Last week, we defined important terms that shape the political alignments and examined the coalitions that mostly define the political sphere.[1] This week, we make some general observations of how the coalitions interact, discuss the “natural” pairings of the coalitions and examine historical examples. We will conclude with market ramifications.

Observations There is a division between class and identity. This is probably the greatest cause of confusion among political pundits and the general public alike. Sometimes voters will select a candidate who is detrimental to their economic interests. They usually do this because, at the time of their vote, identity was a stronger factor than class. Because it is more emotional and tribal, identity makes it hard to project outcomes. Class is fairly easy to observe; one can use wealth as a proxy. But identity, because it is multi-dimensional and somewhat fluid, can turn elections in unexpected ways. Our “laundry list” of surprises, the anti-establishment political outcomes noted in Part I of this report, were partly due to decisions based on identity.

Political leaders tend to use identity to woo voters outside the coalition of their class. This is done by either claiming affiliation to a group or by warning against the negative outcomes if another group takes office. Nearly every campaign story has some “origin myth,” where the candidate (usually RWE or LWE) harkens back to some period of their lives when they were living a hardscrabble existence so they can claim affinity to the populists to attract their vote. In some cases, the candidate is so removed from struggle that they have to cite the origin myths of their parents, grandparents or great-grandparents.

The other tactic often deployed is to suggest that if the other establishment candidate wins he/she will support policies that will undermine a populist group’s identity. For example, if a LWE candidate is trying to gain support from LWP voters, he will cite the threat to immigration or reproductive rights if the other candidate wins. A RWE may use similar tactics on the RWP, suggesting a LWE candidate will undermine gun ownership or religious liberties.

[Posted: 9:30 AM EDT] Although it was a quiet weekend, we have had a busy morning. Here is what we are watching:

Iran: There was media sniping this morning, which appears to have started in Iran. First, President Rouhani of Iran warned the U.S. not to escalate tensions with his country, suggesting that a confrontation would lead to the “mother of all wars.” He also indicated that the U.S. could not stop Iran from exporting its oil.[1] This statement is, obviously, incorrect. Although Iran has often threatened to shut down the Strait of Hormuz, which is perhaps the most important oil shipping chokepoint in the world, the U.S. could actually close off Iranian shipping and exports through financial sanctions and the U.S. Navy’s ability to implement a blockade. President Trump reacted through social media, sending out an all-caps response late last night.

To Iranian President Rouhani: NEVER, EVER THREATEN THE UNITED STATES AGAIN OR YOU WILL SUFFER CONSEQUENCES THE LIKES OF WHICH FEW THROUGHOUT HISTORY HAVE EVER SUFFERED BEFORE. WE ARE NO LONGER A COUNTRY THAT WILL STAND FOR YOUR DEMENTED WORDS OF VIOLENCE & DEATH. BE CAUTIOUS![2]

This escalation appears to have been prompted by comments from SoS Pompeo, who described Iran’s leaders as the “mafia” and promised to back Iranians unhappy with their government.[3] Pompeo reiterated the U.S. goal of lowering Iran’s exports to “as close to zero as possible” by November 4. While it is obvious this administration is taking a hostile line toward Iran, Pompeo’s comments about supporting anti-government elements in Iran are probably a mistake. There has been rising unrest in Iran due to the deteriorating economy. But, the elements opposing the mullahs in Iran may not necessarily be pro-U.S. By indicating the U.S. would aid such groups, they are immediately tainted as not being loyal to Iran. This is a mistake that is common for Western governments; regime change may not necessarily make conditions better or empower a new, Western-friendly government.

The comments appear to have lifted oil prices. However, prices are also higher on reports that some North Sea oil platforms have been hit with a 24-hour strike.[4]

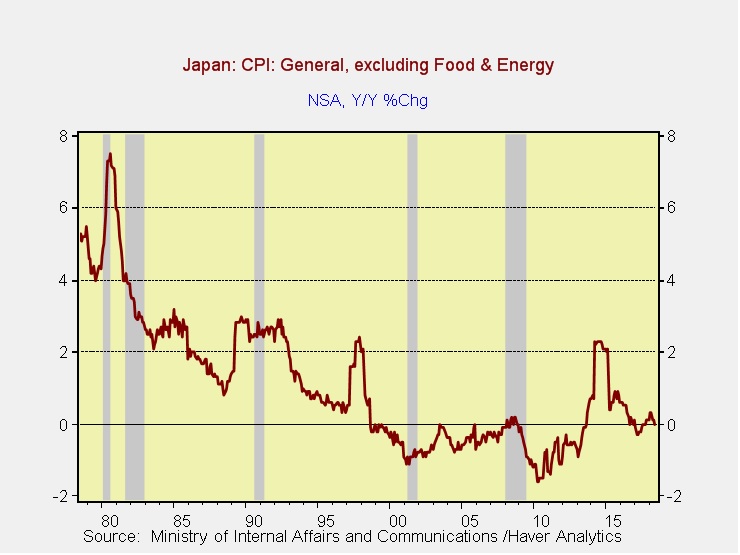

Change at the BOJ? We did see a jump in Japan’s 10-year government yields overnight on fears of tightening monetary policy. The Bank of Japan continues to struggle with policy. The central bank continues to see inflation below its 2% target with little evidence it’s rising.

This chart shows Japan’s core CPI (y/y% change). Although we did see a jump in 2014, that was due to a hike in consumption taxes. Currently, the inflation rate is zero. At the same time, zero interest rates are distorting the economy and undermining how the financial system functions. What does the BOJ need to do? The best outcome it could achieve would be to steepen the yield curve, which would help the financial system. Currently, the BOJ pegs the 10-year rate at zero. There is talk that it may allow the 10-year rate to become more volatile, but the risk to this policy is that it further confirms the low inflation policy and lifts the JPY. The central bank meets next week; we suspect these “leaks” are really trial balloons, and the market’s reaction thus far (rising 10-year yields and a stronger JPY) will support the doves on the board to leave policy unchanged.

