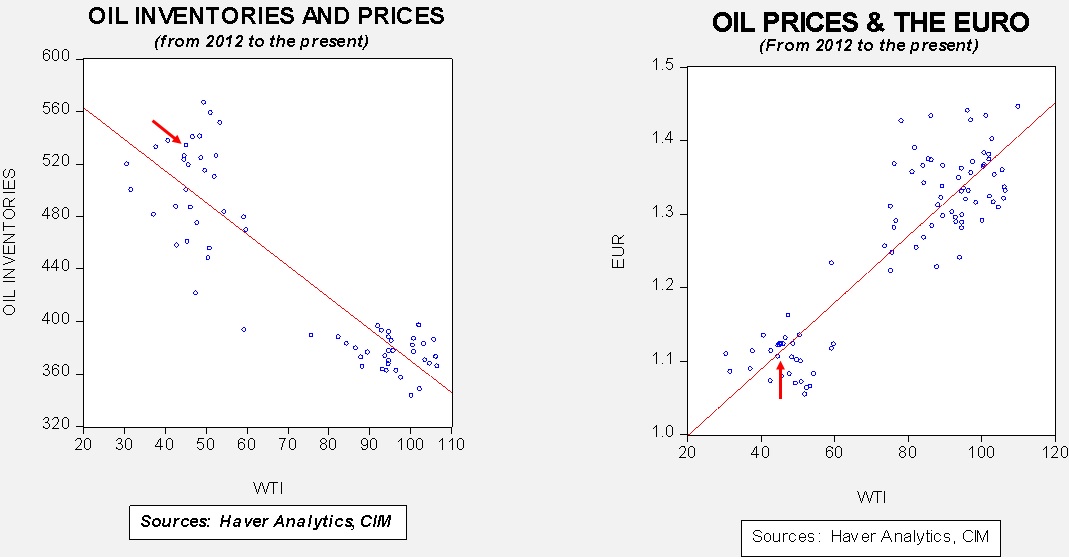

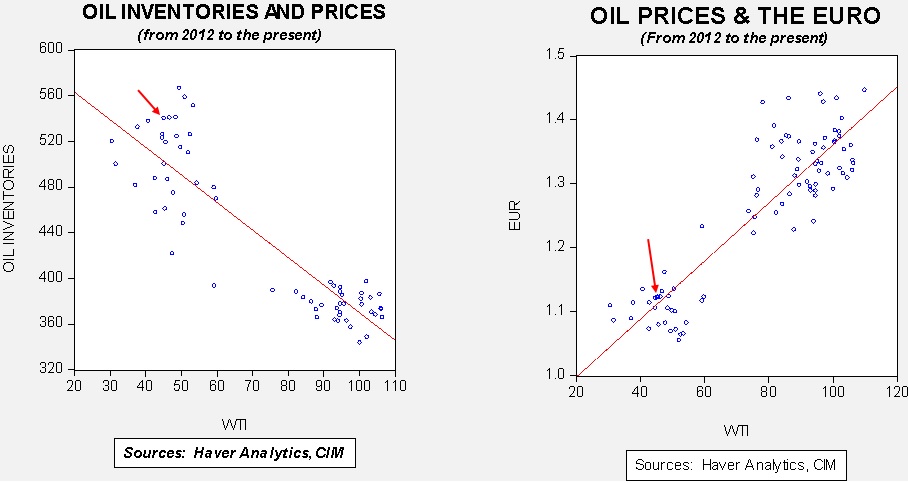

Based on inventories alone, oil prices are overvalued with the fair value price of $40.27. Meanwhile, the EUR/WTI model generates a fair value of $52.55. Together (which is a more sound methodology), fair value is $48.61, meaning that current prices are well below fair value. Currently, prices are below our expected trading range; we view oil prices as attractive on a short-term trading basis. Yesterday’s DOE data was bullish. The drop in prices is therefore a worry because markets that fail to positively react to bullish data usually face further selling. We do expect oil prices to rise in the coming weeks, simply because the fundamentals are supportive.

[Posted: 9:30 AM EDT] It’s a fairly quiet morning, typical of mid-summer. Here are the issues we are watching:

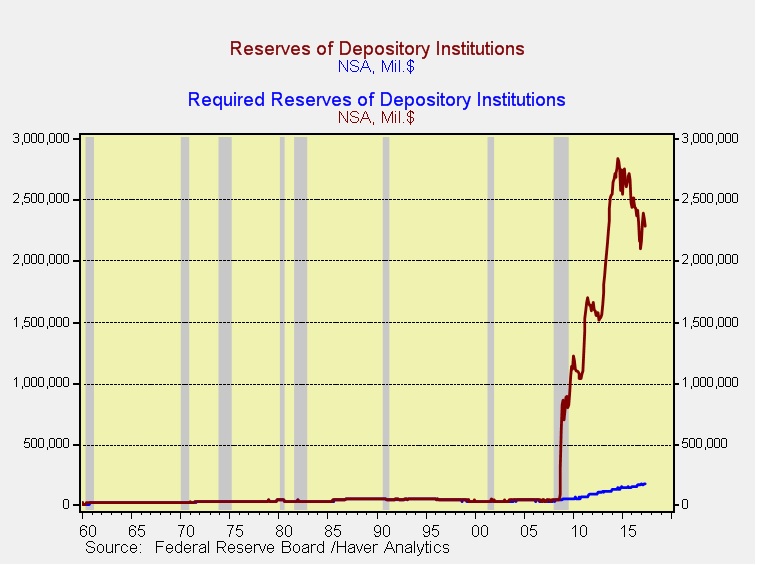

Fed minutes: Most of the media recaps focused on the reduction of the balance sheet. As we have noted in the past, in theory, this action shouldn’t be a big deal. Most of QE ended up sitting harmlessly in the banks as excess reserves. Simply put, the funds from QE were injected into the banking system and then simply sat. Thus, taking them away shouldn’t have much of an impact.

