Author: Amanda Ahne

Bi-Weekly Geopolitical Report – Israel’s Pager Caper and Supply Chain Security (October 21, 2024)

by Bill O’Grady and Patrick Fearon-Hernandez, CFA | PDF

Can you trust your refrigerator? What if it could be weaponized against you, perhaps by being booby-trapped to explode, release poisonous gas, or just stop working on the command of some foreign enemy communicating with its computer chip? Just as important, if everyday products connected to the internet or communication networks could become that dangerous, what would you want your government to do to protect you? What could your government do to protect you?

These questions may sound strange, but they demand attention after hundreds of Hezbollah militants in Lebanon were maimed by simultaneously exploding pagers and walkie-talkies on September 17 and 18. Dozens of militants died in the attacks, which have been attributed to Israel. In this report, we explore how this groundbreaking attack has probably transformed national security requirements and will likely lead to big, costly changes in global supply chains in the coming years. We will also delve into the underlying philosophies that help explain why this could impact globalization. As always, we wrap up with a discussion of the implications for investors.

Don’t miss our accompanying podcasts, available on our website and most podcast platforms: Apple | Spotify

Asset Allocation Bi-Weekly – #127 “The Yield Curve Un-Inverts” (Posted 10/14/24)

Asset Allocation Bi-Weekly – The Yield Curve Un-Inverts (October 14, 2024)

by the Asset Allocation Committee | PDF

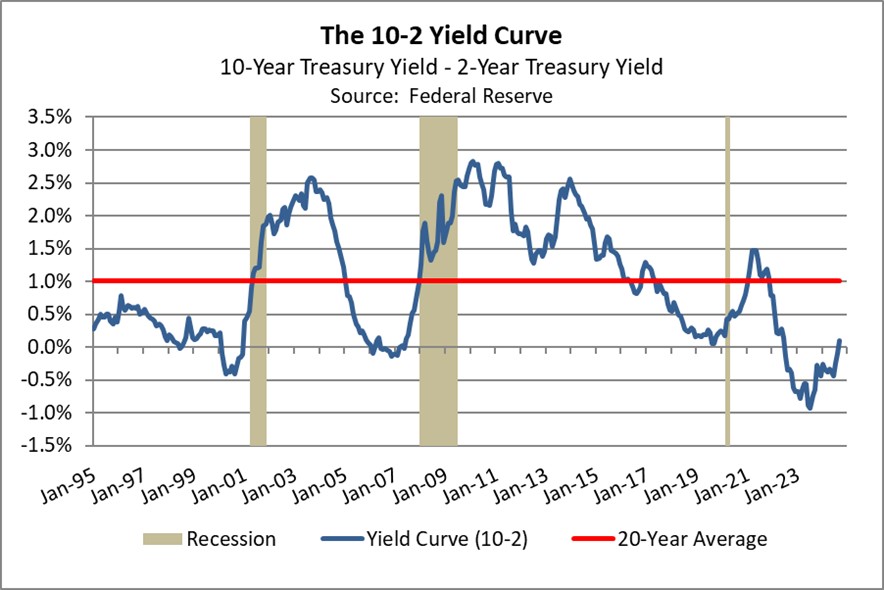

Although the financial press has failed to discuss it at length, the United States bond market has just exited a long period in which the yield curve (the range of bond yields across maturities) was inverted (longer-term yields were lower than shorter-term yields). One popular summary measure of the yield curve is the difference between the 10-year Treasury note’s yield and the yield on the two-year Treasury note. By that measure, based on month-end figures, the yield curve was inverted for 25 straight months from July 2022 through August 2024. At its nadir of -0.93% in July 2023, the 10-year Treasury yield was 3.90% and the two-year Treasury yield was 4.83%. At the end of September 2024, this measure of the yield curve had turned positive at 0.10%, with the 10-year Treasury yield falling 18 basis points to 3.72% and the two-year Treasury yield falling 121 basis points to 3.62% (see table below). Positive, upward-sloping yield curves are considered more normal.