Trade: Trade issues continue unabated. SoT Mnuchin was at the G-20 over the weekend in Argentina. By all accounts, not much changed. The Trump administration continues to press for bilateral trade agreements and the rest of the world doesn’t want anything to change.[5] Mnuchin added to the president’s recent currency comments about foreign nations depreciating their currencies for trade advantage.[6] It should be remembered that Mnuchin made weak dollar comments at Davos earlier this year. On Wednesday, the president of the EU Commission, Jean-Claude Juncker, will meet with President Trump in a bid to forestall auto tariffs.[7] We would not be surprised to see some sort of deal on autos; it appears President Trump is rather isolated even within his own administration on this issue.[8] However, we do offer one note of warning: U.S. light trucks enjoy 25% tariffs which date back to the Johnson administration (the “chicken tax”[9]). If that gets negotiated away, it would likely be a major negative factor for U.S. automakers.

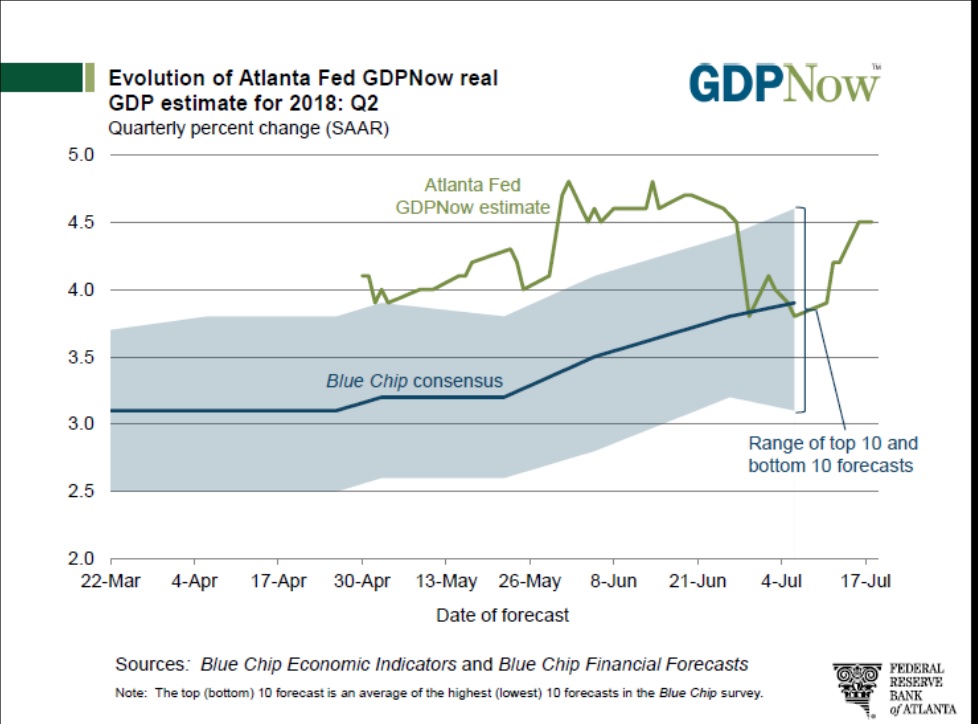

Q2 GDP: The latest reading from the Atlanta FRB’s continuous forecast for GDP is suggesting a robust quarter.

The current estimate is for a 4.5% quarter. In looking at the contributions to growth, consumption, net exports and inventories account for about 3.3% of that growth. Government spending is adding 57 bps. New investment is the remainder. Such growth bolsters the Fed’s case for higher interest rates.

AMLO—let’s make a deal! The president-elect of Mexico penned a letter[10] to President Trump indicating he is ready to “start a new stage of U.S.-Mexico relations” and wants to conclude the renegotiation of NAFTA. Although there have been worries about deteriorating relations due to AMLO’s nationalist stance, it does appear he is trying to work with the U.S. If the Trump administration responds positively, it could be supportive for Mexican financial markets.

Meat Mountain:[11]Although macroeconomic theory highlights the inflationary impact of trade impediments, the reality is somewhat more complicated. Yes, the combination of higher import prices and the loss of efficiencies that come from trade is inflationary. However, there is the short-run effect that exporters, whose markets become closed in retaliation, find themselves sitting on rising inventories. Eventually, these inventories are worked off and production is cut to adapt to lower demand. However, this can lead to “fire sale” prices during the adjustment process. It appears U.S. exports of meats are facing trade impediments and inventories are rising. This will eventually lead to lower meat prices in the U.S. (although this is dependent upon the competitive structure of the grocery and restaurant markets; some of this price decline could show up as better margins in those industries). Declining meat prices, while not as important to consumer confidence as energy, could be a popular event as we head into the mid-term elections.

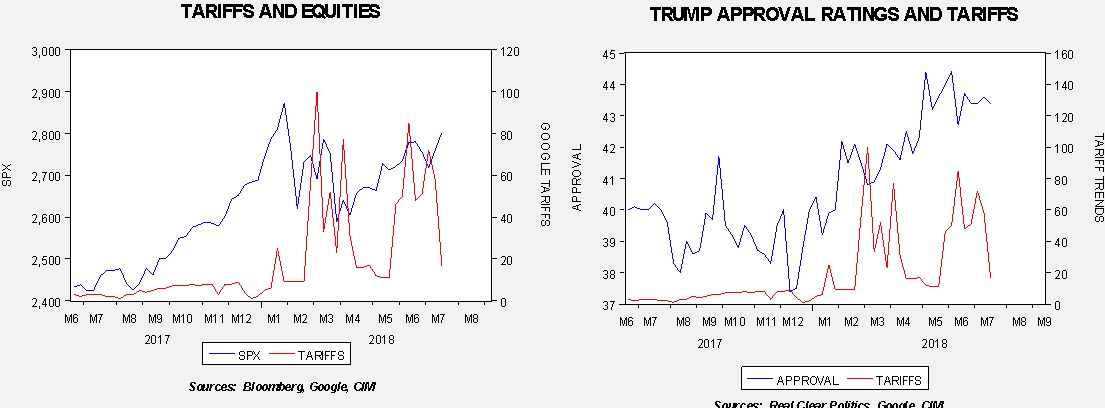

Although earnings are rising, equity markets have been range-bound since February.