As this chart shows, excess reserves are almost 13x more than required reserves. Since tapering began, the level of excess reserves has started to decline but still remains high. Therefore, removing some of these reserves probably won’t prevent loans from being given.

The bigger concern is the psychological impact of shrinking the balance sheet.

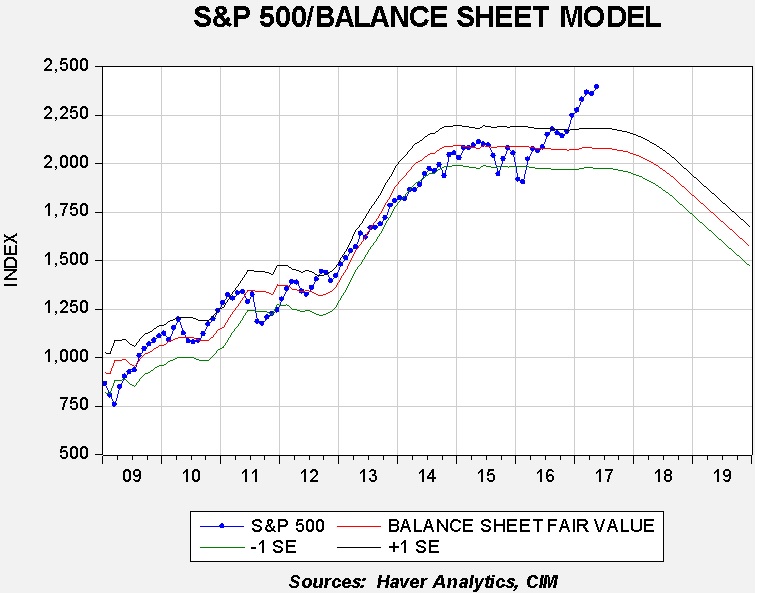

This is a chart we have shown for a while with a new twist; we assume the Fed will begin its process of reducing the balance sheet in September and follow the plans previously released. Obviously, if the balance sheet affected equity markets in a mechanical fashion, a bear market is looming. We don’t think this is the case. We believe that the impact of QE on equities was to reassure investors that the Fed wasn’t lacking tools to stimulate the economy. If investors are confident about continued economic growth, the impact of balance sheet contraction shouldn’t be a big deal. However, since we have never seen anything like this before, it is difficult to quantify the risk factor.

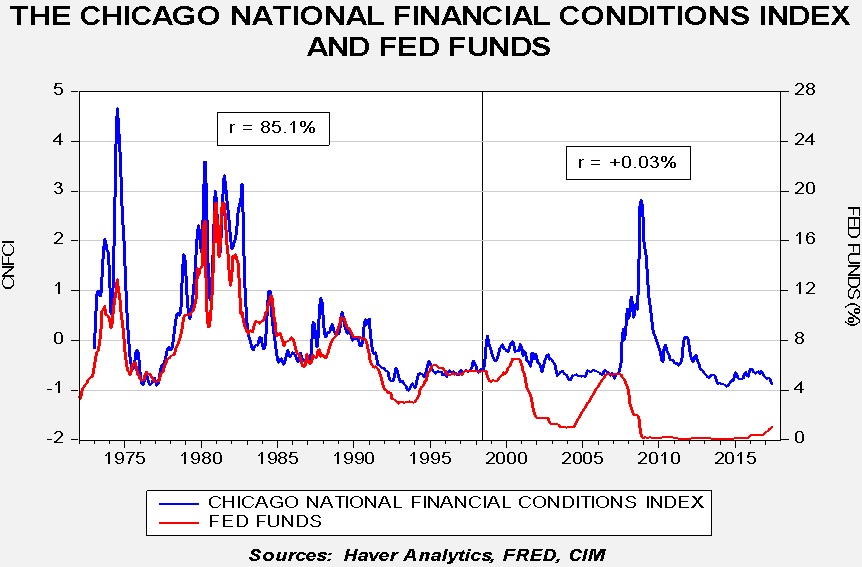

Buried in the minutes were concerns expressed about the “increased risk tolerance” of investors as a reason for tighter policy. As we have noted before, the Fed has lost control of financial conditions. Until the late 1990s, the Fed could affect financial stress via changes in fed funds. That relationship broke down in the late 1990s.

This chart shows the relationship of the Chicago FRB Financial Conditions Index and fed funds. The blue line measures financial stress, with a higher number indicating elevated stress. Note that the two series were tightly correlated from 1973 into 1998. Since then, the two have become almost completely independent. We believe that the primary reason for the breakdown is transparency; from the late 1980s to the present, the Fed has become increasingly transparent and the more the Fed telegraphed its policy actions, the less policy activity affected stress. Thus, when financial conditions deteriorated in 2007-10, the policy rate fell to zero and had to be held there before stress declined. We note that NY FRB President Dudley suggested in a recent speech that the FOMC should be raising rates due to low levels of financial stress. This could be considered a type of “controlled burn” by the Fed. What is interesting is that if the relationship between fed funds and the above stress index had remained consistent since the 1973-98 period, then financial stress would be almost twice as low! Thus, if the FOMC raises rates to lift stress, it will almost certainly overtighten. This says nothing about the policy nightmare the Fed would face if it made the P/E a policy goal.

The takeaway from the minutes is that the FOMC is on a path of policy tightening and risks will rise over time.

The G-20: This promises to be a contentious meeting. Merkel and Trump are not getting along. The presidents of Russia and the U.S. will meet for the first time. There is talk of trade wars over steel tariffs. Given that expectations for this meeting are already low, it is hard to imagine there will be a disappointment. Normally, G-20 meetings are snoozers. We do expect some friction given all the tensions in the world, but the most likely outcome is that the meeting “won’t be that bad,” mostly because our expectations are so depressed.

North Korea: There isn’t much new to report. The UNSC took up the issue yesterday. As expected, Russia and China were reluctant to press hard on North Korea. The U.S. is making military threats but there isn’t much evidence of mobilization. As we have noted before, there are no good outcomes with North Korea.