The yield curve is closely tracked because inversions have often signaled an impending recession and falling values for risk assets. At this point, it appears that the latest inversion was a false signal of recession. It does appear that US economic growth has slowed, but there are only limited signs currently that the economy could be heading into a broad decline. Investment strategists have nevertheless begun to focus on the implications of the yield curve turning positive again. Many are urging investors to rotate into longer-maturity bonds, apparently on the conviction that longer-maturity bonds will see big price gains (implying big yield declines), while shorter-maturity bonds will see smaller price gains (implying smaller yield declines). Is this reasonable?

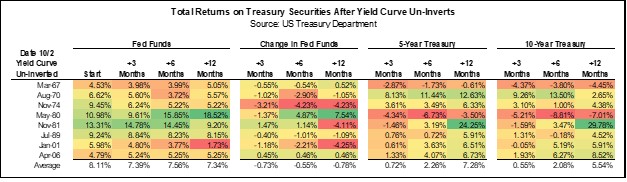

To get at that question, we analyzed the total return (yield plus price change) for both five-year and 10-year Treasury notes after each of the eight un-inversions of the yield curve since the early 1960s. We focused on the total return for Treasury notes at three months, six months, and 12 months after the end of each inversion. The results of our analysis are shown in the table below.

The table shows that in the 12 months after the un-inversions since the 1960s, the average total returns on five-year and 10-year Treasury notes have been positive but not spectacular. The table suggests that the key variable is what happens with the Federal Reserve’s benchmark fed funds interest rate in the year after the un-inversion. To the extent that the fed funds rate declines in the year after un-inversion, total returns for longer-maturity Treasury obligations are greater. If the fed funds rate is basically stable in the year after un-inversion, investors’ total returns from longer-maturity Treasurys have been similar to the yield on those obligations. But if the fed funds rate increases in the year after un-inversion, the total returns on longer-maturity Treasurys have typically been negative.

Looking out at the coming year, investors widely expect the Fed to keep cutting the fed funds rate, so today’s ubiquitous calls for longer-maturity Treasurys may make some sense. However, investors should also not forget the burgeoning bond issuance that could potentially outpace demand. In our view, in addition to lower policy rates, the Fed may need to end its balance sheet reduction program to help alleviate some of the liquidity concerns in the bond market. Policymakers could also decide to cut rates gradually over the coming year and only moderate the pace of balance sheet reduction. That’s especially so after the strong September employment report, which pointed toward rebounding demand for labor and increased wage pressures. More broadly, modest policy easing would be expected if US economic growth remains healthy and/or consumer price inflation doesn’t cool as much as anticipated. Based on the analysis presented here, the resulting “restrictive for longer” approach to monetary policy would likely limit the total returns for longer-dated Treasurys. An economic soft landing and modest monetary easing mean the maturity extension trade probably doesn’t work.

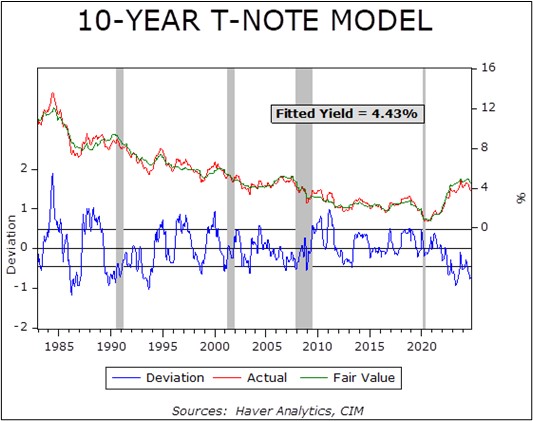

We also note that in the year after an un-inversion, the average total return on five-year Treasury notes is better than the total return on 10-year Treasurys, especially in cases where the fed funds rate increases. We see a similar implication from our bond model, which we use to predict fair value bond yields based on key economic indicators. When we plug a 3.25% fed funds rate into the model (roughly the level policymakers expect to reach by year-end 2025), we get a projected decline in the five-year Treasury yield from current levels but a rise to nearly 4.00% for the 10-year yield. (At today’s fed funds rate of 4.75% to 5.00%, the model estimates a fair value of 4.43% for the 10-year Treasury, as shown in the chart below.)