(Source: Bloomberg)

This chart shows the S&P 500; after peaking around 2870, prices have been in a range roughly from 2600 to 2800. Although monetary policy tightening is partly to blame, the Fed was lifting rates during the period when the market was making new highs. Instead, it appears the market reversal was caused by the threat of trade impediments.

The chart on the left shows the S&P 500 and the number of times Google Trends reports the popularity of the word “tariff,” with 100 being most popular and zero being no reports of the word getting used. Note that when tariff chatter started to rise, the uptrend in equities stalled. The chart on the right shows President Trump’s approval ratings and the same Google Trends data. Approval ratings bottomed in December, about the time the tax bill passed. Approval ratings began to rise with the onset of tariff mentions. Note that as tariff mentions have declined recently the president’s trend in approval ratings has stalled and equities (on the left chart) have started to rally. Although the correlations are not perfect, overall, when remarks about tariffs are elevated, equities decline and the president’s approval ratings rise. Thus, it would make sense for the president to keep pushing on tariffs as it’s improving his political situation.

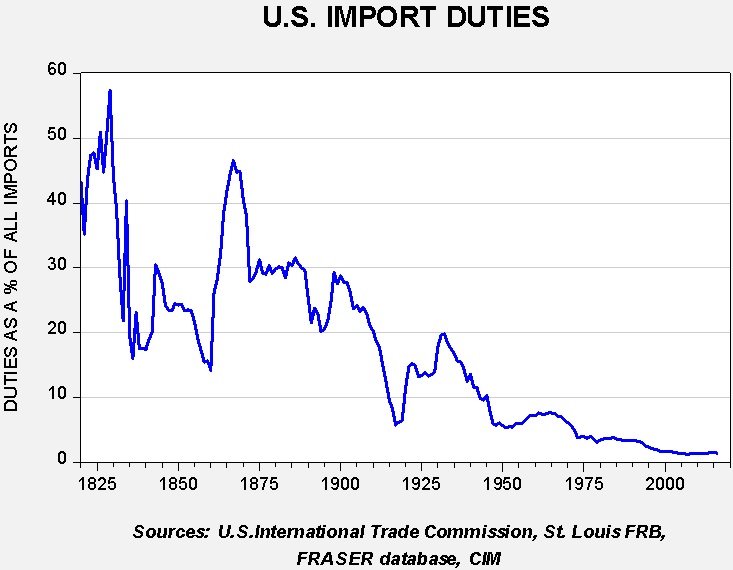

A major issue with trade policy is how the market discounts a turn to protectionism. That is mostly because we haven’t seen U.S. protectionism as official policy since the 1920s.

This chart shows the level of duties as a percentage of all imports. The U.S. was a high tariff nation, although tariffs did decline steadily until 1917. Tariff rates rose sharply after WWI into the early 1930s, culminating in the Smoot-Hawley Tariffs of 1930. Since then, tariff rates have steadily declined to the current low level of 1.4%. Simply put, there is no market analyst alive today who was an adult working in the markets the last time we had a major increase in tariff rates. And, if they were, it’s important to remember that this was under the gold standard so no one really has any experience in how a trade conflict will affect the world economy and financial markets in a floating fiat currency environment. All we can rely on is theory.

Our expectation is that tariffs will act as a supply constraint on dollars, which would be expected to be dollar bullish. However, as noted above, there is no reasonable way to indicate how much the dollar would rise because there isn’t a historical precedent to compare. So far, the financial markets appear to believe that the administration’s tariff threats are designed to prompt negotiations for more favorable trade terms. Thus, the dollar’s direction has been more a function of U.S. monetary policy—as the Fed continues to tighten the dollar has moved higher. However, if sentiment toward trade turns from mere posturing to deglobalization, the dollar could move significantly higher. A much stronger dollar would be very bearish for emerging markets and commodities and also a negative factor for developed markets as well. It would be bullish for Treasuries and small cap equities.

[Posted: 9:30 AM EDT] There is a lot going on. Let’s dig in:

The president speaks: For the most part, President Trump has been opposed to a weak dollar. At Davos this year, Treasury Secretary Mnuchin suggested a weaker dollar might be in U.S. interests if the goal was a narrower trade deficit. President Trump publicly criticized Mnuchin’s comment, suggesting the dollar should be strong. For many Americans, currency markets are something of a mystery. Unlike consumers of other countries, Americans are mostly insulated from dealing with exchange rates. We note that President Reagan was supportive of a strong dollar until it reached a level that became unsustainable. In response, at the Plaza Hotel in NYC the G-5 adopted the “Plaza Accord,” which was a multi-lateral policy shift to deliberately weaken the dollar.

We may be seeing a shift. This morning, on social media, President Trump openly criticized the EU and China for currency manipulation. The dollar has plunged on the news, while gold and other commodities are higher.[1] Although it’s difficult to know for sure, this development could be quite significant. Tariffs, by themselves, are dollar bullish as they reduce the supply of dollars on world markets (see this week’s Asset Allocation Weekly below). But, if the president has figured out that foreign nations are allowing their currencies to depreciate in order to offset tariffs, and he begins to jawbone the dollar lower, we will likely see a declining dollar. It should be remembered that the dollar is overvalued by most valuation metrics, so an official weak dollar position could find a path of little resistance.