Employment day tomorrow: Current forecasts call for non-farm payrolls to rise 177k, with an unemployment rate of 4.3% and average hourly earnings rising 2.6%.

[Posted: 9:30 AM EDT] Back to work! Here are the items we are following this morning:

North Korea’s ICBM: Over the holiday, North Korea launched an ICBM that is at least capable of reaching Hawaii and Alaska and could hit much of Asia, along with northern Australia. Although there is no official red line from the Trump administration, an ICBM that could hit the U.S. mainland is probably it. As we discussed recently in our WGR series on North Korea,[1] there really aren’t any good options. The South Korean government has offered a freeze of current technology in return for negotiations. We doubt that will work because Kim Jong-un is convinced that without a deliverable nuke he risks the same fate as Saddam Hussein and Muammar Gaddafi. The U.S. has discussed attacking missile sites pre-launch to ensure that the U.S. would not be hit. However, North Korea has rolled out a solid propellant rocket that can be launched quickly, making that defense questionable. As we noted, if the U.S. decides to go to war, Seoul is in range of North Korea’s massed artillery. So far, the U.S. and South Korea have held joint missile exercises in response. The situation in North Korea is becoming increasingly untenable and the risks of war are rising. Does this mean war is a risk within the next few months? Probably not, although the potential is rising given the pace of escalation. So far, there isn’t clear evidence that North Korea can put a warhead on these missiles but most analysts expect that it’s only a matter of time.

The G-20 begins Friday: President Trump will visit Poland before the G-20 meeting in Germany. Already, Chancellor Merkel has made harsh comments about Trump’s policies; this could prove to be a frosty meeting, at least with the Europeans. The president is also expected to meet with Russian President Putin. We doubt anything comes of it, although there is great concern about the meeting in the media. Rarely do important decisions get made in brief meetings.

Qatar facing further isolation? The GCC nations are considering expelling Qatar from the group. The GCC made a list of demands to Qatar which it describes as “non-negotiable.” The problem is that the more the GCC isolates Qatar, the more it will align with Turkey and perhaps even Iran. The Trump administration remains divided on this issue, with SOS Tillerson calling for meetings and restraint while President Trump appears to be cheering on the GCC. We expect this standoff to continue; if it escalates to military action, regional stability could be at risk.

Russia says “nyet” to further cuts: Oil prices are weaker this morning after Russia indicated it would not support additional supply cuts. This isn’t really a surprise. If further cuts are coming, the Saudis will have to bear the loss of market share. We continue to hold that oil prices are in a trading range; we are up from the bottom of the range but expect choppy markets as prices approach the high $40s.

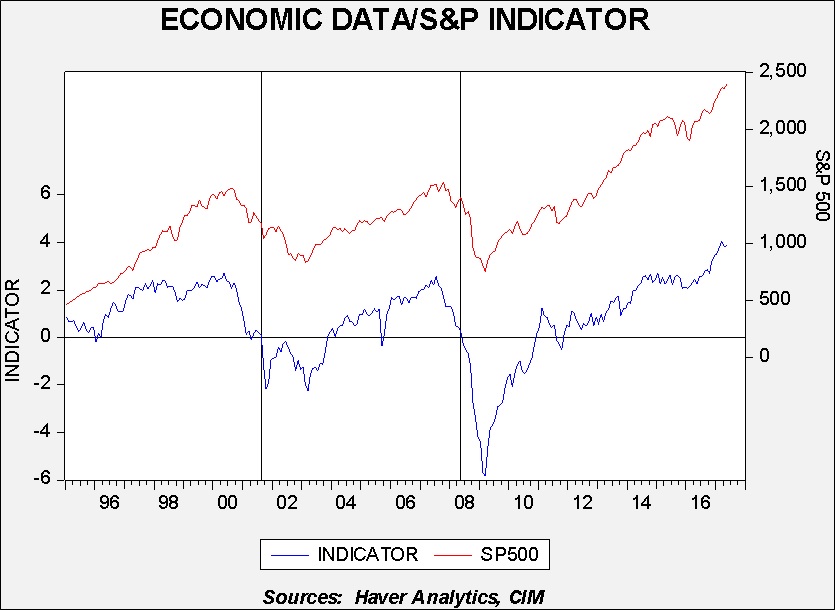

For equity investors, there is always a concern about the major market declines; being able to reduce market exposure prior to crashes like the ones in 2000 or 2008 is always desirable. Although large declines have occurred outside of economic recessions, they have become increasingly rare. The last major market pullback absent a recession was the 1987 crash. Thus, an indicator that can use high frequency economic data (data that is available on a weekly basis) and relate it to equities should have some value.

This chart shows one of our recent efforts. The upper line is the monthly average for the S&P 500; the lower line is an indicator built of three economic numbers—initial claims, the CRB commodity index and the Conference Board’s Consumer Confidence data. We have standardized[1] the economic data and created an indicator, shown on the bottom of the graph. In general, a positive reading is generally bullish for equities. We have placed vertical lines on the chart to indicate when the indicator turned negative with persistence. These are usually periods of falling equities.

Although useful, it is clear that the indicator is somewhat “late” in that the equity decline is well underway by the time it becomes negative. That would suggest that a momentum number based off the economic indicator might be helpful.