In sum, rotating into longer-maturity bonds to generate greater returns may not make sense right now, even if some observers are calling for it. Further normalization of the yield curve may indeed be in store as the Fed keeps cutting short-term interest rates, but those rate cuts may well prove modest if the US economy keeps growing. That could limit any price gains and total return opportunities in longer-dated fixed income. If the economy avoids a recession and reaccelerates, pushing up inflation again and potentially requiring renewed rate hikes, longer-maturity obligations could produce negative total returns. Keeping most bond exposure relatively short still seems to make sense today, even as it might be prudent to maintain some longer-maturity exposure to hedge against geopolitical risks.

Bi-Weekly Geopolitical Podcast – #54 “The US Presidential Election: Foreign Policy Implications” (Posted 10/7/24)

Bi-Weekly Geopolitical Report – The US Presidential Election: Foreign Policy Implications (October 7, 2024)

by Daniel Ortwerth, CFA and Thomas Wash | PDF

History shows that, despite the promises made as candidates, United States presidents display remarkable foreign policy consistency from one administration to the next. While often distinguishing themselves in the realm of domestic policy, the imperatives of national security tend to force the hands of presidents into choices that change very little (if at all) with party affiliation. In other words, foreign policy tends to be remarkably consistent.

Nevertheless, foreign policy typically provides at least some room for maneuver, and presidents use this wiggle room to pursue their priorities as circumstances permit. Often these priorities are different from one candidate to the next. With the presidential election looming in November, we need to understand these differences and their investment implications.

This report analyzes how US foreign policy might look in a new term for former President Donald Trump, the Republican candidate, and in an initial term for Vice President Kamala Harris, the Democratic candidate. It begins with a characterization of the two candidates according to the main American foreign policy traditions. It considers the kinds of cabinet members they will probably choose to fill the rosters of their foreign policy teams, and it culminates with a review of their priorities as we know them. As always, we conclude the report with implications for investors, in this case as they differ between the two candidates.

Don’t miss our accompanying podcasts, available on our website and most podcast platforms: Apple | Spotify

Daily Comment (October 3, 2024)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Good morning! The market is currently awaiting the release of the jobs report data and Israel’s response to Iran. In sports news, Lionel Messi’s Inter Miami has won the 2024 Supporters’ Shield for the second year in a row. Today’s Comment will discuss the ongoing dockworkers’ strike, how hurricanes can impact inflation, and the implications of the French government’s debt plan. As usual, the report concludes with a roundup of international and domestic data releases.

Union Tension with AI: The ongoing dockworkers’ strike may be a prelude to future disputes over AI and automation.

- US dockworkers have gone on strike at both East and Gulf Coast cargo facilities, demanding higher wages and a ban on automation for certain jobs. The strike is in its early stages, but it appears that workers have the upper hand. President Joe Biden has warned that if employers fail to reach an agreement with workers, it could lead to a man-made disaster. Meanwhile, both Vice President Kamala Harris and former President Donald Trump have expressed sympathy for the workers’ demand for higher wages to offset the rising cost of living.

- One of the most overlooked issues in this strike is the role of automation and AI. While lawmakers have primarily focused on immigration as a means of protecting workers, few have specifically addressed the potential for technology to displace them. Politicians’ reluctance to discuss the impact of automation on the job market is linked to the hope that new technology will be crucial in boosting productivity, which can not only help lower inflation but also increase profit margins.