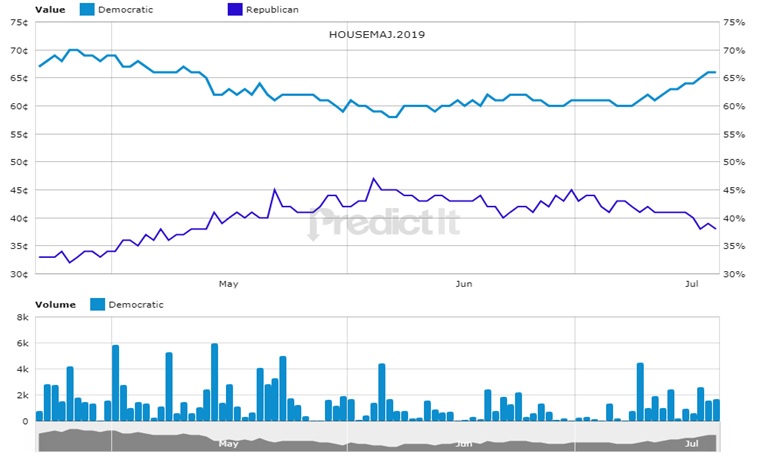

But wait…there’s more! However, this isn’t the only thing the president has said over the past 24 hours. He also indicated he is ready to slap $505 bn of new tariffs on China.[2] We note that the National Economic Council’s director Larry Kudlow has noted there are no talks with China. There is a school of thought that China may be concluding that the GOP will lose the House in November. If that’s the case, President Trump will find himself dealing with everlasting investigations and thus will be less able to prosecute a trade war. We note that the prediction markets are projecting a change in control for the House.

(Source: PredictIt)

If China has taken this position, then it would make sense for the Chinese to simply stall until November and then see U.S. trade policy moderate due to distractions at the White House. Of course, the administration can do this calculation as well and may try to force an agreement. Although it is still not clear whether this is really China’s policy, it makes sense to us and thus we would not be surprised to see mostly silence from Beijing.

Trump and the Fed: As noted above, the dollar has been strong this year. As we noted in this week’s Asset Allocation Weekly (see below), one of the factors boosting the greenback is the potential for a trade war. Rising tariffs, in theory, are bullish for the dollar because they act as a constraint on dollar supply. U.S. monetary policy is another factor that has supported the dollar. The Fed has been steadily raising rates when the rest of the world has mostly been holding to accommodative monetary policy.

One of the factors we have been monitoring is the White House’s position on monetary policy. Earlier this year, Larry Kudlow, the director of the National Economic Council, hinted that the Fed shouldn’t raise rates due to fiscal stimulus because the tax cuts would boost investment and thus add to productive capacity. Although that point is debatable (as we noted in last week’s AAW, it appears the tax cuts may be going to stock buybacks), the bigger issue was the interference in monetary policy. During Bill Clinton’s presidency, Robert Rubin, who became his treasury secretary, convinced the administration to avoid commenting or criticizing the conduct of monetary policy. The idea was that if the White House allowed the Fed to run policy and bring down inflation, the decline in long-term interest rates would be the best stimulus the economy could receive. Since then, the unwritten rule has been that administrations leave the Fed alone. And, for the most part, they have. Despite what you are seeing in the media,[3] prior to Rubin’s directive, administrations often commented on, or overtly tried to sway, monetary policy.[4] In the footnote below, we cite Mallaby’s biography of Alan Greenspan. This history shows that presidents not only tried to manipulate monetary policy, but Greenspan himself likely participated in a scheme to undermine Chair Arthur Burns to force him to conduct an inappropriately accommodative policy during the Nixon years. Rubin’s argument was that Fed independence would yield a better outcome than giving the impression that politicians were guiding policy. In other words, Fed independence would lead to lower inflation expectations and a better long-term economy.

In a CNBC interview[5] and in a “hailstorm” of tweets this morning,[6] President Trump has become increasingly critical of the Fed’s tightening policy. Although this action is clearly a divergence from policy of the past two decades, as we note above, it isn’t at all unprecedented. One of the hallmarks of President Trump is his desire to overturn precedent.

To some extent, we have been expecting the president to become critical of the Fed. It is important to remember that the Fed wasn’t always “independent.” Until 1951, the Fed acted as the funding arm of the Treasury. That is partly how the government funded the war effort with almost no rise in interest rates; the Fed simply expanded its balance sheet, absorbing the government’s borrowing. William Martin negotiated an “accord” with the White House and Congress in 1951 which gave the Fed independence from the Treasury. However, there is nothing written on stone tablets that says a central bank must be independent. In fact, central bank independence is really more a function of inflation policy. If the goal is low inflation, central bank independence is a good idea. If a nation wants to reflate, preventing the central bank from thwarting that goal is also appropriate. If populism is really about reflation, reducing Fed independence is likely going to occur. We may be seeing a move in that direction.

Bottom line: We have policies that are divergent. On the one hand, tariffs are dollar bullish. On the other, jawboning for a weaker dollar and threatening Fed independence could be significantly dollar bearish. We note that any move to undermine Fed independence will also increase the risk of rising inflation expectations, which would play havoc on the bond market. So, risks are rising.

Italy again:The populist coalition is threatening to oust Italy’s finance minister, Giovanni Tria, over Tria’s nominations for the state lending bank, CDP. Tria is considered an establishment figure and his appointment led to stabilization of the Italian bond market. We note that this news led the Italian 10-year rate to jump from 2.50% to 2.58%.