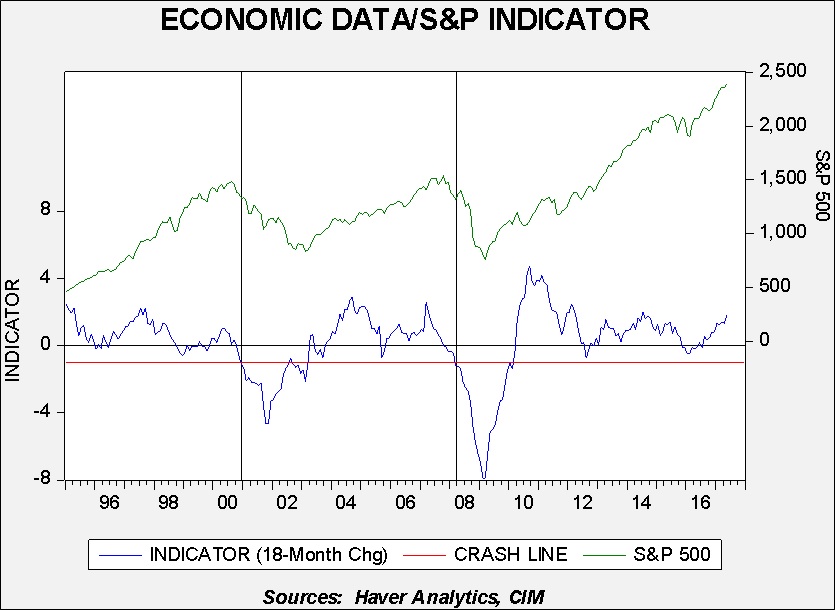

To achieve this, we calculated the 18-month change in the above indicator and set a “crash line” at -1.0. The adjustment improves the indicator’s value, indicating an investor should reduce equity exposure sooner than the unchanged index would suggest. At the same time, using a -1.0 reading eliminated the false exit signals.

There is an element of “data mining” here and we would not recommend using this indicator as a “precision instrument.” However, it does show that these three standardized data points are fairly good coincident indicators of the economy and, using an 18-month change and a filter, do offer reasonably good warnings when one should reduce exposure and when a market pullback is a mere correction.

We use the period since 1997 because it makes the data easier to observe. But, we did look at data from 1980 and the performance is similar. As we would expect, the indicator did not help at all during the 1987 crash, confirming that its usefulness is as a gauge of the interaction between equities and the economy, not as a pure market indicator.

What is it telling us now? The economy is doing well enough that market declines will probably not be more than normal pullbacks. Of course, this sort of indicator won’t necessarily be helpful if a geopolitical event triggers a major market decline. But, the most common cause of bear markets in equities are recessions. For now, that doesn’t appear to be on the horizon.

[1] Standardizing entails subtracting the raw data by its average and dividing by its standard deviation. The resulting number is then adjusted by how far it is from average and how far it is from its normal deviation. Standardizing allows one to combine unlike indicators and essentially balance their relative effect. In this case, the formula is Indicator = (standardized CRB + standardized Consumer Confidence) – standardized Initial Claims. We subtract the claims data because lower claims indicates a stronger economy. Subtracting that number thus allows the indicator to rise when economic data are improving and vice versa.

[Posted: 9:30 AM EDT] N.B. Due to the upcoming Independence Day holiday, the next issue of the Daily Comment will be published on July 5th. We want to wish you a happy and safe holiday!

We expect a quiet trade today; it’s a summer Friday, there’s a holiday looming, Canada is off today for Canada Day (Happy 150th!) and markets have been rather choppy recently. A pause to consolidate makes sense. The key issue we are seeing is a rapid shift in policy expectations. Although the Fed has been on a tightening path for some time (arguably since the onset of tapering), it appears the ECB, BOE and BOC are in the process of either ending stimulus or beginning to tighten. Tight policy almost everywhere (the BOJ being the last holdout) hasn’t been a feature in the financial markets since 2007. Thus, some concern is probably warranted. However, as we note in this week’s AAW (see below), economic conditions generally would not indicate that a major selloff is in the offing. Thus, if one occurs, it will probably come from something other than the economy.

Other news items of note:

A trade war brewing? President Trump ran a campaign promising to restrict trade to boost U.S. growth and jobs. According to Mike Allen at Axios,[1] the vast majority of Trump’s cabinet opposed deploying steel tariffs. The report puts the vote at 22-3. However, Trump was one of the three, thus the plan is expected to move forward. Tariffs on steel could hit 20% and the report suggests that other items, including aluminum, semiconductors, paper and appliances, could be next. Trade wars are tricky; it’s hard to avoid self-inflicted wounds. Raising the price of steel will adversely affect consumers (automakers, for example) and bring inflation. And, depending on the price elasticity, it can actually reduce demand to the point where domestic steel producers could be harmed. For example, if the price rises to the point where automakers reduce their steel consumption and substitute carbon fiber or plastic, all could be worse off. In addition, retaliation is always possible. If the U.S. hits Chinese steel exports with a tariff, expect China to hit American exports to China, such as agriculture products. This could get quite interesting.

Rising tensions with China: The issues with China are really a string of tit-for-tat headlines. The U.S. has approved a $1.4 bn arms sale to Taiwan.[2] China is building new military facilities in the South China Sea islands.[3] The U.S. has cut off China’s Bank of Dandong from the U.S. financial system over ties to North Korea.[4] The bank is rather small but the move is likely designed to send a clear signal to other Chinese banks about their business dealings with North Korea. It is becoming apparent that the warm ties from earlier meetings between President Trump and Chairman Xi have dissipated.

The G-20: The world group meets next week but already it looks like it will generate lots of news. Yesterday, we noted that Chancellor Merkel, the host of this gathering, will strongly oppose protectionism and isolationism and made no attempt to veil her displeasure with the U.S. President Trump announced yesterday he will meet with Russian President Putin; there are reports the administration intends to surround Trump with staff to avoid any compromising images from developing. These meetings are usually non-events, but this one may be full of “fireworks.”