- While the overall impact of AI on jobs may be overstated, the fear is real. According to a study by MIT professor Daron Acemoglu, AI is currently capable of doing only about 5% of jobs. Although this offers some reassurance to workers, it’s unlikely to quell their anxieties as 38% of workers think AI will hurt their jobs. Consequently, resistance to AI integration is likely to intensify in the coming years. This growing opposition could hinder firms’ efforts to increase productivity through AI, potentially leading to a reevaluation of AI’s promise and contributing to future inflationary pressures.

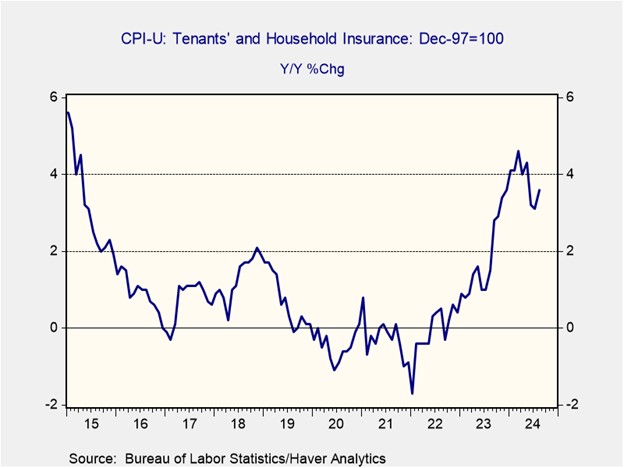

Insurance Costs: The estimate for the damage from Hurricane Helene is increasing, but this might not have as significant of an impact on insurance premiums as many would expect.

- The storm’s total economic losses are expected to reach approximately $35 billion. However, insurance companies are not anticipated to incur significant losses. Unfortunately for most homeowners, the majority of the damage caused by the storm was due to flooding, which is typically underinsured, as most policies only cover large-scale wind damage. Insurance companies in Florida, a region prone to hurricanes, are expecting damages from Helene to result in moderate losses compared to the devastation caused by Hurricane Ian in 2022 and Hurricane Michael in 2018.

- Although overall price pressures have eased this year, insurance costs remain persistently high. This inflationary trend is largely attributable to several factors: pandemic-related restrictions, rising operational expenses, and escalating repair costs. Unlike many other businesses, insurance companies cannot immediately adjust premiums to offset losses, as policies are typically locked in for a set term. Consequently, they are forced to wait until the renewal period to implement pricing changes that reflect the growing risks in the market, which is why insurance inflation can rise even as other prices are moderating.

- Insurance serves as a poignant reminder of the capricious nature of inflation. Certain factors can dramatically influence price levels without warning, underscoring the necessity for investors to be cognizant of the potential inflation volatility in the years ahead. Economic shocks stemming from natural disasters, geopolitical events, and pandemics are particularly concerning. While Hurricane Helene is not anticipated to influence inflation for the upcoming year, the likelihood of other events affecting it remains elevated, especially as the world transitions away from globalization.

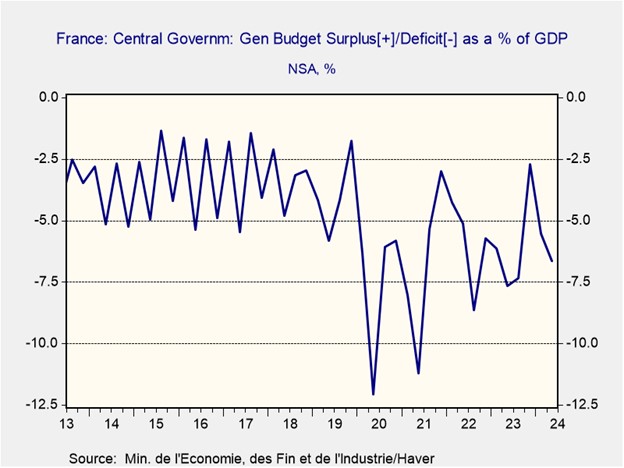

Tackling the Budget: After pressure from Brussels to rein in its budget, it looks like France is finally doing something about it.