[Posted: 9:30 AM EDT] Global equity markets are lower this morning. The EuroStoxx 50 is down 0.3% from the last close. In Asia, the MSCI Asia Apex 50 was down 0.2% from the prior close. Chinese markets were down, with the Shanghai composite down 0.5% and the Shenzhen index down 0.8%. U.S. equity index futures are signaling a lower open. With 55 companies having reported, the S&P 500 Q2 earnings are above expectations at $39.31 compared to the $39.20 forecast for the quarter. The forecast reflects a 19.9% increase from Q2 2017 earnings. Thus far this quarter, 92.7% of the companies reported earnings above forecast, while 3.6% reported earnings below forecast.

We are in the back half of the week! Everything is down this morning except the dollar. Here is what we are watching:

Brexit thoughts: Yesterday’s vote in the House of Commons actually suggests a rather interesting informal coalition may be evolving. As we noted yesterday, PM May avoided a no-confidence vote by gathering enough Remain supporters among the Tories and by finding a few Labor MPs to support her as well; the Labor defectors also support either a soft Brexit or staying in the EU. The Labor MPs could have easily forced a no-confidence vote and new elections where the Labor Party would have a good chance of winning control of Parliament. However, that is not necessarily a favored outcome if one is a “Blairite” Labor MP, which is essentially an establishment center-left politician. In other words, pushing for elections that lead to Jeremy Corbyn becoming prime minister is probably not an attractive outcome. Thus, we may be seeing an informal grouping of Blairite Labor MPs joining Tory Remainers to keep Theresa May in office. If our theory is correct, May will remain as PM and there will be a soft Brexit. That would be a bullish outcome for the GBP.

Trade talk: The G-20 Finance Ministers meet this weekend. Discussions are expected to focus on trade. The Commerce Department is holding a day-long hearing today on auto tariffs. There are 45 witnesses scheduled; only one, Jennifer Kelly of the UAW, is expected to be supportive of auto tariffs. Companies are uniformly opposed to tariffs as automobile production has become increasingly globalized. Later this month, EU President Jean-Claude Juncker is expected to visit Washington, and there are hopes he will bring some tariff concessions on European tariffs.[1] Even trade hawks in the Trump administration see the auto tariffs as misguided and would like to see some modest concessions offered that would allow the president to declare victory[2]. The administration is apparently investigating the uranium market to see if U.S. miners are being unfairly affected; if so, we could see tariffs implemented on that commodity[3]. Meanwhile, NEC’s Larry Kudlow blamed Chairman Xi for the lack of movement on Chinese/U.S. trade negotiations.[4] The Chinese suggest otherwise.[5] The bottom line is that there are no talks occurring between the two nations. As we note in the next segment, China appears to be using the currency as a weapon.

[1] Actually, the history of light-truck tariffs, where the U.S. imposes a 25% tariff on imported light trucks, is fascinating. Here is a like to the background: https://en.wikipedia.org/wiki/Chicken_tax

We expect that Fed policy will continue tightening through year-end, with as many as two additional increases in the fed funds rate in tandem with a measured reduction in the size of the Fed’s balance sheet, but the prospect for a recession is not included in our cyclical forecast.

Our expectations are for continued GDP growth throughout the balance of this year and into 2019. Accordingly, equity exposures remain elevated across all strategies relative to our historic allocations, with a 60% growth style bias among U.S. equities.

The outlook for the U.S. dollar is path dependent upon the durability of both trade conflicts and Fed posture into and through next year.

We retain a modest allocation to gold given the combination of the potential for global political instability and its current price well below our estimate of fair value.

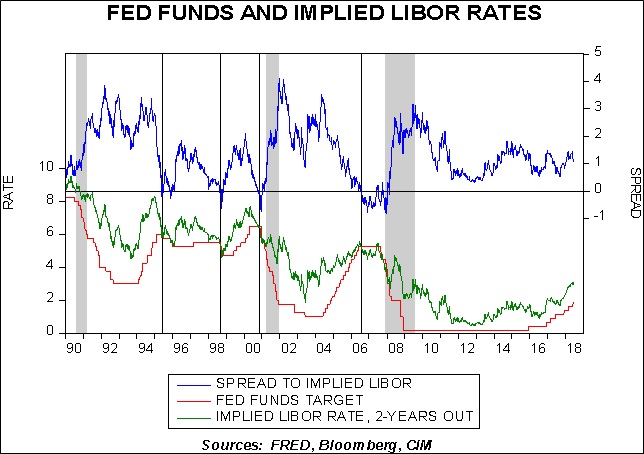

Continued tightening by the Federal Reserve, with its two increases in the fed funds rate thus far this year, combined with the gradual reduction in its balance sheet and the gravitational pull of negative yields in much of the developed world have led to a flattening of the U.S. Treasury yield curve. While our view is for continued economic growth until nearing the end of our three-year forecast cycle, we remain wary of the potential for a misstep by the Fed that would lead to excessive tightening and increase the odds of a recession. Though an inverted yield curve is widely viewed as being indicative of an impending recession, a flattening curve is not necessarily a precursor to an inversion. What we have found to be an even more important metric to measuring Fed policy than either the spread between fed funds and the 10-year or the 2/10 segment of the curve is the spread of fed funds to the implied LIBOR rate advanced two years. As the accompanying chart indicates, implied LIBOR has increased since mid-2016 and remains comfortably in excess of fed funds. When this measure falls into negative territory, it is a signal from the financial markets that the Fed has overtightened policy. If or when this occurs, it will cause us to reassess the probability of a near-term recession. Until that point in time, we are consoled by the high levels of several sentiment indices, including the U.S. NFIB Business Optimism Index, the Conference Board’s Consumer Confidence Index and the University of Michigan’s Index of Consumer Sentiment. In addition, low unemployment and strong GDP figures compel us to retain equity exposures at their historically high levels for the portfolios until such time that potential risk outweighs expected return. Finally, inflation expectations remain around the 2% level, which creates a stable backdrop for both bonds and equities. While we are cognizant that the mid-term elections in the U.S. may engender fiscal changes that could challenge the economic environment, we find it premature to factor any effects into our forecast.