[Posted: 9:30 AM EDT] Here are some of the items we are tracking this morning:

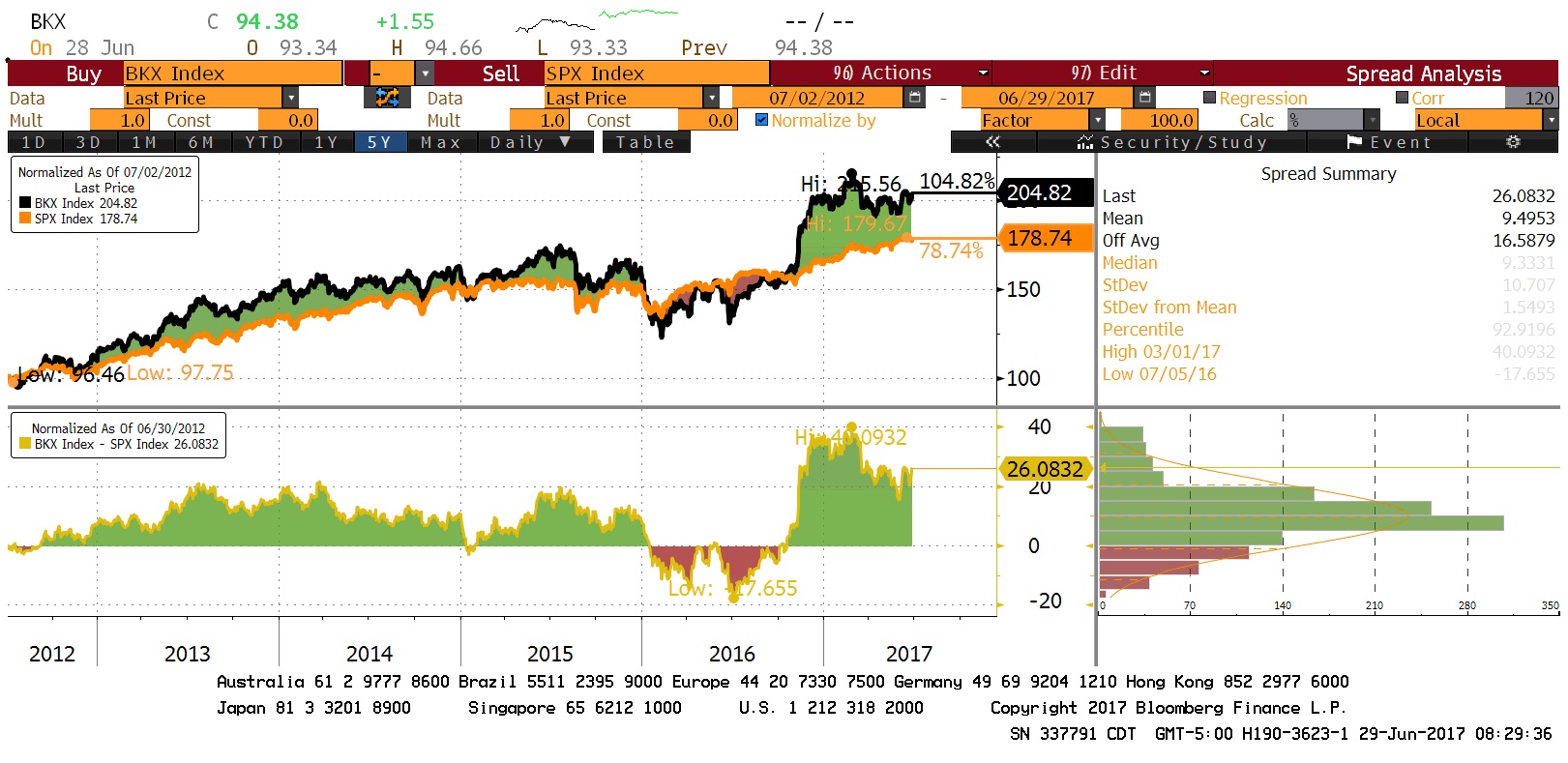

Fed stress tests give banks a green light: The banks performed well on the Federal Reserve stress tests, opening the sector to increasing dividends and stock buybacks. Bank stocks lifted the broader indices yesterday and this trend will likely continue.

(Source: Bloomberg)

This chart shows the KBW Bank Index relative to the S&P 500. Note that bank stocks jumped after the elections but have been consolidating for the past couple of months. The stress test results will likely lead to another leg higher in these equities.

On the other hand, central banks are turning hawkish: In central bank meetings in Portugal, ECB officials hinted that tapering of their QE is in the offing, while the BOC and BOE both indicated that policy is set to tighten. This policy change is significant because the equity bull market that began in March 2009 has enjoyed the backdrop of supportive monetary policy. We are starting to see a backup in long duration Treasury yields (which is actually bullish for banks) and the dollar is weakening as other central banks signal a withdrawal of stimulus. We are probably embarking on a new phase in this cycle that carries new risks. Although policy tightening doesn’t necessarily signal the bull market is in trouble, policy will likely become a headwind in the near future and will no longer be a tailwind.

The South Korean president visits: Moon Jae-in visits the White House today amid reports[1] that the U.S. is preparing contingency plans that include military action if North Korea shows it has built a nuclear warhead[2] and/or has created an ICBM that can reach the U.S. mainland. As we have recently discussed, a war on the Korean peninsula would be, to quote SOD Mattis, “catastrophic.”[3] Moon will likely try to buy time because, in a war, his capital will be a primary target for North Korea’s massed artillery.

The fate of the former crown prince: The NYT reports[4] that the recently demoted Prince Mohammed bin Nayef is under house arrest, confined to his palace. This report has been denied by the kingdom but the story is being widely reported in the regional media; the Iranian news agency FARS reports [5] that five other Saudi princes are also being confined to quarters. Although none of this is definitive, if true, it would suggest that King Salman’s decision to elevate his son to crown prince has caused consternation among the royal family. If this conflict escalates, it would be a potentially bullish event for crude oil because we doubt unrest will be contained in the kingdom.

Kurdish and Turkish forces fired on each other: There are reports that Kurdish YPG militias, one of the most effective fighting forces against IS, have also been engaging in skirmishes with Turkish forces.[6] Turkey fears Kurdish nationalism because it could undermine the territorial integrity of Turkey itself. The Kurds are considered to be the largest ethnic group in the world without a state; they have wanted a Kurdish state for well over a century. One of our worries is that the fall of IS will simply lead to a series of wars as various actors attempt to control swaths of what used to be Iraq and Syria.