- French President Emmanuel Macron has endorsed raising taxes on the country’s largest companies. His shift from his typical pro-business stance comes amid calls for the government to get its fiscal house in order. The government is expected to make around 60 billion EUR ($66 billion) in spending cuts and tax increases for the next budget year. Much of the increased tax revenue will be targeted toward wealthy individuals, large corporations, and activities that are harmful to the environment. Meanwhile, two-thirds of the savings are expected to come from cuts to ministries, local authorities, and the social security system.

- The shift to reduce its deficits comes as France has pushed to extend the deadline for meeting EU deficit targets. The French government is expected to lower its deficit from its current rate of 6% of GDP to 5% of GDP by 2025, with an overall goal of bringing the deficit below the 3% fiscal ceiling by 2029, two years later than it had anticipated. While the plan is not considered ideal, EU officials seem satisfied with the proposal, provided the government can enact the necessary reforms to lend it credibility.

- The shift to make the wealthy primarily responsible for repaying debt shows that governments are becoming less willing to impose austerity measures on the general population. This is a significant change from a few years ago when France increased taxes on the lower and middle classes, leading to the Yellow Vest protests. Targeting the wealthy and corporations may result in capital outflows to countries with more favorable tax policies and could lead to increased resistance to green initiatives in Europe.

In Other News: Microsoft-backed startup OpenAI has asked its investors not to support rival xAI as it looks to ensure dominance within the space. New Japanese Prime Minister Shigeru Ishiba downplayed the need for another rate hike due to the state of the economy, which has weighed on the yen (JPY). Additionally, Bank of England Governor Andrew Bailey has suggested that the central bank may favor cutting rates aggressively if inflation shows signs of improving.

Daily Comment (October 2, 2024)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Good morning! Markets are still grappling with the ongoing Middle Eastern conflict. Today’s Comment will analyze the escalating Israel-Iran tensions, explore the reasons behind the positive surprise from JOLTS, and provide our perspective on the recent vice presidential debate. Finally, we’ll conclude with a roundup of key domestic and international economic data.

Israel-Iran: The two countries have launched attacks against one another in a sign that tensions in the Middle East are rising.

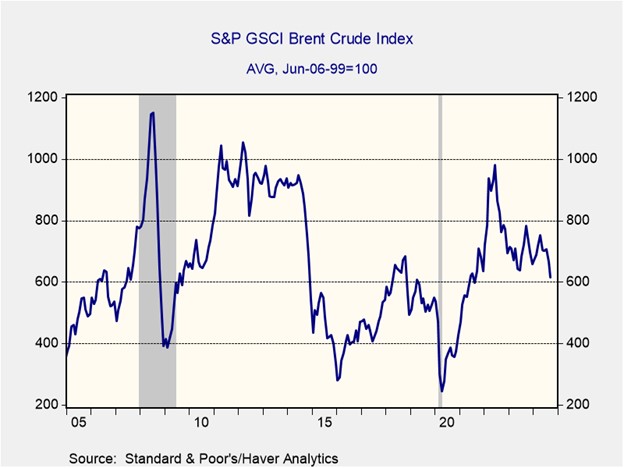

- Iran launched a massive barrage of 180 ballistic missiles against Israel on Tuesday, hours after the White House issued a stern warning about potential Iranian retaliation for a ground incursion into Lebanon. While most of the missiles were intercepted, the recent rocket launches penetrated farther into Israeli territory and came with less warning than the previous attack in April. So far, there is uncertainty as to whether tensions will escalate further, with Israeli Prime Minister Benjamin Netanyahu vowing that Iran “will pay” for the attack and Iran insisting that it is not interested in a broader war.