The global economic environment, while still positive, faces a number of challenges. The imposition of tariffs by the U.S. and, as a result, several of its trading partners, holds the potential to develop into a full-scale trade war with obvious downward implications for global growth. Although Europe is still in expansion, the ECB has maintained a dovish stance on rates and has indicated it might forestall a reduction in its balance sheet until mid-2019, citing a moderation in growth in the first half of the year and concerns emanating from increased protectionism. The Japanese economy has similarly exhibited recent signs of difficulty. After eight straight quarters of GDP growth beginning in 2016, the economy shrank in the first quarter. Although it was a modest decline of -0.2%, it echoes the moderation in Europe and encourages the extension of the BOJ’s asset purchase program. Of even greater consequence to the global economic environment is China’s response to U.S. protectionism. We believe China has the will and determination to engage in a full-scale trade war with the U.S. In addition, China may employ any economic weakness accruing from a reduction in its trade to contain its debt growth, which is prominent in Chairman Xi’s economic construct.

Given the global dispersion of economic growth rates and central bank policies combined with the potential for protectionism to take hold, we find the value of the U.S. dollar versus other currencies to be on a knife’s edge. Continued U.S. economic expansion and weakness abroad are normally a recipe for U.S. dollar strength relative to other currencies. However, though the interest rate differentials support a strong U.S. dollar and a global trade war would lead investors to seek safety in the greenback, leading to the potential for the U.S. dollar to reach historically high valuations, a more localized trade dispute solely with China would limit the overall economic impact. In the event that the goal of the U.S. administration’s trade rhetoric is simply to improve America’s bargaining position, the U.S. dollar could be vulnerable to a pullback to its fair valuation. If the Trump administration openly opposes Fed policy tightening, then the dollar could be especially vulnerable.

STOCK MARKET OUTLOOK

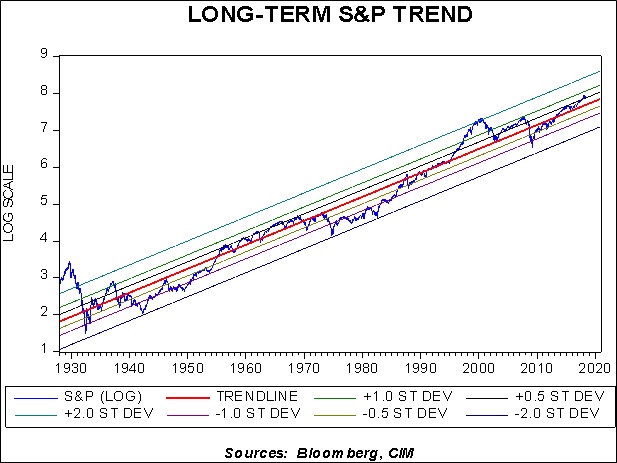

Despite trade tensions and the potential for a misstep by the Fed, our views remain favorable on U.S. equities. Our assessment is that inflation should remain contained, the low level of unemployment will persist and GDP growth will be maintained. As expected, the level of share repurchases, M&A activity and repatriation of overseas assets have been elevated since the passage of the tax act at the end of last year. Current readings show no indication of these trends abating in the near-term. Although equity prices, as measured by the S&P 500, are in excess of the long-term trend, as shown in the accompanying chart, expectations of higher corporate earnings and solid economic data combined with high levels of consumer and business confidence encourage us to retain our historically high equity allocations in each of the strategies. In addition, due to the current stage of the economic cycle, we maintain the 60% tilt toward growth equities, yet without an overt overweight to any particular growth-oriented sector due to potential effects on the Technology and Consumer Discretionary sectors from the upcoming introduction of the new Communications Services sector at the end of September. The overweight to the traditionally value-oriented sectors of Energy, Financials and Materials that have existed since the beginning of the year are supported by attractive valuations and are therefore retained.

Mid-cap and small cap exposures have an identical tilt to growth equities and are both overweight in our strategies that have growth as an objective. Outside the U.S., we retain most of the posture from last quarter. The factors discussed above regarding the U.S. dollar exchange rate will naturally create either a headwind or tailwind for returns on non-U.S. equities, but the attractive relative valuations advocate for their retention.