A militant Germany: Chancellor Merkel gave a remarkably critical speech today, criticizing the rise of protectionism and weakening international cooperation, laying the blame squarely on President Trump. Her and her country’s discomfort with the change in U.S. policy is completely understandable—Germany prospered under Pax Americana because it no longer had to fear invasion from its neighbors. The U.S. guaranteed it wouldn’t happen. She is also correct that isolationism and protectionism won’t solve the world’s problems; however, if the U.S. has decided it’s getting out of the hegemony business, these positions may not help the world but they just might help the bottom 80% of the American household income distribution. What will become worrisome is if Germany, sensing the vacuum, begins to reassert itself on the regional and world stage. It will raise fears across Europe of the pre-1945 world in which the German problem was the key problem of Europe. America’s hegemonic behavior since WWII has allowed the rest of the world to focus on their own issues and simply follow U.S. foreign policy. Those conditions would change if the U.S. withdraws from the world and Merkel’s comments reflect the unease this change is triggering.

U.S. crude oil inventories rose 0.1 mb compared to market expectations of a 2.3 mb draw.

This chart shows current crude oil inventories, both over the long term and the last decade. We have added the estimated level of lease stocks to maintain the consistency of the data. As the chart shows, inventories remain historically high but they are declining. We also note that, as part of an Obama era agreement, there was a 1.4 mb sale of oil out of the Strategic Petroleum Reserve. This is part of a $375.4 mm sale (or 17.0 mb) done, in part, to pay for modernization of the SPR facilities. We note that sales have reached 12.7 mb this year, which likely means we should see these sales end in the coming weeks. International agreements require that OECD nations hold 90 days of imports in storage. Due to falling imports, the current coverage is near 140 days. Taking that into account, the draw would have been 1.3 mb, which is less than forecast.

As the seasonal chart below shows, inventories are usually well into the seasonal withdrawal period. The typical decline has stalled; although currently below the usual September trough, the slowdown in withdrawals has been a bearish factor for oil prices. If we take the SPR sale into account, the decline has been more in line with normal seasonal withdrawals and therefore we can conclude that the SPR sale has played a role in pushing oil prices lower.

(Source: DOE, CIM)

Based on inventories alone, oil prices are overvalued with the fair value price of $38.30. Meanwhile, the EUR/WTI model generates a fair value of $52.23. Together (which is a more sound methodology), fair value is $47.86, meaning that current prices are well below fair value. Currently, prices are below our expected trading range; we view oil prices as attractive on a short-term trading basis.

[2] A warhead can be placed on a missile, survive launch and re-entry and detonate. A device is a non-deliverable nuclear appliance that can explode and is used for testing and development. So far, North Korea has proved it can do the latter but not the former.

[3] See our recent two-part WGR series on The Second Korean War: Part I, 6/19/17; and Part II, 6/26/17.

[Posted: 9:30 AM EDT] There was quite a bit of news from yesterday through this morning:

ECB tells market “you misunderstand”: Yesterday, ECB President Draghi gave a speech that was taken to suggest that tapering was going to occur because the Eurozone economy is doing better. The EUR rallied and we had a significant rise in long duration yields in Europe and the U.S. The ECB took an unusual step to release a statement this morning indicating that the markets had misinterpreted Draghi’s comments and policy tightening isn’t imminent. The EUR, which was rising this morning, pulled back sharply (U.S. Treasuries have rallied, too). This will be an important test for the markets. If the markets believe that what Draghi said yesterday is true, then the ECB correction this morning should be treated the same way as intervention against the trend; it will be seen as a EUR buying opportunity by traders. If the ECB is successful in changing the narrative, the EUR’s rally and Treasury weakness will stall. We tend to lean toward the former—that the EUR will likely continue to rally and Treasuries, which have been strong, could come under some pressure.

Health care vote gets extended: As the Senate GOP leadership unveiled its health care plan it became rather obvious that the vote would fail. Majority Leader McConnell had previously indicated that a vote, up or down, would be held by July 4th, prior to the recess. In something of a surprise, McConnell has decided to extend the debate on health care, suggesting he really wants a deal. Equity markets didn’t like the shift at all. It appears that equity markets care little about health care reform but are very interested in tax reform. As long as Congress is focusing on health care, taxes are not being addressed and so extending the debate past the recess means that tax reform will be delayed. Even worse, political capital is being depleted on health care that could be used for tax reform. This is why we had the strong drop yesterday.

A coup brewing in Venezuela? A helicopter, which appears to have been commandeered by rogue elements of the military, flew toward Caracas and dropped two hand grenades on the Supreme Court (only one detonated) and then moved to the Interior Ministry building and opened fire on it. There are growing signs that elements of the military want to oust President Maduro and replace him with someone else. It is important to note here that this threat isn’t coming from outside the ruling coalition but from within it. The elements of the military that participated in this action appear to be aligned with the Socialists but are disenchanted with Maduro and are especially incensed by his scheme to change the constitution. Recently, Maduro replaced the head of the country’s Strategic Operational Command, firing Gen. Vladimir Padrino Lopez and replacing him with Adm. Regigio Ceballos Ichaso. Maduro should have a healthy fear of his military. The late Hugo Chavez, being an officer himself, had a certain degree of respect from the military; Maduro, a former bus driver, doesn’t. It should also be recognized that we wouldn’t anticipate a major policy shift if Maduro is replaced. The coup plotters appear to be leftists who simply want a different leader. However, if unrest rises, it could further reduce oil supplies and might be bullish for oil in the short run.