- The recent attack on Israel has triggered a sharp spike in oil prices, with Brent crude climbing above $75 a barrel — a level not seen since August. While the immediate impact of the attack is clear, the longer-term price trajectory remains less certain. Before the incident, the two warring factions in Libya agreed to a compromise, paving the way for a resumption of oil exports. Meanwhile, the Saudi-led OPEC+ alliance is scheduled to convene today to discuss increasing its production target. As a result, the potential increase in supply is likely to keep oil prices in check.

- The extent to which the conflict escalates will significantly influence oil prices. A broader war, involving Israeli strikes on Iranian oil infrastructure or an Iranian blockade of the Strait of Hormuz, could drive crude prices substantially higher. Currently, there is no indication that either side is seeking a major escalation. The US and its allies are actively working to de-escalate the situation. However, Israel’s recent denial of entry to UN Secretary-General António Guterres has raised concerns about its willingness to reduce tensions.

Job’s Surprise: Job openings surged in August; however, there are still signs that the labor market is cooling.

- The Job Openings and Labor Turnover Survey (JOLTS) revealed a surge in job openings in August, reaching a three-month high of 8.04 million. This uptick was primarily fueled by increased openings in construction and state and local government sectors. Despite the rise in available positions, concerns persist regarding labor demand. Hiring rates dipped to 3.3%, equaling their lowest point since the pandemic began. The number of job openings to the number of unemployed ratio was held to a three-year low of 1.1, down from the post-pandemic peak of 2.0 and slightly below the pre-pandemic ratio of 1.2.

- The mixed JOLTS report has muddied the waters on the labor market’s true health. The rise in construction jobs was likely fueled by lower interest rates, reflecting expectations of Fed cuts. The 10-year Treasury yield declined by nearly 50 basis points from early July to late August. Although this did not lead to an increase in construction spending, there was a noticeable rise in activity, particularly in housing starts. However, sectors less sensitive to interest rate changes, such as retail trade and transportation, experienced noticeable declines, which is likely to reinforce concerns that hiring is cooling.

- The size and timing of the Fed’s next rate cut will be heavily influenced by the jobs report, which will be released on Friday. While the JOLTS report was broadly positive, other surveys released last month have predominantly flashed warning signs that the labor market is cooling. If the BLS jobs report shows a slowdown in job creation or another uptick in the unemployment rate, Fed officials may seek to adjust policy to ensure that they do not lose control over the maximum employment mandate.

Vice Presidential Debate: The contest between the two vice-presidential candidates may not have produced sound bites, but it offered both sides a strong platform to share their visions for the country.

- During the debate, both sides tried to highlight the qualifications of their respective presidential candidates. Senator JD Vance argued that former President Donald Trump helped to lower inflation to 1.5% and increase take-home pay for American families while he was in office. Meanwhile, Minnesota Governor Tim Walz argued that Vice President Kamala Harris had helped lower insulin prices and had passed much-needed infrastructure legislation. Neither candidate made a significant impact, but they did not make any major mistakes either.

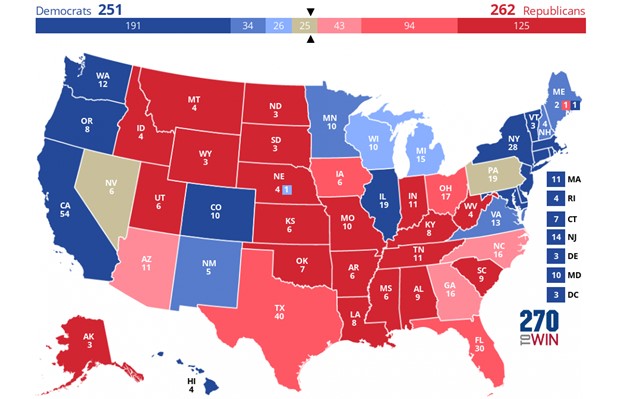

- With 33 days remaining until the election, there doesn’t appear to be a clear front-runner, which is different from previous election cycles. In the last election, President Joe Biden was considered the comfortable favorite to win the presidency and enjoyed very favorable polling. However, this year, the polls have tightened considerably, with Harris trailing broadly across swing states, according to data collected by Real Clear Politics.

