Asset Allocation Weekly (June 16, 2017)

by Asset Allocation Committee

Last week, the Federal Reserve published its Financial Accounts of the United States report, more commonly called the “Flow of Funds” data. The report offers a plethora of insights into the economy. This week we want to examine the household debt situation.

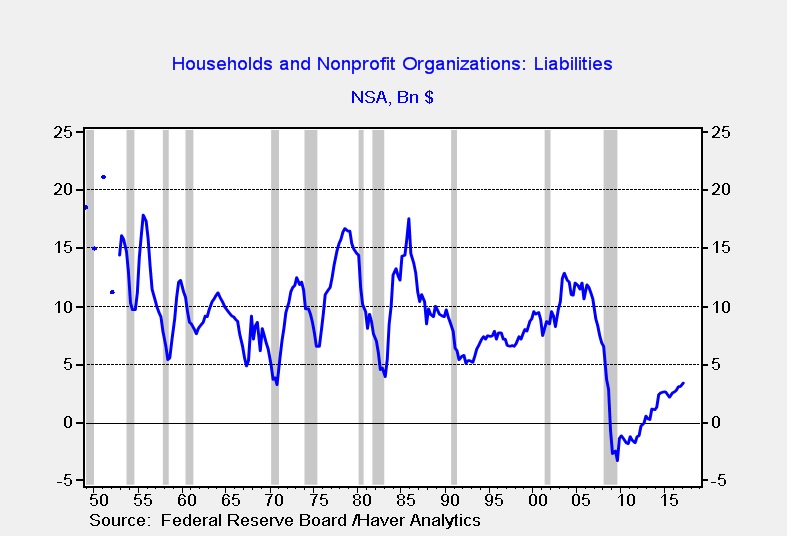

In Q1, household debt reached $15.1 trillion, up 3.4% from the previous year.

Although the growth in liabilities is positive for consumption, note that the current growth rate is well below the 9.8% average from 1946 through 2006. As we will show below, deleveraging continues but the pace has slowed dramatically. Still, part of the reason for sluggish growth is that households are simply not borrowing as quickly as what we have seen in the postwar period.

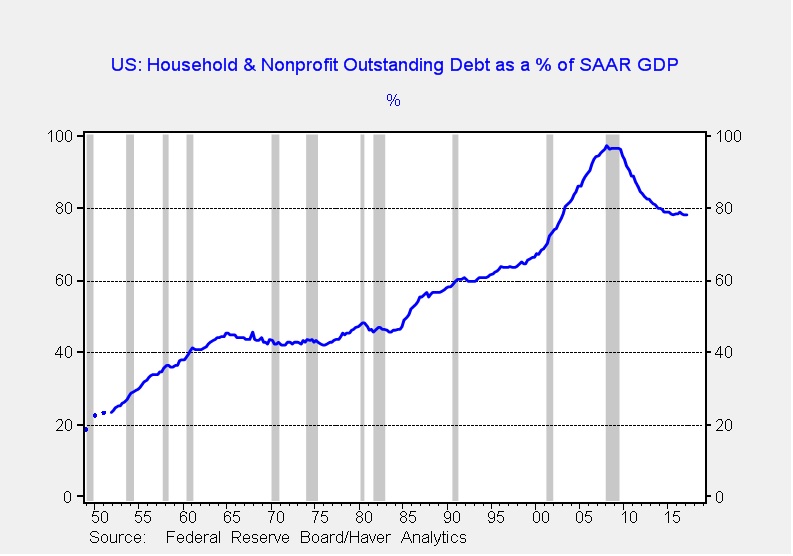

As noted, deleveraging has continued but the pace has slowed to a crawl.

Household debt (non-profit debt is not meaningful) is down to 78.2% of GDP after peaking at 97.7%. It is virtually impossible to determine the “correct” or sustainable level of debt, but a solid case can be made that any reading above 60% is probably not manageable over the long run. Of course, there are three ways this ratio can decline, falling levels of debt, rising real GDP relative to debt or rising inflation relative to debt. The lack of inflation has probably prevented an even larger drop in this ratio.

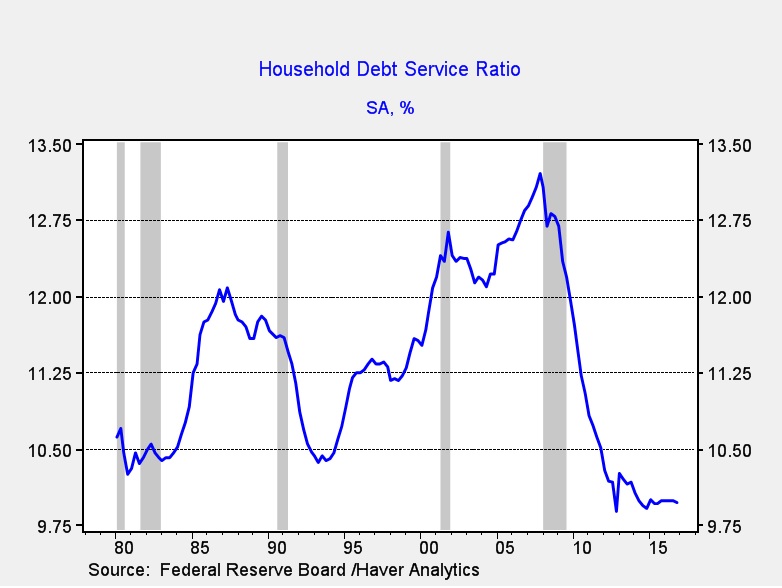

Low interest rates have reduced the servicing costs.

This chart shows household debt service costs as a percentage of after-tax income. Debt service costs rose steadily from 1993 into 2007. The combination of falling interest rates and the level of debt has led to a sharp drop in debt service costs. At these levels of debt service, one would expect that households would be encouraged to expand their debt levels. However, the “hangover” from the debt crisis has not yet diminished.

As long as households are reluctant to borrow, economic growth will remain slow and inflation low. This combination should lead to moderate policy tightening from the FOMC and an extended business cycle. If borrowing were to increase, these conditions might change but, for the foreseeable future, we expect borrowing to remain sluggish and economic growth to remain weak as well.