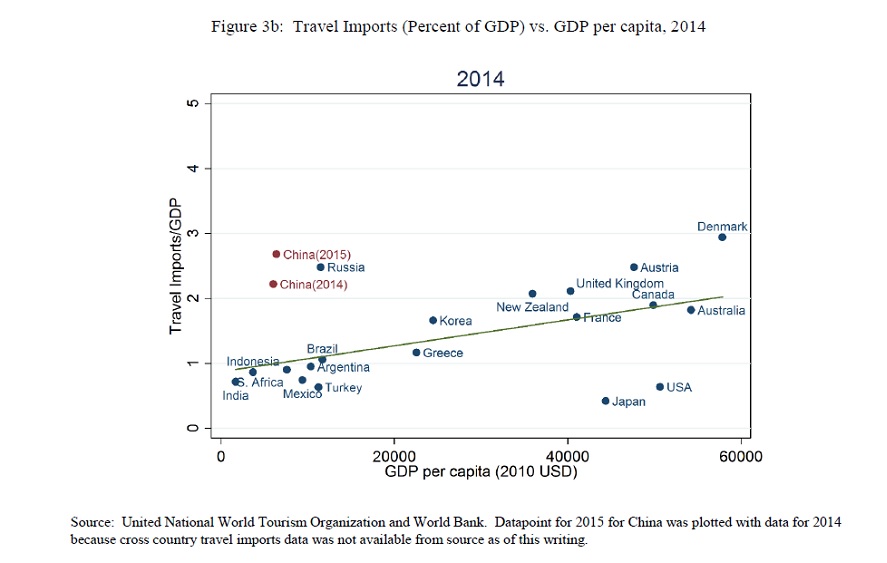

China’s new avenue for capital flight—tourists! A recent study by the Federal Reserve[1] suggests that Chinese spending on tourism is much higher per capita than one usually observes. The anecdotal evidence is that Chinese tourists are using their foreign trips to purchase assets in foreign nations, evading Chinese capital controls. Below is a telling chart from the paper.

(Source: Federal Reserve, page 49)

The regression line shows the normal spending one would expect given the level of per capita income. Although we don’t show the chart here, in 2010, Chinese travel imports were on the regression line. The above chart shows that China’s travel spending is near that of Denmark, which has a per capita GDP about 2.5x greater. Note that Russia, another nation plagued by capital flight, is in the same area of the graph as China. Besides the obvious conclusions drawn, that Chinese investors are clearly willing to take unusual steps to move funds out of the country, it also means that this spending is really capital account spending and the Chinese current account surplus is understated because tourist spending is considered a form of imports and thus is part of the current account.

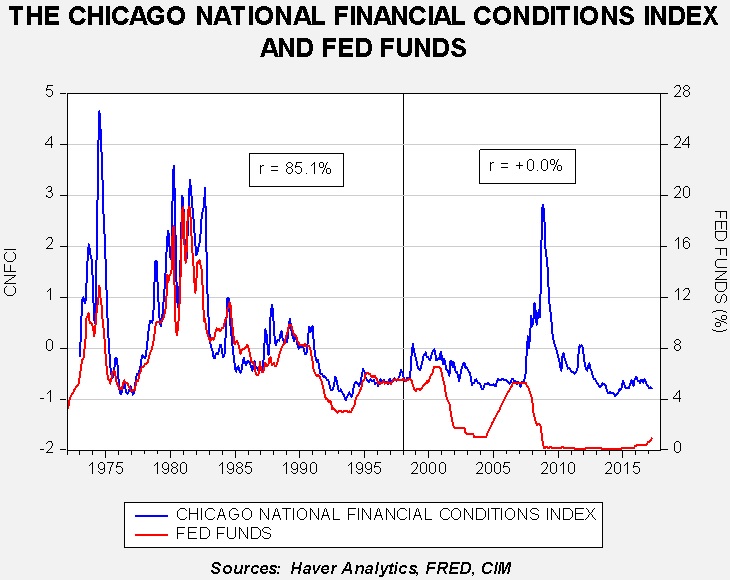

Growing concern about financial stress (or the lack thereof): NY FRB President Dudley, Chair Yellen and Vice Chair Fischer have all recently commented about the lack of financial stress in the system. We have discussed this issue consistently now for a few years.

This chart shows the Chicago FRB index of financial conditions and fed funds. The conditions index is a measure of stress—the higher the index, the greater the level of stress. From the early 1970s into 1998, fed funds and the conditions index closely tracked each other; in fact, we would argue that stress acted as a force multiplier for policy. As the FOMC raised rates, stress rose, further contracting lending and signaling rising risk in the financial system. This led to slower growth. As the Fed cut rates, the opposite occurred. What changed? We think two things. First, as the Fed has become increasingly transparent, it has become easier for the financial markets to predict policy. In fact, the Fed seems to pride itself on not surprising the markets. Thus, there is little fear of policy even when rates are increased because the hikes can be discounted well in advance. Second, as the financial system has become more concentrated, the Fed is concerned that it has become more fragile. Thus, it works to contain financial stress (or keep financial conditions calm) as it feels it can’t risk policy induced stress because it can’t easily control the impact of stress. The data tend to bear this out. Once stress rose in 2008-09, it took years of low rates, forward guidance and QE to bring it down again. Recent comments from Yellen, et al. suggest that the FOMC would like to inject some stress into the financial system to prevent “irrational exuberance.” The problem is that we fear they don’t have the tools to contain it once introduced. The Fed is acting like a forest manager who never allows fires; eventually, a fire naturally occurs and there is so much built up tinder due to fire suppression that a major outburst becomes impossible to contain. Thus, we are leery of these recent comments because by the time stress begins to rise it may not be easily contained.

[Posted: 9:30 AM EDT] BREAKING NEWS: THE IMF HAS LOWERED U.S. GDP GROWTH FORECASTS FOR 2017-18. GROWTH FOR 2017 WAS CUT TO 2.1% FROM 2.3%. FOR 2018, THE FORECAST FALLS TO 2.1% FROM 2.5%. LACK OF FISCAL SPENDING ON INFRASTRUCTURE AND LACK OF TAX REFORM WERE CITED.