(Source: www.270towin.com and Polymarket)

(Source: www.270towin.com and Polymarket)

- While Ohio Senator JD Vance appeared the most poised and composed during the debate, the lack of viral moments may render the contest inconsequential to the election. According to our current electoral forecast, based on betting odds, the election is likely to be a toss-up, potentially coming down to Pennsylvania. Betting odds slightly favor Harris, although polling shows an advantage in the other direction. It’s important to note that the president’s impact on financial markets is not as significant as that of the legislative branch, with betting odds currently favoring a split Congress.

In Other News: French Prime Minister Michel Barnier has proposed raising taxes to address the country’s debt, indicating a move towards unpopular measures. At the same time, dockworkers in the US have gone on strike, which could potentially disrupt US supply chains. Additionally, UK Prime Minister Keir Starmer is heading to Brussels to help improve relations with the EU as the two sides seek to secure deals on defense and food.

Daily Comment (October 1, 2024)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment today opens with news that consumer price inflation in the eurozone is now below the European Central Bank’s target of 2% for the first time in three years — a development that portends further interest-rate cuts and potentially renewed depreciation of the euro. We next review several other international and US developments with the potential to affect the financial markets today, including the inauguration of a new president in Mexico and a statement by Federal Reserve Chair Powell suggesting US interest rates will fall only gradually going forward.

Eurozone: In an initial estimate, the September consumer price index was up just 1.8% from the same month one year earlier, after a 2.2% gain in the year to August. That means price inflation is now below the European Central Bank’s target of 2.0% for the first time in three years. The continued cooling in inflation, which stems in part from weakening economic activity, will likely encourage the ECB to keep cutting interest rates at its next policy meeting later this month. As a result, the euro so far today is trading about 0.5% lower to $1.1079.

Japan: The Bank of Japan’s third-quarter “tankan” index of major manufacturers’ sentiment came in at a relatively subdued +13, matching the second-quarter figure. The third-quarter reading suggests Japanese manufacturers remain cautious as they face slowing economic growth in China and an appreciating yen (JPY). As we mentioned in our Comment yesterday, they are also now dealing with a new prime minister, Shigeru Ishiba, who was confirmed by the Diet today.

Russia-Ukraine: The Russian government’s proposed budget for 2025 envisions defense outlays jumping to the equivalent of $145 billion, up 25% from 2024. According to the government, the proposed military budget is necessary to ensure victory in the invasion of Ukraine. The huge increase also suggests President Putin is comfortable with the massive economic stimulus that has come with increased defense spending.

- The proposed defense budget would equal almost 7% of Russian gross domestic product, as forecasted by the International Monetary Fund. As we’ve noted before, higher defense spending tends to correlate with higher economic growth, so long as the “defense burden” remains below about 10.0% of GDP.

- However, given that the Russian military retains so many Soviet-style habits and operational approaches, it would not be surprising if Russia was hiding some defense spending in ostensibly civilian budget accounts or off budget. If so, Russia’s total defense spending could be above 10% of GDP, in which case it could soon start to weigh on the country’s economy.

Israel-Hezbollah: The Israeli military last night began what it called “limited, localized” ground raids against Hezbollah positions in southern Lebanon, marking Israel’s latest step in its nearly year-long war to eliminate the threats from Iran-backed Islamist militants. Israel’s increasingly aggressive moves suggest Prime Minister Netanyahu senses his country’s huge preponderance of power versus Hamas, Hezbollah, and Iran and is looking to defang them while he can.