BOND MARKET OUTLOOK

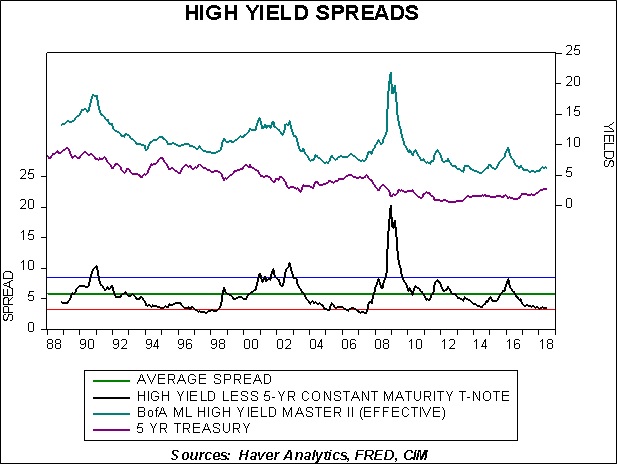

The more hawkish composition of voting members of the Fed’s Board of Governors as compared to last year produces the expectation of continued tightening and balance sheet unwinding. Combined with a stable inflationary outlook, this leads to a forecast of an extremely flat yield curve over our three-year cyclical outlook. Though this bodes well for the longer rungs on the ladder, as well as the long-term Treasuries employed in the income-oriented strategies, such a flattening will impact the intermediate rungs of the ladder. However, given our outlook for the full three-year cyclical period, any price pressure on the intermediate rungs will prove ephemeral as their roll toward maturity will find them comfortably recovering. While our view of the bond market is sanguine over the cyclical time frame, we harbor some level of trepidation in the speculative bond space. As the chart alludes, spreads are at post-recession tight levels. In addition, Moody’s estimates that $952 billion of high-yield bonds will be maturing between 2019 and 2022, most of which will be seeking refinancing. Coupled with the tax legislation limitation of interest deductibility to 30% of EBITDA by corporations, this may pressure spreads to widen. Accordingly, exposure to speculative grade bonds remains at the low end of our historic levels in the strategies.

OTHER MARKETS

We retain the allocation to real estate in the more income-oriented strategies given attractive and improving dividend yields. As a function of yield relative to potential risk, we view REITs more favorably than speculative bonds.

We also retain our allocation to gold, which was introduced last quarter. Owing to the fact that gold can serve as a safe haven during periods of heightened geopolitical and currency risks, and the knife’s edge of the U.S. dollar’s exchange value, we find the modest allocation to be helpful as a governor of risk. In addition, gold is currently trading well below its fair value price as suggested by our analysis.

[Posted: 9:30 AM EDT] Equity markets are quiet this morning; the biggest market moves are in currencies and commodities. The dollar is up this morning in the aftermath of the Powell testimony, which is dragging commodities and emerging markets lower. Here is what we are watching:

Google fined: Google (GOOG, 1198. 80) was hit with the largest fine ever levied by the EU, at €4.3 bn. EU regulators accused the company of anti-competitive behavior in the distribution of its operating system. This action is important on a macro level because government regulation may be the only threat to the market dominance of the major tech firms. We do expect the company to appeal the decision but we would not expect the EU to reverse this verdict.

The Powell testimony: Although the testimony generally went according to script, there were two takeaways from the discussion that we see as important. First, Powell continues to stress that the economy is robust and that economic strength justifies tighter policy. Focusing on economic strength should inoculate the Fed from criticism from the White House. Of course, any modest weakness might trigger a strong push from the White House for rate cuts. Second, Powell signaled that the quarterly cycle of rate hikes will be ending at some point. Powell appears uncomfortable with the notion of forward guidance and wants to inject some degree of uncertainty into monetary policy. We agree with this position. The move to holding press conferences after every meeting next year will give the Fed more flexibility to raise rates faster if necessary. At the same time, it can introduce the potential for pauses in tightening as well. We note that the implied three-month LIBOR rate from the two-year deferred Eurodollar futures did not change after the testimony; it still signals a terminal fed funds rate of 3% in two years.

May survives (again): U.K. PM Theresa May is becoming the Houdini of politics; this morning, she survived a vote[1] against the hard Brexit wing of the Tories by the pro-EU wing of her party. The hard Brexit group appeared to be pushing May into a complete exit position which is opposed by a large group of her party. The pro-EU faction forced a vote that could have brought down the government. But, in the end, a group of Labour MPs[2] voted with the pro-EU Tories and so May lives on another day.

Putin:A Russian aircraft carrying President Putin violated Estonian airspace[3] yesterday, passing through the NATO nation without clearance. This is a clear provocation after the recent events in Helsinki.

[Posted: 9:30 AM EDT] Tonight’s midsummer classic, the All-Star Game, is really the official midpoint of summer. Markets are quiet this morning. Here is what we are watching:

Did the president go too far? Criticism of President Trump’s performance at the press conference with Russian President Vladimir Putin was widespread. Even Fox News, which is generally supportive of the White House, was remarkably critical.[1] Our primary concern is always the impact of actions on the financial markets. It’s too early for any reliable polling to tell us much and there was no significant movement in the prediction markets, either. The history of populism does show that sometimes populist leaders, mostly due to inexperience, can overshoot their support. If Trump’s approval wanes, it might not necessarily be bearish for financial markets because it may slow the trade conflict. For now, we are treating yesterday’s Russia event as an item to watch. However, we must say that the breadth of condemnation was rare.

Powell to the Hill: Chair Powell goes to the Senate this morning for his semiannual testimony on monetary policy. Below we discuss a couple of charts worth noting.

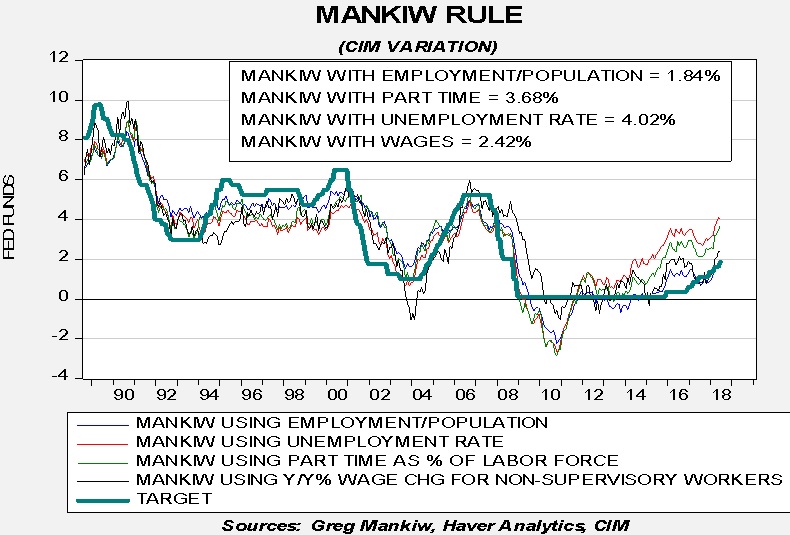

First, we have updated our Mankiw model with four variations. The Mankiw rule models attempt to determine the neutral rate for fed funds, which is a rate that is neither accommodative nor stimulative. Mankiw’s model is a variation of the Taylor Rule. The latter measures the neutral rate using core CPI and the difference between GDP and potential GDP, which is an estimate of slack in the economy. Potential GDP cannot be directly observed, only estimated. To overcome this problem, Mankiw used the unemployment rate as a proxy for economic slack. We have created four versions of the rule, one that follows the original construction by using the unemployment rate as a measure of slack, a second using the employment/population ratio, a third using involuntary part-time workers as a percentage of the total labor force and a fourth using yearly wage growth for non-supervisory workers.