Here are the news items we are watching:

Draghi the hawk? ECB President Draghi gave a speech overnight where he offered a rather upbeat assessment of the Eurozone economy. He suggested that growth is picking up, headwinds are abating and inflation is likely to rise. Despite these improvements, he argued for continued monetary stimulus. The financial markets are taking the speech as a precursor to eventual policy tightening; the EUR is up sharply this morning and commodities are rebounding off of recent lows.

Trump administration warns Syria: Late yesterday, the White House issued a press statement warning Syria that another chemical weapons attack would invite a response from the U.S. and the Assad regime “would pay a heavy price” if it uses these weapons. The U.S. is suggesting that it has intelligence that Syria was taking steps to deploy these weapons. Such public warnings coming directly from the White House are unusual; normally, this type of warning would have been sent from the Defense Department or State Department. It would appear the president is taking a personal interest in this situation. If Assad defies the U.S. there would almost certainly be a response given the White House statement, which could lead to a situation of Iran and Russia against the U.S.

Filling the Fed Governor vacancies: The administration has apparently decided that it wants to announce all three vacant Fed governor positions at the same time. Randal Quarles and Marvin Goodfriend appear to have the inside track on two of the positions but the remaining position traditionally goes to a community banker to offer some representation from small banks on the FOMC. The Trump administration is facing a similar problem to what the Obama administration faced—Fed rules require divestiture of ownership in most cases and that is an unattractive requirement. So far, three candidates have withdrawn their participation because they didn’t want to sell their interests in their bank affiliations. The delay in filling these spots reduces the administration’s influence on the FOMC and it would behoove them to act sooner rather than later.

The Italian job: Yesterday, we noted that Italy bent EU banking rules to bail out two banks with taxpayer funds while protecting bondholders. The backlash has now begun in earnest. Germany is apparently furious with Italy’s behavior and is pressing Brussels to tighten rules to prevent bondholders from being protected while taxpayers are hit with the bailout. Germany’s concern is that, eventually, the Eurozone will have a unified banking system and it doesn’t want its taxpayers to be bailing out bank bondholders in other countries. Italy argued that the failure of the two banks would not bring systemic risk to the Eurozone and thus could be resolved using Italian regulations. The real problem was that most of the senior bondholders were ordinary depositors who were sold the bonds as savings alternatives. The political fallout from liquidating the bondholders before the taxpayers would have been a major problem. We will be watching for whether Germany can force the EU to close the loophole Italy used for this bailout. If Germany can, future bank failures will tend to put senior bondholders at risk. At the same time, bank failures always run the risk of becoming unexpectedly systemic and it seems unrealistic for Berlin to expect that Eurozone nations will allow a small bank to implode their national financial systems. We still expect the Eurozone to eventually shrink due to the inconsistencies between Germany’s goals and the inability of much of the Eurozone to achieve Germany’s position.

May has a government: Yesterday, PM May officially built a coalition of the Tories and the Democratic Unionist Party (DUP) of Northern Ireland. It’s mostly a marriage of convenience and may not last. The DUP, first and foremost, received money; Northern Ireland is going to get an additional £1.0 bn in extra spending over the next two years. The agreement could potentially upset the delicate peace process in this area of the U.K. Currently, Northern Ireland has some degree of self-governance (devolution), but only if the Catholics and Protestant parties can agree (the DUP represents the latter). The DUP was able to place strongly unionist language in the coalition agreement which will not sit well with the Catholic parties. It is possible that London will need to take over the government in Northern Ireland if the two groups can’t agree. The other problem is that the DUP is a “soft Brexit” party; although it did support Brexit last year, it does not want a hard border with Ireland as would be necessary if the Brexit agreement with the EU is strict. Thus, the DUP could rebel if the May government pushes a hard Brexit policy. On the other hand, this coalition may force May into a softer position on Brexit which could lead to a backbench revolt within the Tories. Finally, the DUP is a socially conservative party that holds many positions the Tories find distasteful. All this leads us to believe that this government may not have staying power.

Growing tensions with China: Axios is reporting that the White House is becoming jaded with China. The hope was that by offering trade concessions China would ratchet up pressure on North Korea. The realization is setting in that Beijing isn’t ever going to put enough pressure on Pyongyang to stop its nuclear weapons program. This was apparently the reason for inviting Indian PM Modi to Washington. India is a geopolitical rival to China and the optics of the warm embrace won’t be lost on Chinese leaders. It should be noted that Reuters reported yesterday that the U.S. plans to place China on its global list of worst offenders of human trafficking and forced labor. The State Department compiles this report but there are leaks that indicate SOS Tillerson has decided to put China into “Tier 3,” the lowest grade, suggesting it is among the worst offenders. In the 2016 report, Tier 3 nations included Iran, Russia, Sudan, Syria, Venezuela, North Korea, et al. If this leak is true, it will anger China and suggest deteriorating relations.

(N.B. Due to the Independence Day holiday, our next report will be published on July 10th. That edition will be our Mid-Year Geopolitical Update.)

Last week, we offered background on the situation with North Korea. We presented a short history of the Korean War with a concentration on the lessons learned by the primary combatants. We also examined North Korea’s political development from the postwar period through the fall of communism and how these conditions framed North Korea’s geopolitical situation. We also analyzed U.S. policy with North Korea and why these policies have failed to change the regime’s behavior.

The primary concern is that North Korea appears on track to developing a nuclear warhead and a method of delivery that would directly threaten the U.S. This outcome is intolerable and will trigger an American response.

In Part II, we will discuss what a war on the peninsula would look like, including the military goals of the U.S. and North Korea. This analysis will include the signals being sent by the U.S. that military action is under consideration and a look at the military assets that are in place. War isn’t the only outcome; stronger sanctions or a blockade are possible, as are negotiations. An analysis of the chances of success and likelihood of implementation will be considered. As always, we will conclude with market ramifications.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.