- The risk, of course, is that Netanyahu could go too far, perhaps by attacking Iran directly to try to eliminate its nuclear program.

- Such a scenario could prompt Iran to retaliate against Israel or other regional countries with whatever weapons it can muster, leading to further destruction and potential economic disruptions across the region.

Mexico: Claudia Sheinbaum of the leftist Morena Party will be inaugurated today as the country’s new president. However, all signs suggest outgoing President Andrés Manuel López Obrador, the founder of Morena, will remain closely involved in governance and constrain Sheinbaum’s actions as she manages problems such as Mexico’s expanding budget deficit and high crime rate. Both those problems have hurt Mexico’s ability to benefit from global fracturing and the shifting of production toward the US from China.

US Politics: Republican vice presidential candidate JD Vance and his Democratic counterpart, Tim Walz, will square off in their only debate of the campaign season tonight at 9:00 PM ET. Vice presidential debates typically get somewhat less television viewership and attention than presidential debates. However, given how close this year’s race is, the success or failure of either vice presidential candidate could have a meaningful impact on who wins the presidency.

US Monetary Policy: At a conference yesterday, Fed Chair Powell said that the monetary policymakers are aiming to cut interest rates only to the “neutral” level, and that the course to get there is not pre-set. Rather, Powell said the path of rate cuts could still be gradual, depending on how the economic data comes in. In other words, Powell seemed to be suggesting that the Fed could cut rates more slowly than some investors still expect.

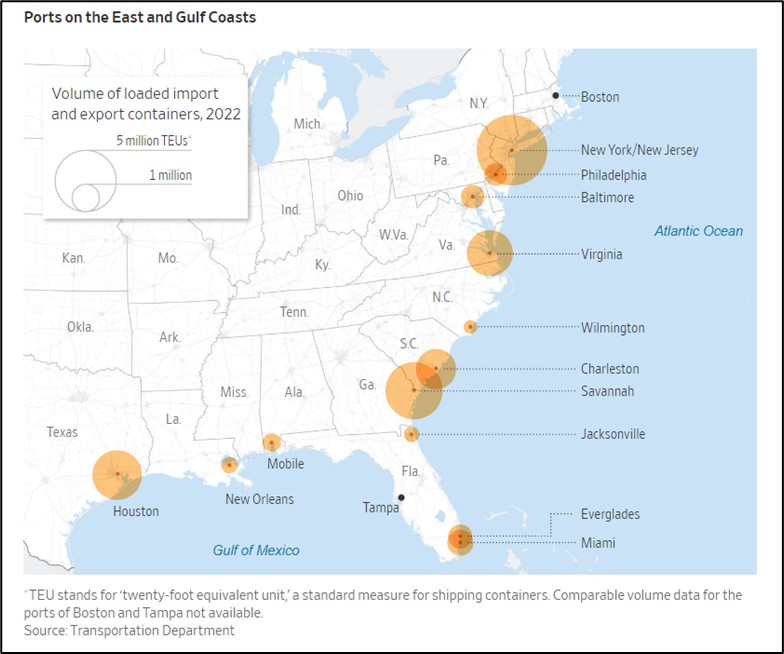

US Shipping Industry: As expected, the International Longshoremen’s Association today launched its big strike at East Coast and Gulf Coast ports. The affected ports typically account for about 41% of US containerized shipping volume, so the work stoppage is anticipated to have a major impact on the country’s exports and imports for as long as it lasts. Importantly, the disruption to imports could spark a new round of price inflation. As we’ve noted before, key issues in the dispute center on dockworker pay and the use of automation at the ports.

US Storm Damage: Authorities are still assessing the damage caused by Hurricane Helene as it moved across Florida, Georgia, and the Carolinas over the weekend, but it now appears the storm killed more than 100 people. In addition, Moody’s has estimated the massive hurricane caused at least $15 billion in property damage, and Fitch Ratings puts insurable losses between $5 billion and $10 billion.