Using the unemployment rate, the neutral rate is now 4.02%, down from 4.14%, reflecting the rise in the unemployment rate. Using the employment/population ratio, the neutral rate is 1.84%, up modestly from May’s 1.81%. Using involuntary part-time employment, the neutral rate is 3.68%, up from the last calculation of 3.50%. Using wage growth for non-supervisory workers, the neutral rate is 2.42%, roughly unchanged from the last report of 2.48%. June’s employment data was mostly in line with May’s so the neutral rate calculations didn’t change a lot. The only variation that is policy neutral is the one using the employment/population ratio. Thus, given that the majority of the FOMC still holds to some sort of Phillips Curve model for monetary policy, the bias should be for additional rate hikes.

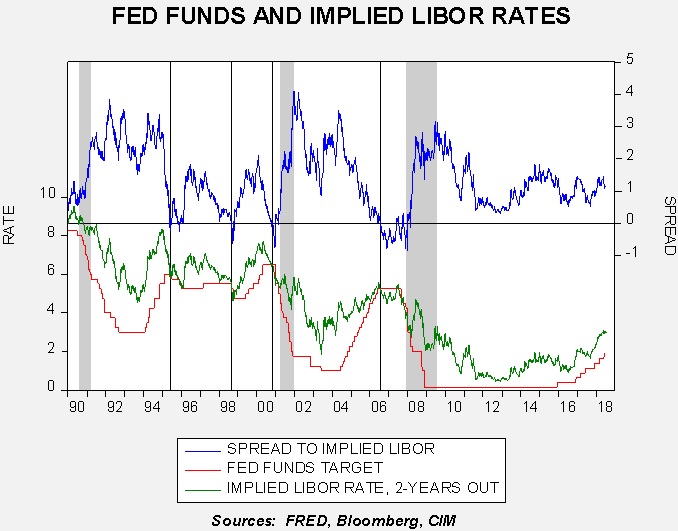

The second chart is our estimate of what the financial markets have discounted in terms of tightening. The chart below compares the fed funds target to the implied three-month LIBOR rate, two-years deferred, which comes from the Eurodollar futures market. Historically, the FOMC tends to tighten until the implied LIBOR rate equals the fed funds target. In fact, when the target overshoots the implied rate, the odds of recession increase. Currently, the implied LIBOR rate is near 3.00%, suggesting the Fed has four more hikes to go. Clearly, the financial market’s estimate of the terminal rate is well below what the dots plot or the majority of the Mankiw rule estimates suggest for the terminal rates. If the FOMC continues on its expected path, meaning two more hikes this year and perhaps more in 2019, the odds of recession will begin to rise.

We are already hearing discordant voices from the FOMC. Minneapolis FRB President Kashkari[2] (not a current voter) is calling for a pause, citing the rapid narrowing of the yield curve. We don’t expect anything from Powell other than “steady as she goes,” but concerns about monetary policy will likely rise by year’s end.

The rise of populism and the preference for unconventional leaders are upending the world order that the U.S. created after WWII. Accordingly, across the West, we are seeing a steady rejection of centrist, establishment parties. Here are some of the changes we have observed recently:

France: Emmanuel Macron was elected to the presidency last year without previous experience of holding an elected office. He started a new party which now holds the majority in the French National Assembly. His election and new party are clear rejections of the existing establishment parties.

Germany: Although Chancellor Merkel continues to hold power, her party, the CDU, had the weakest performance in last year’s election since 1949. The SDU, the other party in the “grand coalition,” had its worst showing since WWII. The Alternative for Germany (AfD), a populist right-wing party, was the first of its kind to win seats in the Bundestag in the postwar era and is the official opposition.

Italy: Voters rejected mainstream parties and elected a coalition consisting of the Five-Star Movement, a left-wing populist party, and the League, a right-wing populist party.

Mexico: Lopez Obrador, better known as AMLO, won the election held on July 1. He is the first Mexican president since 1929 who doesn’t represent one of the mainstream parties.

United States: Donald Trump, who had never held elected office, won the presidency and has been mostly governing as a right-wing populist.

This list isn’t exhaustive. Populists are currently governing in Hungary, the Czech Republic, Austria and Poland. It is quite possible that Brazil’s October presidential election will give the office to Jair Bolsonaro, who seems to be running as a right-wing populist strongman. In addition, Brexit is a populist movement; if Theresa May’s government, which is teetering toward a no-confidence vote, fails, there is a good possibility that a populist left-wing government led by Jeremy Corbyn will emerge.

In the media, there is much consternation about a number of developments, including non-establishment candidates on both the left and right defeating experienced political figures. This report is our attempt to put context around these developments.

In Part I of this report, we will define the terms that we use to describe the political landscape. These definitions will be used to characterize the four major political coalitions and their basic policy positions. Part II will begin with general observations about the effects of class and identity. From there, we will discuss actual historical developments that describe how these four coalitions interact. As always, we will conclude with market ramifications.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.